Financial accounting mgt101 power point slides lecture 14

16

Financial Accounting 1 Lecture – 14 09 – Paid to Mr. A Rs. 25,000 through cheque Bank Account Code 02 Date No Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr) Feb 01 Balance B/F 130,000 130,000 Feb 02 01 Cash deposited 25,000 155,000 Feb 05 03 Expenses payable paid 15,000 140,000 Feb 15 08 Fixed deposit placed 75,000 65,000 Feb 17 09 Paid to A 25,000 40,000 Mr. A Code 07 Date No Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr) Feb 01 Balance B/F 15,000 (15,000) Feb 10 06 Credit purchase from B 60,000 (75,000) Feb 17 09 Paid to A 25,000 (50,000)

-

Upload

abdul-wadood-ansary -

Category

Business

-

view

109 -

download

10

Transcript of Financial accounting mgt101 power point slides lecture 14

Financial Accounting

1

Lecture – 14

09 – Paid to Mr. A Rs. 25,000 through cheque

Bank AccountCode 02

Date No Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 130,000 130,000

Feb 02 01 Cash deposited 25,000 155,000

Feb 05 03 Expenses payable paid 15,000 140,000

Feb 15 08 Fixed deposit placed 75,000 65,000

Feb 17 09 Paid to A 25,000 40,000

Mr. ACode 07

Date No Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 15,000 (15,000)

Feb 10 06 Credit purchase from B 60,000 (75,000)

Feb 17 09 Paid to A 25,000 (50,000)

Financial Accounting

2

Lecture – 14

10 – Received cash from Mr. B. Rs. 75,000.

Cash AccountCode 01

Date No. Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 35,000 35,000

Feb 02 01 Cash deposited 25,000 10,000

Feb 06 04 Cash received from B 14,000 24,000

Feb 20 10 Received from B 75,000 99,000

Mr. BCode 09

Date No. Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 15,000 15,000

Feb 06 04 Cash received from B 14,000 1,000

Feb 07 05 Discount given to B 1,000 0

Feb 12 07 Credit sale to B 95,000 95,000

Feb 20 10 Received from B 75,000 20,000

Financial Accounting

3

Lecture – 14

11 – Salaries accrued Rs. 5,000.

SalariesCode 10

Date No. Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 5,000 5,000

Feb 28 11 Salaries Accrued 5,000 10,000

Expenses AccruedCode 12

Date No. Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 20,000 (20,000)

Feb 03 02 Expenses payable reduced 5,000 (15,000)

Feb 05 03 Expenses payable paid 15,000 0

Feb 28 11 Salaries Accrued 5,000 (5,000)

Financial Accounting

4

Lecture – 14

12 – Expenses accrued Rs. 15,000.

Expenses AccruedCode 12

Date No. Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 20,000 (20,000)

Feb 03 02 Expenses payable reduced 5,000 (15,000)

Feb 05 03 Expenses payable paid 15,000 0

Feb 28 11 Salaries Accrued 5,000 (5,000)

Feb 28 12 Expenses accrued 15,000 (20,000)

Expense AccountCode 01

Date No. Narration Dr. Rs. Cr. Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 20,000 20,000

