Peter Gutmann Presentation - CSO Perspectives Roadshow Auckland 9th Mar 2015

Upload

zouheir-ben-tamaroutCategory

view

122download

1

Market Perspectives

March 2015

Mar. 6th, 2015

www.finlightresearch.com

Profits recession is underway…

“profit margins are probably the most mean-

reverting series in finance, and if profit margins do

not mean-revert, then something has gone badly

wrong with capitalism. If high profits do not attract

competition, there is something wrong with the

system and it is not functioning properly.”– Jeremy Grantham

2

FinLight Research | www.finlightresearch.com

Executive Summary: Global Asset Allocation

� Deflation fears are fading and growth hopes are rising..

� The broad uptrend in equity markets is still intact. But, between slowing growth,

weakening earnings prospects, coming rate hikes, falling oil, and the strength of

the dollar, we still believe equity markets are on borrowed time.

� In our view, the equity bull market is mature and offers a poor risk-reward

� We also believe that artificially low interest rates, set by Central Banks, lead to a

misallocation of capital, asset bubbles and, finally, to a big bust.

� Good news is bad news again! February jobs growth was stronger than

expected and market took it as a bad news as it pushed odds of a Fed rate hike

higher...

� The hunger for yield remains intense. BoJ and ECB QE should force JPY- and

EUR-based investors to seek yield in other currencies (USD among others).

� The divergence theme continues to propel the dollar higher

� Commodity prices continue to fall as the dollar strengthens.

� Volatility in commodities and currencies is propagating to stocks. Our

regime switching model is pointing to a major shift in the S&P500 volatility

regime.

� We remain underweight government bonds and corporate credit overall

(but with an intra-asset class preference for IG vs HY, and Eurozone vs US non-

financials), Overweight US dollar (supported by divergence Fed policy from

that of the ECB and BOJ) and UW commodities (specially on energy and

precious metals)

� We summarize our views as follows �

3

FinLight Research | www.finlightresearch.com

MACRO VIEW

� The Good� February jobs growth was stronger than expected, confirming that labor market has

improved. Market took it as a bad news as it pushed odds of a Fed rate hike higher...� The fall in oil prices is boosting retail spending and manufacturing output. But the benefits to

consumption growth should be fully exhausted over few months.� Consumers are quite optimistic. Michigan sentiment stand at a strong level (95.4). � China’s Manufacturing and Non-Manufacturing PMI have slightly rebounded in February

� The Bad� Earnings forward expectations are showing lower guidance and slower growth. At 85%

on the S&500, Q1 negative earnings guidance is well above average. Forward earnings estimates continue to decline.

� Goldman Sachs Global Leading Index has slipped in contraction phase, since January. Bad news for stocks, in our opinion.

� GDP gains slowed to 2.2% in Q4-2014� Existing home sales disappointed. They stand at their lowest level since May, 2014

� The Ugly � Main systemic risk resides in China : China’s economy is supported by approximately six

trillion dollars of 'shadow debt', which may eventually create major systemic issues. � We are building a boom-bust economy that is increasingly dependent on central bankers

inflating policies. The end game is clear even if the timing is anything but.

4

FinLight Research | www.finlightresearch.com

5

FinLight Research | www.finlightresearch.com

The Big Four Economic Indicators

� The overall picture had been one of a slow recovery, but there is no indication of a recession using the indicators monitored by the NBER.

� The Big Four average shows some signs of exhaustion…

6

FinLight Research | www.finlightresearch.com

US Inflation

� Inflation rate went negative (-0.09%annualized) as a result of the pullback in oil(and gasoline) prices

� Even on a core basis (ex food and energy)inflation is low and seems trending lower.

7

FinLight Research | www.finlightresearch.com

Consumer Sentiment

� Consumers are quite optimistic.

� Both the Michigan Sentiment Index andthe Conference Board's consumerconfidence are still near long-term highs

8

FinLight Research | www.finlightresearch.com

Chinese Economy

� Chinese economic momentum isdecelerating. Industry seems to facerecessionary pressure.

� China Manufacturing and Non-Manufacturing PMI have slightly reboundedin February

� Manufacturing PMI recovers a little (from48.9 to 49.9) but is still in contractionmode.

