Financial Instruments: FX Market

52

Financial Instruments: FX Market Alexander Pisanov FXMM Research Analyst Bank of Russia

-

Upload

alexander-pisanov -

Category

Economy & Finance

-

view

119 -

download

0

Transcript of Financial Instruments: FX Market

Financial Instruments: FX Market

Alexander Pisanov FXMM Research Analyst

Bank of Russia

Outline

• FX instruments overview

• Interest Rate Parity

• Triangular arbitrage

• FX instruments pricing

• Case study: RUB FX spot market

• Useful information

20.10.2016 2

FX instruments overview

20.10.2016 3

FX instruments overview

5 asset classes with different underlying assets:

• Equity: asset is a stock

• Fixed Income: asset is a loan

• Commodities: asset is a commodity

• Real Estate: asset is a real estate object

• FX: asset is a foreign currency

20.10.2016 4

FX instruments overview

FX:

• Spot

• Derivatives (everything else):

– FX derivatives: forwards, futures, options

– FX/IR derivatives: currency swaps, swaptions

When we say “spot” we mean either the above-mentioned classification or the particular term of settlement (spot settlement = T+2). Hereinafter we’ll use the word “spot” to refer to our classification. We’ll dive into the details about each class shortly.

20.10.2016 5

FX instruments overview

Buying into an asset class requires a transaction (trade). If we speak about FX, it is a conversion one. As a result of the trade, you may own a “physical” foreign currency (FX spot):

• FX spot trade – when a trader pays an amount A of currency 1 and gets an amount B of currency 2

• A/B is the exchange rate (ER) for the trade

20.10.2016 6

FX instruments overview

FX spot trades are settled in T+2. But maybe you don’t want to settle in T+2. You can negotiate to make a conversion trade later at a preset ER. This is an FX forward contract:

• FX forward contract – a conversion trade with settlement > T+2

• Generally, settlement may be “physical” (FX spot delivery) or “cash” (on the next page!)

20.10.2016 7

FX instruments overview

FX forwards may be:

• With physical settlement (deliverable). It is when we move the whole notional amount at expiry

• With cash settlement (non-deliverable, NDF). It is when we move only the difference between the negotiated ER an some “reference” ER

20.10.2016 8

FX instruments overview

When negotiating an FX forward, you should set a bulk of parameters. If we “standardize” the bulk and centralize trading, clearing and settlement, we get an FX futures:

• FX futures is a standardized FX forward

• Centralization means that you trade, clear and settle your transactions through a single venue (single for each stage)

20.10.2016 9

FX instruments overview

Most popular MOEX FX futures: Si (USDRUB)

20.10.2016 10

FX instruments overview

You may want to trade a right to make an FX trade at some point in the future with an ER agreed now. This is an FX option contract. As forwards or futures, options break down into:

• Deliverable

• Non-deliverable (NDO)

We can also distinguish between exchange-traded and OTC-traded options. We won’t discuss options as only an introduction will eat the whole lecture.

20.10.2016 11

FX instruments overview

Next are currency swap contracts:

• A currency swap is when a trader borrows an amount A of currency 1, and simultaneously lends an amount B of currency 2

• It is an FX/IR instrument because you can’t simply separate its “credit” features from its “FX” features

20.10.2016 12

FX instruments overview

By settlement rules, currency swaps are:

• FX swaps

• Cross-currency swaps

In general, FX swaps and cross-currency swaps are the same in terms of structure and pricing.

Depending on an agreed interest rate, cross-currency swaps can be further broken down into floating-for-floating (also known as basis) and fixed-for-floating. However, we won’t discuss this taxonomy here.

20.10.2016 13

FX instruments overview

Let’s consider an FX swap. It comprises 2 “legs”:

• First you lend an amount A of currency 1 and borrow an amount B of currency 2

• After a while you get your currency 1 in an amount of A + interest and pay currency 2 in an amount of B + interest

In practice, the interest is paid in one of the currencies, namely quote currency. The rate is therefore adjusted to “incorporate” the second rate.

20.10.2016 14

FX instruments overview

The whole structure is that simple

20.10.2016 15

FX instruments overview

In other words,

• You trade currency 1 for 2 at an ER = A/B

• Then you do a reverse at an ER = (A+a)/(B+b)

Hmm… These are 2 FX trades! So FX swaps can be viewed as pairs of FX trades (typically spot and forward).

