Financial Considerations for Redundancy - UniSuper/media/files/slide decks... · $18,201 - $37,000...

31

16/09/2013 1 Financial Considerations for Redundancy 16 September, 2013 Financial Considerations for Redundancy – 16 September, 2013 2 The information contained within this presentation is intended to provide general advice only. It has been prepared without taking into account your objectives, financial situation or personal needs. Prior to making any investment decisions, you should speak with a financial adviser to consider whether this information is appropriate for your needs, objectives and circumstances. You should obtain a copy of the relevant product disclosure statement (PDS) prior to making a decision regarding any investment in any financial product. This information is current as at July 2013 and is based on our understanding of legislation at that date. Information relating to the 2012/13 & 2013/14 Federal Budgets, and announcements made by the Federal Government on 5 April 2013 is based on our understanding of the proposals. The information provided in this presentation in relation to these announcements is subject to change and certain proposals may not become effective until they are enacted by Parliament. You should not rely on this information and it should be verified prior to making any decision The information contained in this presentation is not legal, taxation or accounting advice. Professional advice should be obtained before making any decisions. Whilst care has been taken in the preparation of this information, the accuracy or completeness of the information is not guaranteed. This presentation was prepared and issued by UniSuper Management Pty Ltd ABN 91 006 961 799, AFSL No: 235907, which is also the administrator of, and wholly owned by, the UniSuper Superannuation fund (ABN 91 385 943 850). UniSuper Limited (ABN 54 006 027 121) is the trustee of the fund. If you would like to contact us please do so on 1800 331 685 or alternatively send us an email to [email protected]

-

Upload

phungxuyen -

Category

Documents

-

view

216 -

download

3

Transcript of Financial Considerations for Redundancy - UniSuper/media/files/slide decks... · $18,201 - $37,000...

16/09/2013

1

Financial Considerations for Redundancy

16 September, 2013

Financial Considerations for Redundancy – 16 September, 2013 2

The information contained within this presentation is intended to provide general advice only. It has been prepared without taking into account your objectives, financial situation or personal needs. Prior to making any investment decisions, you should speak with a financial adviser to consider whether this information is appropriate for your needs, objectives and circumstances.

You should obtain a copy of the relevant product disclosure statement (PDS) prior to making a decision regarding any investment in any financial product.

This information is current as at July 2013 and is based on our understanding of legislation at that date.

Information relating to the 2012/13 & 2013/14 Federal Budgets, and announcements made by the Federal Government on 5 April 2013 is based on our understanding of the proposals. The information provided in this presentation in relation to these announcements is subject to change and certain proposals may not become effective until they are enacted by Parliament. You should not rely on this information and it should be verified prior to making any decision

The information contained in this presentation is not legal, taxation or accounting advice. Professional advice should be obtained before making any decisions. Whilst care has been taken in the preparation of this information, the accuracy or completeness of the information is not guaranteed.

This presentation was prepared and issued by UniSuper Management Pty Ltd ABN 91 006 961 799, AFSL No: 235907, which is also the administrator of, and wholly owned by, the UniSuper Superannuation fund (ABN 91 385 943 850). UniSuper Limited (ABN 54 006 027 121) is the trustee of the fund. If you would like to contact us please do so on 1800 331 685 or alternatively send us an email to [email protected]

16/09/2013

2

Financial Considerations for Redundancy – 16 September, 2013

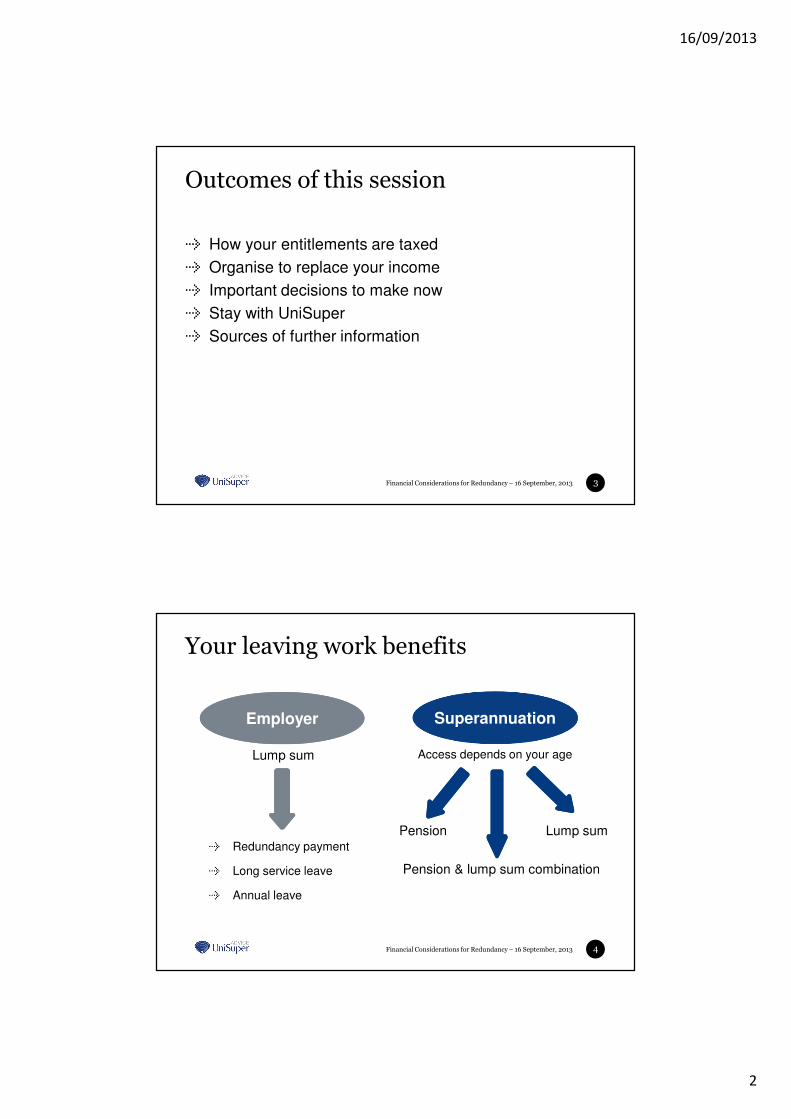

Outcomes of this session

3

How your entitlements are taxed

Organise to replace your income

Important decisions to make now

Stay with UniSuper

Sources of further information

Financial Considerations for Redundancy – 16 September, 2013

Your leaving work benefits

4

EmployerEmployer

Pension Lump sum

Pension & lump sum combination

Lump sum

SuperannuationSuperannuation

Redundancy payment

Long service leave

Annual leave

Access depends on your age

16/09/2013

3

Financial Considerations for Redundancy – 16 September, 2013

Redundancy payment

5

Your entitlements may be based upon a combination of:

Contractual or statutory provisions of employment

Gratuity payments or payments in lieu of notice

Unused RDO’s or sick leave (if applicable)

Financial Considerations for Redundancy – 16 September, 2013

Taxation of Redundancy payment

6

Based on:

The tax components of the payment

Your age

Your length of service

You will receive a quote from your employer showing

the before and after tax payment

16/09/2013

4

Financial Considerations for Redundancy – 16 September, 2013

Taxation of Redundancy payment

7

Tax free portion of ETP

Taxable portion of ETPUp to ETP cap of $180,000*

Over ETP cap of $180,000*

ETP = Employment Termination Payment

* Based upon 2013/14 rates. No tax free amount if age 65 or over.

Tax free amount*First $9,246 +($4,624 x complete years of service)

0% tax

0% tax

Under age 55

31.5% tax

Over age 55

16.5% tax

46.5% tax

Relates to portion of pre 1/7/1983 service

Financial Considerations for Redundancy – 16 September, 2013

2013/14 tax rates

8

Taxable income Salary sacrifice

0-$18,200 Nil

$18,201 - $37,000 19c for each $1 over $18,200

$37,001 - $80,000 $3,572 plus 32.5c for each $1 over $37,000

$80,001 - $180,000 $17,547 plus 37c for each $1 over $80,000

$180,001 and over $54,547 plus 45c for each $1 over $180,000

16/09/2013

5

Financial Considerations for Redundancy – 16 September, 2013

Tax on other payments

9

Type of payment Tax deducted by employer at the lower of

Long Service Leave* Marginal tax rate OR 31.5%

Annual Leave Marginal tax rate OR 31.5%

* If your employer service period pre-dates 16 August 1978, you may pay less tax on the Long Service Leave portion of your payment.

