Financial ServiceS - Roland...

14

Focus Digital reengineering as a cost-cutting lever Business RETAIL BANKING Dutch consumers do not yet trust their banking to tech companies INSURANCE Customer retention: major challenge for 2016 BANKING The state of the top three Dutch banks: 2014 financial performance assessment International AFRICA Growing opportunities for corporate and investment banking activities FINANCIAL SERVICES Newsletter NETHERLANDS EDITION | Q1 2016

Transcript of Financial ServiceS - Roland...

FocusDigital reengineering as a cost-cutting lever

BusinessRETAIL BANKINGDutch consumers do not yet trust their banking to tech companies

INSURANCECustomer retention: major challenge for 2016

BANKINGThe state of the top three Dutch banks: 2014 financial performance assessment

InternationalAFRICAGrowing opportunities for corporate and investment banking activities

FinancialServiceSNewsletter

neTHerlanDS eDiTiOn | Q1 2016

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger2

This not only concerns the exploitation of customer data and commercial development – digital technology is also a key cost-cutting lever. Beyond “traditional” cost-cutting measures such as abandoning activities that have become less useful, outsourcing or implementing shared services, digital technology can help to achieve additional cost savings in the range of 30% to 40%.

Based on our experience, we have identified five main levers for digital reengineering. These primarily apply to business processes, be it subscription processes, administration or claims handling.

1. NATIVE DEMATERIALIZATIONThis involves working without paper, either by getting the employee to carry out an activity directly within an IT tool or by scanning the paper document and managing it using a digital image. As well as reducing the cost of the process, dematerialization improves customer satisfaction, makes risks easier to trace and increases the effectiveness of fraud management.

2. AUTOMATION OF DECISION-MAKINGDecision-making algorithms are implemented for simple or standard processes. For example, this is what many reinsurers do for provident insurance subscription. 70% of these policies are processed without human intervention. Shorter waiting times have resulted in a reduction in drop-out rates from 27% to 12%.

FOCUSDigital reengineering

as a cost-cutting lever

Digital reengineering as a cost-cutting leverFintechs are all the rage. Banks and insurance companies are increasingly striving to connect with start-ups, to invest in them, or even to become operators of them. Exploiting digital technology to launch new activities is pertinent, and capitalizing on this to transform existing business is equally relevant.

