FINANCIAL STATEMENTS 2016 - assets.upm.comassets.upm.com/Investors/2016/Q4 2016 presentation.pdf ·...

29

FINANCIAL STATEMENTS 2016 Jussi Pesonen President and CEO 31 January 2017

Transcript of FINANCIAL STATEMENTS 2016 - assets.upm.comassets.upm.com/Investors/2016/Q4 2016 presentation.pdf ·...

FINANCIAL STATEMENTS 2016Jussi Pesonen

President and CEO

31 January 2017

| © UPM

2016 demonstrated the results of UPM

transformation and sets the stage for the future

• Differentiating, agile business model

– Business area commercial strategies, growth and competitiveness

– Capturing corporate benefits

• Disciplined capital allocation

– Focus on returns in growth investments

– Industry leading balance sheet

• Continuous improvement programmes

– Variable and fixed costs, safety, compliance, working capital

– Efficient use of assets, including restructuring

Today’s UPM is earnings growth oriented, capable and financially strong

2

| © UPM

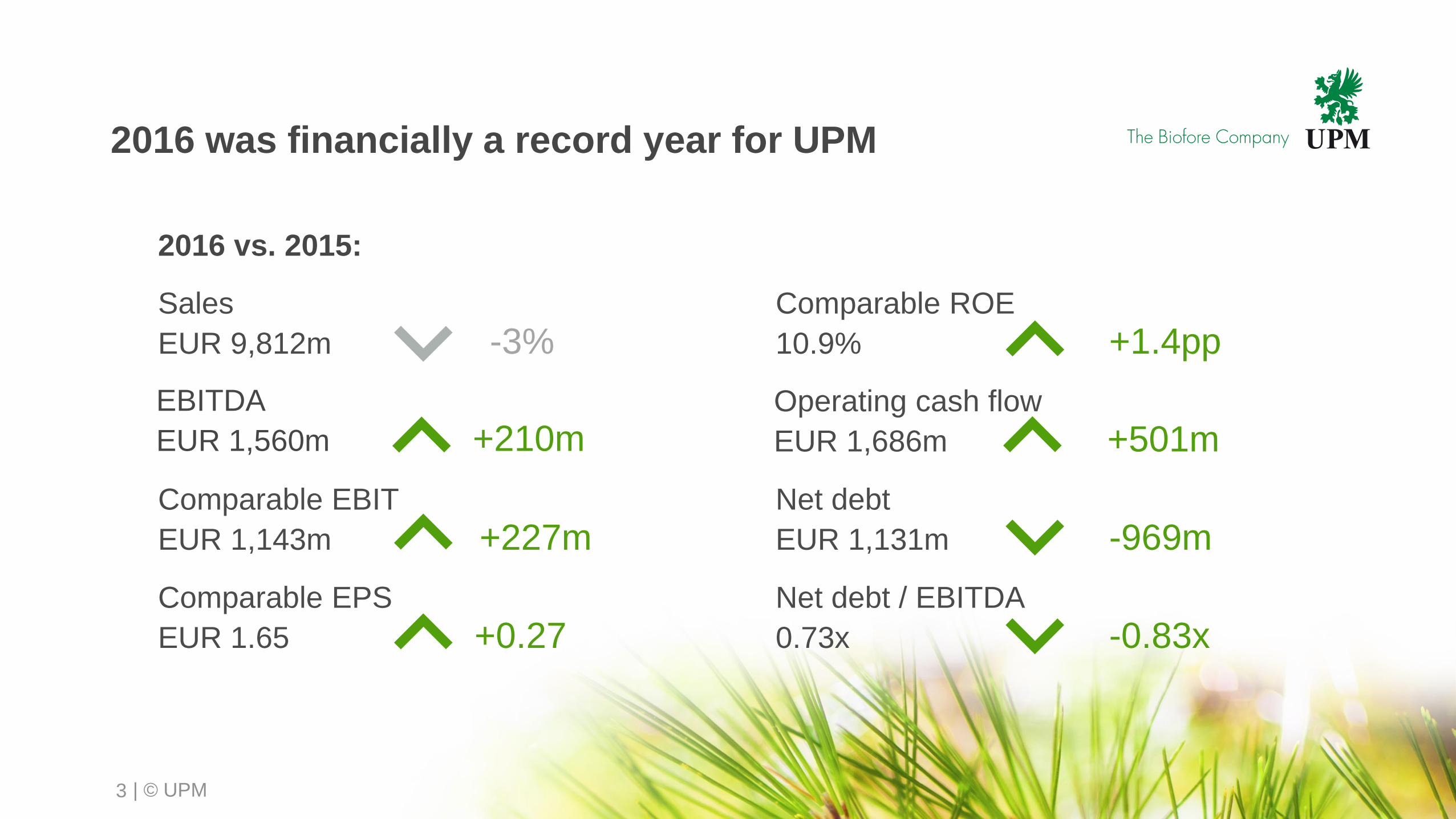

Sales

EUR 9,812m -3%

EBITDA

EUR 1,560m +210m

2016 was financially a record year for UPM

Comparable EBIT

EUR 1,143m +227m

2016 vs. 2015:

Comparable EPS

EUR 1.65 +0.27

Net debt

EUR 1,131m -969m

Operating cash flow

EUR 1,686m +501m

Net debt / EBITDA

0.73x -0.83x

Comparable ROE

10.9% +1.4pp

3

| © UPM

Growth projects contributed significantly and cost

efficiency measures continued on a strong track

4

0

200

400

600

800

1 000

1 200

1 400

2015 2016

Variable

costs

Fixed

costs

Deliveries

other BAs

Deliveries

Paper ENA

Currency

Comparable EBIT 2016 vs. 2015

Prices

Other

9169.0%

1,14311.6%

EURm

| © UPM

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2011 2012 2013 2014 2015 2016

Record strong cash flow and balance sheet

5

Net debt / EBITDA(trailing12 months)

Net debt

Net debt / EBITDA

0.73x

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2011 2012 2013 2014 2015 2016