Feb 03 02 Expenses payable reduced 5,000 15,000

Feb 28 12 Expenses accrued 15,000 30,000

Financial Accounting

5

Lecture – 14

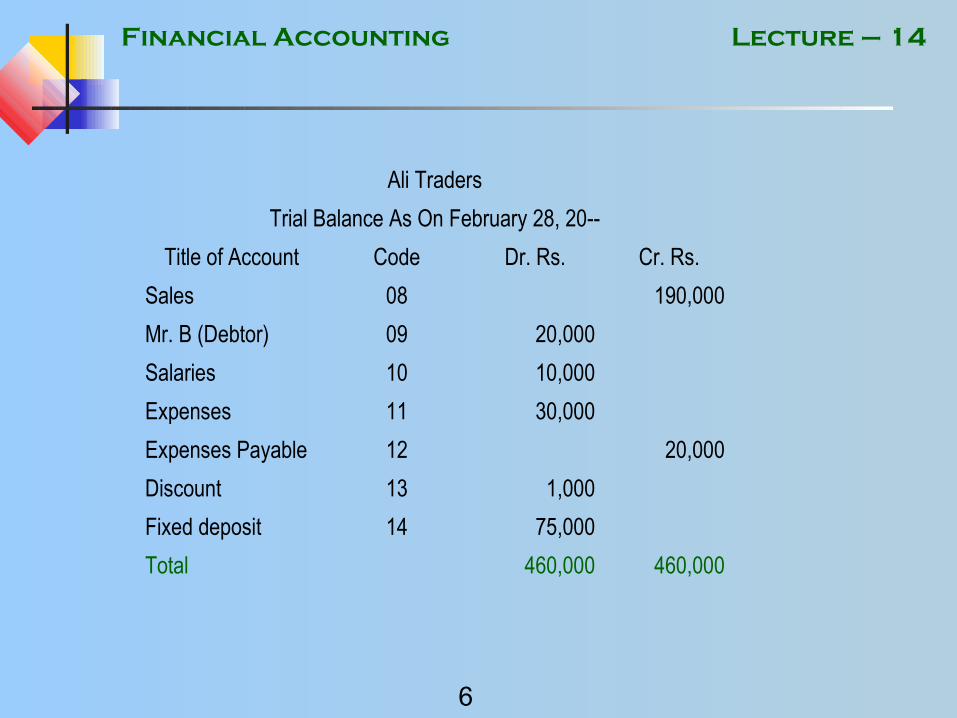

Ali Traders

Trial Balance As On February 28, 20--

Title of Account Code Dr. Rs. Cr. Rs.

Cash Account 01 99,000

Bank Account 02 40,000

Capital Account 03 200,000

Furniture Account 04 15,000

Vehicle Account 05 50,000

Purchases Account 06 120,000

Mr. A (Creditor) 07 50,000

Trial Balance

Financial Accounting

6

Lecture – 14

Ali Traders

Trial Balance As On February 28, 20--

Title of Account Code Dr. Rs. Cr. Rs.

Sales 08 190,000

Mr. B (Debtor) 09 20,000

Salaries 10 10,000

Expenses 11 30,000

Expenses Payable 12 20,000

Discount 13 1,000

Fixed deposit 14 75,000

Total 460,000 460,000

Financial Accounting

7

Lecture – 14

• Items purchased for own use of the business are charged as expense, e.g. tube lights, bulbs, stationery etc.

• Items purchased for the purpose of resale are treated as Purchases.

Financial Accounting

8

Lecture – 14

Stock

• Stock is the quantity of unutilized or unsold goods lying with the organization.

Financial Accounting

9

Lecture – 14

Types of Stock

• In case of Trading Concern (an organization that does not manufacture goods and but resells the purchased goods.) Stock in Trade (Finished goods)

• In case of Manufacturing Concern (an organization that purchases material and converts into a finished product by putting it through a process). Raw Material Stock Work in Process Finished Goods Stock

Financial Accounting

10

Lecture – 14

Stock Account

• Stock Account is Debited with the Value of the Goods Purchased.

• Stock account is Credited with the Purchase Price of the Goods Sold / Issued for Production.

• Stock Account shows the cost / purchase value of unsold goods.