Payments must be taken as cash

Financial Considerations for Redundancy – 16 September, 2013

Example 1

10

Mark

Age: 46

Service: 12 years & 6 months

Redundancy payment: $50,000

Annual Leave:$8,000

Long Service Leave:$26,000

Tax free amount$50,000

Tax on Redundancy payment = $0

Calculate Tax Free Amount $9,246 + ($4,624 x 12) = $64,734

ETP$0

Annual Leave$5,480

Tax on Annual Leave $8,000 x 31.5% = $2,520

Tax on Long Service Leave $26,000 x 31.5% = $8,190

LS Leave$17,810

16/09/2013

6

Financial Considerations for Redundancy – 16 September, 2013

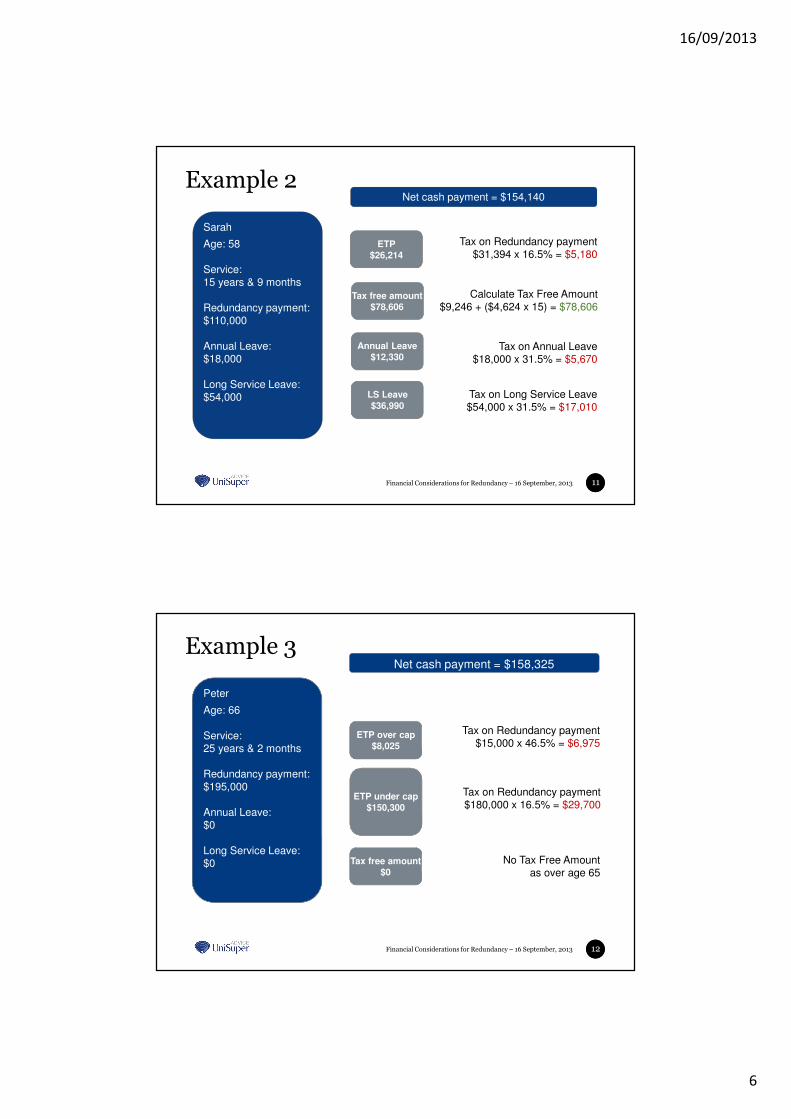

Example 2

11

Net cash payment = $154,140

Sarah

Age: 58

Service: 15 years & 9 months

Redundancy payment: $110,000

Annual Leave:$18,000

Long Service Leave:$54,000

Tax free amount$78,606

Tax on Redundancy payment $31,394 x 16.5% = $5,180

Calculate Tax Free Amount $9,246 + ($4,624 x 15) = $78,606

ETP$26,214

Annual Leave$12,330

Tax on Annual Leave $18,000 x 31.5% = $5,670

Tax on Long Service Leave $54,000 x 31.5% = $17,010

LS Leave$36,990

Financial Considerations for Redundancy – 16 September, 2013

Example 3

12

Net cash payment = $158,325

Peter

Age: 66

Service: 25 years & 2 months

Redundancy payment: $195,000

Annual Leave:$0

Long Service Leave:$0 Tax free amount

$0

Tax on Redundancy payment $180,000 x 16.5% = $29,700

No Tax Free Amount as over age 65

ETP under cap$150,300

ETP over cap$8,025

Tax on Redundancy payment $15,000 x 46.5% = $6,975

16/09/2013

7

Financial Considerations for Redundancy – 16 September, 2013

Income options available

13

You may choose to source your ongoing living needs from

Drawing on your Redundancy lump sum

Part time / casual / contract work

Centrelink benefits

Lump sum withdrawals* from super

A pension* commenced with your super

A combination of the above

*Subject to age and work status

Financial Considerations for Redundancy – 16 September, 2013

Age Pension eligibility

14

Men WomenQualification Age Date of birth Qualification Age

65 yearsBefore 1 January 1949 Age reached

1 January 1949 – 30 June 1952 65 years

Note: After 1 July 2017, the qualifying age for an Age Pension will be

increasing progressively from 65 to 67 years of age.

Current arrangements

16/09/2013

8

Financial Considerations for Redundancy – 16 September, 2013

Potential Centrelink entitlements

15

Age Pension

No waiting period

Must be Age Pension age

Satisfy income and assets test

Single Couple (combined)

Fortnightly income less than $1,773 $2,714

Homeowner’s assets less than $735,750 $1,092,000

Non-homeowner’s assets less

than $878,250 $1,234,500

Full Age Pension

Single $808.40 pf

Couple $1,218.80 pf

Rates as at 1 July 2013

Includes supplement

Financial Considerations for Redundancy – 16 September, 2013

Potential Centrelink entitlements

16

Newstart Allowance

Under Age Pension age

Waiting period based on Redundancy

Undertake Activity Test (job search, volunteer, training)

Satisfy income and assets test

Single Couple (combined)

Fortnightly income less than $935.67 $853.84 each

Homeowner’s assets less than $196,750 $279,000

Non-homeowner’s assets less

than $339,250 $421,500

Full Allowance

Single $505.40 pf

Couple $456.30 pf each

Rates as at 1 July 2013

16/09/2013

9

Financial Considerations for Redundancy – 16 September, 2013

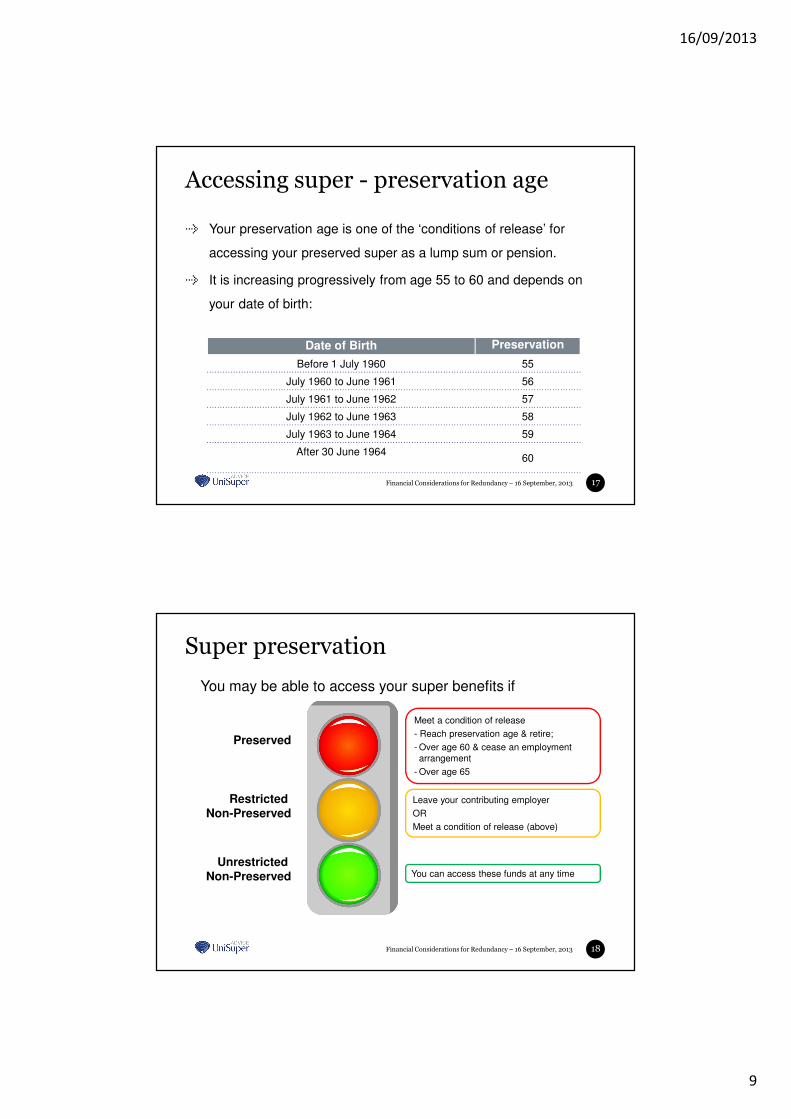

Accessing super - preservation age

17

Your preservation age is one of the ‘conditions of release’ for

accessing your preserved super as a lump sum or pension.

It is increasing progressively from age 55 to 60 and depends on

your date of birth:

Date of Birth Preservation

Before 1 July 1960 55

July 1960 to June 1961 56

July 1961 to June 1962 57

July 1962 to June 1963 58

July 1963 to June 1964 59

After 30 June 196460

Financial Considerations for Redundancy – 16 September, 2013

Super preservation

18

You may be able to access your super benefits if

Unrestricted Non-Preserved

Restricted Non-Preserved

Preserved

Meet a condition of release

- Reach preservation age & retire;

- Over age 60 & cease an employment arrangement

- Over age 65

You can access these funds at any time

Leave your contributing employer

OR

Meet a condition of release (above)

16/09/2013

10

Financial Considerations for Redundancy – 16 September, 2013

Tax on lump sum super withdrawals

19

Tax Free Component Taxable Component

Under PA* 0% 21.5%

Between PA* and age 59 0%First $180,000

Over $180,000

0%

16.5%

Over age 60 0% 0%

* PA = Preservation Age.