Operating cash flow Net debt

1,131

2,100

1,686

1,185

Net debtEURm

Cash flow after

investing activities

Operating cash flow

EURm

Working

capital

decreased by

EUR 195m in

2016

| © UPM

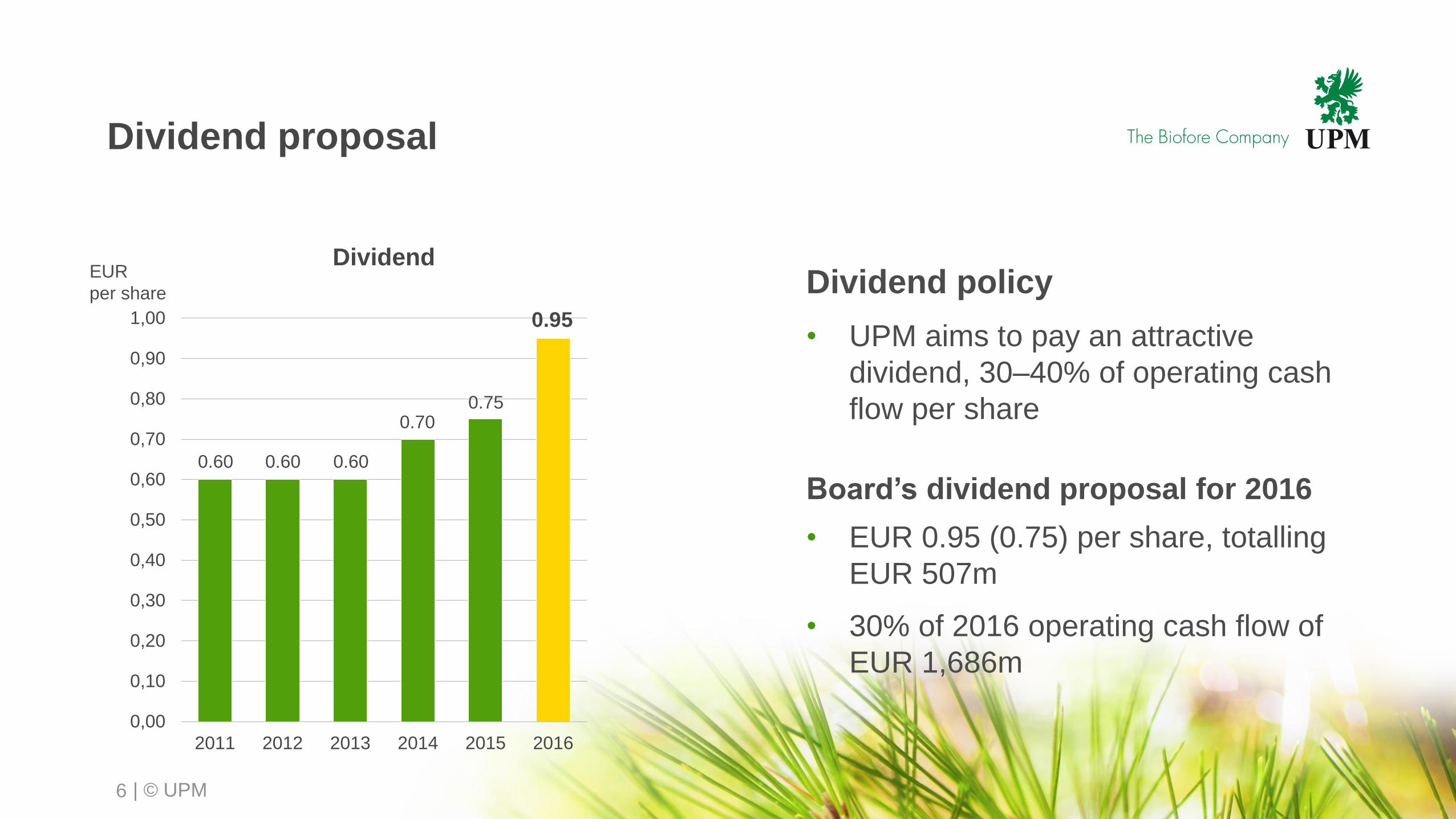

Dividend proposal

6

0,00

0,10

0,20

0,30

0,40

0,50

0,60

0,70

0,80

0,90

1,00

2011 2012 2013 2014 2015 2016

DividendEUR

per share Dividend policy

• UPM aims to pay an attractive

dividend, 30–40% of operating cash

flow per share

Board’s dividend proposal for 2016

• EUR 0.95 (0.75) per share, totalling

EUR 507m

• 30% of 2016 operating cash flow of

EUR 1,686m

0.60 0.60 0.60

0.70

0.95

0.75

| © UPM

0

50

100

150

200

250

300

350

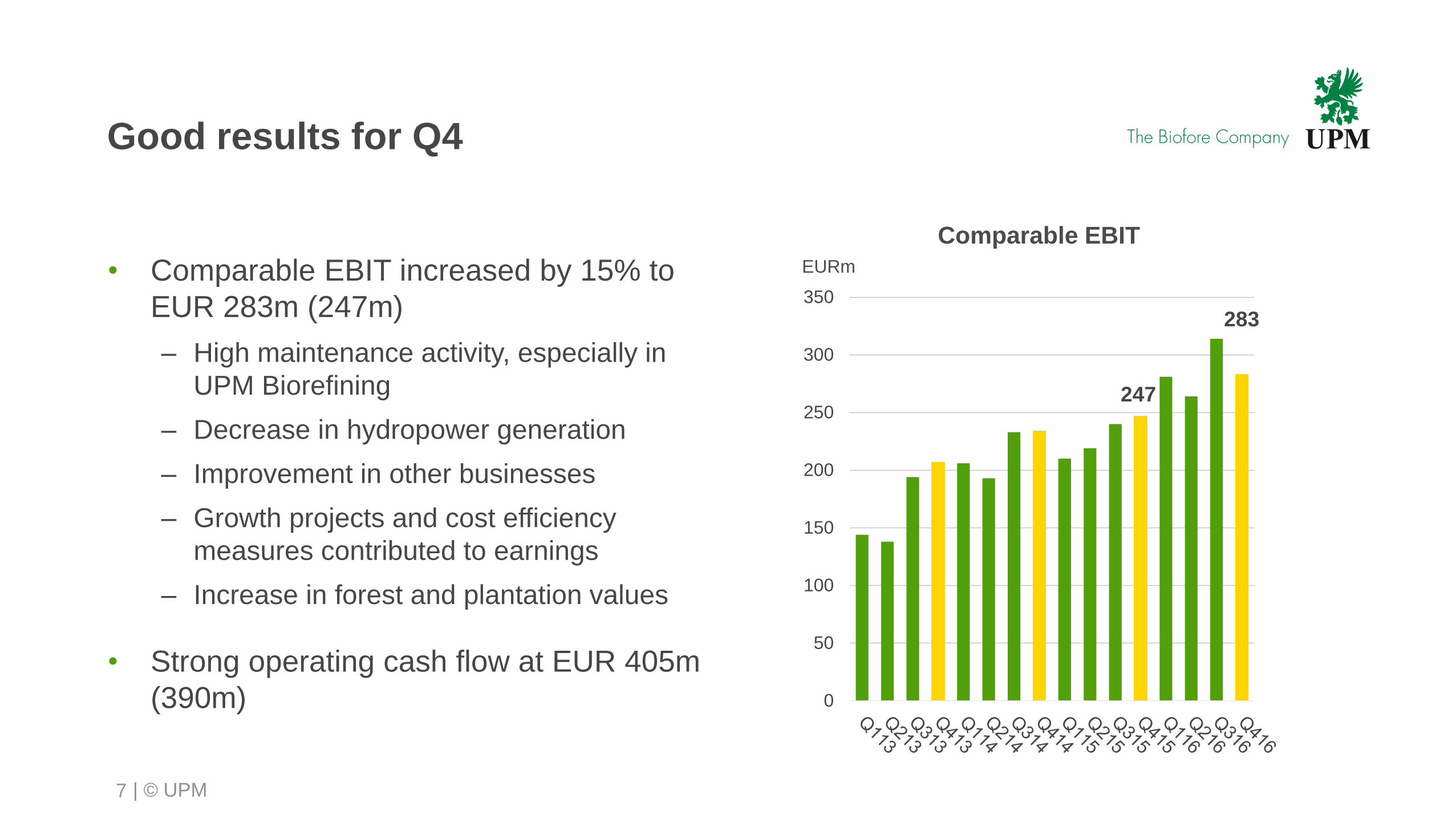

Good results for Q4

• Comparable EBIT increased by 15% to

EUR 283m (247m)

