FINANCING STRATEGIES IN A HEALTH REFORM ENVIRONMENT July 9, 2013 William J. TenHoor AHP Healthcare...

23

FINANCING STRATEGIES IN A HEALTH REFORM ENVIRONMENT July 9, 2013 William J. TenHoor AHP Healthcare Solutions

-

Upload

jonah-oconnor -

Category

Documents

-

view

215 -

download

0

Transcript of FINANCING STRATEGIES IN A HEALTH REFORM ENVIRONMENT July 9, 2013 William J. TenHoor AHP Healthcare...

FINANCING STRATEGIESIN A HEALTH REFORM ENVIRONMENT

July 9, 2013

William J. TenHoor

AHP Healthcare Solutions

2

Objective

1. Gain a better understanding of financial reimbursement approaches under Health Care Reform

2. Gain a better understanding financing strategies and opportunities as a business development executive

3

Why the ACA Necessitates Action

• Payment models (financing) influence care systems and drive the possible• Service goes where the dollar flows

• ACA important departure from earlier health and human service financing paradigms• Great Society (public federal-local grants)(60’s)

• Block Grants (public federal-state grants with private charities)(80’s)

• Universal Health Insurance Coverage (pubic and private health insurance)(today)

4

What the ACA Establishes

• Benefits for all Americans framed in 10 Titles

• Quality, Affordable Health Care for All Americans

• The Role of Public Programs

• Improving the Quality and Efficiency of Health Care

• The Prevention of Chronic Disease and Improving

Public Health

• More . . .

