Financing Airport Development

35

Financing Airport Development Prof. Amedeo Odoni Airport Planning and Management Module 21 January 2016 Istanbul Technical University Air Transportation Management M.Sc. Program

Transcript of Financing Airport Development

Financing Airport DevelopmentProf. Amedeo Odoni

Airport Planning and Management

Module 21

January 2016

Istanbul Technical University

Air Transportation Management

M.Sc. Program

Financing Airport Development

q Objective: Review the financing needs and

sources of financing for infrastructure

development at large airports, as well as the

main sources of revenue

q Outline

– Sources of financing

– Recent financial performance of large airports

– Principal sources of revenue

– Risks in airport financing and airport defenses

Page 2

Financing NeedsAirport infrastructure development requires large

amounts of financing

– Airport construction and expansion projects with

cost of more than $1 billion are becoming

increasingly common even at secondary airports

– Several projects around the world (e.g.,

London’s additional runway, Hong Kong, New

Istanbul, Singapore, Dubai, etc.) will cost well

beyond $10 billion

Airports or governmental entities undertaking such

projects must raise sufficient capital from public or

private sources (or a combination of both)

Page 3

Page 4

SIN – 2-runway configuration

5750 ft (1750 m) between runway centerlines

2014: 54.1 mio pax, 341K mvts

Singapore Changi Airport with Third Runway

Page 5Source: Wikipedia (2011)

Page 6

Hong Kong: 2 independent parallel

Page 7

Hong Kong: Third Runway Project (March 2012)

New Istanbul Airport (Feb 2015)

High Variability

Availability of alternative sources of funding and

the best combinations of funding vary widely

depending on several factors

– National policies and practices

– Legal requirements and restrictions

– Size of airport and of project

– Creditworthiness of the airport operator

– Access to financial markets

Page 9

Financing Needs [2]Most of the costs in question are capital costs

but, in some cases, airports may seek financing

to support operations, as well

Another important consideration in less

developed economies is that debt may often

have to be repaid in foreign currency because it

may involve advanced technology equipment or

facilities

– Competes with the country’s other internal

needs for foreign currency

– Is exposed to the uncertainties of the currency

exchange markets

Page 10

Page 11

Financing Airport Capital Investments [1]

1. Outright Government Grants

– Direct funding (e.g., Airport Improvement Program -- $3.5

billion per year in US favoring medium-size and small

airports)

– Provision of resources other than funding (e.g., land,

materials, access to utilities)

2. Special-Purpose Taxes

– Passengers pay a fee that goes to a fund that supports

eligible airport-related development projects (e.g.,

Passenger Facility Charge (PFC) in US, $4.50 per ticket)

• Airlines are strongly opposed to “pre-funding” of

projects

• These special-purpose taxes are sometimes used

inappropriately

Financing Airport Capital Investments [2]

3. Government or Development Bank Loans

– Typically issued on very favorable terms (low interest,

long payback periods)

– Several international development banks (e.g., World

Bank, Inter-American Bank, European Investment

Bank) provide these, mostly for developing countries,

but also for some developed economies

4. Self-generated Operating Surpluses

– Increasingly popular and feasible, as airports become

more self-supporting financially, generating healthy

surpluses

– Now very common for medium-size and small-size

projects

Page 12

Financing Airport Capital Investments [3]

5. Commercial Bank Loans

– A number of commercial banks provide loans for

airport capital development

– Typically have the highest interest rates; the rates may

be reduced through governmental loan guarantees

6. Tax-exempt, General Obligation Bonds

– Raised from commercial capital equity markets,

including private investors, banks, investment houses,

or fund pools

– Backed by the "full faith and credit" of a governmental

unit and secured by taxes collected by it (from the

taxpayers)

– In developed economies, these are now largely

replaced by tax-exempt revenue bonds (see next) Page 13

Financing Airport Capital Investments [4]

7. Tax-exempt Revenue Bond

– In some countries, this is now the most common type of

financing for infrastructure development at large airports;

can be divided into several categories:

– General airport revenue bonds (GARBS) are secured by

the revenues of the airport as a whole

– Revenue bonds secured by long-term airline leases

– Revenue bonds secured by approved airport

development taxes (e.g., PFCs) or by future expected

government grants

– Revenue bonds backed solely by revenues from a facility

constructed with the proceeds of these bonds

Page 14

Capital Project Financing, USA (2001-2004)

Page 15

Source: ACRP

Synthesis 1 (2007)

Innovative Finance

and Alternative

Sources of Funding

Financing Airport Capital Investments [5]

8. Private financing against specified rights to airport

revenues

– May involve the construction of a single facility (e.g.,

a parking facility) or of an entire airport

– BOT agreements typically include such financing

q There are many variations of the eight types of financing

outlined above.

q For large airport infrastructure development projects,

several of these types of financing are often used

concurrently.