– High maintenance activity, especially in

UPM Biorefining

– Decrease in hydropower generation

– Improvement in other businesses

– Growth projects and cost efficiency

measures contributed to earnings

– Increase in forest and plantation values

• Strong operating cash flow at EUR 405m

(390m)

EURm

Comparable EBIT

283

247

7

| © UPM

0

50

100

150

200

250

300

350

Q4/15 Q4/16

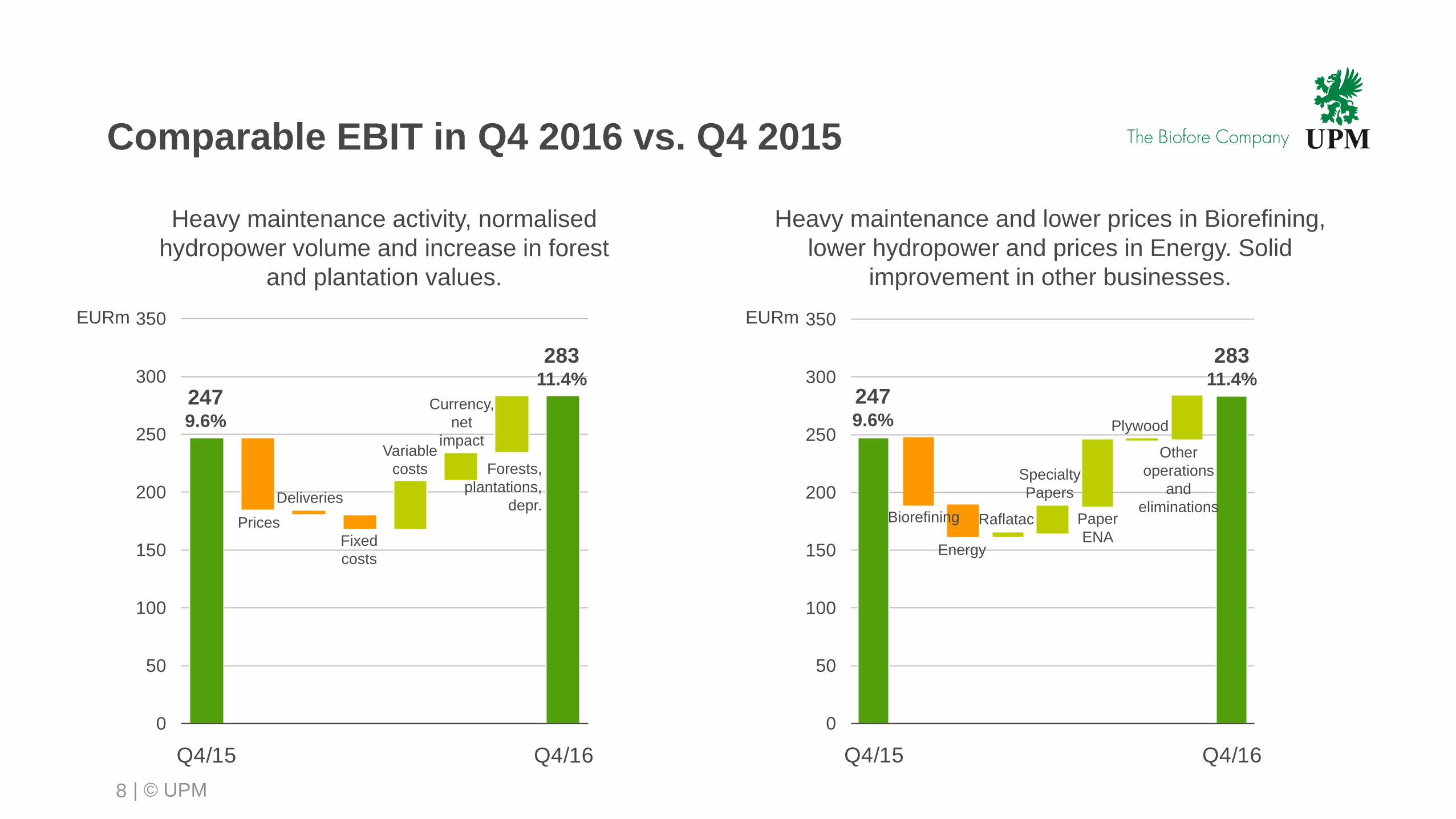

Comparable EBIT in Q4 2016 vs. Q4 2015

Raflatac

Specialty

Papers

Other

operations

and

eliminations

Energy

Biorefining Paper

ENA

Plywood

0

50

100

150

200

250

300

350

Q4/15 Q4/16

EURm

Prices

Variable

costs

Fixed

costs

Deliveries

Heavy maintenance activity, normalised

hydropower volume and increase in forest

and plantation values.

EURm

Heavy maintenance and lower prices in Biorefining,

lower hydropower and prices in Energy. Solid

improvement in other businesses.

2479.6%

28311.4%

Currency,

net

impact

2479.6%

28311.4%

8

Forests,

plantations,

depr.

| © UPM

Comparable EBIT by business area

9

0

2,5

5

7,5

10

12,5

0

10

20

30

40

50

0

5

10

15

20

25

0

30

60

90

120

150

0

15

30

45

60

0

20

40

60

80

0

2

4

6

8

10

0

10

20

30

40

50

-2

0

2

4

6

8

10

-25

0

25

50

75

100

125

0

4

8

12

16

20

0

5

10

15

20

25

EURm % of salesUPM Specialty Papers EURm % of salesUPM Paper ENA EURm % of salesUPM Plywood

EURm % of salesUPM RaflatacEURm % of salesUPM EnergyEURm % of salesUPM Biorefining

| © UPM

Outlook for 2017

• UPM’s profitability improved significantly in 2016 and is

expected to remain on a good level in 2017.

• Demand growth is expected to continue for most of

UPM’s businesses, while demand decline is expected

to continue for UPM Paper ENA. The focused growth

projects continue to contribute gradually to UPM’s

performance.

• Following a deflationary environment in recent years,

2017 is expected to show modest input cost inflation.

UPM will continue measures to reduce fixed and

variable costs to mitigate this.

• 2017 starts with lower pulp prices and lower availability

of hydropower than in the beginning of 2016.