5

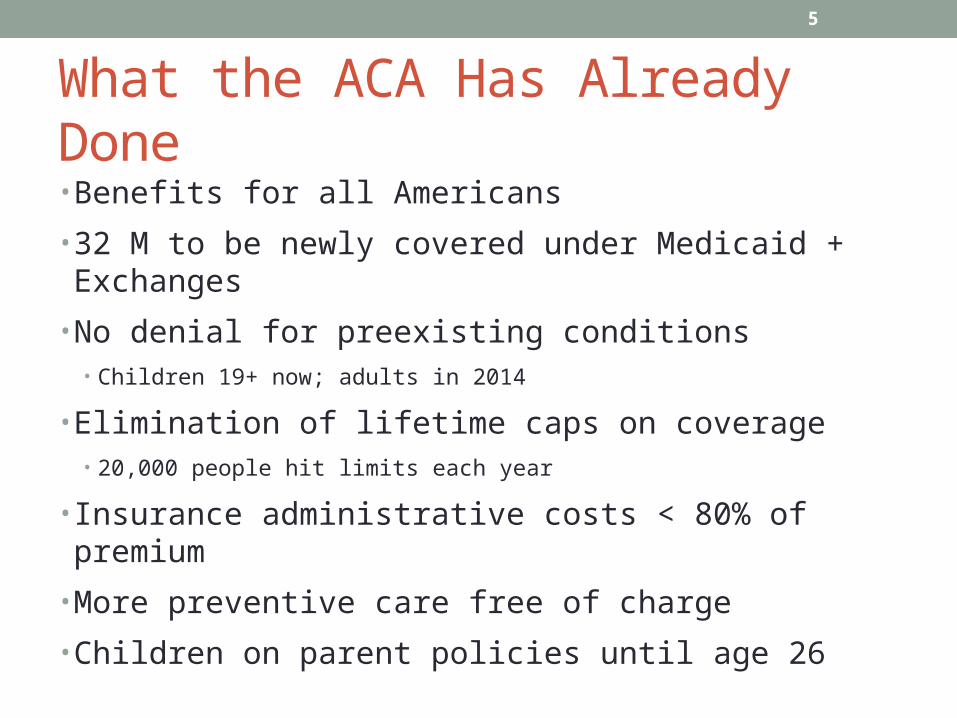

What the ACA Has Already Done

• Benefits for all Americans

• 32 M to be newly covered under Medicaid + Exchanges

• No denial for preexisting conditions• Children 19+ now; adults in 2014

• Elimination of lifetime caps on coverage • 20,000 people hit limits each year

• Insurance administrative costs < 80% of premium

• More preventive care free of charge

• Children on parent policies until age 26

6

Critical Challenges for SUD Executives

1. Understand your environment

2. Integrate

3. Grow – consider networks, merger

4. Join ACOs

5. Become providers for all major insurers

6. Increase your financial IQ

7

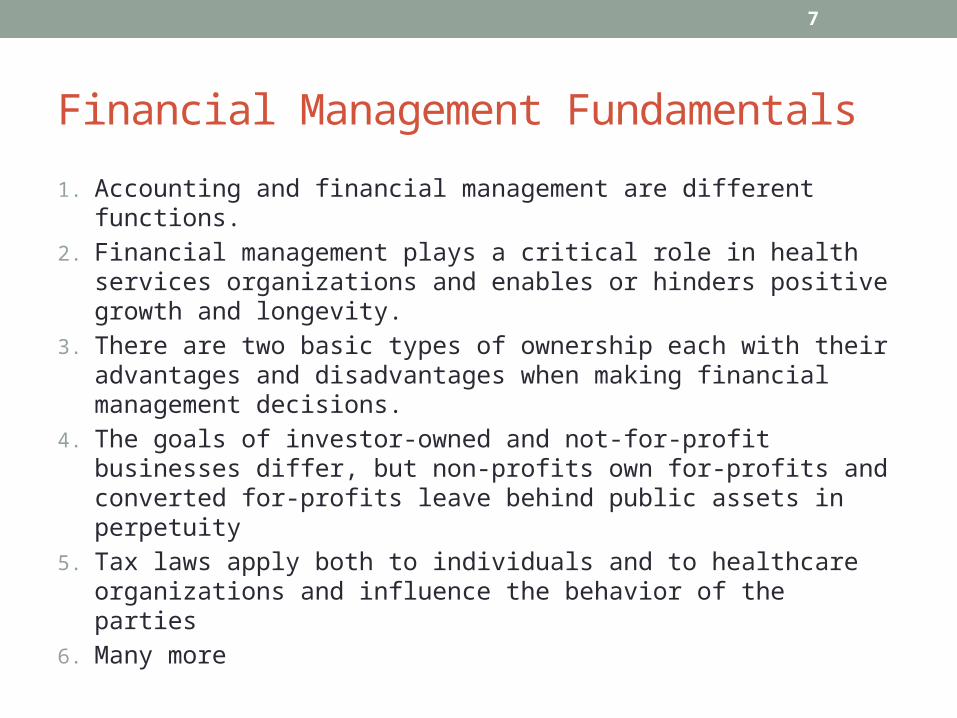

Financial Management Fundamentals

1. Accounting and financial management are different functions.

2. Financial management plays a critical role in health services organizations and enables or hinders positive growth and longevity.

3. There are two basic types of ownership each with their advantages and disadvantages when making financial management decisions.

4. The goals of investor-owned and not-for-profit businesses differ, but non-profits own for-profits and converted for-profits leave behind public assets in perpetuity

5. Tax laws apply both to individuals and to healthcare organizations and influence the behavior of the parties

6. Many more

8

Understand Your Markets• Good performance compels expertise• Understanding markets, their payers, parity and reform• The Markets

• Public Market: Federal MH and SUD Block Grants, State and Local Government, Medicaid, Medicare, TriCare, HRSA

• Commercial Market:, Self Insured Employers (Large Group, Small Group) Individual, MCO and Traditional Insurers, HMOs, MBHOs

• Self-Pay Market

• Markets versus Products (Health Plans)• Recognize consolidation and merger acquisition activity

9

Recent M&A Example• FL “Aspire Health Partners” will begin operating July 1• Is a merger of three SUD NFPs with none of the entities

buying the assets of the others• All three organizations split the legal costs of the merger• New board will consist of all the members of all three

existing boards• Existing chief executives take on new roles as 1 CEO, 2.

President, and 3 COO • Aspire has a three-year plan

• Integrate the organizations• Emphasize and incorporate best practices • Transitioning to new leaders as existing 3 CEOs nearing retirement

10

Paradigm Shift: Insurance Vs. Grants

• CURRENT SYSTEM• Grant (versus contract)• Broad purposes couched

within broad legislation• Relationship among

Parties• State, clients, provider• Loosely bound, unspecified

• Billed monthly• More proforma

• FUTURE SYSTEM• Insurance Contract• Specific purposes, terms,

conditions• Relationship among

parties• Insurer, insured, provider• Tightly contracted

• Billed daily• Heavy admin. Overlay (UM,

clean claim, CMS 1500 form)

