4 Minute Financial Check-up that could increase your wealth! Check Your Financial Fitness.

Upload

yardley-hansonCategory

view

21download

1description

Financial Check Up

John B. Penson, Jr.Regents Professor and

Stiles Professor of AgricultureTexas A&M University

Seen the Doc Lately? Benefits from an

annual financialfinancial checkup.

Treadmill stress test your financialfinancial strength.

Get your visionvision examined.

What is the status of your…. Liquidity? Solvency? Profitability? Efficiency? Debt

repayment capacity?

Survivability?

Key Financial IndicatorsKey Financial Indicators Measures of liquidity

See equations 1 and 2; page 13 of booklet Measures of solvency

See equations 3 – 6; page 14 Measures of profitability

See equations 7 – 8; page 15 Measures of economic efficiency

See equations 10 – 14; pages 16-17 Measures of debt repayment

capacity See equations 15 – 17; page 17

Measures of Liquidity

1. Current ratioCurrent ratio:• Current assets divided by current liabilities.• Demonstrates ability to cover scheduled current liabilities for the coming year out current assets and still have “cash” left over.• Should exceed 1.0exceed 1.0 to be technically liquid.• Some firms fail despite exceeding this hurdle.

Measures of Liquidity

1. Current ratioCurrent ratio:• Current assets divided by current liabilities.• Demonstrates ability to cover scheduled current liabilities for the coming year out current assets and still have “cash” left over.• Should exceed 1.0exceed 1.0 to be technically liquid.• Some firms fail despite exceeding this hurdle.

2. Working capitalWorking capital:• Current assets minus current liabilities.• Expresses liquidity in dollars rather than ratio.• Should be positive.• Cash is King!Cash is King!

Liquidity TrendsCurrent Ratio

0.00

0.501.00

1.50

2.00

2.503.00

3.50

4.00

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Page 13

Liquidity TrendsCurrent Ratio

0.00

0.501.00

1.50

2.00

2.503.00

3.50

4.00

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

MinimumMinimum

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Page 13

Liquidity Trends

Working Capital-to-Total Assets

0.000.050.100.150.200.250.300.350.400.45

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Desired level varies by type of firm

Desired level varies by type of firm

Page 14

Measures of Solvency

1. Debt ratioDebt ratio:• Total debt divided by total liabilities.• Demonstrates ability to liquidate the firm, cover all liabilities out of all assets, and still have “cash” left over.• Should not exceed 0.50not exceed 0.50 to minimize financial risk exposure.• Some firms fail however at lower levels.

Measures of Solvency

1. Debt ratioDebt ratio:• Total debt divided by total liabilities.• Demonstrates ability to liquidate the firm, cover all liabilities out of all assets, and still have “cash” left over.• Should not exceed 0.50not exceed 0.50 to minimize financial risk exposure.• Some firms fail however at lower levels.

2. Leverage ratioLeverage ratio:• Total debt divided by equity or net worth.• Often a credit standard in loan approval decisions.• Should not exceed 1.0not exceed 1.0 to minimize financial risk exposure.• Effects of rising interest rates.