10 | © UPM

| © UPM

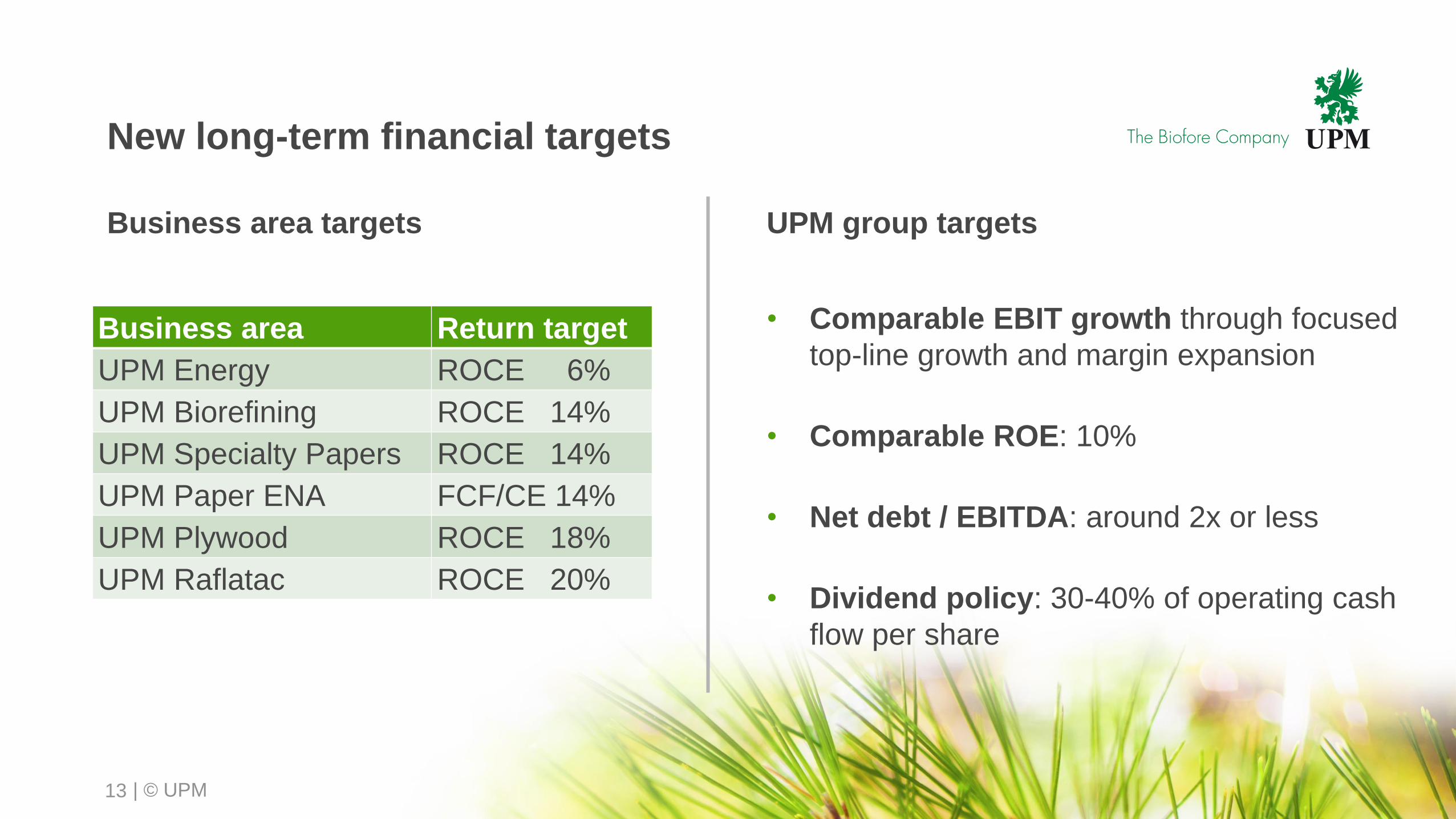

UPM aims higher with renewed long-term

financial targets

11

UPM renews its long-term financial targets:

• Business area long-term return targets increased

• Growth target introduced for group comparable EBIT

• Comparable ROE target increased

• A new financial policy on leverage based on net debt/EBITDA introduced

• The cash flow-based dividend policy remains unchanged.

| © UPM

New long-term financial targets

12

Business area returns Group earnings growth

Earnings growth through focused top-

line growth and margin expansion

Comparable EBIT

Increased return targets for

each business area

ROCE, FCF/CE

Capital structure and shareholder returns

Efficient capital structure, investment grade rating

and attractive shareholder returns

Net debt / EBITDA

ROE %

Dividend policy

| © UPM

New long-term financial targets

Business area targets UPM group targets

• Comparable EBIT growth through focused

top-line growth and margin expansion

• Comparable ROE: 10%

• Net debt / EBITDA: around 2x or less

• Dividend policy: 30-40% of operating cash

flow per share

13

Business area Return target

UPM Energy ROCE 6%

UPM Biorefining ROCE 14%

UPM Specialty Papers ROCE 14%

UPM Paper ENA FCF/CE 14%

UPM Plywood ROCE 18%

UPM Raflatac ROCE 20%

| © UPM

New business area long-term targets compared

with realised returns

14

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30ROCE %

UPM

Specialty Papers

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30FCF/CE %

UPM

Paper ENA

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30ROCE %

UPM

Plywood

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30ROCE %

UPM

Raflatac

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30ROCE % *)