Financial Accounting

11

Lecture – 14

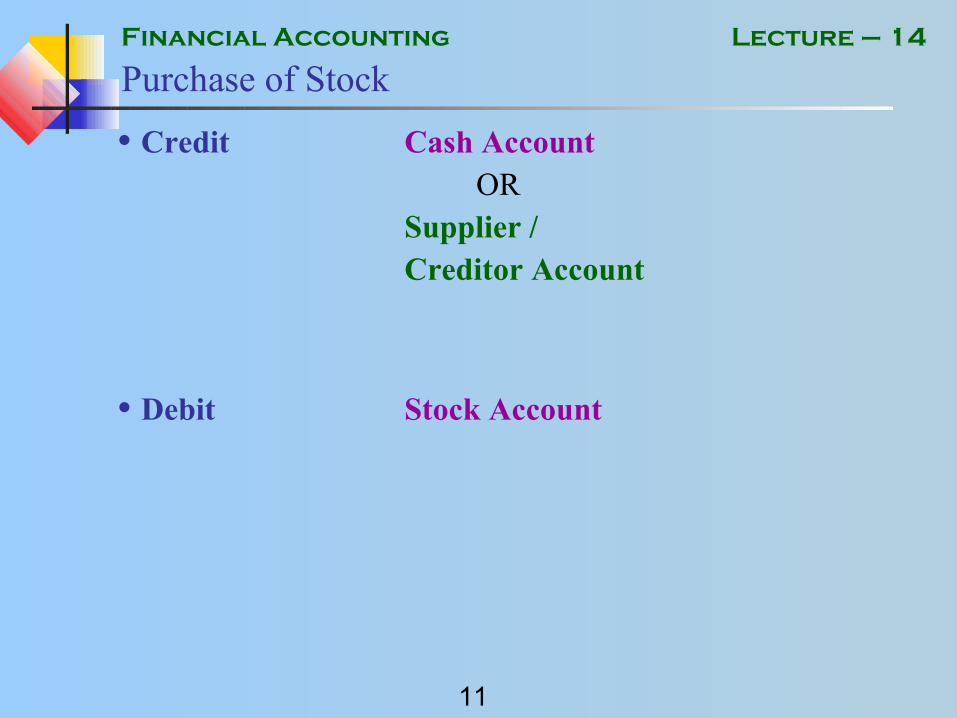

Purchase of Stock

• Credit Cash Account OR

Supplier / Creditor Account

• Debit Stock Account

Financial Accounting

12

Lecture – 14

Payment to Creditors

• Debit Supplier / Creditor Account

• Credit Cash Account

Financial Accounting

13

Lecture – 14

Sale of Goods

• Debit Cost of Goods Sold

• Credit Stock Account

Financial Accounting

14

Lecture – 14

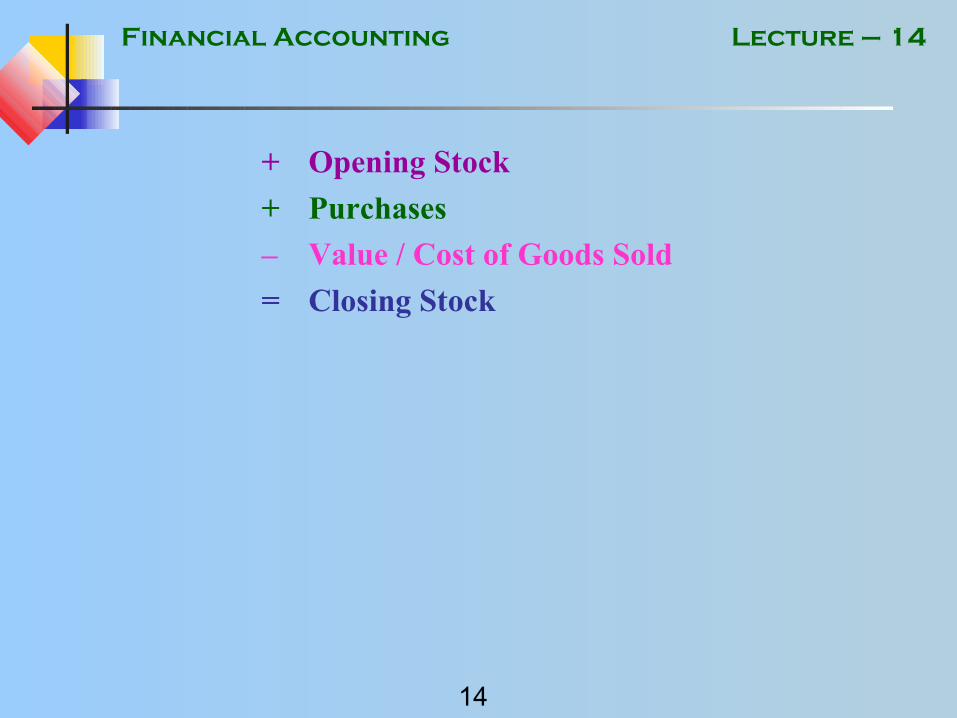

+ Opening Stock

+ Purchases

– Value / Cost of Goods Sold

= Closing Stock

Financial Accounting

15

Lecture – 14

Cost of Goods Sold

• Trading Concern

Purchase Price of the Goods Sold

• Manufacturing Concern

+ Cost of Raw Material Consumed

+ Other Manufacturing Costs e.g. salaries of labour, cost

of machinery

Financial Accounting

16

Lecture – 14

Stock & Cost of Goods Sold In Manufacturing Conc.

Raw Material Stock Other Costs Accounts

Work in Process Account

Finished Goods Account

Cost of Goods Sold Account