Financial S rvices - European...

32

Financial Services: Implementing the framework for financial markets: Action Plan Communication of the Commission COM(1999)232, 11.05.99

Transcript of Financial S rvices - European...

Financial S€rvices:Implementing the framework

for financial markets:Action Plan

Communication of the Commission

COM(1999)232, 11.05.99

2

I. Introduction:

A single market for financial services hasbeen under construction since 1973.Important strides have been madetowards providing a secure prudentialenvironment in which financialinstitutions can trade in other MemberStates. Yet, the Union’s financial marketsremain segmented and business andconsumers continue to be deprived ofdirect access to cross-border financialinstitutions. Now, the tempo haschanged. With the introduction of theeuro, there is a unique window ofopportunity to equip the EU with amodern financial apparatus in which thecost of capital and financialintermediation are kept to a minimum.Corporate and household users offinancial services will benefitsignificantly, and investment andemployment across the Union will bestimulated. The structural changestriggered by the euro also herald newchallenges for financial regulators andsupervisors which call for effectiveanswers, with a view to ensuring thebalanced regional distribution of thebenefits of competitive and integratedfinancial services markets.

In recognition of this changing financiallandscape, the Cardiff European Councilin June 1998 invited the "Commission totable a framework for action... toimprove the single market in financialservices"1. In response to this mandate,the Commission published aCommunication2 which identified a rangeof issues calling for urgent action tosecure the full benefits of the singlecurrency and an optimally functioningEuropean financial market. Fiveimperatives for action were highlighted:• the EU should be endowed with a

legislative apparatus capable ofresponding to new regulatorychallenges;

• any remaining capital marketfragmentation should be eliminated,thereby reducing the cost of capitalraised on EU markets;

• users and suppliers of financialservices should be able to exploitfreely the commercial opportunitiesoffered by a single financial market,while benefiting from a high level ofconsumer protection;

• closer co-ordination of supervisoryauthorities should be encouraged;and

• an integrated EU infrastructure shouldbe developed to underpin retail andwholesale financial transactions.

The Vienna European Council, inDecember 1998, considered it vital totranslate the clear consensus on thechallenges and opportunities thatconfront EU financial markets into aconcrete and urgent work programme3 -stressing the importance of the financialservices sector as a motor for growth andjob-creation and the need to confront thenew challenges posed by theintroduction of the single currency. Agroup of personal representatives ofECOFIN Ministers and the EuropeanCentral Bank, meeting under theChairmanship of the Commission, wasthus entrusted with the task of assistingthe Commission in selecting priorities foraction for consideration by the May 25ECOFIN Council.

The Financial Services Policy Group(FSPG) met on three occasions. Itsdeliberations, together with the broadconsultation undertaken earlier for the

3

Implementing the framework for financial markets: Action Plan

1 Pt. 17, Presidency Conclusions from Cardiff EuropeanCouncil (15/16 June 1998).

2 COM (1998) 625. 28.10.98: "Financial Services:building a framework for action".

3 Pt. 51, Presidency conclusions from Vienna EuropeanCouncil (11/12 December 1998).

Framework for Action and the Resolutionof the European Parliament4, have greatlyassisted the Commission in developing afresh perspective to its work. TheCommission now presents thisCommunication which, although not areport from the FSPG, is based on itswork and reflects the broad discussionsin the Group. The Commission tables thisCommunication as a possible basis for afuture work programme in this area,building on agreed Commission policy asdeveloped in discussions with the FSPGand in the European Parliament. TheCommunication seeks to: • confirm the objectives which could

guide the financial services policyover the coming years;

• assign a relative order of prioritiesand an indicative time-scale for theirachievement; and

• identify a number of mechanismswhich may contribute to theirrealisation.

The annexed Framework for Action is anaspirational programme for rapidprogress towards a single financialmarket. It is an illustrative plan whichmay be pursued by the nextCommission, which will of course needto decide conditions under which thedifferent actions will be initiated. Theindicative timeframe reflects the prioritiesas suggested by discussions in the FSPGand the European Parliament. TheEuropean Parliament and the Council, fortheir part, are invited to confirm thecontent and urgency of the Action Plan.To the extent that political support at thehighest level is forthcoming, theEuropean Parliament and the Council areinvited to make every effort to ensurerapid agreement and implementation ofthe individual measures.

II. Tackling urgent on-going business:

Several proposals of immediate andsignificant relevance to the functioning ofEU financial markets have fallen victim to

protracted political deadlock. Theirresolution would constitute an immediateand tangible contribution to thefunctioning of the single financial marketand a clear signal of the politicalcommitment to make progress asurgently as possible. In February,ECOFIN Ministers agreed to intensifyefforts to reach agreement on four keylegislative initiatives (the two proposalson the winding-up and liquidation ofcredit institutions and of insurancecompanies; the proposal for a 13thCompany Law Directive (Take-over bids)and the European Company Statute)5.No definitive break-through has yet beenrecorded, but progress has been made.

The Council is invited to confirm thefundamental importance of theseinitiatives for an effective singlefinancial market and to seek toresolve the outstanding difficulties asurgently as possible.

Further initiatives were singled out asbeing a high priority for adoption beforethe next century. In the annexedframework for action plan, both sets of

4

4 Ref. PE 229.721 fin, EP. 15.04.99. 5 The Proposal for a Directive on the winding-up and

liquidation for credit institutions will help to clarifyand contain counter-party risk. As such, it is animportant firebreak against systemic risk and anindispensable component of a blue-print for soundand stable financial markets. The Proposal for aDirective on the winding up and liquidation forinsurance for insurance would offer insurancecompanies, their policy-holders, employees andcreditors the legal security and confidence needed totake advantage of a single financial market. TheEuropean Company Statute (proposals for a Directiveand Regulation) will contribute to increasedtransparency regarding management and ownershipstructures, as well as a rationalised legal template forpan-European operations. This will be a usefulcontribution to an integrated primary market and willalso serve as an important step towards (market-driven) emergence of corporate governance patternsin the EU. The proposal for take-over bids (13thCompany Law) Directive will facilitate therestructuring of the financial industry – a processwhich is gathering pace – and mark an importantmilestone in the emergence of an open market in EUcorporate ownership.

these initiatives are clearly identified asurgent. They include:• the two proposals for Directives

relating to Undertakings for CollectiveInvestments in Transferable Securities(UCITS);

• the proposal for a directive on thedistance selling of financial services;

• the proposal for a directive onelectronic-money

The Council and the EuropeanParliament are invited to take allnecessary steps to secure politicalagreement on these importantproposals before 31.12.99.

III. Fresh priorities for a singlefinancial market:

The wide consultations undertaken overthe past 12 months, the Resolution of theEuropean Parliament and the work of theFSPG have confirmed that a freshimpetus is called for to harvest theundeniable opportunities offered by thesingle financial market and the singleEuropean currency. The present actionplan consolidates the issues which haveemerged from the Commissioncommunication, as fleshed out by theFSPG discussions. In respect of most ofthe following actions, he Commission hasalready the occasion to confirm orannounce its intention to proceed withinitiatives as they have emerged fromthese discussions. Essentially action isenvisaged under three headings:wholesale markets; retail markets, andsound supervisory structures. TheFramework plan (annexed) provides thedetailed basis for this work, whichshould build on efforts undertaken inother formal or informal bodies whereappropriate. Some of the issues relatingto flanking policies signalled in theCommission communication of October1998 are dealt with in the last chapter ofthis paper.

Wholesale markets:

The euro is the catalyst for a market-driven modernisation of EU securitiesand derivatives markets. Profoundchanges in the organisation of the EUfinancial marketplaces are already visible,notably in the relationship betweendifferent exchanges and in theconsolidation of payment and securitiessettlement systems. These hold out theprospect of cheaper and more flexiblefinancing arrangements for corporateborrowers, including innovative start-upcompanies. Similarly the present mass oflegal and administrative barriers need tobe stripped away lest the emergence ofbetter integrated securities tradingsystems driven by market forces isfrustrated and the benefits of access toEU-wide capital markets denied.Broadly, action is needed under fivechapters:

1. Common rules for integrated securities

and derivatives markets.