UPM

Energy

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30ROCE %

UPM

Biorefining

*) shareholdings in UPM Energy valued at fair value Long-term return target

| © UPM

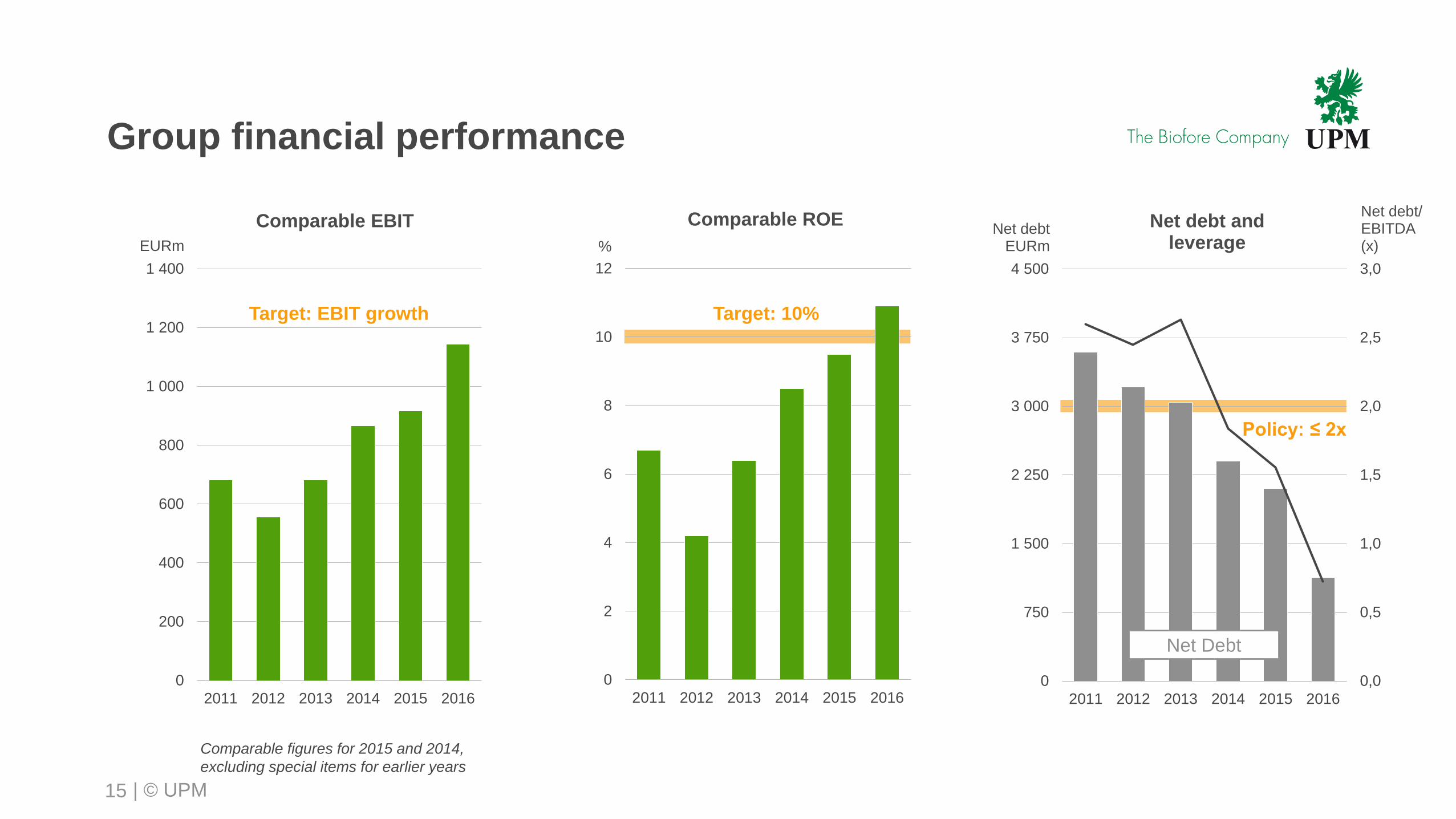

Group financial performance

15

0

200

400

600

800

1 000

1 200

1 400

2011 2012 2013 2014 2015 20160,0

0,5

1,0

1,5

2,0

2,5

3,0

0

750

1 500

2 250

3 000

3 750

4 500

2011 2012 2013 2014 2015 2016

Net Debt

Policy: ≤ 2x

Net debtEURm

Net debt/EBITDA(x)

Comparable EBIT

0

2

4

6

8

10

12

2011 2012 2013 2014 2015 2016

Target: 10%

%

Comparable ROE Net debt and leverage

Comparable figures for 2015 and 2014,

excluding special items for earlier years

EURm

Target: EBIT growth

| © UPM

Summary

16

• 2016 was financially a record year, demonstrating the results of

UPM transformation

• Board proposes a dividend of EUR 0.95 (0.75) per share

• UPM aims higher with renewed long-term financial targets

| © UPM

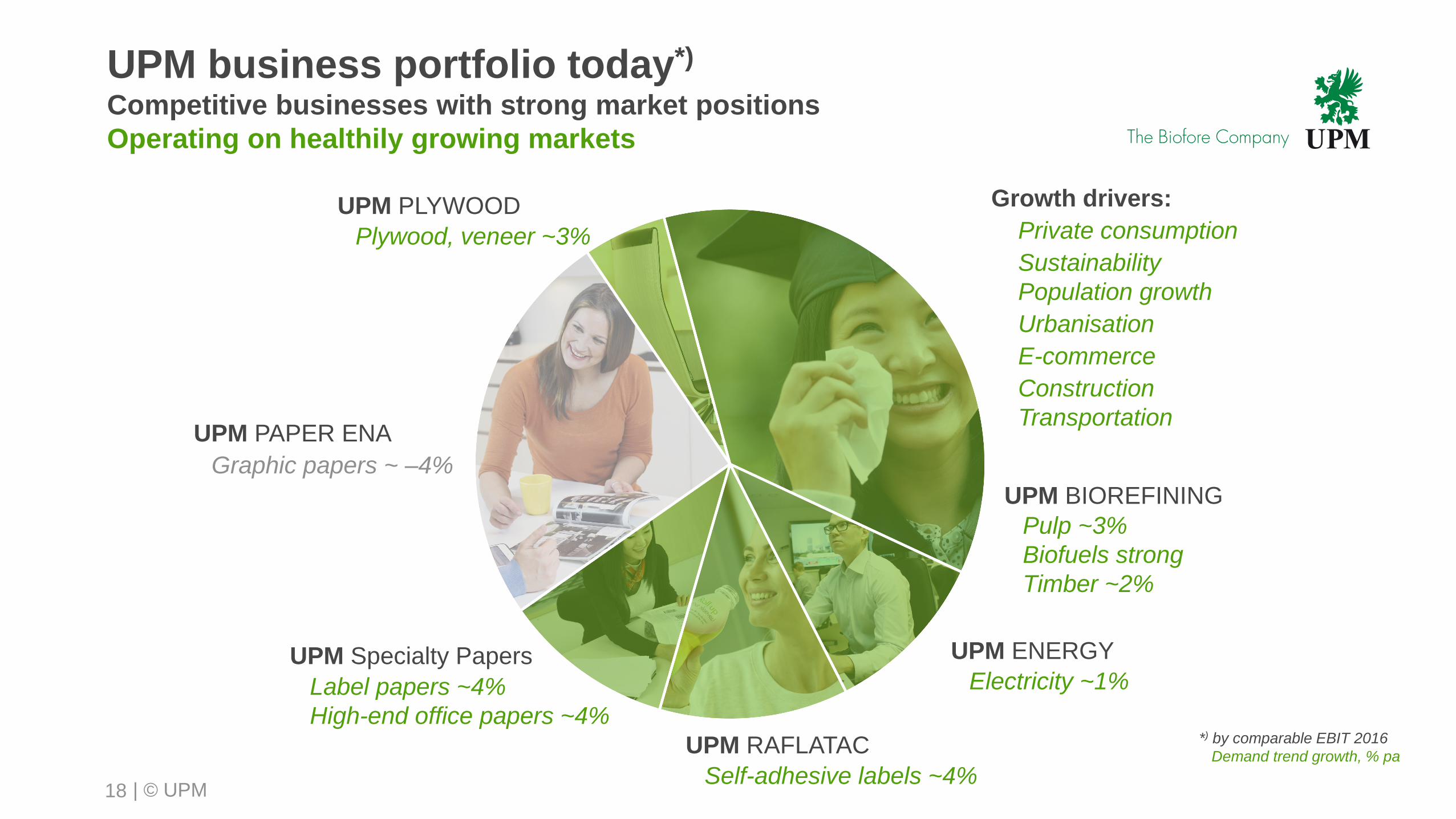

UPM business portfolio today*)

