FINANCIAL STATEMENTS INDEPENDENT AUDITOR'S … · financial statements and independent auditor's...

29

FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT TOWN OF WHEATLAND, WISCONSIN December 31, 2014

Transcript of FINANCIAL STATEMENTS INDEPENDENT AUDITOR'S … · financial statements and independent auditor's...

FINANCIAL STATEMENTS AND

INDEPENDENT AUDITOR'S REPORT

TOWN OF WHEATLAND, WISCONSIN

December 31, 2014

T A B L E 0 F C 0 N T E N T S

INDEPENDENT AUDITOR'S REPORT

BASIC FINANCIAL STATEMENTS

STATEMENT OF NET POSITION - MODIFIED CASH BASIS

STATEMENT OF ACTIVITIES - MODIFIED CASH BASIS

STATEMENT OF ASSETS AND FUND BALANCE - MODIFIED CASH BASIS GOVERNMENTAL FUNDS

STATEMENT OF CASH RECEIPTS, CASH DISBURSEMENTS, AND CHANGES IN FUND BALANCE - MODIFIED CASH BASIS -GOVERNMENTAL FUNDS

STATEMENT OF ASSETS AND LIABILITIES - MODIFIED CASH BASIS -FIDUCIARY FUNDS - PROPERTY TAX AGENCY FUND

NOTES TO FINANCIAL STATEMENTS

SUPPLEMENTAL INFORMATION

'i

STATEMENT OF CASH RECEIPTS, CASH DISBURSEMENTS, AND CHANGES IN FUND BALANCE - MODIFIED CASH BASIS BUDGET AND ACTUAL - GENERAL FUND

. .. . .·,

STATEMENT OF CASH RECEIPTS, CASH DISBURSEMENTS, AND CHANGES IN FUND BALANCE- MODIFIED CAsH BASIS BUDGET AND ACTUAL - FIRE DEPARTMENT FUND

OTHER REPORTS

INDEPENDENT AUDITOR'S REPORT ON· COMPLIANCE AND ON INTERNAL CONTROL OVER FINANCIAL REPORTING BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

SCHEDULE OF FINDINGS AND RESPONSES

Page

3

7

8

9

10

11

12

23

25

27

29

-ITO~RUD ""~ ___ ---~~ ~~:!~

Your Business Safety Net

Town Board Town of Wheatland De Soto, Wisconsin

INDEPENDENT AUDITOR'S REPORT

Report on the Financial Statements

609 S. 4th S tree1,. Suite B La'(rosse, WI 54601

Phone: 608·784·8060 Fax: 608~784·8167

We have audited the accompanying financial statements of the governmental· activities, each major fund, and the aggregate remaining fund information of the Town of Wheatland, Wisconsin as of and for the year ended December 31, 2014, and the. related notes to the financial statements, which collectively comprise. the Town's. basic financial statements as listed in the table of contents.

M.anagement's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financialstatements in accordance with the modified cash basis of accounting described. in Note A; this includes determining that the modified cash basis of accounting is an acceptable basis for the preparation of . ·the. financial statements in the circumstances. Management is also responsible· for the design, implementation, . and maintenance of internal controls relevant. to the . prep~ration and fair presentation of financial statements ·_that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express op1n1ons on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the . standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An ~udit involves pe~forming procedures to obtain. audit. evidence about th,e ·amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, . the auditor considers internal controls relevant to the Town's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate

-3-

in the circumstances, but not for purpose of expressing an opinion on the effectiveness of the Town's internal controls. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund information of the Town of Wheatland, Wisconsin, as of December 31, 2014, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Basis of Accounting

We draw attention to Note A of the financial statements, which describes the basis of accounting. The financial statements are prepared on the modified. cash basis of accounting, which is a basis of accounting other than accounting principles generally accepted in the United States of America. Our opinion is not modified with respect to this matter.

Other Matters

Required Supplementary Information

Management has omitted the management's discussion and analysis that is required to be presented to supplement the basic financial statements. ·such missing information, although not a part of the basic financial statements~ ·is required by the Governmental . Accounting Standards Board, who considers · it· to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context • Our· opinion on the. bai;:iC. financial statements· is not affected by. this missing information. · · .

The budgetary· comparison information on pages 23 through 25 is presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the· Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in. an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information oin accordance with auditing standards generally accepted in the United States of America, which· cons.isted of .. inquiries. of management about the methods . of .

·preparing the information and comparing the information for consistency with management's responses to our inquiries, ·the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

-4-

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated November 5, 2015, on our consideration of the Town's internal

·control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Town's internal control over financial reporting and compliance.

IY":- /::- - ~ c::::_ #~ r)-~?{252- •

November 5, 2015

-5-

BASIC FINANCIAL STATEMENTS

-6-

Town of Wheatland, Wisconsin STATEMENT OF NET POSITION - MODIFIED CASH BASIS

December 31, 2014

Governmental Activities Total

ASSETS Cash and investments $ 97,983 $ 97,983

Total assets $ 97,983 $ 97,983

LIABILITIES Payroll liabilities $ 2,537 $ 2,537

Total liabilities 2,537 2,537

NET POSITION Restricted

Special revenue funds 16,839 16,839 Unrestricted

Board designated-seal coat 18,003 18,003 Other unrestricted 60,604 60,604

78,607 78,607

Total net position 95,446 95,446

Total liabilities and net position $ 97,983 $ 97,983

The accompanying notes are an integral part of this statement.

