Financial Stability and Payment Systems Report 2010 · Financial Stability and Payment Systems...

36

Financial Stability and Payment Systems Report 2010 1 by Dato’ Mohd Razif Abd. Kadir Deputy Governor 23 March 2011 Financial Stability and Payment Systems Report 2010 Briefing to Analysts & Fund Managers

Transcript of Financial Stability and Payment Systems Report 2010 · Financial Stability and Payment Systems...

Financial Stability and Payment Systems Report 2010

1

byDato’ Mohd Razif Abd. Kadir

Deputy Governor

23 March 2011

Financial Stability and Payment Systems Report 2010

Briefing to Analysts & Fund Managers

Financial Stability and Payment Systems Report 2010

2

Stability of the financial sector was preserved throughout 2010

- strong fundamentals contributed towards efficient financial intermediation

- orderly and efficient conditions in financial markets, and payments and settlements systems facilitated trade and domestic activities

Financial Stability and Payment Systems Report 2010

3

Financial system continues to be resilient

• Strong capital and liquidity buffers

• Improved profitability

• High asset quality

• Have capacity to withstand extreme macroeconomic and financial conditions

Banking Sector (%) 2009 Jan’11Capital Adequacy

Risk-Weighted Capital RatioCore Capital RatioCapital Buffer (RM bil)

15.413.864.6

14.112.460.5

ProfitabilityReturn on AssetsReturn on Equity

1.214.0

1.819.7

Asset QualityNet Non Performing Loan* Ratio 1.8 2.2

Liquidity PositionLiquidity buffer (<1 mth, % of deposits) 18.2 14.8

Insurance/Takaful Sector (%) 2009 2010Capital Adequacy

Capital Adequacy Ratio^Capital Buffer^ (RM bil)

225.718.6

224.618.6

ProfitabilityProfit Before Tax (RM bil) 14.7 16.3

* 2011 position based on impairment methodology ^ Conventional industry only

Financial Stability and Payment Systems Report 2010

4

Banking system recorded RM22.8 bil in pre-tax profit

Conventional Banking System

2010 RM bil

2010 growth

Net interest income 27.5 +15.8%

Fee/Commission-based income

8.1 +11.2%

Net trading & investment gains

7.4 +62.4%

Staff cost and overheads 20.2 +14.4%

Pre-tax profit 19.7 +37.1%

Islamic Banking System

2010 RM bil

2010 growth

Net income 6.8 +12.2%

Fee/Commission-based income

0.7 +13.7%

Net trading & investment gains

0.4 +17.8%

Staff cost and overheads

3.6 +56.1%

Pre-tax profit 3.1 +16.9%

Conventional banking system: PBT of RM19.7 billion

Islamic banking system: PBT of RM3.1 billion

Financial Stability and Payment Systems Report 2010

5

Life insurance & family takaful: Excess of income over outgo of RM14.1 bil

Insurance and takaful sector registered RM16.3 bil in pre-tax profit

2010Life Insurance Family Takaful Total

RM bil growth RM bil growth RM bil growthNet premiums/ contribution 21.9 15.9% 3.3 21.3% 25.2 11.5%Net policy/ certificate benefits 13 9.2% 1.6 75.8% 14.6 14.7%Net Investment income 5.4 10.2% 0.5 42.9% 5.9 11.5%

Net unrealised and capital gains 4.2 44.9% 0.01 -83.3% 4.3 46%

Excess income over outgo 12.7 16.5% 1.4 -15.6% 14.1 12.1%

General insurance & takaful: Operating profits of RM2.2 bil

2010General Insurance General Takaful TotalRM bil growth RM bil growth RM bil growth

Gross direct premiums/ contribution 15.2 8.6% 1.4 26.3% 16.6 10%Net claims incurred 6.8 11.5% 0.5 34.5% 7.3 12.3%Net Investment income 0.8 3.9% 0.1 17.7% 0.9 6.2%Net unrealised and capital gains 0.06 -75% 0.04 96.7% 0.1 -68.1%Operating Profit 1.9 2.7% 0.2 12.5% 2.1 3.8%

Financial Stability and Payment Systems Report 2010

6

Premiums for insurance sector continued to grow, driven by investment-linked and motor businesses

