Financial Crisis. An overview of the crisis This crisis is called: Mortgage subprime crisis or...

46

Financial Crisis

-

date post

22-Dec-2015 -

Category

Documents

-

view

216 -

download

0

Transcript of Financial Crisis. An overview of the crisis This crisis is called: Mortgage subprime crisis or...

Financial Crisis

An overview of the crisis

This crisis is called: Mortgage subprime crisis or Liquidity crisis It started in July 2007 in the US

Glossary

CDO: Collateralized debt obligation (eg mortgage credits) These assets generate cash flows to those holding them.

MBS: mortgage backed securities ABS: asset backed securities

Glossary

Securitization: a method of selling assets, a form of structured finance

initially developed in the early 1980's in MBS format.

It matured in the late 1980's in both MBS and ABS formats.

it spread to Europe (the largest market outside the U.S.), Latin America and Southeast Asia (primarily Japan).

Securitization

It involves bundling of credit sensitive assets into a

pool tranching them and creating a new asset

and then selling them to investors Once these are sold they are removed from

the balance sheet of the originator

Securitization

Credit sensitive assets that generate cash flows

Pooling of

Assets

Create new liabilities by tranching and selling them to investors

originator

investor

SPE

underwriter

Cash flow assets

Sponsor

Law firms

Rating agencies

fees

securitization

Revenue from securitization

This revenue becomes the source of new credit. (credit expansion)

Tranching enables the distribution of risk.

Hence credit becomes cheaper.

Subprime lending

Subprime: lending to borrowers who have less than “prime” creditworthiness.

In the case of mortgage credits, subprime credits are those that go to people without a stable job or credit history.

Subprime lending was encouraged by securitization.

Securitization

Banks

Monthly mortgage payments

Pool of

assets

Coupon payments to holders of securities

1 2 3

1. Least risky asset gets paid first

2. More risky asset getspaid second etc

Credit Default Swap (CDS)

This is insurance against credit default risk (eg, of the payments on mortgage credit).

If the coupon payment is not made on the security, the party that has purchased insurance is compensated.

The party that invested in the CDS (insurer) makes the payment.

Advantages of securitization

Enables the seller to monetize its assets

Remove credit sensitive assets from its balance sheet: originate and hold vs orginate and distribute.

Enables diversification of risk by putting different assets into the same bundle

Glossary

Glass Steagall Act Traditional banking Investment banking Deregulation Shadow banking

Traditional Banking

Financial institutions that accept deposits and give credits.

Because they know their clients, asymetric information issues are reduced.

They are highly regulated and there is deposit insurance against the risk of a bank run.

Investment Bank

Financial institutions that deal with raising capital, trading in securities and managing corporate mergers and

acquisitions.

Source of investment bank profits

raising money through issuing and selling securities in the capital markets (both equity, bond)

insuring bonds (selling credit default swaps),

providing advice on transactions such as mergers and acquisitions.

Glass-Steagall Act

A 1933 act that prohibited commercial banks from undertaking investment banking activities such as underwriting the securities of private corporations.

Objective: prevent banks from entering into nonfinancial businesses (for example, owning corporate stock) and more risky activities.

Major investment bankers

Bear Stearns: established in 1923 to March 2008

Merrill Lynch: established in 1914 acquired by bank of America in September 2008

Lehman Brothers: established in 1850 announced bankruptcy in September 2008

Goldman Sachs: established in 1869. Morgan Stanley: established in 1935 On September 22, 2008, these two became

traditional bank holding companies,

Financial deregulation

The Gramm-Leach-Bliley Act, (1999) repealed part of the Glass-Steagall Act of 1933, opening up competition among banks, securities companies and insurance companies.

The Glass-Steagall Act prohibited a bank from offering investment, commercial banking, and insurance services.

Shadow banking system

The traditional banking system was highly regulated.

The shadow banking system is comprised of all financial intermediaries involved in facilitating the creation of credit across the global financial system, but whose members are not subject to regulatory oversight.