Financial Considerations for Redundancy – 16 September, 2013

Lump sum withdrawal example

20

Diane is aged 56 and decides to retire after receiving a Redundancy package.

She wants to withdraw $220,000 from her super to repay her mortgage.

Her super has the following components:

• Tax free $50,000

• Taxable $450,000

How much tax will she pay?

For this withdrawal, 10% is tax free ($50,000/$500,000)

Components of $220,000 withdrawal:

Tax free $22,000

Taxable $198,000

Tax on taxable component:

= ($198,000 - $180,000) x 16.5%

= $2,970

16/09/2013

11

Financial Considerations for Redundancy – 16 September, 2013

UniSuper pensions

21

UniSuper offers three styles of pensions:

Flexi Pension

Commercial Rate Indexed Pension

Defined Benefit Indexed Pension – restricted to

Defined Benefit Division (DBD) members who joined

the Defined Benefit Division prior to 1 July 1998

Financial Considerations for Redundancy – 16 September, 2013

UniSuper Pensions

22

Flexi PensionCommercial Rate Indexed Pension

Defined Benefit Indexed Pension

Investment choice ���� � �

How is your annual pension calculated?

Member nominates pension amount (subject to annual

minimum)#

Fixed CPI indexed pension based on initial sum invested

Fixed CPI indexed pension based on Trust Deed factors

Can you make lump sum withdrawals?

����# � �

How long will the pension last?

Until the account balance is zero

Lifetime (10-year guarantee period)

Lifetime

What benefits are paid when you die?

Remaining account balance paid as either a reversionary pension to spouse or child or

lump sum to beneficiaries

Joint pension paid to surviving spouse, or sum within guarantee period

To surviving spouse only (or

dependent children)

# Restrictions apply when taking a pension under transition to retirement rules

16/09/2013

12

Financial Considerations for Redundancy – 16 September, 2013

Tax on Pensions

23

Super Pension

Investment earnings 15% 0%

Annual pension income

Under age 60 Age 60 and over

Taxable proportionMarginal tax rate

(less 15% tax offset)0%

Tax-free proportion 0% 0%

Financial Considerations for Redundancy – 16 September, 2013

Tax on pensions

24

Ordinary income Pension income

Other taxable income $50,000 -

Pension income (100% taxable)

- $50,000

Taxable income $50,000 $50,000

less tax* ($7,797) ($7,797)

plus tax offset for pension (15% x $50,000)

- $7,500

Net income after tax $42,203 $49,703

Medicare levy ** ($750) ($750)

* Based on 2013/14 tax rates and does not include any tax offsets which may be available.

** Medicare levy has been included; however, the amount payable can vary between taxpayers depending on their own incomes, their combined family incomes & the number of dependent children (if any).

Compare earnings of $50,000 p.a. as ordinary income versus pension income when under the age of 60

16/09/2013

13

Financial Considerations for Redundancy – 16 September, 2013

What happens when I leave my employer?

25

1. Your employer will notify UniSuper that you have left

2. Information pack on your UniSuper Benefit and Options

- automatically sent by UniSuper

3. If a Defined Benefit Division member, you have 90 days

from your employment finish date to let UniSuper know

what you would like to do with your benefits

Financial Considerations for Redundancy – 16 September, 2013

• DBD benefit is transferred to an Accumulation 1 account

• Investment choice now important

• DBD benefit is transferred to an Accumulation 1 account

• Investment choice now important

The first 90 days are important

26

Defined Benefit Division (DBD)

members

Defined Benefit Division (DBD)

members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to

age & work status)

3. Open a UniSuper pension (subject to

age & work status)

4. Defer DBD membership

4. Defer DBD membership

1. Get new employment

1. Get new employment

5. Do nothing5. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

16/09/2013

14

Financial Considerations for Redundancy – 16 September, 2013

The first 90 days are important

27

Defined Benefit Division (DBD)

members

Defined Benefit Division (DBD)

members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to

age & work status)

3. Open a UniSuper pension (subject to

age & work status)

4. Defer DBD membership

4. Defer DBD membership

1. Get new employment

1. Get new employment

5. Do nothing5. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

• Withdrawal (lump sum if eligibl)

• Rollover to another fund

• Withdrawal (lump sum if eligibl)

• Rollover to another fund

Financial Considerations for Redundancy – 16 September, 2013

• Defined Benefit Indexed Pension (if eligible)

• Commercial Rate Indexed Pension

• Flexi Pension

• Defined Benefit Indexed Pension (if eligible)

• Commercial Rate Indexed Pension

• Flexi Pension

The first 90 days are important

28

Defined Benefit Division (DBD)

members

Defined Benefit Division (DBD)

members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to

age & work status)

3. Open a UniSuper pension (subject to

age & work status)

4. Defer DBD membership

4. Defer DBD membership

1. Get new employment

1. Get new employment

5. Do nothing5. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

16/09/2013

15

Financial Considerations for Redundancy – 16 September, 2013

• Stay a member of the DBD (benefit growth limited – age factor only)

• Possibly re-activate DBD membership at a later date

• Retain eligibility for DB Indexed Pension

• Stay a member of the DBD (benefit growth limited – age factor only)

• Possibly re-activate DBD membership at a later date

• Retain eligibility for DB Indexed Pension

The first 90 days are important

29

Defined Benefit Division (DBD)

members

Defined Benefit Division (DBD)

members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to

age & work status)

3. Open a UniSuper pension (subject to

age & work status)

4. Defer DBD membership

4. Defer DBD membership

1. Get new employment

1. Get new employment

5. Do nothing5. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

Financial Considerations for Redundancy – 16 September, 2013

• DBD benefit is transferred to an Accumulation 1 account

• Investment choice now important

• DBD benefit is transferred to an Accumulation 1 account

• Investment choice now important

The first 90 days are important

30

Defined Benefit Division (DBD)

members

Defined Benefit Division (DBD)

members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to

age & work status)