New business premiums for Life and Family Takaful

2.62.22.7

1.91.81.3

4.13.83.5

0

2

4

6

8

10

2008 2009 2010

RM bil

Investment-linked Par-productsNon-Par products Annuity

Gross Premiums for General Insurance and General Takaful

Business

6.05.35.0

2.12.11.9

1.31.21.2

3.43.23.0

0

4

8

12

16

2008 2009 2010

RM bil

Motor FireMAT Others

Financial Stability and Payment Systems Report 2010

7

Manageable trend in payouts of benefits and claims

6.8

0.9

0

1

2

3

4

5

6

7

8

1H 2H 1H 2H 1H 2H

%

Total benefits payments (Life Insurance)

Total benefit payments (Family Takaful)

2008 2009 2010

80.5

70.8

62.5

59.6

40

50

60

70

80

90

100

1H 2H 1H 2H 1H 2H

%

Gen. Insurance (Motor) Gen. Takaful (Motor)Gen. Insurance (Total) Gen. Takaful (Total)

2008 2009 2010

Total benefit payments of RM13 bil or 58.1% of premium

New motor cover framework that is being formulated to preserve access to affordable motor cover while ensuring its sustainability over the longer term

Claims experience in motor continues to remain high

Financial Stability and Payment Systems Report 2010

8

Continued access to financing by all sectors

• Outstanding banking system financing grew by 13.1%

– Continued expansion to all segments, including SMEs

• Bank deposits increased by 9.1%– Loan-to-deposit ratio stable at 81.2%

• Favourable condition since 2H 2010 facilitated fund raising in PDS market

– New corporate debt securities and sukuk issuances of RM76 bil

– Danajamin approved RM4.6 bil worth of guarantees

Financial System: Outstanding Financing1,190.21,145.11,120.11,080.9

0200

400600

8001000

12001400

Mar Jun Sept Jan 2011

RM bil

6

8

10

12

14%

Large Enterprises SMEHousehold OthersDebt securities Annual growth (RHS)

Banking System: Deposits

1,091.41,073.3 1,159.41,113.7

0200400600800

1,0001,2001,400

Mar Jun Sept Jan 2011

RM bil

8

8.2

8.4

8.6

8.8

9

9.2%

Business HouseholdOthers Annual growth (RHS)

Financial Stability and Payment Systems Report 2010

9

Higher new loans to large businesses and SMEs

0

10

20

30

40

50

60

70

80

90

100

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

RM bil

Loans approved - Large BusinessesLoans approved - SMEsLoans approved - Households

20102009

• Outstanding loans to businesses grew 10.1% to RM336.9 bil

– More moderate growth of 2.8% for SME loans

– Adjusting for graduated accounts of business reclassification as large enterprises, SME loans had grew by 11.5%

• Bulk of new approvals to:– Manufacturing (RM22 bil)– Construction (RM25.5 bil)– Wholesale & retail (RM18.9 bil)– Real estate activities (RM18.5 bil)

Ave. 2009: RM71.7 bil

Ave. 2010: RM85.8 bil

Financial Stability and Payment Systems Report 2010

10

Overall financing quality remained intact

4.8

3.2

2.21.8

2.3 2.2

0

1

2

3

4

5

6

2006 2007 2008 2009 2010 Jan-11

Increase in NPLs reflect adoption of impairment methodology since FYE 2010

5.4

4.9

2.32

3

4

5

6

7

8

9

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

%

Large businesses SMEs Households

Stable loans-in-arrears accounted for 4.1% of total loans

0

10

20

30

40

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

RM bil

0

1

2

3

4

5

%

1-<2 month 2-<3 month1-<2 month (% of total loans) 2-<3 month (% of total loans)

Increase in NPLs of large businesses amid adoption of impairment classification under FRS139

