FINANCIAL - Weebly

52

Financial Management GA, GK, IF

Transcript of FINANCIAL - Weebly

Financial Management

GA, GK, IF

Financial Management

このTopicの特徴は

会社の経営が大丈夫かどうか 改善できる点はないのか

いくつかの方程式を学習します。

たとえば流動比率とか

日本人受験生には有利なTopicです。

方程式も簡単です。実務でアナリストが駆使するような難しいのは

一切出題されません。

日々の業務に役立つため、興味を持てると思います。

1

Financial Management

WORKING CAPITAL

A. (Net) Working Capital = Current Assets - Current Liabilities

1. Working Capital: Measure of liquidity

2. Liquidity: Ability of an entity to meet its short-term obligations as they becomedue

a. Positive: Current assets are greater than current liabilities, implying thecompany is able to satisfy its short-term debt

b. Negative: Current assets are less than current liabilities, suggesting thefirm may experience difficulties in satisfying its short-term debt

c. Zero: Current assets equal current liabilities (rare, both in practice andon exam)

B. Current Ratio = Current Assets / Current Liabilities

C. Current Assets

1. Definition: Assets that can be used, consumed, liquidated, or converted intocash within one year or one operating cycle, whichever is longer

2. Examples: Cash, marketable securities, accounts receivable, prepaid items,and inventory

D. Current Liabilities

1. Definition: Liabilities that must be satisfied within one year or one operatingcycle, whichever is longer, by using current assets or replacing with other currentliabilities

2. Examples: Accounts payable, wages payable, taxes payable, and unearned fees

Independently answer questions 1-4.

Notes:

Current Assets Current Liabilitiesa. Increase by $100 Decrease by $30b. Increase by $160 Increase by $40c. Decrease by $150 Increase by $50d. Decrease by $120 Decrease by $85

[7359]

2

Financial Management

1. Which one of the following wouldincrease the net working capital of a firm?a. Payment of wages payableb. Collection of accounts receivablec. Refinancing a short-term note payable

with a three-year note payabled. Purchase of a new building financed

with a 25-year mortgage [7289]

2. What ef fect wi l l the issuance ofcommon stock for cash have on a firm'sworking capital and current ratio?

3. Adam Company's board of directorshas identified four alternative courses ofaction to increase working capital next year. which option should Adam choose tomaximize net working capital?

4. Jean Company is evaluating a plan toexpand its capacity that will affect thefollowing financial statement amounts.

CashMarketable Securities Accounts ReceivableInventoryFixed AssetsAccounts Payable Mortgage Payable (current)Mortgage Payable(long-term)Retained Earnings

What is the estimated effect of the expan-sion on Jean's working capital?a. Increase of $22,000b. Increase of $19,000c. Increase of $13,000d. Decrease of $3,000 [7288]

QUESTIONS

Working Capital Current Ratioa. Increase Decreaseb. Decrease Increasec. Increase Increased. Decrease Decrease

[7359]

Current Plan$ 4,000 $10,000

20,000 11,00045,000 60,00043,000 53,00050,000 70,000

(37,000) (46,000)

(18,000) (34,000)

80,000 95,00050,000 75,000

○

○

○

○

3

Financial Management

CASH

A. Reasons to Hold Cash

Cash is the Special Toilet Paper of the Future

1. Compensating Balance: Compensate banks for services provided to the firm

2. Speculation: Unplanned bargain purchases

3. Transactions: Routine

4. Precautionary Measure: Contingency for uncertainty of forecasts

5. Future Cash Requirements: Special outlays such as dividends, debt or taxpayments

B. Increasing the Cash Balance

1. Speed up cash collections

2. Slow down disbursements or payments

3. Float is the time between when a customer mails a payment and when itbecomes available in the firm's bank account

a. Mail Float: Time between when a customer mails a payment (check)and when the company receives the payment

b. Processing Float: Time between when the company receives a pay- ment (check) and when the check is deposited at the bank

c. Check-Clearing Float: Time between when the payment (check) isdeposited at the bank and when the funds become available to thecompany

this is day to day operations

4

Financial Management

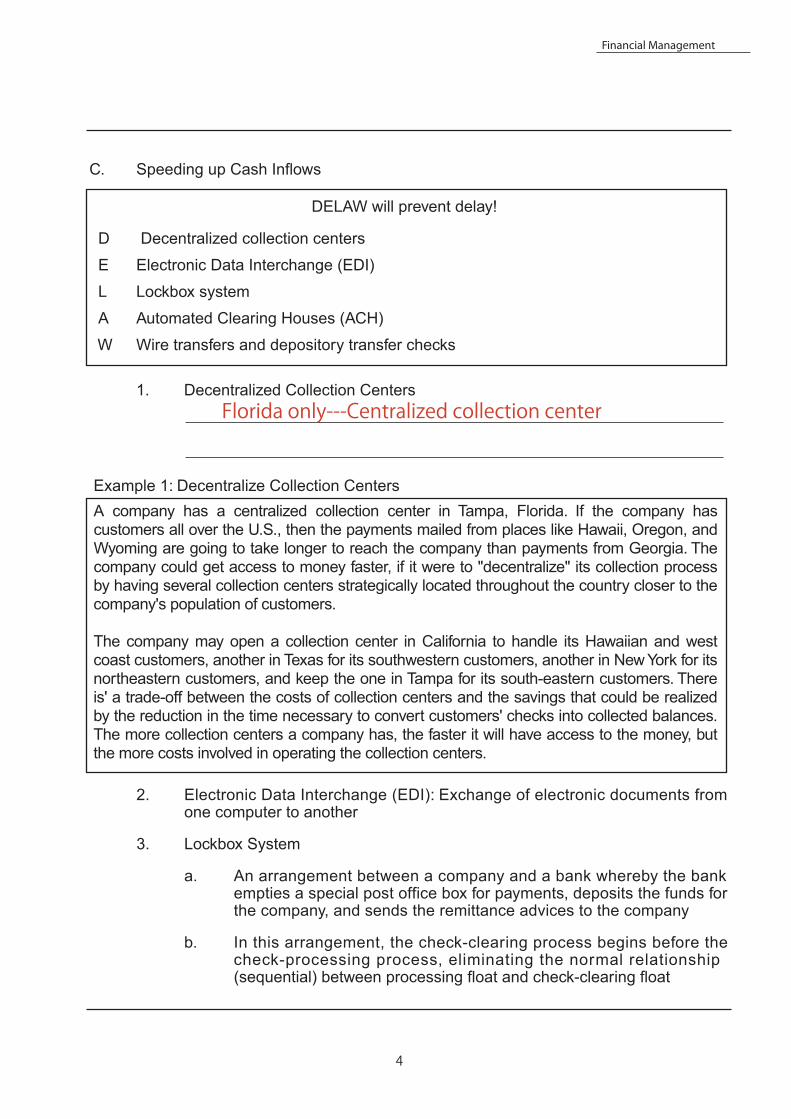

C. Speeding up Cash Inflows

DELAW will prevent delay!

D Decentralized collection centers

E Electronic Data Interchange (EDI)

L Lockbox system

A Automated Clearing Houses (ACH)

W Wire transfers and depository transfer checks

1. Decentralized Collection Centers

Example 1: Decentralize Collection CentersA company has a centralized collection center in Tampa, Florida. If the company has customers all over the U.S., then the payments mailed from places like Hawaii, Oregon, and Wyoming are going to take longer to reach the company than payments from Georgia. Thecompany could get access to money faster, if it were to "decentralize" its collection processby having several collection centers strategically located throughout the country closer to thecompany's population of customers.

The company may open a collection center in California to handle its Hawaiian and westcoast customers, another in Texas for its southwestern customers, another in New York for itsnortheastern customers, and keep the one in Tampa for its south-eastern customers. Thereis' a trade-off between the costs of collection centers and the savings that could be realizedby the reduction in the time necessary to convert customers' checks into collected balances. The more collection centers a company has, the faster it will have access to the money, butthe more costs involved in operating the collection centers.

2. Electronic Data Interchange (EDI): Exchange of electronic documents fromone computer to another

3. Lockbox System

a. An arrangement between a company and a bank whereby the bankempties a special post office box for payments, deposits the funds forthe company, and sends the remittance advices to the company

b. In this arrangement, the check-clearing process begins before thecheck-processing process, eliminating the normal relationship(sequential) between processing float and check-clearing float

Florida only---Centralized collection center

5

Financial Management

4. Automated Clearing House (ACH)

a. Electronic network operated by the Federal Reserve

b. Electronic depository transfer checks are used to move funds from onebank to another and the funds are available for use within 1 day

5. Wire Transfers and Depository Transfer Checks

a. A wire transfer is a fast way to move funds, as they are availableimmediately

b. Costly approach

Example 2: Lockbox System Evaluation

A firm has daily cash receipts of $200,000. A commercial bank has offered to reduce the collection time by 3 days. The bank requires a monthly fee of $4,000 for providing this service. If money market rates will average 12% during the year, should the firm adopt the lockbox system and why?