Competitive businesses with strong market positions

Operating on healthily growing markets

18

UPM ENERGY

UPM RAFLATAC

UPM PAPER ENA

UPM PLYWOOD

Electricity ~1%

Pulp ~3%

Biofuels strong

Timber ~2%

Graphic papers ~ –4%

Plywood, veneer ~3%

Self-adhesive labels ~4%

UPM Specialty Papers

UPM BIOREFINING

Growth drivers:

Private consumption

Sustainability

Population growth

Urbanisation

E-commerce

Construction

Transportation

*) by comparable EBIT 2016

Demand trend growth, % pa

Label papers ~4%

High-end office papers ~4%

| © UPM

Mostly favourable market demand in 2016

19

Growing demand

• Pulp

• Advanced biofuels

• Self-adhesive label

materials

• Label, pack and release

materials

• Office papers in Asia

• Plywood

• Sawn timber

• Electricity

Declining demand

• Graphic papers in Europe

and North America

| © UPM

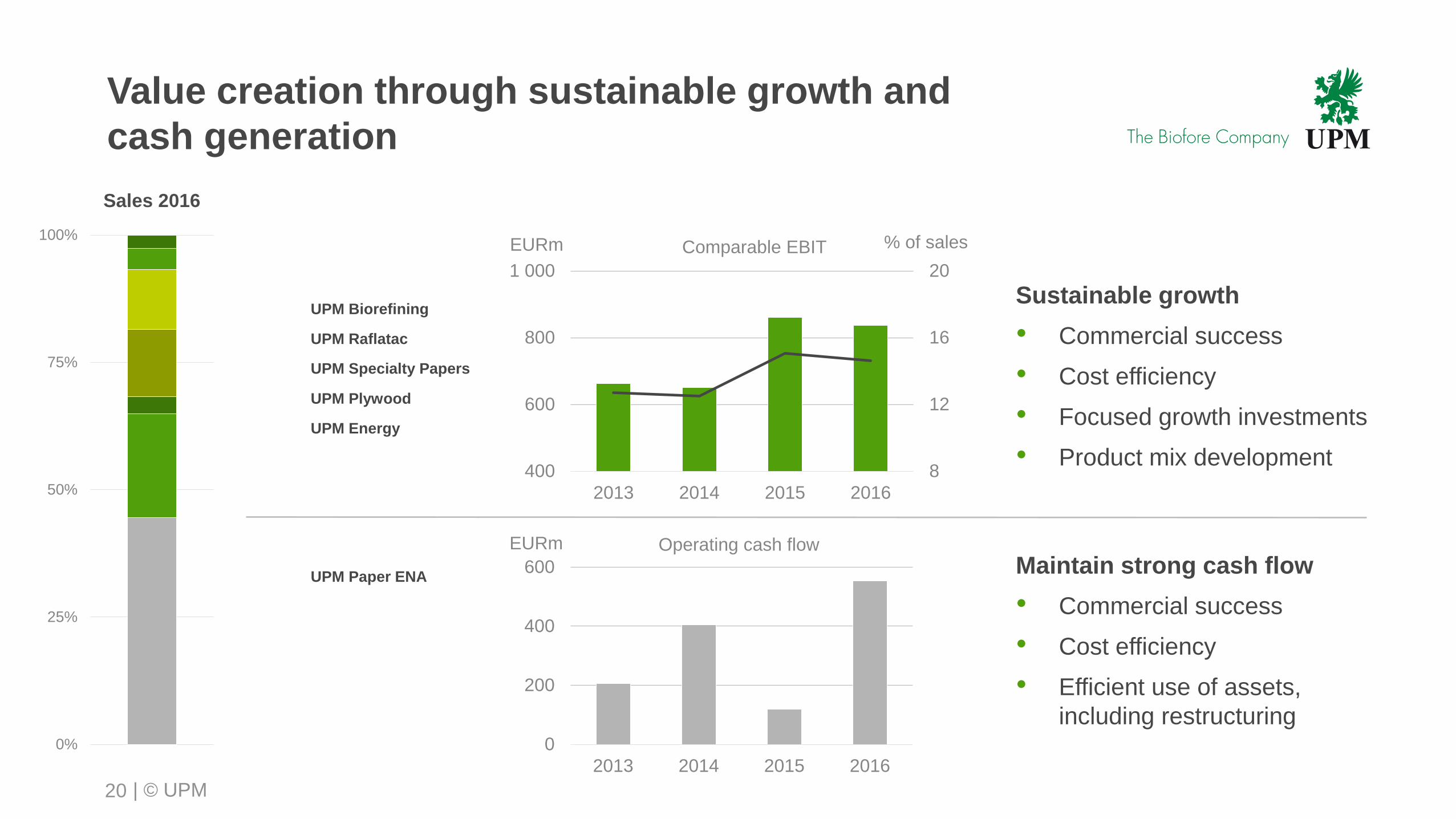

Value creation through sustainable growth and

cash generation

20

UPM Biorefining

UPM Raflatac

UPM Specialty Papers

UPM Plywood

Sales 2016

UPM Paper ENA

UPM Energy

8

12

16

20

400

600

800

1 000

2013 2014 2015 2016

% of salesEURm Comparable EBIT

Maintain strong cash flow

• Commercial success

• Cost efficiency

• Efficient use of assets,

including restructuring

Sustainable growth

• Commercial success

• Cost efficiency

• Focused growth investments

• Product mix development

0

200

400

600

2013 2014 2015 2016

EURm Operating cash flow

0%

25%

50%

75%

100%

| © UPM

Focused growth investments contributed

significantly to 2016 results

21

Fully contributing in 2016

• Pietarsaari pulp mill expansion

• Fray Bentos pulp mill expansion

• Kymi pulp mill expansion

• Raflatac expansion in APAC, Poland