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger3

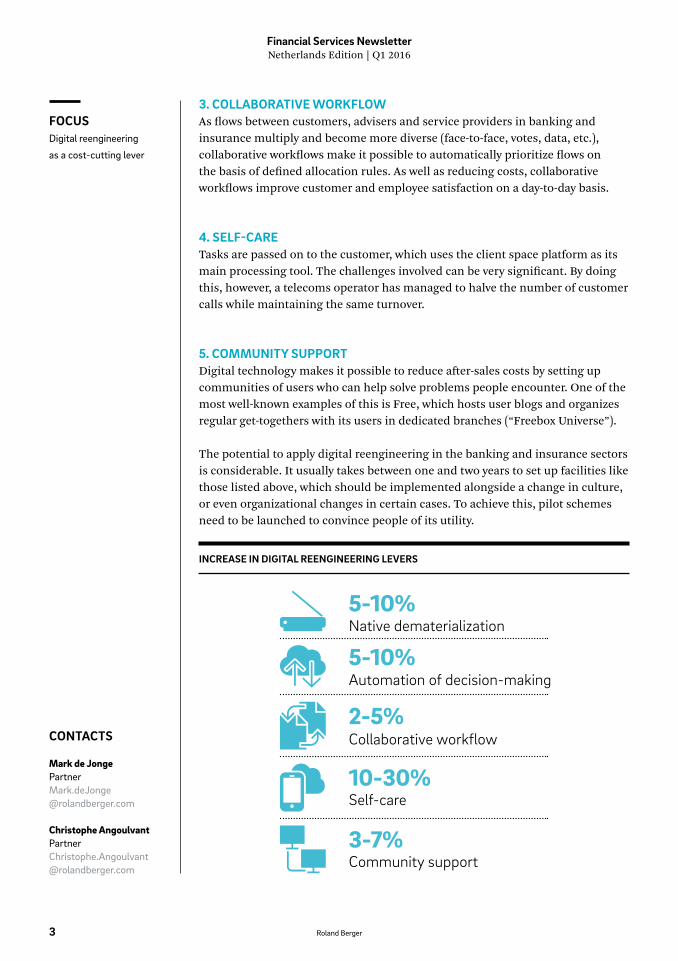

3. COLLABORATIVE WORKFLOWAs flows between customers, advisers and service providers in banking and insurance multiply and become more diverse (face-to-face, votes, data, etc.), collaborative workflows make it possible to automatically prioritize flows on the basis of defined allocation rules. As well as reducing costs, collaborative workflows improve customer and employee satisfaction on a day-to-day basis.

4. SELF-CARETasks are passed on to the customer, which uses the client space platform as its main processing tool. The challenges involved can be very significant. By doing this, however, a telecoms operator has managed to halve the number of customer calls while maintaining the same turnover.

5. COMMUNITY SUPPORTDigital technology makes it possible to reduce after-sales costs by setting up communities of users who can help solve problems people encounter. One of the most well-known examples of this is Free, which hosts user blogs and organizes regular get-togethers with its users in dedicated branches (“Freebox Universe”).

The potential to apply digital reengineering in the banking and insurance sectors is considerable. It usually takes between one and two years to set up facilities like those listed above, which should be implemented alongside a change in culture, or even organizational changes in certain cases. To achieve this, pilot schemes need to be launched to convince people of its utility.

CONTACTS

Mark de [email protected]

christophe [email protected]

INCREASE IN DIGITAL REENGINEERING LEVERS

Native dematerialization5-10%

Automation of decision-making5-10%

Community support3-7%

Collaborative workflow2-5%

Self-care10-30%

FOCUSDigital reengineering

as a cost-cutting lever

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger4

This was the conclusion of a study that Roland Berger and Visa Europe conducted among 1000 consumers through the market researcher GfK. The study revealed that consumers appreciate new technologies, but that security is number one. As a result, the much-anticipated disruption to existing retail banks seems further away than we thought.

The study had another important message for banks: in order to understand the current needs of today’s banking client, their traditional segmentation between income, wealth and purchased financial products is no longer sufficient. This traditional segmentation throws everyone who look the same on paper together in one pile, but they actually want to handle their affairs differently. Clients want service that matches their “digital affinity” – the use of mobile banking is a strong indicator of this.

THE BRANCH IS STILL IMPORTANTDespite the technological developments underway in the banking world, consumers continue to value face-to-face contact at the branch. Interestingly enough, this is especially important for the younger generations. Less than one-fifth of 18-29 year olds believe that a telephone call or contact via webcam can replace a visit to the bank, while a quarter of 30-49 year olds think they can. Two-thirds of the sales of complex financial products (mortgages or personal loans) take place at the branch. No less than 57 percent of the younger genera-tions would not become a client at a digital-only bank.

BUSINESSRetail banking

Dutch consumers do not

yet trust their banking to

tech companies

Dutch consumers do not yet trust their banking to tech companies Only one in ten Dutch consumers would entrust tech companies like Google or Facebook with their banking. The majority of Dutch consumers highly values personal contact and security during their interactions with banks – only at that point can innovation come into play.

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger5

CONTACTLESS PAYMENTS ARE NOT POPULAR YET The study also revealed that consumers put more trust in traditional payment methods than in new ones. To pay at a checkout, those surveyed trust pinning the most: 91% consider this secure. Cash and credit cards follow. Contactless payments with a card came in in fourth place at 28%. Trust in a new payment method always has to build up at first. Most of the time, trust follows use – and the use of contactless payment is growing by dozens of percentage points every month. Nevertheless, there will always be a group of consumers who prefer cash. A small group, but one we should not forget.