Solvency Trends

Total Debt-to-Total Assets

0.000.100.200.300.400.500.600.700.800.90

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Page 15

Solvency Trends

Total Debt-to-Total Assets

0.000.100.200.300.400.500.600.700.800.90

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

MaximumMaximum

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Page 15

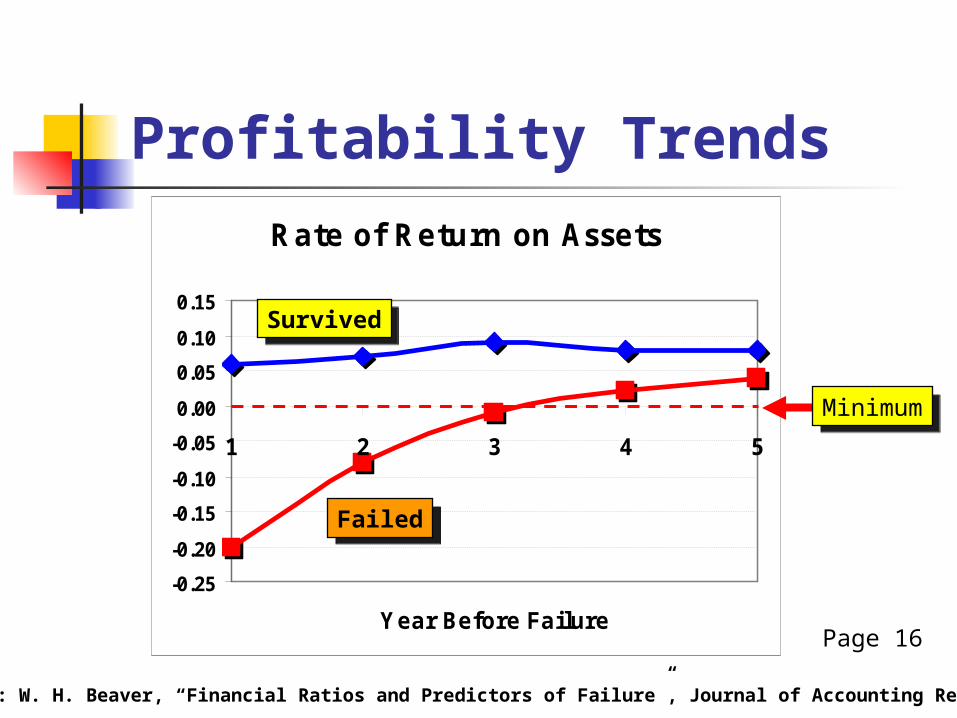

Measures of Profitability

1. Rate of return on assetsRate of return on assets:• Net farm income before interest divided by total assets.• Demonstrates the return to management and total capital invested in the firm. • Should be positivepositive; the higher the better.

Measures of Profitability

1. Rate of return on assetsRate of return on assets:• Net farm income before interest divided by total assets.• Demonstrates the return to management and total capital invested in the firm. • Should be positivepositive; the higher the better.

2. Rate of return on equityRate of return on equity:• Net farm income divided by total equity.• Demonstrates return to owner’s investment in the firm.• Should be positivepositive; the higher the better.

Profitability TrendsRate of Return on Assets

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Page 16

Profitability TrendsRate of Return on Assets

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

MinimumMinimum

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Page 16

Measure of Debt Repayment Capacity

1. Term Debt and Capital Lease Coverage RatioTerm Debt and Capital Lease Coverage Ratio:• Net cash income divided by scheduled principal payments on term loans and capital leases• After provision for taxes and withdrawals. • Should be greater than 1.0greater than 1.0.

Measure of Debt Repayment Capacity

1. Term Debt and Capital Lease Coverage RatioTerm Debt and Capital Lease Coverage Ratio:• Net cash income divided by scheduled principal payments on term loans and capital leases• After provision for taxes and withdrawals. • Should be greater than 1.0greater than 1.0.

2. Debt burden ratioDebt burden ratio:• Total liabilities divided by net income• After provision for taxes and depreciation• Should be as low as possible to avoid financial risk exposure

