Financing Urban Infrastructure

26

The Project Cycle World Bank Identification: Who is the responsible authority? Who are the stakeholders? How are they involved in the project? Is the project consistent with a wider plan or programme such as an economic development strategy? Have all options (including datum) been considered in the delivery of the wider plan? Is there a budget? How and who will finance the project? Preparation: Prepare several options. Produce feasibility study which sets out facts and figures for options. Determine the criteria for evaluation. Appraisal : This involves comparing the options identified. Determine appraisal components (e.g. CBA, financial analysis, environmental assessment) Negotiation/ Decision: Are decision makers satisfied with appraisal information? Implementation: Monitoring and review during life of project (not just construction). Are the objectives being met? Mid-term review. Evaluation: On completion: Has the project achieved i ts aims? Why is there a different outturn? Financial Plan

Transcript of Financing Urban Infrastructure

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 1/30

The Project Cycle

World Bank

Identification: Who is the responsible authority? Who are the

stakeholders? How are they involved in the project? Is the projectconsistent with a wider plan or programme such as an economicdevelopment strategy? Have all options (including datum) beenconsidered in the delivery of the wider plan? Is there a budget?How and who will finance the project?

Preparation: Prepare several options. Produce feasibility studywhich sets out facts and figures for options. Determine the criteriafor evaluation.

Appraisal: This involves comparing the options identified.Determine appraisal components (e.g. CBA, financial analysis,

environmental assessment)Negotiation/ Decision: Are decision makers satisfied withappraisal information?

Implementation: Monitoring and review during life of project (not just construction). Are the objectives being met? Mid-term review.

Evaluation: On completion: Has the project achieved its aims?Why is there a different outturn?

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 2/30

Financial Plan

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 3/30

Financial Analysis

UE1 Term 2 Session 3 17

DSM Land Civil Works Equipment Staffing Materials Repayments Self-gen Grants Loan

Year 1 1 25 16 10

Year 2 1 25 16 10

Year 3 1 30 15 16 30

Year 4 10 10 5 2 5 5 12 15

Year 5 12 2 5 10 9

Year 6 12 2 5 10 9

Year 713 2 5 11 9

Year 8 13 2 5 11 9

Year 9 14 2 5 12 9

Year 10 14 2 5 12 9

…

Year n 20 2 5 15 12

Affordability at Appraisal: Are there sufficient sources of funds to finance the applications?

Capital costs Recurrent costs Revenues

APPLICATION OF FUNDS SOURCES OF FUNDS

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 4/30

Key Challenges:

Challenge Characteristics Case Studies

Limited resource raising authority of UrbanBodies

Municipal vs State vs National allocation of municipal taxes, duties, tolls and fees.

State vs Municipal resource raising in India

Short & Long Term Capital Investment returns after 20-30 years Istanbul, Turkey

Use values vs Exchange values Insertion of commercial space to financebasic use values

King's Cross Redevelopment, London

Fiscal health of national government Issuing bonds on behalf of municipalities inhigh risk areas rather than guaranteeing

municipal bonds

Infrastructure Finance Corporation Limited,South Africa

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 5/30

Sub-National Expenditure Responsibilities in China

(Peterson 2007)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 6/30

(Peterson 2007)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 7/30

Financing Public Projects

Developer PaysCharacteristics Examples

Tax Incremental Financing Financing municipal bonds or developer investmentsthrough increased taxes, based on property values

Chicago TIF areas, USA

Community incentives with recapture agreements

• Clawbacks

• Recision

• Recalibration

Supply-side economics to maximise jobs & tax-base.- Recover all subsidy costs.

- Cancel subsidy agreement.- Adjust subsidy to reflect changing business condition.