9

FinLight Research | www.finlightresearch.com

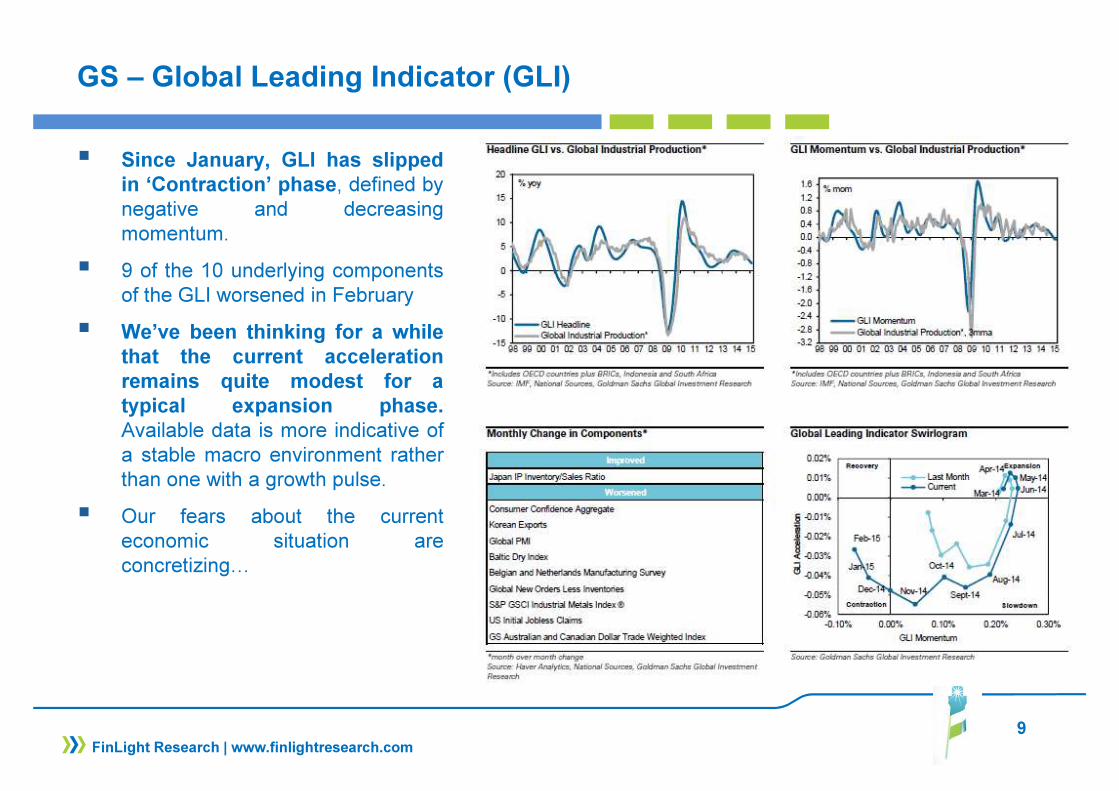

GS – Global Leading Indicator (GLI)

� Since January, GLI has slippedin ‘Contraction’ phase, defined bynegative and decreasingmomentum.

� 9 of the 10 underlying componentsof the GLI worsened in February

� We’ve been thinking for a whilethat the current accelerationremains quite modest for atypical expansion phase.Available data is more indicative ofa stable macro environment ratherthan one with a growth pulse.

� Our fears about the currenteconomic situation areconcretizing…

10

FinLight Research | www.finlightresearch.com

EQUITY

� The bull trend on equities remains intact. We still believe that equity markets are living on borrowed time. Market breadth does not suggest there is much strength beneath the surface. But central bank interventions continue to work their magic to keep the bull market going.

� Economic fundamentals are bullish in the US, but valuations are clearly bearish. By every technical measure, the risk-return profile for equities appears less attractive and should imply some cautious. With that said, we remain skeptical that this market will move much higher without a sharp pullback.

� Rationally, the upside on stocks is exhausted by a limited multiple expansion and margins being at peak levels. But the current environment of unprecedented monetary stimulus across the globe is making rationality irrational.

� On the S&P500 earnings front, and according to FactSet data, analysts are now expecting a YoYdecline for both Q1 and Q2-2015. Revenues are also expected to decline in H1-2015, mostly due to the energy sector. The consensus is still too optimistic in its earnings expectations for the H2-2015

� Energy sector's earnings expectations continue to be revised to the downside (37% since the start of 2015) and the sector is expected to earn just half of what it did in 2014

� Too little cash is left on the sidelines, as investors moved massively into equities and out of bonds and cash. Excessive optimism makes the equity market more vulnerable, pushing the volatility to the upside.

11

FinLight Research | www.finlightresearch.com

EQUITY

� Strong US dollar and currency volatility are headwinds to earnings guidance, specially for multinational companies. Volatility in commodities, currencies, and bonds is now filtering to stocks. Equity implied volatility is clearly shifting to a higher regime.