The Investment Services Directive (ISD)is in urgent need of upgrading if it is toserve as the cornerstone of an integratedsecurities market. We must pave the wayfor effective cross-border provision ofinvestment services. Even though theISD requires Member States to take intoaccount the extent to which theclient/investor is sophisticated enough toassume full responsibility for determiningwhich rules should apply, obstacles tocross-border business persist. Despitethis provision, host country authoritiesare unwavering in applying their conductof business rules. However, there mayultimately be a need to reconsider theextent to which host country applicationof business conduct rules - which is thebasic premise of ISD – is in keeping withthe needs of an integrated securitiesmarket.

5

A communication summarising thecommon interpretation betweennational supervisory authorities couldbe an important first step in clarifyingthe boundary between the sophisti-cated investor (where the choice of"conduct of business" regime can beleft to the two contracting parties)and the less professional "household"investor (where local rules couldcontinue to be applied).

New regulatory issues: Newdevelopments and technologies alsopose a major new challenge. A modernlegal framework for competitivesecondary markets requires a commonunderstanding on:• the definitions of markets and

exchanges (to ensure thatresponsibility for authorisation andsupervision is clearly allocated);

• the conditions under which brokersand dealers qualify automatically forremote membership of all regulatedmarkets and the elimination of anyother restrictions on exercise ofrelated activities;

• a common approach to theauthorisation and supervision of"alternative trading systems";

• Stringent safeguards to countermarket manipulation.

Consultations will be undertaken withall interested parties (exchanges,regulated markets, supervisors, inter-mediaries, issuers) on the basis on aCommission Green Paper. In addition,possible adaptation of the ISD itselfwill be considered. The utility ofproposals for specific legislation tocounter market manipulation will alsobe given full consideration.

2. Raising capital on an EU-wide basis.

Producing multiple sets of officialdocumentation before issuers can offersecurities in other Member States is costlyand undoubtedly inhibits pan-EU activity.The application of additional national

requirements has thwarted the mutualrecognition of prospectuses which the1989 Public-Offer Prospectus Directiveaimed to achieve.

The Commission communication entitled"risk-capital: a key for job-creation in theEU"6, endorsed by the European Councilat Cardiff, has underlined the missedopportunities for Europe in terms ofinvestment and job-creation stemmingfrom the underdeveloped nature of risk-capital markets. A number ofimpediments to the emergence ofeffective risk-capital provision relate tofragmented approaches to the regulationof securities business. Thesediscrepancies prevent risk-capital marketsfrom acquiring sufficient critical-mass torepresent a viable alternative to morecostly and inflexible forms of financingfor innovative start-up companies.Actions identified in the risk-capitalpaper, coupled with the possiblemeasures presented in this document,will stimulate the emergence of deeperand more liquid markets at EU level.Closer collaboration at the level ofsecurities supervisors will also serve thisobjective. These actions have now beenintegrated within the Framework ActionPlan. and thus the pressure for changewill be maintained.

To secure practical improvements inthe operation of the Public-OfferProspectus Directive, collaborationbetween the Commission and FESCO7

will be intensified. Building on thiswork, the Directives on prospectusesmay be upgraded. These adjustmentscould reinforce the practicalimplementation of mutual recogni-tion of prospectuses and provide fornew streamlined procedures forraising subsequent instalments ofcapital (in particular, laying downthe basis for common acceptance ofshelf-registration techniques).

6

6 SEC (1998) 552 final, April 98.7 The Forum of European Securities Commissions

In order to sustain the politicalmomentum in respect of risk-capitalmarkets, an interim report onprogress of Member States in theimplementation of the risk-capitalaction plan, endorsed by theEuropean Council at Cardiff, will bepublished in the coming months. Thisreport will highlight the steps taken byMember States to harness the potentialcontribution of vibrant and dynamicrisk-capital markets to job-creation.

3. Financial reporting.

Comparable, transparent and reliablefinancial information is fundamental foran efficient and integrated capital market.Lack of comparability will discouragecross-border investment because ofuncertainty as regards the credibility offinancial statements. FSPG discussionspinpointed the urgent need for solutionswhich give companies the option ofraising capital throughout the EU usingfinancial statements prepared on thebasis of a single set of financial reportingrequirements. Capital-raising does notstop at the Union's frontiers: ourcompanies may also need to raisefinance on international capital markets.Solutions to enhance comparabilitywithin the EU market must mirrordevelopments in internationally acceptedbest practice. At the present juncture,International Accounting Standards (IAS)seem the most appropriate bench-markfor a single set of financial reportingrequirements which will enablecompanies (which wish to do so) to raisecapital on international markets. In thesame way, International Standards onAuditing appear to be the minimumwhich should be satisfied in order to givecredibility to published financialstatements.

Discussions in the FSPG havetriggered an important debate on howthe twin objectives of comparablefinancial reporting and alignment oninternational best practice can besimultaneously achieved.Consideration is currently beinggiven to a possible solution whichwould provide companies with anoption (as the sole alternative topreparing financial statements inaccordance with national lawstransposing EU accounting Directives)to publish financial statements on thebasis of IAS standards. The objectiveof comparability in financialreporting will be secured by excludingnational deviations from IAS forcompanies exercising this option. Ascreening mechanism will berequired in order to ensure that IASoutput conforms with EU rules andcorresponds fully with EU publicpolicy concerns. Securities marketssupervisors could be associated to thistask. These issues will be amplified ina Commission Communication to bepublished by the end of 1999, whichwill prefigure amendments of the 4thand 7th Company Law Directives.Auditing issues will be addressed in aseparate CommissionRecommendation.

4. A single market framework for

supplementary pensions funds.

It is the competence of the MemberStates to organise pension provisions inthe light of national circumstances andrequirements. However, where theyexist supplementary pension funds(employment related) should be able tooperate in a coherent single marketframework. The establishment of such aframework was regarded as such a

7

priority by FSPG members that itwarranted a specific debate. This debatecentred on the extent to which anappropriate prudential framework forsuch financial services can enable fundmanagers to improve fund performancewithout in any way compromising theprotection of fund members. With theintroduction of the euro, the use ofcurrency matching rules and stringentasset-category rules can increasingly -though not exclusively- be replaced byqualitative prudential rules. In this waypension funds can be permitted to selectassets that better match the real, longterm nature of their liabilities and thusreduce risk. In order to facilitate thedevelopment of funded pensionschemes, a rigorous prudentialframework is needed in order to ensurethe security of pension fundbeneficiaries. Providing for a high oflevel of protection and improve fundperformance to the benefit of theirmembers, will not only stimulateemployment creation by lowering non-wage labour costs but also alleviate thegrowing burden of financing old agepensions due to demographic change. Indeveloping new thinking, great care hasbeen taken to ensure the maintenance ofa level-playing field on a For allproviders of occupational pensionschemes.

By providing a ready source of long-termcapital, pension funds will also stimulatethe flow of funds available for privatesector investment (thus promoting job-creation and growth). This approach canserve as one of a range of measures tohelp to reduce the burden of financingold age pensions caused by demographicchange. The general lack of aCommunity framework also discourageslabour mobility in that it is both difficultto transfer employee rights from oneMember State to another and impossiblefor residents of one Member State to joina pension scheme in another.

The contours of a prudentialframework for supplementary pensionfunds have been discussed with theFSPG and the Insurance Committee. ACommunication which consolidatesrecent consultations and discussionsis envisaged. This Communicationcould serve as the basis for a proposalfor a Directive on the prudentialsupervision of pension funds. Theenvisaged prudential frameworkwould take into account the diversityof pension funds currently operatingin the EU and will cover:authorisation, reporting, fit andproper criteria, rules on liabilities andinvestments with a combination ofqualitative and quantitative rules. Co-ordination of the tax arrangementsgoverning supplementary pensionsand the removal of the obstacles tolabour mobility would also beexplored.