2008 2009 2010

2008 2009 2010

• New NPLs average at RM2.4 billion a month

• Loan loss coverage at 90.7%

Financial Stability and Payment Systems Report 2010

11

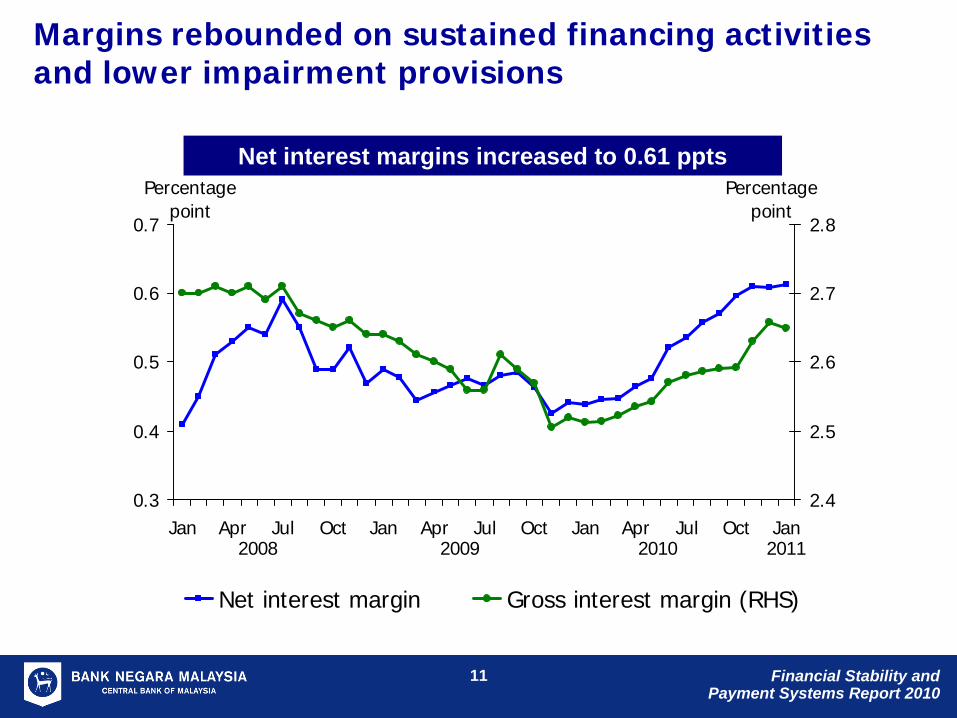

Margins rebounded on sustained financing activities and lower impairment provisions

0.3

0.4

0.5

0.6

0.7

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan2.4

2.5

2.6

2.7

2.8

Net interest margin Gross interest margin (RHS)

Percentage point

Percentage point

2008 2009 2010 2011

Net interest margins increased to 0.61 ppts

Financial Stability and Payment Systems Report 2010

12

Manageable credit risk from business - sustained debt servicing capacity of businesses

Profitability continues to uptrend despite moderating interest-coverage

ratio

5.7

7.5

5.5

9.7

012345678

1Q2009

2Q 3Q 4Q 1Q2010

2Q 3Q 4Q

%

02468101214

Times

ROA (Export-related sectors)ROAInterest coverage ratio (Export-related sectors) (RHS)Interest coverage ratio (RHS)

Year Downgrades Upgrades Ratio

2009 23 11 2.09

2010 22 15 1.47

Leverage position sustained <50%(Debt-to-Equity Ratio)

44.5 45.6

20

30

40

50

60

1Q2009

2Q 3Q 4Q 1Q2010

2Q 3Q 4Q

%

Source: RAM and MARC

Improved downgrade-to-upgrade ratio

*Export-related sectors include timber & wood-based products, textiles & apparels, rubber gloves, plantation & agriculture, packaging materials, O&G, furniture, E&E, chemicals & chemical products

Financial Stability and Payment Systems Report 2010

13

Rising household indebtedness supported by strong financial buffers…

Household Debt-to-GDP Ratio (%)75.976

50

60

70

80

2006 2007 2008 2009 2010

Household debt-to-GDP ratio unchanged at 75.9%

Household financial assets are 2.4 times of household debts

Household Financial Assets, Deposits and Debts

0

200

400

600

800

1,000

1,200

1,400

1,600

2006 2007 2008 2009 20100

50

100

150

200

250

300

Financial Assets (LHS) Debts (LHS)

Fin. Asset-to-Debt Ratio Deposit-to-Debt Ratio

RM billion %

Financial Stability and Payment Systems Report 2010

14

Composition of HH Financial Assets(RM1,386 bil)

Savings with EPF

30%

Unit Trust funds16%

Equity Holdings

17%

Endowment policies

6%

Deposits with FIs

31%

…and high level of liquid assets, while bulk of borrowings are for purchase of assets

Secured financing constitute 64.9% of household debt

Composition of HH Financial Debts(RM581 bil)

