Finding Stability Amid Volatility - Cushman & Wakefield/media/reports/singapore/CW MIDYEAR...

13

ASIA PACIFIC OFFICE OUTLOOK Finding Stability Amid Volatility AUGUST 2016

Transcript of Finding Stability Amid Volatility - Cushman & Wakefield/media/reports/singapore/CW MIDYEAR...

ASIA PACIFIC OFFICE OUTLOOK Finding Stability Amid Volatility

AUGUST 2016

CO

NT

EN

TS

EXECUTIVE SUMMARYThe year 2016 has so far turned out

to be quite eventful. We began

the year with a global financial

market rout that had its origin in

China, the Bank of Japan ushering

a new monetary policy regime by

adding negative interest rates and

possibly “helicopter money”, which

is a direct cash injection into the

Japanese economy, and the impact

of Brexit continues to unravel. The

year also marks the changing of the

guards in many countries across the

region. Welcoming a new leader is

an economic event in itself, but this

transition comes at a crucial time

given that maintaining the status

quo is not an option. Their economic

views will certainly affect their

economies. Despite all of these,

economic performance in the region

has remained steadfast, the property

markets showed positive leasing

momentum, and the investment

market was brimming with activity,

even witnessing some landmark

transactions this year.

Going forward, economic growth is

poised to improve in 2017. Emerging

countries, including India and those

in Southeast Asia, especially the

Philippines and Vietnam, will be the

growth leaders. China, even with

its slowing growth, will remain an

important engine as its economy

gradually transitions to a consumer-

based one. With this, the region’s

office sector is expected to remain

on solid ground.

Leasing demand in the 30 major

cities we track will reach new highs

through next year. In some markets,

this coincides with a wave of new

supply that could lead to higher

vacancies. For 2017, rent increases

will be more pronounced in many

markets across the region with about

14 cities expected to post record

rents since the global financial crisis.

While higher rents are emblematic of

strong leasing market performance,

this is a trend that could add further

strain on corporate expansion in an

environment that is focused on cost

containment.

For investment activity, the volume

for the first half of 2016 was below

that of the same period last year,

but we can expect a rebound in the

second half. The current environment

remains very conducive to investing,

similar to 2015, which was a record

year for the region in terms of

investment volume. If anything, the

lack of assets for sale will be the only

limiting factor.

Regional Economy: Resiliency in Tough Times 6

Occupier Focus | Co-working: 9 A Glimpse of The Future for Corporate Office Occupiers?

