Financial Results & Business Update · 2020. 1. 24. · (Security code #6787) May 21, 2014...

28

(Security code #6787) May 21, 2014 Financial Results & Business Update FY2013 (Ended March 31, 2014)

Transcript of Financial Results & Business Update · 2020. 1. 24. · (Security code #6787) May 21, 2014...

(Security code #6787) May 21, 2014

Financial Results & Business Update

FY2013 (Ended March 31, 2014)

1

1

2

FY2013 Summary

FY2014 Forecast

2

FY2013 Summary

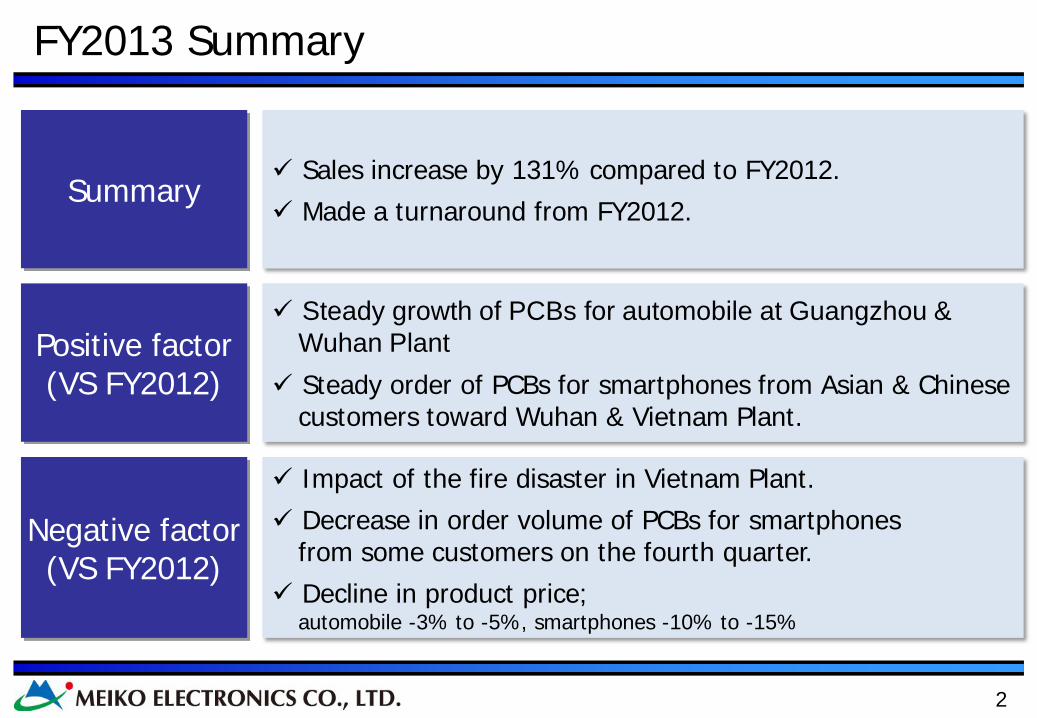

Sales increase by 131% compared to FY2012. Made a turnaround from FY2012.

Summary

Positive factor (VS FY2012)

Negative factor (VS FY2012)

Steady growth of PCBs for automobile at Guangzhou & Wuhan Plant

Steady order of PCBs for smartphones from Asian & Chinese customers toward Wuhan & Vietnam Plant.

Impact of the fire disaster in Vietnam Plant. Decrease in order volume of PCBs for smartphones

from some customers on the fourth quarter. Decline in product price;

automobile -3% to -5%, smartphones -10% to -15%

3

FY2013 Consolidated Financial Results

FY2013 results

FY2012 results

YoY Growth margin

Net sales 79,231 60,709 18,522 130.5%

Operating income

1.2% 922 -1.0% -605 1,527 -

Ordinary income

2.4% 1,931 -0.6% -386 2,317 -

Net income 0.0% 23 -2.6% -1,567 1,590 -

(unit: million of JPY)

4

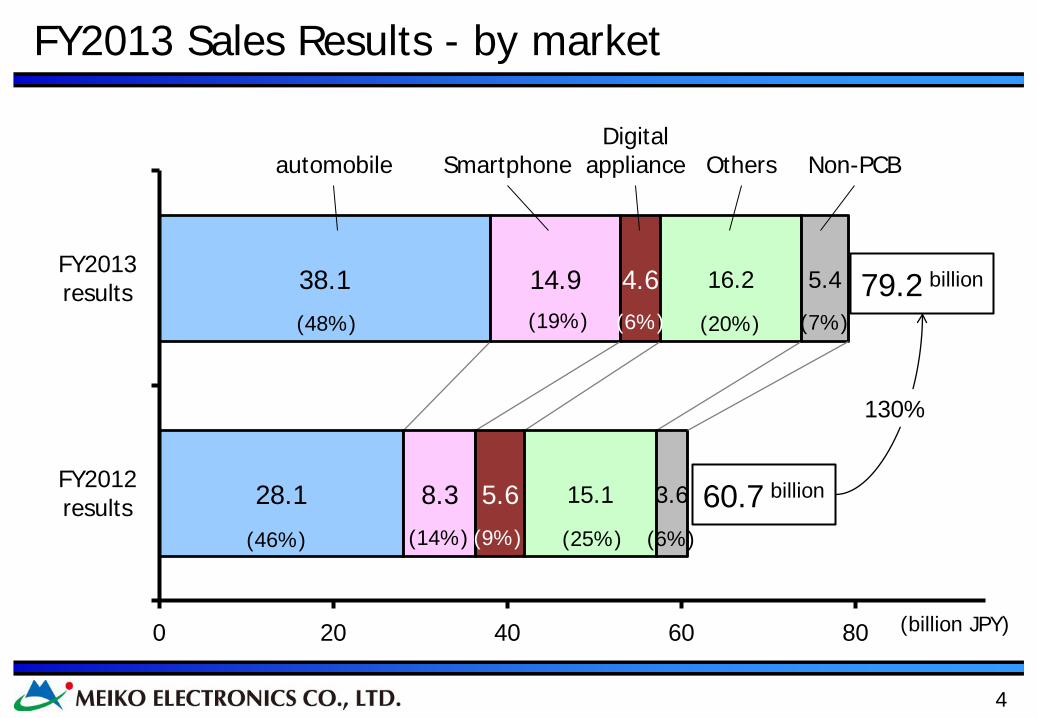

FY2013 Sales Results - by market

28.1

38.1

8.3

14.9

5.6

4.6

15.1

16.2

3.6

5.4

0 20 40 60 80

FY2012 results

FY2013 results

(billion JPY)

automobile Smartphone Digital

appliance Others Non-PCB

79.2 billion

60.7 billion

130%

(48%) (19%) (20%) (7%) (6%)