D. Slowing Down Cash Disbursements

1. Pay by draft (checks/use of float)

Step 1: Compute the increase in funds available: $200,000 per day x 3 days = $600,000increase in cash

Step II: Compute the amount of interest that can be generated from the extra fundsInterest = Principal x Interest Rate x Time $600,000 x 12% x 1 = $72,000

Step III: Compute the annual lockbox cost: $4,000 per month x 12 months = $48,000

Step IV: Compute the net benefit (loss)

Increase in interest due to increased cash balance (Step II) $72,000

Less: Annual lockbox cost (Step III) 48,000

Net Benefit $24,000

6

Financial Management

2. Payable-through-drafts

a. Drafts, but not checks, not payable on demand; drawee is the payee

b. A payable-through-draft must be presented to the issuer and then beaccepted by issuer

c. Slower, but more expensive than checks (higher processing costs)

d. Vendors prefer checks

3. Zero-balancing checking accounts (account with a zero balance)

a. When check comes in, the resulting overdraft is covered by funds froma parent account

b. The costs may be higher because the bank may charge a fee for sucha service

4. Pay beyond normal credit terms

a. Risk ill will

b. incur interest charges

Independently answer questions 5-9.

7

Financial Management

5. Four major motives for holding casharea. Speculative, social, future needs, and

precautionary purposes.b. Speculative, fiduciary, compensating

balances, and transactional purposes.c. Transactional, psychological, future

needs, and social purposes.d. Transactional, precautionary, compen-

sating balance, and speculativepurposes. (9911)

6. Which of the following would not resultin accelerating cash inflows?

a. Compensating balancesb. Decentralize collectionsc. Lockbox arrangementd. Initiating controls to accelerate the

collection and deposit of checks over$225 (9911)

7. Which of the following is a method ofslowing down cash outflows?a. Electronic funds transfersb. A zero-balance checking accountc. Lockbox systemsd. Wire transfers [7295]

8. A compensating balancea. Is a level of inventory held to com-

pensate for changes in the averagequantity used over a 4-month periodof time.

b. Compensates a bank for the servicesit renders to its depositor.

c. Is the amount of money withheld by abank on a discounted note.

d. Is used to compensate for possibleLosses on the company's long-termportfolio of securities available for

)2927( .elas

9. Kemerer Corp uses a central col-lection system that requires all checks to be sent to its Miami, Florida, head-quarters. An average of 5 days is requiredfor mailed checks to be received, 4 days for processing, and 2 days for the checks to clear the bank. A Lockbox system would reduce the mail and process time to 5 days and the check-clearing time to 1 day. Kemerer Corp has average daily collections of $150,000. If Kemerer Corp adopts the lockbox system, by how much would its average cash balance increase?a. $ 225,000b. $ 750,000c. $ 825,000d. $1,050,000 [7294]

QUESTIONS

○

○

○

○

○

8

Financial Management

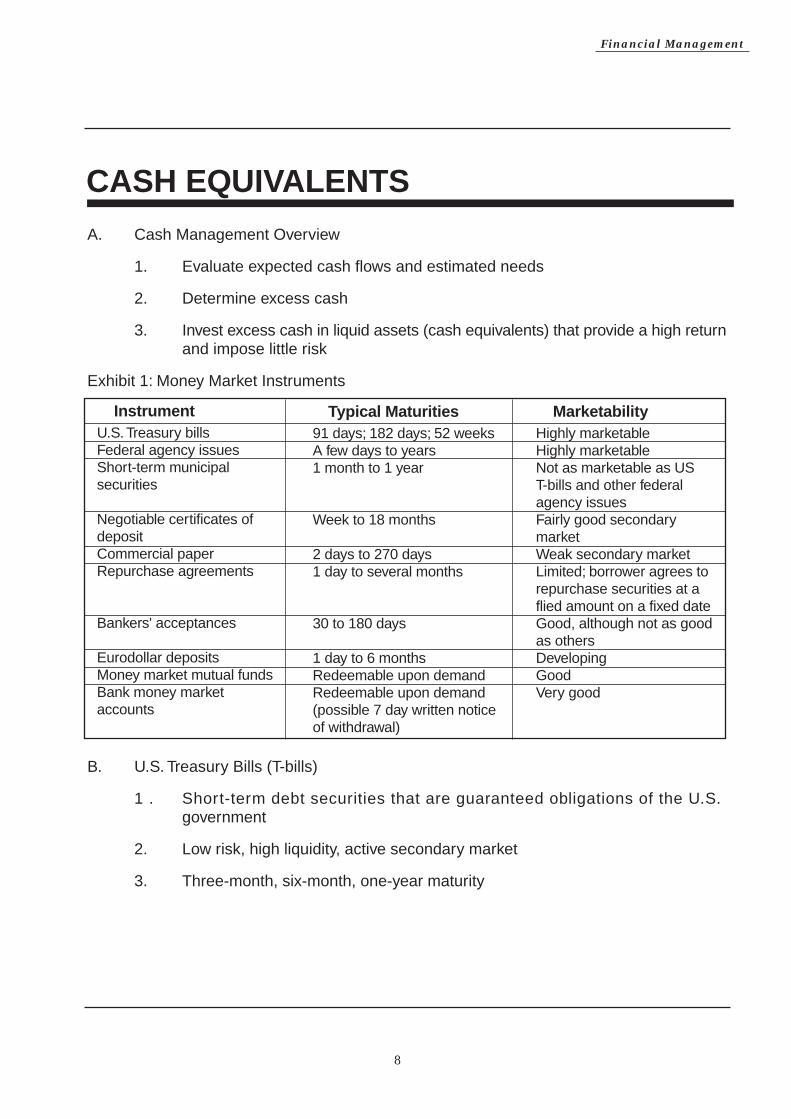

A. Cash Management Overview

1. Evaluate expected cash flows and estimated needs

2. Determine excess cash

3. Invest excess cash in liquid assets (cash equivalents) that provide a high returnand impose little risk

Exhibit 1: Money Market Instruments

B. U.S. Treasury Bills (T-bills)

1 . Short-term debt securities that are guaranteed obligations of the U.S.government

2. Low risk, high liquidity, active secondary market

3. Three-month, six-month, one-year maturity

CASH EQUIVALENTS

Instrument U.S. Treasury billsFederal agency issuesShort-term municipalsecurities

Negotiable certificates ofdeposit Commercial paper Repurchase agreements

Bankers' acceptances

Eurodollar depositsMoney market mutual fundsBank money marketaccounts

Typical Maturities91 days; 182 days; 52 weeksA few days to years1 month to 1 year

Week to 18 months

2 days to 270 days1 day to several months

30 to 180 days

1 day to 6 monthsRedeemable upon demandRedeemable upon demand (possible 7 day written noticeof withdrawal)

Marketability Highly marketable Highly marketable Not as marketable as US T-bills and other federalagency issues Fairly good secondarymarket Weak secondary market Limited; borrower agrees torepurchase securities at aflied amount on a fixed date Good, although not as goodas others Developing Good Very good

9

Financial Management

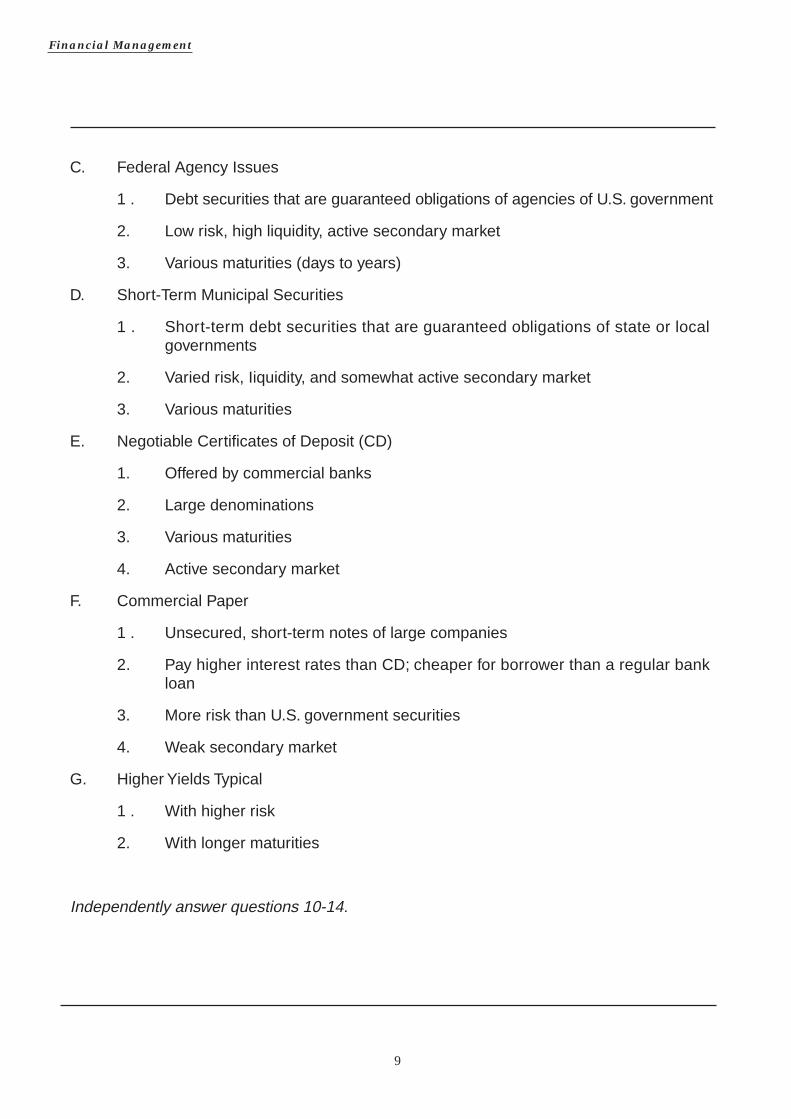

C. Federal Agency Issues

1 . Debt securities that are guaranteed obligations of agencies of U.S. government

2. Low risk, high liquidity, active secondary market

3. Various maturities (days to years)

D. Short-Term Municipal Securities

1 . Short-term debt securities that are guaranteed obligations of state or localgovernments

2. Varied risk, Iiquidity, and somewhat active secondary market

3. Various maturities

E. Negotiable Certificates of Deposit (CD)

1. Offered by commercial banks

2. Large denominations

3. Various maturities

4. Active secondary market

F. Commercial Paper

1 . Unsecured, short-term notes of large companies

2. Pay higher interest rates than CD; cheaper for borrower than a regular bankloan

3. More risk than U.S. government securities

4. Weak secondary market

G. Higher Yields Typical

1 . With higher risk

2. With longer maturities

Independently answer questions 10-14.