Technology 11 Equipping the New Age Broker

Office Sector: The Rising Tide is Lifting All Boats 12

Investment Activity: The Show Must Go On 13

Tokyo: Stable and Consistent 14

Seoul: Muddling Through 14

Beijing and Shanghai: Still Room to Grow 15

Hong Kong: Bracing for Slower Growth 16

Singapore: Looking Beyond the Subdued Market 16

Jakarta: Gradual Liftoff 18

Manila: Continuing to Shine 18

Ho Chi Minh City: Ready for Take-off 19

India: The Cycle Turns Up 19

Sydney and Melbourne: The Only Way is Up 20

GREATER CHINA

SOUTH ASIA SOUTHEAST ASIA

Seoul Tokyo

AUSTRALIA &NEW ZEALAND

NORTH ASIABeijing

Chengdu

GuangzhouShanghai

Shenzhen

Hong Kong

Taipei

Bangkok

Hanoi

Ho Chi Minh City

Manila

Kuala Lumpur

Jakarta

Singapore

Ahmedabad

BengaluruChennai

Hyderabad

Kolkata

Mumbai

New Delhi

Pune

AdelaideBrisbane

Perth Sydney

Melbourne

Auckland

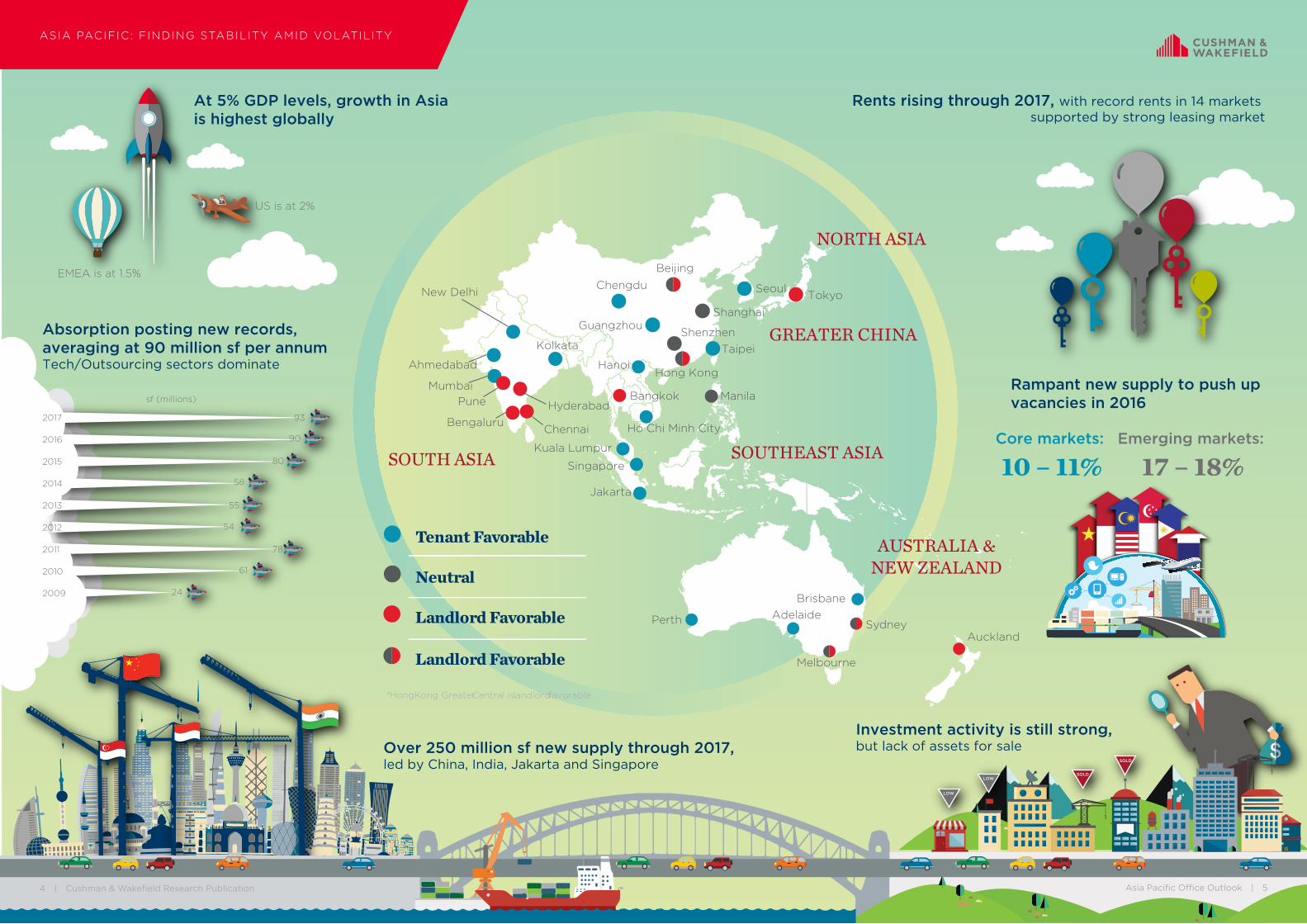

*Hong Kong Greater Central is landlord favorable

Tenant Favorable

Neutral

Landlord Favorable

Landlord Favorable

At 5% GDP levels, growth in Asia is highest globally

Absorption posting new records, averaging at 90 million sf per annum Tech/Outsourcing sectors dominate

Rents rising through 2017, with record rents in 14 markets supported by strong leasing market

Rampant new supply to push upvacancies in 2016

Investment activity is still strong,but lack of assets for sale

Core markets:

10 – 11%Emerging markets:

17 – 18%

US is at 2%

EMEA is at 1.5%

24

61

78

54

55

58

80

90

93

sf (millions)

2017

2016

2015

2014

2013

2012

2011

2010

2009

Over 250 million sf new supply through 2017,led by China, India, Jakarta and Singapore SOLD

SOLDLOW

LOW

4 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 5

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

Regional Economy: Resiliency in Tough TimesEconomies across the Asia-Pacific

region have posted steady growth

this year, even with a challenging

global landscape. Policymakers

across the region have maintained

accommodative policy settings

that in turn, have sustained Gross

Domestic Product (GDP) GDP

growth in the 5.0% range thus

far. Subdued global conditions,

especially a slowing Chinese

economy, continue to weigh on

export activity, with Japanese

exports under further pressure from

the yen's ascent. Lower oil prices

have been a boost for the region’s

net oil importers, but declines in

prices for metals, minerals, and

agricultural products continued to

impact commodity producers in the

region.

Nonetheless, Australia’s economy

is transitioning away from mining-

driven growth as record low interest

rates keep consumption resilient.

India’s high GDP growth gives

strong indication of strong domestic

demand and may rise further if

promised legislation on a national

Goods & Services Tax (GST) finally

gets approved. Similarly, in emerging

Association of Southeast Asian

Nations (ASEAN) members, the

Philippines and Vietnam, continue

to outperform their peers, thanks to

robust consumption and investment.

Looking ahead, Asia Pacific is

projected to remain the fastest-

growing region. However, the

region is destined to remain in a

below-trend growth environment

in the near term, especially as

the slowdown in China restrains

trade activities. The combination

of macroeconomic discipline,

supportive policies, and structural

reforms will remain essential for

achieving stable growth in the

medium to long run. Summarized

below are five key takeaways of our

economic outlook:

Lower Growth Remains the Norm

The global economy is poised to

post lower growth in the near term.

The World Bank pegs global GDP

growth at 2.4%, down from the 2.9%

forecast in January 2016, and slower

than last year’s already weak pace. It

also cut its outlook slightly for 2017

to 2.8% from 3.1%. Similarly, growth

is also forecast to be moderate

in two of Asia Pacific’s largest

economies, Japan and China.

China will continue at about the

same pace as last year as the

authorities steer the economy

toward a more sustainable,

consumption-driven growth path.

However, concerns about an abrupt

halt in economic growth and the

health of China’s financial system

seem overdone. China’s deceleration

is projected to be orderly and largely

predictable thus allowing the market

to readjust to the new, lower growth.

Transitioning to an upper-middle-

income economy will provide new

opportunities, while targeted policy

support and structural reforms will

allow the nation to remain a major

engine of global growth.

In Japan, GDP growth is expected

to rise by a modest 1.0% annually.

Faster wage growth will be

necessary for improvements in

consumer sentiment and spending,

while domestic and external

pressures will hamper manufacturing

and export conditions. While we

expect a recovery in global trade

in 2017, it will be gradual and mild,

leading to modest recoveries in the

open economies of South Korea,

Taiwan, Thailand, and Singapore. In

Hong Kong, export performance

will be subdued, as the slowdown

in China drags down demand for its

goods with the impact on the retail

luxury sector seen as particularly

pronounced.

Expect “Extraordinary” Expansionary Policies

Policy makers are remaining

resolute in the face of renewed

global volatility following the

United Kingdom’s (UK) unexpected

referendum result on June 24.

On July 5, the Bank of England’s

Financial Policy Committee said it

agreed to lower capital requirements

for UK banks in a move that should

allow them to lend an extra £150

billion (US$199 billion) to UK

businesses and households, and

keep the economy flush with credit.

Such policies would augur well for

real estate as corporate borrowing

costs become lower when liquidity

enters the financial system. In

addition, slower interest rate

increases for the United States (US)

Federal Reserve Bank (Fed) are in

the cards, as well as a real possibility

of more monetary easing programs

by the European Central Bank (ECB),

and the Bank of Japan (BOJ).

In the Eurozone, the situation is

still fragile, and the ECB may face

pressure to step up again given

lower growth and weak inflation.

In Japan, the government is also

recalibrating its fiscal policy levers

as its growth remains tepid; Prime

Minister Shinzo Abe recently delayed

2017’s April sales tax hike by two

more years. Price declines across

Japan, combined with a stronger

yen, will likely compel the BOJ

to expand its monetary stimulus

arsenal.

In Australia, with Prime Minister

Malcolm Turnbull winning

the Federal election, the new

government is expected to focus

on shoring up the economy. An

accommodative monetary policy

combined with steady domestic

demand, should support economic

activity through the rest of 2016.

