Financial Markets Lec 2

of 66

-

Upload

hrshtkatwala -

Category

Documents

-

view

215 -

download

0

Transcript of Financial Markets Lec 2

-

8/4/2019 Financial Markets Lec 2

1/66

Dr. P.R .KULKARNI

Financial Markets

-

8/4/2019 Financial Markets Lec 2

2/66

Agenda

14 April 2012Dr. P.R Kulkarni2

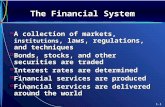

Financial System

Financial Market

Money Market

Call Money

Debt Market

Capital Market

-

8/4/2019 Financial Markets Lec 2

3/66

Financial System

14 April 2012Dr. P.R Kulkarni3

The Financial System represents a channel

through which savings are mobilized through thesurplus units and routed to the deficit units.

-

8/4/2019 Financial Markets Lec 2

4/66

Financial System

Seekers ofFunds (mainly

business firms and

government)

Flow of Funds(Savings)

Suppliers of

Funds (Mainly

Households)

Flow of Financial

Services

Incomes, and FinancialClaims

Functions of Financial System

Savings FunctionLiquidity Function

Payment Function

Risk Function

Information Function

-

8/4/2019 Financial Markets Lec 2

5/66

Importance of Financial System

14 April 2012Dr. P.R Kulkarni5

Only the act of savings will not guaranteeeconomic progress. This is due to the fact thatsavings and investments are usually be carriedout by different groups, savings comes from the

household sector and the investments are beingmade by the corporate sector. Hence, thereshould be a mechanism to ensure that savingsflow from those who save to those who wish toinvest. The process will enable the utilization of

excess idle funds, there by enhancing their value.Enabling such a transfer of funds from the saversto the borrowers is the Financial System

-

8/4/2019 Financial Markets Lec 2

6/66

Functions of Financial System

14 April 2012Dr. P.R Kulkarni6

The role of the Financial system can be broadlyclassified into the following:

1) Savings Function Mobilize savings in a a way toprovide potentially profitable and low risk outlet.

2) Policy FunctionThrough the policy function, theGovernment ensures a smooth flow of funds fromsavings into investments in order to stabilize theeconomy.

3) Credit Function It ensures that these savings will

transform into the necessary credit for investmentand spending purposes.

-

8/4/2019 Financial Markets Lec 2

7/66

Constituents of Financial System

14 April 2012Dr. P.R Kulkarni

7

Financial System

Financial Assets Financial Markets Financial Intermediaries

Forex Market Capital Market Money Market Credit Market

Primary Market

Secondary Market

-

8/4/2019 Financial Markets Lec 2

8/66

Characteristics of Financial MarketsPurpose Players Regulator

Money Market

Short-term Rupee

finance

Banks, Government,

FIs, Corporate, FIIs,MFs, Individuals

RBI

Capital Market

Long-term Rupee

finance

Corporate, Banks, FIs,

Individuals, MFs, FIIs SEBI

Forex Market

Short/Long term

foreign currency

finance

Banks, Corporate,

Forex Dealers RBI

Credit Market

Short/Long term

Rupee finance

Banks, FIs, NBFCs

RBI

14 April 2012Dr. P.R Kulkarni

8

-

8/4/2019 Financial Markets Lec 2

9/66

Financial Market

14 April 2012Dr. P.R Kulkarni

9

Financial System tries to fulfill its role through theFinancial Markets.

Financial Markets aid in increasing production

and income for the various units. It channelize the savings of households and

surplus budget to those institutions that needfund.

The quantum of funds are made available to theborrowers.

-

8/4/2019 Financial Markets Lec 2

10/66

Money Markets

Call Money Market

Treasury Bills

Commercial Paper

Certificate of deposit

MMMFs

Capital Markets

Primary Markets Secondary Markets

Public Issue

Rights Issue

Bonus Issue

Private Placement

Bought-out Deals

Trading Systems

Depositories

Clearing mechanism

Carry Forward System

Settlement Procedure

Financial Markets

-

8/4/2019 Financial Markets Lec 2

11/66

Functions of Financial system

14 April 2012Dr. P.R Kulkarni

11

The saving Function:

Savings find their way into the hands of thosein the production through the financial system.