� We repeat our disagreement with those who continue to assert that lower oil prices are good for the US economy and the stock market, as the benefits to consumers is supposed to outweigh the decline in the energy sector (less than 10% of corporate earnings and market valuation). The sharp decline in oil prices is simply killing the growth from a sector that have generated a double-digit growth over the last years.

� Investors are showing more and more concern about the future path of U.S. monetary policy. Strong employment gains are clearly putting some pressure on the Fed to act soon. The coming rate hikes (probably in Q2-2015) will depress all asset prices for at least part of next year, in our view

� You can lough at us but we still believe that the current market cycle is simply a very verystrong cyclical bull within a secular bear market!

12

FinLight Research | www.finlightresearch.com

EQUITY

� Bottom line :� Nothing new compared to our previous report. We remain Neutral equities. At this stage,

expansionary monetary policies, low interest rates and abundant liquidity are keeping us from moving to an underweight on equities. Even bad news for the economy (in Europe, Japan and China) appear as good news for stocks, as they allow for further stimulus.

� We may revise our view to OW after a clean break of the 2075-2125 range on the S&P500, and to UW below the trend from Nov. ‘12 lows

� We think it is wise to incrementally "de-risk" your portfolios by focusing on higher quality / more defensive / more favorably priced companies

� While we remain long-term OW on Japan (always on an FX hedged basis) as we see further upside for Japanese stocks from the improvement in corporate earnings momentum, we tactically take part profit on unsupportive technicals and move Neutral on the short-term. A correctiionshould be expected shortly.

� A number of factors are helping European growth: lower oil prices, weaker Euro, and fading credit headwinds. We remain Neutral on Europe vs. US. We think that markets are too reliant on the new ECB’s QE. If the ECB loses the market’s confidence, European stocks would underperform severally.

� We remain UW in US small caps vs large caps, and UW EM stocks vs US large caps

13

FinLight Research | www.finlightresearch.com

Earnings

� While prices are still going up, forward earnings expectations start moving down, pushing P/E even higher…

� The forward 12-month P/E ratio for the S&P 500 now stands at 17.1, well above historical averages: 5-year (13.7), 10-year (14.1)

� The 12-month EPS estimate is now at $122.88, decreasing from $126.87 at Dec. 31st.

� For Q1 2015, 82 companies have issued negative EPS guidance and 15 companies have issued positive EPS guidance

� For Q1 2015 and Q2 2015, analysts predict YoYearnings declines of 4.6% and 1.5%, respectively

14

FinLight Research | www.finlightresearch.com

Earnings

� Despite the negative outlook forS&P500 earnings in H1-2015,analysts continue to see Q3-2015operating earnings at all-time highsthrough a profit margin expansionfrom current levels (10.1%, a multi-decade high).

� According to FactSet, theexpectation is that margins will riseto 10.6% in Q4-2015.

15

FinLight Research | www.finlightresearch.com

S&P500 – A Long-Term Perspective

� The market moved higher into overvaluation territories…

� We watch 4 long-term indicators : 2 P/E ratios and Q Ratio through their deviation to their arithmeticmeans and the inflation-adjusted S&P Composite deviation to its exponential trend.

� Based on the average of these indicators, the market looks 80% overvalued (the highest level outside theTech Bubble), suggesting a cautious long-term outlook

16

FinLight Research | www.finlightresearch.com

S&P500 – A Short-Term Perspective

� The S&P 500 has been consolidating inrecent weeks, but the underlyingmomentum is still intact, and willremain so as far as the primaryuptrend from Oct. ‘11 lows (~1870) ispreserved

� The level to watch over the ST is 2064that combines the prior ceiling and the50d MA.

17

FinLight Research | www.finlightresearch.com

Emerging Markets

� The equity market picture inEM has been complicated byenergy price volatility.

� EM stocks have been tradingsideways for years now,despite weaker currencies.

� We see no positive catalysts at this stage, and believe growth dynamics to remain poor.

� Therefore, we prefer to remain UW EM.

MSCI EM Equities in local cur.

EM FX vs. USD

18

FinLight Research | www.finlightresearch.com

Trading Model – S&P500

� Our prop. Short-Term trading model went massively long on Jan. 6th at 2002.61 on the index. The model increased its longs on Jan 28th (@2002.16), then on Jan 30th (@1994.99), reversed it position on Feb 12 (@2088.48) and went massively short on Feb 20th (@2110.30)

� As of Mar 6th, the model is becoming modestly long again.� The model targets 2083 and 2103 on the upside, but still expect a breach of the 2062-2041 area

to the downside.