Page 16

Page 17

Financing of New Athens International Airport (1996-

2001)

European Investment Bank $1,128 47%

Consortium of commercial banks $ 360 15%

Airport development fund (Greece) $ 288 12%

European Union grants $ 264 11%

Greek State grants $ 168 7%

Share capital $ 144 6%

(55% Greek State, 45% German group)

Secondary debt (commercial rates) $ 48 2%

(taken on by shareholders)

Total $ 2,400 million

A Financially Sound Industry Large airports, as an industry, have generally performed

well financially despite the economic volatility associated

with the air transportation sector

Major credit rating agencies (e.g., Moody’s, Fitch,

Standard & Poor’s) consider airports, overall, as

financially sound and highly creditworthy

Credit ratings of airports naturally fluctuate in response to

economic and political events (e.g., downgrading of

ratings of many US airports in 2001)

In the United States there has never been a default on

GARBS

However, there have been several instances of airline

special facility debt defaults

Page 18

2013 Airport Industry Revenues and Costs

Total

Revenue

Aeronautical

Revenue*

Non-Aeron’al

Revenue**

%

Aeron’al

Total Costs

(Operating

+ Capital)

Africa 2.9 2.1 0.8 72% 2.1

Asia-Pacific 37.0 18.8 18.2 51% 25.8

Europe 49.8 30.1 19.7 60% 42.1

Latin America

– Caribbean

7.0 4.4 2.6 63% 5.1

Middle East 8.7 4.4 4.3 51% 7.4

North

America

25.5 13.9 11.6 55% 22.7

Total 130.9 73.7 57.2 56% 106.5

Page 19

Amounts shown are in Billions of US$ (1900 airports, 150 countries)

* Includes ground-handling income

** Includes non-operating income

Source: Airport World,

February – March 2015

Distribution of Non-Aeronautical Income (2013)

Retail

Concessions

Car

Parking

Real

Estate

Rental

Cars

Food +

Beverage

Advert’ng Other

Africa 44 15 18 4 1 8 10

Asia-Pacific 33 8 23 1 3 4 28

Europe 35 15 19 2 5 2 28

Latin

America --

Caribbean

25 9 14 3 6 5 38

Middle East 49 8 11 2 5 3 22

North

America

8 39 13 17 7 6 10

Total 27 20 18 6 5 4 20

Page 20

All figures shown in the Table are percentages (%)

Source: Airport World, February – March 2015

Financial Performance: 100 Largest Airport

Operators (2012)

Page 21

Total revenue $ 77 billion

Net operating result $ 16.4 billion

Operating margin 21.2%

Average operating margin (2008-2012) 17.9%

Net result $ 8.2 billion

Net margin 10.6%

Average net margin (2008-2012) 8.9%

Source: FlightGlobal/ Airline

Business, October 2013.

Financial Results: Airports vs. Airlines (2007-12)

Page 22

AIRLINE-AIRPORT PROFITABILITY GAP

Top 100/50 airport group financial results

2012 2011 2010 2009 2008 2007

Operating margin % 21.2 19.1 17.2 14.0 18.2 20.7

Net margin % 10.6 9.5 9.8 6.0 8.5 12.8

Top 150 airline group financial results

2012 2011 2010 2009 2008 2007

Operating margin % 2.9 3.1 5.5 0.0 -2.6 5.3

Net margin % 0.6 0.9 3.3 -1.5 -5.8 4.1

Profitability Gap (airport vs airline group)

2012 2011 2010 2009 2008 2007

Operating margin 18.3 16.0 11.7 14.0 20.8 15.4

Net margin 10.0 8.6 6.5 7.5 14.3 8.7

Source: FlightGlobal/ Airline

Business, October 2013.

30 Airport Operators with Highest Revenue (2012)

Page 23Source: FlightGlobal/ Airline Business, October 2013.