-7-

Town of Wheatland, Wisconsin STATEMENT OF ACTIVITIES - MODIFIED CASH BASIS

For the year ended December 31, 2014

Functions/Programs

Governmental activities Current

General government Public safety Public works Health and human services Capital outlay Debt service

Total governmental activities

Total municipality

$

Expenses

85,186 23,837

268,269 225

14,890 95,987

488,394

Charges for Services

$ 27,038

487 137

27,662

Program Revenues Operating Grants and

Contributions

$

$===4=8=8='=3=9=4 = $====2=7='=6=6=2= $============= General revenues

Taxes Property taxes, levied for general purposes Mobile home fees Managed forest taxes

Grants and contributions not restricted to specific programs

Shared revenues Other

Licenses Interest and investment earnings Miscellaneous

Total general receipts

Change in net position

Net position at January 1

Net position at December 31

The accompanying notes are an integral part of this statement.

-8-

Capital Grants and

Contributions

Net (Expense) Revenue and Changes in Net Position

Governmental Activities

259,514 2,645 4,764

18,522 6,783 1,010 1,323

14,571 309,132

33,594

61,852

$ 95,446

Total

259,514 2,645 4,764

18,522 6,783 1,010 1,323

14,571 309,132

33,594

61,852

$ 95[446

Town of Wheatland, Wisconsin STATEMENT OF ASSETS AND FUND BALANCE - MODIFIED CASH BASIS

GOVERNMENTAL FUNDS December 31, 2014

Assets Cash and cash equivalents

Total assets

Liabilities Current liabilities

Payroll liabilities

Total liabilities

Fund balance Restricted - fire department Unrestricted

Committed - seal coat Unassigned

Total liabilities and fund balance

General Fund

$ __ 8_1__:..., 1_4_4_

$==8=1='=1=44==

$ 2,537 ---'----2,537

18,003 60,604 78,607

$==8=1='=1=4=4==

Fire Department

$ __ 1_6__:,_, 8_3_9_

$==1=6='=8=3=9=

$ ___ _

16,839

16,839

$==1=6='=8=3 9==

The accompanying notes are an in~egral part of this statement.

-9-

Total

$ __ 9_7..:.., _9_83_

$==9=7='=9=8=3=

$ 2, 537 _ _ __,__ __ 2,537

16,839

18,003 60,604 95,446

$==9=7='=9=83==

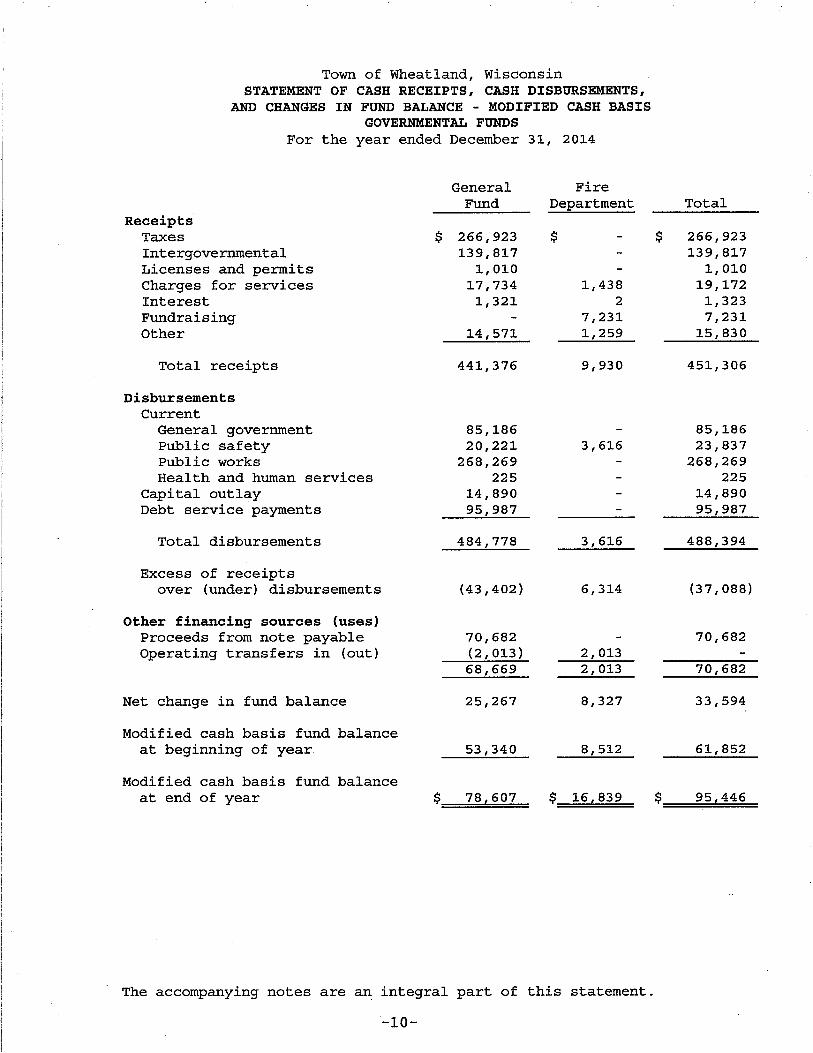

Town of Wheatland, Wisconsin STATEMENT OF CASH RECEIPTS, CASH DISBURSEMENTS,

AND CHANGES IN FUND BALANCE - MODIFIED CASH BASIS GOVERNMENTAL FUNDS

For the year ended December 31, 2014

Receipts Taxes Intergovernmental Licenses and permits Charges for services Interest Fundraising Other

