FINANCIAL INSTRUMENTS FOR OCEAN POWER · Isle of Skye and the Scottish mainland, four tidal energy...

16

FINANCIAL INSTRUMENTS FOR OCEAN POWER Brussels, 4 April 2014

-

Upload

dangkhuong -

Category

Documents

-

view

216 -

download

0

Transcript of FINANCIAL INSTRUMENTS FOR OCEAN POWER · Isle of Skye and the Scottish mainland, four tidal energy...

FINANCIAL INSTRUMENTS

FOR OCEAN POWER

Brussels, 4 April 2014

2

Overview

EIB Group: an introduction

Instruments relevant to the ocean energy sector

Who is investing? Who is not?

Towards bankability

EIB Group

EIB + EIF = EIB Group

EIB = EU's long-term lending institution

Established 1958, owned by the 28 EU Member States

Policy driven, innovation and climate action as high priorities

3

4

EIF’s Shareholders

EIB: Main shareholder (61%)

European Community represented by the European

Commission (29%)

30 public and private financial institutions from 17

countries (9%), including:

* 1% of EIF’s shares are still to be issued

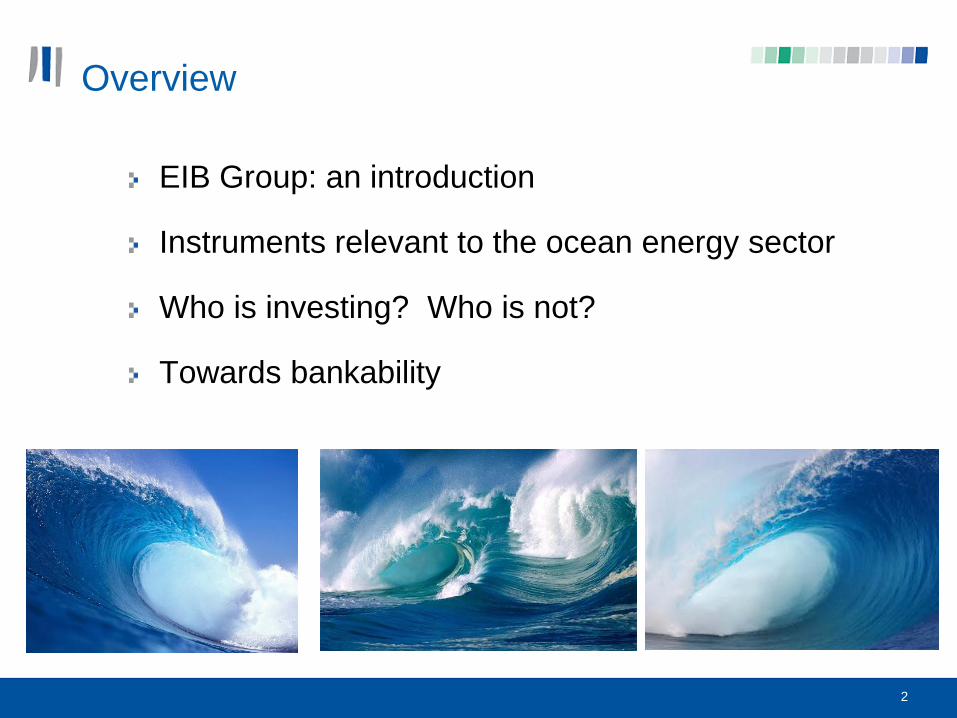

EIF/EIB financing: an overview

•Risk Capital • CIP Resources (SME) • RSFF (SME / MidCap)

•Entrepreneur, friends, family

•Business Angels

•Seed/Early Stage VC Funds

•VC Funds

•Bank Loans and Guarantees

•Seed / Start-Up Phase •Emerging Growth Phase •Development Phase

Facility: High Growth

Innovative SME

Scheme (GIF), Ecotech

Purpose: IP financing,

technology transfer,

seed financing,

investment readiness

Target Group: VC

Funds, Business Angels

EIF Product: Fund-of-

Funds

Competitiveness and

Innovation Program

(CIP) Guarantee

schemes

Growth financing for

SMEs

VC Funds, CLOs

SME guarantees (loans,

microcredit,

equity/mezzanine,

securitisation)

RSFF including RSI and

soon MCI /GFI

Innovation financing

SMEs/MidCaps, Banks,

PE Investors (sub-

investment grade)

Loans (incl. Mezzanine),

Funded Risk Sharing

Facilities with Banks

(Investors)