10

Financial Management

10. Which of the following is the leastappropriate substitute for cash?a. Banker's acceptanceb. Commercial paperc. Convertible bondsd. U.S. Treasury bills (7364)

11. Commercial papera. Generally has interest rates that are

Lower than treasury bills.b. Is a secured promissory note.c. Typically does not have an active

secondary market.d. Has maturities of greater than 1 year.

[7363]

12. Short-term notes issued by FederalNational Mortgage Association (FNMA) are calleda. Agency securities.b. Banker's acceptances.c. Municipal bonds.d. Repurchase agreements.e. Treasury bills. (7301 )

13. Which of the following is most oftenused as a cash substitute?a. Banker's acceptancesb. Certificate of depositsc. Municipal bondsd. Golde. Treasury bills (7302)

14. Which of the following is the mar-ketable security with the least default risk?a. Banker's acceptancesb. Certificate of depositsc. Municipal bondsd. Golde. Treasury bills (7304)

QUESTIONS

○

○

○

○

○

11

Financial Management

ACCOUNTS RECEIVABLE

A. Credit Policy: Firms should analyze the impact of their credit policies on profits

1. Credit Standards: Financial attributes of customers to which a company givescredit

2. Credit Quality: Probability of default

a. Difficult to identify individuals who will default

b. For a given group, can predict the level of defaults

3. Credit Period: Duration of the credit

a. Longer credit periods may increase sales

b. Shorter credit periods may discourage sales

c. Shorter credit periods generally result in fewer defaults

4. Cash Discounts

5. Collection Policies

a. Sales

b. Bad debt expenses

c. Collections expenses

d. Other expenses associated with A/R

B. Ratios

1. Receivables Turnover Ratio (RTO) = Sales/Average Account Receivables

2. Average Collection Period (ACP)

a. Average number of days to collect a receivable

b. Formula: ACP = Days in year / RTO

12

Financial Management

Example 3: Credit Policy Change Evaluation

Slick requires a rate of return of 12% and has a variable cost ratio of 60%.

Old NewSales $4.8m $5.0mACP 30 days 36 days

For a 360-day year, what is the pretax cost of carrying the additional investment inreceivables?

1 . Determine Old A/R Balance

ACP = 360 / RTO RTO = Sales / Average A/R 30 days = 360 days / RTO 12 times = $4,800,000 / Average A/R

RTO = 360 days / 30 days Average A/R = $4,800,000 / 12RTO = 12 times Average A/R = $400,000

2. Alternatively

Average daily sales ($4,800,000 / 360 days) $ 13,333ACP (in days) 30Average A/R $400,000

3. New A/R Balance

ACP = 36 days = 360 / RTO RTO = Sales / Average A/R36 days = 360 / RTO 10times = $5,000,000 / Average A/RRTO = 360 days / 36 days Average A/R = $5,000,000 / 10RTO = 10 timesAverage Average A/R = $5,000,000 / 10

4. Alternatively

Average daily credit sales ($5,000,000 / 360) $ 13,889ACP (in days) x 36Average A/R $500,000

5. Cost of Additional Investment

Increase in A/R $100,000Cost of credit sales 60 %Additional investment $ 60,000Return rate 12 %Pre-tax cost $ 7,200

Answer question 15

RTO=Receivables Turnover Ratio

ACP=Average Collection Period

13

Financial Management

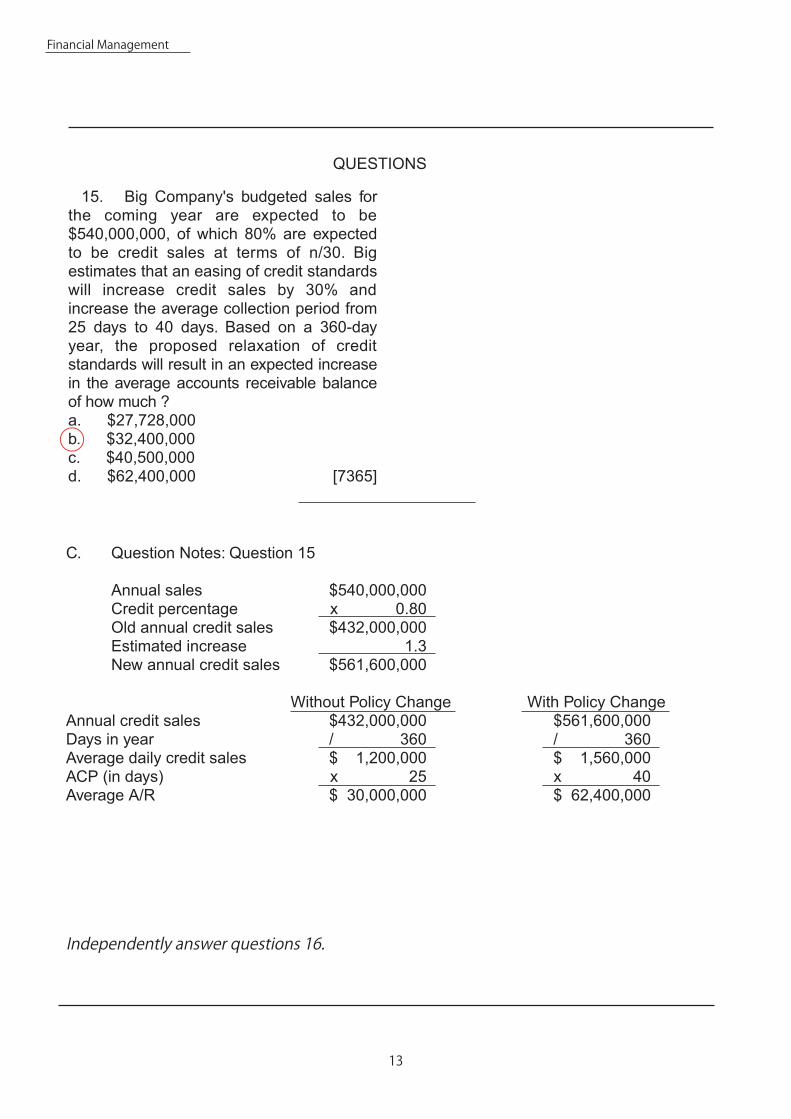

15. Big Company's budgeted sales forthe coming year are expected to be $540,000,000, of which 80% are expected to be credit sales at terms of n/30. Big estimates that an easing of credit standards will increase credit sales by 30% and increase the average collection period from 25 days to 40 days. Based on a 360-day year, the proposed relaxation of credit standards will result in an expected increase in the average accounts receivable balance of how much ?a. $27,728,000b. $32,400,000c. $40,500,000d. $62,400,000 [7365]

QUESTIONS

C. Question Notes: Question 15

Annual sales $540,000,000Credit percentage x 0.80Old annual credit sales $432,000,000Estimated increase 1.3New annual credit sales $561,600,000

Without Policy Change With Policy ChangeAnnual credit sales $432,000,000 $561,600,000D 063 / 063 / raey ni syaAverage daily credit sales $ 1,200,000 $ 1,560,000ACP (in days) x 25 x 40Average A/R 000,004,26 $ 000,000,03 $

Independently answer questions 16.

○

14

Financial Management

16. Smith Wholesale Company hasaverage daily sales of $50,000 based on a 360-day year. All of Smith's sales are on credit with terms of 2/10, net 45. Customers representing 30% of sales pay on day 45 and the remaining customers take the discount and pay on day 10. What are Smith's average daily collections from customers?a. $34,300b. $45,000c. $49,300

)5137(000,05$ .d

QUESTION

○

15

Financial Management

INVENTORY

A. Ordering Costs: Costs of placing and receiving an order of goods.

1. Quantity discounts lost

2. Shipping costs

3. Purchasing costs

4. Set-up costs (manufacturing environments)

B. Carrying Costs: Costs of holding inventory for a given period of time

1. Handling costs

2. Interest on invested capital

3. Storage costs

4. Obsolescence

C. Stockout Costs: Costs incurred when a firm is unable to fill an order

1. Lost sales

2. Rescheduling production

3. Expediting special orders

D. Goal: Balance costs

1. Ordering costs

2. Carrying costs

3. Stockout costs

E. Economic Order Quantity (EOQ)

1. EOQ Formula

EOQ = 2OD

C

2. Basic EOQ Model Mnemonic: To overdose oversea makes you a square root

a. To: 2

b. O: Ordering costs per order

c. D: Annual demand in units

d. C: Carrying costs per unit

16

Financial Management

Example 4: EOQ Model

Florida Electronic Tools (FET) uses integrated circuits in the manufacturing of calcula-tors. The annual demand for its integrated circuits is 110,000 units. Each integrated circuits costs $2. It costs an average of $0.30 per year to carry one integrated circuit in inventory and $41.25 to place an order. It takes about 15 days from the time an order is placed until it is received. FET assumes there are 250 working days per year in its calculations.

