Financial Assessment of Wind Project 18-19, 2011 | Dhaka, Bangladesh . Agenda What is financial...

24

1.800.580.3765 ▪ WWW.TTECI.COM Financial Assessment of Wind Project Presented to: USAID Wind Workshop October 18-19, 2011 | Dhaka, Bangladesh

Transcript of Financial Assessment of Wind Project 18-19, 2011 | Dhaka, Bangladesh . Agenda What is financial...

1.800.580.3765 ▪ WWW.TTECI.COM

Financial Assessment of

Wind Project

Presented to:

USAID Wind Workshop October 18-19, 2011 | Dhaka, Bangladesh

Agenda

What is financial assessment? • Revenue

• Capital costs

• Operating costs

Financial statements and metrics

What is the associated uncertainty? • Project stages

• Reduction in uncertainty

What are the financing options? • Organizational structure

• Financing structure

Module Objectives

Learning Objectives

• Understand the components of financial model

• Understand the components of revenue in a wind project

• Understand the components of capital cost

• Understand the components of recurring cost

• Understand the financial performance metrics

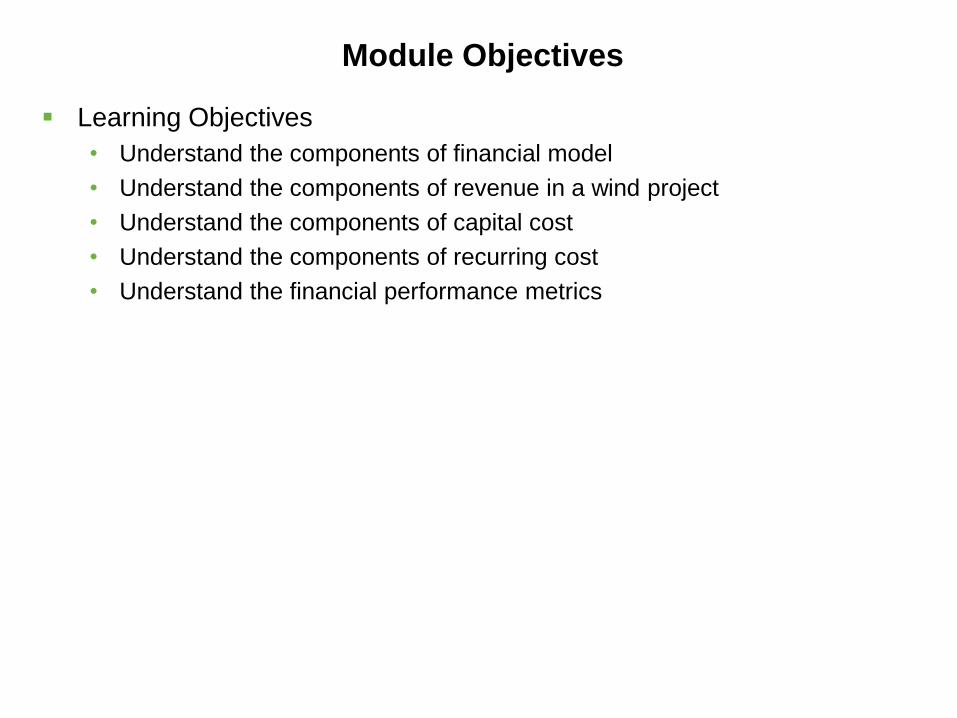

Financial Assessment

Role of Financial Assessment in Wind Project

Prospecting Wind Resource

Assessment

PPA

Financing

Engineering

Procurement

Contracting

Construction Installation

Commissioning

Operations & Maintenance