CONTACT

Sjors van der ZeeProject [email protected]

Sameer [email protected]

BUSINESSRetail banking

Dutch consumers do

not yet trust their banking

to tech companies

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger6

For traditional insurers with significant car and home insurance portfolios, the main challenge in 2016 will be to increase their customer retention capacity. The implementation of a specific customer retention scheme is generally a prerequisite for this. This scheme can be built around four axes:

1. CUSTOMER LOYALTYMeasuring “hot” and “cold” customer satisfaction (e.g. NPS) forms the basis of a customer loyalty system, which can be used to implement measures to improve customer satisfaction on an ongoing basis. Cross-functional initiatives can rein-force these measures: loyalty programs, loyalty contracts, systematic “cocooning” of new customers, etc. And not to forget multi-service offers, which are still the main source of customer loyalty.

2. DETECTION AND PREVENTIONThe implementation of a dynamic system to detect at-risk customers (fragility scores, predictive attrition models, etc.) and high-value customers makes it possible to deploy specific customer loyalty measures on a targeted and profit-able basis, measures that anticipate these customers’ demands. To establish this detection system, the insurer’s internal data (in particular any customer interaction data) must be exploited on a large-scale. External data, such as data concerning the monitoring of customers’ online activity, makes it possible to increase the performance of predictive attrition scores significantly.

BUSINESSInsurance

Customer retention:

major challenge for 2016

Customer retention: major challenge for 2016Many industry players are stepping up their marketing and sales activities to acquire new customers. Price-comparison service providers’ advertising expenditure is expected to rise sharply, bank insurers will leverage the amount of time they spend interacting with their customers and launch campaigns to sell insurance, brokers will expand their capacity to transform leads, and more.

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger7

The profitability of a loyalty system largely depends on the capacity to finely calibrate the level of investment in prevention measures (e.g. modification of guarantees, changes to pricing, additional services, etc.) based on attrition risk and the value of the customer.

3. CONSERVATIONCustomers in the process of terminating their contracts can often be retained with aggressive offers. This calls for a capacity to deal with customer announcements (oral and written) in a systematic and responsive manner, by understanding the reasons why they are leaving and putting forward a modified value proposition (offers with improved conditions, new relationship channels, etc.). Here, too, understanding the value of the customer makes it possible to calibrate the measures to be implemented to retain said customer.

4. RECAPTURINGLost customers can sometimes be recaptured the following year, especially by using prior knowledge of these customers and the reasons why they left. To this end, customer databases need to be maintained after termination and campaigns to “recontact” former customers need to be organized via services adapted to specific needs.

The four axes will help to accelerate the “customer-centric” transformation of insurers. A major rethink of traditional customer retention methods is required to convert these into genuinely structured and cross-functional business mechanisms and to fully exploit the improvement in customer knowledge brought about by the digital wave and analytics.

CONTACT

Sjors van der ZeeProject [email protected]

BUSINESSInsurance

Customer retention:

major challenge for 2016

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger8

Like ABN AMRO, ING and Rabobank, the peer group banks have strong market shares in their respective domestic markets. These ten banks also focus on retail, private banking and commercial clients, and are larger universals under ECB su-pervision. The 2014 financial performance of all thirteen banks was measured by looking at return on equity (ROE), which was broken down into a driver tree that assessed operational profitability and equity leverage in detail. Financial perfor-mance was thus measured in two ways: a bank’s performance relative to the peer group, and a bank’s development relative to 2013, the previous year (figure 1).

RETURN ON EqUITYAveraged together, the top three Dutch banks saw a 2014 ROE at 7.2%, falling within the peer group ROE average and marking a 1.6% improvement over 2013. The driver tree results indicate, however, that their combined ROE is driven by relatively low profitability compensated by high leverage.

BUSINESSBanking

The state of the top

three Dutch banks: 2014

financial performance

assessment

FIGURE 1. FINANCIAL CHECKUP: BANK PERFORMANCE RELATIVE TO PEERS AND BANK YOY

DEVELOPMENT RELATIVE TO 2013

The state of the top three Dutch banks: 2014 financial performance assessmentEach year, Roland Berger Amsterdam gauges the financial state of the Dutch banking sector by looking closely at its top three performers – ABN AMRO, ING and Rabobank – compared to a peer group of similar banks across Europe.