19

FIXED INCOME & CREDIT

� The global central bank landscape remains highly supportive of fixed income markets.

� the significant QE buying from the ECB and BoJ is happening in a market where yields are already rock bottom and in a number of cases are negative. We thus do not expect that this QE will lead to much lower yields in euros and yen and will instead force investors there to seek better yields elsewhere, depressing their own currencies and yields in other markets.

� We still look for the bear market on USTs to resume but patience seems to be needed

� Despite the recent rebound, we believe that US yields are set to stay low both because low inflation will transmit to the US via the strengthening dollar but also because yield hungry investors in Japan and the Eurozone will simply buy USTs.

� We’ve been Neutral UST since end of Nov. ’14, and decided to stay Neutral as far as the 10y yield remains below 2.25.

� The negative net issuance in the Euro area combined with the continuing duration withdrawal in Japan provides a supportive backdrop for global fixed income markets

� We remain neutral on German yields despite the ECB QE that we expect to keep German bond yields at very low levels. But until fiscal solutions are seen, the potential for a reflation trade (similar to the one we initiated in the US after Fed’s QE3) remains very limited, in our view.

� The hunger for yield remains intense. BoJ and ECB QE should force JPY- and EUR-based investors to seek yield in other currencies (USD among others).

FinLight Research | www.finlightresearch.com

20

FIXED INCOME & CREDIT

� The sharp rise in yields after the upside surprise in the US employment report shows that yield markets are vulnerable to the timing of the first Fed hike.

� We expect the Fed to start tightening in June and to hike rates more than is currently priced in: Thus, the re-pricing of Fed expectations is likely to take place very soon in the short end of the curve.

� While US yields in the short end are expected to go higher driven by Fed expectations, the medium to long end of the curve will be supported by abundant liquidity and by spillover effects from ECB and BoJ QE as investors struggle for yield. We continue to bet on a significant flattening of the US yield curve.

FinLight Research | www.finlightresearch.com

21

FIXED INCOME & CREDIT

� Credit markets have performed strongly since the ECB announced an expanded asset purchase program at the end of January. Since then, the search for yield resumed and we saw investors moving down the quality spectrum, buying high yield bonds and growth sectors.

� We remain UW on corporate credit, due to valuation, to rising corporate leverage (specially in the US), to position within the credit cycle, to the expected rise in government bond yields and given the weak total return forecast

� Within the credit pocket, and over the very short-term, we continue to prefer Eurozone corporates (specially IG and non-financials) to US corps, because of the ECB massive QE

� In the medium-term (6 months), we expect the pattern of European outperformance to reverse.

� We still prefer IG over HY on a risk-adjusted basis as we expect higher volatility on spreads

� Bottom line : Neutral Govies, Neutral Eurozone vs. US Govies, Long flatteners on the US yield curve, UW credit, OW Eurozone vs US credit (specially IG and non-financials), Neutral TIPS and OW HICP Inflation, UW High Yield vs High Grade, Neutral on EM corporates

