Financing the Mozal Project_Total_1

22

Group 2 Vivek Agrawal ( 203) Shubhra Sanghi (229) Nimish Lahoti (257) Asis Kumar Mandal (325) Vivek Bhatia (356) Mahak Mehra (427) Financing the Mozal Project

-

Upload

shubhra-sanghi -

Category

Documents

-

view

966 -

download

16

Transcript of Financing the Mozal Project_Total_1

Group 2

Vivek Agrawal ( 203)

Shubhra Sanghi (229)

Nimish Lahoti (257)

Asis Kumar Mandal (325)

Vivek Bhatia (356)

Mahak Mehra (427)

Financing the Mozal Project

* Aluminium Industry– Two important facts

- Aluminium smelting is very energy-intensive.

- Aluminium prices are generally very volatile

Primary Al Production

Price Fluctuations in Al over a year

$/to

nn

e

Project Highlights

•$1.4 billion aluminium smelter in Mozambique

•Low cost, high quality operation

•250,000 tonnes of primary aluminium a year

• Joint venture• Alusaf

• IDC

•Aluminium Industry• 5 million tons –new capacity required in 10 years

• LME Price – highly volatile

Project Status

Financing Needs* IFC Approval (to invest $120m) in $1.4bn pending

* Investment worth $420m is still on paper i.e. w/o any lender commitment

Operational Needs* Construction yet to start

* Raw material supply – contract signed for another 25 years - price agreement in place

* Electricity supply – contract signed for another 25 years – price agreement in place

* Labour supply – certain (cheap)

Assumptions* Cash flow projections – too low an IRR (7% for first 15 years, 12% for first 25 years)

* Average Al price over the last 10 years ($1650/tonne) with only less than 20% occurrences over $1750/tonne

* Political Stability

* What are the greatest risks?

• Expropriation• Changes in

Taxing regime and other policies

Political Risk

• Civil War• Breakdown of

Democracy

Sovereign Risk

• Fall in prices of Aluminium

• Fall in the Market Demand for Al

Market Risk

• 50% of Equity investment, 25% of Debt commitments not assured of

Financing Risk (at present)

• Electricity Prices and RM prices linked to LME prices for Al (25 year contract).

Counterparty Risk

HAVE THEY BEEN ADEQUATELY DISCUSSED?

Political & Sovereign Risk – Involvement of IFC (Risk Mitigation: Exhibit #12)Market Risk: Partially hedged by linking direct costs to the output priceFinancing Risk: Involvement of IFC (“A” Cat Loans, Subordinated contribution as well)Counterparty Risk: Long- established relations with the partners

Risks identified by Project Team

•Expropriation•Changes in Tax Regimes on other policies

Political Risk

•Civil War•Breakdown of Democracy

Sovereign Risk

•Source of 50% equity investment unclear•Source of 25% debt investment unclear•Need for IFC involement

Financing Risk

•Involvement of IFCSolution to all above

risk

Additional Risks That Exist

•40% of production cost still uncovered•Contribution to Fixed Asset creation and Margin also uncovered

Market Risk

•Would the Raw material and electricity partners meet the contract agreement if LME price were to hit bottom.

Counter Party Risk

HAVE THEY BEEN ADEQUATELY DISCUSSED?

Political & Sovereign Risk – Involvement of IFC (Risk Mitigation: Exhibit #12)Market Risk: Partially hedged by linking direct costs to the output priceFinancing Risk: Involvement of IFC (“A” Cat Loans, Subordinated contribution as well)Counterparty Risk: Long- established relations with the partners

Will the sponsors be able to finance the deal?

EquityGencor/Alusaf $125IDC 125Others 250

Total 500 37%

Quasi-equity (subordinated debt)IFC 65Other development

financial institutions 85Total 150 11

Cash generation 35 35 2

Export creditIDC--arranged 400Coface insured 140

LoansIFC 55Other development

financial institutions 85Total Senior Debt 680 50

Total Sources 1,365 100

Sources of Cash

Gencor/Alusef

Gencor group’s PAT of $564.9mn

in 1996

deal amount is 22.13% of PAT

Proven record-Hilton Smelter

IDC(Industrial Development Corporation)