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger9

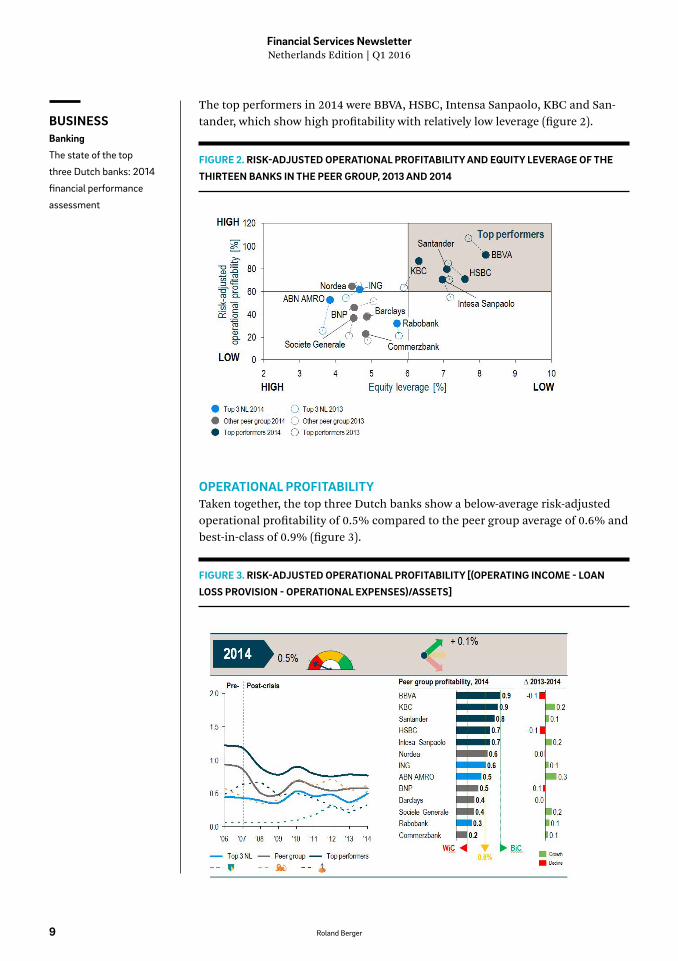

The top performers in 2014 were BBVA, HSBC, Intensa Sanpaolo, KBC and San-tander, which show high profitability with relatively low leverage (figure 2).

OPERATIONAL PROFITABILITYTaken together, the top three Dutch banks show a below-average risk-adjusted operational profitability of 0.5% compared to the peer group average of 0.6% and best-in-class of 0.9% (figure 3).

FIGURE 2. RISK-ADjUSTED OPERATIONAL PROFITABILITY AND EqUITY LEVERAGE OF THE

THIRTEEN BANKS IN THE PEER GROUP, 2013 AND 2014

FIGURE 3. RISK-ADjUSTED OPERATIONAL PROFITABILITY [(OPERATING INCOME - LOAN

LOSS PROVISION - OPERATIONAL ExPENSES)/ASSETS]

BUSINESSBanking

The state of the top

three Dutch banks: 2014

financial performance

assessment

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger10

This is driven mainly by relatively lower non-interest income generation: F&C, fi-nancial and other income are below average, and the net interest margin, though slightly above average, does not compensate for the lack of non-interest income. Their comparatively lower income levels are only partly compensated by relatively lower operational expenses, resulting in below-average profitability overall.

However, while the peer banks’ profitability levels have dropped sharply since 2006, the Dutch levels have remained relatively stable thanks to their strong cost control measures and stable operational income levels compared to the peer group.