FinLight Research | www.finlightresearch.com

22

FinLight Research | www.finlightresearch.com

European Bonds

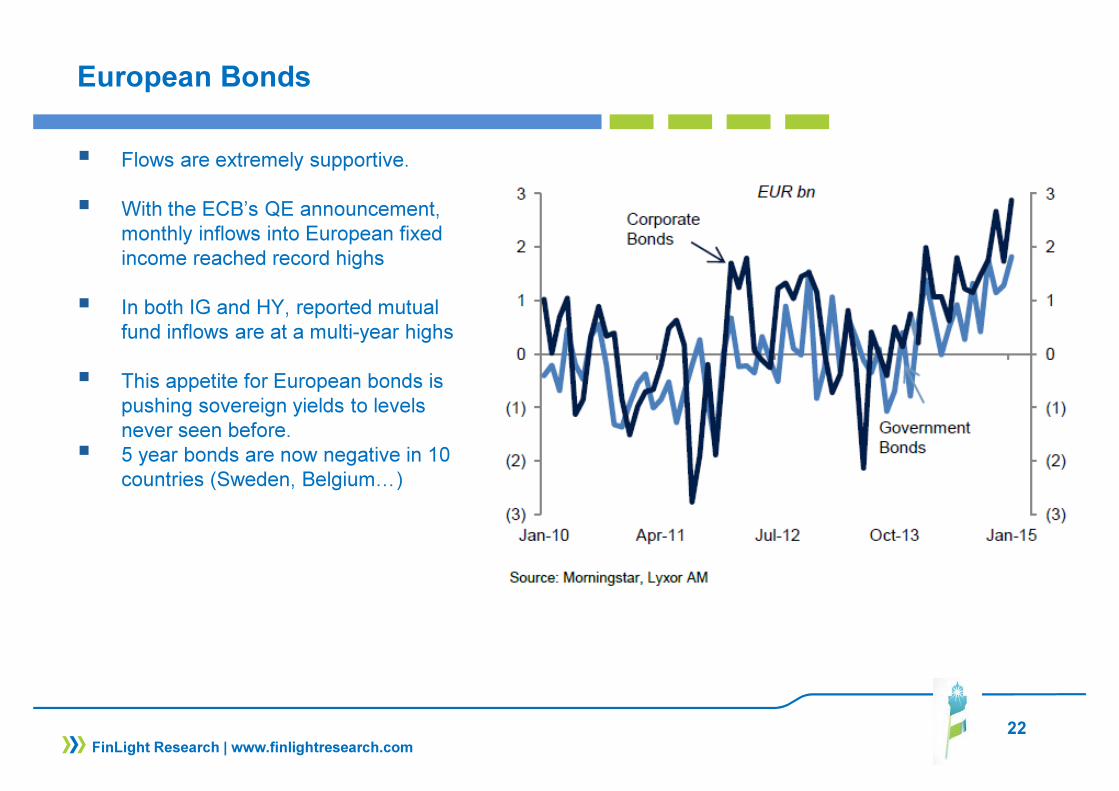

� Flows are extremely supportive.

� With the ECB’s QE announcement, monthly inflows into European fixed income reached record highs

� In both IG and HY, reported mutual fund inflows are at a multi-year highs

� This appetite for European bonds is pushing sovereign yields to levels never seen before.

� 5 year bonds are now negative in 10 countries (Sweden, Belgium…)

23

FinLight Research | www.finlightresearch.com

10-year USTs

� In our previous report, we said : “Market rejection of the 1.77 resistance would increase the likelihood for a base pattern formation. In that case, a bounce to 1.9-2.0 becomes possible.”

� The rebound did occur slightly below 1.70, and went through the 2.0 target

� After a consolidation period (around 2.10), 10-year yields have jumped up on last macro news. The next level to watch now is 2.25

� We’ve been Neutral UST since end of Nov. ’14, and decided to stay Neutral as far as the 10y yield remains below 2.25.

.

24

FinLight Research | www.finlightresearch.com

Credit – Investment Grade

� After declining for most of H2-2014, the investment grade fund beta has sharply rebounded on ECB announcement of its sovereign QE on Jan. 22nd.

� Does that mean that fund managers are accumulating risk again ?

� The answer should be Yes if we trust the spread differential between single-Bs and BBs which has declined significantly from the recent wides.

25

EXCHANGE RATES

� Policy divergence between the US on one hand, and Japan and the Eurozone on the other, should continue to provide an environment supportive of the dollar.

� Currency war is raging… Signs of global economic weakness and deflation persist in Europe, Japan and even China, pushing these countries to debase their currencies in order to fight off deflation and grow their exports. But currency debasement is exporting deflation to the U.S. by strengthening the dollar

� We see further medium term USD gains against the major crosses, especially EUR and JPY

� EUR-USD underlying structure still looks very heavy. Our ST target of 1.12-1.10 has already been reached. We remain UW EUR-USD as long as the pivot stays below 1.16 and move Neutral above to play the correction towards 1.25-1.30. Our next target is 1.02-1.00.

� We remain OW USD-JPY as far as the pivot stays above 116 (lower bound of the consolidation triangle). Our ultimate target remains at 124-125 over the medium-term

� The best hope for a broad USD breakout rests on consistent inflation surprises in the US

FinLight Research | www.finlightresearch.com

26

US Dollar – A Long-Term Perspective

� Dollar moves tend to be persistent, with rallies typically running for 5-6 years and 40% gain versus G10 currencies.

� We see further USD upside over the medium/long-term, with around 10%+ additional gains versus G10

FinLight Research | www.finlightresearch.com

27

US Dollar Index

� Relatively to the expected rate hike in June, the current dollar appreciation appears to match the pace of 1994 and 1999 cycles.