5. Collateral.

Work on the implementation of theSettlement and Finality Directive showsthe importance of common rules forcollateral pledged to payment andsecurities systems. Priority should begiven to further progress in the field ofcollateral beyond this field. The mutualacceptance and enforceability of cross-border collateral is indispensable for thestability of the EU financial system andfor a cost-effective and integratedsecurities settlement structure. At present,these conditions are not fulfilled: there isa higher risk of invalidation of cross-border collateral arrangements anduncertainty as regards enforceabilityshould the collateral provider becomeinsolvent. If such difficulties are notresolved, cross-border securitiestransactions will be subject to highercosts and risks.

8

In close cooperation with thefinancial services sector and nationalauthorities, the Commission will beginwork on proposals for legislativeaction on collateral.

6. A secure and transparent environment for

cross-border restructuring.

The EU is currently in the throes ofwidespread industrial restructuring. Thefinancial sector is to the forefront of thisdevelopment. Early adoption of theTake-Over Bids Directive and theEuropean Company Statute will providemuch-needed legal underpinning forprotection of minority shareholdings anda more rationalised organisation ofcorporate legal structures in the singlemarket. Early progress on the EuropeanCompany Statute will also pave the wayfor the Commission to come forwardwith long overdue and importantproposals for Directives on cross-bordermergers of public limited companies, andon the transfer of company seat

Ensuring a secure and transparentenvironment for restructuring is ofparticular importance when it involvesthe financial services industry. Prudentialconsiderations must of course be fullytaken into account. At the same time,arriving at configurations that bring aboutgreater efficiency is crucial given the keyrole that financial services play inensuring an efficient allocation ofresources throughout the EU economy.Therefore, the supervisory authorities,while taking prudential considerationsfully into account when dealing with therestructuring process (mergers,acquisitions, take-over bids etc.), shoulddo so in full respect of the principles oftransparency and non-discrimination. Inorder to avoid that prudentialconsiderations – left unspecified – couldresult in unjustified actual or potentialobstacles to restructuring operations, itwould be appropriate that any required

authorisation process be based on a setof objective and publicly disclosedcriteria, stable over time. Such anapproach has been set out by theCommission in its Communication oncertain legal aspects concerning intra-EUinvestments8 in particular to ensure freemovement of capital and freedom ofinvestment.

Retail Markets:

Fundamental change in the EU financialmarkets is clearly being driven bywholesale services. However, the retailsector is itself in the process ofconsiderable adaptation. Action at EUlevel for retail markets and for theprotection of consumers thus remains ahigh priority.

The policy for the single market infinancial services has already introduceda legal framework that allows financialinstitutions to offer their servicesthroughout the Union and established abulwark against institutional failure andsystemic risk. Depositors and insurancepolicy holders are already well-protectedagainst the financial trauma of default.Yet many hurdles to cross-borderprovision of services remain. In particularthe conditions under which financialproducts are sold (e.g. marketing rules)should be addressed. Member Statescontinue to apply national rules as adefence against unfair trading practicesand to ensure the soundness andintegrity of financial services and theirproviders. This situation preventsconsumers and suppliers from reapingthe single market benefits of increasedchoice and competitive terms. Cross-frontier trading will only flourish ifconsumers are confident about theintegrity of the service being providedand the selling methods used bysuppliers; the credentials of the supplier,

9

8 OJ C 220, 19.07.97

the availability and efficacy of redressprocedures in the event of a dispute.Similar factors may also deter suppliersfrom supplying services to consumersresident in another Member Statebecause of the increased costs and/orrisks that such transactions entail for thesupplier. Rather than attemptingharmonisation of financial products,mutual recognition of essentialrequirements should be pursued.

Regulatory and structural problemswhich prevent financial service suppliersand consumers from mutually benefitingin a climate of trust and legal securitymust be tackled head on. Appropriateand progressive harmonisation ofmarketing and information rulesthroughout the Union together with apragmatic search for non-legislativesolutions offers the prospect of a trulyintegrated retail market fully respectingthe interests of consumers and suppliers.The Commission has identified six keyareas for action.

1. Information and transparency.

Clear and understandable information forconsumers is vital when they areinvesting significant savings in anothercountry. Consumers need information toassess the characteristics of the contract,the service provider, and the proposedinvestment. Industry must do everythingpossible to meet such needs. Clearunderstanding of what information isrequired will also be of benefit to serviceproviders in facilitating effective action topartner country markets. TheCommission will encourage aconstructive dialogue between suppliersand users whilst itself remaining fullyprepared to respond to citizens'concerns, if necessary by legislativeaction.

The Commission will pursue the policyof Dialogue between financial servicesproviders and consumers, initially byissuing a Recommendation to follow-up on a code of good practice oninformation provision in the area ofmortgage credit. It will also seek todevelop an over-arching policy in thisarea. This will be reflected in aCommunication to be publishedwhich will examine possible guidingprinciples for the full range of cross-border financial services, takingaccount of provisions laid down inexisting EU and national provisions.

2. Redress procedures.

Amongst the most significant stumbling-blocks to the single financial market isthe consumer's uncertainty about thepossibilities of redress in the eventualityof cross-border contractual dispute. Weneed to find an efficient and effectivejudicial and extra-judicial settlement ofdisputes to provide the necessaryconfidence in cross-border activity.

On the basis of the Commission'spolicy of administrative cooperationwithin the Single Market, theCommission could consider thedevelopment of a Union-widecomplaints network (including theuse of an ombudsman for financialservices). In the field of consumerdisputes, the Commission will base itsaction on its Recommendation on theprinciples applicable to the bodiesresponsible for out-of-court settlementsof consumer disputes9 and will followthe methodology foreseen in that text.

10

9 Recommendation 98/257 of 30.03.98.

Thus, in order to promote co-operation between these extra-judicialbodies in charge of consumerdisputes, the European Commissionwill encourage networking betweenthese bodies with a view to resolvingcross-border disputes. Ultimately,consumers should be able to refercross-border disputes to the extra-judicial body which is competent andwhich respects the criteria of theRecommendation in the foreigncountry via the corresponding extra-judicial body in their own country. Itgoes without saying that recourse toextra-judicial bodies can neverpreclude the right of consumers tobring their action before judicialcourts. In addition, the Commissionpolicies of Dialogue with Citizens andwith Business could also be developedto provide advice and help oncomplaints procedures throughout theUnion.

3. A balanced application of consumer

protection rules.

If all Member States have the same basiclevel of protection in place, nationalauthorities should be more ready toallow financial services providersauthorised in other Member States todeal with their clients without settingadditional requirements on thoseproviders.

For a number of specific financialproducts, the Commission couldanalyse national consumer protectionrules (including general provisionsthat affect other Member States'products/suppliers). Detailed workcould be undertaken to establishpossible equivalence between clearlysimilar rules. This work couldculminate in detailed report to theCouncil and EP on the basis of which

conclusions for future policy will bedrawn. The Commission has alreadyannounced its intention to issue acommunication on the application ofthe general good in the insurancesector.

4. Paving the way for e-commerce based

retail financial business.

E-commerce is already revolutionisingretailing and distribution of manyfinancial services. Suppliers - EU andnon-EU - will be able to make contactwith potential users across nationalboundaries at minimal distribution cost.Users will benefit from a wider range ofinnovative products. The overall impactwill be to reinforce and cement marketintegration. Proposals for E-Commerceand Distance Selling Directives are onthe table, which will facilitate theemergence of these activities. However,discussions in the FSPG highlighted theneed for clarification and coherence incertain areas (e.g. existing differences inprudential procedures and notificationarrangements). Many of the issues,already identified for cross-border salesin retail financial markets, will be throwninto even sharper relief.

The Commission envisages publishinga Green Paper to establish whether theprovisions of existing financiallegislation contain coherentprovisions on prudential proceduresprovide a propitious legalenvironment in which e-commercebased financial services business canthrive, while ensuring that consumers'interests are fully safeguarded.

5. Insurance intermediaries.

Member States have developed consumerprotection safeguards in relation toinsurance intermediaries, but varying

11

national legislation has been drawn upalong very different lines which acts tohamper the free provision of services.Given their key importance in enhancingthe functioning of the single insurancemarket, there is a need to provide a clearand common approach to regulation ofinsurance intermediaries, thus facilitatingthe free provision of services whilestrengthening consumer protection at ahigh level.