Others10%

Purchase of

Securities5%

Auto financing

20%

Personal use15%

Credit Card5%

Housing loan45%

Liquid assets accounted for 64.6% of financial assets

Financial Stability and Payment Systems Report 2010

15

Personal financing grew 17.5% driven by salary deduction scheme

Composition of household debts

15%8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Others Securities Credit cards

Personal use Transport Vehicles Housing Loans

• Personal financing (PF) accounted for 14.6% of household debts

– Personal financing by banks grew at lower rate of 13%

– Account for less than 5% of banks’ loans

– NPL ratio of 2.5%

• Driven by development financial institutions, cooperatives and building societies

– Approx. 80% under salary deduction schemes

Financial Stability and Payment Systems Report 2010

16

Household NPLs Ratio (%)

3.2

1.22.51.9

0.70123456789

2007 2008 2009 2010

Overall Housing loansCar financing Personal useCredit cards Purchase of securities

Household loan quality remained intact

• Debt servicing capacity of households remains sound

– Delinquencies continued to improve– Banking system gross NPL ratio:

2.3% (2009: 3.1%)– LIAs at 4.7% of total banking system

loans

• Banks maintain prudent loan underwriting standards and risk management practices

• Supported by comprehensive credit information system and infrastructure

Household Loans in Arrears Ratio (%)

3.9

8.35.9

2.81.80

2468

101214

2007 2008 2009 2010

Financial Stability and Payment Systems Report 2010

17

Comprehensive and pre-emptive strategies to preserve household sector resilience

Prudential policies

•Loan-to-value ratio of 70% applied to 3rd housing loans onwards

•New credit card guidelines •Higher minimum income eligibility from RM18k to RM24k per annum

•Limit on no. of cards and credit limit for cardholders earning <RM36k per annum

•Increased risk-weights for housing loans with LTV >90% and personal financing with tenure >5 years

Intensive supervisory oversight

Standards on prudent and responsible lending practices

- Suitability and affordability assessments

Targeted financial education programme by AKPK

- Including advisory and support arrangements

Financial Stability and Payment Systems Report 2010

18

Ensuring prudent and responsible conduct for retail financing as part of measures to preserve household sector resilience

• Inculcate responsible lending practices by financial institutions in dealing with retail customers

• Requirements NOT intended nor expected to hamper credit availability

• Key requirements include– Suitability and affordability assessment– Verification of customers' income– Product disclosure sheet to facilitate informed decision making– Compensation of sales and marketing personnel to take into account fair dealing