Further optimisation potential

• Lappeenranta biorefinery

• Changshu speciality papers

Ramp-up in progress

• Otepää plywood mill expansion

• Kaukas pulp mill efficiency

Under construction

• Kymi pulp mill expansion

• Raflatac expansion in Poland

80% run-rate of the

EUR 200m EBITDA

target achieved in 2016

| © UPM

Focused investments are delivering growth

22

Pulp CAGR +3%

Biofuels New business

Standard products CAGR +4%

Films and specials CAGR +8%

Label materials CAGR +4%

Cut-size CAGR +6%

Plywood CAGR +3%

Average delivery growth 2011 –2016

UPM Biorefining

UPM Raflatac

UPM Specialty Papers

UPM Plywood

Sales 2016

0%

25%

50%

75%

100%

| © UPM

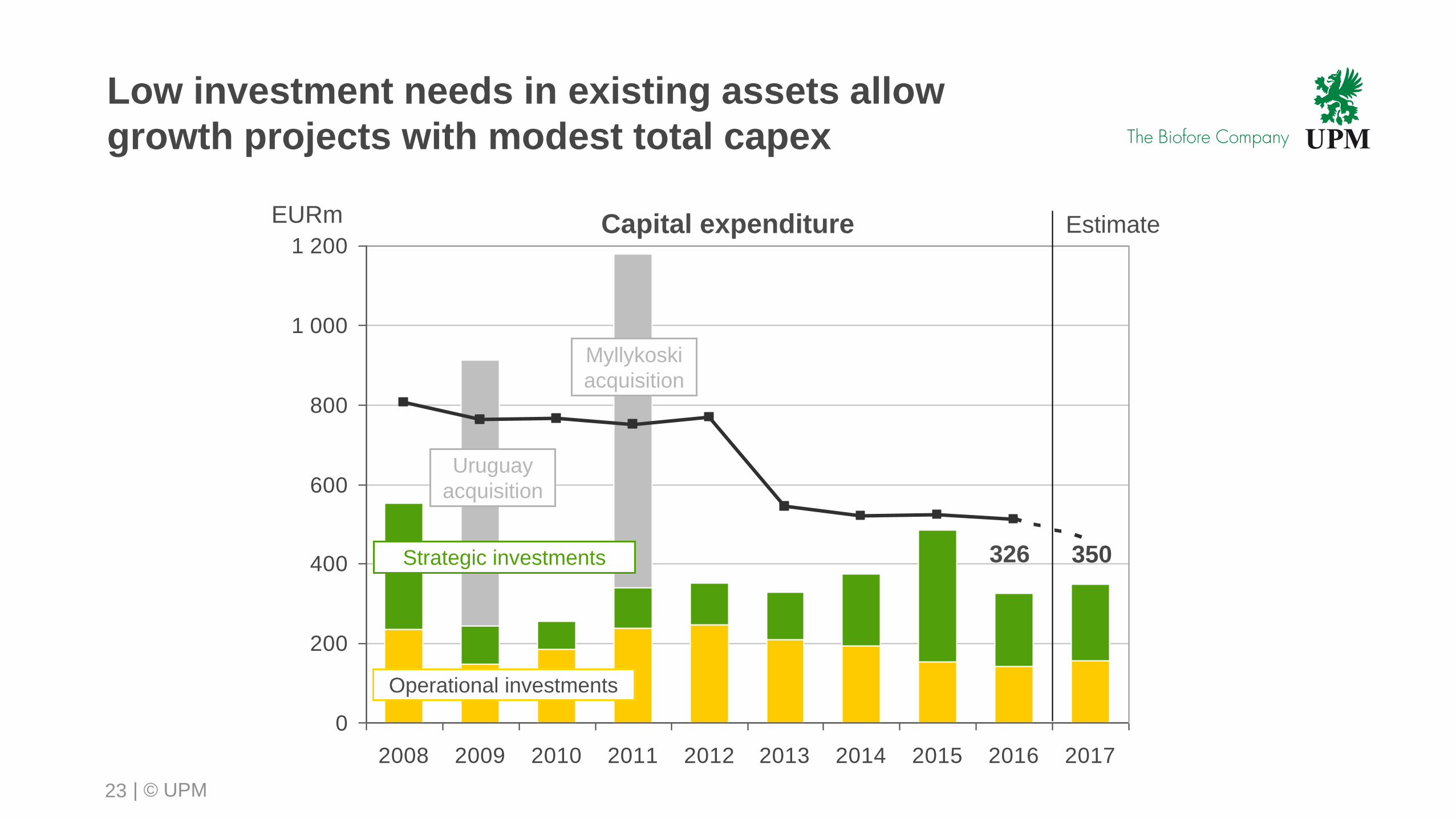

Low investment needs in existing assets allow

growth projects with modest total capex

23

0

200

400

600

800

1 000

1 200

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

EURm

Operational investments

Capital expenditure

Strategic investments

Uruguay

acquisition

486

Estimate

326 350

Myllykoski

acquisition

| © UPM

Maturity profile and liquidity

0

200

400

600

800

1 000

0

200

400

600

800

1 000

24

Maturity profile of outstanding debt Committed credit facilities’ maturities EURm EURm

Liquidity

Liquidity was EUR 1.6bn on 31 December 2016(cash and unused credit facilities)

Bilateral committed credit facilities EUR 656m

Committed credit facilities

| © UPM

Chemical pulp market

25

Source: PPPC World-20 statistics

Pulp inventories

Days of

supply

300

400

500

600

700

800

900

1 000

1 100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

USD/tonne

Q4 NBSK pulp price remained stable from Q3

Q4 BHKP pulp price decreased 2% from Q3

BHKP

NBSK

Source: FOEX Indexes Ltd.