Special Operations

•RSFF / Investment Loans

RSFF

Investment Loans

RDI financing

MidCaps/Large

Corporates/Public

Sector Entities

(investment grade)

Guarantees

Special Operations

•Later Stage

• Counterparts

• EIF EIB

EIB Financing Instruments

We have an extensive range of instruments to finance public and private

sectors at investment and sub-investment grades of risk

•EIB lending instrument for Investment Grade operations

•Special Activities

•For low and sub investment Grade operations

•Project Finance

•Direct Loans

Project

•Project finance with

direct project risk

•LGTT/RSFF

•(Mezzanine)

•Equity through

•Funds

•Intermediated

Loans

Banks

•Public Sector

Financing

6

7

Principal Features of an EIB Loan

Benefits of low cost of funding passed on to clients: Up to 50% of project costs financed (extended to 75% for eligible environmental projects), at competitive interest rates

Broad range of currencies

Long maturities

Catalyst for participation of other banking or financial partners

Two main facilities: Direct Loans - Large-scale projects (more than EUR 25m)

Corporate and project finance

Risk sharing finance facility (RSFF) may be of particular interest to ocean energy sector: complementary to other sources of debt capital available for low/sub investment grade RDI intensive corporates

Intermediated Loans

Small and medium-scale loans (particularly to SMEs) via national and regional intermediary banks

Lending decision remains with the financial intermediary

8

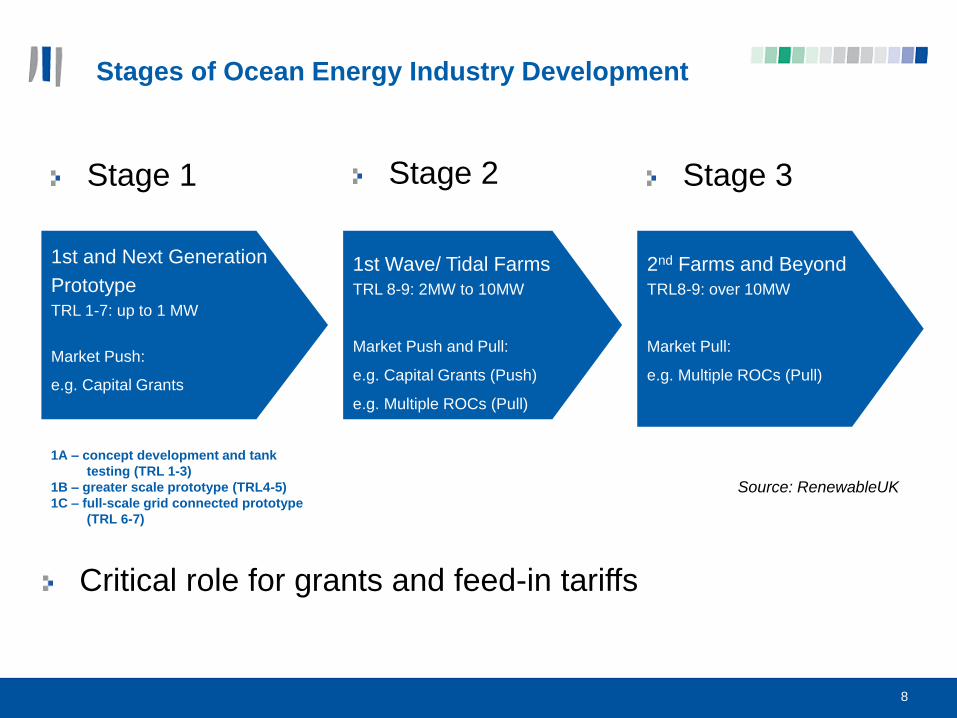

Stages of Ocean Energy Industry Development

1st and Next Generation

Prototype

TRL 1-7: up to 1 MW

Market Push:

e.g. Capital Grants

1st Wave/ Tidal Farms

TRL 8-9: 2MW to 10MW

Market Push and Pull:

e.g. Capital Grants (Push)

e.g. Multiple ROCs (Pull)

2nd Farms and Beyond

TRL8-9: over 10MW

Market Pull:

e.g. Multiple ROCs (Pull)

Source: RenewableUK

1A – concept development and tank

testing (TRL 1-3)

1B – greater scale prototype (TRL4-5)

1C – full-scale grid connected prototype

(TRL 6-7)