conduct

• Complete submissions should not result in processing delays

Financial Stability and Payment Systems Report 2010

19

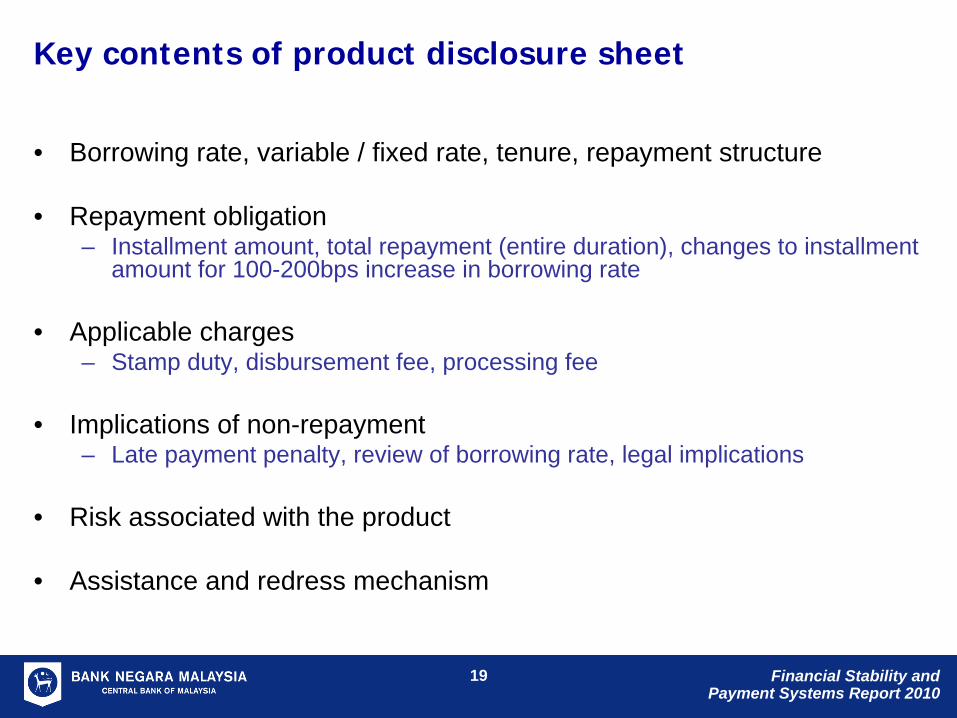

Key contents of product disclosure sheet

• Borrowing rate, variable / fixed rate, tenure, repayment structure

• Repayment obligation– Installment amount, total repayment (entire duration), changes to installment

amount for 100-200bps increase in borrowing rate

• Applicable charges – Stamp duty, disbursement fee, processing fee

• Implications of non-repayment – Late payment penalty, review of borrowing rate, legal implications

• Risk associated with the product

• Assistance and redress mechanism

Financial Stability and Payment Systems Report 2010

20

Financial markets exhibited enhanced capacity to intermediate larger and more volatile portfolio flows

Volatility of asset prices remained low

90-day volatility (%)

0

5

10

15

20

25

30

35

40

Jan-08

Apr-08

Jul-08

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

KLCI MGS (5-year yield) [RHS]

Lehman collapse

European sovereign debt crisis

Returns-to-turnover ratio was lower, denoting higher

resilience

Ratio

0.000

0.004

0.008

0.012

0.016

0.020

Jan-08

Apr-08

Jul-08

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

0

0.1

0.2

0.3

0.4

FBM KLCI MGS [RHS]

Ratio

Avg 2010: 0.04

Avg 2010: 0.006

Source: Bloomberg

Financial Stability and Payment Systems Report 2010

21

Portfolio inflows channeled to more diversified asset classes

Bulk of inflows into debt securities with rising equity participation

5

7

9

11

13

15

17

19

M J S D M J S D

%

19

20

21

22

23%

Debt securities as % of outstandingEquities as % of market capitalisation (RHS)

Strong increase in non-residents' holdings of KLCI and CPO futures

15

20

25

30

35

40

45

M J S D M J S D

%

10

15

20

25

30

35%

KLCI futures as % of number of contractsCPO futures as % of number of contracts (RHS)

2009 2010 2009 2010

Financial Stability and Payment Systems Report 2010

22

No material changes in risk-taking by FIs

(RM bil) 2008 2009 2010Dealing Securities

51.7 46.4 69.2

Investment Securities

163.5 199.3 201.6

Shares 1.8 2.2 3.1MGS 61.4 90.7 84.0BNM Debt

15.3 14.0 47.2

PDS 59.2 60.1 59.9

(RM bil) 2008 2009 2010

Investment Securities

72.2 87.8 101.7

Shares 12.4 20.0 21.3

MGS 16.2 15.7 22.1

BNM Debt

0.09 0.02 1.23

PDS 43.6 52.1 57.0

• Trading portfolio of banks grew 49.2% in 2010

– Due primarily to higher holdings of BNM papers (+237.1%)

Banking System: Securities Portfolio Insurance Sector: Securities Portfolio

• Equity holdings increased slightly to 16.5% of assets (2009: 13.5%)

• Helps reduce mismatch in returns

Financial Stability and Payment Systems Report 2010

23

Rise in market risk exposures of FIs is manageable

Banking system: Market Risk Exposure

(as % of Capital Base)

0

2

4

6

8

Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec

Equity holdingsForeign currency net open positionDuration weighted net position (interest rate risk)

2008 2009 2010

%

• FCY exposures edged up to 3.8% of capital base, more active hedging by customers

– Stable FCY deposits from non-residents

Insurance sector:

Components of Market Risk

Financial Stability and Payment Systems Report 2010

24

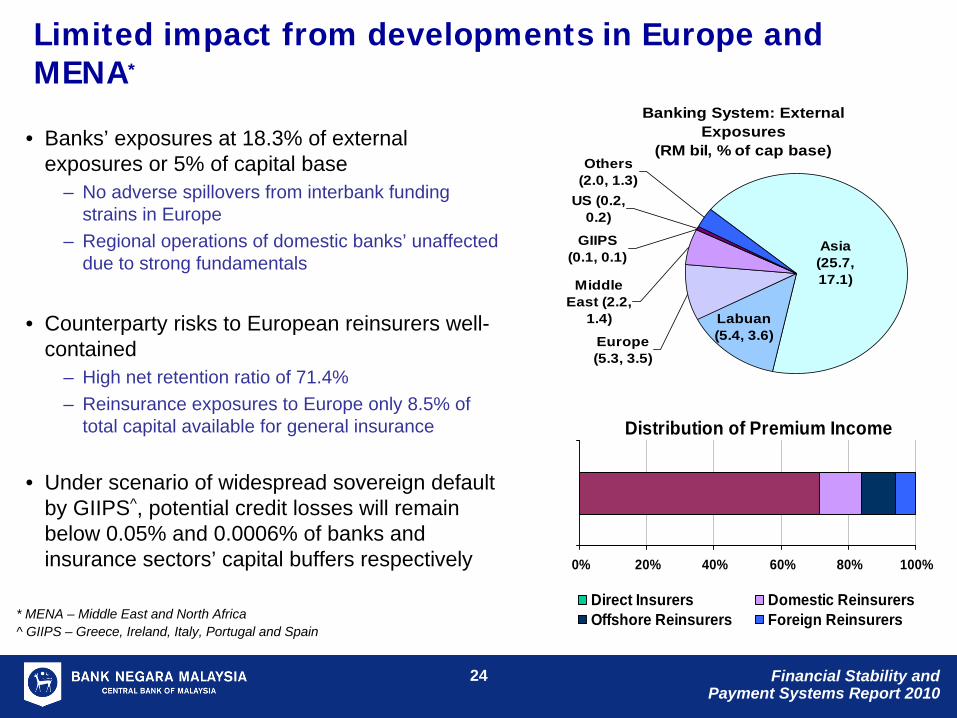

Limited impact from developments in Europe and MENA*

• Banks’ exposures at 18.3% of external exposures or 5% of capital base

– No adverse spillovers from interbank funding strains in Europe

– Regional operations of domestic banks’ unaffected due to strong fundamentals

• Counterparty risks to European reinsurers well- contained

– High net retention ratio of 71.4%– Reinsurance exposures to Europe only 8.5% of

total capital available for general insurance

• Under scenario of widespread sovereign default by GIIPS^, potential credit losses will remain below 0.05% and 0.0006% of banks and insurance sectors’ capital buffers respectively

Banking System: External Exposures

(RM bil, % of cap base)

GIIPS (0.1, 0.1)

US (0.2, 0.2)

Others (2.0, 1.3)

Asia (25.7, 17.1)Middle

East (2.2, 1.4)

Europe (5.3, 3.5)

Labuan (5.4, 3.6)

Distribution of Premium Income

0% 20% 40% 60% 80% 100%

Direct Insurers Domestic Reinsurers Offshore Reinsurers Foreign Reinsurers* MENA – Middle East and North Africa

^ GIIPS – Greece, Ireland, Italy, Portugal and Spain

Financial Stability and Payment Systems Report 2010

25

Domestic banking groups have presence in 19 countries worldwide with a higher

share of overseas assets and income

MBB, RHB, Public, HL

MBB

MBB, CIMB, RHB, HL, AM

MBB, CIMB, AM

CIMB, RHB

Public

CIMB

MBB, CIMB, Public

MBB, CIMB, Public, HL, AM

MBB, CIMB, Public, HL

Expanded overseas presence of domestic banking groups in East Asia

Malaysian financial institutions have continued to strengthen their regional presence

Intensified domestic competition

Rising needs of internationalisation of local firms

Greater trade & investment linkages

Growth opportunities in new markets

Key Drivers for Expansion Abroad

2002 2010Assets RM3.3

bilRM258

bil

Revenue -4.3% 16.7%*

* 2009

Enhanced capacity to expand overseas

Financial Stability and Payment Systems Report 2010

26

Overseas operations remained well capitalised

Banking System: Assets of Overseas Operations

(and # of establishments)