FinLight Research | www.finlightresearch.com

28

US Dollar Index - DXY

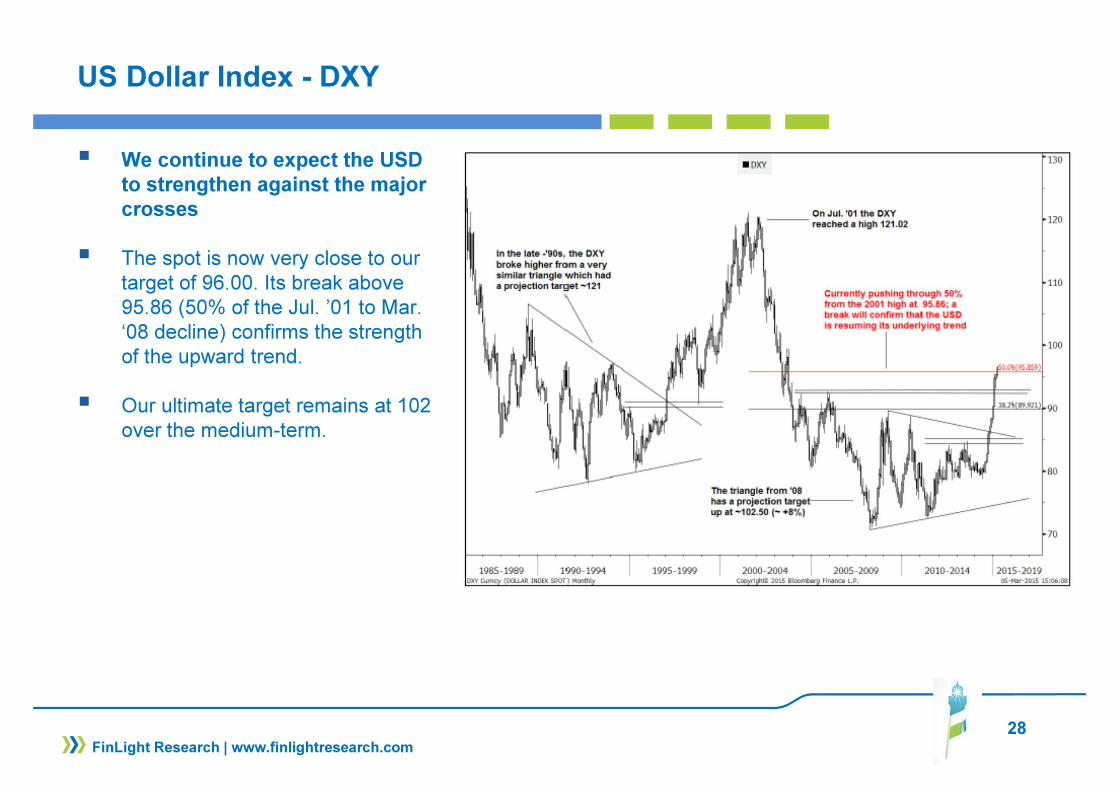

� We continue to expect the USD to strengthen against the major crosses

� The spot is now very close to our target of 96.00. Its break above 95.86 (50% of the Jul. ’01 to Mar. ‘08 decline) confirms the strength of the upward trend.

� Our ultimate target remains at 102 over the medium-term.

FinLight Research | www.finlightresearch.com

29

EUR-USD

� Things are going very fast. Our ST target of 1.12-1.10 has already been reached.

� Now that the 1.10 support is breaking, we expect the momentum to accelerate down.

� Next main levels to be watched are 1.0737 and 1.0245 (our ultimate target, at this stage)

� Our medium-term view remains biased towards a strengthening of USD

� We remain UW EUR-USD as long as the pivot stays below 1.16 and move Neutral above to play the correction towards 1.25-1.30

FinLight Research | www.finlightresearch.com

30

USD-JPY

� Breaking the 120.75 resistance is the sign to watch for a confirmation of the uptrend

� Our ultimate medium-term target remains at ~ 124-125. We will take a more neutral stance as soon as it is reached.

� We remain OW USD-JPY as far as the pivot stays above 116 (lower bound of the consolidation triangle) and below the 124-125 area.

FinLight Research | www.finlightresearch.com

31

COMMODITY

� Over the short-term, the trend remains bearish. We still watch for a bottom formation.� USD strengthening remains a big headwind to commodities

� We remain UW commodities. We continue, however, to like owning the GSCI index, and thinkthat commodities hold value as cross-asset portfolio diversifiers.