3. Open a UniSuper pension (subject to

age & work status)

4. Defer DBD membership

4. Defer DBD membership

1. Get new employment

1. Get new employment

5. Do nothing5. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

16/09/2013

16

Financial Considerations for Redundancy – 16 September, 2013

• Participating employer –Accumulation 2 can continue

• Other employer – choice means you stay with UniSuper (Accumulation 1 account)

• Participating employer –Accumulation 2 can continue

• Other employer – choice means you stay with UniSuper (Accumulation 1 account)

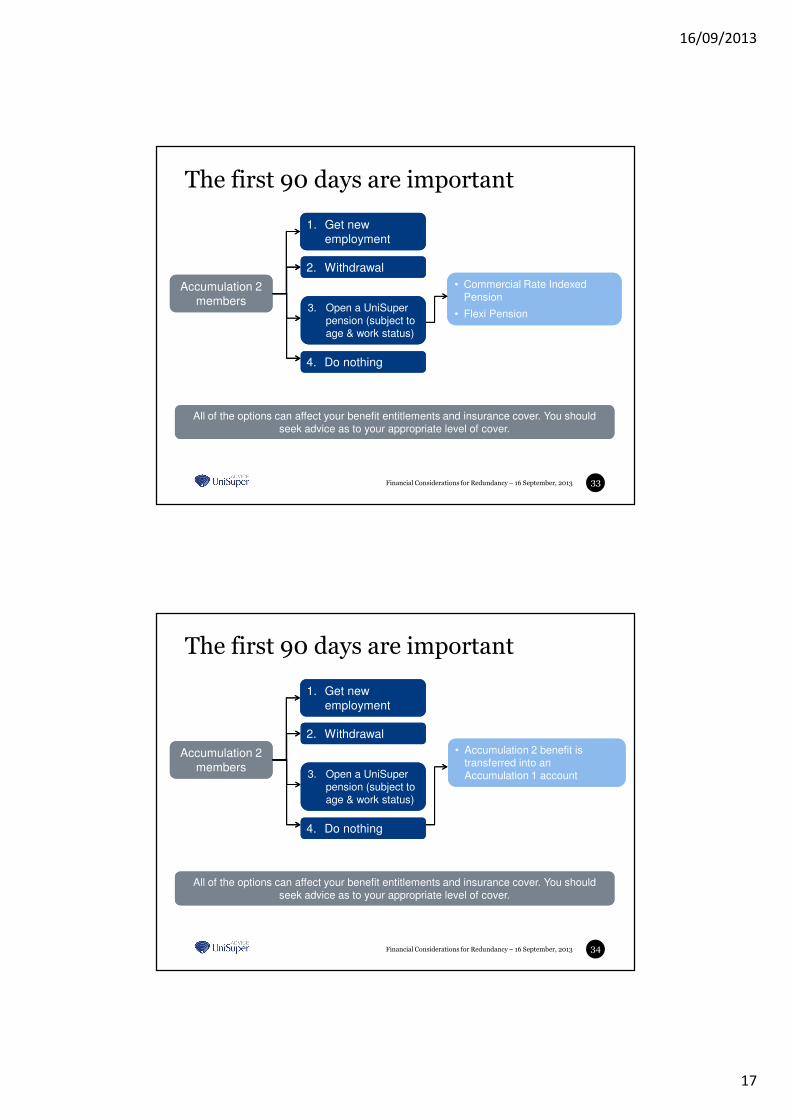

The first 90 days are important

31

Accumulation 2 members

Accumulation 2 members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to age & work status)

3. Open a UniSuper pension (subject to age & work status)

1. Get new employment

1. Get new employment

4. Do nothing4. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

Financial Considerations for Redundancy – 16 September, 2013

• Withdrawal (lump sum if eligible)

• Rollover to another fund

• Withdrawal (lump sum if eligible)

• Rollover to another fund

The first 90 days are important

32

Accumulation 2 members

Accumulation 2 members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to age & work status)

3. Open a UniSuper pension (subject to age & work status)

1. Get new employment

1. Get new employment

4. Do nothing4. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

16/09/2013

17

Financial Considerations for Redundancy – 16 September, 2013

The first 90 days are important

33

• Commercial Rate Indexed Pension

• Flexi Pension

• Commercial Rate Indexed Pension

• Flexi Pension

Accumulation 2 members

Accumulation 2 members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to age & work status)

3. Open a UniSuper pension (subject to age & work status)

1. Get new employment

1. Get new employment

4. Do nothing4. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

Financial Considerations for Redundancy – 16 September, 2013

• Accumulation 2 benefit is transferred into an Accumulation 1 account

• Accumulation 2 benefit is transferred into an Accumulation 1 account

The first 90 days are important

34

Accumulation 2 members

Accumulation 2 members

2. Withdrawal2. Withdrawal

3. Open a UniSuper pension (subject to age & work status)

3. Open a UniSuper pension (subject to age & work status)

1. Get new employment

1. Get new employment

4. Do nothing4. Do nothing

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

All of the options can affect your benefit entitlements and insurance cover. You should seek advice as to your appropriate level of cover.

16/09/2013

18

Financial Considerations for Redundancy – 16 September, 2013

What if I start a new job?

35

In the higher education and research sector

- You can provide your UniSuper membership number for future contributions

Outside the higher education sector

- You have the option to elect UniSuper as your preferred super fund

- If so desired, complete the Choice of Fund forms and provide to your new employer

Financial Considerations for Redundancy – 16 September, 2013

Your UniSuper membership advantages

36

Keep in mind that no matter what your next step is, you can remain a UniSuper member and benefit from:

� competitive fees

� a choice of investment options

� insurance cover (if applicable)

� access to UniSuper’s pension products

� personal advice from UniSuper Advice (at competitive fee for service rates)

16/09/2013

19

Financial Considerations for Redundancy – 16 September, 2013

How UniSuper can help

37

UniSuper offers 3 levels of advice:

General Advice (phone-based)

- Not specific to your personal situation

Limited Advice (phone-based)

- Single issue personal advice specific to your situation

Comprehensive Personal Advice (face to face)

- Full personal advice covering multiple issues specific to your

situation

Financial Considerations for Redundancy – 16 September, 2013

How UniSuper can help

38

A UniSuper Private Client Adviser can help give you

peace of mind

The advice is charged at an hourly rate, with no

commissions paid

There is no charge for the first appointment

Call UniSuper Advice today on 1300 331 685 for a complimentary

initial assessment on the level of advice that might suit you

16/09/2013

20

Financial Considerations for Redundancy – 16 September, 2013

Need more information?