Shadow banking system

It escaped regulation primarily because it did not accept traditional bank deposits.

As a result, many of the institutions and instruments were able to employ higher market, credit and liquidity risks, and did not have capital requirements in line with those risks.

Shadow banking system

It also refers to unregulated activities by regulated institutions.

Examples of intermediaries not subject to regulation: hedge funds

Examples of unregulated activities by regulated institutions: credit default swaps (CDS).

Lending practices

Securitization meant that banks were not carrying the risk and earned fees for transactions, Banks no longer cared about the

quality of their lending.

Lending practices

mortgage brokers maximize their income by generating larger volumes of mortgages

banks maximize their income by packaging these loans into mortgage-backed securities (MBS’s).

Investment banks earn fees for re-packaging these securities in tranches of collateralized debt obligations, or CDO’s (and sometimes into CDO’s of CDO’s).

Lending practices

Sub-prime mortgages

in more than 50% of all US mortgages in 2005-2007, reckless lending practices :

no down-payments, no verification of borrowers’ incomes and

assets, interest-rate-only mortgages, teaser rates

Ingredients of Liquidity Crisis

U.S. Trade and CA Deficit Financing the deficit meant an inflow

capital and excess liquidity This was coupled with:

1. Fed monetary policy: low interest rates

2. Deregulation of financial system

Ingredients of Liquidity Crisis

Ample liquidity and Fed monetary policy of low interest

rates Financial deregulation caused : Risk to be priced low.

High availability of loanable funds

Low nominal and low real interest rates

Real cost of borrowing low Borrowing increasing A lot of loans extended by banks (with

a lot of money coming from ‘shadow banks’)

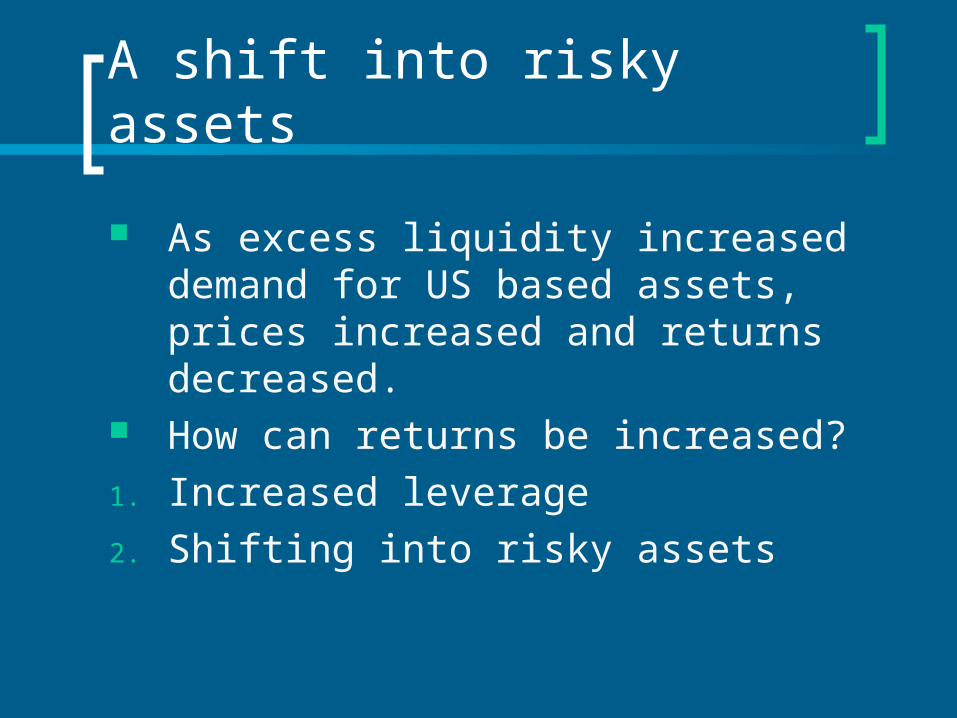

A shift into risky assets

As excess liquidity increased demand for US based assets, prices increased and returns decreased.