The Commission is working towardstabling a Directive:1) to update the 1976 Directive on

insurance intermediaries and2) to strengthen consumer protection

by establishing commonrequirements on inter aliaregistration, financial securityand information disclosure to theconsumer.

6. Cross-border retail payments.

Without impetus at the highest politicallevel, there is a danger that the individualcustomer of financial services will bedeprived of some of the tangible benefitsof a single currency.

In particular, low value credit transfersbetween euro-zone countries willcontinue to attract high charges untilsuch time as a modern paymentsinfrastructure which is capable ofsupporting efficient, secure and low-costcross-border payments is put in place.The current relatively low-volumes ofcross-border credit transfers combinedwith a range of structural andadministrative factors stand in the way of"state-of-the-art" linkages. However,citizens are unwilling - and rightly so - totolerate a situation where cross-borderpayments incur charges which far exceedthose charged by domestic transfersystems. If charges could be reduced to alevel comparable to domestic credit

transfers, savings of several billion eurocould be made. Remedying theinfrastructural gaps requires a concertedstrategy, supported at the highestpolitical level and including the EUinstitutions, the ESCB and the privatesector to surmount the technical andcommercial hurdles.

Likewise, charges for cross-border card-payments are higher (and often moreopaque) than fees for domestic cardpayments – although the differences areless marked than for credit transfers. Inthis area, the Commission believes that acombination of efforts to increasetransparency, reduce fraud and reinforcecompetition disciplines erode suchdifferentials.

There is a clear need for integratedretail payments systems, whichprovide for secure and competitivesmall-value cross-border transferscomparable with the service providedwithin domestic payment systems, tobe put in place before the end of theeuro transitional period. A concertedeffort involving the ESCB, EUinstitutions and the private sectorshould be launched to deliver atechnically secure and operationalsolution as a matter of utmosturgency . The Council and theEuropean Parliament are invited toendorse this as a foremost politicalobjective in the financial services fieldand to play their full part insupporting the implementation of asolution which will serve the needs ofcitizens. The Commission intends topublish a Communication mappingout a strategy for ensuring progresstowards this objective.

12

Sound supervisory structures:

The EU’s supervisory and regulatoryregime has provided a sound basis forthe emergence of a true single financialmarket which goes hand in hand withprudential soundness and financialstability. Steady EU-led convergence inregulatory requirements, has beenunderpinned by a comprehensive systemof informal bilateral memoranda ofunderstanding between financialsupervisors. This system has providedcommon ground-rules and pragmaticmeans of implementing and applying theEU Directives for a single market forfinancial services. However, the futurewill bring fresh challenges. Theheightened tempo of consolidation in theindustry, and the intensification of linksbetween financial markets because of theeuro call for careful consideration ofstructures for containing and supervisinginstitutional and systemic risk. In anenvironment characterised by strong andimmediate transmission effects betweenEU banking and securities markets, thereare reasons to believe that the status quomay not tenable over the longer-term.There is now a greater need and awillingness to engage in an opendiscussion on the structures that will beneeded to ensure appropriate regulationand supervision of a single financialmarket.

As regards regulation, the Union shouldstrive to maintain the highest standardsof prudential regulation for its financialinstitutions. These standards must bekept up-to-date with marketdevelopments and capital requirementsmust accurately reflect the risks run bybanks, insurance undertakings andsecurities firms in the Union. Combinedfinancial operations may also create newprudential risks or exacerbate existingones. Capital requirements must beadequate and proportionate to meet therisks undertaken in financial groups thatstraddle traditional sectoral boundaries.

The Commission will continue toexercise its right of initiative inpromulgating proposals to address newregulatory issues. It would however,draw great benefit from cross-sectoralstrategic input of the type which couldbe delivered by the mechanismpresented in section IV.1 of this paper.This perspective would be valuable indefining broad orientations forappropriate regulatory approaches inareas such as conglomerates The EUmust also assume a key role in ensuringthat its voice is clearly heard ininternational financial regulatory fora toensure that sound and coherentregulations are promulgated thatguarantee level-playing fields. Theglobal dimension to regulation offinancial services is set to acquireincreasing importance as internationalliberalisation gathers pace under theaegis of the WTO10.

In the area of supervision, closer marketintegration has pushed the issue ofreinforced EU collaboration to theforefront. The continuing process ofinternationalisation, disintermediation,and globalisation of financial serviceschallenges the way in which we havestructured the present means of co-operation and co-ordination betweenauthorities. The following practicalsteps, which build on existingarrangements, could take account of thegreater cross-border and cross-sectoraldimension to ensuring financial stability.

1. Increasing cross sectoral complexitiesunderline the need for clarity insupervisory roles. Many themes thatare discussed within a banking,insurance, or securities perspective inreality cut across all financial sectors.There is therefore a pressing need for

13

10 Ratification of the 1997 Agreement is proceeding andattention is turning to a second round of GATSliberalisation

increased collaboration, monitoringand better understanding ofexperiences and risks in all sectors,including those that would normallygo beyond individual banking,insurance or securities supervisoryperspective. At present, there is nofocal point for forging commonapproaches across sectors to the day-to-day application of prudential rulesto individual cases. The Commissionwould see great merit in developing"ad hoc" and streamlinedarrangements for close coordinationbetween front-line authorities. Suchan arrangement could draw from themembership of existing structures. Inthis way, it would avoid duplicationand proliferation of structures11.Although the Commission’s vocationin the financial services field isregulatory, it stands ready to assistMember States in developing theseideas.

2. In the field of securities markets,closer cooperation between securitieshas taken a step forward followingthe creation of FESCO. As cross-border trading and issuance becomesa common-place, policy concernssuch as market integrity will assumethe properties of a common good. Intime, the option of a single authorityto oversee securities marketssupervision may emerge as ameaningful proposition in the light ofchanging market reality. The EU hasalso been hamstrung by the absenceof a committee of appropriatestanding to assist the EU institutionsin the developing and implementingregulation for investment services andsecurities markets.

3. EU legislation provides a legallybinding underpinning for cross-border cooperation between bankingsupervisors. These rules are managedthrough bilateral Memoranda ofUnderstanding between nationalsupervisors. Recently, some haveargued that these arrangements are

no longer sufficiently robust tocontain cross-border effects of failureof large institutions. The Commissiondoes not subscribe to the view thatpresent arrangements are unsuitablefor the present state of the singlebanking market. However, itconsiders that there is a need forhigh-level political assessment,encompassing all national and EUlevel institutions with an interest inbanking supervision, of theconditions under which a review ofpresent arrangements for bankingsupervision could be required.

At present, decisions on appropriatesupervisory arrangements are determinedat national level, and the supervision ofthe banking, insurance and securitiessectors is predominantly conducted atthat level. Member States have developeddifferent models for performing thesetasks. Mutual confidence in theeffectiveness of partner country financialsupervision and regulation – whetherthat be undertaken by a consolidatedauthority for the entire sector or byseparate sectoral authorities that co-operate and co-ordinate effectively – isthe key ingredient for successful cross-border supervision.

The Commission intends to presentproposals to maintain high standardsof banking, insurance and securitiesprudential legislation. To this end thework of existing bodies will be takeninto account as much as possible(Basle Committee, FESCO etc). Workon the prudential supervision offinancial conglomerates will be takenin hand. Appropriate and efficientarrangements will be put in place toincrease cross-sectoral discussion andco-operation between authorities on

14

11 E.g. Groupe de Contacte, FESCO and Conference ofinsurance supervisors and their parent committees –BAC, HLSS and IC.

issues of common concern. In thesecurities field, the Commissionenvisages the creation of a SecuritiesCommittee, in the light of any futureinter-institutional decision on"comitology". It also advocates theinitiation of high-level considerationof the conditions under which presentsupervisory arrangements in thebanking sector might need to bereviewed.