Components of Financial Model

Deterministic Financial Model

Capital & Operating

Cost

PPA

Average Annual Energy Prod

Risk

Cost

Time

Others

PPA

Risk-based Financial Model

Scenarios Uncertainty Impact on financial

performance

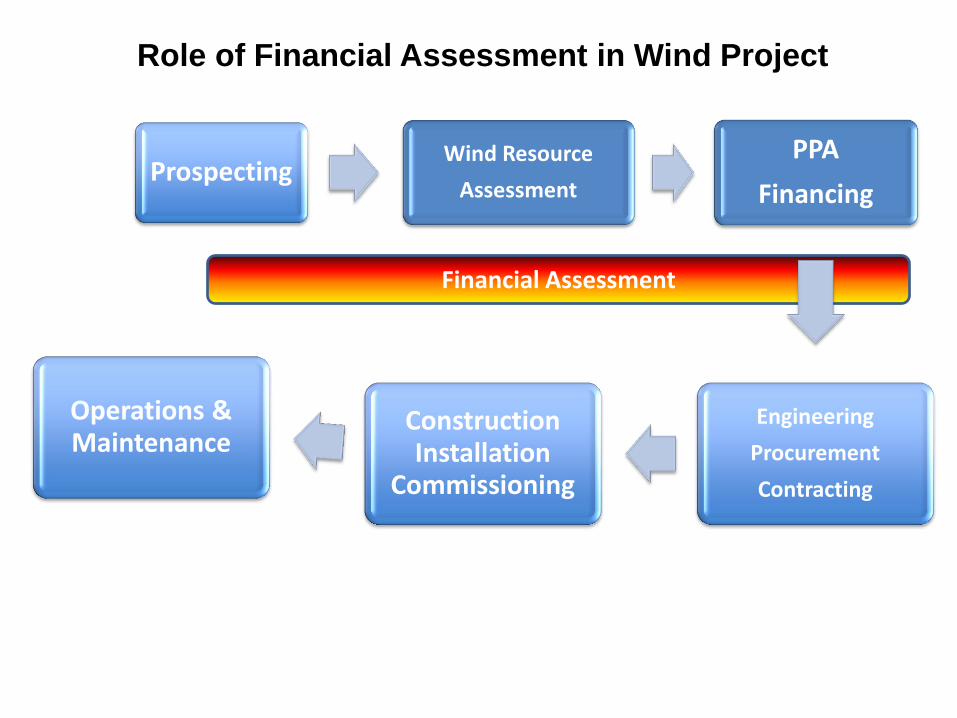

Revenue Sources

Sale of Electricity

PPA

Market

FiT

Net-Meter

Sale of Environmental

Attributes

• Negotiated • Long-term

• Spot market • High volatility

Captive use

Mandated

Tax Benefits

Energy

Carbon CER

$

• Carbon credits • Renewable Energy

Certificates

Energy PTC

Taxable Income

Taxes

Tax >= PTC

PTC

TE Partner

• Tax incentives tied to amount of energy produced •Accelerated depreciation

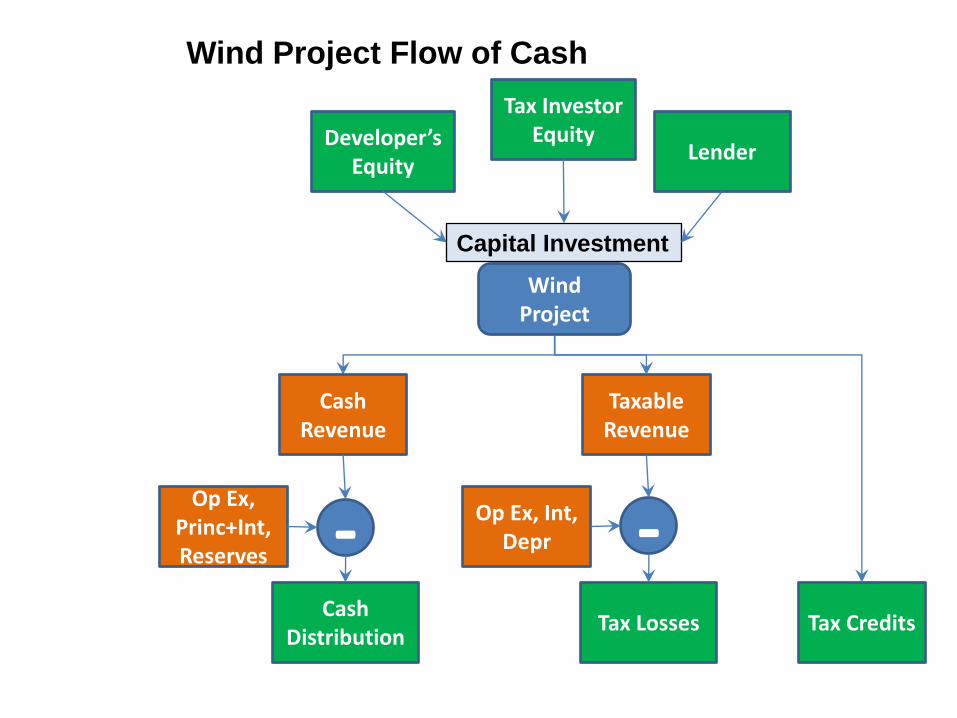

Wind Project Flow of Cash

Wind Project

Developer’s Equity

Tax Investor Equity

Lender

Capital Investment

Cash Revenue

Taxable Revenue

Tax Credits

Op Ex, Princ+Int, Reserves

Op Ex, Int, Depr - -

Cash Distribution

Tax Losses

Sale Price of Wind Energy in US, Source Lawrence Berkeley National Labs

Source: P. Jain, Wind Energy Engineering, 2010

Range of Capital Costs & Recurring Costs

Range, $/kW Reasons for variance

Capital Costs (Total Installed Cost)

$1,200 to $2,200 Normal range: $1,800 to $2,100

India costs are: $1,200 to $1,500/kW US costs are: $1,800 /kW Europe costs are: $2,000/kW Shipping cost, Terrain, Insurance