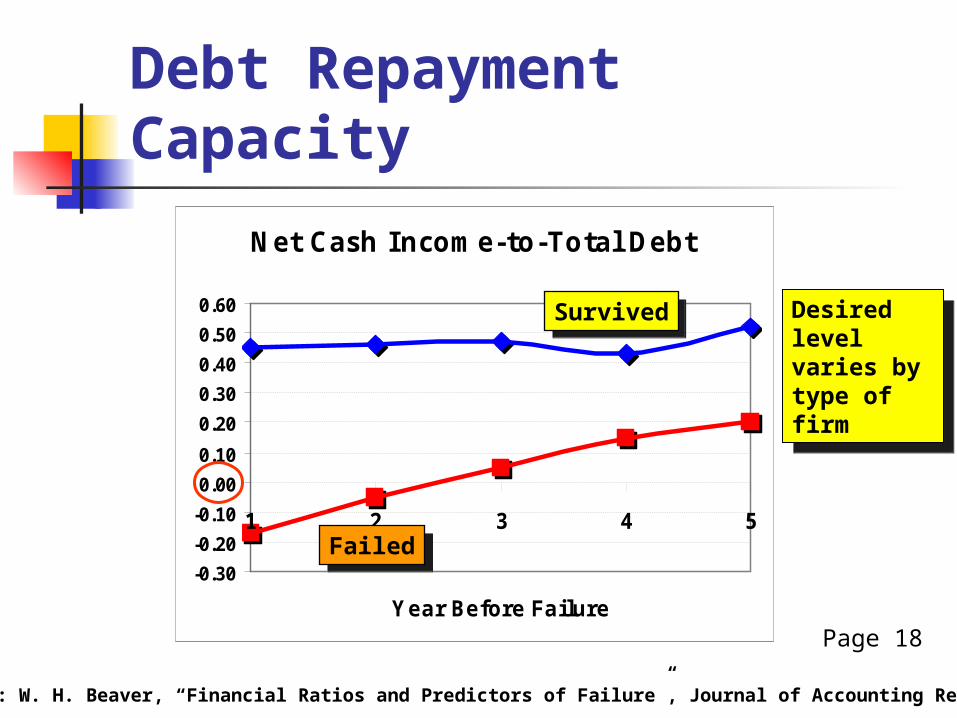

Debt Repayment Capacity

Net Cash Income-to-Total Debt

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

1 2 3 4 5

Year Before Failure

SurvivedSurvived

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Desired level varies by type of firm

Desired level varies by type of firm

Page 18

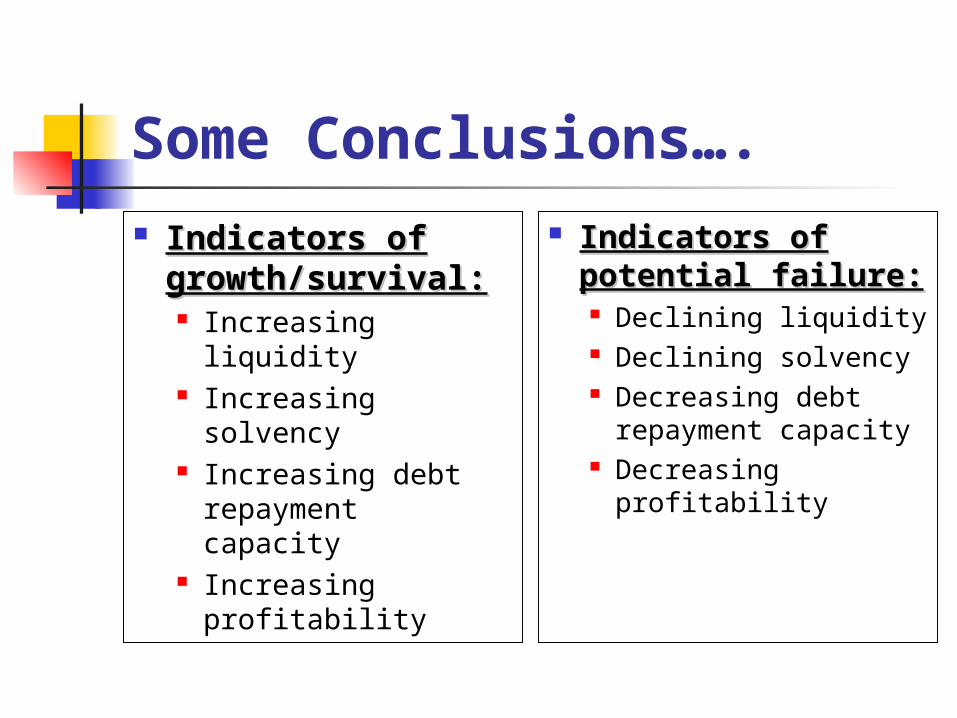

Some Conclusions…. Indicators of Indicators of

growth/survival:growth/survival: Increasing liquidity Increasing solvency Increasing debt

repayment capacity Increasing

profitability

Indicators of Indicators of potential potential failure:failure: Declining liquidity Declining solvency Decreasing debt