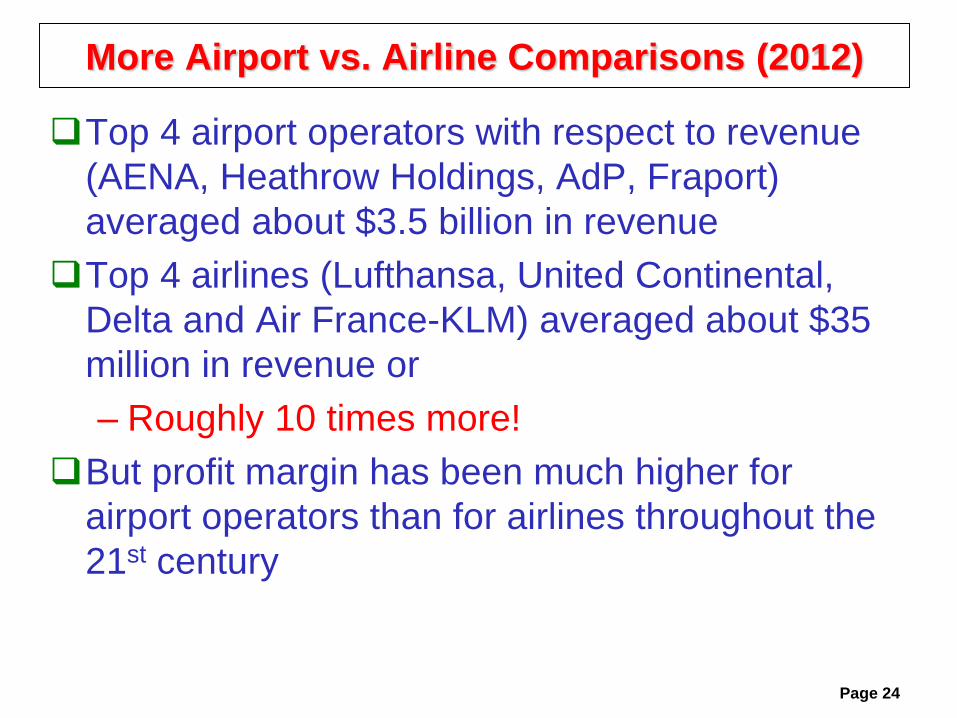

More Airport vs. Airline Comparisons (2012)

Top 4 airport operators with respect to revenue

(AENA, Heathrow Holdings, AdP, Fraport)

averaged about $3.5 billion in revenue

Top 4 airlines (Lufthansa, United Continental,

Delta and Air France-KLM) averaged about $35

million in revenue or

– Roughly 10 times more!

But profit margin has been much higher for

airport operators than for airlines throughout the

21st century

Page 24

Page 25

Financial Statistics for 30 Busiest US Airports (2009)

Revenues of 30 busiest airports ($14.3 billion)

equal 61% of total revenues ($23.4 billion) of 519

airports with commercial service

Expenditures:

– Operating: $6.6 billion ($2.7 billion for personnel,

$2.0 billion for contractual services)

– Non-operating: $2.5 billion for interest

– Depreciation: $3.1 billion

Expenditures for projects: $6.8 billion ($3.1 billion

for terminals, $1.3 billion for airfields)

Bond proceeds: $3.8 billion

Bond indebtedness: $49 billion

Risks in Airport Financing

Overly Optimistic Forecasts

– “The forecast is always wrong”

– Forecasting for airports has historically proved to

be very difficult and often very wrong

– Tendency to be over-optimistic (several reasons)

– Numerous examples internationally

Geopolitical events with disruptive impacts

– Economic recessions, wars, epidemics (e.g.,

SARS, Ebola), terrorism

Page 26

Forecasts of Total U.S. Airport Operations

Source: FAA, Terminal Area Forecasts, 2001-2012

Prepared by Joakim Karlsson and Amon Tarakemeh

Tower Operations by Aviation Segment

Rio de Janeiro/Galeão–Antonio Carlos Jobim (GIG)

2013: 25-year concession to consortium of Oderbrecht (Br, 60%)

and Changi Airport (Sin, 40%); ~$8 billion for 51% share; forecast:

175% growth in 15 yrs (~7.5/year); ~17.5 mio pax in 2012

ATH: Main and Satellite Terminal Buildings

Risks in Airport Financing [2]

Airline-related changes

– Bankruptcies (Eastern Miami, Sabena

Brussels, Swissair Zurich, Malev Budapest)

– Mergers (Delta – Northwest Minneapolis,

American – TWA St. Louis and Kansas City)

– Network reconfigurations (Alitalia Rome vs.

Milan, USAir Philadelphia vs. Pittsburgh)

– Limited “loyalty” to airports, especially by some

low-cost carriers

Page 32

Airport Defenses

Strong O/D traffic

– Airlines come and go, but airport traffic base remains

strong

– Several “Compensatory” system airports in the US are in

this category

Presence of strong dominant airline(s) with long-term

commitment to the airport

Long-term airline leases and commitments (e.g., for

exclusive-use terminal facilities)

For airports relying on connecting traffic

– Airline-airport partnerships

– “Residual” system of charges, under which airlines

benefit from non-aeronautical revenues in exchange for

assuming financial risk Page 33

References

de Neufville, R. and A. Odoni (2013) Airport Systems: Planning, Design and Management, 2nd

Edition, McGraw-Hill Education. [Chapters 7 and 8]

Graham, Anne (2014) Managing Airports: An International Perspective, 4th Edition, Routledge Publishers. [Chapters 2, 3 and 4]

ACRP – Airport Cooperative Research Program (2007) Innovative Finance and Alternative Sources of Revenue for Airports, Washington, DC.

Page 34

Questions? Comments?

Page 35