Operations and maintenance

$20 to $50/kW annually Normal: $40/KW

Duration of manufacturer warranty Remoteness of site

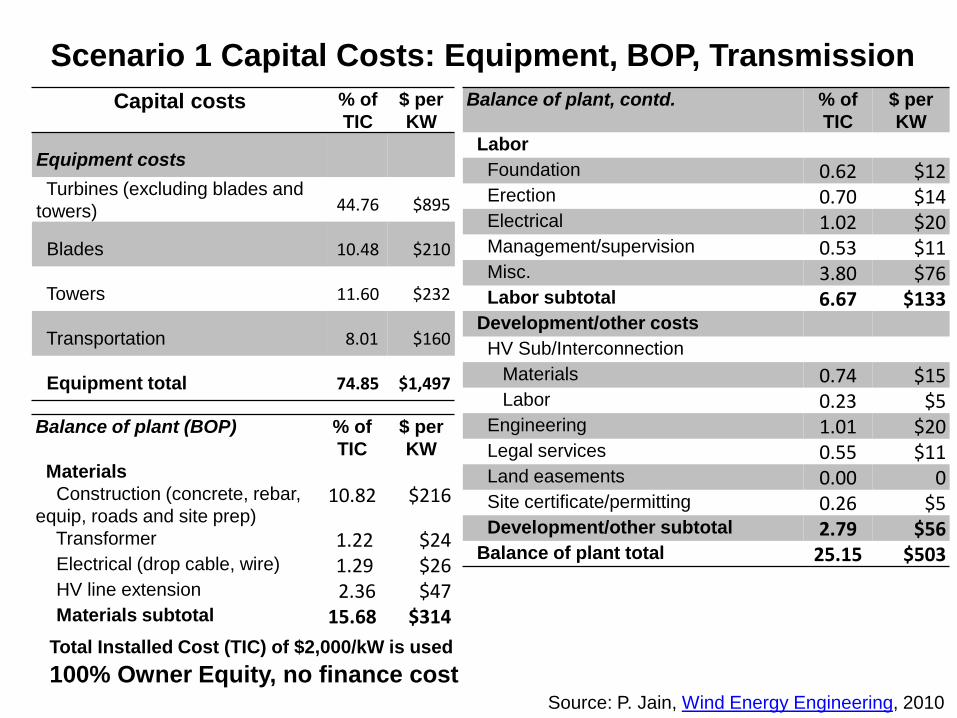

Scenario 1 Capital Costs: Equipment, BOP, Transmission

Capital costs % of

TIC

$ per

KW

Equipment costs

Turbines (excluding blades and

towers) 44.76 $895

Blades 10.48 $210

Towers 11.60 $232

Transportation 8.01 $160

Equipment total 74.85 $1,497

Balance of plant, contd. % of

TIC

$ per

KW

Labor Foundation 0.62 $12 Erection 0.70 $14 Electrical 1.02 $20 Management/supervision 0.53 $11 Misc. 3.80 $76 Labor subtotal 6.67 $133 Development/other costs HV Sub/Interconnection Materials 0.74 $15 Labor 0.23 $5 Engineering 1.01 $20 Legal services 0.55 $11 Land easements 0.00 0 Site certificate/permitting 0.26 $5 Development/other subtotal 2.79 $56 Balance of plant total 25.15 $503

Balance of plant (BOP) % of

TIC

$ per

KW

Materials

Construction (concrete, rebar,

equip, roads and site prep) 10.82 $216

Transformer 1.22 $24 Electrical (drop cable, wire) 1.29 $26 HV line extension 2.36 $47 Materials subtotal 15.68 $314