Indeed, monetary policy will remain

loose across the region, especially

with inflation expectations remaining

subdued, or inflation targets being

met in most parts of the region.

Meanwhile, healthy government

finances mean that fiscal policy can

remain supportive.

Walking the Reform Talk

This year seemed to mark a pivot

towards bolder reform measures

after a period of stasis in the region’s

00

02

04 06

08

102.4%Global

00

02

04 06

08

106.5%China

00

02

04 06

08

101.0%Japan

lower growth remains the norm

Negative Interest Rates!!wi

th

Such policies would augur well for real estate as corporate borrowing costs become lower when liquidity enters the financial system.

China’s economy will slow down as the authorities steer the economy toward a more sustainable, consumption-driven growth path.

INFRASTRUCTURE

TAXES

AVIATION

LABORREFORM

RETAIL

6 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 7

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

largest emerging economies.

With the Indian economy making

progress, attention has turned back

to reforms, which we believe will

unlock the country’s true potential.

In June, the Indian government

announced sweeping changes to its

foreign investment rules. While the

economy is still hampered by the

country’s infrastructure deficiencies,

the changes should boost

investment, and enhance India’s

standing in the international markets.

Notably, these new rules, together

with seeking government approval,

will allow foreign investors to

establish 100% ownership of

companies involved in defense, civil

aviation, and food products. Foreign

investors will also be permitted

to buy up to 74.0% of Indian

pharmaceutical companies even

without seeking the government’s

go-signal. Additionally, Prime

Minister Narendra Modi is expected

to win passage of a new law allowing

the imposition of a uniform goods

and services tax on the country.

Envisioned to take the place of the

current state-by-state taxation,

the new law makes it easier for

businesses to operate nationally.

The tax change, together with new

rules on foreign investment, could

have significant impact on India’s

economy.

In Indonesia, President Joko

Widodo’s reform agenda is looking

brighter after a lackluster 2015.

Following the deregulation drive

last year, he eased rules on foreign

ownership of companies in a wide

range of industries in February

2016. In April, he announced plans

to cut the corporate-income tax

rate to 20.0% from 25.0%, in a bid

to bring onshore profits that are

currently booked in Singapore. In

June, Indonesia’s Parliament passed

a tax amnesty bill that it hopes will

draw an estimated US$41.8 billion

of offshore funds. The government

hopes that these reforms will

increase overseas optimism in

Indonesia, and help to boost foreign

direct investments (FDI).

Emerging ASEAN Markets Poised for Take Off

Economic performance in emerging

Southeast Asia is poised to improve

further in 2017 as Indonesia and the

Philippines ramp up investment,

Vietnam sustains its expansion,

and Thailand gathers momentum.

However, weak oil prices will

continue to weigh on Malaysia. The

Philippine economy is set to lead the

ASEAN region, with the country’s

growing middle class, thriving

business process outsourcing (BPO)

sector, and the new administration’s

fiscal policy seen as drivers of

growth.

Newly-installed Philippine President

Rodrigo Duterte recently unveiled

a ten-point agenda for growing the

economy. These include reducing

tax rates and improving collection,

decreasing restrictions on FDI, and

increasing infrastructure spending

to more than 5.0% of GDP. If

implemented, these measures, along

with his pledge to lower corruption,

would help boost the economy’s

growth potential over the medium

term. With the new government,

we also believe that the Real Estate

Investment Trust (REIT) law will be

revisited.

Vietnam will also be a top growth

performer in the region. The

emergence of a highly competitive

export sector, benefiting from

manufacturers looking for more

Occupier Focus | Co-working: A Glimpse of The Future for Corporate Office Occupiers? Co-working spaces continue to grow in

popularity in the region. Since January

2015, the co-working segment has signed

over 1.0 million square feet (msf) of leases

in several gateway cities in the region.

Co-working spaces are popular choices for

independent workers, but the concept is

gaining traction among large corporations

with flexible staffing needs. Below are

some observations of our Workplace

Strategy expert, Marc Shamma’a:

I had the good fortune to visit Second

Home and WeWork co-working spaces in

London recently. Both are places where

innovative, independent, like-, community-,

and socially-minded people go in order

to ‘be somewhere’ when they are ‘getting

stuff done’.

‘Stuff’ (is) what we throwbacks in the fusty

old corporate world refer to using a four-

letter word, ‘work’.

Our interface with each other, as with the

outside world, is increasingly mediated

by a glowing screen, sometimes with a

keyboard attached. ‘Getting stuff done’ is

therefore location-independent, but just

because we can ‘get stuff done’ from our

homes does not mean that we want to.

We humans, want to ‘be somewhere’. We

are, by turns, solitary and social. Some

of us lean one way more than the other,

but mostly we want to ‘be somewhere’;

that adds zest to our daily experience,

and to whatever ‘stuff’ we need to do. In

addition to helping us ‘get stuff done’, that

somewhere must offer us the opportunity

either for social intercourse, to be alone in

public, as well as to hide away.

Co-working spaces meet these needs.

Second Home is situated just off Brick

Lane, in London's East End. It feels like a

university Student Union – bold colors,

with low-cost finishes that are nonetheless

thoughtfully put together. Its denizens are

often uber-informal in their appearance:

baggy sweaters, ripped jeans, Doc

Martens, and pony tails.

WeWork, another co-working space that

caters to a more upmarket user segment

(features occupants with) Dockers, blazers,

Timberlands, and tidy haircuts. They have

taken seven floors of a nine-story building

in the City of London, the Central Business

District (CBD); a Grade A prime location

next to the Moorgate Underground

Station. While Second Home’ rough edges

are absent, colors, finishes, and furnishings

are simple yet refined.

Both Second Home and WeWork have

oodles of buzz, and whatever your attire,

either of these two locations feels like a

great place to go in order to ‘get stuff

done’. Corporate offices rarely have the

same buzz. Why? It is not about cost.

A bag-of-fag-packet calculation shows

that the cost for a company to take up

space in WeWork could be 50.0% less

than the equivalent space they actually

lease. However, these spaces tend to

have less flexible terms, less appealing

environments, and none of the cool vibe.