Stage 1 Stage 2 Stage 3

Critical role for grants and feed-in tariffs

14/04/2014 9

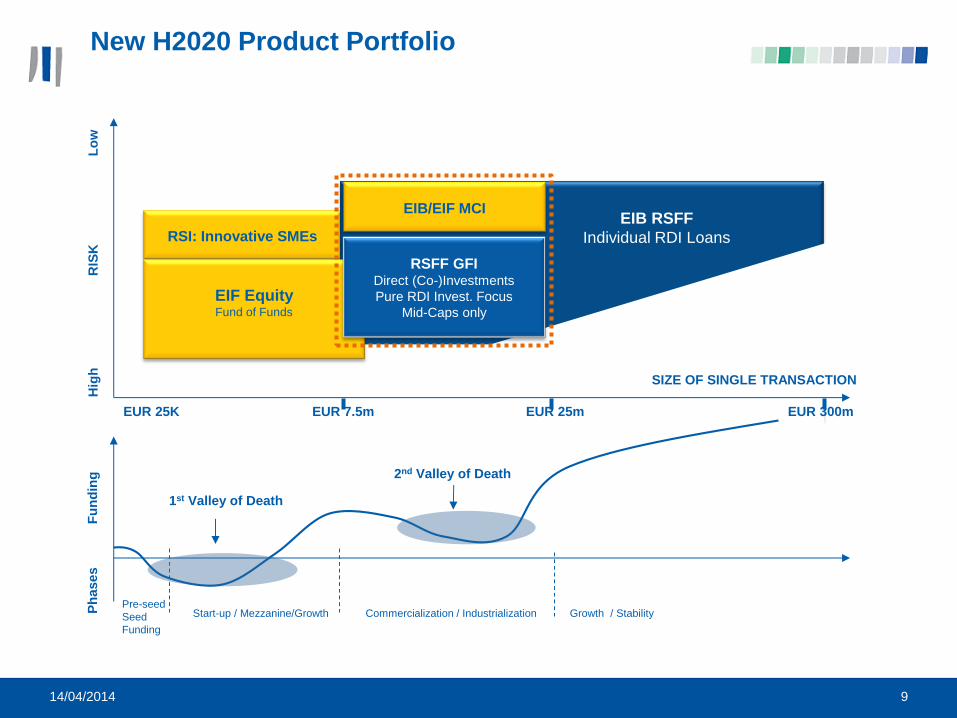

New H2020 Product Portfolio

RSI: Innovative SMEs

Hig

h R

ISK

L

ow

EIB/EIF MCIEIB RSFF

Individual RDI Loans

EIF EquityFund of Funds

RSFF GFIDirect (Co-)Investments

Pure RDI Invest. Focus

Mid-Caps only

SIZE OF SINGLE TRANSACTION

Fu

nd

ing

Pre-seed

Seed

Funding

Start-up / Mezzanine/Growth Commercialization / Industrialization Growth / StabilityPh