Required: Determine the economic order quantity.

EOQ = 2* $41.25* 110,000 0.3

EOQ = 5,500 units

Required: Determine the number of orders that will be placed each year.

Number of orders = Annual Demand / EOQ = 110,000 units / 5,500 units = 20 orders

Required: Determine the reorder point.

ROP = Lead Time x Daily Demand

= 15 days x 110,000 units per year/250 days

= 15 days x 440 units per day

= 6,600 units

Required: Determine the safety stock.

ROP = EOQ + Safety Stock

If FET desired to maintain a 2 day safety stock, they would reorder at the pointwhere inventory reached a level of 7,480 units (6,600 plus 880)

ROP=Reorder point

17

Financial Management

F. Reorder Point (ROP)

1. The level of inventory in which the company must place an order so that it doesnot run out of inventory

2. ROP = Lead Time x Daily Demand

G. Safety Stock

1. Buffer or excess in case it takes longer than the lead time (due to variability)

2. Refined ROP = Lead Time x Daily Demand + Safety Stock

Independently answer question 17-21.

18

Financial Management

17. The economic order quantity for a product is 1,000 units. However, new orders require 5 working-days lead time during which time 100 units will be used. What is the economic order quantity? a. 900 units b. 1,000 unitsc. 1,025 unitsd. 1,100 units (9911)

18. In inventory management, the safety stock will tend to decrease if thea. Cost of running out of stock increases.b. Variability of the lead time decreases.c. Variability of the usage rate increases.d. Carrying costs decrease. [7372]

19. An increase in which one of the following variables would decrease the economic order quantity?a. Carrying costsb. Safety stock levelc. Annual salesd. Cost per order [7369]

20. What costs are included in carrying cost in the economic order quantity model?a. Shipping costsb. Quantity discounts lostc. Handling costsd. Purchasing costs [7269]

21. Which of the following is least likely to affect the inventory safety stock level?a. The degree of customer intolerance

for back ordersb. The degree of sales forecast

uncertaintyc. The degree of shipment lead time

uncertaintyd. The order placement costs e. Stock out costs (7346)

QUESTIONS

○

○

○

○

○

19

Financial Management

SHORT-TERM DEBT

A. Borrowing Considerations

1. What is the amount of cost?

2. When should we borrow?

3. When should a firm pay within the cash discount period?

B. Annual Financing Costs (AFC): Cost of not taking the discount, assuming we would otherwise borrow money to pay within the discount period

1. A firm should pay within the discount period when the firm's cost of capital is less than the cost of not taking the discount

2. Take cash discount, if we can borrow at an AFC that is lower than the rate implied by the cash discount

C. Annual Financing Costs (AFC)

1. Formula for One-Year Loan: AFC = Borrowing Costs / Net Funds Available

2. Formula for All Loans: AFC = Loan Costs x Days in Year / Net Funds Available x Loan Term

D. Cash Discount on Purchases

1. Take cash discount, if we can borrow at an AFC that is lower than the rate implied by the cash discount

2. AFC Implied by Cash Discount

Discount % / (100% – Discount %) x 360 days / (Full Credit Period – Discount Period)

a. Loan Term: Full credit period less discount period

b. Credit Terms: 1/15, Net 30

(1) If paying within 15 days, take a 1% discount

(2) If paying within 30 days, pay the full amount

20

Financial Management

22. The annual interest cost associated with a company offering credit terms of 2/10, net 30, based on a 360-day year, is

a. 35.3%b. 24.0%c. 36.0%

]9437[ %7.63 .d

QUESTION

23. A firm requires payment within 45 days but allows customers to take a discount of 2% if paid within 15 days. Assuming a 360-day year the annual interest cost of the trade credit terms isa. 16%.b. 24%.c. 48%.

]9437[ .%2 .d

24. An organization usually would offer credit terms of 2/10, net 30 whena. The cost of capital is approximately

the prime rate.b. The organization can borrow funds at

a rate that exceeds the annual financing costs.

c. All of its major competitors are offer-ing the same terms and the organi-zation has a shortage of cash.

d. The organization can borrow funds at a rate less than the annual financing costs. (7310)

QUESTIONS

Example 5

The credit terms are 1/15, n30. What is the cost of not taking the discount?

1% / (100% – 1%) x 360 days / (30 days – 15 days)1% / (99%) x 360 days / (15 days) = 24.24% annualized interest

Answer question 22 with Kevin

E. Question Notes: Question 22

2% / 360 days x (100% – 2%) / (30 days – 10 days) %2 x 360 days / 98% x 20 days

ilaunna %37.63 zed interest

Independently answer questions 23-24.

○

○○

21

Financial Management

Notes:

F. Question Notes: Question 23

2%/ (100% – 2%) x 360 days/(45days – 15days) 2%/ 98% x 360days / 30days 24.49% annualized interest

G. Compound Interest

1. Might not be tested

Example 6: Compound Interest

The credit terms are 1/15, n30. What is the cost of not taking the discount, assuming compounded interest?

Annual Financing Costs (AFC) = 27.3% [1 + [Disc % / (100 – Disc %)]] (360/Disc) –1 [1 + [1% / (100% – 1%)]] (360/15) –1 [1 + (1%/99%)]24 –1 [1 +0.0101]24 –1 1.272755 –1

2. Compound vs. Simple Interest

a. Simple interest, 24.2% (Example 5)

b. Compound interest, 27.3% (Example 6)

c. Compounding grows faster

Answer questions 25-26

22

Financial Management

25. AC, Inc. issues 3-month commercial paper with a face value of $500,000 for $490,000 and incurs transaction costs of $1,000. The effective annualized percentage cost of the financing, based on a 360-day year, will bea. 8.16%.b. 8.00%.c. 2.00%.

)1199(.%00.9 .d

26. What is the effective interest rate on a loan if a firm borrows $400,000 at 8% and is required to maintain $50,000 as a minimum compensating balance at the bank, based on a 360-day year?a. 8.0%b. 9.1%c. 12.2%d. 20.5% [7374]

QUESTIONS

H. Question Notes

1. Question 25

a. AFC = Loan Costs x Days in Year / Net Funds Available x Loan Term = $11,000 x 360 days / ($490,000 – $1,000) x 90 days = $11,000 x 4 / $489,000 = 9.00%

b. Interest = Amount to repay – Net funds available = $500,000 – $490,000 = $10,000

c. Effective Interest

(1) Difference in face amount and proceeds, $10,000

(2) Transaction costs, $1,000

2. Question 26

a. AFC = Loan Costs x Days in Year / Net Funds Available x Loan Term

$32,000 x 360 days / $350,000 x 360 days

$32,000 x 1 / $350,000 = 9.1%

Interest = Principal x Rate x Time = $ 400,000 x 8% x 360/360 = $32,000

Independently answer questions 27-31.

○

○

23

Financial Management

27. Hardy must maintain a compensating balance of $60,000 in its checking account as one of the conditions of its short-term 8% bank loan of $600,000. Hardy's checking account earns 3% interest. Ordinarily, Hardy would maintain a $50,000 balance in the account. What is the loan's approximate effective interest rate? Ordinarily, Hardy would maintain a $50,000 balance in the account. What is the loan's approximate effective interest rate?a. 8.00%b. 8.08%c. 8.73%

]3537[%98.8 .d

Items 28 through 30 are based on the following information.

Fox Company needs to pay a supplier's invoice of $50,000 and wants to take a cash discount of 2/10, net 30. The firm can borrow the money for 20 days at 10% Perannum with an 8% compensating balance. Fox assumes a 360-day year.

28. The amount Fox Company must borrow to pay the supplier within the discount period and cover the compensating balance isa. $50,000.b. $54,348.c. $53,261.d. $49,000. (9911)

29. If Fox Company borrows the money on the last day of the discount period and repays it 20 days later, what is the effective interest rate on the loan?a. 10.0%b. 10.9%c. 8.0%d. 9.9% (9911)

30. If Fox fails to take the discount and pays on the 30th day, what effective rate of annual interest is it paying the vendor?a. 24%b. 36.73%c. 2%d. 24.49% (9911)

31. A firm is considering factoring its accounts receivable. The finance company requires a 5% reserve and charges a 1.5%commission on the amount of the receivables. In addition the amount advanced to the firm is also reduced by an annual interest charge of 12%. What is the amount of proceeds (rounded to the nearest dollar) the firm will receive from the finance company at the time a $200,000 account due in 90 days is factored?a. $187,000b. $181,390c. $191,090d. $176,000 (9911)

QUESTIONS

○

○

○

○

○

Financial Management

I. Question Notes

1. Question 27

a. Interest = Principal x Rate x Time = $600,000 x 8% x 360/360 = $48,000

b. Compensating Balance

(1) Hardy ordinarily would maintain $50,000

(2) Due to loan requirements, Hardy must maintain $60,000

(3) $10,000 more than Hardy ordinarily would maintain

(4) Interest earned on compensating balance somewhat offsets theinterest paid

c. Net Funds Available = Loan Proceeds - Compensating Balance =$600,000 - $10,000 = $590,000

d. AFC = Loan Costs x Days in Year / Net Funds Available x Loan Term = ($48,000 - $300) x 360 / ($600,000 - $10,000) x 360 = $47,700 / $590,000 = 8.08%