How can returns be increased?

1. Increased leverage

2. Shifting into risky assets

A shift into risky assets

For example stocks, becuase the rate on risk-free assets (T-bills) is quite low.

Demand increases for hedge funds and equity funds

Equity funds: stocks Hedge funds: combination of stocks

and derivatives and options to minimize risk exposure

Risk spread

Difference between the return on equity and risk free asset

Spread is compressed for a given risk free rate

Risk is priced lower than it should. Securitization gave the impression that

risk was distributed.

Risk and securitization

Securitization was supposed to do a better job of spreading and reducing risk.

But during the crisis, it became apparent that risk was hidden rather than reduced.

Investors had no idea how exposed they were.

Housing Bubble

Federal Reserve Chair Alan Greenspan declined, and even denied the existence of a bubble.

“I would tell audiences that we were facing not a bubble but a froth – lots of small, local bubbles that never grew to a scale that could threaten the health of the overall economy.” Alan Greenspan, The Age of Turbulence.

Housing Bubble

The Fed had the view that it was not in its job description to manage asset prices.

This view is challenged now.

No Controls Over Predatory Lenders

The combination of financial deregulation and the housing bubble created the circumstances in which aggressive lenders could abuse vulnerable borrowers.

The terms of the loan does not matter so long as the value of the house is going up.

Financial Deregulation and Unchecked Financial Innovation

Traditionally, banks made mortgages and held them.

In the new era, mortgages were made available widely and with little review of recipients' qualifications because of a shift in institutions holding the mortgages.

Financial Deregulation and Unchecked Financial "Innovation."

In the new era, banks and non-bank mortgage lenders made loans, but then sold the loans to others.

Investment banks packaged lots of mortgage loans into "Collateralized Debt Obligations" (CDOs) and then sold them on Wall Street, with a promise of a steady stream of revenue from interest payments.

Financial Deregulation and Unchecked Financial "Innovation."

These operations were pretty much unregulated.

No one took account of how shoddy the loans were or the certainty that huge numbers would go bad if and when the housing bubble burst.

Effective regulation of lending practices could have prevented the abusive loans, but none was to be found.

Private Regulatory Failure

It was the job of ratings agencies (like Standard and Poor's, and Moody's) to assess the CDOs and give investors guidance on how risky they were.

They failed because they wanted to maintain good relations with the investment banks issuing the CDOs.

Evolution of the liquidity crisis

Financial instruments backed by home mortgages shut down because there are no buyers.

This could cause a chain reaction of debt defaults.

Evolution of the crisis

First, the housing bubble burst. Then subprime melted down. Then there was a loss of confidence:

The yield spread betwee corporate bonds and government bonds increased.

Evolution of the crisis

collapse of two hedge funds operated by Bear Stearns

BNP Paribas, a large French bank, suspended the operations of three of its own funds because of “the complete evaporation of liquidity in certain market segments” — that is, there are no buyers.

Evolution of the crisis

When liquidity dries up, it can produce a chain reaction of defaults.

Financial institution A can’t sell its mortgage-backed securities, so it can’t raise enough cash to make the payment it owes to institution B,

Evolution of the crisis

Institution A can’t raise enough cash to make the payment it owes to institution B,

which then doesn’t have the cash to pay institution C —

and those who do have cash sit on it, because they don’t trust anyone else to repay a loan, which makes things even worse.

Liquidity crisis

But when liquidity dries up, the normal tools of policy lose much of their effectiveness.

Reducing the cost of money doesn’t do much for borrowers if nobody is willing to make loans.

Injecting banks with plenty of cash doesn’t do much if the cash stays in the banks’ vaults.

Sources:

Paul Krugman, “Very Scary Things” New York Times, August 10, 2007

Nouriel Roubini, “Dark Matter of Financial Globalization” Project Syndicate , Oct.17, 2007.