Total Installed Cost (TIC) of $2,000/kW is used

Source: P. Jain, Wind Energy Engineering, 2010

100% Owner Equity, no finance cost

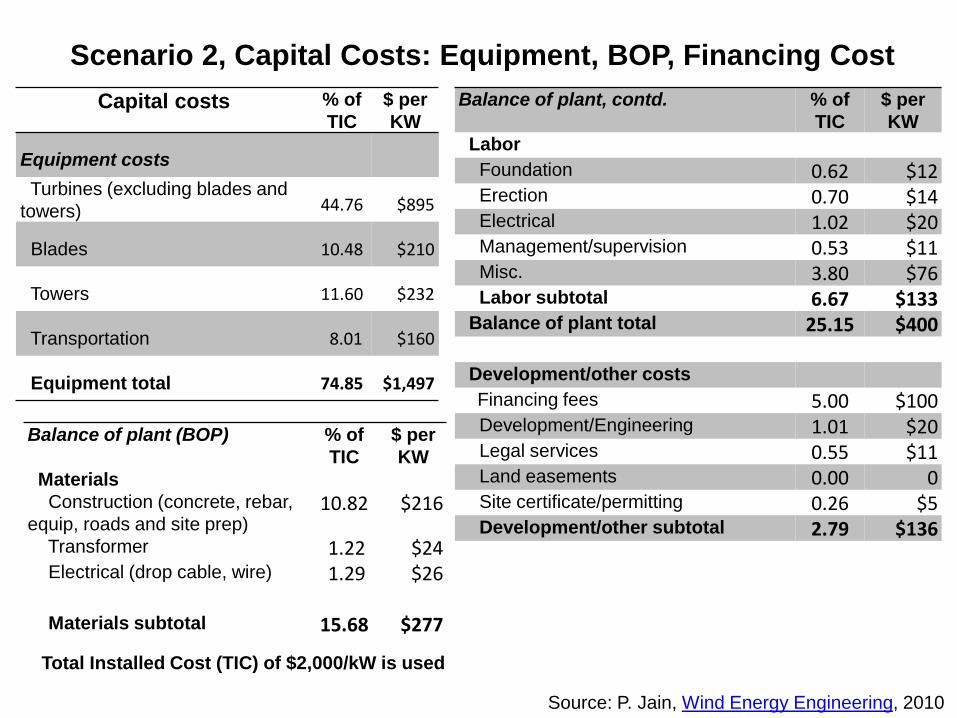

Scenario 2, Capital Costs: Equipment, BOP, Financing Cost

Capital costs % of

TIC

$ per

KW

Equipment costs

Turbines (excluding blades and

towers) 44.76 $895

Blades 10.48 $210

Towers 11.60 $232

Transportation 8.01 $160

Equipment total 74.85 $1,497

Balance of plant, contd. % of

TIC

$ per

KW

Labor Foundation 0.62 $12 Erection 0.70 $14 Electrical 1.02 $20 Management/supervision 0.53 $11 Misc. 3.80 $76 Labor subtotal 6.67 $133 Balance of plant total 25.15 $400

Development/other costs Financing fees 5.00 $100

Development/Engineering 1.01 $20 Legal services 0.55 $11 Land easements 0.00 0 Site certificate/permitting 0.26 $5 Development/other subtotal 2.79 $136