20.10.2016 16

FX instruments overview

Cross-currency swap is essentially the same, but it involves periodic interest payments in each of the currencies. After you get the point, you may want to trade a right to make a currency swap. This would be an FX swaption contract.

20.10.2016 17

Interest Rate Parity

20.10.2016 18

Interest Rate Parity

How would you price FX instruments?

• Concept of deterministic fair value?

• Theoretical models?

• Derivatives?

20.10.2016 19

Interest Rate Parity

20.10.2016 20

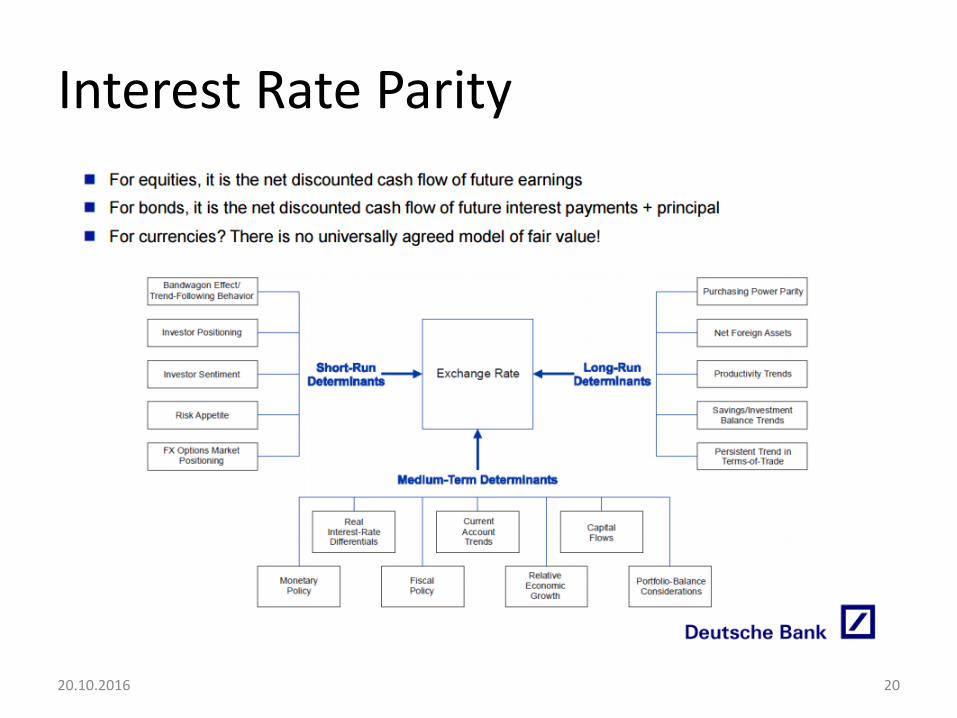

Interest Rate Parity

There is no deterministic fair exchange rate. However, every currency pays some interest rate, so you earn a return on some asset in this currency. Some points arise:

• Different currencies = different interest rates

• Different rates = different returns on assets

• Different returns maybe on “same” assets

• But there must be no arbitrage…

20.10.2016 21

Interest Rate Parity

Interest Rate Parity is a no-arbitrage condition for assets denominated in different currencies to pay the same risk-adjusted return. Assumptions: perfect capital mobility, perfect substitutability between domestic and foreign assets. Two forms:

• Uncovered Interest Parity (UIP)

• Covered Interest Parity (CIP)