39

Read through your Benefit Options pack and information

UniSuper’s website www.unisuper.com.au

Call the UniSuper Helpline – 1800 331 685

- call UniSuper Advice direct on – 1300 331 685

Talk to your Superannuation Officer

Contact Centrelink’s Financial

Information Service

Financial Considerations for Redundancy – 16 September, 2013

Any questions?

40

16/09/2013

21

Financial Considerations for Redundancy – 16 September, 2013

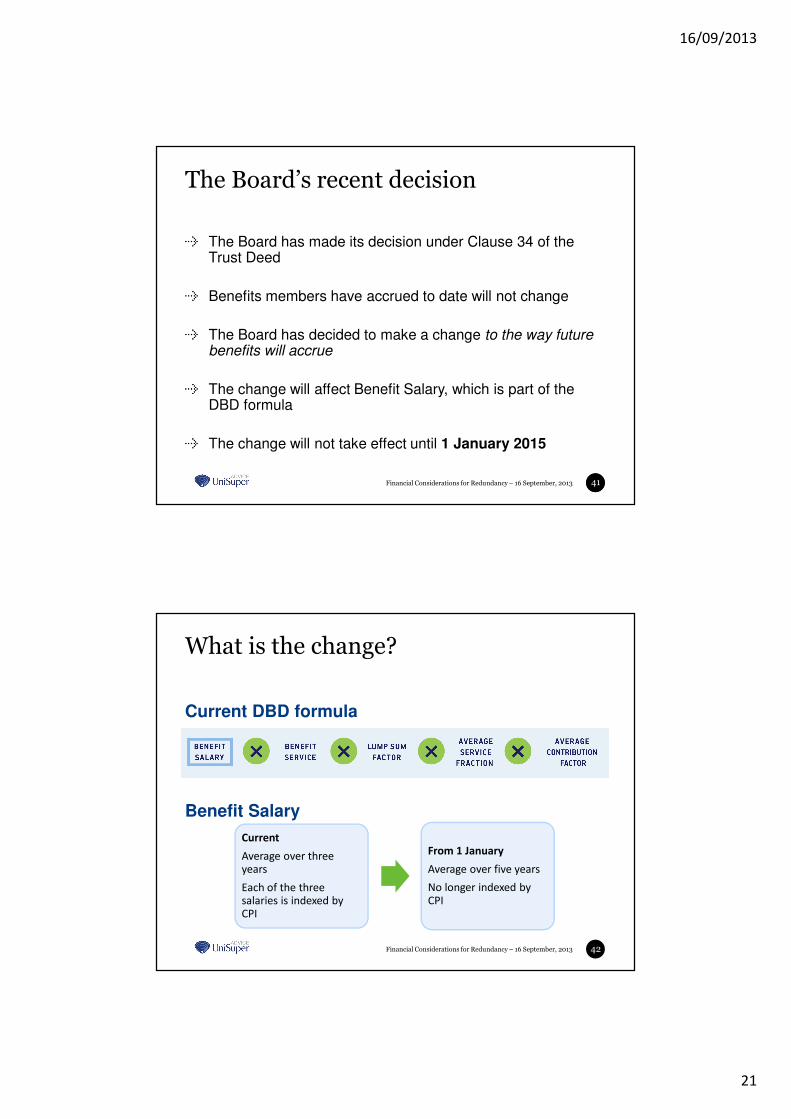

The Board’s recent decision

The Board has made its decision under Clause 34 of the Trust Deed

Benefits members have accrued to date will not change

The Board has decided to make a change to the way future benefits will accrue

The change will affect Benefit Salary, which is part of the DBD formula

The change will not take effect until 1 January 2015

41

Financial Considerations for Redundancy – 16 September, 2013

What is the change?

42

Current DBD formula

Benefit Salary

Current

Average over three years

Each of the three salaries is indexed by CPI

From 1 January

Average over five years

No longer indexed by CPI

16/09/2013

22

Financial Considerations for Redundancy – 16 September, 2013

Further information . . .

Go to:

www.unisuper.com.au/dbdupdate

43

Financial Considerations for Redundancy – 16 September, 2013

Appendix

Further detail on UniSuper Pensions

44

16/09/2013

23

Financial Considerations for Redundancy – 16 September, 2013

Flexi Pension

account-based pension

minimum commencement sum of $25,000

able to withdraw lump sums (commutation).

45

You decide:

• how it is invested – choice of investment option(s)

• payment frequency (fortnightly, monthly, quarterly, bi-

annually or annually)

• pension amount (subject to minimums).

You decide:

• how it is invested – choice of investment option(s)

• payment frequency (fortnightly, monthly, quarterly, bi-

annually or annually)

• pension amount (subject to minimums).

You decide:

• how it is invested – choice of investment option(s)

• payment frequency (fortnightly, monthly, quarterly, bi-

annually or annually)

• pension amount (subject to minimums).

Financial Considerations for Redundancy – 16 September, 2013

Flexi Pension

The minimum pension is calculated upon commencement and at 1

July each year thereafter.

It’s based on your age and account balance.

46

Age % factor (2013/14)

55 – 64 4%

65 – 74 5%

75 – 79 6%

80 – 84 7%

85 – 89 9%

90 – 94 11%

95+ 14%

Example:

On 1 July 2013, Carol is aged 66 and has

an account balance of $400,000.

Her minimum pension for 2013/14 is

$16,000 (i.e. $400,000 x 4%)

Carol nominates to receive a pension of

$2,200 per month ($26,400 p.a.)

16/09/2013

24

Financial Considerations for Redundancy – 16 September, 2013

Commercial Rate Indexed Pension

Lifetime pension purchased using super balance (minimum of $25,000)

Monthly pension indexed in line with the Consumer Price Index (CPI) each July

10-year guarantee period

Pension quote is based on interest rate and age factors.