Balance of plant (BOP) % of

TIC

$ per

KW

Materials

Construction (concrete, rebar,

equip, roads and site prep) 10.82 $216

Transformer 1.22 $24 Electrical (drop cable, wire) 1.29 $26

Materials subtotal 15.68 $277

Total Installed Cost (TIC) of $2,000/kW is used

Source: P. Jain, Wind Energy Engineering, 2010

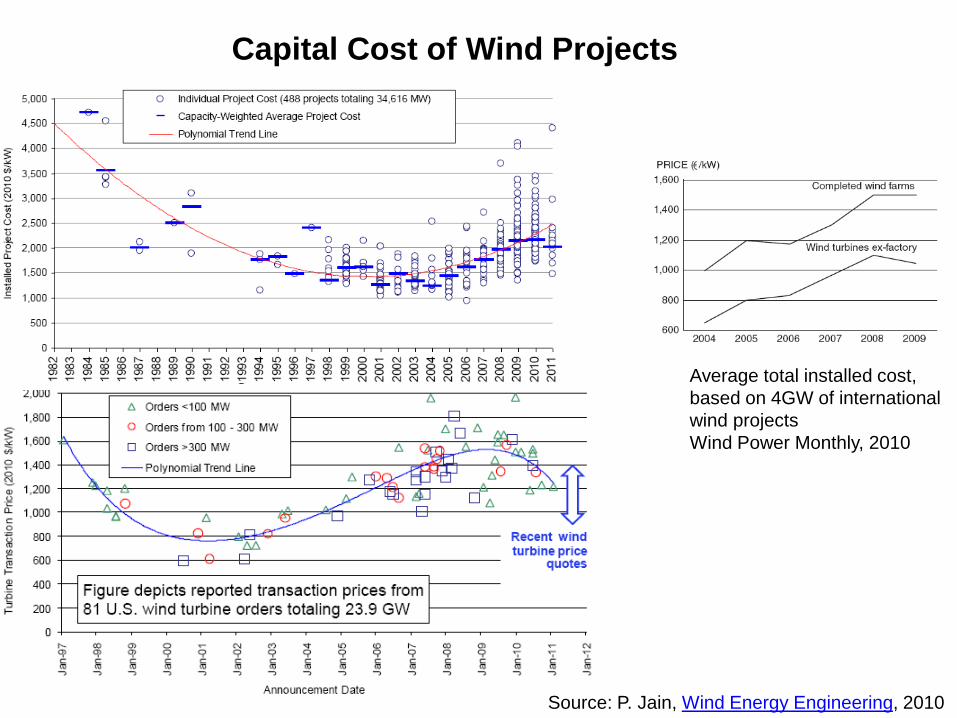

Capital Cost of Wind Projects

Average total installed cost,

based on 4GW of international

wind projects

Wind Power Monthly, 2010

Source: P. Jain, Wind Energy Engineering, 2010

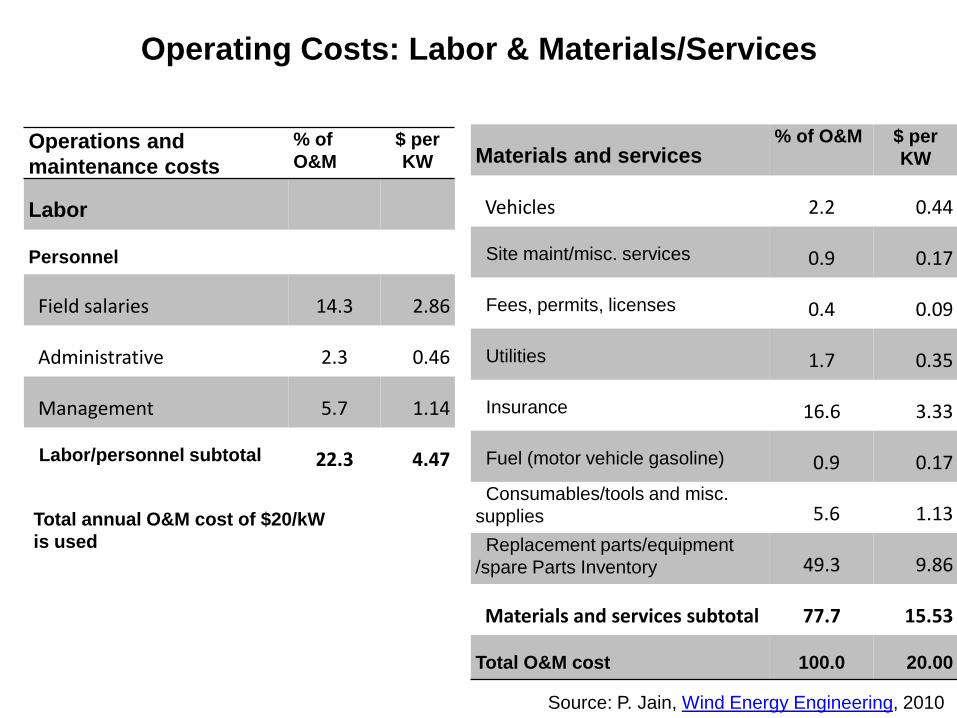

Operating Costs: Labor & Materials/Services

Operations and

maintenance costs

% of

O&M

$ per

KW

Labor

Personnel

Field salaries 14.3 2.86

Administrative 2.3 0.46

Management 5.7 1.14

Labor/personnel subtotal 22.3 4.47

Materials and services % of O&M $ per

KW

Vehicles 2.2 0.44

Site maint/misc. services 0.9 0.17

Fees, permits, licenses 0.4 0.09

Utilities 1.7 0.35

Insurance 16.6 3.33

Fuel (motor vehicle gasoline) 0.9 0.17

Consumables/tools and misc.

supplies 5.6 1.13

Replacement parts/equipment

/spare Parts Inventory 49.3 9.86

Materials and services subtotal 77.7 15.53

Total O&M cost 100.0 20.00

Total annual O&M cost of $20/kW

is used

Source: P. Jain, Wind Energy Engineering, 2010

Questions?

Questions?

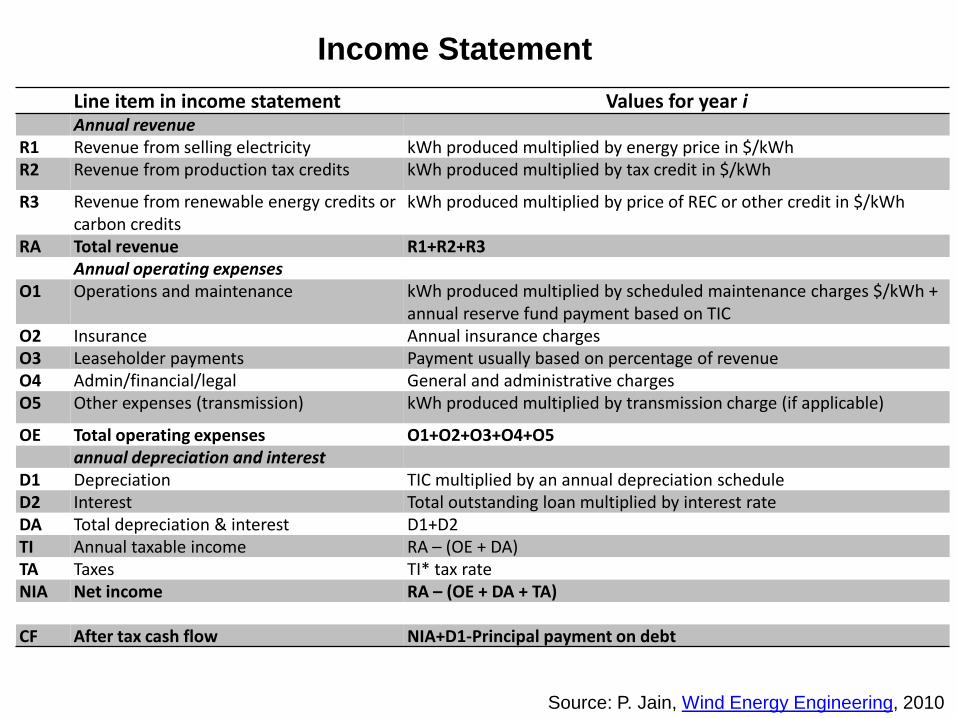

Line item in income statement Values for year i Annual revenue

R1 Revenue from selling electricity kWh produced multiplied by energy price in $/kWh

R2 Revenue from production tax credits kWh produced multiplied by tax credit in $/kWh