Total receipts

Disbursements Current

General government Public safety Public works Health and human services

Capital outlay Debt service payments

Total disbursements

Excess of receipts over (under) disbursements

Other financing sources (uses) Proceeds from note payable Operating transfers in (out)

Net change in fund balance

Modified cash basis fund balance at beginning of year

Modified cash basis fund balance at end of year

General Fund

$ 266,923 139,817

1,010 17,734

1,321

14,571

441,376

85,186 20,221

268,269 225

14,890 95,987

484,778

(43,402)

70,682 (2,013) 68,669

25,267

53,340

$·==7=8~,.;;;,6::0::::7 =

Fire Department

$

1,438 2

7,231 1,259

9,930

3,616

3,616

6,314

2,013 2,013

8,327

8,512

$ 16,839

The accompanying notes are an integral part of this statement.

-10-

$

Total

266,923 139,817

1,010 19,172

1,323 7,231

15,830

451,306

85,186 23,837

268,269 225

14,890 95,987

488,394

(37,088)

70,682

70,682

33,594

61,852

$====9=5='=4=4=6 =

Assets

Town of Wheatland, Wisconsin STATEMENT OF ASSETS AND LIABILITIES - MODIFIED CASH BASIS

FIDUCIARY FUNDS - PROPERTY TAX AGENCY FUND December 31, 2014

Cash and investments $ ==3=9=7='=9=74==

Liabilities Unearned revenue - property taxes Due to other governments

Total liabilities

The accompanying notes are an integral part of this statement.

-11-

$ 77,814 320,160

$ ==3=9=7='=9=74==

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS

December 31, 2014

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accounting policies of the Town of Wheatland, Wisconsin conform to the modified cash basis of accounting consistent with its annual report filing with the State of Wisconsin, which is a basis of accounting other than accounting principles generally accepted in the United States of America. The following is a summary of the more significant policies.

l. Reporting Entity

The Town operates under a Town Board form of government and can the following services as authorized by its charter: public highways and streets, sanitation, health and social services, and recreation, public improvements, planning and zoning, and administrative services.

provide safety, culture general

This report includes all of the funds of the Town of Wheatland. The reporting entity for the Town is based upon criteria established by the Governmental Accounting Standards Board (GASB) Statement No. 14, "The Financial Reporting Entity." All functions of the Town for which it exercises oversight responsibility are included. The oversight responsibility includes, but is not limited to, financial interdependency, selection of governing authority, designation of management, ability to significantly influence operations and accountability for fiscal matters.

2. Component Units

The Town uses the modified cash basis of accounting, which is consistent with its annual report filing with the State of Wisconsin. The modified cash basis of accounting is a basis of accounting other than accounting principles generally accepted in the United States of America, and requires that these financial statements include the primary government and its component units. Component units are separate organizations that are included in the Town's reporting entity because of the significance of their operational or financial relationships with the Town. All significant activities and organizations with which the Town exercises oversight responsibility have been considered for inclusion in the financial statements. The Town has no component units, and it is not included in any other governmental reporting entity.

3. Basis of Presentation

Government-wide Statements The statement of net position and the statement of activities present financial information about the Town's governmental and business-type activities (if any) . These statements include the financial activities of the overall government in its entirety, except those that are fiduciary. Eliminations have been made to minimize the double counting of internal transactions. These statements distinguish between the governmental and business-type activities (if any) of the Town. Governmental activities generally are', financed through taxes, intergovernmental revenues, and other nonexchange transactions. Business-type activities are financed, at least in part, by fees charged to external parties. The Town has no business-type activities.

-12-

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - CONTINUED

3. Basis of Presentation - Continued

Government-wide Statements - Continued

The statement of. activities presents a comparison between direct expenses and program revenues for business-type activities (if applicable) and for each function of the Town's governmental activities. Direct expenses are those that are specifically associated with and are clearly identifiable to a particular function. Program revenues include (a) charges paid by the recipients of goods or services offered by the programs and·· (b) grants and contributions that are restricted to meeting the operational or capital requirements of a particular program. Revenues that are not classified as program revenues, including all taxes, are presented as general revenues.

Fund Financial Statements - The fund statements provide information about the Town's funds, including its fiduciary fund. Separate statements for. each fund category -- governmental and fiduciary ~

are presented. The emphasis of fund financial statements.is on major governmental and enterprise funds (if applicable), each displayed in

. a separate column. All. remaining governmental and enterprise funds are aggregated and reported as non-major funds. ·

The Town does riot operate any proprietary or enterprise funds.