(46%) (14%) (25%) (6%) (9%)

5

FY2013 Sales Results - by product

6.4

7.3

22

29.9

11.2

12.5

14.3

21.4

3.2

2.7

3.6

5.4

0 20 40 60 80

FY2012 results

FY2013 results

79.2billion

60.7billion

Double-sided 4 layers 6 layers or more Other PCB Non-PCB HDI

(9%) (38%) (27%) (7%) (16%)

(11%) (36%) (24%) (5%) (18%) (6%)

(3%)

(billion JPY)

6

-6.1

86.8

-29.3

-17.4

-3.3 -10.3

-11.3 9.2

-20

0

20

40

60

80

FY2012 FY2013

Marginal profit

increase due to sales growth

Labor cost increase

Utility expense increase

Repair expense increase Other fix cost

increase Sales, general & admin expense increase

Analysis on Variation of Operating Income FY2013

(unit: 100 million JPY)

Improved by 1.5billion JPY

7

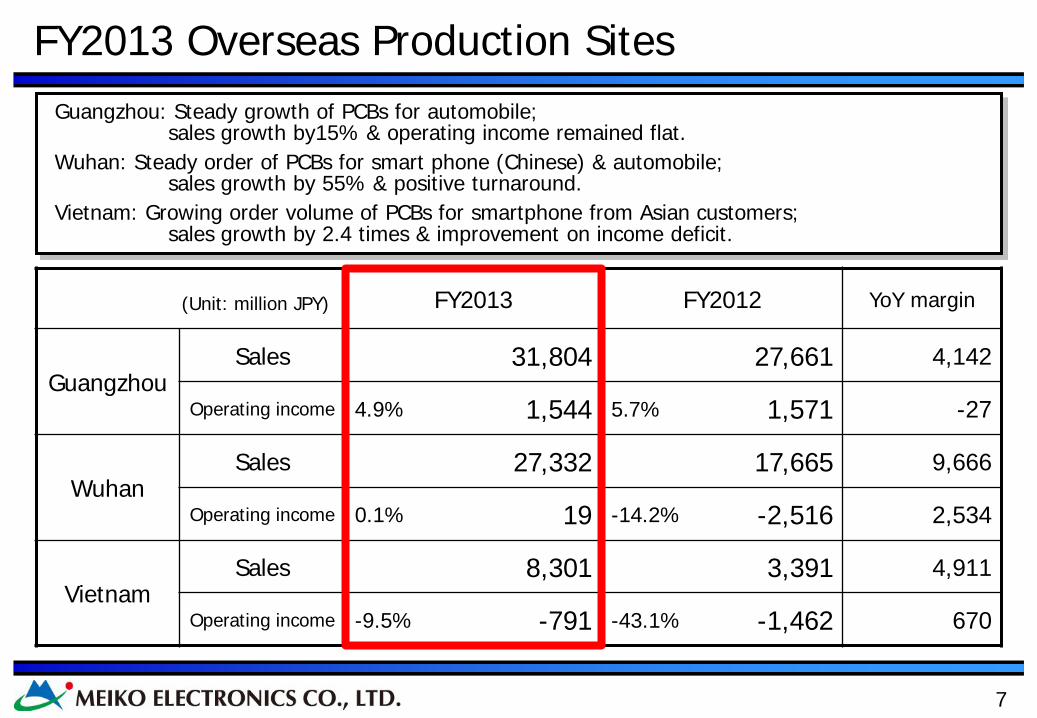

FY2013 Overseas Production Sites Guangzhou: Steady growth of PCBs for automobile;

sales growth by15% & operating income remained flat. Wuhan: Steady order of PCBs for smart phone (Chinese) & automobile;

sales growth by 55% & positive turnaround. Vietnam: Growing order volume of PCBs for smartphone from Asian customers;

sales growth by 2.4 times & improvement on income deficit.

FY2013 FY2012 YoY margin

Guangzhou Sales 31,804 27,661 4,142

Operating income 4.9% 1,544 5.7% 1,571 -27

Wuhan Sales 27,332 17,665 9,666

Operating income 0.1% 19 -14.2% -2,516 2,534

Vietnam Sales 8,301 3,391 4,911

Operating income -9.5% -791 -43.1% -1,462 670

(Unit: million JPY)

