Final Thesis - Catherine Mahony (11377841)

75

i An exploratory analysis of the financial performance and characteristics of the grocery retail industry in three major economies between the period 2011-2015. Submitted in partial fulfilment of the requirements of the Masters in International Management, School of Business, Trinity College Dublin. Prepared By: Catherine Mahony (Bachelor of Business Studies) Supervisor: Mr. Gerard McHugh July 2016

-

Upload

katie-mahony -

Category

Documents

-

view

1.170 -

download

3

Transcript of Final Thesis - Catherine Mahony (11377841)

i

An exploratory analysis of the financial performance and

characteristics of the grocery retail industry in three major

economies between the period 2011-2015.

Submitted in partial fulfilment of the requirements of the Masters in International Management,

School of Business, Trinity College Dublin.

Prepared By: Catherine Mahony (Bachelor of Business Studies)

Supervisor: Mr. Gerard McHugh

July 2016

i

I have read the University’s code of practice on plagiarism. I hereby certify this material, which I

now submit for assessment on the programme of study leading to the award of MSc.

(International Management) is entirely my own work and has not been taken from the work of

others, save and to the extent that such work has been cited within the text of my work.

Student ID Number: 11377841

Name of Candidate: Catherine Mahony

Signature of Candidate: Catherine Mahony

Date: 24th July 2016

ii

Abstract

This paper acts as an exploratory analysis in order to gain greater understanding of the financial

performance and characteristics of the grocery retail industry in three major economies for the

period 2011 to 2015. Starting in September, I will begin my career within this industry, to be

specific, in Lidl’s finance and accounting department. Therefore, this dissertation serves the

purpose of a developmental project as well as an interesting investigation. To attain an overview

of the industry, it was important to consider the historical development of the industry from the

year 1912 to the present. The changes in trends, format and structure has led us to the fast-paced,

constantly changing, highly competitive and concentrated grocery retail industry that we know

today. Incumbents in the industry fight hard to maintain market share and increasingly tight

margins, and as such, incumbents are interested in the next wave of development to stay ahead. A

present day competitive analysis of the industry was conducted using Porter’s five forces

framework. This further enhances understanding of the industry, its profitability and where it is

likely to go in the future. High buyer/retailer power is a key characteristic of the industry, as is

high competitive rivalry and a lack of substitutes. Signs indicate that the battle will only intensify

in the future. This was beneficial as it provides a theoretical proxy for what we might expect to

see from the quantitative financial analysis such as tight margins indicative of the industry and the

competitive atmosphere. To add depth to the literature and further enhance understanding of the

industry, a high-level quantitative exploration of the financial performance of three grocery retail

companies in the US, EU and the UK over a five year period using certain financial metrics was

carried out. Using the DuPont analysis as a guide, it was possible to assess the declining returns of

both assets and equity for the industry as a whole which was unsurprisingly due to declining

margins and increased leverage. We can see that margins are small at 2% on average and asset

turnover is high for this industry, these financial observations reiterate the literature based on this

industry’s characteristics. What was surprising was that the large decline in the 2015 figures was

largely impacted by the UK numbers and therefore, a cross-jurisdictional analysis provided

greater depth. Explanations are put forward but are not exhaustive. The aim of the research is to

provide an overview of the industry and its financial performance, and present observations for

the sample data, however, further research is invited that would build on the findings through an

in-depth financial analysis.

iii

Acknowledgements

I would firstly like to thank my supervisor Mr. Gerard McHugh for providing excellent guidance

in terms of the research topic chosen, his constant feedback during regular meetings, and for

providing his much-appreciated expertise in this area of research. I would like to thank my family,

friends and classmates for supporting me throughout the MSc and dissertation preparation.

Finally, the input of various lectures in a myriad of disciplines throughout the year helped shape

this thesis.