20.10.2016 22

Interest Rate Parity

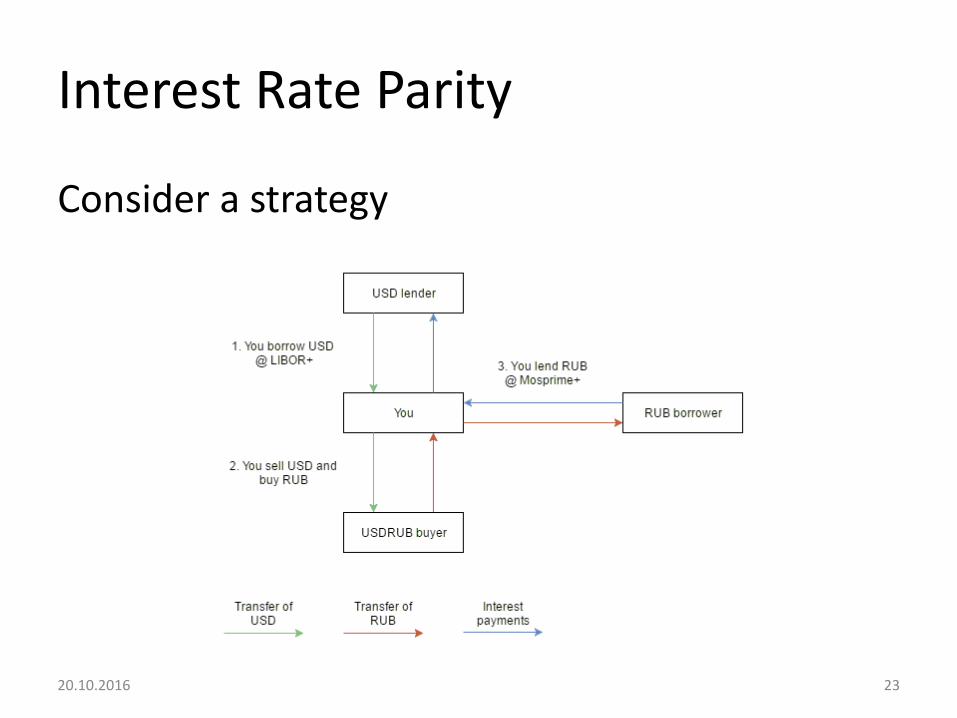

Consider a strategy

20.10.2016 23

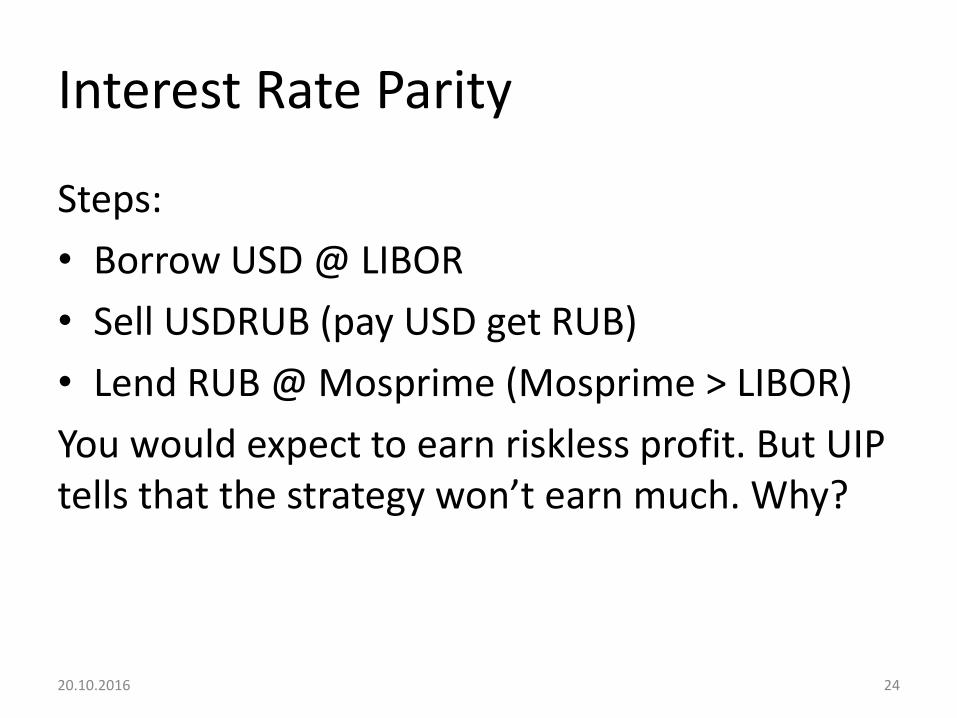

Interest Rate Parity

Steps:

• Borrow USD @ LIBOR

• Sell USDRUB (pay USD get RUB)

• Lend RUB @ Mosprime (Mosprime > LIBOR)

You would expect to earn riskless profit. But UIP tells that the strategy won’t earn much. Why?

20.10.2016 24

Interest Rate Parity

This is what UIP tells us:

• 1 + 𝑟𝑅𝑈𝐵,𝑡 =𝐸 𝑈𝑆𝐷𝑅𝑈𝐵𝑡

𝑈𝑆𝐷𝑅𝑈𝐵01 + 𝑟𝑈𝑆𝐷,𝑡

• USDRUB will rise so that in USD terms, RUB profits will deteriorate to make final return equal to that earned by a smaller USD rate

20.10.2016 25

Interest Rate Parity

Generally UIP doesn’t hold. Partly because when you make that trade you expose yourself to FX risk and your profits are not arbitrage profits, meaning that there is already no arbitrage.