8

1

2

FY2013 Summary

FY2014 Forecast

9

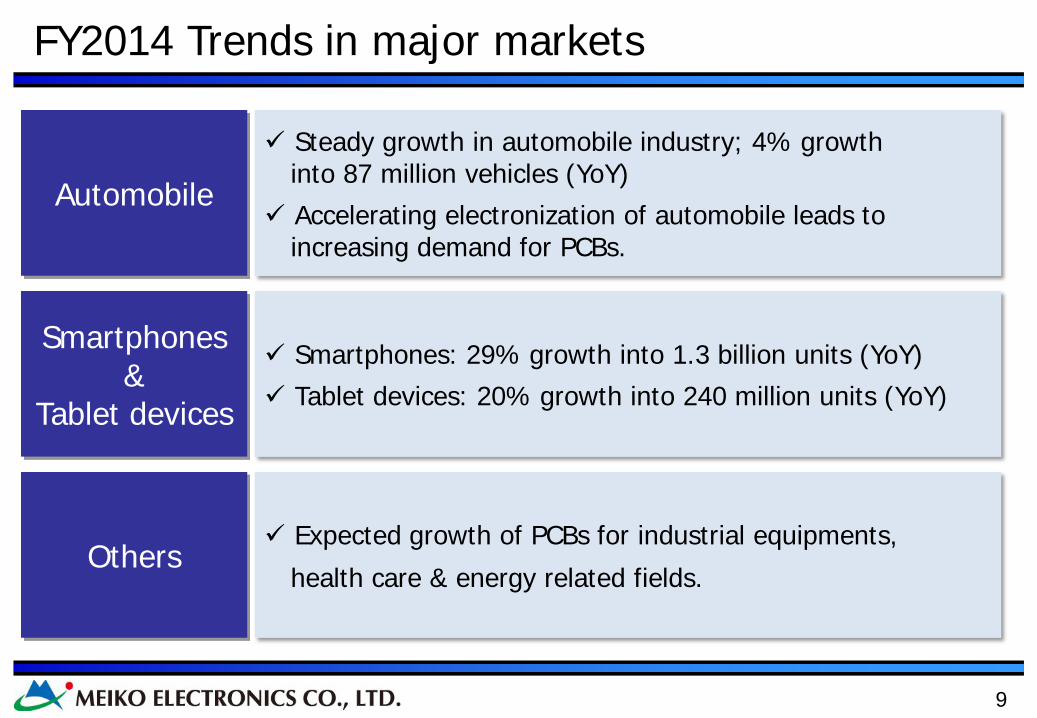

FY2014 Trends in major markets

Expected growth of PCBs for industrial equipments,

health care & energy related fields. Others

Smartphones: 29% growth into 1.3 billion units (YoY) Tablet devices: 20% growth into 240 million units (YoY)

Smartphones &

Tablet devices

Steady growth in automobile industry; 4% growth into 87 million vehicles (YoY)

Accelerating electronization of automobile leads to increasing demand for PCBs.

Automobile

10

FY2014 Business Initiatives

Sales 1. Improving sales structure toward automobile market. 2. Sales promotion for PCBs for high-end smartphones. 3. Generating leads in ASEAN region.

Production 1. Enhancing & developing the production system in Vietnam. 2. Establishing the production basis aiming for No. 1 quality &

capacity of PCBs for automobile.

R&D 1. Developing & launching new products, looking ahead of

customers’ needs. - Automobile: HDI & Radio Frequency (RF) PCB - High-end smartphone: High layer count Anylayer PCB

Expanding sales by centering on automobile & smartphone market. Higher earnings on higher sales through further improvement on quality & cost

reduction.

11

FY2014 Consolidated forecast

FY2014 forecast FY2013 results

YoY margin (ratio)

1st half 2nd half Annual

Net sales 41,500 44,500 86,000 79,231 +6,769 (108.5%)

Operating income

1.6% 4.1% 2.9% 1.2% +1,578 (2.7 times) 670 1,830 2,500 922

Ordinary income

0.6% 2.8% 1.7% 2.4% -431

(77%) 260 1,240 1,500 1,931

Net income 0.2% 1.4% 0.9% 0.0%

+677 (30.4 times) 70 630 700 23

(unit: million of JPY)

12

28.1

38.1

401

8.3

14.9

198

5.6

4.6

4.5

15.1

16.2

165

3.6

5.4

5.1

0 20 40 60 80

FY2012

FY2013

FY2014 forecast

(billion JPY)

(48%) (19%) (20%) (7%) (6%)

(46%) (14%) (25%) (6%) (9%)

(47%) (23%) (19%) (6%) (5%)

79.2billion

60.7billion

130%

86.0billion

109%

Automobile Smartphone Digital

appliance Others Non-PCB

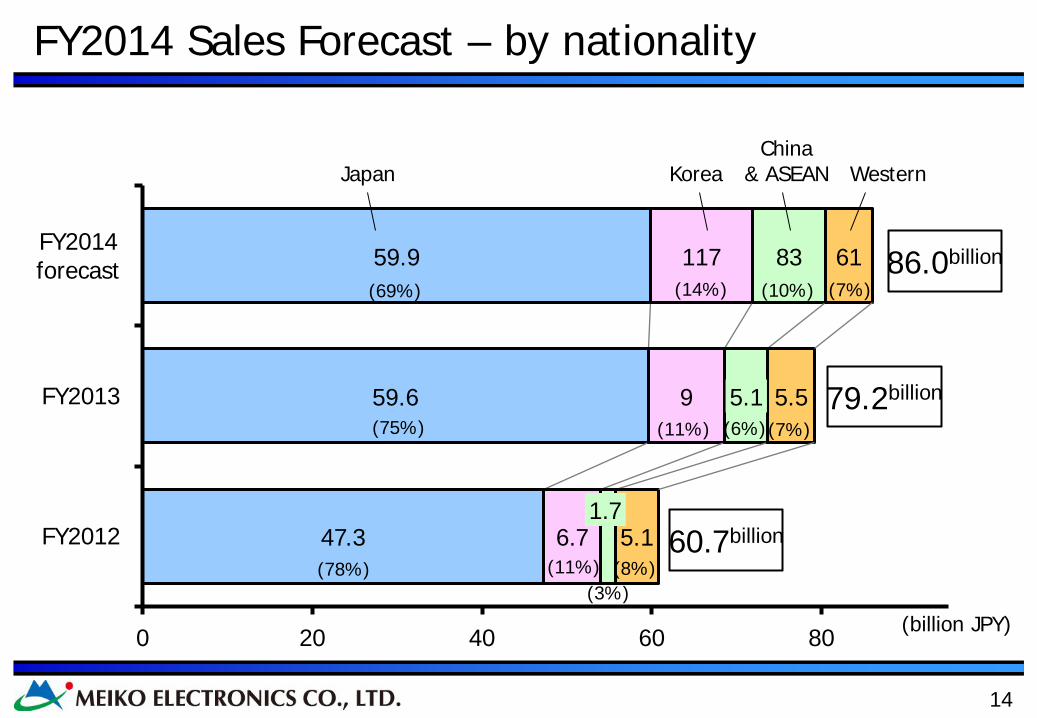

FY2014 Sales Forecast – by market

13

6.4

7.3

7.3

22

29.9

32.6

11.2

12.5

13.4

14.3

21.4

25.5

3.2

2.7

2.1

3.6

5.4

5.1

0 20 40 60 80

FY2012

FY2013

FY2014 forecast

79.2billion

60.7billion

86.0billion (8%) (38%) (30%)