R3 Revenue from renewable energy credits or carbon credits

kWh produced multiplied by price of REC or other credit in $/kWh

RA Total revenue R1+R2+R3

Annual operating expenses

O1 Operations and maintenance kWh produced multiplied by scheduled maintenance charges $/kWh + annual reserve fund payment based on TIC

O2 Insurance Annual insurance charges O3 Leaseholder payments Payment usually based on percentage of revenue

O4 Admin/financial/legal General and administrative charges

O5 Other expenses (transmission) kWh produced multiplied by transmission charge (if applicable)

OE Total operating expenses O1+O2+O3+O4+O5

annual depreciation and interest D1 Depreciation TIC multiplied by an annual depreciation schedule

D2 Interest Total outstanding loan multiplied by interest rate

DA Total depreciation & interest D1+D2

TI Annual taxable income RA – (OE + DA) TA Taxes TI* tax rate

NIA Net income RA – (OE + DA + TA)

CF After tax cash flow NIA+D1-Principal payment on debt

Income Statement

Source: P. Jain, Wind Energy Engineering, 2010

Balance Sheet

Balance sheet line items Values for year i Current assets

B1 Cash in bank Year-end cash position

BA Total current assets B1

Fixed assets

FA1 Machinery and equipment Total installed cost of the project

FA2 Less accumulated depreciation Sum of depreciation claimed up to current year

FAA Total fixed assets FA1 – FA2

Total assets FAA + B1

Liabilities and equity

L1 Current liabilities Short-term debt L2 Long term debt Long-term debt LA Total liabilities L1 + L2

Owner’s equity

C1 Invested capital Equity investment in project

C2 Retained earnings From income statement CA Total owner’s equity C1 + C2

Total liabilities + owner’s equity LA + CA

Source: P. Jain, Wind Energy Engineering, 2010

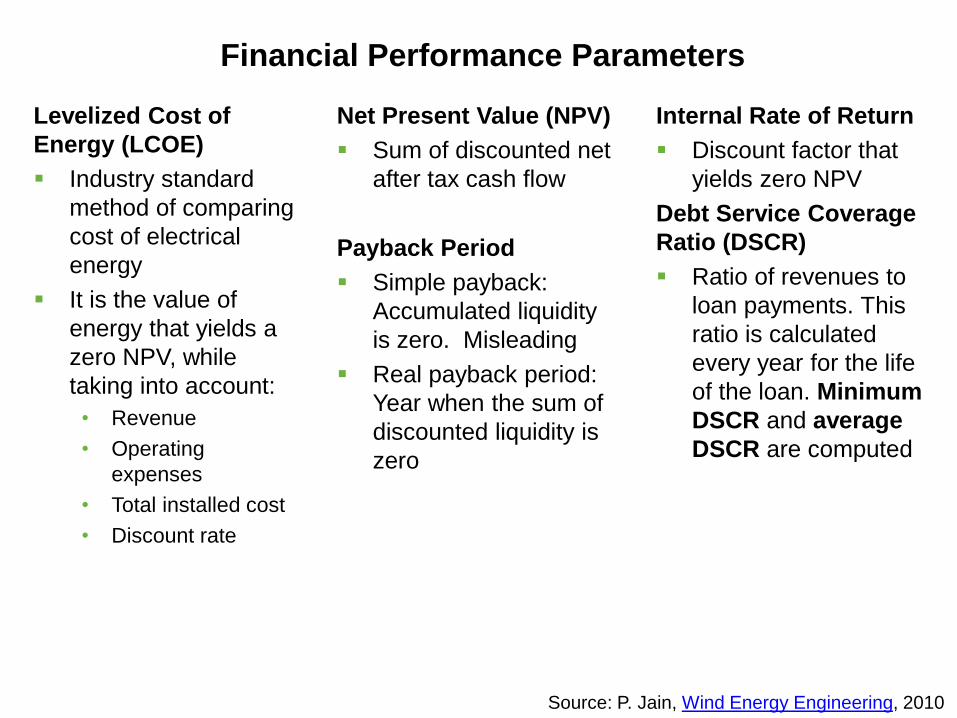

Financial Performance Parameters

Levelized Cost of

Energy (LCOE)

Industry standard

method of comparing

cost of electrical

energy

It is the value of

energy that yields a

zero NPV, while

taking into account:

• Revenue

• Operating

expenses

• Total installed cost

• Discount rate

Net Present Value (NPV)

Sum of discounted net

after tax cash flow

Payback Period

Simple payback:

Accumulated liquidity

is zero. Misleading

Real payback period:

Year when the sum of

discounted liquidity is

zero

Internal Rate of Return

Discount factor that

yields zero NPV

Debt Service Coverage

Ratio (DSCR)

Ratio of revenues to

loan payments. This

ratio is calculated

every year for the life

of the loan. Minimum

DSCR and average

DSCR are computed

Source: P. Jain, Wind Energy Engineering, 2010

Implications of Debt Service Coverage Ratio

Common to have minimum DSCR in the first year of operation

• This is because of ramp up of production, leading to lower revenue

Minimum DSCR limits the amount of debt

• => higher equity requirement

• => lower return

Tricks used:

• Front load the PPA (through constant nominal payments)

• Back load debt payments

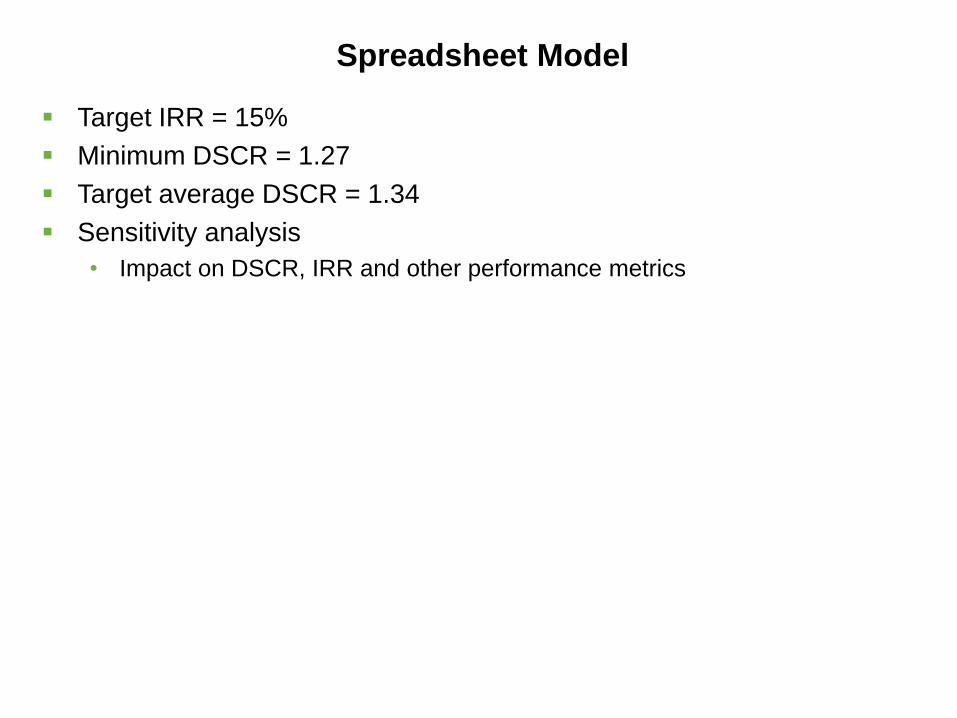

Spreadsheet Model

Target IRR = 15%

Minimum DSCR = 1.27

Target average DSCR = 1.34

Sensitivity analysis

• Impact on DSCR, IRR and other performance metrics

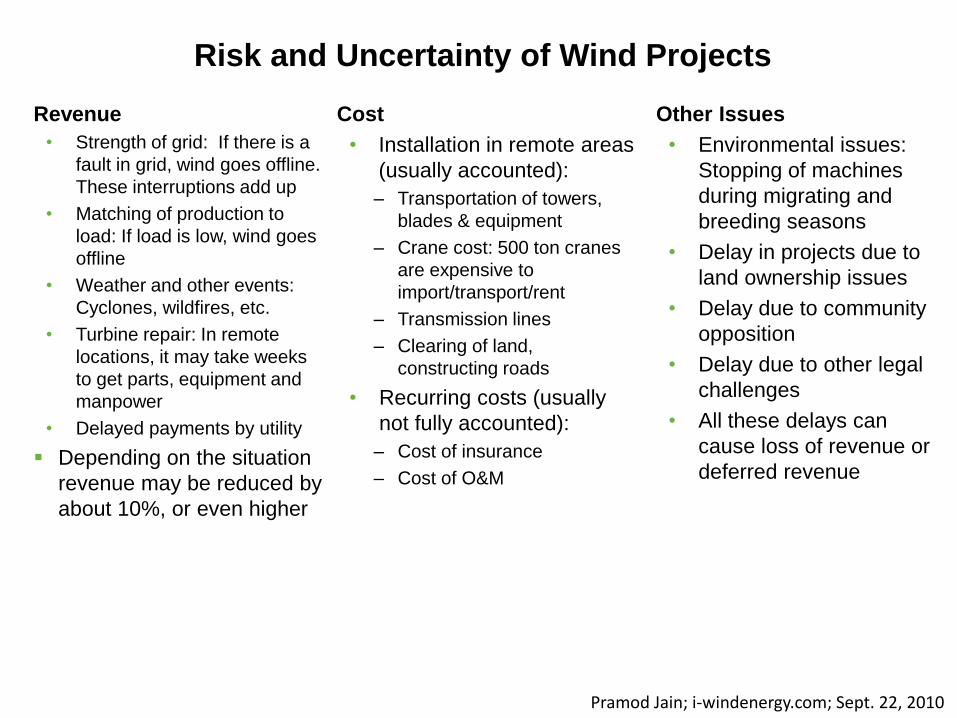

Risk and Uncertainty of Wind Projects

Revenue

• Strength of grid: If there is a

fault in grid, wind goes offline.