15

20

25

30

35

40

45

50

55

60

65

2008 2009 2010 2011 2012 2013 2014 2015 2016

Hardwood

inventories

Softwood

inventories

| © UPM

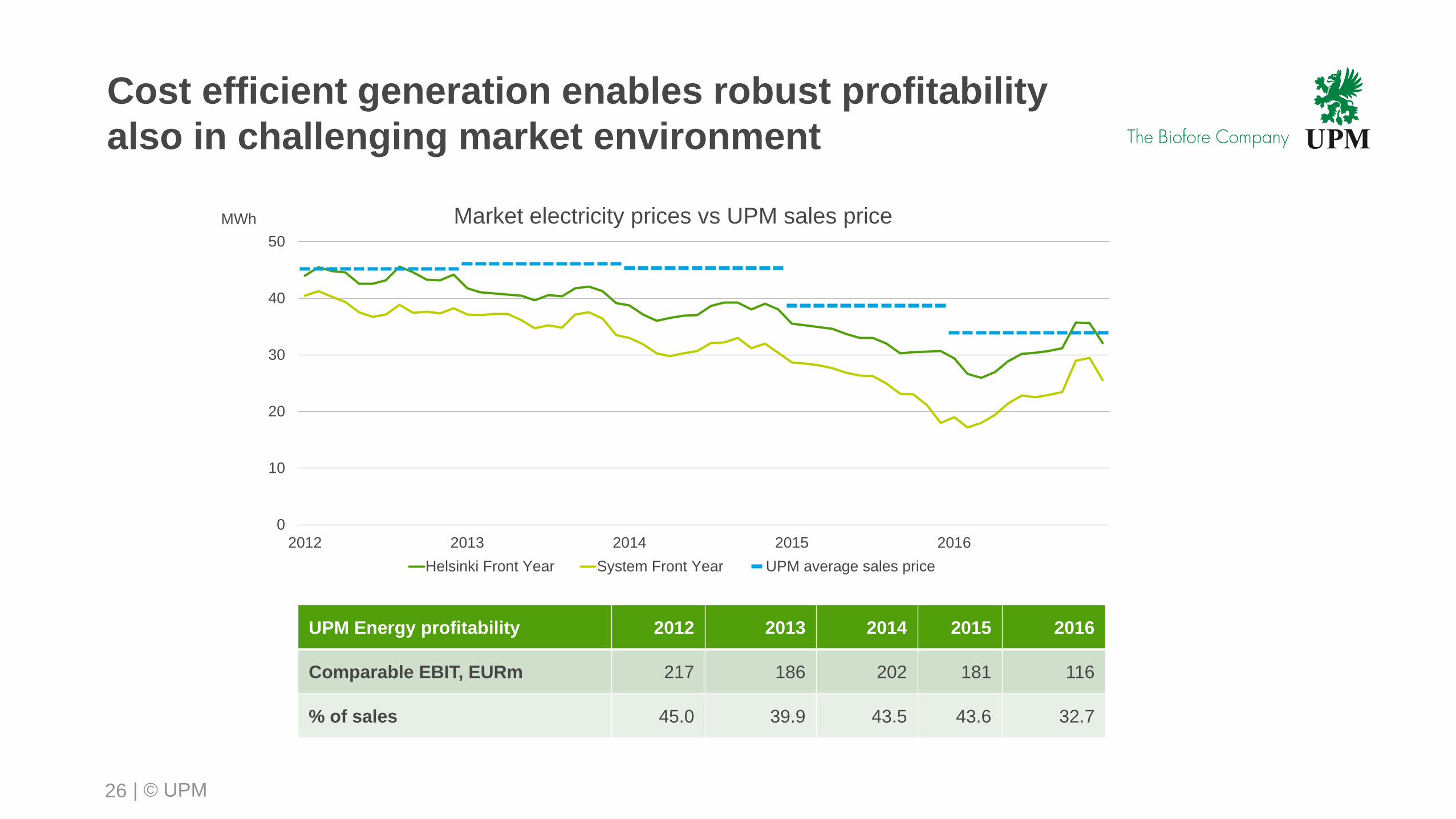

Cost efficient generation enables robust profitability

also in challenging market environment

26

0

10

20

30

40

50

2012 2013 2014 2015 2016

MWh Market electricity prices vs UPM sales price

Helsinki Front Year System Front Year UPM average sales price

UPM Energy profitability 2012 2013 2014 2015 2016

Comparable EBIT, EURm 217 186 202 181 116

% of sales 45.0 39.9 43.5 43.6 32.7

| © UPM27

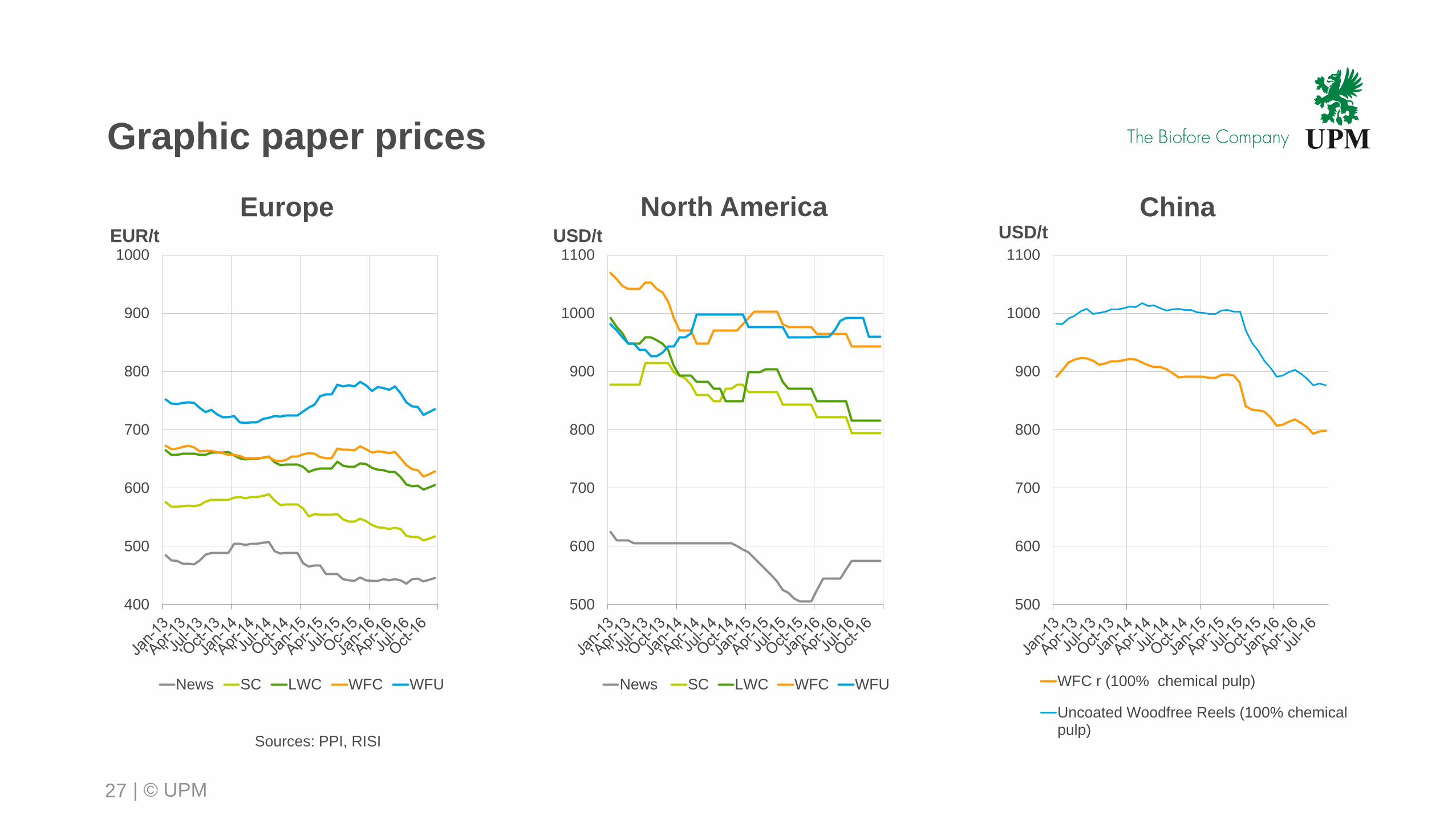

EUR/t

EuropeUSD/t USD/t

ChinaNorth America

Sources: PPI, RISI

500

600

700

800

900

1000

1100

WFC r (100% chemical pulp)

Uncoated Woodfree Reels (100% chemicalpulp)

Graphic paper prices

400

500

600

700

800

900

1000

News SC LWC WFC WFU

500

600

700

800

900

1000

1100

News SC LWC WFC WFU

| © UPM

Demand-supply balance in European graphic paper

is visible in margins

28

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Cash cost of a marginal producer

Price

EUR/t

Sources: PPI, RISI, Pöyry