General conditions for an efficient EUfinancial market:

1. Corporate governance.

Investors in the single market mayexperience unnecessary uncertainty dueto differences in corporate governancearrangements. Differences in corporategovernance arrangements could give riseto legal or administrative barriers whichmight frustrate the development of an EUfinancial market (e.g. practicalarrangements for the exercise of votingrights by shareholders in partnercountries). However, the term "corporategovernance" covers a wide series ofissues whose ramifications for the singlefinancial market are at present unclear.Furthermore, national arrangementsspring from long-standing legal andsocio-economic traditions. At the presentjuncture, any EU involvement in this areashould be confined to identifying anybarriers to the development of the EUfinancial market resulting from corporategovernance arrangements.

A review of existing national codes ofcorporate governance will belaunched with a view to identifyingany legal or administrative barrierswhich could frustrate the developmentof a single EU financial market.

2. Taxation.

For the sake of a smoothly functioningsingle market for financial services,

contributing to an efficient allocation ofresources throughout the EuropeanUnion, the further integration of financialmarkets must proceed broadly in parallelwith an adequate process of tax co-ordination.

The liberalisation of capital movementsin 1988 – a key step, inter alia, forensuring a single market for financialservices – was due to be accompaniedby parallel measures in the area ofsavings taxation in order to eliminate orreduce the risks of distortion, tax evasionand/or tax avoidance. In fact, the Councilwas unable to reach agreement on theDirective proposed in 1989.

A second key step in financialliberalisation took place with theadoption of specific sectoral financialservices directives, again withoutprogress in the field of taxation. Forexample, barriers arising from the taxtreatment of insurance premium continueto act as a serious barrier to a singleinsurance market.

This framework action plan is intendedas the third key step towards a singlemarket for financial services. A numberof Member States, together with theCommission, consider that it would betechnically unbalanced and politicallydifficult to implement this third stagewhile the process of tax co-ordination infinancial markets is still less developed.

The Council is invited to adopt the1998 proposal for a Directive toensure a minimum effective taxationof cross-border savings income. TheCommission will continue its efforts totackle tax barriers to a fullyfunctioning single market forfinancial services. The Commissionwill present proposals, in the light ofthe Taxation Policy Groupdiscussions, as regards pension fundsand insurance.

15

IV. Delivering the Framework actionplan:

FSPG discussions have permitted a longoverdue stock-taking of our approach tolegislating for financial markets. It tookmore than a decade to agree the SingleMarket financial services legislationwhich gave effect to the guidingphilosophy of the "single passport/home-country control". We are now embarkingon a qualitatively more challengingprocess which aims to target a broaderrange of policy objectives against thebackdrop of a faster-changing financialworld. If we are successfully toimplement the regulatory blue-print setout in the annex, we will need tooverhaul the way we develop financialservices legislation and achieve highlevels of international cooperation.Mechanisms are required which avoidthe following pitfalls:

1) A piecemeal and reactive approach toproposing and designing actions isinadequate in a situation wherefinancial conglomerates are common-place and the boundaries betweenfinancial services are being steadilyblurred. A holistic, cross-sectoral viewis required in setting regulatorypriorities, in avoiding tensionsbetween policy objectives in differentsegments of the financial markets andin expanding the range of policysolutions. Such considerations militatein favour of a high-level strategicinput in policy-setting;

2) Protracted decision-making processes(witness the debates on winding-upand liquidation of credit institutionsand insurance companies). A moreinclusive and consensual approach inshaping policies from an early stageand in advance of drafting legislationwill deliver dividends when it comesto completing formal (co-decision)procedures. This inclusive approachshould extend to all EU institutions,but also to representatives of market

practitioners, consumers, users andemployees;

3) EU solutions must be characterisedby a degree of flexibility so that theyare not immediately renderedobsolete by the relentless pace ofchange in the markets. Overlyprescriptive EU measures often onlyserve to ossify market structures andbehaviour. This risk is exacerbated bythe length of time needed formally toagree legislative solutions.

The way in which we set aboutimplementing the new frameworkagenda will be critical to its achievement.The following mechanisms can beconsidered.

1. Updating cross-sectoral priorities.

New regulatory challenges will emerge asa potential threat to the stability of EUfinancial markets. To meet suchchallenges a fresh look at the presentorganisation of the Union's structures andprocedures for financial services isneeded.

Without prejudice to the Commission’slegal right of initiative, a mechanismto identify future challenges and toframe priorities in a broad contextcould comprise the followingelements:

• A forum to forge consensus onemerging challenges betweennational ministries involved infinancial services regulation. TheCommission would derive greatbenefit from access to strategicinput similar to that provided bythe FSPG for the period of its short-lived mandate.

• Appropriate arrangements couldbe made to allow policyorientations to be discussedinfomally with EP representativesat an early stage.

16

• A high level forum could becreated to take soundings frombodies representing the principalEU interest groups which have aninterest in the smooth and efficientoperation of financial markets.Chief amongst these would berepresentatives of all segments offinancial markets, exchanges,consumers and (business) users,and employees.

• The recently developed process ofeconomic reform provides essentialinformation and analysis of thefunctioning of product, serviceand capital markets. The Cardiffprocess will serve as a valuableinput in the selection of priorities.

• The Commission should reportregularly to the Council on theprogress made in achieving thedeadlines set in the FrameworkAction Plan and, following a highlevel group examination, inconsidering major new crosssectoral challenges (such asfinancial conglomerates).

2. Selecting the best available technical

solutions.

The Commission intends, at as early astage as possible, to engage the other EUinstitutions and relevant EU-level interestgroups in discussions on the broadcontours of any initiative. Suchconsultations could include thefollowing:1) Input from national authorities

engaged in the regulation andsupervision of markets could beintegrated at an early stage whenCommunity initiatives are beingprepared;

2) EU representative bodies coulddesignate a short-list of experts tohelp the Commission in assessing theimplications of more technicalsolutions.

3. Speedy implementation of agreed solutions.

At present, the adaptation of EUprudential rules to cope with newsources of instability or to align it onstate-of-the-art regulatory/supervisorypractice is painstakingly slow (it is notunusual for legislative procedures to takethree to four years to complete). Theresolution of the European Parliamenthighlights the dangers inherent in thesedelays, whilst underlining the need torespond effectively to concerns about thedemocratic legitimacy of the EU’sdecision-making process.

All agree that we need greatly tominimise the time needed to concludeagreement on individual actions. TheCommission could explore with theParliament and the Council how best toensure the possible acceleration of co-decision procedures provided for underArt. 251 of the Treaty (as introduced byAmsterdam Treaty) can be used.

However, a more wide-ranging rethink ofthe way in which policy for financialmarkets is processed is required. Anymore radical procedural approach mustprovide for rigorous oversight by the EPand Council and must ensure that rulesare, as far as possible, uniformlyinterpreted and applied across the EU;that greater flexibility in regulatory policyis introduced so that where necessary itcan be more promptly adapted (subjectto political oversight) to changingcircumstances.

The Commission could initiateinformal discussions with theEuropean Parliament and MemberStates on the way in which Article251 can be used to accelerate thelegislative process for financialservices. In addition, ways ofdrafting legislation in order tominimise over complexity will be

17

explored. In particular, the framingof single market legislation in thisarea (based on Art. 100a) couldenshrine "essential requirements"which have as their basis a high levelof consumer protection. The coreconcepts at the heart of EU legislationcould be fleshed out in greater detailthrough the use of agreed comitologyprocedures, thus providing for legalcertainty as regards detailedimplementing provisions. Additionalclarification on technical issues, toassist supervisors and other agenciesin day-to-day application offramework rules, would be providedin the form of Commissioncommunications.

The Council and EP are invited to lendtheir support to the implementation ofthis new approach to elaborating andfinalising proposals for EU level action inrespect of financial markets.

18

19

Financial Services Action Plan

Based on the extensive consultationsaround the Commission’s Framework forAction, the following plan confirms thework that must be set in hand to reapthe full benefits of the euro and ensurecontinued stability and competitivenessof EU financial markets. The futureCommission will need to decideconditions under which different actionswill be taken forward. The optimaltimeframe reflects the priorities whichhave emerged from discussions in theFSPG, with the European Parliament andwith other interested parties.