State of Maine Clawback Act 2243, USA

Pay for impact costs of development

• Impact fees• developer exactions (infrastructure or services)

• developer constructed off site infrastructure

Burden of finance to groups not yet present in the area

- Internalising the social costs of marginal development- Based on negotiation

- Spreading benefits to fringe areas

Section 106, UKSection 106, UK

Land Leasing (Long term occupancy & development rights) Ending the free/ cheap use of land resources. Capturingland value increments due to public investments

Guangdong, China

Public Private Partnerships Revenue earmarked to finance contracts Athens International Airport, Greece

Public Financing

Bond Issuance Large Scale projects that can typically pay for themselves TfL, London

Government Fiscal Input Invest early at times of low prices Shanghai Chengtou Corporation

Enterprize Zones Government Incentives Navi SEZ Mumbai, IndiaRevolving Loan Funds (RLF's) Affordable capital for non-traditional businesses South East Community Loan Fund, UK

Amalgamating tax bases Mixing high income and low income areas South African Townships

Cross border jo int ventures Saving costs on basic service provision Local Authori ty Service Procurement- UK

Acquiring Land CPO, Government Offices Relocation Rural Land Acquisition, China

Catalyst Financing

Public Attraction Projects Marketing Projects Guggenheim Museum, Bilbao

Brownfield Projects High initial costs of remediation determining land use Greenwhich Millenium Village, UK

Retail Finance Financing public infrastructure through retail King's Cross, London

Private Financing

Bank Credit Direct and indirect revenue streams outline Marmaray Tunnel Project, Istanbul, Turkey

Joint Ventures Long term partnerships. Profits accruing to both parties First Base & Barking- Dagenham

(Peterson 2007; White, Bingham, and Hill 2003; Chapman 2008)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 8/30

Who pays?: temporal dimensions

Characteristics Example

Previous Generation Monetising an inherited public asset Land leasing

Current Generation Paying for the use of infrastructure User fees

Current to Near Future Generation Paying for the use of new infrastructure Impact fees

Future Generation Repayment of loans Fiscal spending

Adapted from (Peterson 2007)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 9/30

Tax Incremental Financing: An alternative to redistribution?

Designate an area in need of improvement. GIS data can generate boundary lines. Typically the area is run down and there are no city-wide financing opportunities or ones based on user fees. Most States only allow the use of TIF in areas where there is a sufficient

number of 'blighted' properties.

Municipality prepares a redevelopment plan with key projects to be developed within district. These projects include historicpreservation, industrial expansion and downtown redevelopment. All these projects need to create substantial increases in the value of

property.

Municipality in collaboration with developers prepare eligibility study to demonstrate that the area meets 'blight' criteria. Study alsoneeds to prove that no combination of bonds, abatements and tax revenues are sufficient to attract private investment.

Once area is designated all properties within the area are valued and this figure is held constant for a fixed period. All the propertyvalues added together to give a base against which growth will be measured.

Municipality uses coercive powers such as land assembly, site clearance, street improvements to make district attractive to potentialbusinesses or developers.

As private investment is attracted in the area, the assessed value of property and tax are expected to rise. Difference between newassessed value and base is the Tax Increment.

TIF district has overall control of incremental tax over any other taxing bodies with jurisdiction over the area.

To kick-start process, municipalities issue a bond or ask a developer to pay up front. A developer may for example develop a plot of landwhere there is a rent-gap. Any incremental tax due to the new use will be diverted to the TIF. Municipalities then pay the developer once

a year as the incremental taxes are received from the increase in value of all properties.

Critiques

Too often the municipality captures increment which it did not induce. For example city-wide regeneration. School or other tax jurisdictions are therefore losing tax revenue.

Property value increases offset with property value decreases outside TIF areas

Retail moves to different parts of the same region so overall benefits to municipality are offset

Rising property values may in the long run displace residents

(White, Bingham, and Hill 2003)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 10/30