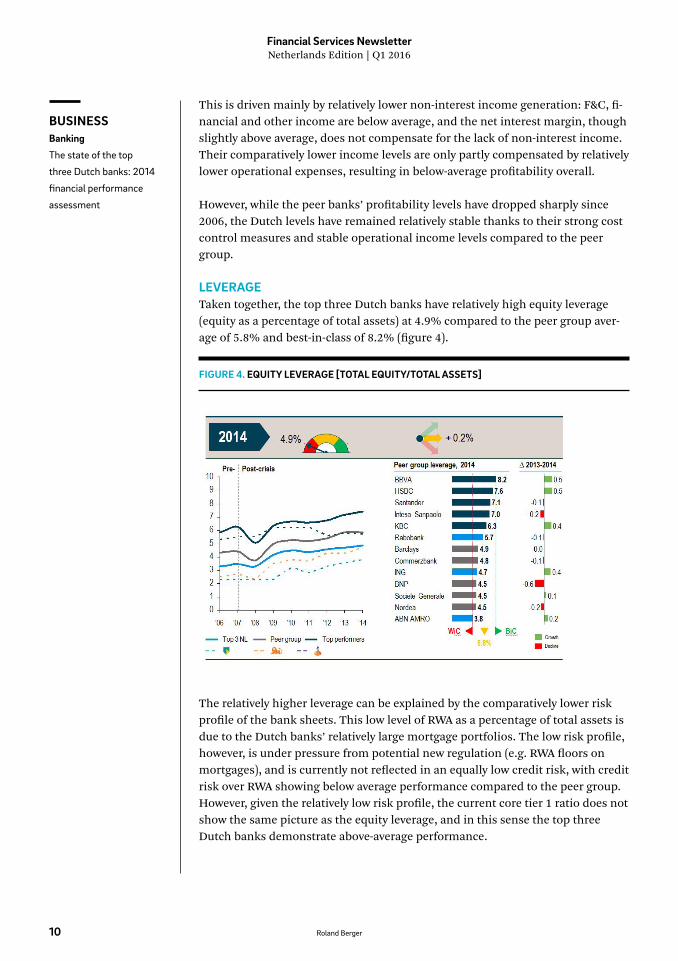

LEVERAGETaken together, the top three Dutch banks have relatively high equity leverage (equity as a percentage of total assets) at 4.9% compared to the peer group aver-age of 5.8% and best-in-class of 8.2% (figure 4).

The relatively higher leverage can be explained by the comparatively lower risk profile of the bank sheets. This low level of RWA as a percentage of total assets is due to the Dutch banks’ relatively large mortgage portfolios. The low risk profile, however, is under pressure from potential new regulation (e.g. RWA floors on mortgages), and is currently not reflected in an equally low credit risk, with credit risk over RWA showing below average performance compared to the peer group. However, given the relatively low risk profile, the current core tier 1 ratio does not show the same picture as the equity leverage, and in this sense the top three Dutch banks demonstrate above-average performance.

BUSINESSBanking

The state of the top

three Dutch banks: 2014

financial performance

assessment

FIGURE 4. EqUITY LEVERAGE [TOTAL EqUITY/TOTAL ASSETS]

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger11

The top three Dutch banks do, however, have a relatively high loan-to-deposit ra-tio, and as a result a higher dependency on capital market funding. This, like the low risk profile, can put pressure on the overall performance of the Dutch banks once all banks need to comply with the new liquidity regulation and are bench-marked on the new Basel III liquidity ratios.

PROFITABILITY AND LEVERAGE STRATEGYCurrent performance and stricter regulations will require Dutch banks to reduce their equity leverage levels and improve liquidity. Because of their relatively low profitability levels, the Dutch banks will therefore need to develop a comprehen-sive strategy that tackles the P&L and balance sheet by building on six main improvement measures:

1. Decrease the high exposure of mortgages (given the future increase in RWA)2. Increase deposit levels in line with stricter liquidity regulation3. Fine-tune risk-based pricing in line with new regulation and the credit risk

profile4. Monetize high online banking penetration and further improve efficiency5. Focus on primary bank clients to optimize costs versus income6. Improve and variabilize F&Cs to award good and penalize bad client behavior