(7%)

(16%) (2%) (6%)

(3%) (27%) (16%) (38%) (9%)

(36%) (11%) (18%) (24%) (5%) (6%)

Double-sided 4 layers 6 layers or more Other PCB Non-PCB HDI

(billion JPY)

FY2014 Sales Forecast – by product

14

47.3

59.6

59.9

6.7

9

117

1.7

5.1

83

5.1

5.5

61

0 20 40 60 80

FY2012

FY2013

FY2014 forecast

Japan Korea China

& ASEAN Western

79.2billion

60.7billion

86.0billion

(11%) (78%)

(18%)

(8%) (3%)

(11%) (75%) (7%) (6%)

(14%) (69%) (7%) (10%)

FY2014 Sales Forecast – by nationality

(billion JPY)

15

9.2

42.1

-14.0

-3.5 -2.2

-3.9 -2.7

25.0

0

20

40

FY2013 FY2014 forecast

(unit: 100 million JPY)

Marginal profit

increase due to sales growth

Labor cost increase

Utility expense increase

Repair expense increase Other fix cost

increase Sales, general & admin expense increase

Improving by 1.58billion JPY

Analysis on Variation of Operating Income FY2014

16

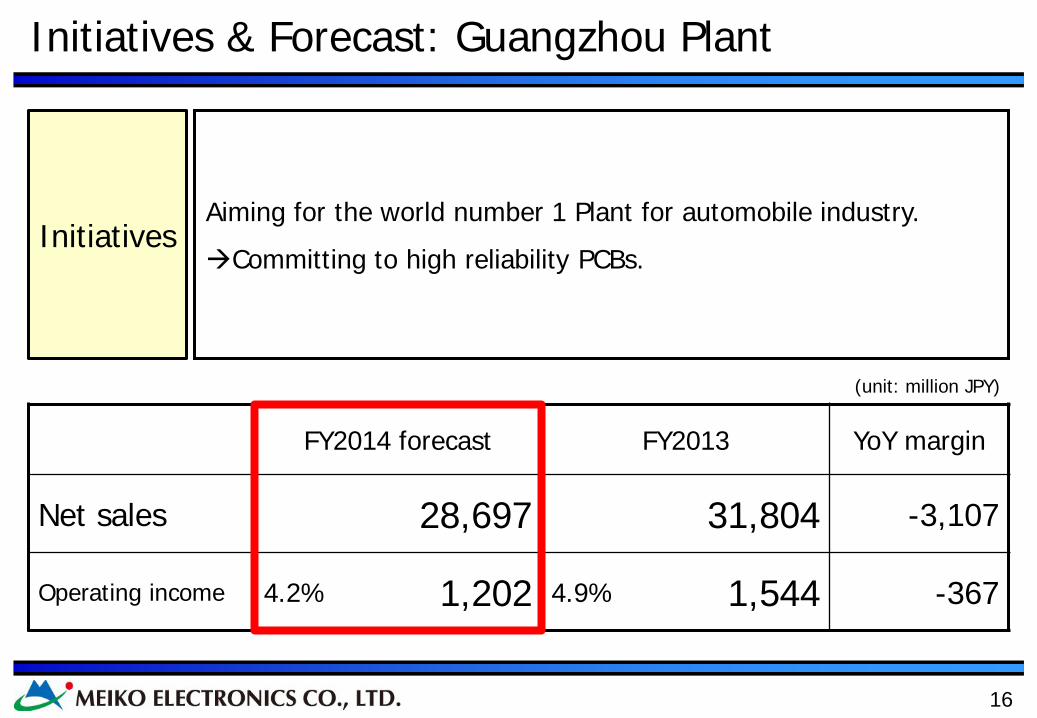

Initiatives & Forecast: Guangzhou Plant

Aiming for the world number 1 Plant for automobile industry.

Committing to high reliability PCBs. Initiatives

FY2014 forecast FY2013 YoY margin

Net sales 28,697 31,804 -3,107

Operating income 4.2% 1,202 4.9% 1,544 -367

(unit: million JPY)