Corporate occupiers, we need to ask

ourselves: “Why wouldn’t we throwbacks

embrace this brave new world of co-

working?” Landlords and developers, we

need to ask ourselves: “When will the

penny drop with the corporates? How can

we be ready when this happens? What can

we do to remain ahead of that curve?”

Watch this space.

Economic performance in emergingSoutheast Asia is poised to improvefurther in 2017

MARC EMILE SHAMMA’A Head of Strategic Consulting Global Occupier Services Asia Pacific

8 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 9

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

cost-effective alternatives to China,

will be pivotal to Vietnam’s economic

growth. Its exports are broad-based,

ranging from garment manufacturing

to electronics, while its export

markets are diverse. Vietnam is also

getting a lift from record FDIs due

to growing attractiveness as an

investment destination.

Prospects for growth in private

investment are enhanced by a

proliferation of trade and investment

agreements concluded over the

past year. These include trade

agreements with the European Union

(EU) and the Republic of Korea,

and commitments to participate

in both the US-led Trans-Pacific

Partnership (TPP), and the Eurasian

Economic Union (EAEU), led by the

Russian Federation. Vietnam is also

expected to benefit from the ASEAN

Economic Community (AEC), whose

members collectively form Vietnam’s

third-largest export market after the

US and the EU. The agreements are

expected to stimulate investments,

and at the same time, serve as

signals to the business community

of the government’s renewed

commitment to liberalize the

economy.

No BREXIT Hangover1.

Economic shock from the British

referendum to exit from the EU

is strongly felt in the UK, but the

overall impact on the rest of the

world will depend largely on the

duration of the economic, financial

and political uncertainty. For Asia,

the equity markets initially tumbled

following the results, but have since

recovered some of the losses. In

addition, given that the region’s

exports to the U.K. only account

1 C&W Flash Market Report | Asia Pacific to Weather BREXIT Spillover

for just over 2.0% of total exports,

we are unlikely to see major impact

on the region’s trade environment.

While knock-on effects on the EU,

which accounts for an estimated

12.0% of exports from Asia Pacific,

could have a deeper impact, the

union’s largest economies, France

and Germany, are expected to

remain resilient. If the UK does exit

the EU, we also see opportunities

for the UK to be more engaged

with the region, as it focuses on

strengthening its relationships

with China, India and other growth

hotspots. are expected to remain

resilient. If the UK does exit the EU,

we also see opportunities for the UK

to be more engaged with the region,

as it focuses on strengthening its

relationships with China, India and

other growth hotspots.

Technology: Equipping the New Age BrokerThe current spate of digital technology

attempts to bridge the information

asymmetries currently inherent in

commercial property markets, whether

due to distance, time or the agency

dilemma, and improving access for

consumers. From the proliferation of

Internet platforms on listings to virtual

viewings that thrive on cutting edge

virtual reality (VR) technology, these

facilitate to a broader audience reach;

with the potential to promote higher

transparency in the many opaque markets

in our region.

This can readily be appreciated in

Geospatial Analytics, indoor mapping,

as well as virtual viewing. These allow

consumers to visualize spaces and

buildings yet to be completed, or in

another location; allowing Commercial

Real Estate (CRE) operators to readily

create specific strategies to market their

spaces. This in turn makes it easier for

decision makers to compare properties,

and do their due diligence even on their

smartphones or desktop. However, at the

moment, due to the higher transaction

values in commercial real estate,

incumbents have every incentive to hoard

data rather than share it. This story is still

in progress, but it is apparent that the

trend is toward increased transparency.

The Internet-of-Things (IoT) is a phrase

that has been discussed and repeated for

some time now. While the evolution of

IoT technologies will no doubt usher in a

new era for smart buildings, it also has the

potential to go beyond just maintenance.

Enhanced tracking and monitoring of a

building, and at the portfolio level, using

portfolio analytics, can result in more

granular valuations. Such data can readily

be called on by market players, such as

investors, to determine the health and

consequently, price of an asset.

Why are all these important? Real estate

in our region remains expensive, and

mistakes will be costly. With technology

aiding better risk management, liquidity

in the marketplace will increase. We

believe these technologies will be able

to entrench another emerging digital

revolution, crowdfunding. Real estate

syndication, which allows investors

to pool capital in order to purchase a

fractionalized interest in a property has

been around for decades, but real estate

crowdfunding takes that process online,

thereby increasing access for investors.

While it will and should attract regulatory

oversight, crowdfunding could set in

motion a new method of raising funds and

financing projects.

In most cases, the dismantling of

barriers will result in a process of

disintermediation. However, we do not

see these technologies as necessarily

displacing the role of a broker but rather

engender an evolution that will help

facilitate the real estate decision making

process. First, the skill sets of the new

age broker will have to expand in order to

differentiate themselves to clients. We see

the rise of a more consultative and tech

savvy broker.

Second, brokerages will also need to

diversify into consultative opportunities

in space needs and location advisory. The

increase in information and transparency

coupled with the rise of a collaborative

economy will continually redefine space

usage. The increase in demand for

flexibility will drive the need to have more

fluid spaces. This will necessitate a hybrid

approach to leases: long-term leases for

large spaces, and short-term leases for

dynamically configurable spaces. We

see the creation of co-working spaces to

be a fundamental requirement of future

developments.

If the UK does exit the EU, we also see opportunities for the UK to be more engaged with the region

10 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 11

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

Office Sector: The Rising Tide is Lifting All BoatsGiven that the economy and the

labor market across the region is

on firm ground, the office sector is

poised for increased demand and

rent gains across the 30 major cities

tracked through 2017. Below are

some of the overarching themes that

we expect over the next two years:

Broad-based absorption gains across the region, posting new records

Absorption is on track to reach an

eight-year high of 90 million square

feet (msf) this year, and is set for

a higher mark of over 93 msf in

2017. All markets will post gains

through 2017 except for Perth in

Australia, where weak demand will

sustain elevated vacancies. Markets

expecting a surge in new supply led

by Shenzhen, Shanghai, and Beijing

in China and Mumbai in India will

see the most sizeable increases.

Even with China growing at a slower

pace, the continued expansion of

its service sector, particularly the

development of financial services

and the Internet, have been fueling

demand. The government has made

innovation and entrepreneurship

a key national policy since 2014,

and has led to a proliferation of

technology companies across China.

In India, absorption is expected

to see a resurgence especially in

Hyderabad and Pune as economic

fundamentals strengthen further.