20.10.2016 26

Interest Rate Parity

Consider a slightly different strategy

20.10.2016 27

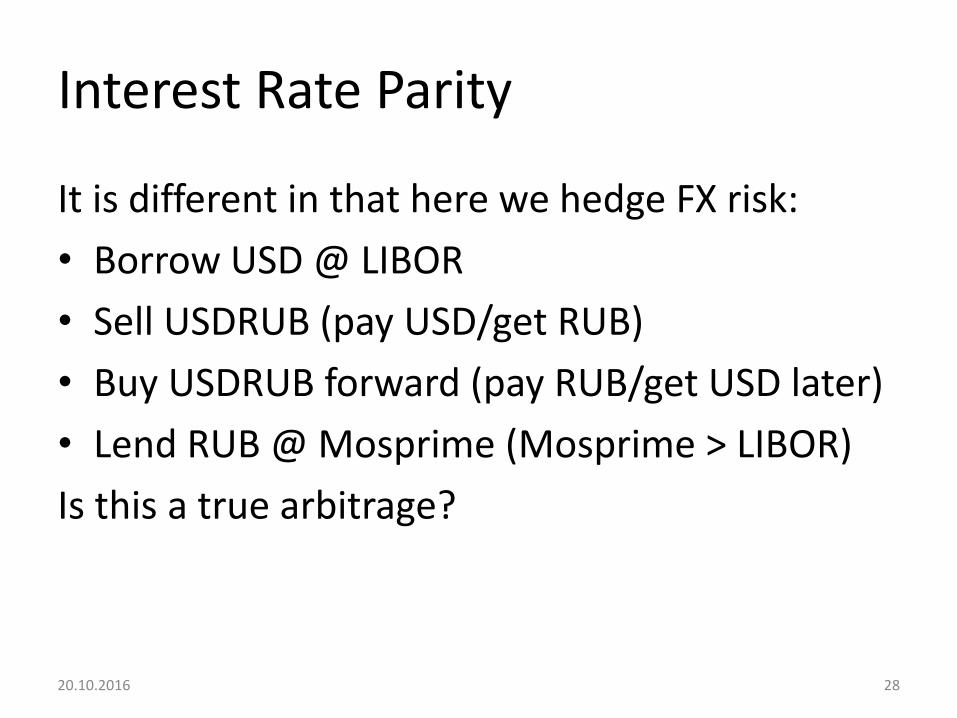

Interest Rate Parity

It is different in that here we hedge FX risk:

• Borrow USD @ LIBOR

• Sell USDRUB (pay USD/get RUB)

• Buy USDRUB forward (pay RUB/get USD later)

• Lend RUB @ Mosprime (Mosprime > LIBOR)

Is this a true arbitrage?

20.10.2016 28

Interest Rate Parity

Yes. And that’s why CIP holds:

• 1 + 𝑟𝑅𝑈𝐵,𝑡 =𝐹 𝑈𝑆𝐷𝑅𝑈𝐵𝑡

𝑈𝑆𝐷𝑅𝑈𝐵01 + 𝑟𝑈𝑆𝐷,𝑡

• If it wouldn’t, you could do it infinitely many times with infinite leverage and become rich!

• But your counterparty setting a forward exchange rate knows about CIP, so the premium is such that you can’t do it

20.10.2016 29

Triangular arbitrage

20.10.2016 30

Triangular arbitrage

Another effective no-arbitrage condition to remember. What if you open your trading station and observe the following:

• 𝑈𝑆𝐷𝑅𝑈𝐵𝑎𝑠𝑘 = 65

• 𝐸𝑈𝑅𝑅𝑈𝐵𝑏𝑖𝑑 = 75

• 𝐸𝑈𝑅𝑈𝑆𝐷𝑎𝑠𝑘 = 1?

20.10.2016 31

Triangular arbitrage

If you are a RUB investor, you can earn riskless profit by making a triangular arbitrage trade:

• Buy USDRUB @ 65 (-65 rub/+1 dollar)

• Buy EURUSD @ 1 (-1 dollar/+1 euro)

• Sell EURRUB @ 75 (-1 euro/+75 rub)

Triangular arbitrage makes cross-rates closely tied. It is an extension of a concept of arbitrage.