17

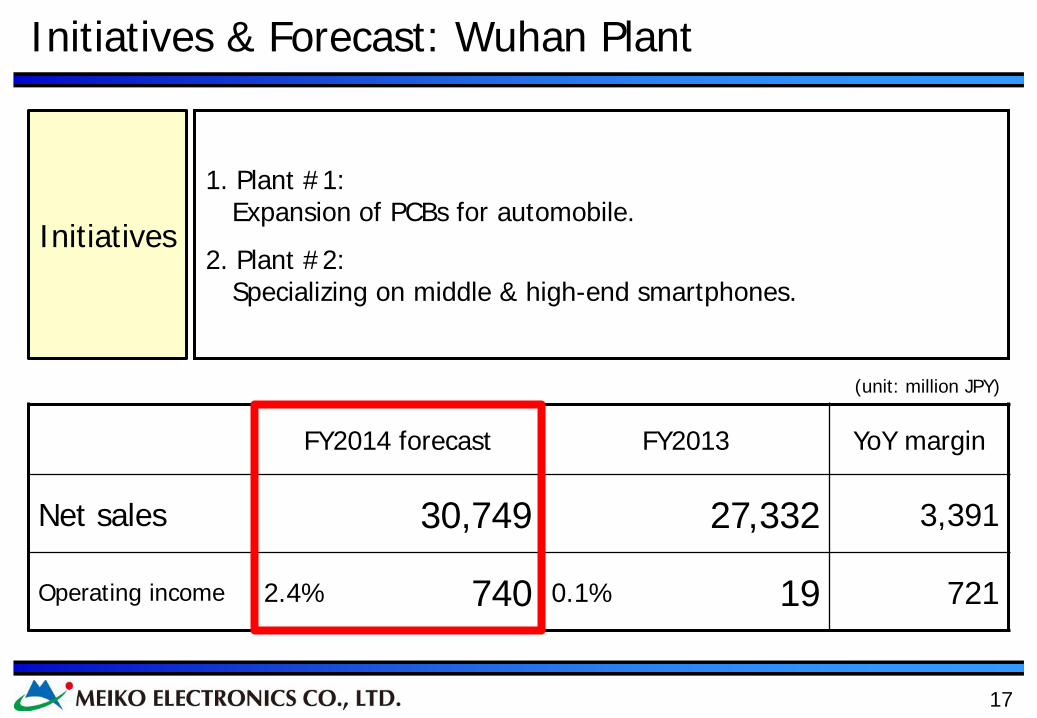

1. Plant #1: Expansion of PCBs for automobile.

2. Plant #2: Specializing on middle & high-end smartphones.

Initiatives

FY2014 forecast FY2013 YoY margin

Net sales 30,749 27,332 3,391

Operating income 2.4% 740 0.1% 19 721

(unit: million JPY)

Initiatives & Forecast: Wuhan Plant

18

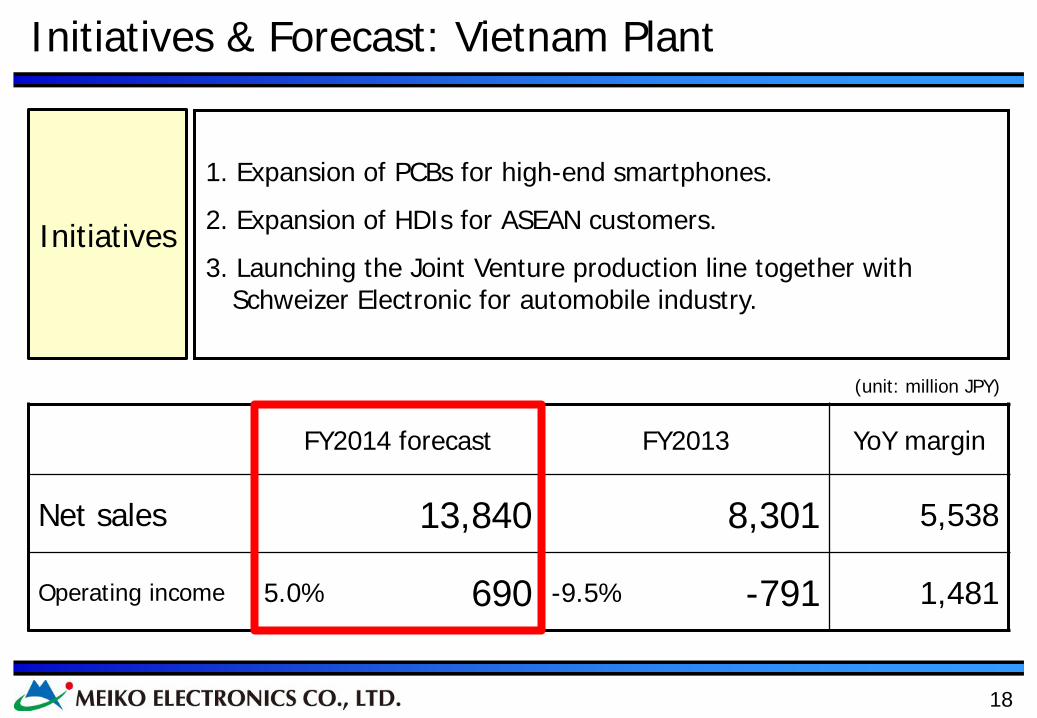

1. Expansion of PCBs for high-end smartphones.

2. Expansion of HDIs for ASEAN customers.

3. Launching the Joint Venture production line together with Schweizer Electronic for automobile industry.

Initiatives

FY2014 forecast FY2013 YoY margin

Net sales 13,840 8,301 5,538

Operating income 5.0% 690 -9.5% -791 1,481

(unit: million JPY)