The European Parliament and theCouncil are invited to endorse thecontent and urgency of the FinancialServices Action Plan. The EuropeanParliament and the Council are alsoinvited to make every effort to ensurerapid agreement and implementation ofthe individual legislative measures.Commitments are also called for toensure the investment of political willand concentration of the necessaryresources to achieve the ambitiousdeadlines that are set in response to thechanging demands of the market, theneed to safeguard consumer interests andto enhance the competitiveness of EUindustry as a whole.

Three indications of priority have beenset for each measure identified in theAction Plan:

Priority 1 actions:

There is broad consensus that theseactions call for immediate attention.These measures are crucial to realisationof the full benefits of the euro and to

ensuring the competitiveness of theUnion’s financial services sector andindustry whilst safeguarding consumerinterests.

• Where legislative proposals arealready on the table EuropeanParliament and Council are invited totake all steps necessary to secure themaximum possible agreement beforeJanuary 1, 2000.

• The Commission confirms that wherean initiative is required, it will comeforward with the necessary actionwithout delay.

• Based on any necessary preparatorywork by the Commission, the Counciland European Parliament are invitedto ensure rapid agreement within twoyears, or at the latest by the end ofthe euro-transitional period, and toexpedite implementation of agreedmeasures without delay.

Priority 2 actions:

The Commission regards these prioritiesas important to the functioning of theSingle Market for Financial Services - inparticular, by amending existinglegislation or adapting present structuresto meet new challenges.

Priority 3 actions:

These actions concern important areaswhere a clear and general consensusexists that new work should be set inhand with a view to finalising acoherent policy by the end of the euro-transitional period.

21

Financial Services Action Plan

Speedy adoption and implementation ofthe following actions12 in order to achievethis strategic objective will: • enable corporate issuers to raise

finance on competitive terms on anEU-wide basis;

• provide investors and intermediarieswith access to all markets from singlepoint-of-entry;

• allow investment service providers tooffer their services on a cross-borderbasis without encounteringunnecessary hindrances oradministrative or legal barriers;

• establish a sound and well integratedprudential framework within whichasset managers can put funds at theirdisposal to their most productive use;

• create a climate of legal certainty sothat securities trades and settlementare safe from unnecessary counter-party risk

22

Strategic objective 1A single EU wholesale market

12 The proposed actions are structured in accordancewith the presentation in the introductory paper

Priority Objective Actors OptimalTimeframe

Action

1

3

Overcoming obstacles to theeffective mutual recognition ofprospectuses, so that a prospectusor offer document approved in oneMember state will be accepted inall. In addition, incorporating "shelfregistration" will provide for easieraccess to capital markets on thebasis of streamlined prospectuses,derived from annual accounts.

More frequent and better qualityinformation will enhance marketconfidence and attract capital

Commission,building uponwork by FESCO13

Commission,followingconsultation withFESCO and themarket

For issue by mid2000Adoption: 2002

Launchconsultation bymid 2000Proposal: 2001Adoption: 2002

Upgrade theDirectives onProspectusesthrough a possiblelegislativeamendment

Update theDirective onRegular Reporting(82/121/EEC)

Raising capital on an EU-wide basis:

13 Forum of European Securities Commissions

23

Priority Objective Actors OptimalTimeframe

Action

1

2

2

Summary of common interpretationof use of investor protection rules,including conduct of business rulesto determine conditions underwhich host country business rulesapply to cross-border securitiestransactions.

Enhance market integrity byreducing the possibility forinstitutional investors andintermediaries to rig markets. Setcommon disciplines for tradingfloors to enhance investorconfidence in an embryonic singlesecurities market.

Wide-ranging review of ISD asbasis for integrated and efficientmarket for investment services.Tackle remaining obstacles tomarket access for brokers/dealers,obstacles to remote membership,and restrictions on trading in T-bonds. Address new regulatorychallenges such as AlternativeTrading systems.

Commission,building uponwork by FESCOand afterconsultation withMember States.

Commission: afterconsultation withMember Statesand markets.

Commission

Draft for issue byend 1999

Proposal by end2000Adoption: 2003

Publish GreenPaper: mid-2000

Issue aCommissionCommunication ondistinctionbetween"sophisticated"investors and retailinvestors.

Directive toaddress marketmanipulation.

Green Paper onupgrading the ISD

Establishing a common legal framework for integrated securities and derivatives markets:

Priority Objective Actors OptimalTimeframe

Action

2

1

2

2

Enabling European companies toaccount for certain financial assetsat fair value, in accordance withInternational Accounting Standards

Map out strategy for enhancingcomparability of financial reportsissued by listed EU companies,based on combination of EUaccounting Directives and financialstatements issued in accordancewith agreed internationalaccounting standards. Strategyshould prefigure mechanism forvetting international benchmarkstandards so that these can be used(with no national variations) by EUlisted companies.

Bringing the 4th and 7th Directivesin line with the needs of the Singlemarket and to take into accountdevelopments in internationalaccounting standard-setting

Upgrading the quality of statutoryaudits in the EU by recommendingspecific measures in the areas ofquality assurance and auditingstandards.

Commission,Council, EP

Commission

Commission,Council, EP

Commission

Proposal autumn-99Adoption: 2001

For issue by end-99

Proposal end-2000Adoption: 2002

For issue by end-99

Amend the 4th and7th Company LawDirectives to allowfair valueaccounting

CommissionCommunicationupdating the EUaccountingstrategy

Modernisation ofthe accountingprovisions of the4th and 7th CompanyLaw Directives

CommissionRecommendationon EU auditingpractices

Towards a single set of financial statements for listed companies:

24

Priority Objective Actors OptimalTimeframe

Action

1

1

Common and coherent applicationof the Directive throughout the EUis important for a smoothfunctioning of systems.

Legal certainty as regards validityand enforceability of collateralprovided to back cross-bordersecurities transactions.

Member States

Commission inconsultation withMember Statesand marketexperts

Commission tocontinuemonitoring ofimplementation ina working Group.Commissionreport to Councilend 2002

Launchconsultationautumn-99:proposal end-2000.Adoption: 2003

Implementation ofthe SettlementFinality Directive

Directive on cross-border use ofcollateral.

Containing systemic risk in securities settlement:

Priority Objective Actors OptimalTimeframe

Action

1

1

3

3

3

Create EU-wide clarity andtransparency in respect of legalissues to be settled in event oftake-over bid. Prevent pattern ofEU corporate restructuring frombeing distorted by arbitrarydifferences in governance andmanagement cultures.

Create optional legal structure tofacilitate companies to place pan-European operations on arationalised single legal umbrella.Within this context clarify scopefor participation by employees –thereby create further commonground in respect of corporategovernance practices.

Identification of legal oradministrative barriers andresulting differences in corporategovernance regimes.

Create the possibility forcompanies to conduct cross-bordermergers

Allow companies to transfer theircorporate seat to another MemberState

Council, EP

Council, EP

Commission,Member States,markets.

Commission

Commission

Mid-99Adoption: 2000

Mid-1999Adoption: 2000

Launch reviewearly 2000

Proposal inautumn-99Adoption: 2002

Proposal inautumn 1999Adoption: 2002

Political agreementof the proposeddirective on TakeOver Bids

Political agreementon the EuropeanCompany Statute

Review of EUcorporategovernancepractices

Amend the 10th

Company LawDirective

14th Company LawDirective

Towards a secure and transparent environment for cross-border restructuring:

25

Priority Objective Actors OptimalTimeframe

Action

1

1

1

Consultation on prudentialframework for second-pillarpension fund schemes to protectbeneficiary rights through stringentprudential safeguards and rigoroussupervision.

Proposal 1 will remove barriers tocross-border marketing of units ofcollective investment by wideningassets in which funds can invest.Proposal 2 would provide aEuropean passport formanagement companies, andwiden the activities which they areallowed to undertake (also beauthorised to provide individualportfolio management services).

Following the policy outlined in itsCommunication, the Commissionwill propose a Directive on theprudential supervision of pensionfunds. It will take into account thediversity of pension funds currentlyoperating in the EU and will coverauthorisation, reporting, fit &proper criteria and rules onliabilities and investments.

