Financial Statement Analysis I: Chapter 4 ©NACM. General Chapter Notes A. The Statement of Cash...

13

Financial Statement Analysis I: Chapter 4 ©NACM

-

Upload

darren-townsend -

Category

Documents

-

view

220 -

download

4

Transcript of Financial Statement Analysis I: Chapter 4 ©NACM. General Chapter Notes A. The Statement of Cash...

Financial Statement Analysis I:Chapter 4

©NACM

General Chapter Notes

A. The Statement of Cash Flows as a Derivative Statement

B. FASB 95 Analysis: Cash flows from Operations,

Investing, and Financing

Slide 4-1

Cash Flows of the Firm

Slide 4-2

General Chapter Notes (cont.)

Slide 4-3

C. How to Calculate Cash Flows

1. Net Income

2. Assets a. Increases are uses of cash (negative cash flows)b. Decreases are sources of cash

(positive cash flows)

3. Liabilities and Equity

a. Increases are sources of cash (positive cash flows)

b. Decreases are uses of cash (negative cash flows)

4. Classifying cash flows as Operating, Investing or Financing

General Chapter Notes (cont.)

D. The ABC Corp. Example Problem (balance sheets and income statement are provided as links to this module)

Cash Flow Statement - Indirect Method

Cash Flows from Operations Net Income $2,500 Depreciation (Change in Accum. Depr.) $1,500 Accounts Receivable ($1,500) Inventory $1,000 Accounts Payable $500 -------- CF from Operations $4,000

Slide 4-4

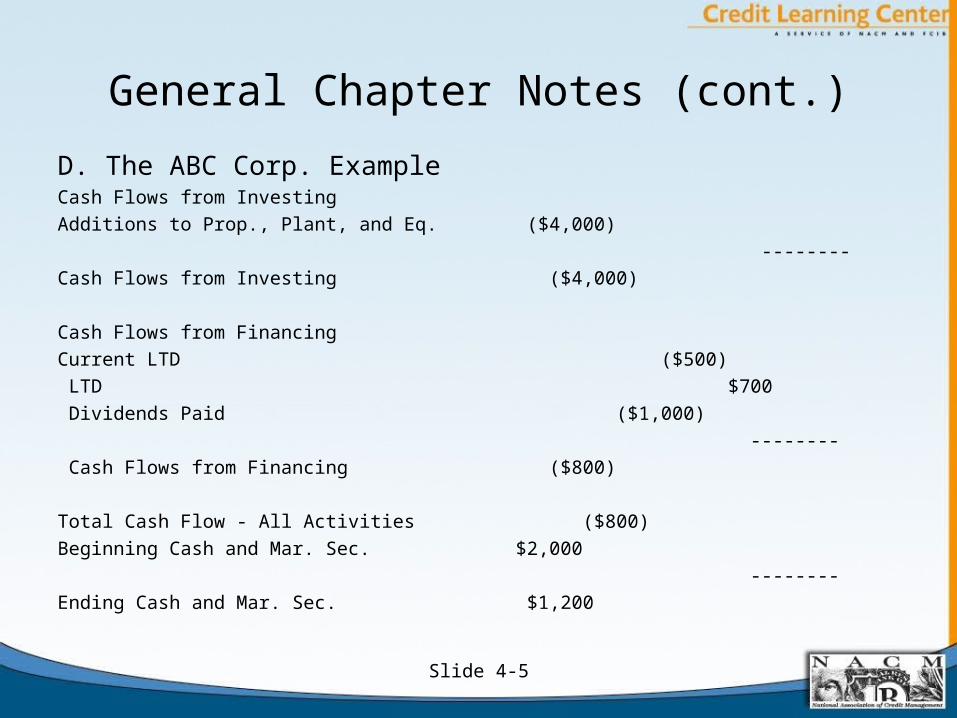

General Chapter Notes (cont.)

D. The ABC Corp. ExampleCash Flows from Investing

Additions to Prop., Plant, and Eq. ($4,000)

--------

Cash Flows from Investing ($4,000)

Cash Flows from Financing

Current LTD ($500)

LTD $700

Dividends Paid ($1,000)

--------

Cash Flows from Financing ($800)

Total Cash Flow - All Activities ($800)

Beginning Cash and Mar. Sec. $2,000

--------

Ending Cash and Mar. Sec. $1,200

Slide 4-5

General Chapter Notes (cont.)