Initiatives & Forecast: Vietnam Plant

19

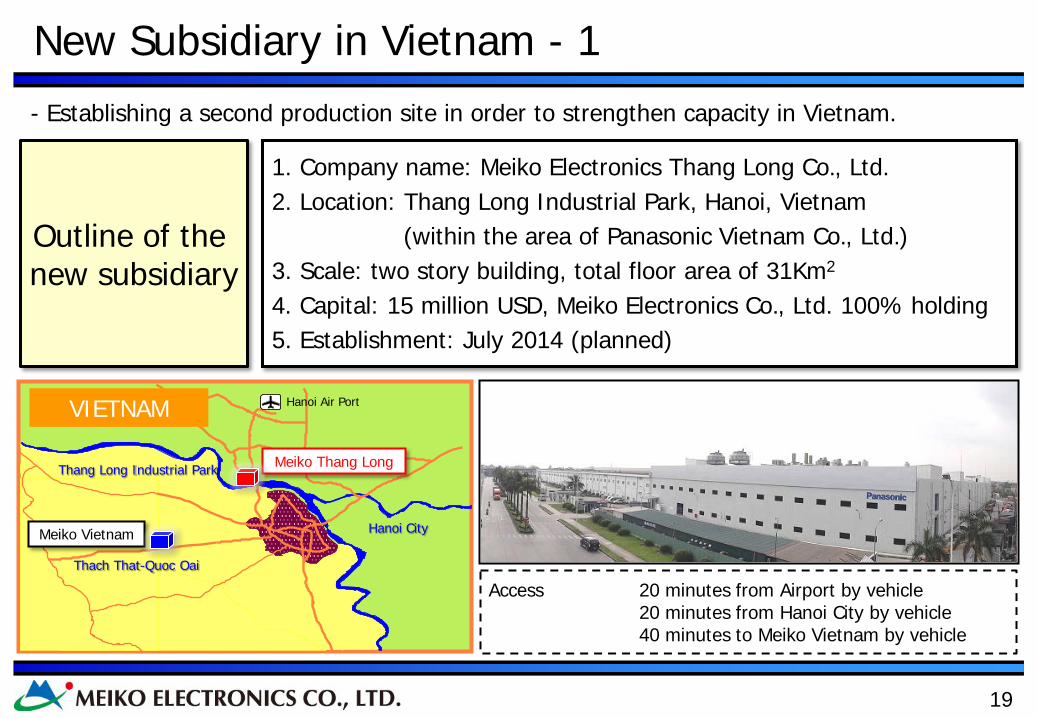

New Subsidiary in Vietnam - 1

1. Company name: Meiko Electronics Thang Long Co., Ltd. 2. Location: Thang Long Industrial Park, Hanoi, Vietnam (within the area of Panasonic Vietnam Co., Ltd.) 3. Scale: two story building, total floor area of 31Km2 4. Capital: 15 million USD, Meiko Electronics Co., Ltd. 100% holding 5. Establishment: July 2014 (planned)

Outline of the new subsidiary

- Establishing a second production site in order to strengthen capacity in Vietnam.

Access 20 minutes from Airport by vehicle 20 minutes from Hanoi City by vehicle 40 minutes to Meiko Vietnam by vehicle

Hanoi City

Hanoi Air Port

Thach That-Quoc Oai

VIETNAM

Thang Long Industrial Park

Meiko Vietnam

Meiko Thang Long

20

New Subsidiary in Vietnam - 2

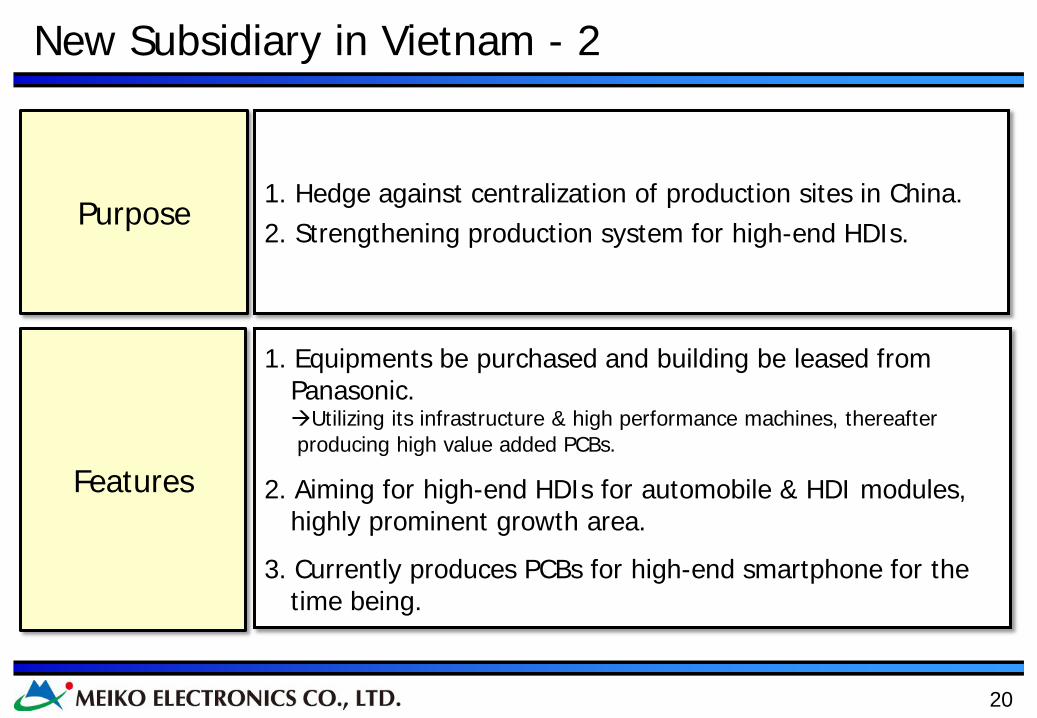

Purpose 1. Hedge against centralization of production sites in China. 2. Strengthening production system for high-end HDIs.

Features

1. Equipments be purchased and building be leased from Panasonic. Utilizing its infrastructure & high performance machines, thereafter producing high value added PCBs.