47

You decide:

• between a single or joint life pension

• if joint, reversionary pension of 100%.

You decide:

• between a single or joint life pension

• if joint, reversionary pension of 100%.

You decide:

• between a single or joint life pension

• if joint, reversionary pension of 100%.

Financial Considerations for Redundancy – 16 September, 2013

Defined Benefit Indexed Pension

Restricted to DBD members prior to 1 July 1998

Lifetime pension based on Trust Deed factors

Monthly pension indexed in line with the CPI each July

Spouse reversionary pension of 62.5%

No residual capital to estate (if not survived by a spouse).

48

You decide:

• whether to take part of the pension as a lump sum prior to

commencement.

16/09/2013

25

Financial Considerations for Redundancy – 16 September, 2013

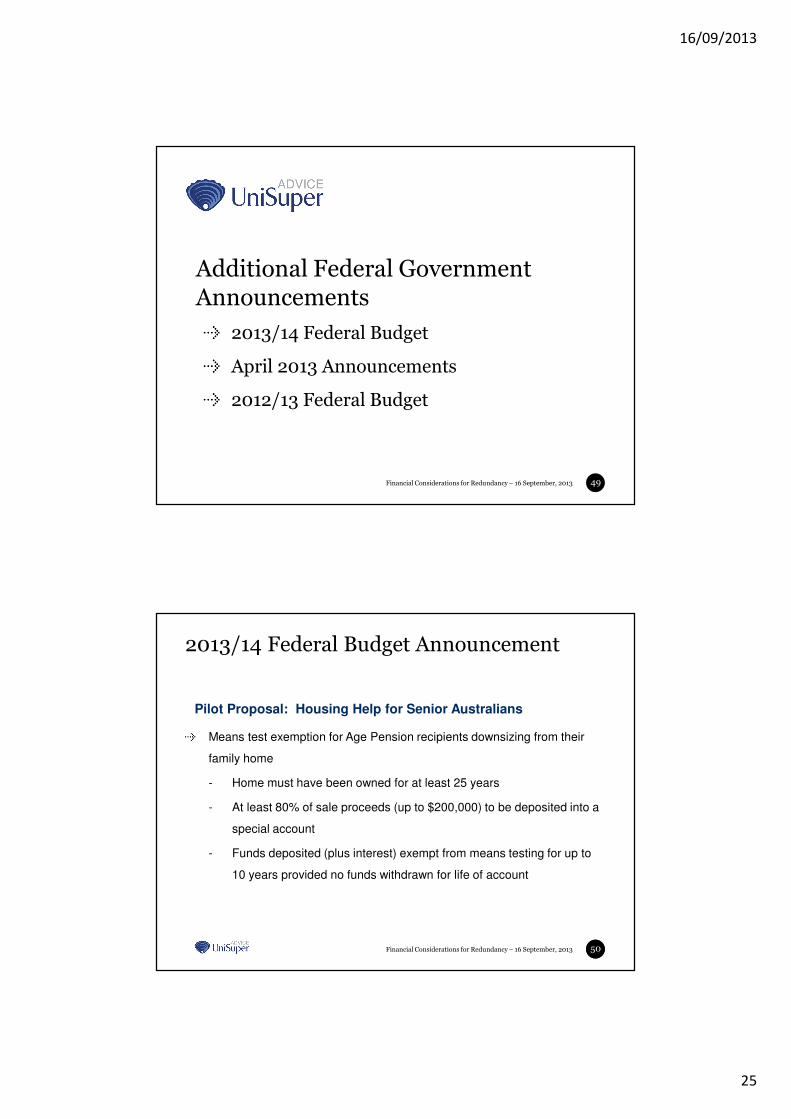

Additional Federal Government Announcements

49

2013/14 Federal Budget

April 2013 Announcements

2012/13 Federal Budget

Financial Considerations for Redundancy – 16 September, 2013

2013/14 Federal Budget Announcement

Pilot Proposal: Housing Help for Senior Australians

Means test exemption for Age Pension recipients downsizing from their

family home

- Home must have been owned for at least 25 years

- At least 80% of sale proceeds (up to $200,000) to be deposited into a

special account

- Funds deposited (plus interest) exempt from means testing for up to

10 years provided no funds withdrawn for life of account

50

16/09/2013

26

Financial Considerations for Redundancy – 16 September, 2013

2013/14 Federal Budget Announcement

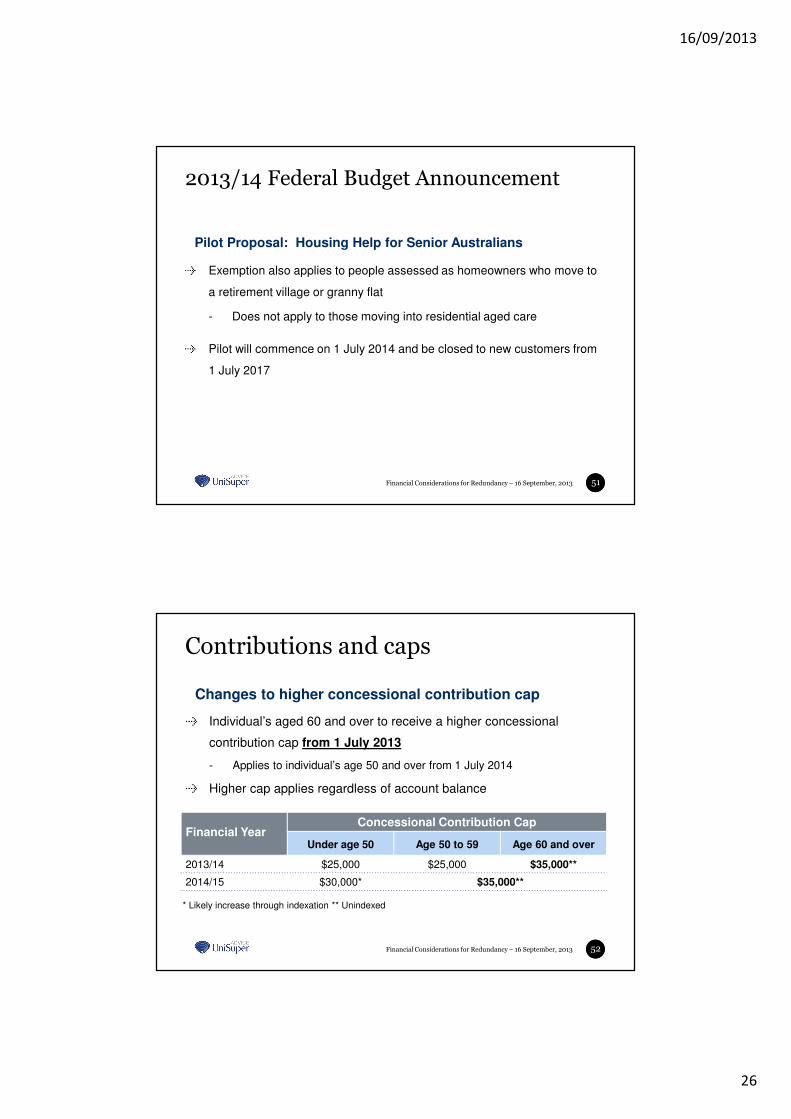

Pilot Proposal: Housing Help for Senior Australians

Exemption also applies to people assessed as homeowners who move to

a retirement village or granny flat

- Does not apply to those moving into residential aged care

Pilot will commence on 1 July 2014 and be closed to new customers from

1 July 2017

51

Financial Considerations for Redundancy – 16 September, 2013

Changes to higher concessional contribution cap

Individual’s aged 60 and over to receive a higher concessional

contribution cap from 1 July 2013

- Applies to individual’s age 50 and over from 1 July 2014

Higher cap applies regardless of account balance

52

Financial YearConcessional Contribution Cap

Under age 50 Age 50 to 59 Age 60 and over

2013/14 $25,000 $25,000 $35,000**

2014/15 $30,000* $35,000**

* Likely increase through indexation ** Unindexed

Contributions and caps

16/09/2013

27

Financial Considerations for Redundancy – 16 September, 2013

April 2013 Federal Government Announcement

Proposal: Cap tax exempt earnings for superannuation income

streams

Includes earnings from dividends, interest and some measure of

assessable capital gains

Applies to all superannuation income streams including defined benefit

pensions

53

Income Stream Earnings Current tax treatment

Proposed tax treatment from 1 July 2014

Up to $100,000 p.a. Nil Nil

Over $100,000 p.a. Nil 15%

Exact details of how the tax will work has not yet been finalised

Financial Considerations for Redundancy – 16 September, 2013

April 2013 Federal Government Announcement

Proposal: Cap tax exempt earnings for superannuation income

streams

Application to defined benefit pensions:

- Notional earnings to be calculated each year per defined benefit

pension member

- Calculations to be based on actuarial calculations, and will depend on

the size of the member’s pension and their age

- Amount of notional earnings will reduce as member grows older

Exact details of how the tax will work has not yet been finalised