2. Question 28: Need to borrow enough money to pay the discounted amount tothe supplier and still keep an 8% compensating balance

Invoice $50,000Less: Discount ($50,000 x 2%) 1,000Pay to supplier $49,000

Loan = $49,000 + 0.08 Loan0.92 Loan = $49,000Loan = $49,000 / 0.92 = $53,261

3. Question 29

a. AFC = Loan Costs x Days in Year / Net Funds Available x Loan Term

b. AFC = $295.89 x 360 / $49,000 x 20 = 10.87%

c. Interest = Principal x Rate x Time = $53,261.00 x 10% x 20/360 = $295.89

24

25

Financial Management

4. Question 30

a. AFC = Loan Costs x Days in Year / Net Funds Available x Loan Term

b. AFC = 2% x 360 days / (100% – 2%) x (30 days – 10 days) = 2% x 360days / 98% x 20 days = 36.73%

26

Financial Management

A. Capital Structure: Mix of debt, preferred, and common equity

1. Overview

a. Assets = Liability + Equity

b. Borrow money or use owners' money

2. Optimal: Mix of financing at which the company's stock price is maximized

a. Involves the trade-offs of higher expected return on equity and earningsper share (EPS) against higher risk

b. Difficult to determine

3. Target: Mix of financing with which the firm intends to raise capital

B . Leverage

1 . Relative amount of fixed cost in a firm's capital structure

a. Fixed asset costs

b. Long-term debt costs

2. Leverage magnifies results

C. Degree of Financial Leverage (DFL): An expression of the relationship between EPS

and earnings available to common shareholders

1 . Financial leverage causes a firm's EPS to fluctuate at a rate which is greaterthan that of the change in earnings before interest and taxes, or EBIT(operating income)

2. Formula

a. DFL = % Change in EPS / % Change in EBIT

b. DFL = EBIT / {EBIT –I– [P / (1-T)]}

(1) I = Interest

(2) P = Preferred dividends

CAPITAL STRUCTURE

27

Financial Management

3. Financial Leverage

a. Generally, firms with high DFL are deemed higher risk than firms withlow DFL

b. High debt and preferred stock is not good for common stockholders inthe event of financial stress

(1) Creditors get paid before owners

(2) Preferred stockholders get paid dividends before common stockholders

c. Why have debt?

(1) Borrowing spreads cost of financing to non-owners (spreading risk)

(2) Tax break on interest costs

D. Degree of Operating Leverage (DOL): An expression of the relationship betweenoperating income and sales

1. Formula

a. DOL = % Change in EBIT / % Change in Sales

b. DOL = CM / EBIT

2. Operating Leverage

a. Involves the use of assets with a fixed cost

b. The more a firm makes use of assets with a fixed cost (operating leverage)the more the variability in EBIT, and thus, the more business risk

Independently answer questions 32-33.

CM=Contribution Margin

28

Financial Management

Items 32 through 33 are based on the following information.

Owen Company sells 200,000 jars of pickles annually for $2 per jar. Variable costs are $0.60 per jar and fixed costs are $70,000 annually. Owen has annual interest expense of $60,000 and a 30% income tax rate.

32. What is Owen's approximate degreeof operating leverage?a. 2.67b. 1.08c. 1.33d. 1.87 [7334]

33. What is Owen's approximate degreeof financial leverage?a. 2.67b. 1.08c. 1.40d. 1.33 [7335]

QUESTIONS

E. Question Notes

1. Question 32

DOL = CM / EBIT

CM = 200,000 x ($2.00–$0.60) = $280,000

EBIT = CM–Fixed Costs (not interest) = $280,000–$70,000 = $210,000

DOL = CM / EBIT = $280,000 / $210,000 = 1.33

2. Question 33

DFL = EBIT / {EBIT – I – [P/(1-T)]}

DFL = $210,000/($210,000-$60,000 – 0) =$210,000 / $150,000 = 1.4

○

○

29

Financial Management

COST OF CAPITAL

A. Cost of Using Money

1 . Sources

a. Borrowing (debt)

b. Operations (retained earnings)

c. Issuing new stock (preferred or common)

2. Equal to the equilibrium rate of return demanded by investors in the capital markets for securities of that degree of risk

a. Determined in capital markets

b. Depends on the risk associated with the firm’s activities

c. What the firm must pay for capital

d. Return required by investors

3. Weighted Average Cost of Capital = Cost of each financing source times its weight

B. Cost of Debt

1. Formula: ki=kd(1 – T)

a. kd = Interest rate on debt being issued

b. T = Tax rate

2. Reflects the tax shield from interest paid on debt

a. If tax rate increases

b. Then, cost of debt decreases

C. Cost of Preferred Stock

1. kp = Dp / Net issuance price

2. Dp = Dividend on preferred stock

30

Financial Management

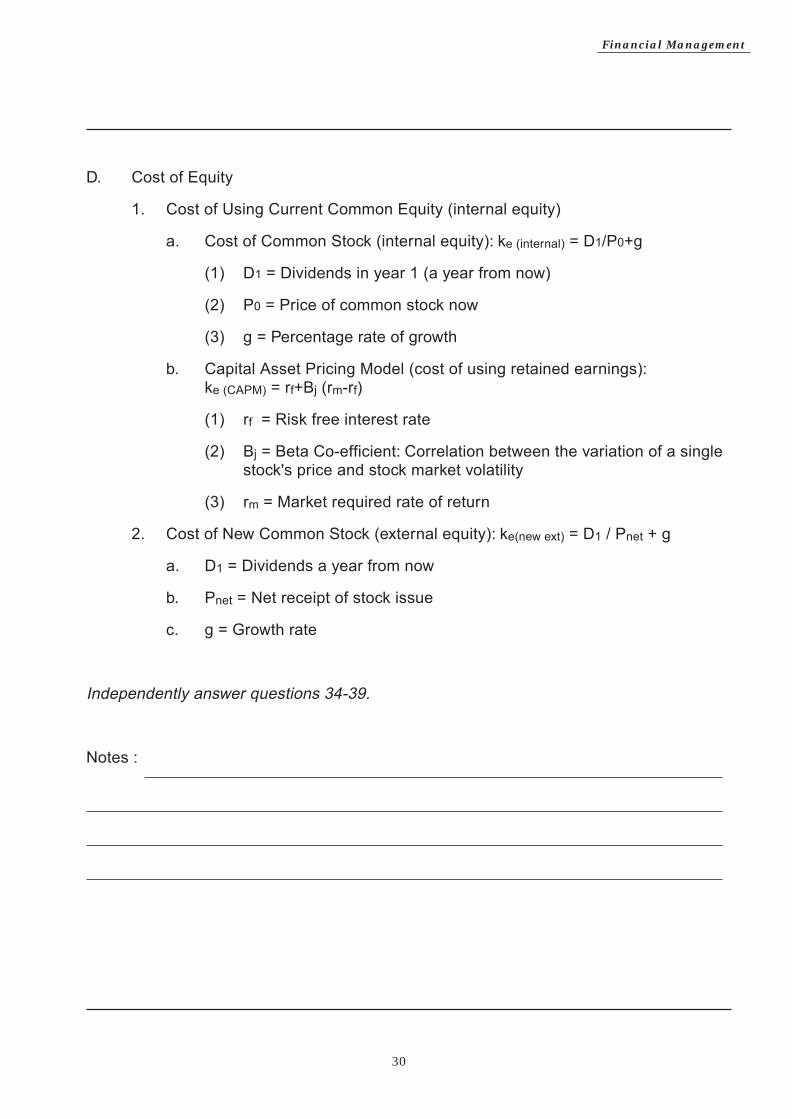

D. Cost of Equity

1. Cost of Using Current Common Equity (internal equity)

a. Cost of Common Stock (internal equity): ke (internal) = D1/P0+g

(1) D1 = Dividends in year 1 (a year from now)

(2) P0 = Price of common stock now

(3) g = Percentage rate of growth

b. Capital Asset Pricing Model (cost of using retained earnings): ke (CAPM) = rf+Bj (rm-rf)

(1) rf = Risk free interest rate

(2) Bj = Beta Co-efficient: Correlation between the variation of a single stock's price and stock market volatility

(3) rm = Market required rate of return

2. Cost of New Common Stock (external equity): ke(new ext) = D1 / Pnet + g

a. D1 = Dividends a year from now

b. Pnet = Net receipt of stock issue

c. g = Growth rate

Independently answer questions 34-39.

Notes :

31

Financial Management

Items 34 through 39 are based on the following information.

Jimmy, Inc., is interested in measuring its cost of capital. It has gathered the following data. Jimmy can sell unlimited amounts of all instruments.• Jimmy can sell $1,000, 7.5%, 15-year

bonds with annual interest payments. In selling the issue, an average premium of $25 per bond would be received, and the firm must pay flotation costs of $25 per bond. The after-tax cost of funds is estimated to be 4.8%.

• Jimmy can sell 9% Preferred stock at $90 per share.

• Jimmy's common stock is currently selling for $100 per share. The firm expects to pay cash dividends of $6 per share next year, and the dividends are expected to remain constant. The stock will have to be under priced by $5 per share, and flotation costs are expected to amount to $4 per share.