Financial claims are issued in the money andcapital markets which promise the future

income flow.

The funds with producers result in productionof better goods and services.

-

8/4/2019 Financial Markets Lec 2

12/66

Liquidity Function

14 April 2012Dr. P.R Kulkarni

12

Money in the from of deposits may give lessreturn

One therefore always prefers to store funds infinancial instruments like stocks, bonds,debentures.

In these instruments risk high and less degree ofliquidity.

The financial market provide the investor with the

opportunity to liquidate the investment.

-

8/4/2019 Financial Markets Lec 2

13/66

Payment Function

14 April 2012Dr. P.R Kulkarni

13

The financial system offer a very convenientmode of payment for goods and services.

Cheque and credit card system are easiest wayof payment.

Various payment system are in operation in themodern financial system.

Risk Function: The financial market provide

protection against life, health and income risk. Life insurance and non life insurance are

provided by the financial market.

The income risk is covered the hedge

instruments.

-

8/4/2019 Financial Markets Lec 2

14/66

Financial Market

14 April 2012Dr. P.R Kulkarni

14

Financial market can be defined as the market inwhich financial assets are create or transferred.

Financial markets are some time classified asprimary and secondary market.

The distinction between two market is bases onthe differences in the period of maturity of thefinancial assets issued in these markets

-

8/4/2019 Financial Markets Lec 2

15/66

Types of Markets

14 April 2012Dr. P.R Kulkarni

15

Depending on the differing requirements,various sub-markets have developed. The mainsegments of the organized Financial Marketsare as follows:

1) Money Market The Money Market is a awhole sale debt market for low-risk, high liquid,short-term instruments. Funds are available inthis market for periods ranging from a singleday up to a year. The market is dominated

mostly by Government, Banks and FinancialInstitutions.2) Capital Market The Capital Market is aimed at

financing the long-term investments. Thetransaction taking place in this market will be

for periods over a year

-

8/4/2019 Financial Markets Lec 2

16/66

Money Market

14 April 2012Dr. P.R Kulkarni16

The market that deals with short-term fundsrequirements is called the money market. Thefunds are available for the period of single day toone year. The Government, Banks and the

financial institutions are main players in themoney market. The instruments in the moneymarket are of short-term nature and highly liquid.

-

8/4/2019 Financial Markets Lec 2

17/66

Need for Money Market

14 April 2012Dr. P.R Kulkarni17

Business units in their day-to-day operationswill be placed generally in a surplus or adeficit position in terms of liquidity or cash.When short-term deficits are not adjustedimmediately, it may eventually lead to aLiquidity crisis. This situation will be worse forbanks. On the other hand, in a surplus shortterm funds situation, the businesses will beleft with idle funds for short period of time

making them non-interest bearing. the effectof this will be greatly felt on banks andfinancial institutions which earn profits throughspreads

-

8/4/2019 Financial Markets Lec 2

18/66

Money Market Players

14 April 2012Dr. P.R Kulkarni18

The money market is dominated by a relatively smallnumber of big players. Given below is the list ofintermediaries participating in the money market

Government

Central Bank Banks

Financial Institutions

Corporate Units

Other institutional bodies MFs, FIIs, etc. Discount Houses and Accepted Houses

-

8/4/2019 Financial Markets Lec 2

19/66

Money Market Instruments

14 April 2012Dr. P.R Kulkarni19

With short- term liquidity being the mainpurpose of money market, various instrumentshave been developed to suit these short-termrequirements. For instance the amount required

of funds by banks to meet their statutory reserveswill vary from one day to a fortnight. Similarlycorporate may require funds for their workingcapital purpose for any period up to a year.

Call money market, treasury bills market andmarkets for commercial papers and certificate ofdeposits are some of the examples.