54

16/09/2013

28

Financial Considerations for Redundancy – 16 September, 2013

New Treatment for Excess Concessional Contributions

Applies to excess concessional contributions from 1 July 2013

Eligible individual’s can withdraw up to 85% of excess concessional

contributions made from 1 July 2013

Special conditions apply to Defined Benefit members

55

Concessional Contributions from 1 July 2013

Tax on Contribution

Up to the CCC 15%

Over the CCC and remaining in superannuation account Amount included in assessable income and

taxed at marginal tax rate plus interest charge payable to the ATOOver CCC but withdrawn from superannuation

account

CCC = Concessional Contribution Cap

Financial Considerations for Redundancy – 16 September, 2013

April 2013 Federal Government Announcement

Proposal: Deeming rules to apply to income from account-

based pensions

For the purposes of calculating Centrelink Pension entitlements under the

Income Test

Applies to all account-based pensions commenced from 1 January 2015

56

Account-based Pension Commencement Date

Assessment of pension income under Centrelink’s Income Test

Before 1 January 2015 Annual Pension less deduction amount

1 January 2015 onwards Annual Pension deemed

16/09/2013

29

Financial Considerations for Redundancy – 16 September, 2013

April 2013 Federal Government Announcement

Proposal: Deeming rules to apply to income from account-

based pensions

Example: Margaret, aged 65 and single, commences an account based

pension with $500,000 drawing an income stream of $35,000 p.a.

57

Account-based Pension Commencement Date

Assessment of pension income under Centrelink’s Income Test

Before 1 January 2015$11,873

($35,000 – ($500,000/21.62))

1 January 2015 onwards$19,319

(45,400 x 2.5%) + ($454,600 x 4%)

Financial Considerations for Redundancy – 16 September, 2013

April 2013 Federal Government Announcement

Other proposals

Further reforms to the arrangements of lost superannuation

Establishment of a Council of Superannuation Custodians

- to ensure future changes are consistent with an agreed Charter of

Superannuation Adequacy and Sustainability

Extending concessional tax treatment to deferred annuities

58

16/09/2013

30

Financial Considerations for Redundancy – 16 September, 2013

Reduced tax concessions for high income earners

New tax rules apply to individuals with income above $300,000 p.a.

‘Income’ includes concessional contributions to superannuation

Concessional contributions maybe taxed at an extra 15%

- Does not apply to Excess Concessional Contributions subject to

Excess Concessional Contributions Tax

59

Financial Considerations for Redundancy – 16 September, 2013

2012/13 Federal Budget Announcement

Employment Termination Payment (ETP) Tax Offset

Changes to the tax offset applied to Employer Termination Payments

for affected ETP’s (e.g. golden handshakes)

- Only the part of the ETP that takes a person’s taxable income

(including the ETP) to $180,000* receives tax offset

- Existing arrangements for ETP’s relating to genuine redundancy,

invalidity, compensation due to an employment related dispute or

death are likely to remain unchanged.

60

* For the 2012/13 financial year

16/09/2013

31

Financial Considerations for Redundancy – 16 September, 2013

2012/13 Federal Budget Announcement

Mature Age Worker Tax Offset

To be phased out for workers born on or after 1 July 1957

Offset to remain available for tax payers who are aged 55 or older on 30

June 2012.

- Maximum benefit is $500 and you must be receiving income from

working (within certain limits)

61