The Town reports the ·following major governmental funds:

General Fund - The General Fund is the operating fUnd of the . Town. It is used to account for all financial resources except · those that are required to be accounted for in other · frinds ~ ..

.. ·.Fire Department .Fund - . The Fire Department ·Fund. is.· a .. special ·. r.even~e fUJ;ld used to account. for .all . of . the. fire department'~ financial assets and activity.

Fiduciary Funds. - Fiduciary Funds account for assets held by the Town in a trustee capacity or as an agent on behalf of others. The Town operates the following fiduciary fund:

Property Tax Agency Fund- Agency Funds are used to account. for assets held by the Town as an agent for individuals, private organizations, other governments, and/or other funds. Agency ·Funds are custodial in nature and do not involve measurement of results of operations. Property tax collections are shown in ali

··.agency ftind since they are collected. for use by· the Town ·and ~other governmental· entities in the subsequent fiscal year. The assets of this fund are excluded from the government-wide . financial st.atements because the Town cannot use these assets to finance its operations·.

-13-

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - CONTINUED

4. Basis of Accounting

Basis of accounting refers to when revenues and expenditures or expenses are recognized in the accounts and reported in the financial statements. Basis of accounting relates to the timing of . the measurement made, regardless of the measurement focus applied.

All governmental funds are accounted for using the modified cash basis of accounting, which is a basis of accounting other than accounting principles generally accepted in the United States of America. Revenues are recognized when cash is collected and available. Taxpayer-assessed income, gross receipts, and sales taxes are considered "measurable" when in the hands of intermediary collecting governments and are recognized as revenue at that time. All revenues such as fees, fines, licenses, permits, public charges, etc., are recorded on the modified cash basis.

Expenditures are generally recognized under the modified cash basis of accounting when the related cash is expended. Supplies are expensed when purchased and are not inventoried.

5. Use of Estimates

The preparation of financial statements in conformity with the modified cash basis of accounting, which is a comprehensive basis of accounting other than accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported period. Actual results could differ from those estimates or assumptions.

6. Budgets and Budgetary Accounting

The Town follows these procedures in establishing the budgetary data reflected in the financial statements:

a. The Town Board develops a proposed operating budget for the_ fiscal year commencing the following January 1. The operating budget includes proposed expenditures and the means of financing them.

b. A public hearing is conducted in the Town Hall to obtain taxpayer comments.

c. Prior to December 1, the budget is legally enacted through passage of a resolution.

d. Any transfers of budget amounts between departments or revisions that alter total expenditures must be approved by the Town Board.

e. Budgets are adopted on a modified consistent with accounting principles United States of America (U.S. GAAP).

-14-

cash basis, which generally accepted

is in

not the

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - CONTINUED

6. Budgets and Budgetary Accounting - Continued

f. Budgetary expenditure control is exercised at the function level ·(i.e., general government, public safety, etc.)

g. Budgeted amounts are as authorized in the original budget resolution and include any subsequent revisions as authorized by the Town Board.

h. Appropriations lapse at year-end.

7. Compensated Absences

Employee benefits for compensated absences do not vest or accumulate and therefore, are not recorded on these statements.

8. Net Position Designations

The Town classifies its net position as follows:

a. Restricted net position .indicates that portion of net position that has been legally segregated for specific purposes.

b. Unrestricted net position indicates that portion of net position for which the Town. has no legal financial obligation.

9. Fund Balance Classifications

The Town classifies .its fund balance as follows:

a. Unrestricted, unassigned fund balance is the residual classification fOr the general fund and includes all amounts not contained in the other classifications.

b. Unrestricted, as:signed fund balances include amounts that cari be spent only for . spe'cific . purposes stipulated by representatives designated by the '.Town Boa-rd. '

c. Unrestricted, committed fund balances include amounts that can be spent only for specific purposes approved by the Town Board.

d. Restricted fund balances include amounts that can be spent only for the specific purposes stipulated by external resource providers (for example, grant _providers), constitutionally, or through enabling legislation (that is, legislation that creates a new revenue source and restricts its use) .

Restricted fund balance classifications followed by unrestricted amounts ·when incurred.

10. State Aids

are considered spent first a • quali!ying . expenditure . is .

State general and categorical aids are recognized as revenue when received.

-15-

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE B - CASH AND INVESTMENTS

Cash and investments as of December 31, 2014, are classified in the accompanying financial statements as follows:

Statement of net position

Governmental activities Fiduciary Fund

Cash and investments as of December 31,

Demand deposits Savings and money market

$

$

2014

$

$

97,983 397,974 495,957

consist of

Carrying Amount 449,990

45,967 495,957

Investments Authorized by the Town•s Investment Policy

the following:

Bank Balance

$ 460,664 45,966

$ 506,630

The Town is required to invest its funds in accordance with Wisconsin Statute 66.0603 and 67.11(2). The Town does not have an investment policy with any specific provisions intended to limit exposure to investment rate risk, credit risk and concentration of credit risk.

Disclosures Relating to Interest Rate Risk

Interest rate risk is the risk that changes in market interest rates will adversely affect the fair value of an investment. Generally, the longer the maturity of an investment the greater the sensitivity of its fair value to changes in market interest rates. As of year-end, the Town had no investments except savings and money market accounts.