2. Aiming for high-end HDIs for automobile & HDI modules, highly prominent growth area.

3. Currently produces PCBs for high-end smartphone for the time being.

21

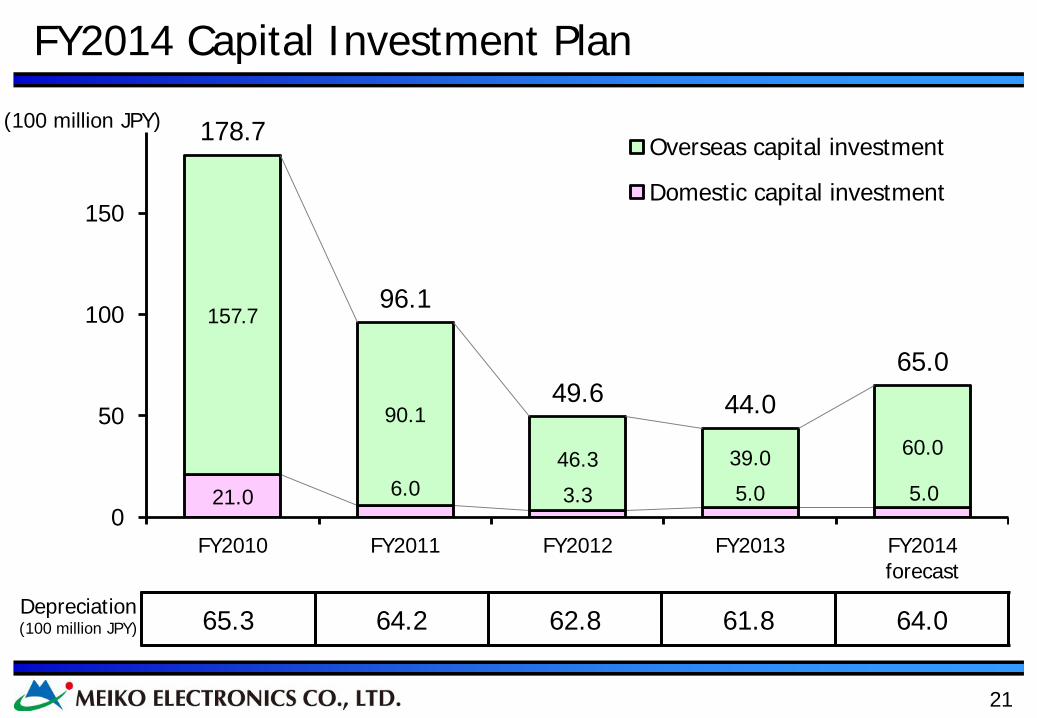

21.0 6.0 3.3 5.0 5.0

157.7

90.1

46.3 39.0 60.0

178.7

96.1

49.6 44.0

65.0

0

50

100

150

FY2010 FY2011 FY2012 FY2013 FY2014 forecast

Overseas capital investment

Domestic capital investment

FY2014 Capital Investment Plan

(100 million JPY)

65.3 64.2 62.8 61.8 64.0 Depreciation (100 million JPY)

22

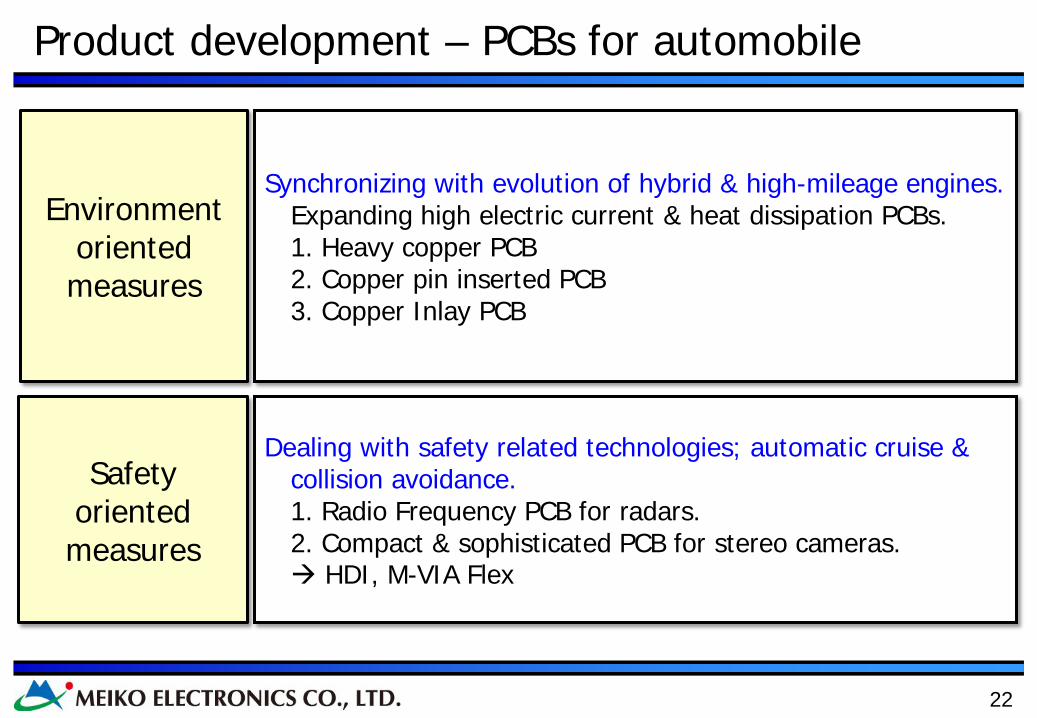

Product development – PCBs for automobile

Environment oriented measures

Safety oriented measures

Synchronizing with evolution of hybrid & high-mileage engines. Expanding high electric current & heat dissipation PCBs. 1. Heavy copper PCB 2. Copper pin inserted PCB 3. Copper Inlay PCB

Dealing with safety related technologies; automatic cruise & collision avoidance.

1. Radio Frequency PCB for radars. 2. Compact & sophisticated PCB for stereo cameras. HDI, M-VIA Flex

23

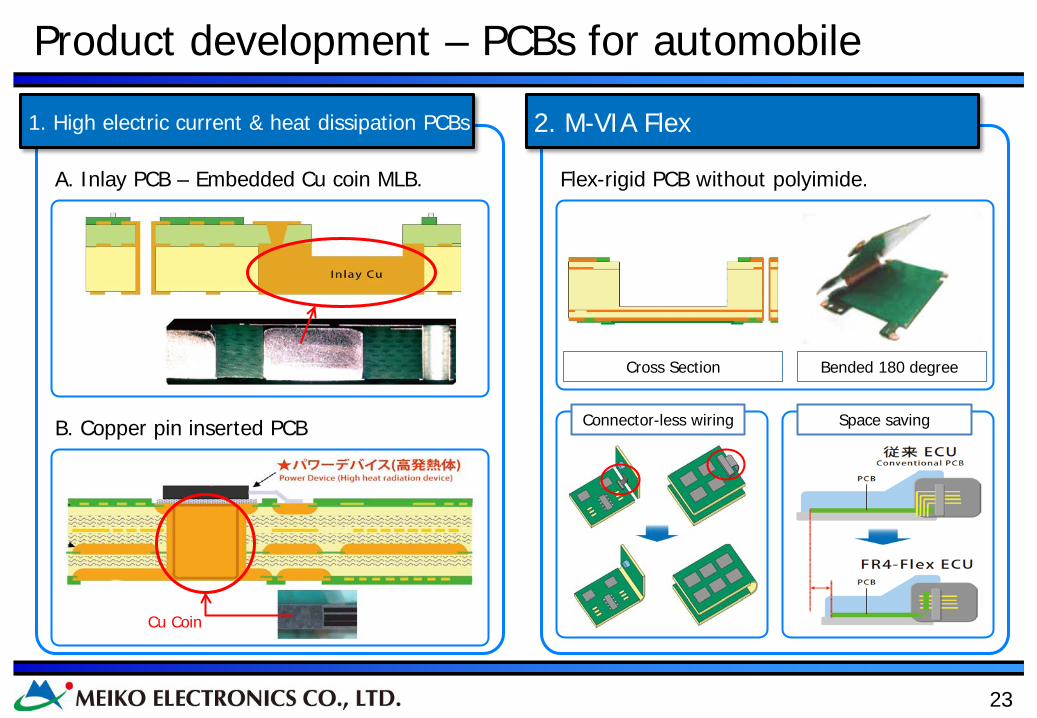

Connector-less wiring Space saving

Cross Section Bended 180 degree

2. M-VIA Flex 1. High electric current & heat dissipation PCBs

Flex-rigid PCB without polyimide.