0

20

40

60

80

100

120

Sing

apor

e

Indo

nesi

a

Chin

a

Labu

an

Hon

gKo

ng

Thai

land

Oth

ers

RM bil

6

4

3

9 72 19

SMEs39%

Personal6%

Others12%

Mortgage13%

Corporate30%

Banking System: Loan Composition of Overseas Operations

Key Financial Soundness Indicators

RWCR: 11.9% - 33.6%Overall NPL ratio: 3.3%

Overall RoA: 1.0%

Financial Stability and Payment Systems Report 2010

27

Islamic banks: Effective management of displaced commercial risk

• Total deposits grew 15.7% to RM218.4 bil– 33% of deposits are

mudharabah general investment accounts

• Active management of displaced commercial risk – Profit equalisation reserves of

RM126.6 mil

Profit Equalisation Reserve

0

50

100

150

200

250

300

350

J A J O J A J O J A J O J A J O J

RM mil

2007 2008 2009 2010

Financial Stability and Payment Systems Report 2010

28

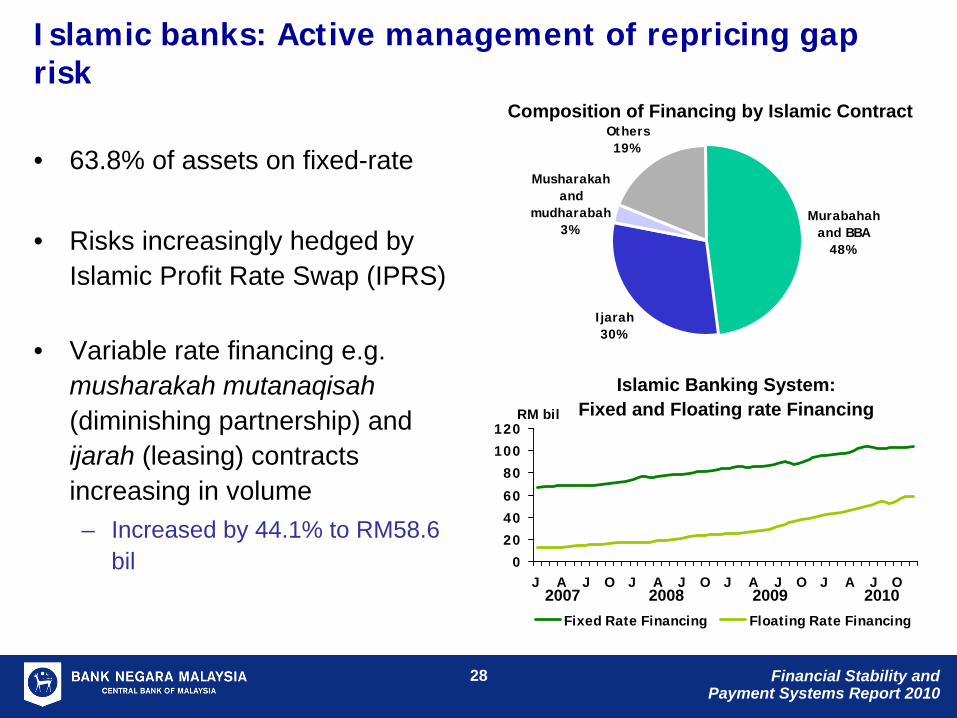

Islamic banks: Active management of repricing gap risk

• 63.8% of assets on fixed-rate

• Risks increasingly hedged by Islamic Profit Rate Swap (IPRS)

• Variable rate financing e.g. musharakah mutanaqisah (diminishing partnership) and ijarah (leasing) contracts increasing in volume– Increased by 44.1% to RM58.6

bil 0

20

40

60

80

100

120

J A J O J A J O J A J O J A J O

RM bil

Fixed Rate Financing Floating Rate Financing

Islamic Banking System: Fixed and Floating rate Financing

2007 2008 2009 2010

Murabahah and BBA

48%

Ijarah30%

Musharakah and

mudharabah3%

Others19%

Composition of Financing by Islamic Contract

Financial Stability and Payment Systems Report 2010

29

Strengthened governance and decision making framework for financial stability

Financial Stability Executive

Committee• High level committee

established under s.37 of CBA 2009 to review and decide on the Bank’s recommendations to manage risks to financial stability

• Entities outside regulatory perimeter of the Bank

• Resolution of systemically important financial institutions

• Involves public funds

Financial Stability Policy Committee (within the Bank)

• Maintaining price stability while giving due regard to the developments in the economy

• Formulation of monetary policy and policies for the conduct of monetary policy operations

• Risk assessment• Macroprudential responses• Microprudential responses • Supervisory interventions