-

8/4/2019 Financial Markets Lec 2

20/66

Call Money Market

14 April 2012Dr. P.R Kulkarni20

In call money market, day to day surplus funds,mostly of banks are traded.

The call money loans are very short term innature and maturity period of these loan varies

from 1to 15 days.

The money that is lend for one is called callmoney

If it is exceed one day but less than 15 days it isreferred as notice money.

Any mount can be lent or borrow at marketinterest rate.

Loan considered as highly liquid.

-

8/4/2019 Financial Markets Lec 2

21/66

Purpose

14 April 2012Dr. P.R Kulkarni21

Bank borrow in call market to

Fill the temporary gap or mismatched in assetsand liability.

Meet sudden demand for fund for large paymentor remittance.

Bank generally borrow from the market to meetCRR requirement.

Location: The call money marker at big industrialcenters such as Mumbai ,Kolkatta, Chennai, Delhiand Ahmedaba

-

8/4/2019 Financial Markets Lec 2

22/66

Participants in Call Money Market

14 April 2012Dr. P.R Kulkarni

22

All scheduled commercial banks private sector,public sector and cooperative banks can operatein this market.

Intermediaries Discount and Finance House of

India (DFHI) and Securities Trading Corporationof India Limited (STCI) are the participants in thelocal call money markets.

-

8/4/2019 Financial Markets Lec 2

23/66

Call Rates

14 April 2012Dr. P.R Kulkarni

23

The interest paid on call loans is known as thecall rates. Though the rate quoted in the market isannualized one, the rate of interest on call moneyis calculated on daily basis. The rate is largely

subjected to influence by the forces of supply anddemand for funds.

-

8/4/2019 Financial Markets Lec 2

24/66

II Certificate of Deposit

14 April 2012Dr. P.R Kulkarni

24

Based on the recommendation of Vaghual CommitteeReport ,RBI formulated a scheme in June 1989 for issueof CD.

Certificate of Deposits are issued by the banks in thefrom of negotiable promissory note and short term

nature.

They are negotiable and are marketable form bearingspecific value and maturity.

They are transferable from one party to other.

CDs are available for subscription for individuals,corporate, companies, trusts NRI ,MFs

CD should be issued in denomination of Rs 1 lakh. Themarket lot (physical or demat) will one lakh or multiple.

-

8/4/2019 Financial Markets Lec 2

25/66

14 April 2012Dr. P.R Kulkarni

25

CD may issued at discounted on the face valuewith the issuing bank FIs having the freedom todetermine the discount rate. The are also issuedon floating rate.

The maturity period of CD should not be less than7 days and more than one year.

FIs can not issue CD for the period less than oneyear and more than three year.

CDs are issued only in dematerialize form.

-

8/4/2019 Financial Markets Lec 2

26/66

Commercial Paper

14 April 2012Dr. P.R Kulkarni

26

Commercial paper (CP) is also money marketinstrument. RBI introduced CP in 1990 enablinghighly rated corporate borrowers to diversify theirsources of borrowings.

CD is an unsecured usance money marketinstrument issued in the from of promissory noteat a discount and is transferable.

CP are issued in denomination of Rs 5Lakh and

multiple thereof. A single investor should notinvest less than Rs 5 lakh of value.

-

8/4/2019 Financial Markets Lec 2

27/66

14 April 2012Dr. P.R Kulkarni

27

All eligible participants have to obtain the creditrating from the credit rating organization.

The minimum rating should be P-2 of CRSIL orsuch equivalent rating by other agencies.

CP can be issued in dematerialized or physicalfrom.

All India financial Institutions and primary dealers

are also allowed to issue CP. CPs are subscribed by individuals, banks,

corporate bodies, NRIs, and FIIs.

CP has minimum maturity period of 15 days and

maximum of one year.

-

8/4/2019 Financial Markets Lec 2

28/66

Eligibility for Corporate

14 April 2012Dr. P.R Kulkarni

28

The net worth of the company should not be lessthan 4 crores.

Company has been sanctioned working capitallimits by the banks.

