Financial Statements for a Corporation CHAPTER 15 Financial statements provide the primary source of...

17

Financial Statements for a Corporation CHAPTER 15 ial statements provide the primary source of inform by owners and managers to make decisions about fut ss activities.

-

Upload

hilda-casey -

Category

Documents

-

view

213 -

download

0

Transcript of Financial Statements for a Corporation CHAPTER 15 Financial statements provide the primary source of...

Financial Statements for a Corporation

CHAPTER 15

Financial statements provide the primary source of information needed by owners and managers to make decisions about future business activities.

2

15-1 INCOME STATEMENT INFORMATION ON A WORK SHEET page 448

3

6. Contra account amounts

REVENUE SECTION OF AN INCOME STATEMENT FOR A MERCHANDISING BUSINESS

11

22

33 44

55

66 7788 99

1. Heading

7. Contra account total

3. Title of revenue account 8. Net Sales

4. Sales amount 9. Net sales amount

5. Less contra accounts

2. Revenue section

page 449

Total Sales - Sales Discount - Sales Returns & Allow = Net Sales

4COST OF MERCHANDISE SOLD SECTION OF AN INCOME STATEMENT FOR A MERCHANDISING BUSINESS

11

2233

page 450

446655

1. Cost of Merchandise Sold section

2. Beginning inventory

3. Purchases section

4. Total cost of merchandise available for sale

5. Ending inventory

6. Cost of merchandise sold

Cost of Merchandise Sold - The original price of all merchandise sold during a fiscal period.

5

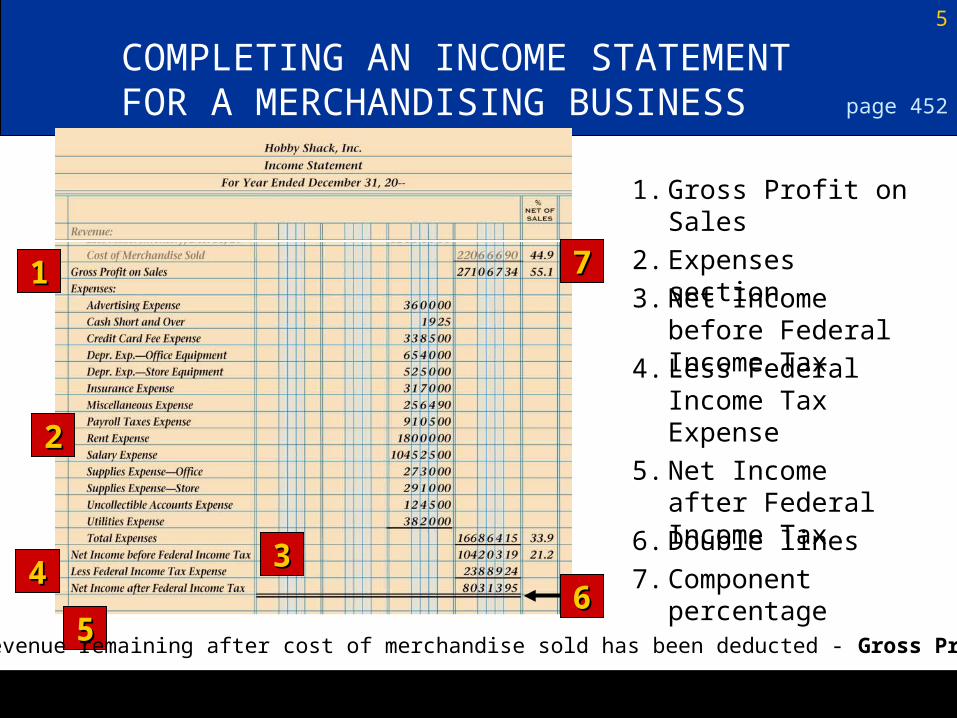

COMPLETING AN INCOME STATEMENT FOR A MERCHANDISING BUSINESS

11

22

44

55

page 452

77

3366

7. Component percentage

6. Double lines

5. Net Income after Federal Income Tax

4. Less Federal Income Tax Expense

3. Net Income before Federal Income Tax

2. Expenses section

1. Gross Profit on Sales

The revenue remaining after cost of merchandise sold has been deducted - Gross Profit on Sales