Recommendations with systemic implications

Monetary Policy Committee

(within the Bank)

Joint meeting for effective deliberation and consideration of macroprudential measures to

safeguard financial and macroeconomic stability

Resolution of individual FI by PIDM

Financial Stability and Payment Systems Report 2010

30

Foundations for financial stability were further strengthened

Enhanced robustness of risk

management, stress testing and

capital management

More effective governance in

financial institutions

Strengthened cross- border supervisory

cooperation

Strengthened prudential standards for Islamic

finance

Enhanced protection for depositors and policyholders

Adoption of more advanced capital approaches under

Basel II

Financial Stability and Payment Systems Report 2010

31

Share premium

14.6%Ordinary

share capital22.9%

Retained profits19.5%

Others6.1%

Stat reserve fund14.9%

General provisions

7.1%

Sub debt capital14.8%

Composition of Insurance and Takaful Sector Capital

High quality capitalisation with >RM80 bil financial buffers

Composition of Banking Sector Capital

Valuation surplus in

fund30%

Retained profits

11%

Tier-2 less deductions

10%

50% of future

bonuses35%

Fully paid up capital

11%

Share premiums

3%

More than 70% of the financial sector’s total capital comprise of equity, reserves and retained profits

Financial Stability and Payment Systems Report 2010

32

Malaysian banking system well-positioned to meet Basel III requirements

• Strong and high quality of bank capital

• Minimum liquidity standards have been in place since 2000– Banks to further strengthen buffers going forward– Currently, banks have liquidity buffer of 14.8% (maturities <1 month)

• Implementation strategy for Basel III to be communicated to industry in 2011– Consider specific characteristics of domestic market– Minimise impact on bank lending and economic growth

Common equity

Tier 1 capital

Total capital Leverage

Minimum requirement 4.5% 6% 8% 3%Minimum requirement + conservation buffer 7% 8.5% 10.5% -

Estimated current position of banking system 9.3% 10.8% 14.5% 5.9%

Financial Stability and Payment Systems Report 2010

33

Malaysian financial sector increasingly integrated with the global financial system facilitating our economic linkages with the world

Financial Liberalisation

Collaborative Arrangements

Free Trade Agreements

Various Avenues for Increased

Internationalisation of the Malaysian Financial Sector

Push for areas that can further interests of Malaysian financial institutions overseas

Regulatory & supervisory cooperation

Capacity building & human capital development

Currency swap agreements

New players with significant value propositions to contribute to economic and financial developmentIncreased diversity of financial institutions operating onshoreLiberal foreign exchange policies to facilitate foreign investment

Ensure sufficient safeguards to preserve economic & financial stability

+ 4 new family takaful licences were issued on 1 Sept 2010

Financial Stability and Payment Systems Report 2010

3434

Malaysia maintains a leading role in development of Islamic finance

Malaysia tops global league tables in sukuk equity and fund management

Source: “Gateway to Asia: Malaysia, international Islamic finance hub” by Pricewaterhouse Coopers 2010

…and home to largest sukuk market

Global Sukuk Outstanding by Country*USD148 billion

*Source: Bloomberg Professional Services Terminal, as at end-2010

Malaysia66%

Indonesia4%

Offshore Centres

16%

Others1%

Saudi7%

Bahrain2%

UAE4%

Singapore0.1%

(USD94 billion)

Financial Stability and Payment Systems Report 2010

35

Outlook for domestic financial stability in 2011 remains positive

• Risks to financial stability largely externally driven

• Pre-emptive measures and strong financial buffers ensure that financial system is well-placed with capacity and flexibility to respond to emerging risks

• Macrosurveillance and supervisory activities in 2011 will focus on:– Ensuring prudent and responsible risk-taking and market conduct by FIs– Ensuring resilience and robustness of major payment and settlement systems– Active engagement in global regulatory and accounting reforms– Further strengthening of regulatory laws and prudential guidelines– Promoting closer domestic, regional and global cooperation and coordination

Financial Stability and Payment Systems Report 2010

36

Moving forward…

The new financial sector blueprint will build on the strong foundations of the Malaysian financial system to:

– remain resilient in withstanding any potential disruptions in the financial system and broader economy;

– to best serve the needs of a high value-added and high income economy;

while further promoting financial inclusion and regional financial integration.