$3.6bn government

owned development

bank

Longstanding relation with

Alusef

$5bn of industrial investment in next 5 years outside SA

Mitsubishi Corporation

$78bn Japanese industrial

conglomerate with large metals

group

Synergy/ Shared interests

Sponsors-Equity

IFC

World bank group promoting private

sector development in developing

countries

Net income of $400mn in 1997

10% of all finance deals in countries with rating less

than 25

IDC(Industrial Development Corporation)

Discussion with CGIC, South African

ECA to provide insurance for

$400mn of senior debt

Protect creditors against losses from

commercial insolvency and political risks

Coface:

85% cover for loans made by french

banks

Sponsors-Debt

Mozal project was viable and had acceptable financial and economic rates of return

How does IFC involvement affect the deal?

IFC Goals

*To fund projects having

*private ownership

*commercial viability

*environmental soundness

*significant development benefits for local economy

*To invest in risky environments

About IFC

• To fund projects having • private ownership• commercial viability• environmental soundness • significant development

benefits for local economy• To invest in risky environments

IFC Goals

• Longer maturity loans• Subordinate loans• Valued development benefits• Loans not backed by sovereign

guarantees

Distinguishing features

of IFC lending

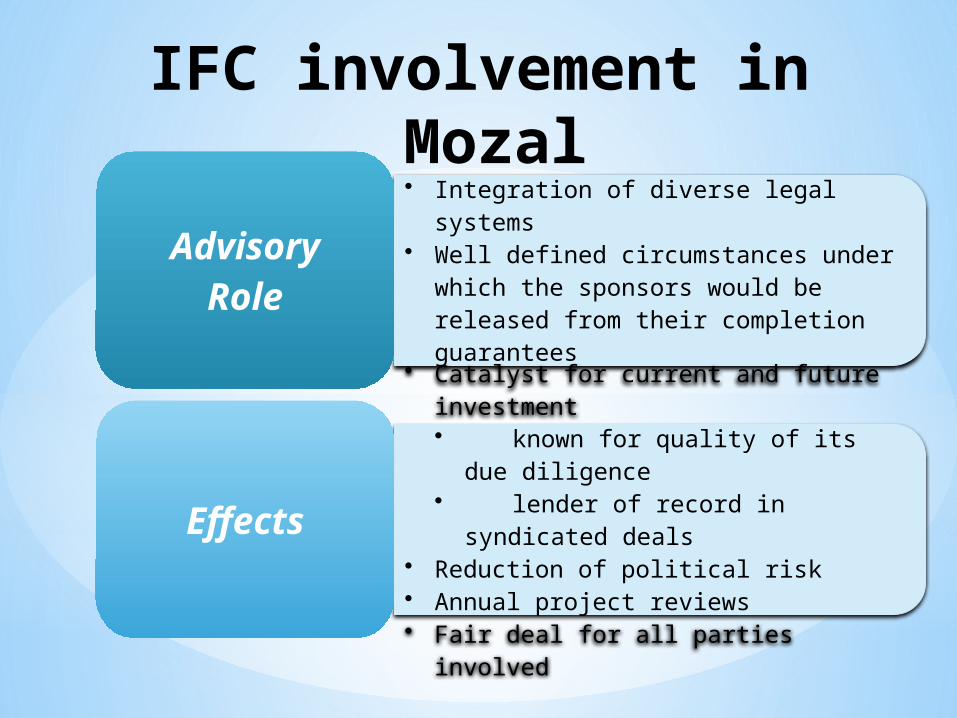

IFC involvement in Mozal• Integration of diverse legal systems• Well defined circumstances under

which the sponsors would be released from their completion guarantees

AdvisoryRole

• Catalyst for current and future investment• known for quality of its due

diligence• lender of record in

syndicated deals• Reduction of political risk• Annual project reviews• Fair deal for all parties involved

Effects

Will the IFC and the sponsors share similar objectives?