ases

1st Valley of Death

2nd Valley of Death

EUR 7.5m EUR 25m EUR 300mEUR 25K

14/04/2014 10

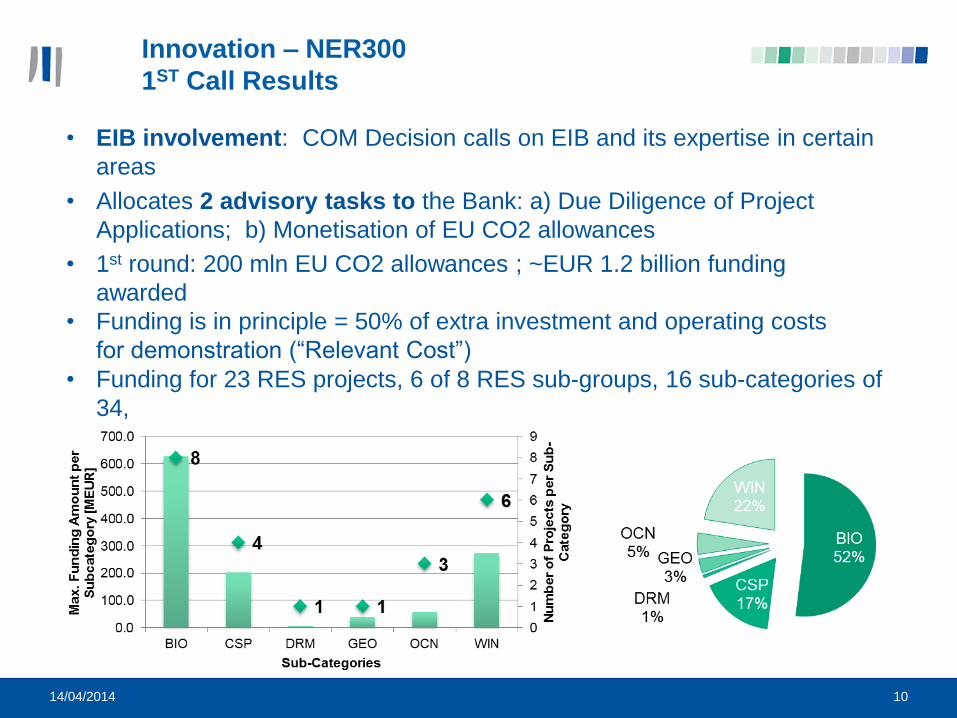

Innovation – NER300

1ST Call Results

• EIB involvement: COM Decision calls on EIB and its expertise in certain

areas

• Allocates 2 advisory tasks to the Bank: a) Due Diligence of Project

Applications; b) Monetisation of EU CO2 allowances

• 1st round: 200 mln EU CO2 allowances ; ~EUR 1.2 billion funding

awarded

• Funding is in principle = 50% of extra investment and operating costs

for demonstration (“Relevant Cost”)

• Funding for 23 RES projects, 6 of 8 RES sub-groups, 16 sub-categories of

34,

14/04/2014 11

Innovation – NER300

1ST Call Results – OCEAN projects

• 3 NER300 ocean categories: Wave (>= 5MW), Tidal (>=5 MW), OTEC1

(>=10MW)

• 8 Project Applications received in all categories

• 5 projects ranked in all categories

• 3 projects attributed for NER300 funding (wave & tidal),

• 1 withdrawn after Award Decision

• Remaining total NER300 funding amount for ocean projects: ~40 MEUR

• Project 1:

UK, Sound of Islay, 10 MWe array, ten grid-connected tidal current

turbines (3-bladed, seabed mounted ), located at the west coast of

Scotland.

• Project 2:

UK, Kyle Rhea, 8 MWe tidal turbine array, located in strait between the

Isle of Skye and the Scottish mainland, four tidal energy twin rotor

turbines each rated at nominal 2 MWe .

1) OTEC = Ocean Thermal Energy Conversion

12

Private Investment Activity – who is investing

Industrial players / Conglomerates: active in recent years

(Siemens, Alstom, other)

Utilities

Individuals/ family offices

JVs favoured: sharing of competences, risk

13

Under-represented investor types

VC and private equity funds: historically cautious given

concerns over time-to-market, technology risks, capital

intensity/dilution

Infrastructure funds: willing to take equity risk but generally

only in proven technologies

Banks via PF structures: function of maturity of the sector

Role for new partnerships, products, even institutions

14

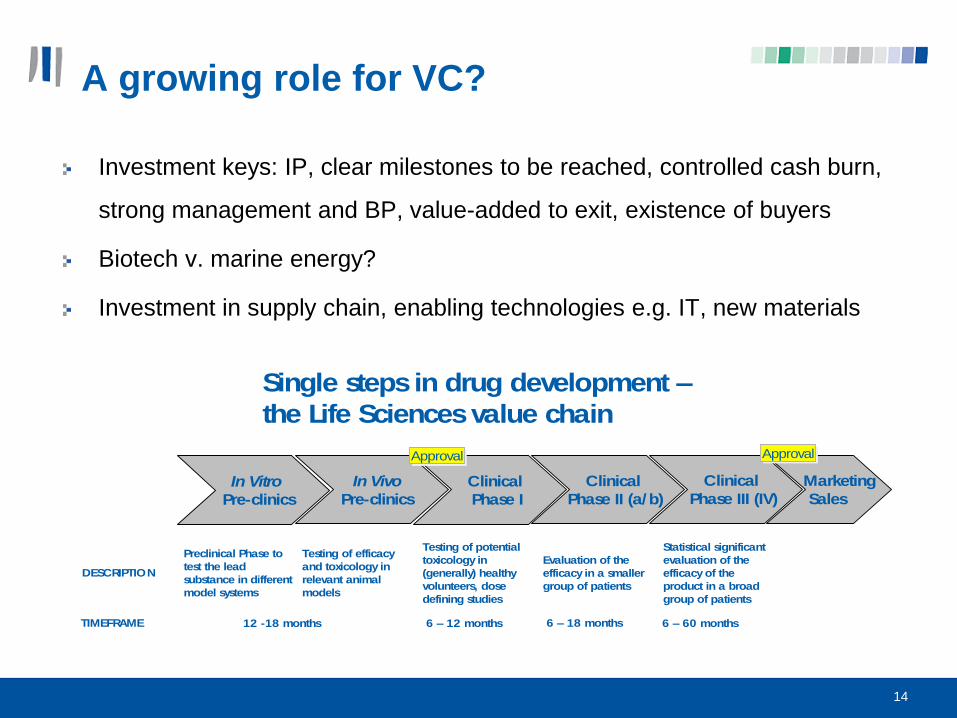

A growing role for VC?