B. Copper pin inserted PCB

Cu Coin

Product development – PCBs for automobile

A. Inlay PCB – Embedded Cu coin MLB.

24

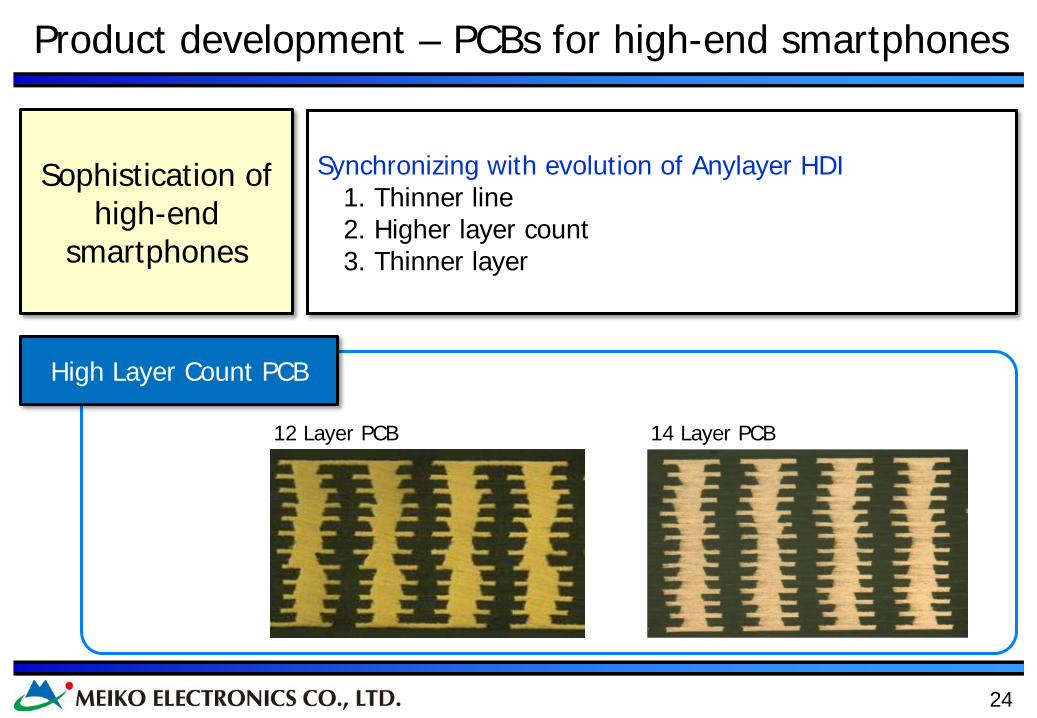

Sophistication of high-end

smartphones

Synchronizing with evolution of Anylayer HDI 1. Thinner line

2. Higher layer count 3. Thinner layer

High Layer Count PCB

12 Layer PCB 14 Layer PCB

Product development – PCBs for high-end smartphones

25

280 352 385 413

331 390 429 446

383

538 666

792

881

730 640

550 1,875

2,010 2,120 2,200

0

500

1,000

1,500

2,000

2013 2014 2015 2016

Feature phone

Low-end smartphone

Middle-end smartphone

High-end smartphone

(million units)

(EM Data Service)

(15%) (18%) (18%) (19%)

(53%)

(64%)

(70%)

(75%)

(100%)

(100%) (100%)

(100%)

Market Trend of Mobile Phones

26

http://www.meiko-elec.com/

27

Disclaimer

This presentation contains forward-looking statements concerning Meiko Group’s future plans, strategies and performance. However, Meiko does not publish this presentation as a disclosure document based on the Financial Instruments and Exchange Act of Japan. These forward-looking statements are not historical facts, rather they represent assumptions and beliefs based on comprehensive data currently available. Furthermore, the Printed Circuit Board business is subject to a number of risks and uncertainties that relate to raw material price, conditions of customers’ market, technological trends, foreign currency exchange rates, tax rules, regulations, disasters, international conflicts and other factors. Meiko therefore wishes to caution that actual results may differ materially from our expectations.

![Results of EGM [Company Update]](https://static.fdocuments.in/doc/165x107/577c7f4b1a28abe054a3ef19/results-of-egm-company-update.jpg)

![Results Press Release & Investor Update [Company Update]](https://static.fdocuments.in/doc/165x107/577cb4891a28aba7118c8067/results-press-release-investor-update-company-update.jpg)

![Financial Results with Results Press Release, Investor Update & Limited Review Report for June 30, 2015 [Company Update]](https://static.fdocuments.in/doc/165x107/577cb40d1a28aba7118c46c3/financial-results-with-results-press-release-investor-update-limited-review.jpg)

![Identification and Characterization of Two Distinct a …cancerres.aacrjournals.org/content/canres/50/21/6787.full.pdf[CANCER RESEARCH 50, 6787-6792. November 1, 1990] Identification](https://static.fdocuments.in/doc/165x107/5b09e6407f8b9a45518b60de/identification-and-characterization-of-two-distinct-a-cancer-research-50-6787-6792.jpg)

![Results Update Presentation [Company Update]](https://static.fdocuments.in/doc/165x107/577ca7a11a28abea748c7c9d/results-update-presentation-company-update.jpg)

![Results Presentation [Company Update]](https://static.fdocuments.in/doc/165x107/577cb4341a28aba7118c5b10/results-presentation-company-update.jpg)