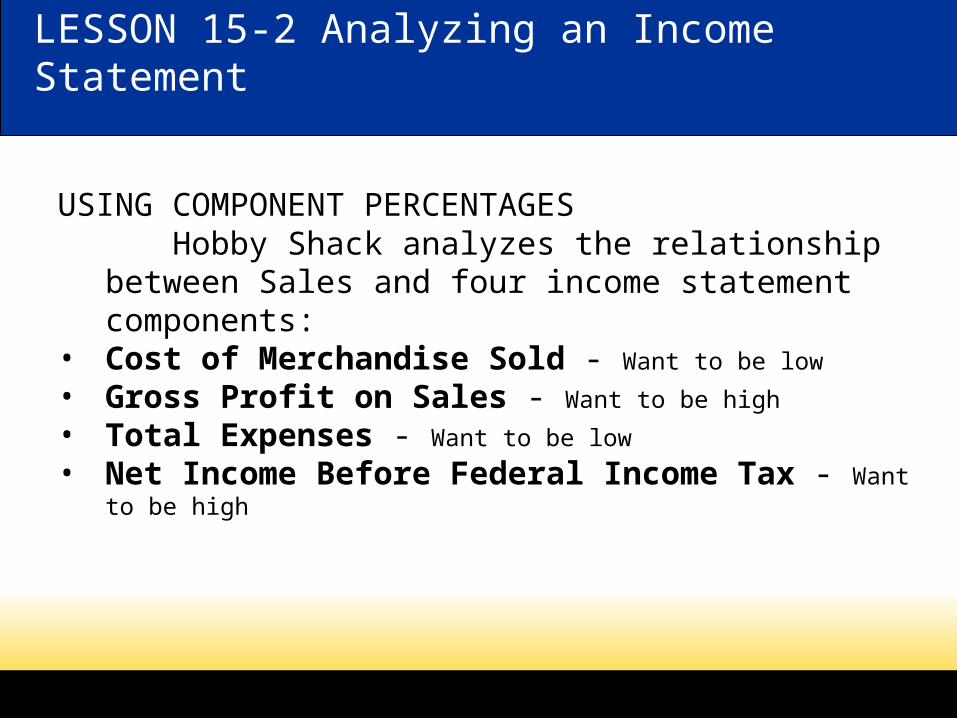

LESSON 15-2 Analyzing an Income Statement

USING COMPONENT PERCENTAGES Hobby Shack analyzes the relationship between Sales and four

income statement components:• Cost of Merchandise Sold - Want to be low

• Gross Profit on Sales - Want to be high

• Total Expenses - Want to be low

• Net Income Before Federal Income Tax - Want to be high

7

ANALYZING AN INCOME STATEMENT SHOWING A NET LOSS page 457

8

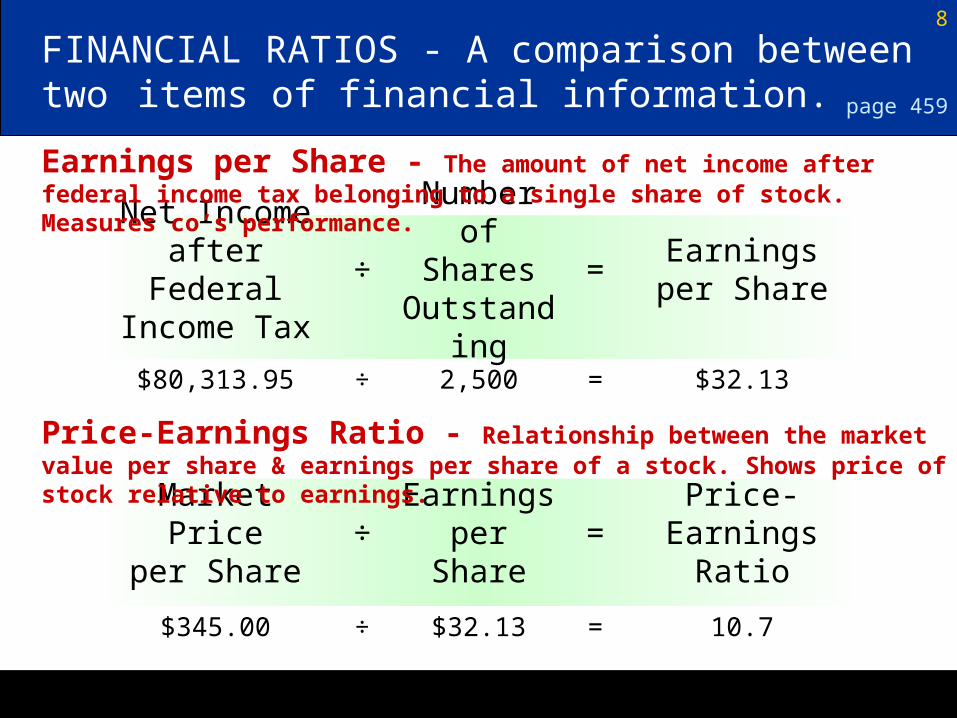

Price-EarningsRatio

=Earnings

perShare

÷Market Price

per Share

Earningsper Share

=Number of

SharesOutstanding

÷Net Incomeafter FederalIncome Tax

FINANCIAL RATIOS - A comparison between two items of financial information. page 459

Earnings per Share - The amount of net income after federal income tax belonging to a single share of stock. Measures co’s performance.