Bottom Line :

� Many factors are weighing on base metals: US Dollar strengthening, the Chinese slowdown,weaknesses in construction / housing sectors in major economies (mainly affecting Copper andNickel) � We remain Neutral on base metals (but we prefer Aluminium, Zinc and Nickel to Copper)

� We remain UW on agriculture (except on Cocoa and Coffee) because of excess supply andsubstantial stocks (built since the 2012 drought). Absent a severe weather shock, it is unlikely thatagriculture prices will spike this year. We rather anticipate they will revert to 2009 levels. Within theAgri complex, we’ve been OW Cocoa and Coffee for a while now. We like Cocoa for its long-termunderlying demand driven by consumption in Asia. Pullback in coffee prices provide a better entryopportunity into this market after the sharp surge we’ve seen in prices because of the drought inBrazil.

FinLight Research | www.finlightresearch.com

32

COMMODITY

� It is too early to expect major upside for the price of oil as the US is sinking deeper in a glut ofexcess oil. Supply is at all-time highs. Without a supply cutback, there is no reason for the current oilprice to go higher.

� No indication of a bottom formation yet as:� Crude Oil Volatility Index (OVX) stands at crisis levels� Energy sector's earnings expectations continue to be revised to the downside (37% since the

start of 2015)� We remain UW oil and target ‘08 lows (around $35) as long as the OPEC doesn’t decide to stop

the bleeding and the excess supply remains. We will move to Neutral if WTI breaks above $52/barrel

� The stimulus provided by the ECB & BoJ is already factored in gold prices. Precious metals are vulnerable to higher US real yields and stronger dollar

� Our strategy on gold remains unchanged: We remain UW above 1150-1170 band. We will moveNeutral below 1150 and switch progressively to OW (accumulate) as the spot slides downtowards 1000-980, which is likely the final leg down.

� Our first target on silver stands at 14.70. We still think that Silver (like gold) is probably ready for its final leg down towards 12.50. At current levels, we are UW. we will switch progressively to OW (accumulate) as the spot breaks the first material resistance around 14.70 and slides down towards 12.50

FinLight Research | www.finlightresearch.com

33

FinLight Research | www.finlightresearch.com

Crude Oil

� The number of U.S. oil rigs out drilling new wells fell for the 13th straight week as the U.S.

� Baker Hughes oil and gas rig count is falling at a speed last seen during the credit crisis.

� Excluding gas rigs, the number of rigs dropped to 922, down 43% since October.

� But there is no cutback in supply yet, and thus no reason for the price of oil to rise rightnow

34

FinLight Research | www.finlightresearch.com

Crude Oil

� At this stage, producers are pumping 1.5 Mln barrelsa day more than the word needs.

� Excluding the Strategic Petroleum Reserve, crude oilstocks rose by another 10.3 million barrels to 444million barrels as of Mar. 4th, the highest since 1982.

� If growth in supplies continues on the currenttrend, Cushing Oklahoma could run out ofstorage in a just a couple of months

� Where are we going to put all this oil?Probably, in oil tankers again…

35

Gold

� Gold has broken sharply belowthe Nov. ‘14 uptrend (1,189).

� It seems now ready for a to makea new low, below 1,132.

� We change nothing to ourprevious strategy: We will moveNeutral below 1150 and switchprogressively to OW (accumulate)as the spot slides down towards1000-980, which is likely thefinal leg down.

FinLight Research | www.finlightresearch.com

36

ALTERNATIVE STRATEGIES

� Hedge funds ended February on a good note (+1.85% on the HFRI Composite). Best performers were Event-Driven (+2.98%, mainly due to Activist and Special Situations strategies)) and Equity Hedge (+2.79%).

� The “normalization trade” has gathered momentum, since end of January, bringing major moves within the hedge fund universe. Previous winners (long-term CTAs, L/S Equity funds) underperformed, while most previous losers (Event-Driven, Convertible Arbitrage) made money.

� During February, Event-Driven funds benefited from a return of risk appetite in the market and positive development on a series of deals.

� CTAs suffered from trend reversal in oil prices and US treasuries, but they still managed to end the month flat.

� We continue to see inflows in HFs as investors position for volatility. � We reiterate our preference for risk diversifiers (pure alpha generation strategies) over return enhancers.

� We maintain our previous positioning and remain OW on:� Equity Market Neutrals both for their “intelligent” beta and their alpha contribution. On several

occasions in 2014, our preference for variable bias and market neutral managers has proven to pay off (compared to long bias) on the back of adequate short positioning.

� CTA’s and Global Macro as a diversifier and tail hedge. � Vol. Arb strategy and prefer funds that trade volatility globally (all assets / all regions). This strategy

has shown a great ability in terms of protecting capital during adverse periods, and a volatility that compares favorably with the hedge fund industry

FinLight Research | www.finlightresearch.com

37

CTAs

� CTAs have lately increase theirequity exposure. That provedespecially rewarding.