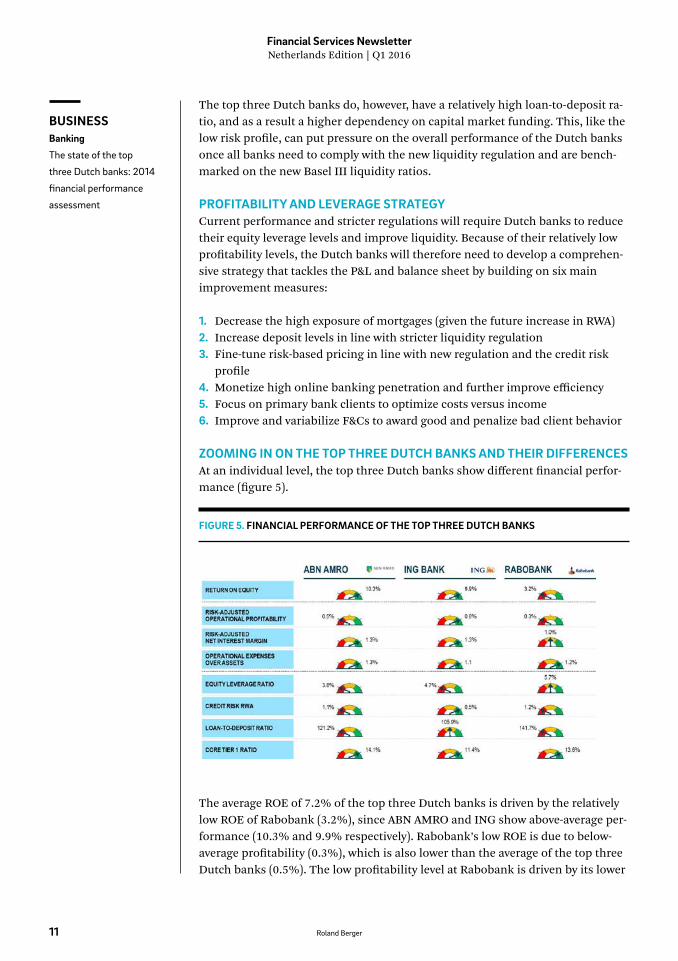

ZOOMING IN ON THE TOP THREE DUTCH BANKS AND THEIR DIFFERENCESAt an individual level, the top three Dutch banks show different financial perfor-mance (figure 5).

The average ROE of 7.2% of the top three Dutch banks is driven by the relatively low ROE of Rabobank (3.2%), since ABN AMRO and ING show above-average per-formance (10.3% and 9.9% respectively). Rabobank’s low ROE is due to below-average profitability (0.3%), which is also lower than the average of the top three Dutch banks (0.5%). The low profitability level at Rabobank is driven by its lower

BUSINESSBanking

The state of the top

three Dutch banks: 2014

financial performance

assessment

FIGURE 5. FINANCIAL PERFORMANCE OF THE TOP THREE DUTCH BANKS

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger12

CONTACT

Frank SchrijverProject [email protected]

net interest margin compared to ABN AMRO and ING (1.0% versus 1.3%). In ad-dition, Rabobank has a slightly lower leverage than ABN AMRO and ING and therefore receives less compensation to offset its relatively low profitability.

Although ABN AMRO and ING have comparable ROEs, the reasons behind their above-average performance are different. ABN AMRO has a relatively low opera-tional profitability compared to ING (0.5% versus 0.6%), but has a higher lever-age (3.8% versus 4.7%) and as a result a slightly higher ROE (10.3% versus 9.9%). The higher leverage of ABN AMRO is not directly reflected in lower credit risk over RWA (1.1% versus 0.5%) or loan-to-deposit ratio (121.2% versus 105.9%), therefore the ROE of ING seems to be a result of more balanced performance. This could indicate that the ROE of ABN AMRO is under increased pressure from new and stricter RWA and capital regulation.

