Fi#ng&Mobile&and&Consumer&RDC& Into&your&Bank's&Retail&Strategy& - IFO · Why&Consumer&RDC?&&...

26

Fi#ng Mobile and Consumer RDC Into your Bank's Retail Strategy Mike Packer, TransCentra

Transcript of Fi#ng&Mobile&and&Consumer&RDC& Into&your&Bank's&Retail&Strategy& - IFO · Why&Consumer&RDC?&&...

Fi#ng Mobile and Consumer RDC Into your Bank's Retail Strategy

Mike Packer, TransCentra

About TransCentra

• Key Facts – ~ $170M in annual revenue – 12 offices across North America – Processes over 640 million payments annually

• History – J&B SoJware, established in 1985 – Regulus Group, established in 1996 – In June 2011 Cerberus acquired J&B SoJware and Regulus and formed TransCentra, an independent, standalone porWolio company

Today’s Agenda

• Retail Banking and Consumer/Mobile RDC – Is there a need for Consumer RDC? – Customer Reten[on – Customer Acquisi[on – Which customers are profitable – Demographics by age, income – Mul[-‐channel – Rate of change

Why Consumer RDC? Who SBll Deposits Checks?

• > 95% received payroll by Direct Deposit • Source: Wincor Nixdorf Inc., Nov. 2011

0 checks 38%

1 -‐ 5 checks 61%

6 or more checks 1%

Checks per Month

Why Consumer RDC? How to Deposit a Check?

• Go to a branch/ATM • Drop it in the mail • Consumer/Mobile RDC

Financial InsBtuBon Challenges

Customer Reten[on

Customer Acquisi[on

Mobile Strategy

Increasing Deposits

Capital Requirements

Bringing New Products to Market

Focusing on Core Services

Maintaining Legacy Systems

Integra[on Consolida[on Regulatory Requirements

ROI of New Investments

Financial InsBtuBon Challenges

Customer Reten[on

Customer Acquisi[on

Mobile Strategy

Increasing Deposits

Capital Requirements

Bringing New Products to Market

Focusing on Core Services

Maintaining Legacy Systems

Integra[on Consolida[on Regulatory Requirements

ROI of New Investments

Customer Reten[on

Customer RetenBon and AcquisiBon Issues

• Cost to acquire new customer is 5x cost to retain exis[ng customer*

• 8.7% switched banks in 2011** Other es[mates at 12.5%

* The Cost of Churn, Chris[ne Durkin, Financial Publishing Services hfp://www.marke[ngexecu[ves.biz/The-‐Cost-‐of-‐Customer-‐Churn ** J.D. Power and Associates, March 1, 2011, N=4,791, hfp://www.pntmarke[ngservices.com/newsfeed/ar[cle/More_customers_switching_banks,_survey_finds-‐800436896.html

Customer RetenBon Issues 2009 vs. 2011

3%

59%

34%

34%

63%

6%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Shopping around

Customer loyalty

Decreased Stayed the same Increased

Source: Accenture, Customer 2012, Accenture Global Customer Behavior Study, 2009

Customer RetenBon Issues

• Customers with mul[ple accounts more loyal • Customers with mul[ple products more loyal • Some products make customers “S[ckier” – On-‐line Bill Pay is especially s[cky • Hard to switch • 12% less likely to switch*

– Consumer/Mobile Deposit creates s[cky customers

* Kirk Gripenstraw, Aspen Marke[ng Services Emmef Higdon, Forrester Research, E-‐Bill's True ROI – The Impact of Online Bill Presentment and Payment on Reten[on and Profitability

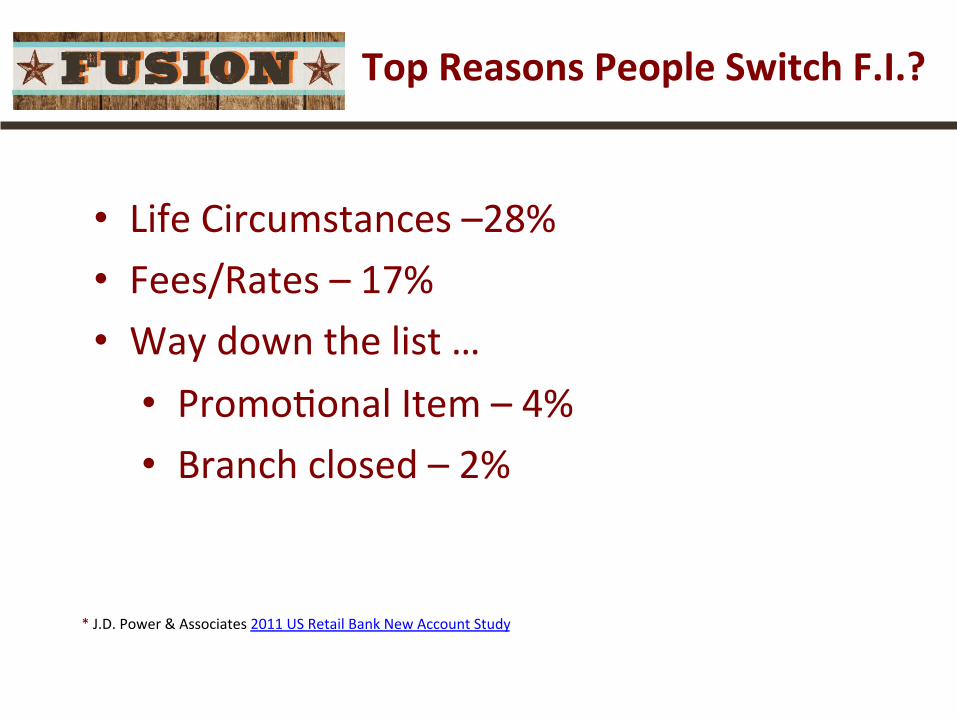

Top Reasons People Switch F.I.?