repayment capacity

Decreasing profitability

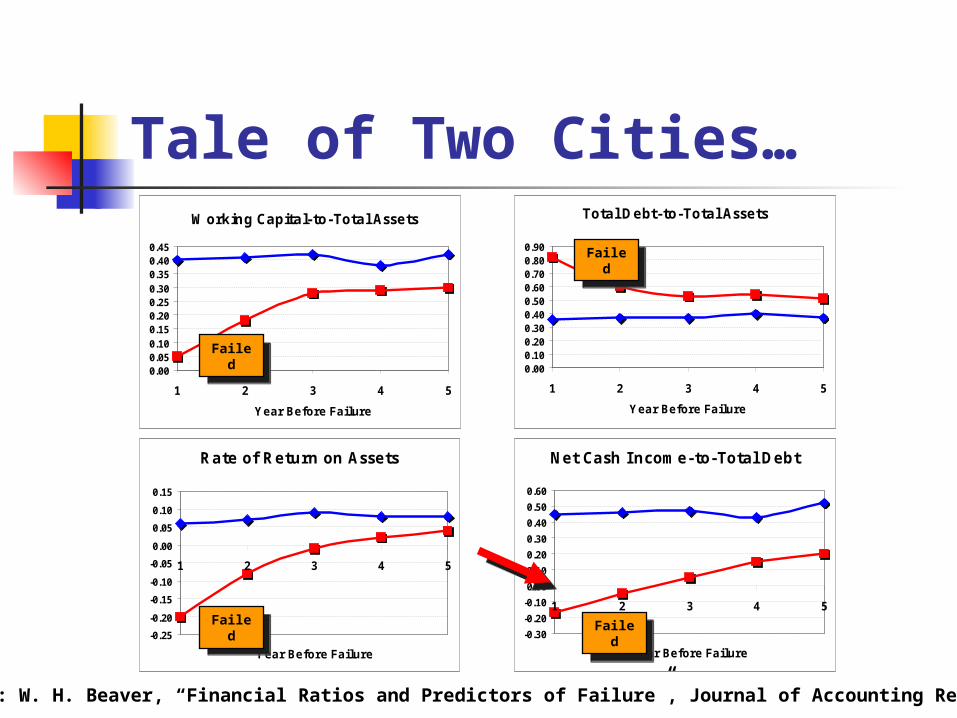

Tale of Two Cities…Working Capital-to-Total Assets

0.000.050.100.150.200.250.300.350.400.45

1 2 3 4 5

Year Before Failure

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Tale of Two Cities…Working Capital-to-Total Assets