The borrowed account of the company isclassified as standard account.

-

8/4/2019 Financial Markets Lec 2

29/66

Capital Market

14 April 2012Dr. P.R Kulkarni

29

The capital market provides the resourcesneeded by medium and large scale industries forinvestment purposes. The capital marketfunctions as an institutional mechanism to

channel long term funds from those who save, tothose who need them for productive purposes.

-

8/4/2019 Financial Markets Lec 2

30/66

Structure of Capital Market

14 April 2012Dr. P.R Kulkarni

30

The capital markets consists of the primarymarkets and the secondary markets and there isa close link between them. The primary marketcreates long term instruments through which

corporate entities borrow from the capital market.But the secondary market is the one whichprovides liquidity and marketability to theseinstruments.

-

8/4/2019 Financial Markets Lec 2

31/66

Primary Market

14 April 2012Dr. P.R Kulkarni

31

To meet the financial requirements of theirprojects companies raises capital through issue ofsecurities (shares and debentures)in the primarymarket.

The primary market created long terminstruments through which corporate entitiesborrow from the market.

The secondary market is the one whichprovides liquidity and marketability to these

instruments.

-

8/4/2019 Financial Markets Lec 2

32/66

Types of Issues

14 April 2012Dr. P.R Kulkarni

32

A company can raises the capital through issue ofshares and debentures by means of :

1. Public Issue

2. Right Issue

3. Bonus Issue

4. Private placement

5. Bought out deals

M d f i i i l i

-

8/4/2019 Financial Markets Lec 2

33/66

Modes of raising capital in

Primary Market Public issue: when the securities are issued tomembers of the public it takes the form of public

issue. Most popular method of raising long termfunds. Securities are allotted to the general public.

Rights issue: Where the equity shares of a body

corporate is made to the existing shareholders as apre-emptive right, it takes the form of rights issue.

Private placement: Where the shares of a bodycorporate are sold to a group of small number ofinvestors it takes the form of a private placement.These investors are selected clients such as FIs,corporates, banks and high net worth individuals.

-

8/4/2019 Financial Markets Lec 2

34/66

Bought out deals

14 April 2012Dr. P.R Kulkarni

34

A small project finds it costly to go for the publicissue.

Bought out deals come out to rescue of thepromoters.

Company initially places its equity shares to

sponsors/ merchant bankers. The sponsors areintermediate investors who buy stake in thecompany.

They in turn offload the shares at appropriate

Ab t P bli I

-

8/4/2019 Financial Markets Lec 2

35/66

About Public Issues

Corporate may raise capital in the primary market by

way of an initial public offer, rights issue or privateplacement. An Initial Public Offer (IPO) is the selling ofsecurities to the public in the primary market.

This Initial Public Offering can be made through thefixed price method, book building method or a

combination of both.

-

8/4/2019 Financial Markets Lec 2

36/66

Secondary Market

14 April 2012Dr. P.R Kulkarni

36

The secondary market is that segment of thecapital market where the securities issued in theprimary market are traded.

It provide the liquidity to various financial

instruments.

The secondary market operate through the stockexchanges.

Stock exchanges are regulated under Securitiescontract Regulation Act1956 and SEBI Act 1990.

The stock exchanges are auction market and it ischaracterized by Bull and Bear.

Bull is the buyer in the market. He may take

-

8/4/2019 Financial Markets Lec 2

37/66

Trading System

14 April 2012Dr. P.R Kulkarni

37

Trading system in the stock exchanges wascarried out by public outcry- in the trading ring.

OTCEI is the first exchange to introduce screenbased trading.

Screen based trading received big boost aftersetting up NSE

All big stock exchanges have introduced the

screen based trading. The fully automated trading system enabled

market participants to login order, execute dealand receive online market information.

-

8/4/2019 Financial Markets Lec 2

38/66

Depository

14 April 2012Dr. P.R Kulkarni

38

Certificate form securities led to problem inphysical storage and transfer of securities.

The transaction cost was also very high.