• Life Circumstances –28% • Fees/Rates – 17% • Way down the list … • Promo[onal Item – 4% • Branch closed – 2%

* J.D. Power & Associates 2011 US Retail Bank New Account Study

Life Circumstance #1 -‐ Moving

• 12.5%* of Americans move annually • OJen, move corresponds with other life changes • Ideal [me for the FI to help

• 69% that move stay in the same county • So each year ~ 9% move within same county • Deposit of checks is primary reason people go to branch • How far will they go for a branch? • Would Consumer/Mobile RDC retain some that leave?

* U.S. 2010 Census Bureau, hfp://www.census.gov/newsroom/releases/archives/mobility_of_the_popula[on/cb11-‐91.html

Life Circumstance #2 -‐ Inheritance

• Parents die • Adult Children inherit $$ • Children don’t have account same F.I. • Children don’t value personal mee[ngs with financial

advisor • Money leaves F.I. quickly

• Or … • Adult Children inherit $$ • Children have same F.I., because they like Mobile Apps

Will the Money stay with the F.I.?

Customer RetenBon Summary

• More expensive to get a new customer vs. retain exis[ng customer

• Consumers are less loyal to FI’s • Addi[onal products increase customer loyalty • Consumer/Mobile RDC increases customer loyalty

• Life circumstances puts FI rela[onship at risk

Customer Acquisi[on and Profitability

All Customers Are Not Created Equal

• 75% no material impact on profits, 5% extremely unprofitable*

• Consumer Mobile RDC can afract, retain the 20% that are profitable

*BRENT J. BAHNUB, Customer Profitability Tune-‐up, Dec 8, 2010, hfp://www.bai.org/bankingstrategies/marke[ng-‐and-‐sales/segmenta[on/customer-‐profitability-‐tune-‐up

Factors in A_racBng Good Customers

• 50% who switched banks said mobile played a role in their primary bank-‐selec[on decision*

• 43% interested in mobile banking cited mobile check deposit as the most important feature of mobile banking that would get them to switch*

• 59% who use mobile banking would be likely to use remote deposit capture via a mobile phone if it were offered by their banks*

* Source: Mercatus MobileSurvey 2010

Consumers, by Age Likely to Use Mobile RDC

Source: Javelin Strategy & Research, March 2011, n=4,267

6

8

12

16

17

18

13

4

6

11

12

15

18

11

17

23

28

27

34

37

27

11

13

10

13

10

9

11

62

50

39

32

24

19

38

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

65+

55 -‐ 64

45 -‐ 54

35 -‐ 44

25 -‐ 34

18 -‐ 24

All Consumers

Very desirable

Somewhat desirable

Not desirable at all

Smartphone Ownership by Age

18-‐24 25-‐34 35-‐44 45-‐54 55-‐64 65+

49% 58%

44%

28% 22%

11%

46% 35%

45%

58%

59%

45%

5% 7% 11% 14% 19%

44%

No cell

Other Cell Phone

SmartPhone

• Source: Pew Research Center’s Internet & American Life Project, July 11, 2011, N=2,277

Consumers, by Income Likely to Use Mobile RDC

Source: Javelin Strategy & Research, March 2011, n=4,267

10

9

10

10

12

14

15

20

11

11

8

8

10

12

13

13

35

23

28

28

30

25

27

25

7

12

8

10

13

9

13

14

37

44

46

44

35

39

32

29

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

< $15,000

$15K-‐$24,999

$25K -‐ $34,999

$35K-‐$49,999

$50K-‐$74,999

$75K-‐$99,999

$100K-‐$150K

> $150K Very desirable

Somewhat desirable

Not desirable at all

Smartphone Ownership by Income

21% 20% 26%

36% 44%

38%

53% 57%

73%

53% 57% 54%

48%

47% 50%

44% 38%

25% 26% 23% 20% 16% 9% 12%

3% 5% 2%

No cell Other Cell Phone SmartPhone

Source: Pew Research Center’s Internet & American Life Project, July 11, 2011, N=2,277

Customer AcquisiBon Profitability Summary

• 20% of customers give you >80% profits • 50% of people switching FI’s said Mobile played a role

• >50% ages 18-‐44 want Mobile RDC • >50% incomes $50K+ want Mobile RDC • The young, the affluent want Mobile RDC • The young, the affluent have Smartphones

MulB-‐Channel

• Consumer/Mobile RDC won’t eliminate the branch – A very few on-‐line only FI’s in the U.S. – RDC for those that don’t/can’t go to branch

• Most banks suppor[ng many channels for Retail Banking clients – Branches – ATM – Internet – Phone (voice) – Mobile Phone

Should you wait?

June 29, 2007

iPhone 1st day of sale

Thank You!