IDC

• Contribute to sustainable growth in south Africa• Promoting entrepreneurship• Financing private sector enterprises

Alusaf

• Profit from the investment• Proximity to hillside smelter• Use of hydroelectric power in Mozambique• Access to competitively-priced power

Eskom

• Utilization of Excess capacity• Expand operations outside of South Africa

Mozambica

n Government

• Improve the macro economic situation• Climate for private investment

IFC

• Promoting private sector investment in developing countries• Reduce poverty• Improves people’s lives

French

Credit Ratin

g Agen

cy

• Supporting the use of Pechiney technology

Mitsubishi

• Equity returns• Sharing the aluminium output

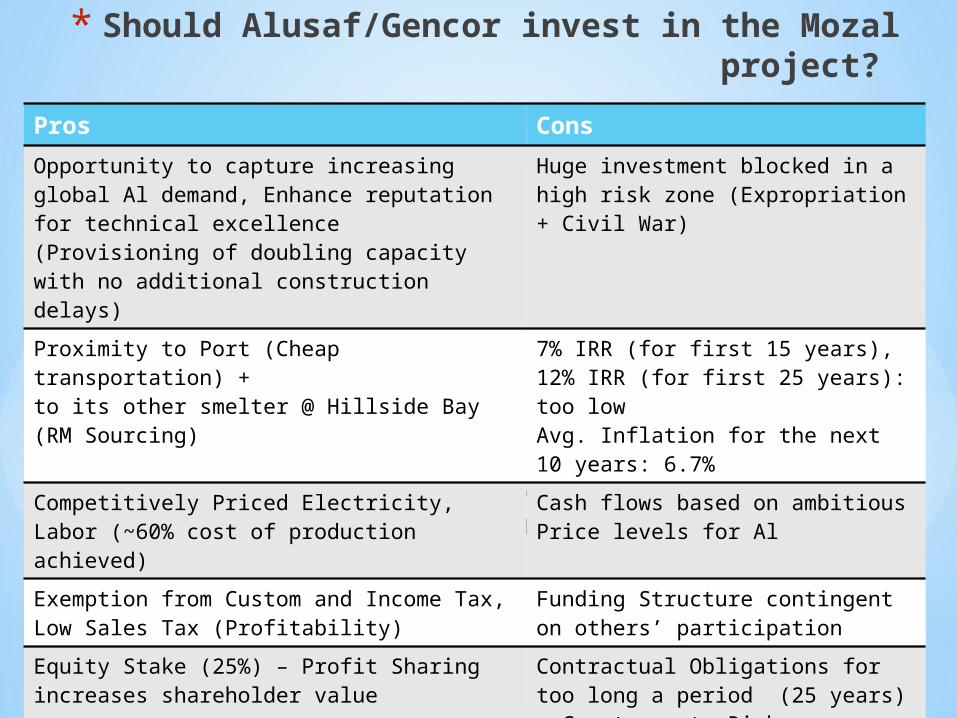

Should Alusaf/Gencor Invest in the Mozal Project?

* Should Alusaf/Gencor invest in the Mozal project?

Pros Cons

Opportunity to capture increasing global Al demand, Enhance reputation for technical excellence(Provisioning of doubling capacity with no additional construction delays)

Huge investment blocked in a high risk zone (Expropriation + Civil War)

Proximity to Port (Cheap transportation) + to its other smelter @ Hillside Bay (RM Sourcing)

7% IRR (for first 15 years), 12% IRR (for first 25 years): too lowAvg. Inflation for the next 10 years: 6.7%

Competitively Priced Electricity, Labor (~60% cost of production achieved)

Cash flows based on ambitious Price levels for Al

Exemption from Custom and Income Tax, Low Sales Tax (Profitability)

Funding Structure contingent on others’ participation

Equity Stake (25%) – Profit Sharingincreases shareholder value

Contractual Obligations for too long a period (25 years) : Counterparty Risk

IFC Funding Approval almost there (opening of doors to get more partners involved)

Good Financing Structure (Lots of players, provision of quasi-equity)

* Should Alusaf/Gencor invest in the Mozal project?

Results

*Completed more than $100M under budget and six months ahead of schedule

*The first aluminum was produced in June 2000

*In 2003, expanded to double its capacity to 500,000 tons per year

*Roads, ports, power generation, telecommunications, water supply, and drainage systems were built or upgraded in order to build Mozal

*Country's exports tripled

*Added more than 7 percent to GDP in its initial years of operation and an estimated 10 percent in 2001

Current Shareholder Pattern

*BHP Billiton Limited (47%)

*Government of Mozambique (4%)

*Industrial Development Corporation of South Africa Ltd (24%)

*Mitsubishi Corporation (South Africa) (25%)