20.10.2016 32

FX instruments pricing

20.10.2016 33

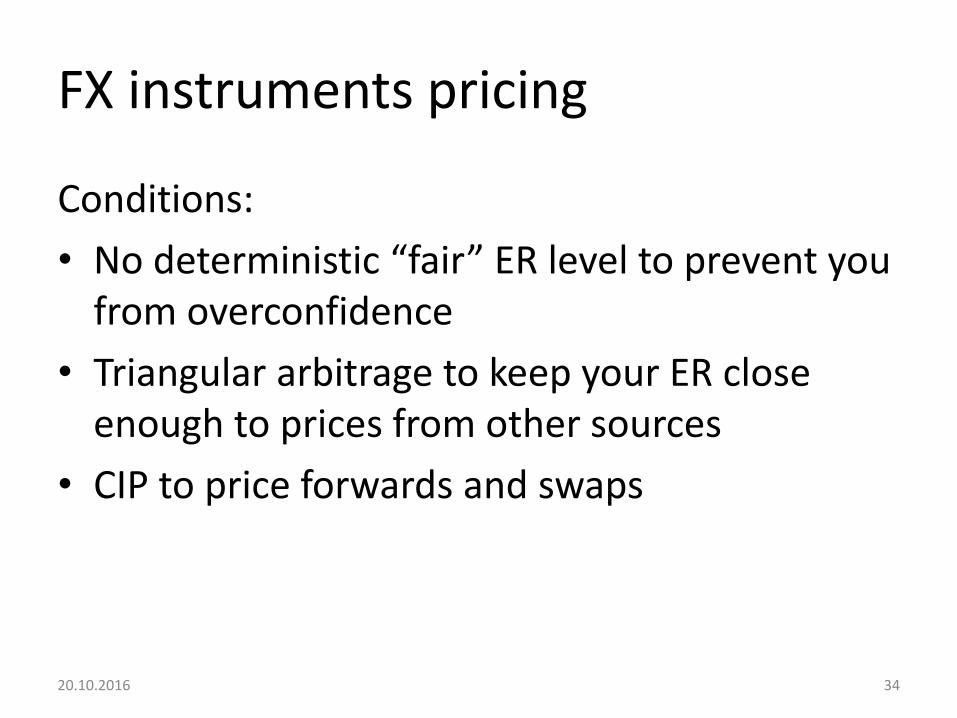

FX instruments pricing

Conditions:

• No deterministic “fair” ER level to prevent you from overconfidence

• Triangular arbitrage to keep your ER close enough to prices from other sources

• CIP to price forwards and swaps

20.10.2016 34

FX instruments pricing

At any time we observe some ER at which we can make an FX spot trade. Recalling CIP, it’s easy to price an FX forward for period t:

• 𝐹 𝑋𝑌𝑡 =1+𝑟𝑌,𝑡

1+𝑟𝑋,𝑡𝑆(𝑋𝑌)

• Here X is base currency, Y is quote currency

• 𝑟∗,𝑡 is interest rate for term t (not annualized!)

20.10.2016 35

FX instruments pricing

Recall that FX swaps can be viewed as a pair of spot and forward trades. Given that, FX swaps are easily priced as a pair of FX trades:

• 1st leg ER is a prevailing ER (usually ER fixing)

• 2nd leg is priced with CIP like an FX forward

• In the market, FX forwards and swaps are quoted as “points”: 𝐹 𝑋𝑌𝑡 − 𝑆(𝑋𝑌)

20.10.2016 36

FX instruments pricing

20.10.2016 37

FX instruments pricing

FX forward example (data for 14.10.2016):