Disclosures Relating to Credit Risk

Generally, credit risk is the risk that an issuer of an investment will not fulfill its obligation to the holder of the investment. This is measured by the assignment of a rating by a nationally recognized statistical rating organization.

Concentration of Credit Risk

Concentration of credit risk is defined as an exposure to a number of counterparties engaged in similar activities and having similar economic characteristics that would cause their ability to meet contractual obligations to be similarly affected by changes in economic or other conditions. The Town does not have an investment policy regarding concentration of credit risk.

-16-

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE B - CASH AND INVESTMENTS - CONTINUED

Custodial Credit Risk

Custodial credit risk for deposits is the risk that, in the event of the failure of a depository financial institution, a government will not be able

· to recover collateral securities that are in the possession of an outside party. The Town does not have an investment policy that would limit the exposure to custodial credit risk for deposits. The Wisconsin State Deposit Guarantee Fund provides coverage for uninsured and uncollateralized cash and investments for up to $400,000 per deposito:i:y, in excess of FDIC coverage, but collection is not certain due to the limited size of the fund.

At December 31, 2014, the Town had no deposits with financial institutions in excess of federal depository insurance limits. There may have been times during 2014 that deposits exceeded FDIC limits and the Town was relying on the Wisconsin State Deposit Guarantee Fund to insure its deposits or there may have been times when the Town had deposits greater than both FDIC and the Wisconsin State Deposit Guarantee Fund limits.

The custodial risk for investments is the risk that, in the event of the failure of the counterparty (e.g., broker-dealer) to a transaction, a government will not be . able to recover the value of its investment or collateral securities· that are in the possession.of another party. The Town does not have an investment policy tha:t would limit the exposure to custodial credit risk for investments. With respect to investments, custodial credit risk generally applies only to direct investments in marketable securities. Custodial credit risk does hot apply to a local government's indirect investment in securitie~ through the use of mutual ·funds or government investment pools .

.. NOTE C - PROPERTY TAXES

Property· :taxes attach ·as an enforceable·· lien: on property as ·of· .January· 1. Property taxes are levied on or about December 1 and payable in .two installments on January 31 and July .31 the following calendar year. Special assessments and charges are payable in full on January 31.

The Town bills and collects its own property taxes. and also collects taxes for the State, County, Area Vocational School, and Area Public Schools until January 31, at which time all uncollected real estate taxes are turned over to the respective counties for. collectiop.. Collection of the taxes and remittance of them to the appropriate. entities are accounted ·for in the Property Tax Agency Fund. Town property ta.X revenues are recognized when settlements are made with the County Treasurer;

The 2014 tax roll that has been collected prior to December 31, 2014 has been set up as amounts due to other governmental linits and as unearned revenue for the Town's portion in the Property Tax. Agency Fiduciary Fund.

-17-

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE D - LONG-TERM OBLIGATIONS

Long-term obligations of the Town at December 31, 2014 consist of the following:

· Balance at Balance .at January 1, December 31,

2014 Additions Payments 2014

Note payable $ 92,435 $ 70,682 $ 92,435 $ 70L682

Current Rate Amount Maturities

Governmental activities Bank note payable 2.25% $ 70,682 $ 23,038

$ 70L682 $ 23L038

The 2014 equalized valuation of the Town as certified by the Wisconsin Department of Revenue is $56,843,500. The legal debt limit and margin of indebtedness as of December 31, 2014, in accordancewithWisconsin State St§itutes, is as follows:

··Debt limit {5% of $56,843,500) Deduct long-term debt applicable · .to debt margin

Margin of indebtedness

. .

$ 2,842,175

70,682

$ 2L771L49J·

Aggregatecash flow.requirenients for the retirement oflong-te):m ·J>r1ncipal.and interest on the note payable is as followsi

~overnmental Activities.

Year ended December 31, 2015

Principal Interest Total 23,038 1,607 ~4,645

20-16 23,562 1,083 24,645 2017 24,082 547 24.,629

.Totals $ 70L682 $ 3L237 $ 73L919

-18-

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE E - EMPLOYEE RETIREMENT PLAN

All eligible Town employees participate in the Wisconsin Retirement System (WRS), a cost-sharing, multiple-employer, defined benefit, public employee retirement system. All employees, initially employed by a participating WRS employer prior to July 1, 2011, expected to work at least 600 hours a year (440 hours for teachers and school district educational support employees) and expected to be employed for at least one year from employee's date of hire are eligible to participate in the WRS. All employees, initially employed by a participating WRS employer on or after July 1, 2011, and expected to work at least 1200 hours a year (880 hours for teachers and school district educational support employees) and expected to be employed for at least one year from employee's date of hire are eligible to participate in the WRS. Note: Employees hired to work nine or ten months per year, (e.g. teachers contracts), but expected to return year after year are considered to have met the one-year requirement.