0.000.050.100.150.200.250.300.350.400.45

1 2 3 4 5

Year Before Failure

Total Debt-to-Total Assets

0.000.100.200.300.400.500.600.700.800.90

1 2 3 4 5

Year Before Failure

FailedFailed

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Tale of Two Cities…

Rate of Return on Assets

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

1 2 3 4 5

Year Before Failure

Working Capital-to-Total Assets

0.000.050.100.150.200.250.300.350.400.45

1 2 3 4 5

Year Before Failure

Total Debt-to-Total Assets

0.000.100.200.300.400.500.600.700.800.90

1 2 3 4 5

Year Before Failure

FailedFailed

FailedFailed

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

Tale of Two Cities…

Rate of Return on Assets

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

1 2 3 4 5

Year Before Failure

Net Cash Income-to-Total Debt

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

1 2 3 4 5

Year Before Failure

Working Capital-to-Total Assets

0.000.050.100.150.200.250.300.350.400.45

1 2 3 4 5

Year Before Failure

Total Debt-to-Total Assets

0.000.100.200.300.400.500.600.700.800.90

1 2 3 4 5

Year Before Failure

FailedFailed

FailedFailed

FailedFailed

FailedFailed

Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

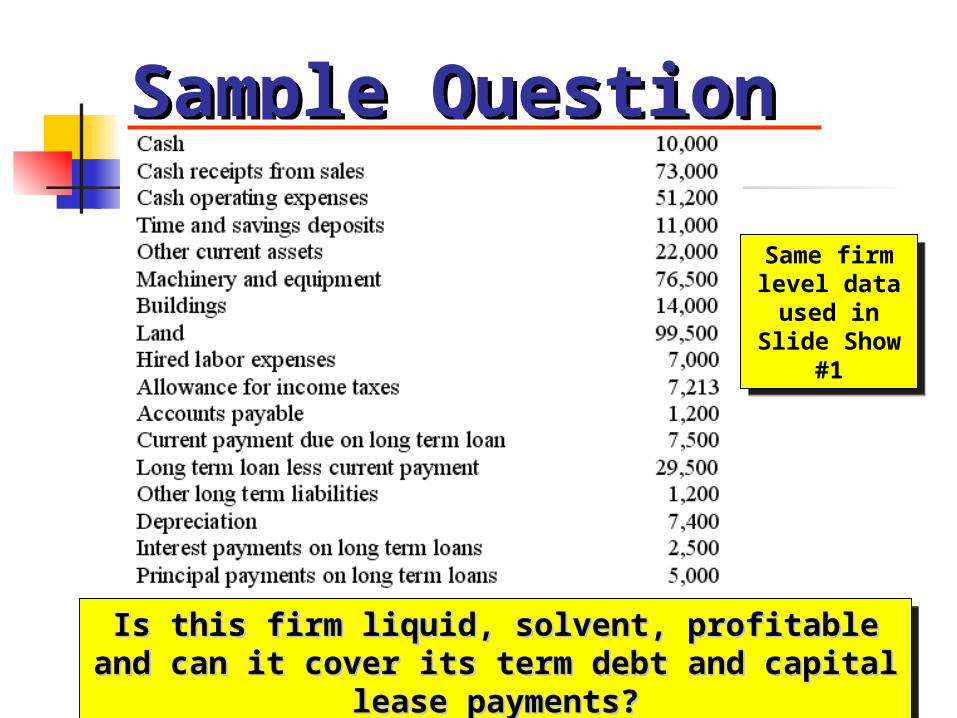

Sample QuestionSample Question

Is this firm liquid, solvent, profitable and can it cover Is this firm liquid, solvent, profitable and can it cover its term debt and capital lease payments?its term debt and capital lease payments?

Is this firm liquid, solvent, profitable and can it cover Is this firm liquid, solvent, profitable and can it cover its term debt and capital lease payments?its term debt and capital lease payments?

Same firm level data

used in Slide Show

#1

Same firm level data

used in Slide Show

#1

Step #1 Calculate the followingStep #1 Calculate the following: 1. Current assets and total assets2. Current liabilities and total liabilities3. Net income4. Equity (or net worth)

Total current assets = 10,000 + 11,000 + 22,000 = 43,000Total current liabilities = 1,200 + 7,500 + 7,213 = 15,913Total assets = total current assets + 76,500 +14,000 + 99,500 = 233,000Total liabilities = total current liabilities + 29,500 + 1,200 = 46,613Equity = 233,000 – 46,613 = 186,387 Cash receipts from product sales = 73,000Total operating expenses = 51,200 + 2,500 + 7,400 = 61,100Net income from operations = 73,000 – 61,100 = 11,900Net income before taxes = 11,900Net income = 11,900 – 7,213 = 4,687

Sample QuestionSample Question

Step #2 Calculate the followingStep #2 Calculate the following: 1. Current ratio2. Debt and leverage ratio

Asset liquidity analysisAsset liquidity analysis:Total current assets = 10,000 + 11,000 + 22,000 = 43,000Total current liabilities = 1,200 + 7,500 + 7,213 = 15,913Current ratio = 43,000/15,913 = 2.702Working capital = 43,000 – 15,913 = 27,087

Solvency analysisSolvency analysis: Total assets = total current assets + 76,500 +14,000 + 99,500 = 233,000Total liabilities = total current liabilities + 29,500 + 1,200 = 46,613Equity = 233,000 – 46,613 = 186,387Debt ratio = 46,613/233,000 = 0.20Leverage ratio = 46,613/186,387 = 0.25

Sample QuestionSample Question

Step #3 Calculate the followingStep #3 Calculate the following: 3. ROA and ROE

Total assets = 233,000Equity = 186,387 Cash receipts from product sales = 73,000Total operating expenses = 51,200 + 2,500 + 7,400 = 61,100Net income from operations = 73,000 – 61,100 = 11,900Net income before taxes = 11,900Net income = 11,900 – 7,213 = 4,687

Profitability analysisProfitability analysis:ROA = (4,687 + 2,500)/233,000 = 0.0308 or 3.1%ROE = 4,687/186,387 = 0.025 or 2.5%

Sample QuestionSample Question

Step #4 Calculate the followingStep #4 Calculate the following: 4. Term debt and capital lease coverage ratio5. Debt burden ratio

Debt repayment capacity analysisDebt repayment capacity analysis:Net cash income = 4,687 + 7,400 = 12,087Principal payments = 5,000Coverage ratio = 12,087/5,000 = 2.42

Debt burden analysisDebt burden analysis:Net income = 4,687Total liabilities = 46,613Debt burden ratio = 46,613/4,687 = 9.95