• Jimmy expects to have $100,000 of retained earnings in the coming year; after these retained earnings are exhausted, the firm will issue new common stock as the form of common stock equity financing.

Jimmy prefers the following capital structure.

• Long-term debt 20%• Preferred stock 30%• Common stock 50%

34. The cost of funds from the sale of common stock for Jimmy, Inc. isa. 6.00%b. 6.32%c. 6.45%d. 6.59% [7375]

35. The cost of funds from retained earnings for Jimmy, Inc. isa. 6.0%b. 7.4%c. 7.6%d. 8.1% [7376]

36. The cost of funds from the sale of 15-year bonds isa. 4.80%b. 6.32%c. 6.45%d. 7.50% (9911)

37. The cost of funds from the sale of preferred stock for Jimmy, Inc. isa. 4.80%b. 7.50%c. 9.00%d. 10.00% (9911)

38. If Jimmy, Inc. needs a total of $500,000, the firm's weighted-average cost of capital would bea. 6.66%b. 6.84%c. 6.96%d. 9.00% [7377]

39. If Jimmy, Inc. needs a total of $1,000,000, the firm's weighted-average cost of capital would bea. 4.80%b. 6.5%c. 6.9%d. 27.4% [7378]

QUESTIONS

○

○

○

○

○

○

32

Financial Management

E. Question Notes

1. Question 34: Cost of New Common Stock = Ke (new ext) = D1 / Pnet + g = $6 / $91 + 0 = 6.59%

Current common stock price $100 Discount 5 Floatation costs 4 Net receipts of common stock issue, per share $ 91

2. Question 35: Cost of Internal Equity = ke(internal) = D1 / P0 + g = = $6 / $100 + 0 = 6%

3. Question 36: Cost of Debt = ki = kd (1 – T)

kd = Interest rate on issued debt

T = Tax rate

4. Question 37: Cost of Preferred Stock Formula = kp = Dp / net issuance price

Dp = Dividend on preferred stock = $90 x 9% = $8.10

kp = ($8.10) / $90 = 9%

5. Question 38: Total Weighted Average Cost of Capital = Cost of each financing source times its weight

WA Cost of Capital Target Capital Structure LT Debt (20% x 4.8%) 0.96% $ 100,000 / $500,000 = 20% PS (30% x 9.0%) 2.70 150,000 / $500,000 = 30% RE (20% x 6.0%) 1.20 100,000 / $500,000 = 20% New Issue (30% x 6.59%) 1.98 150,000 / $500,000 = 30% Total Cost of Capital 6.84% $ 500,000

6. Question 39

WA Cost of Capital Target Capital Structure LT Debt (20% x 4.8%) 0.96% $ 200,000 PS (30% x 9.0%) 2.70 300,000 RE (10% x 6.0%) 0.60 100,000 New Issue (40% x 6.59%) 2.64 400,000 Total Cost of Capital 6.90% $1,000,000

33

Financial Management

INTEREST RATES

A. Components

1 . Risk-free rate

2. Inflation premium

3. Maturity risk premium

B. Graph

C. Yield

1. Typically, yield increases on a non-linear basis with maturity length

2. Usually, the longer the bond term, the higher the interest rate

D. Term Comparison: Note that the yield curve is an upward sloping yield curve

1. As the term of maturity increases the yield increases but not linearly

2. Upward slope due to an increase in expected inflation and increasing maturity risk premium

1 10 20

15

10

5

0

Interest Rate (%)Maturity risk premium

Inflation premium

Real risk-free rate

Years to Maturity

34

Financial Management

A. Security Valuation: Process of determining at what price a security ought to sell

B. Bond Valuation

1. Nature

a. Principal: Debt security where the issuer promises to pay the face amount at a specified future date (maturity date)

b. Interest: Usually, the issuer also promises to pay a stated rate of interest on the face amount

(1) For instance, $1,000 bond at 10% interest, interest is $100 annually

(2) Interest payment is calculated based on face amount, regardless of actual sales price

2. Valuation: Present value of cash flows associated with the bond

Bond Value = PV (Principal) + PV (Interest)

a. Principal Cash Flow: Single sum being received or paid one time at some point, n number of periods in the future

(1) Single payment (one payment of the face amount)

(2) $1,000 five-year term bond, semiannual 10% interest

(3) Promise to pay $1,000 five years into the future

(4) Figure the present value of a single sum

b. Interest Payments Cash Flow: Annuity (series of n equal payments)

SECURITY VALUATION

35

Financial Management

C. Time Value of Money

1. Single Sum: One payment

2. Ordinary Annuity (Annuity in Arrears)

a. Series of payments at end of periods

b. Payments occur at the end of each period

3. Annuity Due (Annuity in Advance)

a. Series of payments at beginning of periods

b. Payment occurs at the beginning of each period

D. Coupon (Stated) Rate

1. Determines interest payments

2. Multiply stated rate times face amount of bonds to determine interest payments

E. Effective (Market) Rate

1. Used for determining the present value of principal and interest payments

2. Used to discount cash flows

3. Determines interest income and expense

F. Sales Price

1. Face Value: When effective interest rate equals stated interest rate

2. Discount

a. When effective interest rate is greater than stated interest rate

b. Issuer must discount bond to attract investors

Example7: Discount

Market interest rate, 12%

Stated interest rate, 10%

Issuer must lower the price of the bond to attract investors

In other words, the bond sells at a discount

36

Financial Management

3. Premium

a. When effective interest rate is less than stated interest rate

b. Investors are willing to pay a premium

Example 8: Premium

Market interest rate, 10%

Stated interest rate, 11%

Investors will bid against each other and increase the price of the bond

Example 9: Discount

On January 1 , 2005, Hound, Inc., issued $100,000 of 10%, five-year bonds with a stated interest rate of 10%. Pay interest semi-annually on June 30 and December 31. Effective rate is 12%.

Conclusion: Bond sells at discount; issuer must lower the price of the bond to attract investors

Interest Payment = $100,000 x 10% x 1/2 = $5,0005 years of semi-annual payments; 10 payments over the life of the bond

Present Value of an Annuity (PVA) PVA = Rents x PVAF (i, n) PVAF = Present value annuity factor i = Effective interest rate = 6% n = Number of payments = 10 PVA = Rents x PVAF (6%, 10) = $5,000 x 7.36 = $36,800

Present Value of a Single Sum (PV) PV = Payment x PVF (i, n) PVF = Present value factor i = Effective interest rate = 6% n = Number of periods = 10 PV = Payment x PVF (6%, 10) = $100,000 x 0.558 = $55,800

PV interest paymentsPV principal paymentPresent Value of Bond

$36,800 55 800

$92,600

37

Financial Management

Example 10: Premium

On January 1, 2005, Hound, Inc., issued $100,000 of 12%, five-year bonds with a stated interest rate of 12%. Pay interest semi-annually on June 30 and December 31. Effective rate is 10%.

Conclusion: Bond sells at premium; investors will bid against each other and increase the price of the bond

Interest Payment = $100,000 x 12% x 1/2 = $6,0005 years of semi-annual payments; 10 payments over the life of the bond

Present Value of an Annuity (PVA)PVA = Rents x PVAF (i, n)PVAF = Present value annuity factori = Effective interest rate = 5%n = Number of payments = 10PVA = Rents x PVAF (5%, 10) = $6,000 x 7.722 = $46,300

Present Value of a Single Sum (PV)PV = Payment x PVF (i, n)PVF = Present value factori = Effective interest rate = 5%n = Number of periods = 10PV = Payment x PVF (5%, 10) = $100,000 x 0.614 = $61,400

PV interest paymentsPV principal paymentPresent Value of Bond

$ 46,30061,400

$107,700

38

Financial Management

G. Stock Valuation

1. Essentially, same as bonds

a. Dividend Purposes: Stock price = PV of future dividends

b. Stock Price Appreciation (what you could sell it for in the future): Stock price = PV of future dividends because you would discount the dividends you expect to receive and then the purchaser would be valuing the stock at the PV of the future cash flows at that point in time.

2. Constant Growth Model: P0 = d1 / (k – g)

a. d1 = Dividend one year from now

b. k = Required rate of return

c. g = Growth rate

Example 11: Constant Growth Stock

IMB stock paid $2/share this year

Dixon Company anticipates a constant growth rate for IMB dividends of 6% Dixon seeks an 8% rate of return

Required: What is IMB stock worth to Dixon?

P0 =d1 /(k – g) = ($2.00 x 1.06) / (8% - 6%) = $2.12/2% = $106.00

Example 12: Zero Growth Stock

IMB stock paid $2/share this year Dixon Company anticipates a zero growth rate for IMB dividends of 6% Dixon seeks an 8% rate of return

Required: What is IMB stock worth to Dixon?

P0 = d1/ (k – g) = ($2.00x1.00) / (8% - 0%) = $2.00 / 8% = $25.00

39

Financial Management

Example 13: Payback

Major Corp. is considering purchasing a new machine for $5,000 that will have an estimated useful life of five years and no salvage value. The machine will increase Major's after-tax cash flow by $2,000 annually for five years. Major uses the straight-line method of depreciation and has an incremental borrowing rate of 10%. The present value factors for 10% are as follows.

Ordinary annuity with five payments 3.79Annuity due for five payments 4.17

Required: How many years will it take to pay back the initial investment?