These interruptions add up

• Matching of production to

load: If load is low, wind goes

offline

• Weather and other events:

Cyclones, wildfires, etc.

• Turbine repair: In remote

locations, it may take weeks

to get parts, equipment and

manpower

• Delayed payments by utility

Depending on the situation

revenue may be reduced by

about 10%, or even higher

Cost

• Installation in remote areas

(usually accounted):

– Transportation of towers,

blades & equipment

– Crane cost: 500 ton cranes

are expensive to

import/transport/rent

– Transmission lines

– Clearing of land,

constructing roads

• Recurring costs (usually

not fully accounted):

– Cost of insurance

– Cost of O&M

Other Issues

• Environmental issues:

Stopping of machines

during migrating and

breeding seasons

• Delay in projects due to

land ownership issues

• Delay due to community

opposition

• Delay due to other legal

challenges

• All these delays can

cause loss of revenue or

deferred revenue

Pramod Jain; i-windenergy.com; Sept. 22, 2010

Organization Structure and Flow of Money

Alternate Organization

Structures

Corporate structure

Tax-equity & flip investor

Debt leveraged

Source: P. Jain, Wind Energy Engineering, 2010

Sources of Investment

Corporate

Tax-equity investor

Equity investor

Banks and other lenders

Government funding agencies

International development financing: ADB, World Bank, USTDA

Export promotion agencies, e.g. USEXIM

Vendor financing or arm of vendor (e.g. GE Capital)

• May be cheaper than others because of lower due diligence and interest in

winning business

• May be easier to get BOP financing

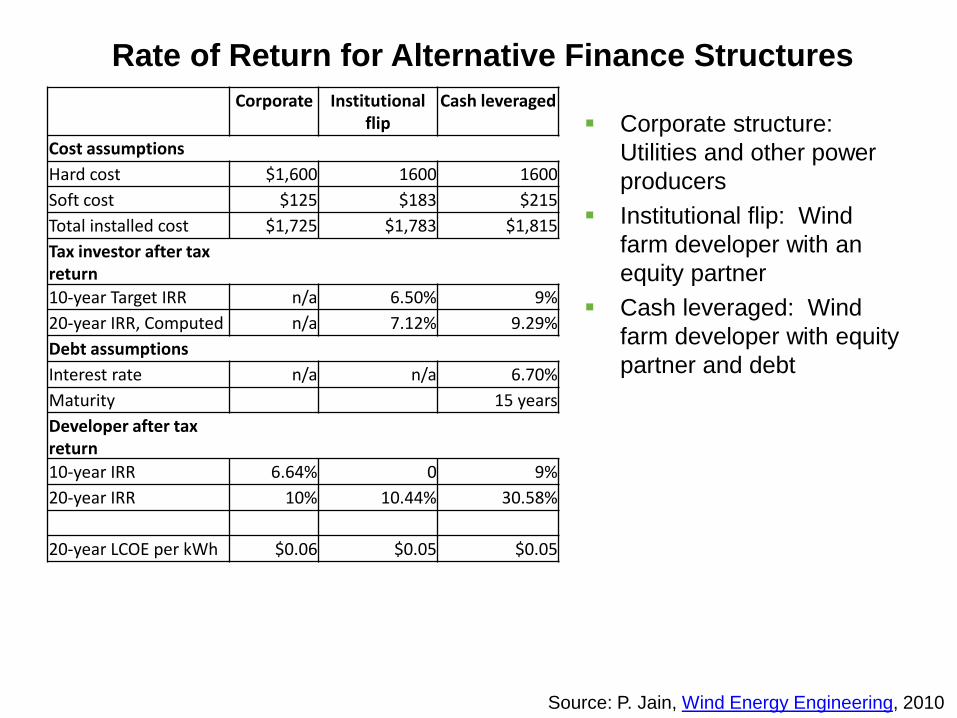

Rate of Return for Alternative Finance Structures

Corporate Institutional flip

Cash leveraged

Cost assumptions

Hard cost $1,600 1600 1600

Soft cost $125 $183 $215

Total installed cost $1,725 $1,783 $1,815

Tax investor after tax return

10-year Target IRR n/a 6.50% 9%

20-year IRR, Computed n/a 7.12% 9.29%

Debt assumptions

Interest rate n/a n/a 6.70%

Maturity 15 years

Developer after tax return

10-year IRR 6.64% 0 9%

20-year IRR 10% 10.44% 30.58%

20-year LCOE per kWh $0.06 $0.05 $0.05

Corporate structure:

Utilities and other power

producers

Institutional flip: Wind

farm developer with an

equity partner

Cash leveraged: Wind

farm developer with equity

partner and debt

Source: P. Jain, Wind Energy Engineering, 2010

Conclusions

Detailed financial analysis requires significant due diligence

Fixed fee construction contracts and third party

maintenance contracts tied to production are strategies to

minimize risk

Wind projects require a framework for risk management for:

• Categorizing risk

• Quantifying risk

• Assessing impact of risk

• Strategies for mitigating risk

Risk management has to be a ongoing task along with

project management