• 3M USD LIBOR rate = 0.88167%

• 3M Mosprime rate = 10.58%

• UDSRUB ER fixing = 62.9493

• 𝐹 𝑈𝑆𝐷𝑅𝑈𝐵3𝑀 =

=1 + 0.1058 ∗

14

1 + 0.0088167 ∗14

∗ 62.9493 = 64.48265

20.10.2016 38

FX instruments pricing

20.10.2016 39

FX instruments pricing

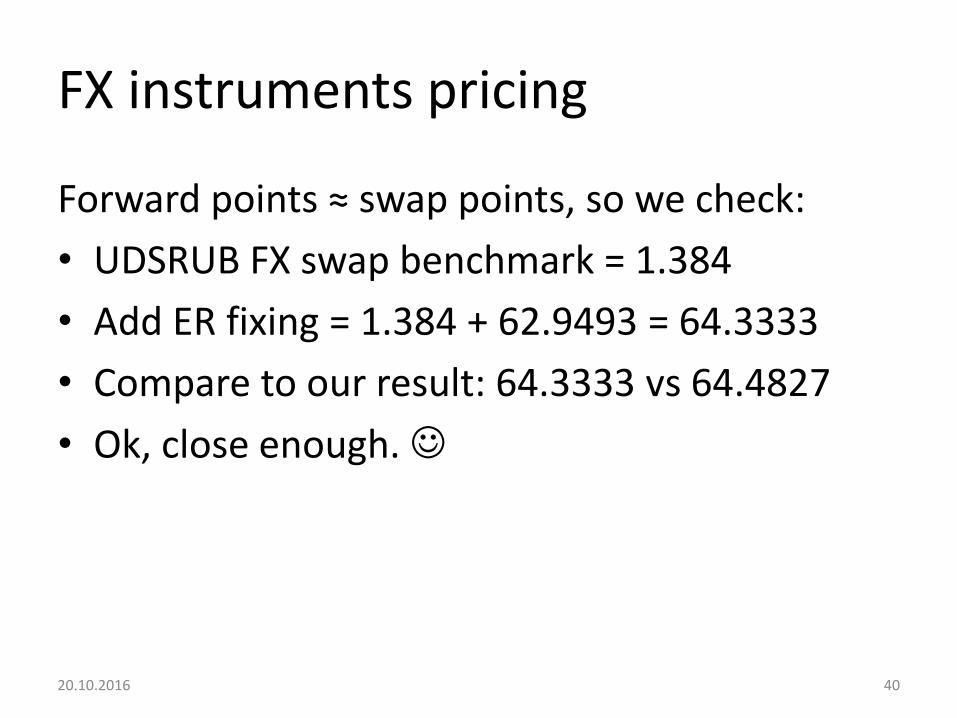

Forward points ≈ swap points, so we check:

• UDSRUB FX swap benchmark = 1.384

• Add ER fixing = 1.384 + 62.9493 = 64.3333

• Compare to our result: 64.3333 vs 64.4827

• Ok, close enough.

20.10.2016 40

FX instruments pricing

Currency swaps are priced as two parallel loans according to interest rate term structures within each of the currencies. The amount of interest is the same as with FX swaps. Currency swaps are quoted as fixed interest rates or spreads over non-USD benchmark interest rate (for basis).

20.10.2016 41

Case study: RUB FX spot market

20.10.2016 42

Case study: RUB FX spot market

Facts about RUB FX spot market:

• Floating exchange rate regime since 2014

• Dominated by trading through MOEX

• Primarily deliverable trading onshore

• Primarily NDFs trading offshore

• Rich set of participants

20.10.2016 43

Case study: RUB FX spot market

MOEX FX section

20.10.2016 44

Case study: RUB FX spot market

02468101214161820

50

55

60

65

70

75

80

85

90

11

.01

.16

22

.01

.16

04

.02

.16

17

.02

.16

02

.03

.16

17

.03

.16

30

.03

.16

12

.04

.16

25

.04

.16

11

.05

.16

24

.05

.16

06

.06

.16

20

.06

.16

01

.07

.16

14

.07

.16

27

.07

.16

09

.08

.16

22

.08

.16

02

.09

.16

15

.09

.16

28

.09

.16

11

.10

.16

USDRUB ER and onshore spot trading volume (source: cbr.ru)