Investment keys: IP, clear milestones to be reached, controlled cash burn,

strong management and BP, value-added to exit, existence of buyers

Biotech v. marine energy?

Investment in supply chain, enabling technologies e.g. IT, new materials

Single steps in drug development –

the Life Sciences value chain

In Vivo

Pre-clinics

Preclinical Phase to

test the lead

substance in different

model systems

Clinical

Phase I

Clinical

Phase II (a/b)

Clinical

Phase III (IV)

Testing of efficacy

and toxicology in

relevant animal

models

Testing of potential

toxicology in

(generally) healthy

volunteers, dose

defining studies

Evaluation of the

efficacy in a smaller

group of patients

Statistical significant

evaluation of the

efficacy of the

product in a broad

group of patients

DESCRIPTION

In Vitro

Pre-clinics

ApprovalApproval

Marketing

Sales

ApprovalApproval

12 -18 months 6 – 12 months 6 – 60 monthsTIMEFRAME 6 – 18 months

15

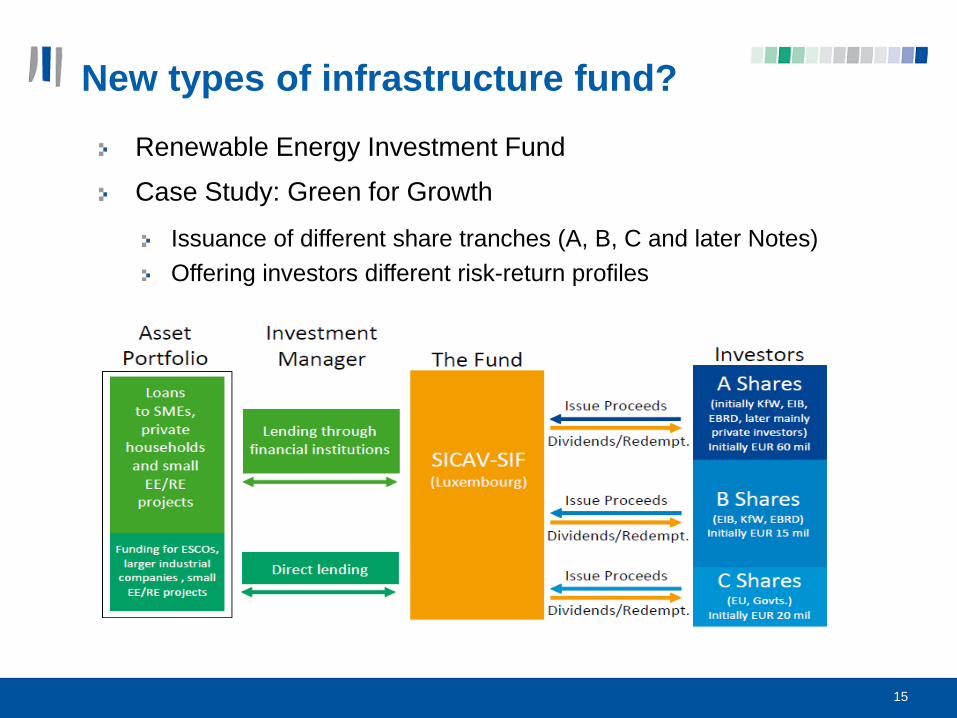

New types of infrastructure fund?

Renewable Energy Investment Fund

Case Study: Green for Growth

Investment Test

Is the fund a sound investment proposition?

Issuance of different share tranches (A, B, C and later Notes)

Offering investors different risk-return profiles

16

Moving towards Bankability? Creating an enabling environment

Regulatory Environment: Feed In Tariff, Permitting

Public Finance:

Government or EU in form of

grants or guarantees

Grid connections

Main barriers to finance:

• High-risk nature of the project

• Lack of commercial viability

• Lack of coordination between

public funding sources

• Commitment of project promoters

• Insufficient technical and financial

advice to make projects investor-ready