11

Insurance: Framework & Characteristics

Characteristics

1. Pooling of losses2. Payment for

random losses

3. Risk transfer4. Indemnification for

illness

Insurer charges individual $250. to cover the risk of extreme illness and/or potential bankruptcy(Anticipated care cost + risk & overhead charge = premium)

1

2

3

12

Basic Reimbursement Schemes• Fee for Service

• Cost based – paid on allowable costs • Positives – assures provider costs are paid

• Charge based – billed charges are paid based on “charge-master”• Paid based on negotiated or discounted charges

• Prospective • Per procedure, diagnosis or per diem• Per episode

• Capitation• Full vs. Partial• Old capitation (‘74 HMO Act) vs. New HR Capitation

Provider Risk Low

Provider High Risk

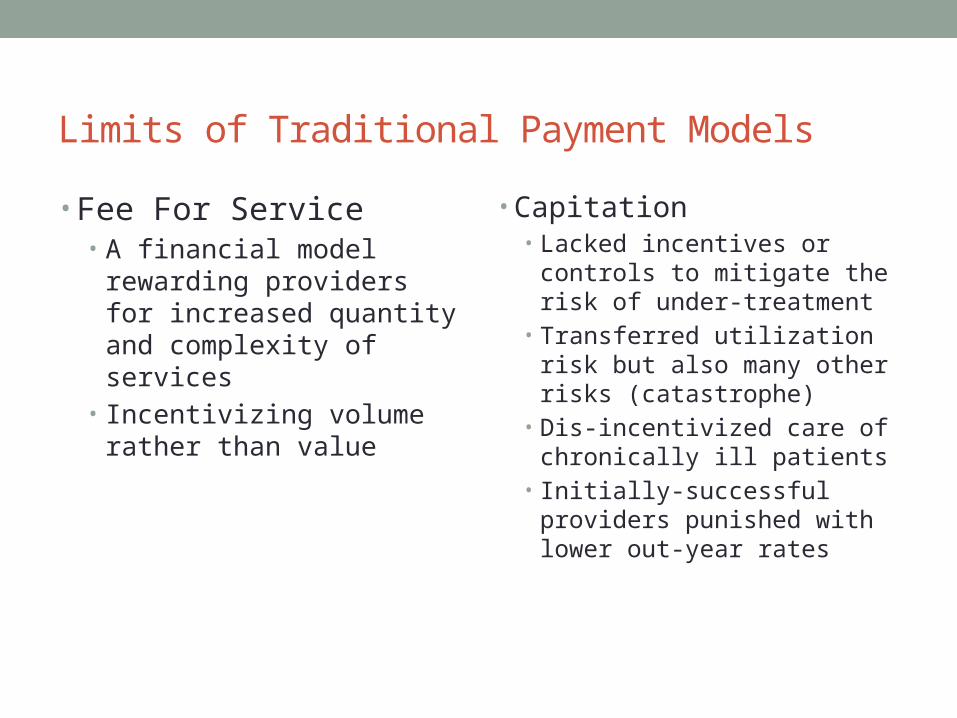

Limits of Traditional Payment Models

• Fee For Service• A financial model rewarding

providers for increased quantity and complexity of services

• Incentivizing volume rather than value

• Capitation• Lacked incentives or controls

to mitigate the risk of under-treatment

• Transferred utilization risk but also many other risks (catastrophe)

• Dis-incentivized care of chronically ill patients

• Initially-successful providers punished with lower out-year rates

Related Payment Model & Limits• Pay for Performance

• Also incents desired behaviors

• Can improve process (eg., care coordination) and outcomes

• Limited incentive• based on physician fees and

not total care costs

• Global or bundled (episode or case based) payments• Achieves results by focusing

on and limiting payment for higher-cost episodes

• CMS’s 4 models• Retrospective & prospective

hospital stay

• Non-comprehensive

15

Risk Arrangements

• Rate setting only for what you can control• Rate fairness - using actuaries, accountants• Payment calculation basis – changes to• Assignment/enrollment procedure• Sufficient numbers and adverse selection• MCO Withholds

• Rationale• Lower is better• Method and timing of distribution

• Stop loss insurance

16

Primary Care Integration Strategy Source; SAMHSA/HRSA Center for Integrated Health Solutions

17

Exchanges & Qualified Health Plan Pricing

• California and Oregon have already published the premium rates that health insurers want to charge for plans to be sold through their health exchanges. Consumers hoping for official quotes on how much they might have to pay for health plans sold on Minnesota's health insurance exchange, dubbed MNsure, are going to have to wait.