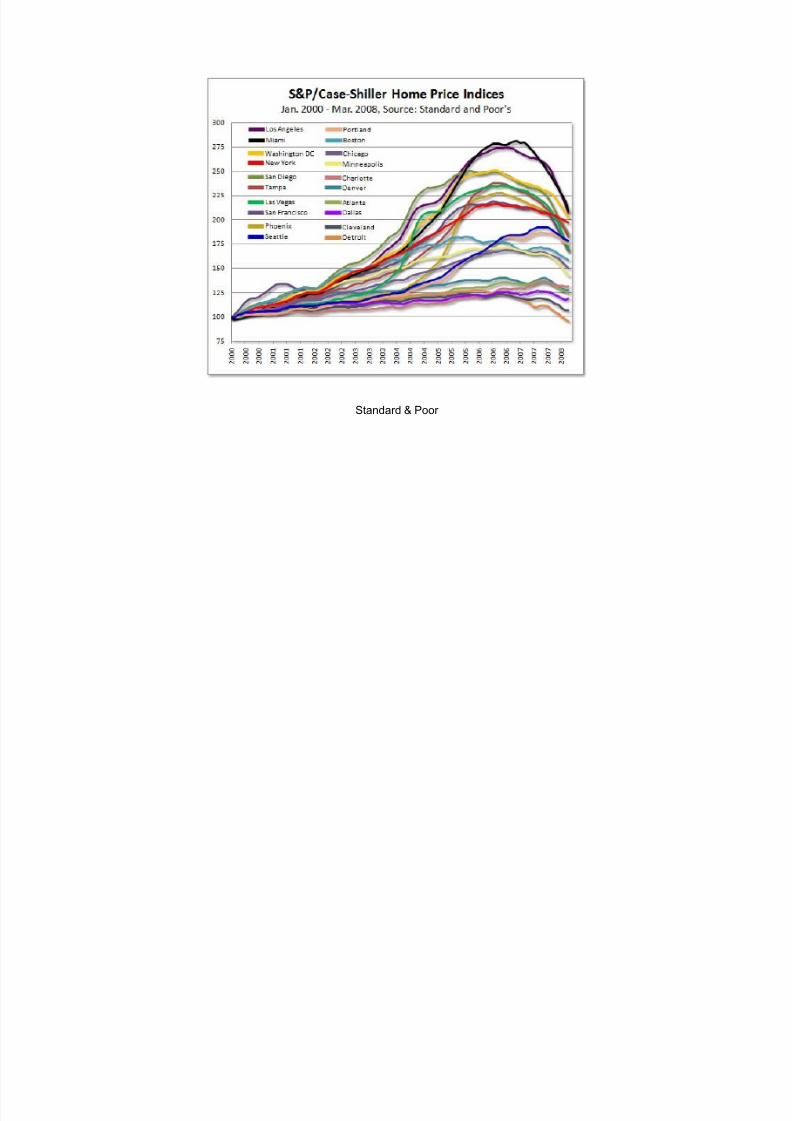

Standard & Poor

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 11/30

Tax Incremental Financing

City of San Antonio

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 12/30

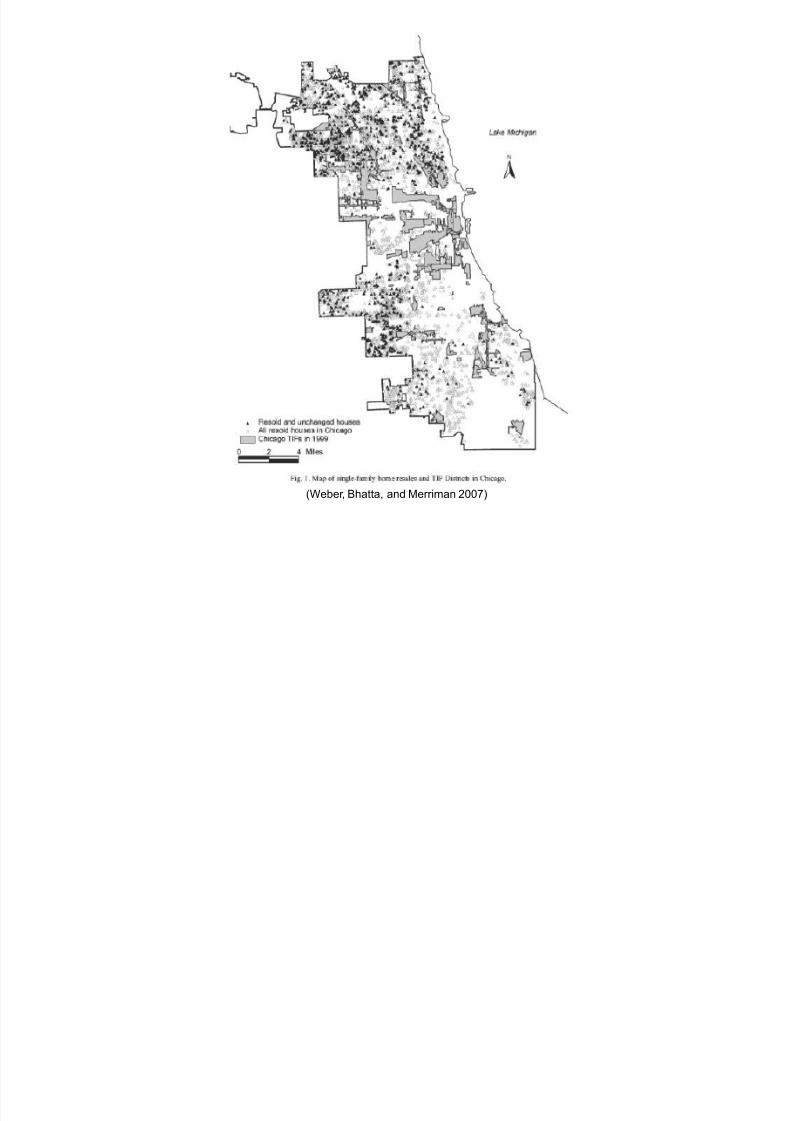

(Weber, Bhatta, and Merriman 2007)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 13/30

Clawbacks, Recisions & Recalibration in Public Subsidies

(White, Bingham, and Hill 2003)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 14/30

Section 106: Rationalising the Impacts of Development

The Standard Charge covers contributions for Education / Training, Sustainable Transportation, Open Space, Sport and Air Quality andwill be sought on applications which:

• A new residential unit is created, £3,000 per additional bedroom will be sought;

• An increase of over 500sqm in commercial floor space (B1/B2/B8), £25 per sqm will be sought

In addition to the obligations outlined above, other potential obligations include:

• Affordable housing • Creation of open spaces, public rights of way

• Community or Affordable Workshop space. • Servicing agreements • CCTV • Adoption of new highways, Travel Plans. • Health Care Provision

• Remove new residents’ rights to parking permits. • Local employment and training strategies

• Compliance with the Considerate Contractors Scheme. • Measures to encourage sustainability and bio-diversity, such as green roofs etc

Brent County Council

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 15/30

Calculating Development Exactions & Impact Fees

Demand: The increased need for infrastructure or services

• Determine 'demand unit': A single identifiable entity with a set infrastructure and service demand

Cost: Outlay necessary to provide the services

• These may need to be paid upfront if they are built prior to the arrival of the units of demand

Revenue: Enhancement to government resources

• New growth should only finance its needs rather than previous infrastructure investments in other areas of the community

• If new growth produces a fiscal surplus, this should be credited against the exaction

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 16/30

The Municipality as an Asset Manager

Hold asset and use as collateral Re-price and set user charges Sell and invest in infrastructure

Risks with Land Leasing & Collateral

Not as regulated as fiscal borrowing andproceeds may be diverted to finance

municipal operating budgets rather thaninvestments.

Real Estate Bubbles. Due to long projectperiods, land values may considerably drop

and not able to match spending.

Increased dissatisfaction of those whoseland is being taken.