Sample QuestionSample Question

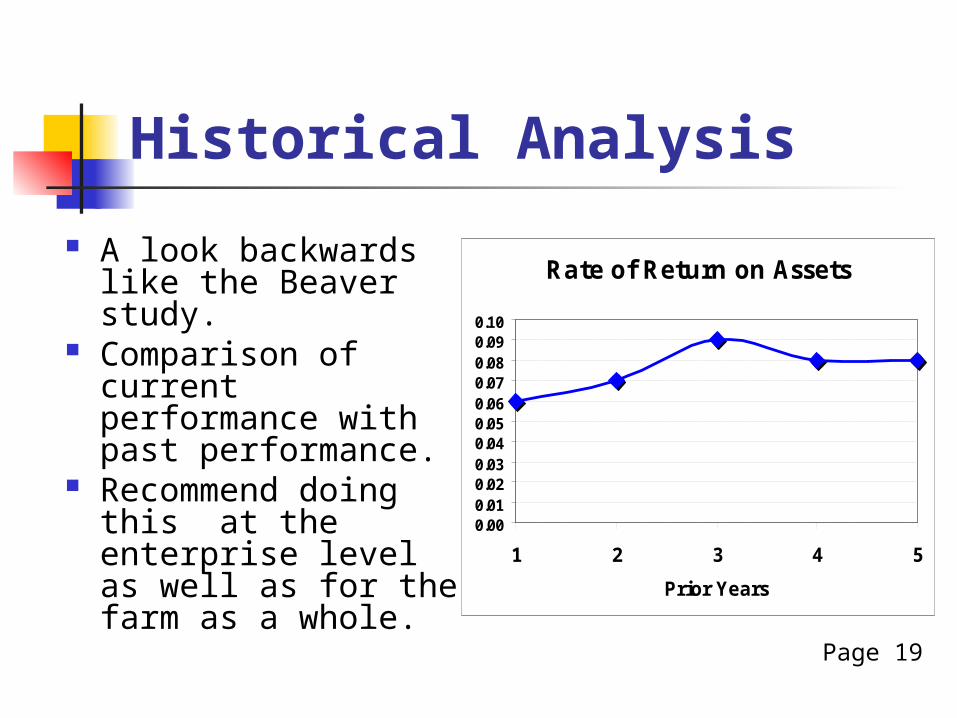

Historical Analysis

A look backwards like the Beaver study.

Comparison of current performance with past performance.

Recommend doing this at the enterprise level as well as for the farm as a whole.

Rate of Return on Assets

0.000.010.020.030.040.050.060.070.080.090.10

1 2 3 4 5

Prior Years

Page 19

Historical Analysis A look backwards like

the Beaver study. Comparison of current

performance with past performance.

Recommend doing this at the enterprise level as well as for the farm as a whole.

Reasons underlying unwanted trends such as the declines in declines in last two years?last two years?

Rate of Return on Assets

0.000.010.020.030.040.050.060.070.080.090.10

1 2 3 4 5

Prior Years

Page 19

Comparative Analysis Compare the firm’s

current performance with the performance of similar operations like the Beaver study did.

Benchmark analysis at enterprise level should be done whenever possible.

Rate of Return on Assets

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

1 2 3 4 5

Prior Years

Your firmYour firm

BenchmarkBenchmark

Page 20

Comparative Analysis Compare the firm’s

current performance with the performance of similar operations like the Beaver study did.

Benchmark analysis at enterprise level should be done whenever possible.

Address reasons why your firm is performing more poorly than other comparable operations before it is too latebefore it is too late.

Rate of Return on Assets

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

1 2 3 4 5

Prior Years

Your firmYour firm

BenchmarkBenchmark

Page 20

Pro Forma Analysis Stress testingStress testing

current expected cash flows by varying prices, unit costs and yields (Slide Show #3).

Look at implications of longer run price and unit cost trends on future financial future financial healthhealth when making major decisions.

Forces of change…. Impacts of rising unit costs of

production inputs. Prices, costs and yields can all

affect the financial health of the firm.

Failure to account for the risk associated with adverse trends can lead to failure of the firm.

Sources of Uncertainty Global trends in

production and consumption

Energy prices and core inflation trends

Interest rates and exchange rates

WTO and the 2007 farm bill

Any Questions?Any Questions?