• “Two weeks ago, Oregon released health plans’ proposed rates for the health insurance exchange. This was, as the Oregonian’s Nick Budnick reported, when the insurers had their rates directly compared with one another online.

• The price disparity was wide. “One health insurer wants to charge $169 a month next year to cover a 40-year-old Portland-area non-smoker,” Budnick wrote. “Another wants $422 a month for the same standard plan. “

• http://www.washingtonpost.com/blogs/wonkblog/wp/2013/05/20/oregon-may-be-the-white-houses-favorite-health-exchange/

18

ACO Development Process• Already 252 ACOS have been created (Bloomberg)• The Centers for Medicare & Medicaid Services has

confirmed that nine of the 32 Pioneer accountable care organizations may walk away from the experiment, which is designed to change the way medical providers are paid to manage care for patients with chronic diseases, Bloomberg reports

ACO-Provider Payment Models

Exhibit taken from The Commonwealth Fund July 2011 “Promising Payment Reform : Risk Sharing with Accountable Care Organizations”

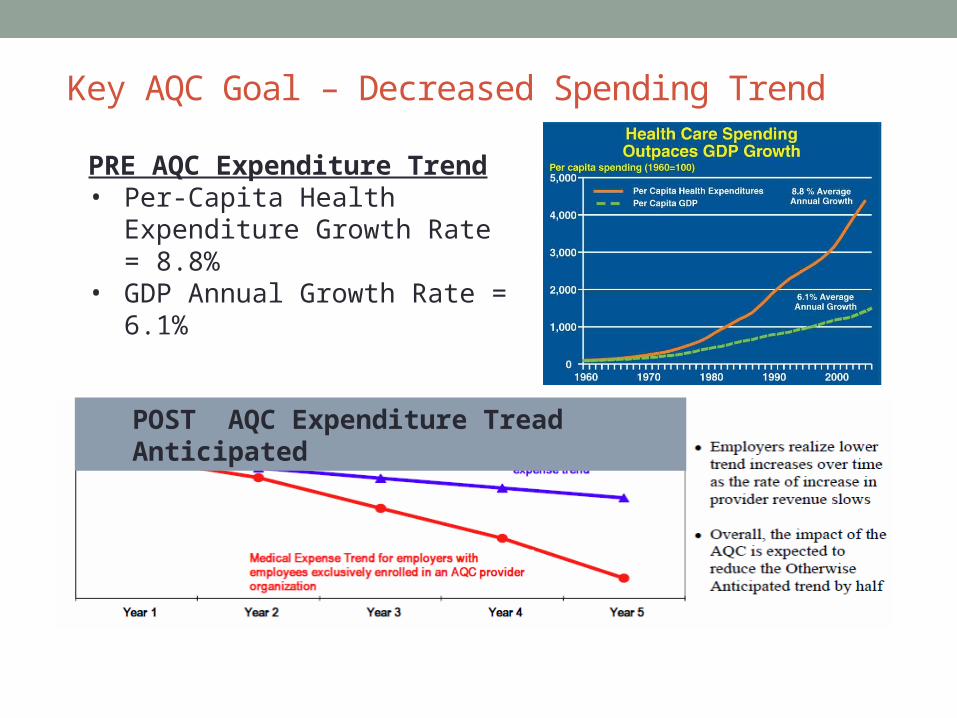

Key AQC Goal – Decreased Spending Trend

PRE AQC Expenditure Trend• Per-Capita Health Expenditure

Growth Rate = 8.8%• GDP Annual Growth Rate =

6.1%

POST AQC Expenditure Tread Anticipated

• Provider group has responsibility for cost and quality of all services

• Initial global budget for all services (in, out, pharmacy, behavioral, etc.) based on cost history

• Annual adjustments for health status/severity and inflation• Groups negotiate risk sharing levels (50%-100%) based on

risk tolerance with stop-loss and other controls available• Group savings if costs go down – intergroup, upside and

downside risks are always equal• Performance incentives of up to 10% of global budget• Interim payments are made on a FFS basis with global

budget reconciliation at year end

Financial Features of the AQC

Comorbidity & Chronic Condition Costs

Source: Wyatt Matas, 2013

23

Questions & Discussion

Bill TenHoor

© 2012 by Advocates for Human Potential – Healthcare Solutions. All rights reserved. No part of this document may be reproduced or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior written permission of AHP.