Commission

Council, EP

Commission

Issue by May 1999

End-1999Adoption: 2000

Proposal: Mid2000Adoption: 2002

CommissionCommunication onFunded pensionSchemes

Political agreementon the proposeddirectives onUCITS

Directive on theprudentialsupervision ofpension funds

A Single Market which works for investors:

Concerted efforts by EU institutions andall interested parties, along the lineslisted below, are needed to:• Equip consumers with the necessary

instruments (information) andsafeguards (clear rights and effectivedispute settlement) to permit their fulland active participation in the singlefinancial market:

• Identify and roll back unjustifiedinsistence on non-harmonisedconsumer-business rules as anobstacle to cross-border provision ofservices;

• Promote the emergence of effectivemechanisms for overcoming fault inthe single retail financial marketwhich have their origin in differencesin private law:

• Create legal conditions in which newdistribution channels and distancetechnologies can be put to work on apan-European scale;

• Encourage the emergence of cost-effective and secure payment systemswhich enable citizens to effect small-value cross-border payments withoutincurring exorbitant charges.

26

Strategic objective 2Open and secure retail markets

Priority Objective Actors OptimalTimeframe

Action

1

2

1

Proposal aims to bring aboutconvergence of rules on business-to-consumer marketing and salestechniques. This will limit exposureof consumers to undesirablemarketing techniques (inertia andpressure-selling) through inclusionof appropriate provisions(generous right of withdrawalrights, prohibitions). Once in place,distance selling via remotetechnologies should be free fromthis category of impediment.

Establish over-arching view ofbasic information requirementsconsumers need in order to assesscredential of (cross-border) servicesuppliers, security/performance ofservices offered by latter (plusredress). Examine extent to whichthese requirements are compliedfor range of retail financialservices.

Building on discussions inConsumer Dialogue, theCommission will publish acommunication to endorseunderstanding in respect ofinformation to be provided inevent of cross-border provision ofmortgage credit services.Commission involvement inmonitoring of compliance.

Council, EP

Commission,Member States.

Commission, bankand consumerrepresentatives.

End 99Adoption: 2000

Review to beginend 99:Communication:mid 2000

For issue by end-99

Political agreementon proposal for aDirective on theDistance Selling ofFinancial Services

Commissioncommunicationcodifying clear andcomprehensibleinformation forpurchasers

Recommendationto support bestpractice in respectof informationprovision(mortgage credit).

27

Priority Objective Actors OptimalTimeframe

Action

3

2

2

2

2

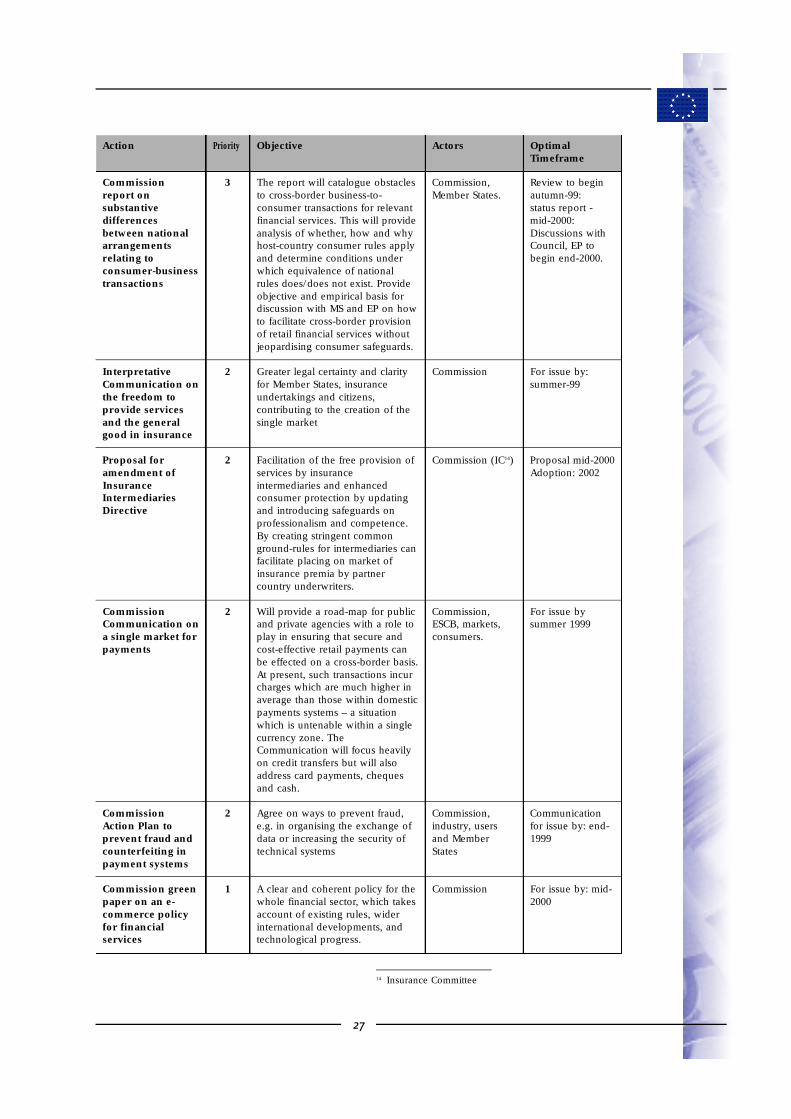

1

The report will catalogue obstaclesto cross-border business-to-consumer transactions for relevantfinancial services. This will provideanalysis of whether, how and whyhost-country consumer rules applyand determine conditions underwhich equivalence of nationalrules does/does not exist. Provideobjective and empirical basis fordiscussion with MS and EP on howto facilitate cross-border provisionof retail financial services withoutjeopardising consumer safeguards.

Greater legal certainty and clarityfor Member States, insuranceundertakings and citizens,contributing to the creation of thesingle market

Facilitation of the free provision ofservices by insuranceintermediaries and enhancedconsumer protection by updatingand introducing safeguards onprofessionalism and competence.By creating stringent commonground-rules for intermediaries canfacilitate placing on market ofinsurance premia by partnercountry underwriters.

Will provide a road-map for publicand private agencies with a role toplay in ensuring that secure andcost-effective retail payments canbe effected on a cross-border basis.At present, such transactions incurcharges which are much higher inaverage than those within domesticpayments systems – a situationwhich is untenable within a singlecurrency zone. TheCommunication will focus heavilyon credit transfers but will alsoaddress card payments, chequesand cash.

Agree on ways to prevent fraud,e.g. in organising the exchange ofdata or increasing the security oftechnical systems

A clear and coherent policy for thewhole financial sector, which takesaccount of existing rules, widerinternational developments, andtechnological progress.

Commission,Member States.

Commission

Commission (IC14)

Commission,ESCB, markets,consumers.

Commission,industry, usersand MemberStates

Commission

Review to beginautumn-99: status report -mid-2000:Discussions withCouncil, EP tobegin end-2000.

For issue by:summer-99

Proposal mid-2000Adoption: 2002

For issue bysummer 1999

Communicationfor issue by: end-1999

For issue by: mid-2000

Commissionreport onsubstantivedifferencesbetween nationalarrangementsrelating toconsumer-businesstransactions

InterpretativeCommunication onthe freedom toprovide servicesand the generalgood in insurance

Proposal foramendment ofInsuranceIntermediariesDirective

CommissionCommunication ona single market forpayments

CommissionAction Plan toprevent fraud andcounterfeiting inpayment systems

Commission greenpaper on an e-commerce policyfor financialservices

14 Insurance Committee

Urgent headway must be made in orderto:• Eliminate any lacunae in EU

prudential framework, arising fromnew forms of financial business orglobalisation, as a matter of utmosturgency.

• Set rigorous and appropriatestandards so that the EU bankingsector can successfully manageintensification of competitivepressures.

• Contribute to the developing of EUsupervisory structures which cansustain stability and confidence in anera of changing market structures andglobalisation.

• Develop a regulatory and supervisoryapproach which will serve as thebasis for successful enlargement.

• Enable the EU to assume a key rolein setting high global standards forregulation and supervision, includingfinancial conglomerates.