Initial investment After-tax cash flowsPayback period (years)

$5,000 / 2,000

2.50

CAPITAL BUDGETING

A. Payback Period: Number of years for the cumulative net after-tax cash Flows from a project to equal the initial cash outlay

1. Simple

2. Based on cash flows

3. Provides a measure of project liquidity and a measure of risk

4. Ignores cash flows after the payback period and the time value of money

B. Accounting Rate of Return (ARR): Average net income / Average investment in project

1 . Advantages: Easily understood

2. Disadvantages

a. Ignores the time value of money

b. Uses accrual numbers, not cash flows

40

Financial Management

Example 14: Accounting Rate of Return

Tam Co. is negotiating for the purchase of equipment that would cost $100,000, with the expectation that $20,000 per year could be saved in after-tax cash costs if the equipment were acquired. The equipment's estimated useful life is 10 years, with no residual value, and would be depreciated by the straight-line method. Tam's predetermined minimum desired rate of return is 12%.

Required: What is the accounting rate of return?

Average after-tax cash savings $20,000 Less: Depreciation 10,000 Average net income $10,000

ARR = $10,000/$100,000 = 10%

C. Internal Rate of Return

1 . Discount rate that equates the PV of net cash flows of a project with the PV of the net investment

a. If IRR > k, acceptable project

b. Assumption: Cash flows are reinvested at IRR

2. Advantages

a. Considers the time value of money

b. Considers all the cash flows

c. Project's rate of return is estimated

3. Disadvantages

a. More difficult to use

b. Cash flows are assumed to be reinvested at rate earned by project

Answer question 40

41

Financial Management

40. Tam Co. is negotiating for the purchase of equipment that would cost $100,000, with the expectation that $20,000 per year could be saved in after-tax cash costs if the equipment were acquired. The equipment's estimated useful life is 10 years, with no residual value, and would be depreciated by the straight-line method. Tam's predetermined minimum desired rate of return is 12%. Present value of an annuity of 1 at 12% for 10 periods is 5.65. Present value of 1 due in 10 periods at 12% is 0.322. In estimating the internal rate of return, the factors in the table of present values of an annuity should be taken from the columns closest to what number?a. 0.65b. 1.30c. 5.00

)1199(56.5 .d

QUESTION

D. Question Notes: Question 40

Net Investment Present Value = $100,000

Cash Flows Present Value = $20,000 x PVAF(i, 10)

IRR = $20,000 x PVAF(i, 10) = $100,000

PVAF(i, 10) = $100,000 / $20,000 = 5.0

○

42

Financial Management

E. Net Present Value (NPV)

1. NPV = PV of the stream of net future cash flows from a project less the project's net investment

a. Rule: NPV > O; acceptable return

b. Company is generating a return greater than the required rate of return, resulting in above-normal profits

2. Advantages: Considers the time value of money

3. Disadvantages: NPV not easily understood

4. Assumes: Cash flows over the project's life reinvested at the required rate of return

F. Relating NPV & IRR

1. Very similar

2. If the NPV & IRR techniques disagree, NPV is preferred

3. Generally

a. If NPV > 0, then IRR > k

b. If NPV < 0, then IRR < k

Example 15: Net Present Value

Helm Foundation, a tax-exempt organization, invested $400,000 in a five-year project. Helm estimates that the annual cash savings from this project will amount to $130,000. The $400,000 of assets will be depreciated over their five-year life on the straight-line basis. For investments of this type, Helm's desired rate of return is 12%. Information on present value factors is as follows:

12% 14% 16%PV of 1 for 5 periods 0.57 0.52 0.48PVA of 1 for 5 periods 3.6 3.4 3.3

What is the net present value of the project?

PV of Cash Inflows ($130,000 x 3.6) $ 468,000 Less: Net Initial Investment (400,000)NPV $ 68,000

43

Financial Management

G. Profitability Index (PI)

1 . Ratio of the PV of future cash flows over the life of the project to the netinvestment

2. PI > 1 ; acceptable project

3. Considers the time value of money.

4. Assumes cash flows reinvested at k

5. Essentially the same as NPV

H. Comparison of PI and NPV

1. Pl > 1 , NPV> $0; accept the project

2. Pl = 1 , NPV = $0; indifferent

3. Pl < 1 , NPV < $0; reject the project

I. Return on Investment (ROI)

1. ROI = Net Income / Average Total Assets

2. ROI = Margin x Turnover = Net Income / Sales x Sales / Average Assets = NetIncome / Average Total Assets

Example 16: Return on Investment

Beazley Company

Sales $500,000 Capital Turnover 4Operating Income 50,000 Imputed Interest Rate 10%

Required: What was Beazley's return on investment?

ROI = NI / Average Total Assets = $50,000 / Average Total Assets

Capital Turnover = Sales / Average Total Assets

4 = $500,000 / Average Total Assets

Average Total Assets = $500,000 / 4 = $125,000

ROI = NI / Average Total Assets = $50,000 / $125,000 = 40%

Capital Turnover=Asset Turnover

44

Financial Management

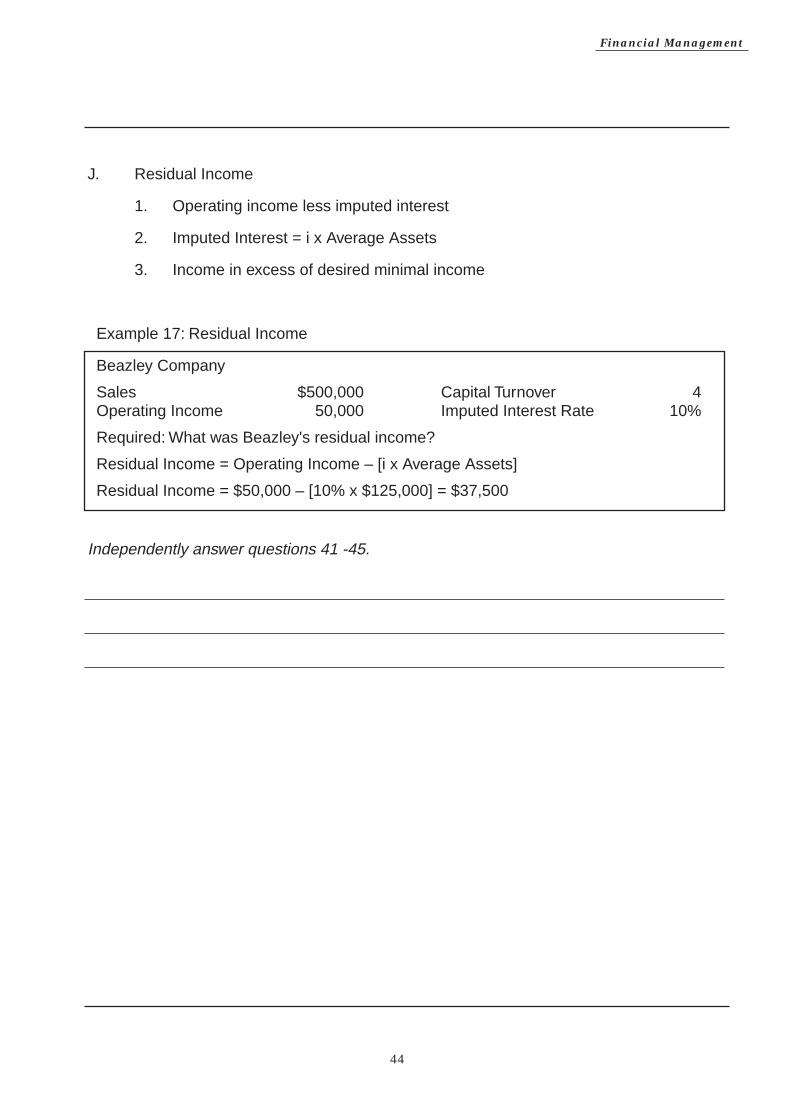

J. Residual Income

1. Operating income less imputed interest

2. Imputed Interest = i x Average Assets

3. Income in excess of desired minimal income

Example 17: Residual Income

Beazley Company

Sales $500,000 Capital Turnover 4 Operating Income 50,000 Imputed Interest Rate 10%

Required: What was Beazley's residual income?

Residual Income = Operating Income – [i x Average Assets]

Residual Income = $50,000 – [10% x $125,000] = $37,500

Independently answer questions 41 -45.

45

F inancial Management

41. Which of the following capital budgeting techniques implicitly assumes that the cash flows are reinvested at the company's minimum required rate of return?

42. A proposed project has an expected economic life of eight years. In the calculation of the net present value of the proposed project, salvage value would be included as a cash inflow at thea. Exclude present value.b. Future value of the estimated salvage

value.c. Estimated salvage value.d. Present value of the estimated salvage

value. (2258)

43. Neu Co. is considering the purchase of an investment that has a positive net present value based on Neu's 12% hurdle rate. The internal rate of return would bea. 0.b. 12%.c. > 12%.d. < 12%. (3371)

44. Which of the following characteristics represent an advantage of the internal rate of return technique over the accounting rate of return technique in evaluating a project?

I Recognition of the project's salvage value.