A depository is an entity which hold the securitiesin the electronic form.

Dematerialization is the process by whichphysical certificates are destroyed and equal

number of securities are credited in the accountof creditors.

The risk of bad delivery is eliminated, transactioncost reduced. SEBI mandated compulsory trading

and settlement in dematerialized form. Two

-

8/4/2019 Financial Markets Lec 2

39/66

Settlement System

14 April 2012Dr. P.R Kulkarni

39

Trading in equities is internationally done onrolling settlement basis.

In India, trading settlement s done on T+2

SEBI is encouraging the stock exchanges toshorten their settlement period cycle further toT+1

-

8/4/2019 Financial Markets Lec 2

40/66

Clearing Mechanism

14 April 2012Dr. P.R Kulkarni

40

The clearing Houses attached to stockexchanges functioned as conduits to delivery ofsecurities and money.

The default risk by the counter party in the

transition continued to remain.

National Securities Clearing corporation assumesthe counter party risk in all trading in NSE.

-

8/4/2019 Financial Markets Lec 2

41/66

Margin Money

14 April 2012Dr. P.R Kulkarni

41

Margin money system help for the smoothrunning of stock exchanges. The margin moneysystem has been streamlined.

SEBI has introduced the concept of mark to

market margin.

-

8/4/2019 Financial Markets Lec 2

42/66

Debt Market

14 April 2012Dr. P.R Kulkarni

42

Government securities are the most importantand unique financial instruments in thefinancial markets of any economy. GOI sec.include debt obligations of the centralgovernment, state government and other

financial institutions owned by central andstate governments. As the repayment ofprinciple as well as interest is secured bygovernment, these instruments are usually

referred to as Gilt-edged Securities. Literallygilt means gold, therefore, a gilt-edgedsecurity implies Security of the Best Quality.

-

8/4/2019 Financial Markets Lec 2

43/66

Types

Central Govt. Securities

State Govt. Securities

Securities Guaranteed byCentral Govt.

Securities Guaranteed by

State Govt.

RBI Treasury Bills

Forms

Stock Certificates

Promissory Notes

Bearer Bonds

Treasury Bills

NSC

Deposit Certificates

Annuity Certificates

PPF

Capital Investment

NDC

Government Securities

Primary Markets Secondary Markets

-

8/4/2019 Financial Markets Lec 2

44/66

Government security Market

14 April 2012Dr. P.R Kulkarni

44

The govt securities are issued by Central, State ,local and semi-government authorities SEB,SFCs NABARD etc.

The government securities are issued with the

maturity ranging from 2 to 31 years, Long termabove 10 years, Medium term 5-10 years andshort term below 5 years.

Individuals ,firms, companies, corporate, State

governments, Banks and all India FinancialInstitutions, Trust, MFs PF are allowed to invest.

The minimum amount of investment inGovernment securities for single investor is of Rs10,000 and multi le therof.

-

8/4/2019 Financial Markets Lec 2

45/66

14 April 2012Dr. P.R Kulkarni

45

The RBI issue government stock to investor by

crediting in their subsidiary General Ledger account.

The fixed interest rate in there on time datedsecurities It is called as a coupon rate. Thesesecurities are essentially fixed income securities.

-

8/4/2019 Financial Markets Lec 2

46/66

Primary and secondary Market

14 April 2012Dr. P.R Kulkarni

In the primary market RBI issue notification on behalfof government indicating quantum and date of issue

of securities and coupon rate.

one can submit more than one bid application at

different yield. On the basis bid received , RBI cut of rate of yield for

allocation.

The RBI will issue these securities at premium in a

such way, the yield maturity to bidder will be equal torates at which they have put their funds.

Banks purchase these securities for maintainingSLR

NSE has a wholesale debt market segment on which

-

8/4/2019 Financial Markets Lec 2

47/66

Advantages of investing in Gilts

14 April 2012Dr. P.R Kulkarni

47

As the security is issued by GOI, it has a minimaldefault risk.