Effective the first day of the first pay period on or after June 29, 2011 the employee required contribution was changed to one-half of the actuarially determined contribution rate for general category employees, including teachers, and executives , and elected officials. Required contributions for protective contributions are the same rate as general employees. Employers are required to contribute the remainder of the actuarially determined contribution rate. The employer may not pay the employee required contribution unless provided for by an existing collective bargaining agreement. Contribution rates for 2014 are:

General (including teachers) Executives & Elected Officials Protective with Social Security Protective without Social Security

Employee 7.00% 7.75%

10.10% 13.70%

Employer 7.00% 7.75% 7.00% 7.00%

The payroll for Town employees covered by the WRS for the year ended December 31, 2014 was $48,709. The employer's total payroll was $121,234. The total required contribution for the year ended December 31, 2014 was $6, 819, which consisted of $3,410, or 7. 00% of payroll from the employer and $3,409, or 7.00% of payroll from employees. Total contributions for the years ending December 31, 2013 and 2012 were $7,127 and . $0, respectively, equal to the required contributions for each year.

Employees who retire at or after age 65 (62 for elected officials and 54 for protective occupation employees with less than 25 years of service, 53 for protective occupation employees with more than 25 years of service) are entitled to receive a retirement benefit. Employees may retire at age 55 (50 for protective occupation employees) and receive actuarially reduced benefits. The factors influencing the benefit are: (1) final average earnings, (2) years of creditable service, and (3) a formula factor. Final average earnings are the average of the employee's three highest years' earnings. Employees terminating covered employment before becoming eligible for a retirement benefit may withdraw their contributions and, by

-19-

I

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE E - EMPLOYEE RETIREMENT PLAN - CONTINUED

doing so, forfeit all rights to any subsequent benefit. For employees beginning participation on or after January 1, 1990, and no longer actively employed on or after April 24, 1998, creditable service in each of five years is required for eligibility for a retirement annuity. Participants employed prior to 1990 and on or after April 24, 1998 and prior to July 1, 2011 are immediately vested. Participants who initially became WRS eligible on or after July 1, 2011 must have five years of credible service to be vested.

The WRS also provide~ death and disability benefits for employees. Eligibility and the amount of all benefits are determined under Chapter 40 of the Wisconsin Statutes. The WRS issues an annual financial report that may be obtained by writing to the Department of Employee Trust Funds, P.O. Box 7931, Madison, WI 53707-7931.

NOTE F - EXCESS OF ACTUAL EXPENDITURES. OVER BUDGET

The following line items had an excess of actual expenditures over budget for the year ended December 31, 2014.

Individual Fund and Department

General fund General government Public works Debt service. , ., Transfer to other funds

Fire department fund Fire protection ·

NOTE G - OTHER POST-EMPLOYMENT BENEFITS

Excess Expenditure

$ 8,027 10,328 70,682

8,013

3,616

The Town offers no material post-employment benefits to employees upon separation from service. Employees receive no payments at or after separation from service. The only post-employment benefit an employee may receive is COBRA continuation of their health insurance, for which the separated employee must pay 100% of their premium.

-20-

Town of Wheatland, Wisconsin NOTES TO FINANCIAL STATEMENTS - CONTINUED

December 31, 2014

NOTE H - RISK MANAGEMENT

The Town is exposed to various risks of loss related to torts; theft; damage to and destruction of assets; errors and omissions; injuries to employees; and natural disasters. These risks are covered by the purchase of commercial insurance. Settled claims from these risks have not exceeded commercial insurance coverage in any of the past three fiscal years.

NOTE I - SUBSEQUENT EVENTS

The Town has evaluated subsequent events through November 5, 2015, the date on which the financial statements were available to be issued.

-21-

SUPPLEMENTAL INFORMATION

-22-

Town of Wheatland, Wisconsin STATEMENT OF CASH RECEIPTS, CASH DISBURSEMENTS,

AND CHANGES IN FUND BALANCE - MODIFIED CASH BASIS BUDGET AND ACTUAL

GENERAL FUND For the year ended December 31, 2014

Budgeted Amounts Original Final

Receipts Taxes

General property taxes Mobile home taxes Managed forest taxes

$ 2641 583 $ 266, 117

Intergovernmental Federal

FEMA grant State of Wisconsin

FEMA grant Shared revenues Fire insurance tax Highway aid Highway grant-TRIP Exempt computer aid DNR aid in lieu of taxes DNR forest crop

County Bridge aid

Licenses and permits Business and occupational Building permits Nonbusiness licenses

and permits

Charges for services Fire services contract Public safety other Public health &

animal control Recycling

Other receipts Interest Sale of material supplies Miscellaneous

Total receipts

1,700 2,150

266,283

18,504 3,000

86,649 61,015

3 5,041 1,000

175,212

760 300

300 1,360

17,000

17,000

1,500

5,250 6,750

466,605

-23-

268,267

20,850

3,476 18,504

3,450 86,649

9

5,041 1,000

138,979

640 200

145 985

17,000

17,000

1,325

11,250 12,575

437,806

Actual

$ 259,514 2,645 4,764

266,923

20,850

3,476 18,522

2,013 86,649

9 6,172

602

1,524 139,817

640 75

295 1,010

17,000 110

137 487

17,734

1,321 14,000

571 15,892

441,376

Variance with

Final Budget Favorable

(Unfavorable)

$ (6,603) 495

4,764 (1,344)

18 (1,437)

1,131 (398)

1,524 838

(125)

150 25

110

137 487 734

( 4)

14,000 (10,679)