28

Strategic objective 3State-of-the-art prudential rules and supervision

29

Priority Objective Actors OptimalTimeframe

Action

1

1

1

1

2

2

Provide a coherent legalframework for the winding-up andliquidation of insurance companiesin the single market through themutual recognition of proceedingsand the principles of unity,universality, publicity and non-discrimination

Common rules on winding-up andliquidation will establish commonprinciples for procedures to befollowed in event of bankinsolvency, identify responsibleauthority. As such will safeguardagainst continued activities byinsolvent institutions which couldrepresent source of counterpartrisk.

Ensure market access and adequateregulation of e-money providers:clarify the prudential rules underwhich institutions other thantraditional credit institutions canprovide e-money services. Enableprovision of this activity on cross-border basis.

Combat fraud and moneylaundering in the financial systemto widen definition of predicateoffences and to extend reporting(‘suspicious transactions’)requirements to relevant non-financial professions.

Enhanced disclosure of theactivities of banks and otherfinancial institutions to allowinvestors to take informeddecisions, and to foster markettransparency and discipline as acomplement to prudentialsupervision

Work on a review of the bankcapital framework to reflect marketdevelopments is running in parallelwith that of the G-10 BasleCommittee on BankingSupervision. This work is expectedto result in a overhaul of the EU’sbank and investment capitalframework.

Council, EP

Council, EP

Council , EP

Commission

Commission

Commission(BAC, HLSS15)Member States,markets

New first readingin EP end 1999Politicalagreement assoon as possibleAdoption: 2001

Common position:end-99Adoption: 2001

Common position:autumn 99Adoption: 2000

Proposal mid 1999Adoption: 2001

Communicationmid 1999

Proposal fordirective: spring2000, pendingdevelopments inBasleAdoption: 2002

Adopt theproposed directiveon the winding-upand liquidation ofinsuranceundertakings

Adopt theproposed directiveon the winding-upand liquidation ofbanks

Adopt theproposal for anElectronic Moneydirective

Amendment of themoney launderingdirective

CommissionRecommendationon disclosure offinancialinstruments

Amend thedirectivesgoverning thecapital frameworkfor banks andinvestment firms

15 Banking Advisory Committee, High Level SecuritiesSupervisors Committee

30

Priority Objective Actors OptimalTimeframe

Action

3

3

1

2

Protection of consumers in thesingle market by ensuring thatinsurance undertakings haveadequate capital requirements inrelation to the nature of their risks.

Basis for international exchange ofinformation to underpin financialstability

Addressing loopholes in thepresent sectoral legislation andadditional prudential risks toensure sound supervisoryarrangements.

A formal regulatory committee inthis field will contribute to theelaboration of EU regulation in thesecurities area. Requireswillingness on part of EUinstitutions to agree an appropriatecomitology procedure.

Commission (IC),Member States,markets.

Commission

Commission:BAC/IC/HLSS,Member States,supervisors andmarkets.

Commission,Council, EP

Proposal fordirective: mid2000Adoption: 2003

Proposal autumn1999Adoption: 2001

Proposal: end-2000Adoption: 2002

Proposal end 2000Adoption: 2002

Amend thesolvency marginrequirements inthe insurancedirectives

Proposal to amendthe insurancedirectives and theISD to permitinformationexchange withthird countries

Development ofprudential rulesfor financialconglomeratesfollowing therecommendationsof the ‘JointForum’

Creation of aSecuritiesCommittee

• Addressing disparities in tax treatment• An efficient and transparent legal

system for corporate governance

31

General objectiveWider conditions for an optimal single financial market

Priority Objective Actors OptimalTimeframe

Action

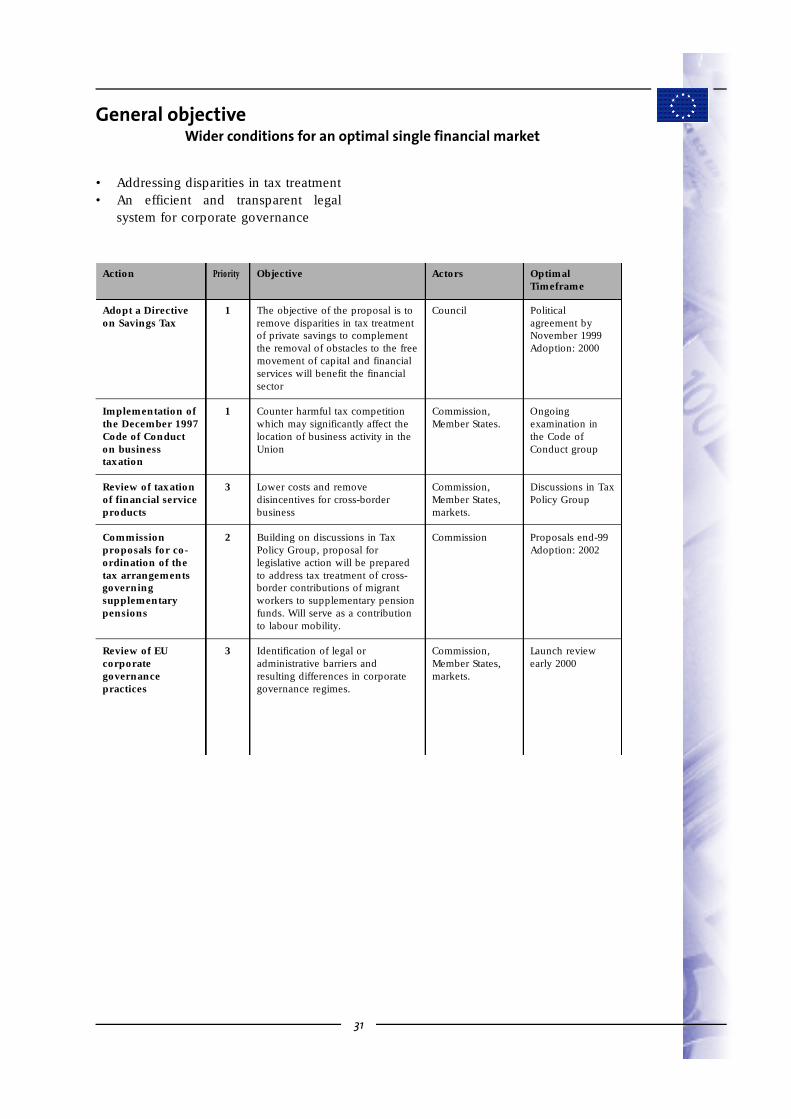

1

1

3

2

3

The objective of the proposal is toremove disparities in tax treatmentof private savings to complementthe removal of obstacles to the freemovement of capital and financialservices will benefit the financialsector

Counter harmful tax competitionwhich may significantly affect thelocation of business activity in theUnion

Lower costs and removedisincentives for cross-borderbusiness

Building on discussions in TaxPolicy Group, proposal forlegislative action will be preparedto address tax treatment of cross-border contributions of migrantworkers to supplementary pensionfunds. Will serve as a contributionto labour mobility.

Identification of legal oradministrative barriers andresulting differences in corporategovernance regimes.

Council

Commission,Member States.

Commission,Member States,markets.

Commission

Commission,Member States,markets.

Politicalagreement byNovember 1999Adoption: 2000

Ongoingexamination inthe Code ofConduct group

Discussions in TaxPolicy Group

Proposals end-99Adoption: 2002

Launch reviewearly 2000

Adopt a Directiveon Savings Tax

Implementation ofthe December 1997Code of Conducton businesstaxation

Review of taxationof financial serviceproducts

Commissionproposals for co-ordination of thetax arrangementsgoverningsupplementarypensions

Review of EUcorporategovernancepractices

![2014 Fall actionplan Forum.pptx [Read-Only] · Microsoft PowerPoint - 2014 Fall actionplan Forum.pptx [Read-Only] Author: wcl6334 Created Date: 11/21/2014 1:34:15 PM ...](https://static.fdocuments.in/doc/165x107/61005dbbf6d54348050e1a82/2014-fall-actionplan-forumpptx-read-only-microsoft-powerpoint-2014-fall-actionplan.jpg)