Price-Earnings Ratio - Relationship between the market value per share & earnings per share of a stock. Shows price of stock relative to earnings.

$32.13=2,500÷$80,313.95

10.7=$32.13÷$345.00

9

15-3 STATEMENT OF STOCKHOLDERS’ EQUITY

1122

3344

55

page 461

1. Heading2. Capital Stock and Par Value

5. Total stock issued at the end of the year

3. Stock at the beginning of the year4. Stock issued during the year

Shows changes in a corporation’s ownership for a fiscal period. Contains two sections - Capital Stock & Retained Earnings.

Par Value - A value assigned to a share of stock & printed on a stock certificate.

10

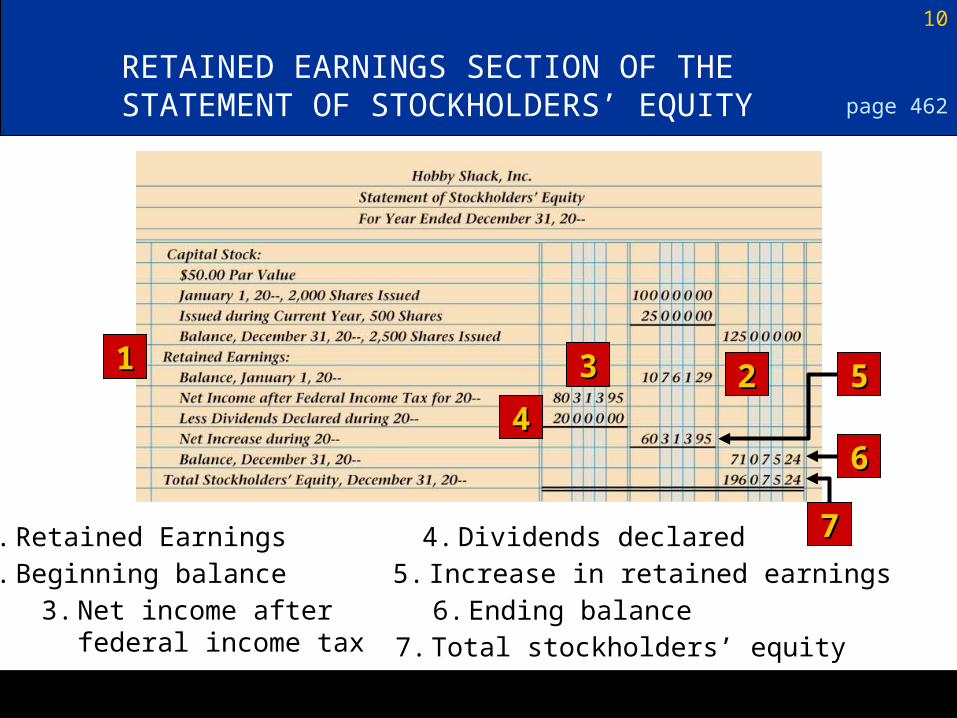

RETAINED EARNINGS SECTION OF THE STATEMENT OF STOCKHOLDERS’ EQUITY

112233

44

page 462

4. Dividends declared

66

77

55

2. Beginning balance

7. Total stockholders’ equity6. Ending balance3. Net income after federal

income tax

5. Increase in retained earnings1. Retained Earnings

11

15-4 BALANCE SHEET INFORMATION ON A WORK SHEET page 464

12

CURRENT ASSETS SECTION OF A BALANCE SHEET

11

22

33

44

55

page 465

3. Book value of accounts receivable

4. Remaining current asset accounts1. Heading