Bengaluru is still expected to

post the highest demand due

to continued expansion of the

Information Technology/Information

Technology Enabled Service (IT-

ITeS), and e-commerce sectors.

At the same time, its outsourcing

industry, the country’ economic

growth pillar, has been bracing for

some disruption. Cloud computing

has begun to affect new space

demand as outsourcing contracts

shrink, and job creation slows down

as more companies are opting

for their own cloud storage, and

replacing custom-made software

with off-the-shelf cloud versions.

Notably, labor and other costs

have increased for these offshore

outsourcers while companies would

still like to see continual savings.

Similarly, Manila, another thriving

hub for BPO services in the region,

is on track to achieve a record

absorption rate through 2017. BPO

demand remains strong, and has

taken up the majority of the new

space expected to be completed

this year. According to the trade

group Information Technology and

Business Process Association of the

Philippines (IBPAP), as automation

starts to displace some humans

from low-end repetitive tasks,

the outsourcing sector is already

mapping out plans to move the

industry towards higher-paying

upscale services, such as health-

care management, animation, game

development, and engineering. At

the same time, the country will face

competition from other emerging

rivals like Indonesia and Vietnam,

who are rapidly developing their own

BPO industries.

Rampant new supply to push up vacancies across the region

Office development will remain

robust, with completions expected

to peak at 140 msf this year, and

120 msf in 2017. The majority

of new developments will be in

emerging markets, where office

stock is set to grow by 27.0% next

year, compared to 15.0% in core

markets. In China, inventory is

expected to double in Shenzhen

by next year, and grow another

50.0% in supply-heavy Chengdu.

Completions will be at their record

levels through 2017 for Ahmedabad,

Mumbai and Jakarta, and will add

more than 25.0% to their current

office stock. Consequently, those

cities mentioned above stand to

post the highest vacancy increases

of 7-10 percentage points, with

Ahmedabad’s vacancy rate of 52.0%

in 2017 being the highest in the

region. Singapore is expected to

post the highest vacancy increase

of 8-9 percentage points between

2015 and 2017. The city state will

witness record supply of 4.0 msf to

be delivered by next year.

Rising Rents through 2017

With strong leasing market

performance come higher rents, a

trend that could add further strain

in this era of cost containment. Most

markets will see an improvement

in rents on the back of stronger

occupancies in 2017, and 14 cities will

even post record rents. The chart-

topping office rents in Hong Kong’s

Greater Central will be underpinned

by the strong interest from mainland

China companies, and also serves as

a testament to the city’s geographic

constraints. However, the pace of

rental increase will slow down further

next year given softer prospects of

the global and Chinese markets.

Falling vacancies through 2017 will

favor landlords in Tokyo, Sydney, and

Melbourne, where strong demand

will keep Grade A vacancies hovering

close to their equilibrium of 7.0%.

Rents could begin to stabilize in

core markets including Singapore,

Brisbane and Perth. Meanwhile,

majority of the emerging cities could

see a resumption of modest rent

growth of 1.0-2.0% through 2017;

only rents in Jakarta are forecasted

to fall by 10.0 % from their 2015

levels.

O�ce development will remain robust, with

completions expected to peak this year at

140 msf and 120 msf in 2017.

Investment Activity: The Show Must Go OnThe flow of investor capital from

around the world into office

properties in the region continues

to be unabated. So far in 2016, over

US$45 billion worth of real estate

have changed hands through June,

slightly below the volume over the

same period a year ago. Singapore

has been the epicenter of landmark

transactions this year. The sale of

Asia Square Tower 1 to the Qatar

Investment Authority for US$2.5

billion set a new record in Asia

Pacific for the largest single asset

transaction in the last five years;

likewise, the purchase of the Straits

Trading Building in Battery Road

for US$2,600.001 per square foot

(psf) set a new record for psf price

in the city-state. Inter-regional

investors continue to be attracted

to Australia’s high-quality assets,

and above-average yield spread.

As highlighted in our Capital

Insights newsletter, A Growing

Disconnect; Sentiment and

Fundamentals, in March, we expect

investment activity in the region

to be supported by conducive

investment policies, ample liquidity,

and sound occupier fundamentals.

Even as the year brought more

uncertainty to the world economy,

we can only expect policies to

remain accommodative and thus,

supportive of investment activity.

Notably, mounting concerns on

the global economy have already

1 The price was S$560 million price, or a record of about S$3,520 psf based on the net lettable area of 158,897 square feet. This would surpass the S$3,125 psf for 71 Robinson Road, which was sold in 2008.

pushed down government bond

yields. In Japan, the 20-year yield

dipped below zero for the first

time on July 6, the 30-year yield

dropped to as low as 0.015%, while

the 10-year yield hit a record low of

minus-0.275%.2

Indeed, such backdrop will

continue to support the attractive

yield spreads seen in many core

markets in the region including

those in Australia, Japan, and

South Korea, and still fuel a yield

compression cycle especially in

some markets with above-average

rent outlook. Additionally, the

push for more comprehensive

reforms, and massive infrastructure

developments in many emerging

countries will draw foreign investor

interest. Consequently, we can

expect a rebound in the second

half since the current environment

is very conducive to investing

similar to 2015, a record year for

the region in terms of investment

volume.

2 “Japan’s 20-Year Bond Yield Turns Negative,” July 6, 2016, Wall Street Journal.

13-1

5%

3-Year Rental growth slowing*

year

‘10-‘13year

‘11-‘13year

‘12-‘15year

‘13-‘16year

‘14-‘17

8-10

%

6-8%

3-5%

3-5%

COMMERCIAL PROPERTY

SUPPLY

OUT OF ORDER OUT OF ORDER OUT OF ORDER OUT OF ORDER OUT OF ORDER OUT OF ORDER

OUT OF ORDEROUT OF ORDER

OUT OF ORDEROUT OF ORDER

OUT OF ORDER

Office developmentwill remain robust,with completionsexpected to peak at140 msf this year, and 120 msf in 2017.

* 5-Year rental reversion for Australia

12 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 13

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

Tokyo: Stable and ConsistentPrime Minister Shinzo Abe

proclaimed that a new raft of

“Abenomics” would be introduced

following the victory of his ruling

coalition in the recent election

for the country’s upper house of

parliament. The government is

expected to prepare a new stimulus

package that could be as large

as JPY10 trillion (US$96 billion),

and includes plans to upgrade the

nation’s transport infrastructure as

well as expanding childcare and

nursing-care services.