E. Analysis of Cash Flow Statement for ABC – What went on during the year

CF from Operations $4,000

CF from Investing ($4,000)

CF from Financing ($800)

-----------

Net Cash Flow ($800)

F. Liquidity and Cash Flow Analysis1. Cash flow problems in the working capital cycle

2. Cash balance

3. Using cash flow analysis in trade credit decisions

Slide 4-6

Notes for Particular Parts of Chapter 4

A. Accrual Accounting for Income versus Cash Flow

B. Cash Flows as a Result of the Firm’s Decisions and

their Outcomes

C. How Interest on Debt is Treated in FASB 95

D. Income Statement Depreciation, Changes in

Accumulated Depreciation, and CF from Operations

E. Direct and Indirect Methods of Calculating Cash Flows

F. Composite Transactions

Slide 4-7

Notes for Particular Parts of Chapter 4 (cont.)

G. Cash Flow and Trade Credit Granting Decisions

H. Profitable but Out of Cash: Nocash Corp.

1. Credit management and inventory management

2. Effects of rapid growth on financing needs

I. Analysis of Cash Flows for Sage Corp.

J. Summary Analysis of Cash Flows

K. Statement Quality and Cash Flow

L. Limitations of Cash Flow Analysis

Slide 4-8

Dragoon Enterprises

Cash Flows From Operationsnet income $ 1,050

increase in accum. depreciation $ 100

increase in accounts receivable $ (550)

decrease in inventory $ 110

increase in accounts payable $ 300

decrease in acc. wages payable $ (100)

decrease in interest payable $ (50)

increase in taxes payable $ 150 --------

Total Cash Flow From Operations $ 1,010

Slide 4-9

Dragoon Enterprises

Cash Flows from Investing

increase in gross PP&E $ (700) Total Cash Flow From Operations $ 1,010

decrease in long term investments $ 140 Total Cash Flow from Investing $ (560)

-------- Total Cash Flow from Financing $ (100)

Total Cash Flow from Investing $ (560) Total Cash Flow (change in cash) $ 350

Cash Flows from Financing Beginning Cash $ 850

decrease in bonds payable $ (300) Total Cash Flow $ 350

increase in capital stock $ 70 Ending Cash $ 1,200

increase in paid in capital $ 330

dividends paid $ (200)

--------

Total Cash Flow from Financing $ (100)

Slide 4-10

Gerber Scientific

Summary Analysis Statement of Cash Flows

Year 2010 % 2009 % 2008 %

Inflows

Cash Flow from Operations $25,096 19.4% $9,774 7.8% $10,205 3.0%

Sale of Investments $464 0.4% $705 0.6% $751 0.2%

Sale of Net Assets $13,709 10.6% $2,622 2.1% $345 0.1%

Debt Proceeds $89,525 69.3% $110,686 88.8% $321,862 95.8%

Common Stock Activities $898 0.7% $1,373 0.4%

Effect of Exchange Rates $333 0.3% $1,413 0.4%

Total $129,127 100.0% $124,685 100.0% $335,949 100.0%

Slide 4-11

Gerber Scientific

Summary Analysis Statement of Cash Flows

Year 2010 % 2009 % 2008 %

Outflows

Capital Expenditures $4,489 3.5% $8,187 6.4% $8,589 2.6%

Purchases of Investments $308 0.2% $457 0.4% $753 0.2%

Business Acquisitions $3,473 2.7% $34,273 26.7% $4,650 1.4%

Inv. in Intangible Assets $1,368 1.1% $828 0.6% $868 0.3%

Debt Repayments $117,176 91.4% $80,271 62.6% $314,256 95.2%

Debt Issuance Costs $494 0.4% $1,174 0.9% $993 0.3%

Common Stock Activities $486 0.4%

Other Financing Activities $341 0.3%

Effect of Exchange Rates $3,074 2.4%

Total $128,135 100.0% $128,264 100.0% $330,109 100.0%

Slide 4-12