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 17/30

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 18/30

PPP Contractual Arrangement Variations

Athens International Airport

30-year concession ratified by Greek Law 2338/95

Airport Company has the exclusive right to occupy and use the site for the purpose of the "design, financing, construction, completion,commissioning, maintenance, operation, management and development of the airport

Shareholders of private company:

Greek Government: 55%HOCHTIEF AirPort GmbH: 26.545%

HOCHTIEF AirPort Capital GmbH: 13.33%Horizon Air Investments S.A.: 5%

Flughafen Athen-Spata Projektgesellschaft mbH (FASP): 0.125% stake

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 19/30

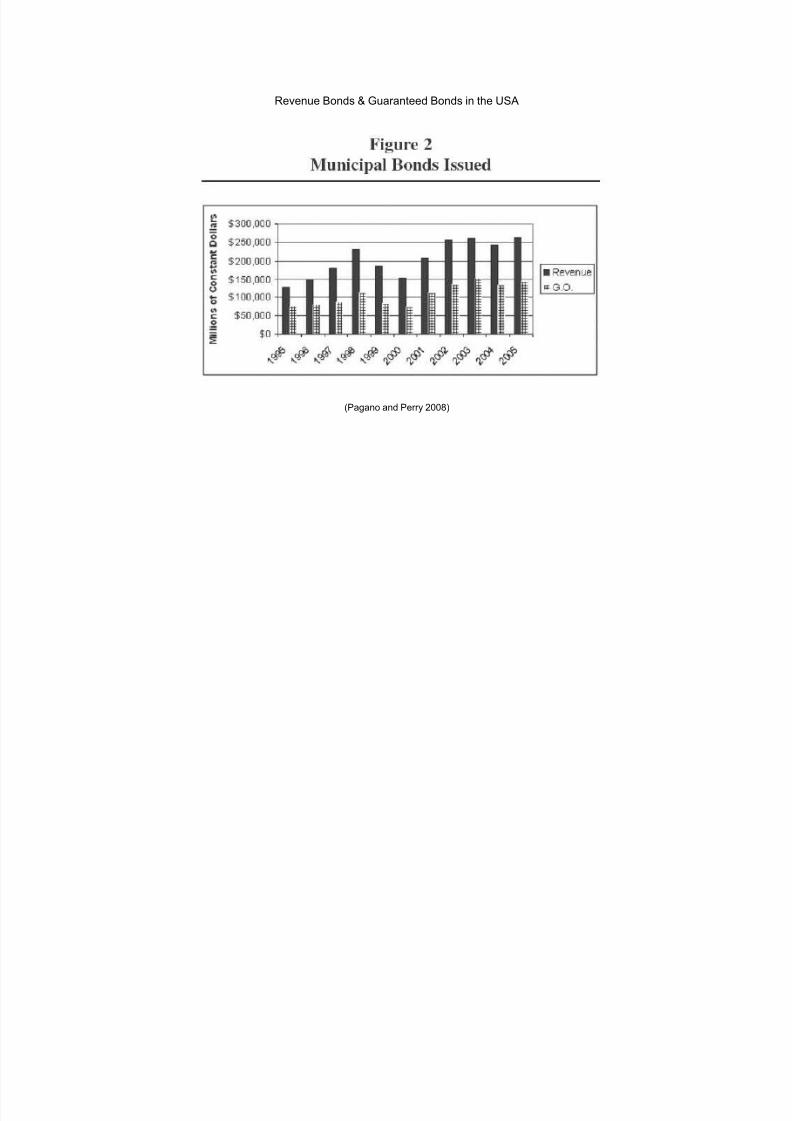

Revenue Bonds & Guaranteed Bonds in the USA

(Pagano and Perry 2008)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 20/30