The unemployment rate has

steadily declined under Abe’s

stewardship. Improved corporate

financial performance backed

by the economic growth has

benefited the office sector through

a commensurate increase in

absorption rates and rents. The BOJ

has been successful in impacting

the capital markets as first, the yield

curve has flattened, second, interest

rates have turned negative in real

terms leading to wider yield gap,

and lastly, property cap rates have

compressed.

With more government support

to sustain economic growth,

we can expect Japan’s external

competitiveness and corporate

profitability to improve, and

consequently maintain the positive

momentum of the office sector.

Given the benign office development

pipeline, we expect the vacancy

rate to remain below 5.0% in 2016

through 2017. However, the pace of

rental increase is expected to be

gradual especially with the expected

high volume of supply after 2017.

As with the last two years, the

Japanese market has more buyers

than it has available assets. Office

assets are investors’ top choice, but

are difficult to source. The retail and

hotel sectors are the other bright

spots in Japan, driven largely by

surging tourism that has, in turn,

been generated by a weak yen over

the last three years, as well higher

incomes. While Tokyo remains

the focus, regional cities are also

drawing investor interest given the

scarcity of investment opportunities

in Tokyo, and in turn, compelling

them to seek opportunities in those

locations.

Seoul: Muddling ThroughSouth Korea’s economy remains

lackluster: exports are slumping,

while domestic demand remains

weak, and consumer spending has

yet to make a solid pickup. As such,

businesses remain cautious in hiring;

hurting employment growth, and

resulting into soft conditions in

the office sector in Seoul. Leasing

volume continues to decelerate this

year as consolidations, relocations,

and renewals dominated activity,

while new supply remained rampant.

Tenants have been cautious in

their expansion plans; as a result,

absorption gains are expected to

remain below average through next

year, and keep vacancy rates at

double-digit levels. On a positive

note, the growth of start-up firms in

the IT industry such as the finance

technology (fintech) sector is

stimulating leasing demand. At the

same time, serviced office providers

are in expansion mode, driven partly

by the boom in start-ups. Shared

workspace provider WeWork, a

US company, recently entered the

Korean market.

The challenging business

environment is causing many

large Korean companies to shed

their unprofitable business arms,

and focus on core business areas

where they have a competitive

advantage. Because of this, many

of their subsidiary companies are

now facing financial restructuring.

The Korean government already

announced plans for a US$17 billion

(KRW20 trillion) fiscal stimulus

package, with a focus on supporting

companies with the most risk from

corporate restructuring. However,

we expect affected companies to

continue divesting their assets.

Case in point is the Samsung Group,

whose affiliates have brought their

properties to the market as they

relocate to the suburbs. In light

of this, we view more investment

opportunities to emerge as

corporations strengthen their

balance sheets. With cap rates still

high relative to other core markets,

and widened spreads following the

recent rate cut, opportunities in

Seoul’s offices remain compelling.

Beijing and Shanghai: Still Room to GrowChina’s tier 1 cities are set to see

record volume of supply through

2017, with Grade A stock expected

to grow 30.0-40.0% from 2015. In

Beijing, we expect nearly 25 msf to

be completed until the end of the

year through 2017, with emerging

submarkets accounting for 60.0%

of new supply. Given high rents

and tight vacancy in the CBD,

especially on Financial Street, the

emerging business districts provide

alternatives for companies looking

to expand or relocate at affordable

rates.

In Shanghai, we expect to see

the completion of another 24

msf through the remainder of

2016 to 2017, with a significant

portion located in decentralized

areas. However, both Beijing and

Shanghai are expected to post high

levels of absorption gains through

next year, with record levels even

likely to be recorded in Shanghai.

Although China’s economy remains

on a structural downward growth

path, we expect an upturn in job

creation to persist in its service

sector especially with innovation

and government reforms being

relied upon to deliver this target.

The service sector is set to add

another 900,000 jobs in both Beijing

and Shanghai through 2017, and

potentially generate around 50-60

msf in net new requirements through

2018. Consequently, while supply

will exceed demand in both cities, we

SHANGHAI, CHINA

14 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 15

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

expect vacancies to remain relatively

low and sustain high rents. On the

investment side, with a favorable

backdrop combined with low interest

rates and a stabilizing Chinese Yuan

(RMB) exchange rate, we expect

more funds to return to the market.

Hong Kong: Bracing for Slower GrowthMainland Chinese demand has

largely been instrumental for

the recovery in Greater Central,

Hong Kong’s CBD, over the past

two years. Grade A rents have

surged close to their peaks last

seen in 2011 while availabilities are

at ultra-low levels, dipping below

5.0% in Greater Central through

June this year. While we expect

sustained demand from mainland

China companies, growth is likely

to moderate to a more sustainable

pace especially as many of the

major Chinese firms already have a

presence in Hong Kong. Given that

Hong Kong’s economy continues

to face challenges from the lack

of other growth drivers outside

of exports, housing and finance,

demand from other corporates will

remain volatile, with a number of

international banks even continuing

to trim headcount. As a result, rental

growth for the CBD is likely to slow

this year. Another factor that can

further hold back rent increases in

2017 is that CBD-alternative supply

is expected to come online in

2017-18. Notably, some of projects

slated to be completed in 2017-2018

are positioned to take front office

tenants from Central, given their

convenient and upscale locations.

These projects should be well suited

for middle office operations of major

investment banks, some of which

are still located in Central. Case

in point is Mizuho Bank, which has

committed more than 100,000

square feet (sf) at K11 development

in Tsim Sha Tsui scheduled for

completion in 2017; its relocation

plans will include vacating its office

space of nearly 60,000 sf in Central.

Nonetheless, major landlords are

proactively locking in their largest

tenants and consequently, we do not

foresee any large spike in vacancies,

and thus expect rents in Greater

Central to remain high and even eke

out modest increases. Additionally,

there are still pockets of demand

strength. Insurance companies

continue to expand their uptakes

especially in decentralized locations;

and recently, Hong Kong welcomed

its first major co-working space

operator WeWork in the city.