Investors have the opportunity to invest in verylong term debt sometimes up to 20 years

because of the long maturity periods.

Tax benefits under section 80L up to Rs. 3000 areavailable with no TDS.

-

8/4/2019 Financial Markets Lec 2

48/66

Treasury Bill Market

A kind of finance bills which are in the natureof promissory notes issued by the Govt for afixed period not exceeding one year,containing a promise to pay the amount stated

therein to the bearer of the instrument areknown as treasury bills.

It is basically an instrument of short term

borrowing by the Government of India

-

8/4/2019 Financial Markets Lec 2

49/66

TBs

Serve as an important tool of monetary management usedby the central bank of the country to infuse liquidity into theeconomy.

Issue procedure:

1. notification 2. tendering (submission oftenders by investors) 3. SGL is maintainedRBI for facilitating purchases and sales bycommercial banks, DFHI,STCI and otherfinancial institutions.4.where this facility is not

available DFHI plays an active role in theprimary auctions etc.

-

8/4/2019 Financial Markets Lec 2

50/66

T-Bills

T-Bills are quoted in yield terms. Y = (100 P) x 365 x 100/ (PXD)

WHERE Y = DISCOUNTED YIELD, P=

Price , and D= Days to maturity

-

8/4/2019 Financial Markets Lec 2

51/66

International Capital Market

14 April 2012Dr. P.R Kulkarni

51

The International capital market traced back to1960 when HNIs in Europe were searching forinvestment avenues.

Until 1970 the international focus on debt finance.

There was restriction on cross border equityinvestment.

The removal exchange control by countries likeUK France ,Japan give boost to equity

investment.

The international capital market also become amajor source of finance for nation with lowinternal savings.

-

International Capital Markets

-

8/4/2019 Financial Markets Lec 2

52/66

Bond Market

Yankee Bonds

Samurai Bonds

Bulldog Bonds

Shibosai Bonds

Equity Market

Foreign Equity Euro Equity

ADR

IDR

GDR

International Capital Markets

Foreign Bonds Euro Bonds

Eurodollar

Euroyen

Europound

-

8/4/2019 Financial Markets Lec 2

53/66

GDR and ADR

14 April 2012Dr. P.R Kulkarni

53

During liberalization many corporate from thedeveloping countries are issuing dollar foreigncurrency denominated equity shares.

The shares issued by the corporate are held by

the depository large international banks. These shares deposited with local custodian

appointed by the depository which issue thereceipt against these shares.

This instrument is called as depository receipts.

The depository receipts are denominated inconvertible currencyusually US Dollar

-

8/4/2019 Financial Markets Lec 2

54/66

14 April 2012Dr. P.R Kulkarni

54

Depository receipt is negotiable certificate issuedby depository banks. It may be listed or traded onmajor exchanges for liquidity purpose.

A GDR is a negotiable instrument which present

publically traded localcurrency equity share. Each depository receipts a specific number of

shares in domestic market. They are entitle fordividend.

ADR is dollar dominated negotiable certificate, itpresent a non US companys publicly traded

equity.

It was devised to help American invest in-

ADR/GDR FEATURES

-

8/4/2019 Financial Markets Lec 2

55/66

ADR/GDR - FEATURES

These are special instruments which are created fromordinary shares to generate funds abroad

The shares of a company are deposited with a bank whichwill issue GDRs and ADRs of equivalent value in a foreigncurrency (normally dollars)

The holder of a GDR does not have voting rights The proceeds are collected in foreign currency thus

enabling the issuer to utilize the same for meeting theforeign exchange component of project cost, repayment of

foreign currency loans, meeting overseas commitmentsand for similar other purposes.

Dividends are paid in Indian rupees due to which theforeign exchange risk or currency risk is placed totally onthe investor

ADR/GDR - FEATURES

-

8/4/2019 Financial Markets Lec 2

56/66

ADR/GDR FEATURES

The GDRs are usually listed at the Luxembourg StockExchange as also traded at two other places besides the

place of listing e.g. on the OTC market in London and onthe private placement market in USA.