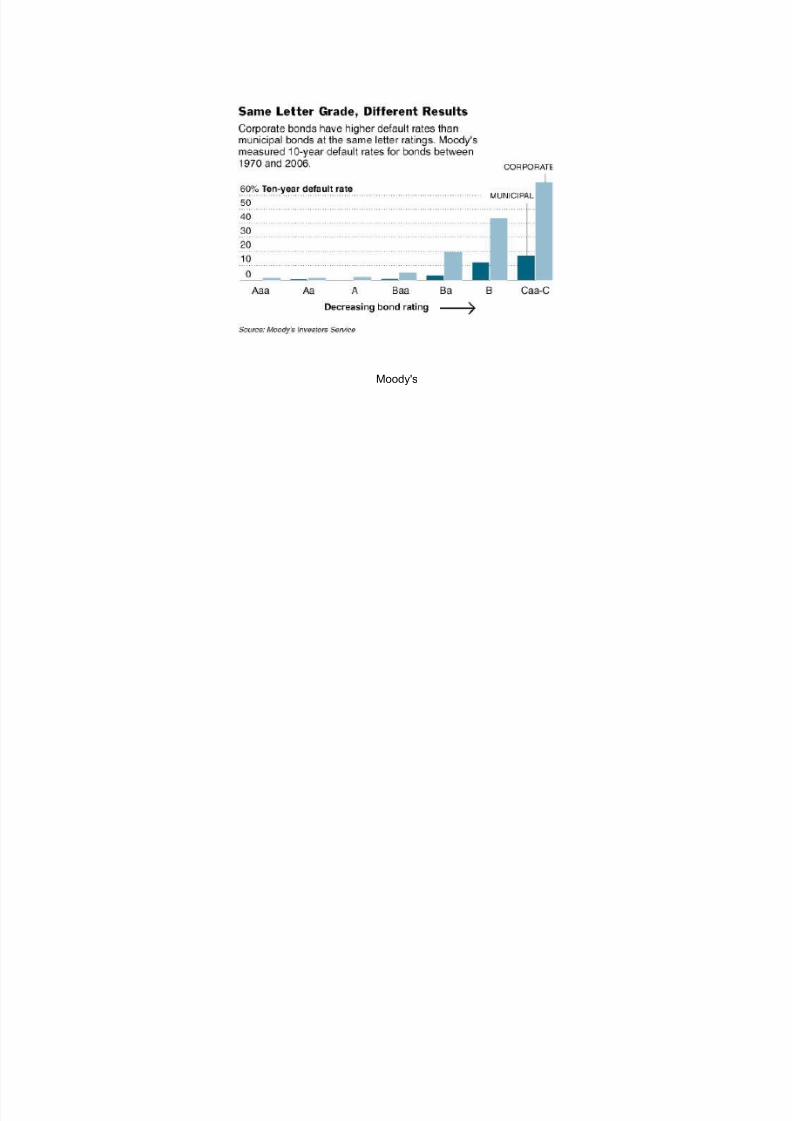

Moody's Ratings Definitions

AaaObligations rated Aaa are judged to be of the highest quality, with minimal credit risk.

AaObligations rated Aa are judged to be of high quality and are subject to very low credit risk.

AObligations rated A are considered upper-medium grade and are subject to low credit risk.

BaaObligations rated Baa are subject to moderate credit risk. They are considered medium-grade and as such may possess certain speculative characteristics.

BaObligations rated Ba are judged to have speculative elements and are subject to substantial credit risk.

BObligations rated B are considered speculative and are subject to high credit risk.

CaaObligations rated Caa are judged to be of poor standing and are subject to very high credit risk.

CaObligations rated Ca are highly speculative and are likely in, or very near, default, with some prospect of recovery of principal and interest.

CObligations rated C are the lowest rated class of bonds and are typically in default, with little prospect for recovery of principal or interest.

Note: Moody's appends numerical modifiers 1, 2, and 3 to each generic rating classification from Aa through Caa. The modifier 1 indicates that the obligation ranksin the higher end of its generic rating category; the modifier 2 indicates a mid-range ranking; and the modifier 3 indicates a ranking in the lower end of that genericrating category.

Moody's

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 21/30

Moody's

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 22/30

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 23/30

Buying Payroll & The Graduated Sovereignty of SEZ

Case Study: Korea, neoliberal pockets within a developmental State

(Park 2005)

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 24/30

Revolving Loan Funds

Traditional Lending Revolving Loan Fund Lending

Capitalised by deposits from account holders Capitalised from low cost government loans or foundations

The Rowntree Foundation

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 25/30

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 26/30

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 27/30

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 28/30

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 29/30

8/14/2019 Financing Urban Infrastructure

http://slidepdf.com/reader/full/financing-urban-infrastructure 30/30