Mainland Chinese companies

continue to show their interest in

acquiring en-bloc office properties

in Hong Kong. The most significant

transaction was the acquisition

of Dah Sing Financial Centre in

Wan Chai by China Everbright for

US$1.3 billion (HK$10.0 billion),

the second largest en-bloc office

transaction ever recorded in Hong

Kong. Given prospects of continued

rental growth, the office sector will

continue to be the main focus of the

Hong Kong investment market.

Singapore: Looking Beyond the Subdued MarketThe combination of a looming

high volume of new supply and

weak demand remains the key

headwinds for the office sector

in Singapore’s CBD. A record 4.0

msf will be completed by next year,

which are largely available to date,

and creating ample opportunities

for tenants to upgrade as seen in

some of the significant transactions

this year. Leasing activity is also

moderating due to international

banks continuing to shrink their

footprints, not to mention that

a slowing economy and low

unemployment rate are holding back

activity.

Rents for Grade A properties in the

CBD have already slipped more

than 15.0% since the first quarter of

2015, and will likely decline another

7.0-10.0% year-on-year (YoY) in 2016

as vacancies soar to their highest

level since the Global Financial Crisis.

However, we view this subdued

performance as transitory. New

construction will moderate

post-2018. Additionally, from

an economic perspective,

progress continues to be

made on the city-state’s

transition to services,

decreasing reliance on

exports.

This sector’s

importance,

relative to

manufacturing,

will continue

to grow

especially

with

HONG KONG

16 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 17

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

Singapore’s stature as a destination

for regional headquarters and as

a financial center in Asia Pacific.

As mentioned in the 2016 global

financial centers index, Singapore

overtook Hong Kong as the third

largest global financial hub, behind

only London and New York.

Singapore is home to over 4,000

headquarters and growing, and

evolving to the Silicon Valley of Asia,

as it is home to many start-ups.

Co-working operators are also

vigorously expanding amidst

sustained demand for more flexible

working spaces. As such, we expect

this changing focus in the city

state’s economy, together with the

government’s ongoing Smart Nation

initiative among others, to provide

new demand growth catalysts that

will further diversify its tenancy and

restore vibrancy in the office market.

Tenants who need not be in the CBD

will also have plenty of alternative

locations in upcoming commercial

clusters including Woodlands

Regional Centre and Paya Lebar

Central.

Jakarta: Gradual LiftoffIn Indonesia, the effects of the

government’s fiscal stimulus policies

are more likely to be seen this

year. Most of the new stimulus

measures are focused on fostering

a friendlier business environment.

In 2015, Indonesia ranked poorly

among its ASEAN peers in the

World Bank Ease of Doing Business

Index, placing it 109 out of 189 total

countries. Fiscal measures are aimed

at enabling land acquisition, and

lowering import duties and export

taxes.

With these positive developments

combined with infrastructure

investments, the government

hopes it will increase optimism

from businesses. Effective public

investment will help advance the

business environment, helping fuel

more investments and job creation.

Consequently, we expect Grade

A absorption to double in 2017,

after dipping to less than 1.0 msf

this year. Occupiers will also be

spoiled for choices as large office

completions are expected through

2018. Additionally, occupiers will be

able to take advantage of lower rents

through 2018 due to the abundance

of options resetting Grade A rents

at least 20.0% lower than their peak

levels in 2014.

Manila: Continuing to ShineBPO remains one of the Philippines’

top employment and broader

economic growth generators. The

IBPAP is projecting the number of

total full-time BPO employees to

hit 2.6 million by 2020, more than

double current levels. If this target

is reached, the BPO industry would

need at least another 50 msf in the

next four years.

Construction is catching up with

nearly 20 msf to be delivered

through 2018, majority of which is

located in Manila’s new prime CBD,

Bonifacio Global City (BGC). While

oversupply concerns have surfaced,

leasing activity continues to show

strength. Pre-leasing activity

remains vibrant, with more than

half of new supply for 2016 already

committed to BPO companies and

other new corporate occupiers. In

addition, we continue to expect

vacancies to remain low, and rents to

maintain their uptrend.

Some developers are also cautious

in launching more office buildings,

with some projects being pushed

for completion to 2017 rather than

this year. Longer term, one of the

biggest risks to the BPO sector

is artificial intelligence (AI). If the

technology succeeds, this has the

potential to replace call center jobs,

which currently account for over

60.0% of outsourcing revenues.

President Duterte has outlined plans

to fund education programs tailored

to the needs of employers, and help

the outsourcing sector fend off the

challenge of AI.

Ho Chi Minh City: Ready for Take-offFDI is seen to strongly support

the expansion of its key sector,

manufacturing; while greater

integration into the global economy

is expected to support the outlook.

Participation in trade pacts will mean

that sectors of its economy will be

open to foreign businesses. Reforms

to regulate the real estate market by

making developers accountable, as

well as loosened foreign ownership

restrictions have boosted business

sentiment.

Consequently, demand for Grade

A spaces is proceeding at a steady

pace, and is keeping vacancy rates

low at 5.9% through the second

quarter of 2016. Leasing activity is

expected to maintain solid expansion

with several projects coming on

stream; leading to single-digit

vacancies and rising rents through

2017. Indeed, sustaining a thriving

office sector requires consistent

policies supporting the development

of infrastructure and human capital,

an improving investment climate,

and government reforms. There is

also a need to develop more efficient

and cost-effective urban centers

that can support growth of varied

businesses.

India: The Cycle Turns UpThe continued expansion in the

IT/ITes sector has been the main

catalyst to the resurgence of the

office sector in the eight major

cities tracked in India. However, the

National Association of Software and

Services Companies (NASSCOM)

predicts that Indian IT companies

will not be hiring as much in 2016

as they had in the past, especially

as the threat of process automation

accelerates.1 Nonetheless, NASSCOM

1 “IT Jobs to Drop 20% in FY17: Nasscom Chief ”, International Business Times, April 22, 2016.

HO CHI MINH CITY, VIETNAM

18 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 19

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

still expects the country’s IT industry

to grow 12.0-14.0% during 2016-17.

Additionally, India can count on

growth from other sectors with

further reforms. Central government

policy makers forecast that their

spending on infrastructure will

rise to around 8.0% of GDP in

a few years from around 5.0%.