An investor who wants to cancel his GDR may do so byadvising the depositary to request the custodian torelease his underlying shares and relinquishing his GDRsin lieu of shares held by the Custodian. The GDR can becanceled only after a cooling-period of 45 days. Thedepositary will instruct the custodian about cancellation ofthe GDR and to release the corresponding shares, collectthe sales proceeds and remit the same abroad.

-

8/4/2019 Financial Markets Lec 2

57/66

ADR/GDR FEATURES Marketing of the GDR issue is done by the investment

banks that manage the road shows, which are

presentations made to potential investors. During theroad shows, an indication of the investor response isobtained. The issuer fixes the range of the issue priceand finally decides on the issue price after assessingthe investor response at the road shows.

Cost of floating an ADR or GDR issue is quite high andis only justifiable if the amount of finance to be raised is

quite large

-

8/4/2019 Financial Markets Lec 2

58/66

14 April 2012Dr. P.R Kulkarni58

GDR and ADR issue should obtain the approvalfrom Government of India, Ministry of Finance.

Bonds: the Indian companies can also raiseforeign currency funds by issuing bonds in

domestic market. Typically a Euro-bonds are issued outside the

country of the currency in which it is dominated.They are listed one or more stock exchanges.

The bonds may be fixed rate bonds or Floatingrate notes.

-

8/4/2019 Financial Markets Lec 2

59/66

Foreign Bonds

14 April 2012Dr. P.R Kulkarni59

These are lesser known bonds issued by foreignentities for raising medium to long-term funds

Yankee Bonds : These are US dollardenominated bonds issued by foreign borrowers

in the US bond market. Samurai Bonds these bonds are issued by no-

Japanese borrower in the domestic JapanMarket.

Bulldog Bonds: These are sterling denominatedbonds which are issued in UK domestic market.

ECB; External commercial borrowing are the

borrowing of Indian corporate made outside India.-

-

8/4/2019 Financial Markets Lec 2

60/66

Derivatives Market

Types

Forwards

Futures

Options

Swaps

Players:

Hedgers

Speculators

Arbitrageurs

Financial Institutions

-

8/4/2019 Financial Markets Lec 2

61/66

Financial Institutions

IDBI

IFCI

ICICI

IIBI

EXIM Bank

SFCs

SIDCs

Investment Institutions

LIC

GIC

UTI

Other Mutual

Funds

-

8/4/2019 Financial Markets Lec 2

62/66

Non-Scheduled Banks Scheduled Banks

Commercial Banks State Cooperative Banks

Reserve Bank of IndiaFunctions: Currency Issue; Bankers Bank; Banker to Government;

Credit Control ; Creation of Money

Indian Banks Foreign Banks

Public Sector Private Sector

Other Nationalized BanksSBI & Subsidiaries Regional Rural Banks

-

8/4/2019 Financial Markets Lec 2

63/66

Financial Sector Reforms

Privatization of Banks

IRDA Established to regulate the Insurance Sector(both Life Insurance & General Insurance)

Non Banking Financial Companies (NBFCs)Investment Trusts/ Companies

Nidhis

Merchant Banks

Hire Purchase Finance Companies

Lease Finance Companies

Housing Finance Companies

National Housing Bank

Venture Capital Funding Companies

-

8/4/2019 Financial Markets Lec 2

64/66

SEBI

14 April 2012Dr. P.R Kulkarni64

The Capital Issue controls on issue of the Capital bythe companies have been substituted by thetransparent and simplified guidelines issued by theSEBI under the SEBI Act,1992. Functions of SEBI arefollowing:

Promote fair dealings by the issuers of securities andensure a market place where funds can be raised at arelatively low cost.

Provide a degree of protection to the investors andsafeguard their rights and interests.

Regulate and develop a code of conduct and fairpractices by intermediaries in the capital market.

-

8/4/2019 Financial Markets Lec 2

65/66

Thank you

-

8/4/2019 Financial Markets Lec 2

66/66

14 A il 2012D PR K lk i