iv

TABLE OF CONTENTS

Declaration ………………………………………………………………………………….……..i

Abstract ……………………………………………………………………………………….…..ii

Acknowledgements ………………………………………………………………………..…...…iii

Tables of Contents ….……………….………...……………………………………………..……iv

List of Tables and Figures………………………………………………………………………....vi

1.0 INTRODUCTION…………………………………………………….……………..……..…1

1.1 Rationale for Research…………………………………………………….....………..1

1.2 Literature Focus………………………....……...……………………………..…….…1

1.3 Method, measures and analysis……………………….………………………..……...2

2.0 LITERATURE FOCUS …………………………………………………….………..……....4

2.1 The historical development of the multinational grocery and general

merchandise retailers 1912-2016. ………….…………………………………………....4

2.1.1 The four major eras in grocery retail format………………….…..……......5

2.1.2 The consolidation wave…………....………........…………………….…….7

2.1.3 A fifth era? - The destructive entry of the German discounters………….…7

2.1.4 On the cusp of a new development - A move towards an online-only grocery

market………....……………………....………...……….…………….……..…...8

2.2 A competitive analysis of the grocery retail industry…………………………….10

2.2.1 Threat of new entrants…………...………...……….………….……..……10

2.2.2 Power of suppliers/retailers as buyers..……….………………..…………12

2.2.3 Power of buyers: end-consumers….………………………………….…...14

2.2.4 Power of substitutes.…………………....………………………..………..15

2.2.5 Competitive rivalry……………………....……………………...…………16

3.0 METHODOLOGY…………………………………………………………………………. 20

3.1 Method, measures and rationale………………………………………...…………20

3.2 An introduction to the sample companies chosen for analysis……...........………21

3.2.1 UK-domiciled companies……...…………………...……………...………21

v

3.2.2 US-domiciled companies……………………………………….……….…24

3.2.3 EU-domiciled companies……………………………….…………………27

4.0 FINDINGS AND ANALYSIS……………………………………………………………….31

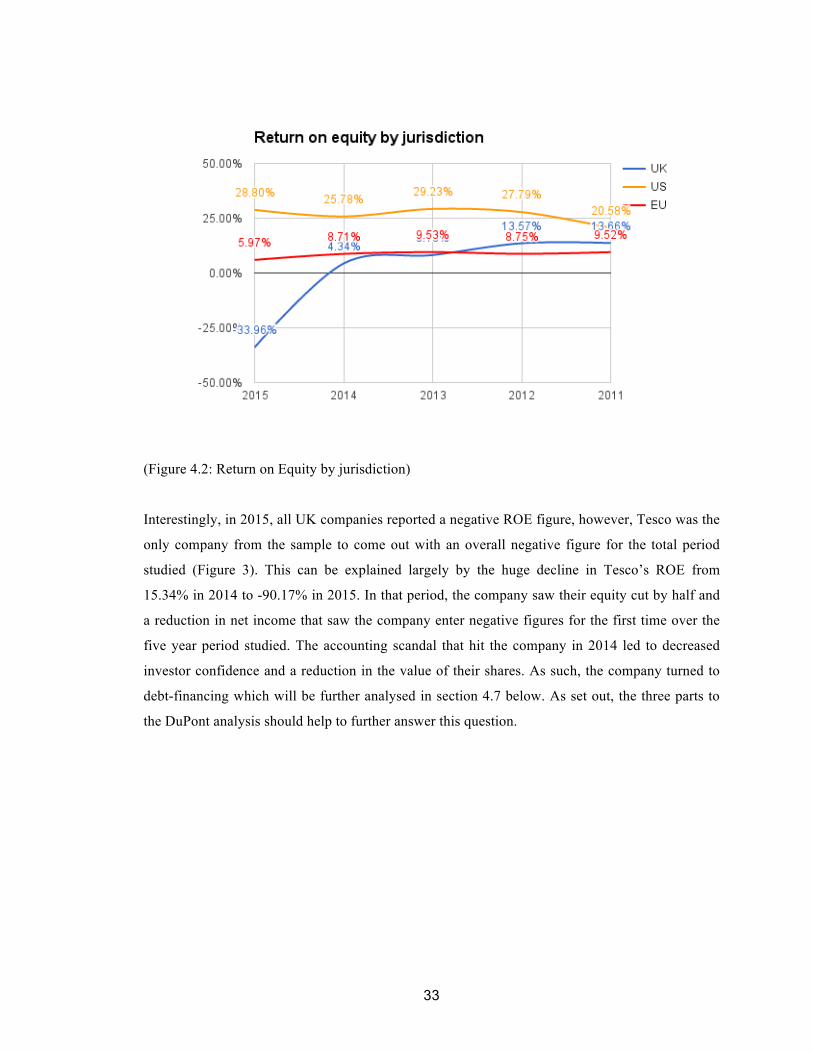

4.1 Return on Equity (ROE) ………………………...…………………………………31

4.2 Return on assets (ROA) ……………………………………………………………34

4.3 DuPont Analysis……………………………………….……………………………36

4.3.1 Gross Profit Percentage………………………………….……………..…36

4.3.2 Net profit margin…………………………………………………….…….40

4.3.3 Asset Turnover………………………………………………….…….……43

4.3.4 Leverage………...………………………………………...…………….…44

5.0 CONCLUSION………………………………………………………………………………48

REFERENCES ………………………………………………………………………….………51

APPENDICES……………………………………………………………………………………64

Appendix 1: Abbreviations…………………………………………...………………………………........64 Appendix 2: Graphical representation of industry averages across all thirteen financial metrics chosen as part of the sample and by jurisdiction averages…………….………………………….…65

vi

List of Tables

Table 1: 3.1: Market capitalisation (2016 approx.), profitability (2015) and turnover (2015) for

each company chosen for sample

Table 2: 4.1: A summary of the findings from the DuPont analysis

List of Figures

Figure 1: 2.1: The evolution of the grocery retail industry

Figure 2: 2.2: The Largest Contributors to Grocery Sales Growth 2015-2020

Figure 3: 2.3: A five forces analysis of the grocery retail industry

Figure 4: 3.1: Great Britain Grocery Market Share 2016. Kantarworldpanel.com, 2016)

Figure 5: 4.1: Return on equity for industry sample

Figure 6: 4.2: Return on Equity by jurisdiction

Figure 7: 4.3: Average ROE by company

Figure 8: 4.4: Return on assets for industry sample

Figure 9: 4.5: Return on assets by jurisdiction

Figure 10: 4.6: Gross Profit Percentage for industry sample