This plan could help attract FDI

flows into manufacturing-related

sectors, and help improve India’s

business environment. Against

this backdrop, we expect positive

business sentiment to spur occupier

demand across its major cities, with

absorption expected to rise through

2017, and rent increasing in some

markets.

Nearly a third of the demand will

continue to be in Bengaluru which

will help sustain its low vacancies.

Similarly, we expect Chennai,

Hyderabad, and Pune to post single-

digit vacancies on account of solid

demand. Notably, Grade A rents

have already risen over 10.0% in

those markets from 2015, and could

climb another 10.0% next year. In

Hyderabad, despite having several

projects underway, majority of

office developments in Madhapur

are already 50.0-60.0% pre-leased.

As a result, much of the availability

will be concentrated in Gachibowli,

and we could expect continued

rental appreciation in Hyderabad.

Meanwhile, Delhi NCR and Mumbai

are also set to record surges in office

completions, resulting in double-digit

vacancies through 2017; however,

much of these availabilities will be

concentrated in suburban locations.

The relaxation of taxation on REITs

has made some developers and

private equity (PE) firms in favor

of establishing REITs. Institutional

investors are continuing to actively

seek opportunities in completed

and leased commercial assets. As

per the Security and Exchange

Board of India (SEBI) guidelines,

REITs are required to invest 80.0%

of their funds in completed, income-

generating, commercial projects.

This also contributed to the increase

in investments in retail assets which

have remained muted to date. As

such, PE investments in office and

retail assets, especially from those

investors planning to launch their

REITs, are expected to rise. The

current Grade A non-strata sold

office inventory has the potential

to generate rental income of about

US$4.3 billion per annum. This is

forecasted to reach over US$7.3

billion annually by 2020 with

Bengaluru, Delhi-NCR, and Mumbai

accounting for about 77.0% of the

share in rental income2.

Sydney and Melbourne: The Only Way is UpStrong results in the business

conditions supports our view that

Australia’s economy continues its

transition towards non-mining-

driven growth. Ongoing employment growth is supporting a renaissance in

the office sector. In the Sydney CBD,

2 India: Well Poised for PERE Investments, Asia Capital Insights, May 2016.

demand gains for the 12 months

ending January 2016 soared to

their highest level since 2007. Even

if stock additions were robust, the

vacancy rate for Grade A space fell

to 5.4% while rents increased for

the 12 months ending January 2016.

Similarly, strong tenant demand

has boosted occupancies and rents

in Melbourne CBD over the same

period.

Going forward, Australia’s

near-term economic outlook

remains upbeat, supported by an

accommodative monetary policy,

and steady domestic demand. The

2016 budget is also noticeably

focused on supporting Australian

businesses, although the final plan

will likely be tweaked due to the

government’s lack control of control

over the Senate. Still, the policies

are geared towards supporting

Australia’s economic transition from

a mining investment-driven growth

to non-mining-led growth. These

include funding for innovation and

science, business tax cuts, and

superannuation changes, among

others. With the changes, we expect

the creation of more service jobs

that will hopefully lift up the office

sector.

With a modest development

pipeline and continued office stock

withdrawals owing to residential

conversion and compulsory

acquisitions to make way for new

infrastructure, we estimate vacancy

rate to trend lower in Sydney, and

underpin the resumption of stronger

rental growth. Similarly, the outlook

for Melbourne CBD calls for falling

vacancy and rising rents, given

the combination of robust tenant

demand, limited new supply, and

continued stock withdrawal.

However, office development

in Sydney could ramp up in the

long term. The City of Sydney is

proposing a change to development

of the CBD in an attempt to balance

the city’s residential boom with the

need for office and hotel projects,

as well as cultural space3. The draft

Central Sydney Planning Strategy

would require at least half of all units

in new towers over 55 meters to be

commercial. As a further incentive,

developers could build above current

height limits, up to 300 meters,

if the towers were exclusively for

commercial use. Another key change

would be the introduction of an

affordable housing levy, phased over

a period of time, but will eventually

cost commercial developers 1.0%

of the value of the project, and

residential developers 3.0% of their

value.4

In terms of investment, Australia

continues to be a preferred

destination by investors seeking

exposure to quality assets, and

steady income yields, which are

amongst the highest in Asia Pacific.

Sydney and Melbourne tend to draw

strong interest, especially as both

cities stand to benefit from ongoing

structural change in Australia’s

economy. However, transaction

volumes are being limited by a lack

of available stock, forcing investors

to increasingly look to non-core

investment options. This combination

of strong buyer demand, improving

fundamentals, and favorable financial

conditions could mean that cap rates

still have room to run.

3 Central Sydney Planning Strategy: Commercial Property Impact, Australia Property Insight, July 2016

4 Sydney CBD plan to curb new apartment towers, Australia Financial Review, July 13, 2016.

SYDNEY, AUSTRALIA

Nearly a third of the demand will continue to be in Bengaluru which will help sustain its low vacancies.

20 | Cushman & Wakefield Research Publication Asia Pacific Office Outlook | 21

ASIA PACIFIC: F INDING STABILITY AMID VOLATILITY

For more information about C&W Research Asia Pacific, contact:

Sigrid ZialcitaManaging Director Research & Investment Strategy, Asia Pacific+65 6232 [email protected]

Jason Whitcombe Managing Director Global Occupier Services, Asia Pacific +65 6232 0896 [email protected]

Gary Hollis Managing Director Head of Capital Markets, Asia Pacific +65 6393 2328 [email protected]

Jeremy Pearson Managing Director Tenant Advisory Group, Asia Pacific +852 2956 7072 [email protected]

For more information about other C&W services, please contact:

SINGAPORE

About Cushman & Wakefield

Cushman & Wakefield is a leading global real estate services firm that helps clients transform the way people work, shop, and live. Our 43,000 employees in more than 60 countries help investors optimize the value of their real estate by combining our global perspective and deep local knowledge with an impressive platform of real estate solutions. Cushman & Wakefield is among the largest commercial real estate services firms with revenue of $5 billion across core services of agency leasing, asset services, capital markets, facility services (C&W Services), global occupier services, investment & asset management (DTZ Investors), project & development services, tenant representation, and valuation & advisory. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

©2016 Cushman & Wakefield, Inc. All rights reserved.

Cushman & Wakefield, Singapore3 Church Street Samsung Hub #09-03 Singapore 049483www.cushmanwakefield.com