II Emphasis on cash flows. III Recognition of the time value of

money.

a. I onlyb. I and IIc. II and IIId. I, II, and III (3482)

45. Para Co. is reviewing the following data relating to an energy saving investment proposal:

CostResidual value at the end of 5 yearsPresent value of an annuity of 1 at 12% for 5 years Present value of 1 due in 5 years at 12%

What would be the annual savings needed to make the investment realize a 12% yield?a. $ 8,189b. $11,111c. $12,306d. $13,889 (4643)

QUESTIONS

Net Present value Internal Rate of Returna. Yes Yesb. Yes Noc. No Yesd. No No (2244)

$50,000

10,000

3.60

0.57

○

○

○

○

○

1

ビジネス環境および諸概念

Business Environment & Concepts

解 答

2

Financial Management Ver. GK (e ラーニングの画面に Ver.GA と出ていますが、講義は GK の内容です。) 1. Ans. C

Working Capital=Current assets-Current liability。Choice Aは現金が減り、W/Pも減り、Working capital変化しません。Choice Bも現金が増え、A/Rが減るのでWorking capitalに変化なし。Choice CはCurrent liability が振替で Long-term liability になるので Working capital は増えます。Choice D は Mortgage の

向こう一年分が Current liability になるので、Working Capital は減ります。 2. Ans. C

Working Capital=Current assets-Current liability。Current Ratio =Current assets-Current liabilities。株を発行すると、お金が入ります。WC も CR も両方、増えます。

3. Ans. A

Working Capital=Current assets-Current liability。Choice A では NET で、$130 の Increase。Choice B では NET、$120 の Increase。Choice C では NET、$200 の Decrease。Choice D では NET、$35の Decrease。

4. Ans. D

Current の WC=4000+20000+45000+43000-37000-18000=$57000。Plan の WC=

10000+11000+60000+53000-46000-34000=$54000。今期と計画では$3000 の Decrease。 5. Ans. D

Cash をもつ理由は5つあります。Compensating balance、Speculation、Transaction、Precautionary Measure、Future cash requirements。これらの Key word を含んでいるのは Choice D。

6. Ans. A

現金の回収を早めないのは? Choice B、C、と D は早めます。Choice A は 現金を持つ理由の一

つです。 7. Ans. B

Slowing Down Cash Disbursement は4つあります。その一つが Zero-balance checking account です。 8. Ans. B

Compensating balance とは Compensates a bank for the services it renders to its depositor。例:銀行

からお金を一億借りたけど、預金口座に 3000 万円の残高を Keep しなければいけない。 9. Ans. B

通常、Cash collection には 11 日必要ですが、Lock-box 導入で 6 日に短縮。5 日分 はやく現金を手に

できます。$150000×5 日=$750000。 10. Ans. C

Bond は Long-Term です。現金の代用にはならない。ほかは、Substitute for Cash。特に、U.S T-bill はMost Popular substitute for Cash。

11. Ans. C

Commercial Paper = Does not have an active secondary market。通常、投資家に直接 渡したりしま

すので、流通市場が存在するわけではありません。Choice A は Higher than treasury bills。Not lower。Choice B、CP は Note だけではありません。Choice D、一年未満の CP もあります。

12. Ans. A

FNMA=ファニィメイと発音する=有名な Agency securities の一種。

3

13. Ans. E Most often used as a cash substitute = Treasury bills=Most safest。

14. Ans. E

The least default risk = Treasury bills 。 15. Ans. B

計算は教科書に掲載されています。 16. Ans. C

Not take discount:30%×$50000=$15000。Take discount:70%×$50000×98%=$34300。合計=

$49300。 17. Ans. B

EOQ は 1000units。Lead time は EOQ 計算には関係ない。惑わされないように。 18. Ans. B

Safety stock will tend to decrease if Lead time の変動が少なくなれば。Order してから届くまで、数日

で必ず届くのであれば、Stock はそんなにいらない。逆に、到着日が 2 日目なのか 15 日目なのか、定

かでなければ The stock tend to increase。ほかの Choice は Increase safety stock。 19. Ans. A

EOQ の計算は√の中で分数。どれを Increase すれば EOQ を減らせますか? 分数の分母=Carrying costs。Choice B は EOQ の計算とは無縁。

20. Ans. C

Choice A と B は Ordering costs。Carrying costs = Handling costs。 21. Ans. D

Choice DのOrder costsはEOQ計算。Safety stockとは無縁です。ほかのChoiceは Increase safety stock level。

22. Ans. D

Cost of Not taking discount 方程式=(Discount %÷(100%-Discount %))×(360÷(Full days-Discount period)。(2%÷98%)×(360÷(30days-10days))=36.73%

23. Ans. B

方程式=(Discount %÷(100%-Discount %))×(360÷(Full days-Discount period)。(2%÷98%)

×(360÷(45days-15days))=24.49% 24. Ans. C

Cash discount を実施する理由は=競争相手が実施している・現金を早く回収したい。ほかの Choiceは関係ない。

25. Ans. D

方程式=(Cost of Borrowing÷Cash Proceeds)×(360 日÷Term)。この問題では、Costs of Borrowingは先に取られた金利分$10000 と Transaction costs$1000 の合計$11000。(11000÷489000)×(360÷90 日)=9%。

26. Ans. B

方程式=(Cost of Borrowing÷Cash Proceeds)×(360 日÷Term)。Costs of Borrowing=400000×8%=32000。$400000 から Compensating balance を引いた金額が Cash proceeds。(32000÷350000)×(360÷360)=9.1%。

4

27. Ans. B 方程式=(Cost of Borrowing÷Cash Proceeds)×(360 日÷Term)。Costs of Borrowing=($600000×8%)-($10000×3%)=$47700、通常の、Compensating balance より$10000 残高を多くします

ので、これには3%の受取利息がつきます。Cash proceeds は$10000 引いた、$590000 です。通常の、

Compensating balance の$50000 はすでに積んであります。(47700/590000)×(360/360)=8.08%。 28. Ans. C

会社がお金を借りて、Discount を使用して支払うのであれば、いくら借りるべきなのか? しかも、

お金を借りた場合、Compensating Balance は借りた金額の8%分 Keep しなくてはいけません。まず、

Discount を使用するのであれば、業者に払う金額は$49000。Loan を X とした場合、X=$49000+0.08Xになります。これで X を求めると 0.92X=$49000。X=$53261 になります。

29. Ans. B

方程式=(Cost of Borrowing÷Cash Proceeds)×(360 日÷Term)。28 番で Loan=$53261 と求めま

した。Costs of Borrowing=53261×10%×(20/360)=$295.89。Cash proceeds は$53261 ではあり

ません。$49000 です。なぜなら、Compensating balance で Loan の 8%分預金しなくてはいけないか

らです。(295.89/49000)×(360/20)=10.87% 30. Ans. B

方程式=(Discount %÷(100%-Discount %))×(360÷(Full days-Discount period)。(2%÷98%)

×(360÷(30-10))=36.73% 31. Ans. B

Account $200000 から、5%Reserve($10000)と 1.5%Commision($3000)を引くと=$187000。さ

らに、ここから、12%×187000=5610 を引いて、$181390 になります。 32. Ans. C

Degree of operating leverage = Contribution margin÷EBIT。 CM=200000 個×($2-$0.60)=

$280000。 EBIT=$280000-$70000=$210000。DOL=280000/210000=1.33 33. Ans. C

DFL=EBIT÷(EBIT-利息-(優先株配当÷(1-Tax rate))。 問題には優先株配当の記載なし。DFL=210000/(210000-60000)=1.4。

34. Ans. A

方程式=配当÷(Net issue price+Growth rate)。 配当は$6。 Net issue price=$100-Discount $5-Flotation Costs$4=$91。Growth rate の記載なし。6÷91=6.59%

35. Ans. A

方程式=配当÷(Current stock price+Growth rate)。6÷100=6% 36. Ans. A

方程式=Bond の利息×(1-Tax rate)。 問題文には、すでに計算されて 初の Section の終りに The cost of funds is 4.8%と記載。

37. Ans. C

方程式=優先株の配当÷優先株の Issue price。 優先株の配当は$90×9%=$8.10。8.10÷90=9% 38. Ans. B

資金調達の割合は問題文に掲載されていました。一連の回答で、各 Costs of funds の%は求めました。

LT-Debt=4.8%(36 番の問題)、PS=9%(37 番の問題)、RE=6%(35 番の問題)、New issue=6.59%(34 番の問題)。問題文では RE の$100000 を使用してから、足りない分を New issue で補うと記述。

つまり、$500000 のうち、Common stock の割り当ては 50%($250000)ですが、RE の$100000 を

考慮します。教科書の解答を参照。

5

39. Ans. C この問題では調達額が$1,000,000 になりますが、同じ解説です。教科書参照。

40. Ans. C

Present value factor=Cost of equipment÷Cash flow per year。$100000÷$20000=5 41. Ans. B

NPV では Minimum required rate of return で Reinvested。しかし、IRR では Reinvested at the Project の rate of return。Not required rate of return。

42. Ans. D

NPV の計算では Salvage value も現在価値で計算に組込みます。 43. Ans. C

NPV が Positive であれば、12%以上の利回り。IRR も同じように 12%以上です。 44. Ans. C

IRR の Advantages over ARR。 I の Salvage value は両方関係ない。II の Cash flow は IRR で使用。ARRでは Accrual の金額を使用。NOT Cash flow。III の Time value of money は IRR で使用。ARR は使用

しない。 45. Ans. C

CNPV が Zero になれば Just 12% yield。Cost は$50000 ですが Residual value が$10000 あります。

Residual value の現在価値は 10000×0.57=5700。Cost of investment は$50000-$5700=$44300。$44300 -(Future cash flow×PV factor)=0。PV factor は 3.60。Future cash flow=Annual savings needed=44300÷3.6=12306。