BUSINESSBanking

The state of the top

three Dutch banks: 2014

financial performance

assessment

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger13

The time is right for the development of corporate and investment banking activities in Africa. Against the backdrop of strong economic growth and the recent decline in revenue from natural resource income, African countries are facing a heightened need for financing to drive their development.

Several channels are helping to accelerate the transformation of the financial services sector: development of local capital markets, increased demand for more sophisticated banking services, and public initiatives to develop financial culture and expertise.

RISK OF GROWTH LOSING STEAM – ALTERNATIVE FINANCING METHODS ARE NEEDEDThe decline in commodity prices, and especially that of oil in 2015, has called into question the financing choices made by certain African countries such as Nigeria, Algeria, Angola, and even the CEMAC nations. These countries, which largely finance their investment plans on the basis of own funds, are now facing the risk of their growth losing steam due to a lack of investment financing. Alternative financing methods allowing access to new resources are vital. In addi-tion to the needs of governments, local private enterprises, which traditionally favor self-financing or bank financing whenever they are able to access it, are suffering from a lack of long-term resources needed to finance their major development projects.

NUMEROUS OPPORTUNITIES FOR CORPORATE AND INVESTMENT BANKING PLAYERS IN A MARKET ESTIMATED AT EUR 14-17 BILLIONThe African market offers opportunities for corporate and investment banking industry players:

→→ In→bank→financing: project financing (PPP, infrastructure), private equity investment financing. The lack of infrastructure deprives the African continent of 45% of its potential growth, and there are numerous opportunities for financing in this field.

INTERNATIONALAfrica

Growing opportunities for

corporate and investment

banking activities

Growing opportunities for corporate and investment banking activities

Financial Services NewsletterNetherlands Edition | Q1 2016

Roland Berger14

As an example, more than 35 African countries have benefited from infrastruc-ture financing provided by China since 2000.

→→ Based→on→market→financing: advisory activities (ECM, DCM, M&A), secondary market activities (African shares and fixed income, commodities, currency hedging, etc.), mediation activities. The capital markets are experiencing strong growth in Africa. For example, we have estimated that the Central African market may reach a size of close to EUR 1.3 billion in 2020 if appropriate measures are implemented.

THE DEVELOPMENT OF AN ECOSYSTEM THAT FAVORS THE CAPITAL MARKET: POTENTIAL MARKET FINANCING REPRESENTING NEARLY 10% OF GDPCorporate and investment banking activities in Africa are driven by the desire of certain governments to develop an ecosystem that favors the capital markets, in particular by:

→→ Developing→national→and→regional→stock→exchanges (BRVM in West Africa, BVMAC and DSX in Central Africa) with the implementation of ambitious programs to make them more dynamic

→→ Creating→regulations that favor the development of market activities and tax incentives for issuers and investors

→→ Promoting→financial→culture and building up expertise by organizing events dedicated to the local press such as the BRVM’s “Media Days”, and setting up a market finance training institute in East Africa, the Securities Industry Training Institute

→→ Building→dialogue between the various stakeholders in the financial ecosystem and the initiatives of market authorities to stimulate disintermediated financing activity. As for the latter, the issue of market depth is crucial, but is not the main obstacle to market development. With the potential to finance projects representing 10% of GDP in certain countries each year, the market offers very good prospects that are often hindered by a lack of financial culture. Improving this is the key challenge.

CONTACT

Pierre [email protected]

Jelmer van de MortelSenior [email protected]

For further information, please contacteline van [email protected]

Roland BergerStrawinskylaan 581 1077 XX AmsterdamTel.: +31 (0) 20 - 79 60 600Fax: +31 (0) 20 - 79 60 699www.rolandberger.nl

This publication has been prepared for general guidance only. The reader should not act according to any information provided in this publication without receiving specific professional advice. Roland Berger shall not be liable for any damages resulting from any use of the information contained in the publication.

© 2016 ROLAND BERGER. ALL RIGHTS RESERVED.

INTERNATIONALAfrica

Growing opportunities for

corporate and investment

banking activities