3,317

3,570

Town of Wheatland, Wisconsin STATEMENT OF CASH RECEIPTS, CASH DISBURSEMENTS,

AND CHANGES IN FUND BALANCE - MODIFIED CASH BASIS BUDGET AND ACTUAL

GENERAL FUND - CONTINUED For the year ended December 31, 2014

Disbursements General government

Town Board $ Legal General administration Financial administration General buildings and plant Insurance

Public safety Fire protection

Public works Highway and street

maintenance Rubbish services Recycling

Health and human services

Culture and recreation

Capital outlay General government Public works - buildings Public works - equipment Public works - roads

Debt service Principal payments Interest expense

Total disbursements

Excess receipts over {under) disbursements

Other financing sources (uses) Proceeds from note payable Transfer {to) from other

funds

Net increase {decrease) in fund balance

Modified cash basis fund balance at January 1

Budgeted Amounts Original

12,414 $ 5,000

14,677 19,272 10,000

8,597 69,960

40,500 40,500

305,557 15,500

900 321,957

375

500

16,008 50,000

18,000 84,008

21,753 3,552

25,305

542,605

{76,000)

6,000 6,000

{70,000)

53,340

Final

14,775 $ 14,000 16,082 19,577

6,000 6,725

77,159

32,100 32,100

241,441 16,000

500 257,941

225

500

47,376 50,000

5,200 18,000

120,576

21,753 3,552

25,305

513,806

{76,000)

6,000 6,000

{70,000)

53,340

Modified cash basis fund balance at December 31 $ {16,660) $ {16,660) $

-24-

Actual

Variance with

Final Budget Favorable

{Unfavorable)

16,956 $ 13,316 19,949 16,866

{2,181) 684

{3,867) 2,711 1,406

{6,780) 4,594

13,505 85,186

20,221 20,221

251,420 16,331

518 268,269

225

14,890

14,890

92,435 3,552

95,987

484,778

{43,402)

70,682

{2,013) 68,669

25,267

53,340

{8, 027)

11,879 11,879

{9,979) {331)

{18) {10,328)

500

47,376 50,000 {9,690) 18,000

105,686

{70,682)

{70,682)

291 028

32,598

70,682

{8,013) 62,669

95,267

78,607 $====9=5=,=2=6=7=

Town of Wheatland, Wisconsin STATEMENT OF CASH RECEIPTS, CASH DISBURSEMENTS,

AND CHANGES IN FUND BALANCE - MODIFIED CASH BASIS BUDGET AND ACTUAL

FIRE DEPARTMENT FUND For the year ended December 31, 2014

Receipts Charges for services

Fire services contract

Other receipts Interest Fundraising Miscellaneous

Total receipts

Disbursements Public safety

Fire protection

Total disbursements

Excess receipts over (under) disbursements

Other financing sources Transfer from general fund

Net change in fund balance

Modified cash basis fund balance at January 1

Modified cash basis fund balance at December 31

Budgeted Amounts Original Final

$ ___ _ $ ___ _

8,512 8,512

$==8=, =5=12== $ 8, 512

Actual

$ 1,438 ---=------1,438

2 7,231 1,259 8,492

9,930

3,616 3,616

3,616

6,314

2,013 2,013

8,327

8,512

$ 16,839

Note: No budgets are formally adopted for the fire department.

-25-

Variance with

Final Budget Favorable

(Unfavorable)

$ 1,438 __......:...... __ _ 1,438

2 7,231 1,259 8,492

9,930

(3,616} (3,616)

(3,616)

6,314

2, 013 2, 013

8,327

$==8='=3=2=7=

OTHER REPORTS

-26-

Cfltified P:ublk A<<OUDtGDff

Your Business Solely Net

INDEPENDENT AUDITOR'S REPORT ON COMPLIANCE AND ON INTERNAL CONTROL

609 S. 4th Street, Suite 8 La Crosse, WI 5460 1

Phon~:. 608-784-8060 Fax:608-784•8167

OVER FINANCIAL REPORTING BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH

GOVERNMENT AUDITING STANDARDS

Town Board Town of Wheatland De Soto, Wisconsin

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial ··audits contained iri Government Auditing Standards, issued by the Comptroller General of the United States, the financial statements of the governmental activities; ·the aggreg~te discretely presented component units, each major fund, and.· the aggregate remaining fund information of the Town of Wheatland, Wisconsin, as of and for the year ended December 31, 2014, and the related notes to the financial statements, which collectively comprise the Town of Wheatland's basic financial statements, and have issued our report thereon dated November 5, 2015.

Internal Control Over Financial Reportin~

In planning and. performing·. OU;J::" audit of the financial . statements I .we considered the Town's internal control over financial reporting (internal controi) to determine the audit procedures that. are appropriate in the·. circumstances, for the pu~ose of expressing our .opJ.nJ.ons on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Town's internal control. Accordingly, we do not express an opinion on the effectiveness of the Town's internal control.

A deficiency in internal control exi.sts when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions,. to prevent, or detect and correct, misstatements on a timely basis~ A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable. possibility. that ·a. material ·misstatement of the Tow's financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

-27-

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies and therefore, material weaknesses or significant deficiencies may exist that were not identified. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. We did identify a certain deficiency in internal control, described as item 2014-1 in the accompanying schedule of findings and responses that we consider to be a significant deficiency.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Town's financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on.· compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Town of Wheatland's Response to Findings

The Town's response to the finding identified in our audit is described in the accompanying schedule of findings c:md • ·responses. The Town' s response was not subjected to the auditing procedures applied in the audit of the financial statements and, accordingly, weexpress no opinion on it .