� Most of the losses were generated oncommodities (specially the shortpositions on oil and Agri. prices) andfixed income (long treasuries)

� The overall long dollar exposure heldby CTAs was unable to compensatefor the losses as the US dollarstopped its upward trend at the end ofFebruary.

� In CTAs space, long-term models kepttheir old exposure and posted losseson shorter term trend reversals(commos, treasury yields…)

� February was a strong month for shortterm CTAs. Short term modelsbenefited from a higher volatilityregime by adjusting quickly to therebound

FinLight Research | www.finlightresearch.com

Bottom Line: Global Asset Allocation

� Deflation fears are fading and growth hopes are rising..

� The broad uptrend in equity markets is still intact. But, between slowing growth,

weakening earnings prospects, coming rate hikes, falling oil, and the strength of

the dollar, we still believe equity markets are on borrowed time.

� In our view, the equity bull market is mature and offers a poor risk-reward

� We also believe that artificially low interest rates, set by Central Banks, lead to a

misallocation of capital, asset bubbles and, finally, to a big bust.

� Good news is bad news again! February jobs growth was stronger than

expected and market took it as a bad news as it pushed odds of a Fed rate hike

higher...

� The hunger for yield remains intense. BoJ and ECB QE should force JPY- and

EUR-based investors to seek yield in other currencies (USD among others).

� The divergence theme continues to propel the dollar higher

� Commodity prices continue to fall as the dollar strengthens.

� Volatility in commodities and currencies is propagating to stocks. Our

regime switching model is pointing to a major shift in the S&P500 volatility

regime.

� We remain underweight government bonds and corporate credit overall

(but with an intra-asset class preference for IG vs HY, and Eurozone vs US non-

financials), Overweight US dollar (supported by divergence Fed policy from

that of the ECB and BOJ) and UW commodities (specially on energy and

precious metals)

� We summarize our views as follows �

38

FinLight Research | www.finlightresearch.com

39

Disclaimer

FinLight Research | www.finlightresearch.com

This writing is for informational purposes only and does not constitute an

offer to sell, a solicitation to buy, or a recommendation regarding any

securities transaction, or as an offer to provide advisory or other services

by FinLight Research in any jurisdiction in which such offer, solicitation,

purchase or sale would be unlawful under the securities laws of such

jurisdiction. The information contained in this writing should not be

construed as financial or investment advice on any subject matter.

FinLight Research expressly disclaims all liability in respect to actions

taken based on any or all of the information on this writing.

About Us…

� FinLight Research is a research-centric company focused on Asset Allocation from a top-down perspective, on Portfolio Construction, and all related quantitative aspects and risk management issues.

� Our expertise expands along 3 axes:

� Asset Allocation with risk control and/or risk budgeting techniques

� Allocation to alternative investments : Hedge funds, rule-based strategies (momentum, value, carry, volatility), real assets (real estate, infrastructure, farmland, timberland and natural resources). Private equity and venture capital should be the next step…

� Allocation with a factorial approach built on the understanding (profiling) of the risk/return drivers of the different asset classes

� FinLight Research is an innovation-oriented company. We target to fill the gap between the academic research and the investment community, especially on real assets and alternatives. We survey on a continuous basis the academic literature for interesting published and working papers related to quantitative investing, non-linear profiling, asset allocation, real assets...

40

FinLight Research | www.finlightresearch.com

Our Standard Offer

Provide tailor-made quantitative analysis of your

portfolios in terms of asset allocation, risk profiling and risk contribution

Provide tailor-made quantitative analysis of your

portfolios in terms of asset allocation, risk profiling and risk contribution

•Risk Profiling

Offer a turnkey 3-step factor-based process in GAA

with factor selection, risk budgeting and

dynamic portfolio protection

Offer a turnkey 3-step factor-based process in GAA

with factor selection, risk budgeting and

dynamic portfolio protection

•Factor-based GAA Process

Provide assistance with alternative

investments (including real

assets) in terms of profiling, and

integration in a GAA

Provide assistance with alternative

investments (including real

assets) in terms of profiling, and

integration in a GAA

•Alternative Investments

Provide assistance with asset

allocation and related risk control

and/or risk budgeting techniques

Provide assistance with asset

allocation and related risk control

and/or risk budgeting techniques

•Global Asset Allocation (GAA)

41

FinLight Research | www.finlightresearch.com