MOEX Interbank USDRUB_TOM

20.10.2016 45

Case study: RUB FX spot market

-1500

-1000

-500

0

500

1000

1500

11

.01

.16

18

.01

.16

25

.01

.16

01

.02

.16

08

.02

.16

15

.02

.16

20

.02

.16

01

.03

.16

10

.03

.16

17

.03

.16

24

.03

.16

31

.03

.16

07

.04

.16

14

.04

.16

21

.04

.16

28

.04

.16

10

.05

.16

17

.05

.16

24

.05

.16

31

.05

.16

07

.06

.16

15

.06

.16

22

.06

.16

29

.06

.16

06

.07

.16

13

.07

.16

20

.07

.16

27

.07

.16

03

.08

.16

10

.08

.16

17

.08

.16

24

.08

.16

31

.08

.16

07

.09

.16

14

.09

.16

21

.09

.16

28

.09

.16

05

.10

.16

12

.10

.16

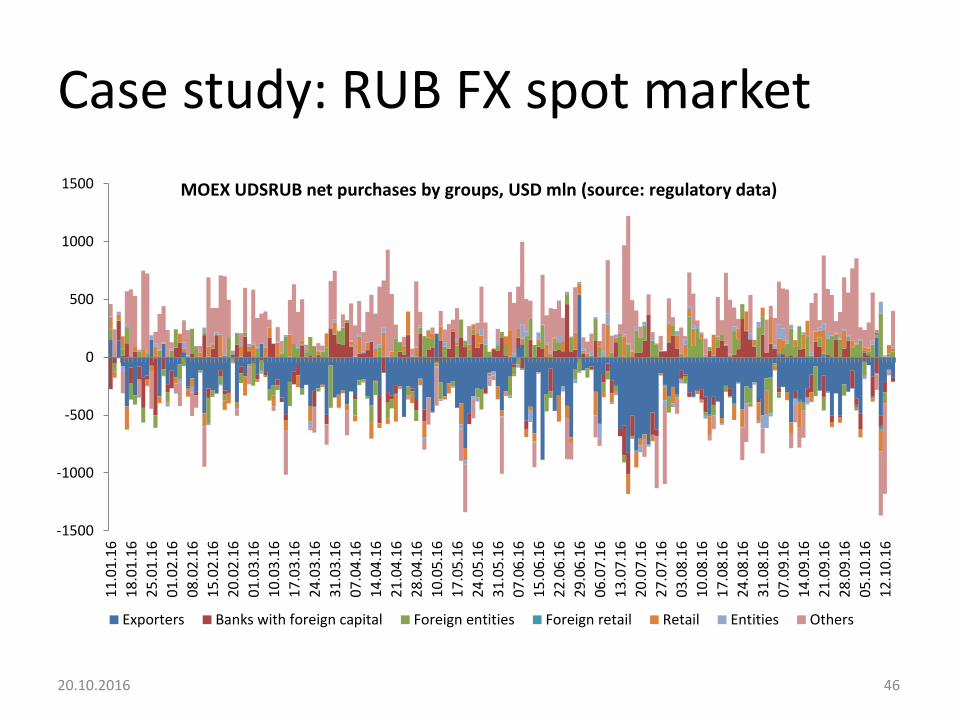

MOEX UDSRUB net purchases by groups, USD mln (source: regulatory data)

Exporters Banks with foreign capital Foreign entities Foreign retail Retail Entities Others

20.10.2016 46

Case study: RUB FX spot market

0

5

10

15

20

25

30

11

.01

.16

18

.01

.16

25

.01

.16

01

.02

.16

08

.02

.16

15

.02

.16

20

.02

.16

01

.03

.16

10

.03

.16

17

.03

.16

24

.03

.16

31

.03

.16

07

.04

.16

14

.04

.16

21

.04

.16

28

.04

.16

10

.05

.16

17

.05

.16

24

.05

.16

31

.05

.16

07

.06

.16

15

.06

.16

22

.06

.16

29

.06

.16

06

.07

.16

13

.07

.16

20

.07

.16

27

.07

.16

03

.08

.16

10

.08

.16

17

.08

.16

24

.08

.16

31

.08

.16

07

.09

.16

14

.09

.16

21

.09

.16

28

.09

.16

05

.10

.16

12

.10

.16

MOEX USDRUB turnover by groups, USD bln (source: regulatory data)

Retail Foreign retail Entities Foreign entities Others

20.10.2016 47

Useful information

20.10.2016 48

Useful information

Links:

• http://cbr.ru/links/

• http://cbr.ru/DKP/

• http://cbr.ru/DKP/?PrtId=kom_sit

• http://moex.com/ru/markets/currency/

• http://www.emta.org/

• http://www.nva.ru/

20.10.2016 49

Useful information

Readings:

• Stigum, Crescenzi. Money Market

• Burghardt. The Eurodollar Futures and Options Handbook

20.10.2016 50

Useful information

My contacts:

• ru.linkedin.com/in/apisanov

• https://argumentone.wordpress.com/

20.10.2016 51

Thank you for attention!

Alexander Pisanov FXMM Research Analyst

Bank of Russia