2. Begin assets section 5. Current assets

13

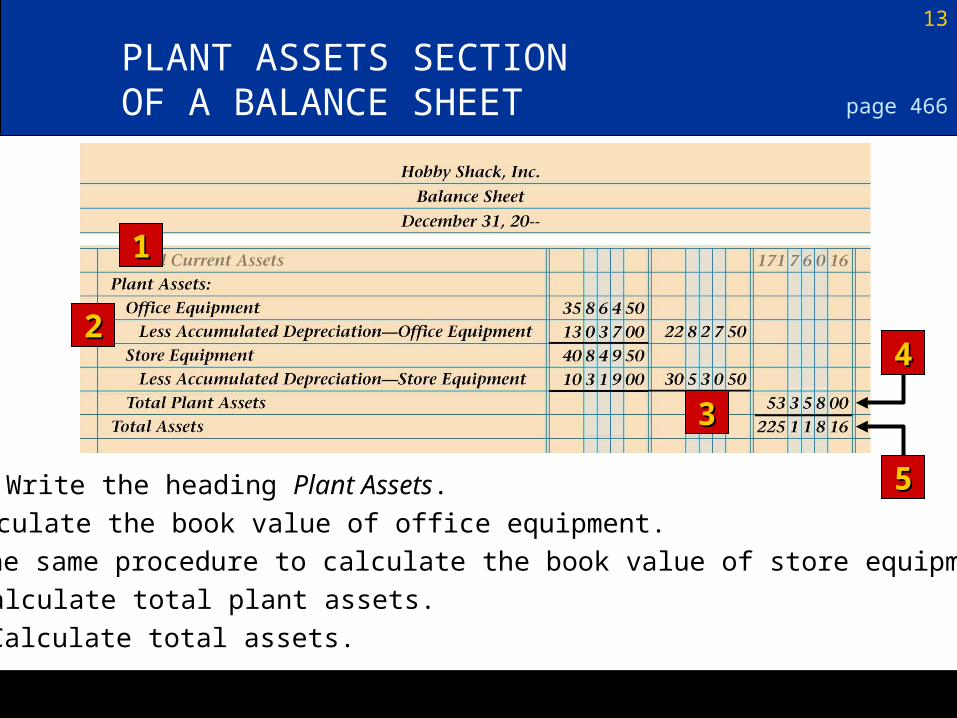

PLANT ASSETS SECTION OF A BALANCE SHEET

11

22

33

page 466

44

551. Write the heading Plant Assets.

2. Calculate the book value of office equipment.

3. Use the same procedure to calculate the book value of store equipment.

4. Calculate total plant assets.

5. Calculate total assets.

14

LIABILITIES SECTION OF A BALANCE SHEET

11

33

page 467

1. Heading

2. Account title and amount of each current liability

3. Total liabilities

22

Current Liabilities - Liabilities due within a short time, usually with in a year.Long Term Liabilities - Liabilities owed for more than a year (ex: mortgage)

15

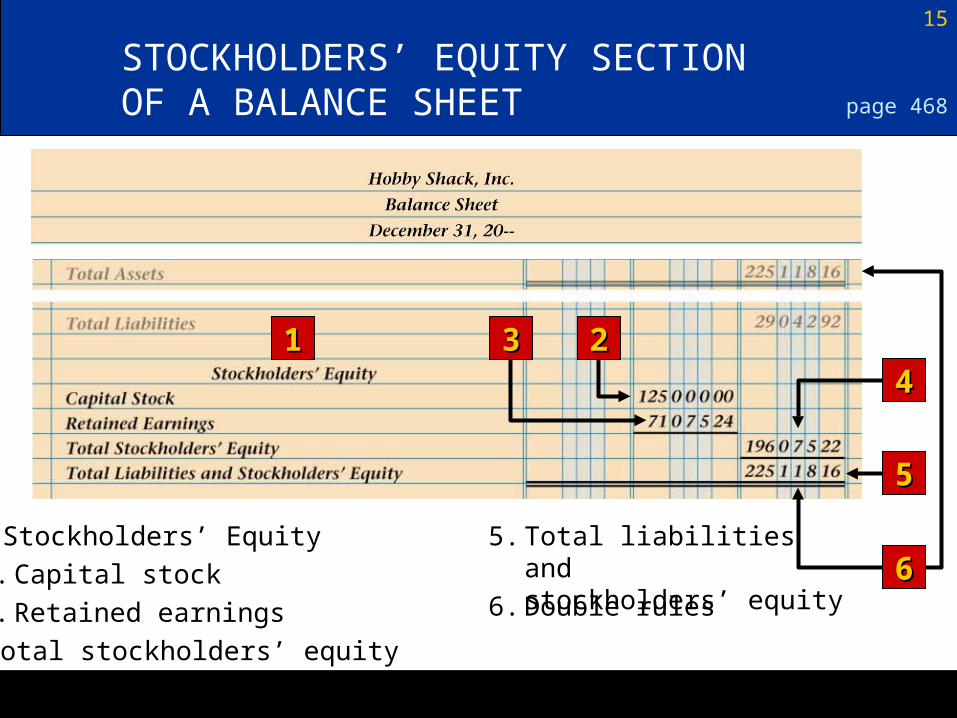

STOCKHOLDERS’ EQUITY SECTION OF A BALANCE SHEET

11

page 468

5. Total liabilities and stockholders’ equity

44

55

2233

2. Capital stock

1. Stockholders’ Equity

3. Retained earnings

4. Total stockholders’ equity

6. Double rules66

16

COMPLETED BALANCE SHEET page 469

(continued on next slide)

17

COMPLETED BALANCE SHEET page 469(continued from previous

slide)

Don’t forget aboutSchedule of Accounts Payable & Receivable!