. Purpose o.f this Report

The purpose of this report is solely to describe the. scope of our testing of internal control and compliance and the result;s of that testing, arid not. to provide an opinion on the effectiveness of the Town's . internal

. ·control. or on compliance. This report is an· :i:nte_gral .. part ·of an ·audit . ·.·performed in accordance with . Governinent · Auditing $taridards . in· considering

the Town's internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Nove~er 5, 2015

-28-

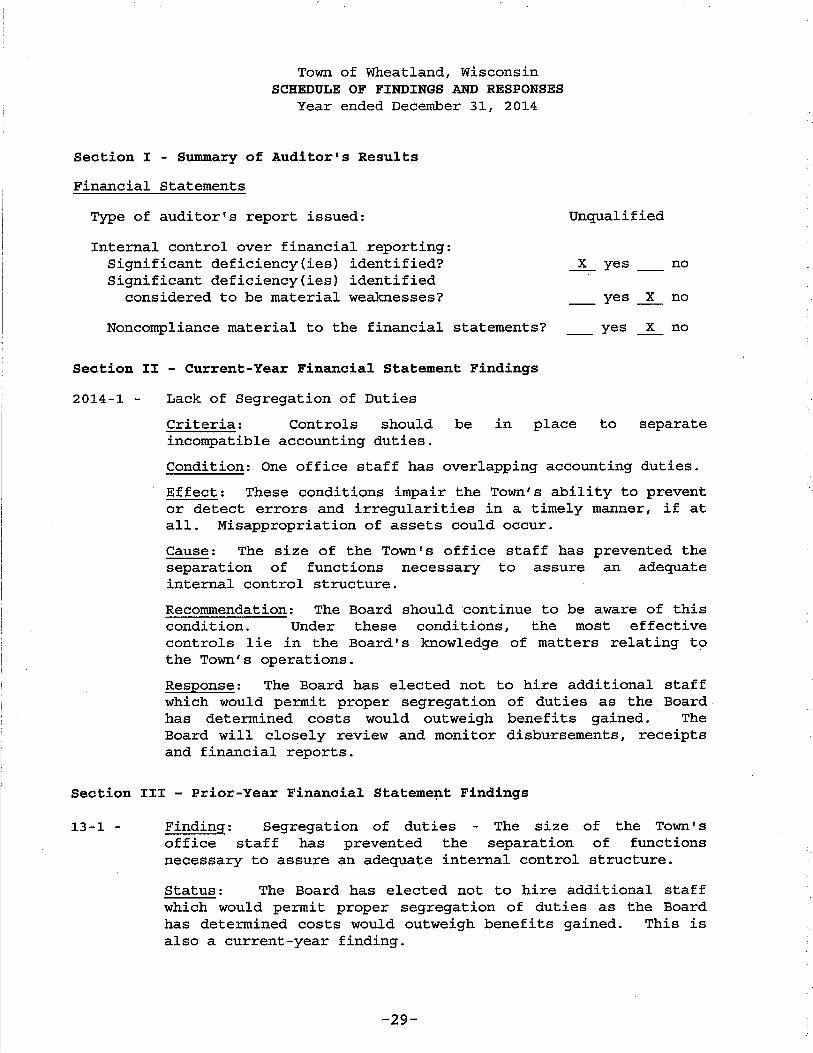

Town of Wheatland, Wisconsin SCHEDULE OF FINDINGS AND RESPONSES

Year ended December 31, 2014

Section I - Summary of Auditor•s Results

Financial Statements

Type of auditor's report issued: Unqualified

Internal control over financial reporting: Significant deficiency{ies) identified? Significant deficiency(ies) identified

considered to be material weaknesses?

X yes no

yes X no

Noncompliance material to the financial statements? ___ yes _!_ no

Section II - Current-Year Financial Statement Findings

2014-1 - Lack of Segregation of Duties

Criteria: Controls should be in place to separate incompatible accounting duties.

Condition: One office staff has overlapping accounting duties.

Effect: These conditions impair the Town's ability to prevent or detect errors and irregularities in a timely manner, if at all. Misappropriation of assets could occur.

Cause: The size of the Town's office staff has prevented the separation of functions necessary to assure an adequate internal control structure.

Recommendation: The Board should continue to be aware of this condition. Under these conditions, the most effective controls lie in the Board's knowledge of matters relating to the Town's operations.

Response: The Board has elected not to hire additional staff which would permit proper segregation of duties as the Board has determined costs would outweigh benefits gained. The Board will closely review and monitor disbursements, receipts and financial reports.

Section III - Prior-Year Financial Stateme~t Findings

13-1 - Finding: Segregation of duties The size of the Town's office staff has prevented the separation of functions necessary to assure an adequate internal control structure.

Status: The Board has elected not to hire additional staff which would permit proper segregation of duties as the Board has determined costs would outweigh benefits gained. This is also a current-year finding.

-29-