Figure 11: 4.7: Revenue growth for industry sample

Figure 12: 4.8: Gross Profit percentage by jurisdiction

Figure 13: 4.9: Net Profit Margin for industry sample

Figure 14: 4.10: Net profit margin by jurisdiction

Figure 15: 4.11: Represents an increase in Tesco’s cost of sales and finance costs, and a reduction

in revenue. Thus, affecting profit margins

Figure 16: 4.12. Asset Turnover for industry sample

Figure 17: 4.13: Leverage for the industry sample has increased

Figure 18: 4.14: Leverage by jurisdiction

Figure 19: 4.15: UK leverage including all companies over a five year period. In 2015, all UK-

domiciled companies increased leverage, especially Tesco

1

INTRODUCTION

1.1 Rationale for research

The aim of this paper is to gain greater understanding of the financial performance and

characteristics of the grocery retail industry in three major economies for the period between 2011

and 2015. There are three main motivations behind choosing the outlined topic. Perhaps the most

pertinent and arguably, the most important reason is my general and professional interest in the

areas of finance and accounting. I am interested in this particular industry as I will begin my

career with Lidl in September. Conducting research on the retail grocery industry in three of the

main economies will give me a greater understanding of the competitive landscape of the industry

as a whole before entering it. Having a base knowledge of the industry will hopefully allow me to

further my career with the company. Therefore, this dissertation not only acts as an interesting

investigation, but also as a developmental project. As a result, I chose to conduct an exploratory

analysis in order to understand the industry, its characteristics and its financial performance.

Through the literature we know that the industry is fast-paced, constantly changing, highly

competitive and concentrated. A brief overview of a range of financial metrics for the industry

sample gives greater insight into financial performance and a cross-jurisdictional analysis allows

us to spot any interesting similarities and/or differences between different economies.

1.2 Literature focus

To ensure a full understanding of the grocery retail industry, I will present a brief history of the

industry from the year 1912 to the present day. We have seen a massive increase in scale and

scope due to the ‘consolidation wave’, increased internationalisation, lower prices with the

emergence of discounters, decreased supplier power and constantly changing consumer shopping

preferences. For the purpose of later analysis, the focus is on three of the major economies, the

United States (US), the European Union (EU) and the United Kingdom (UK) and as a sample are

considered to be indicative of the wider industry as a whole. In an industry characterised by low

growth, tight margins and fierce competition, the incumbents are constantly searching for new

ways of selling things and new models of efficiency. Hence why we have seen changes in store

formats and the expansions of many major players overseas in search of greater growth

opportunities as mature markets fail to supply sufficient returns. I would argue that we are at the

2

cusp of a new change within the industry and in light of this, it is important to gain a greater

understanding of where the industry has come from to get to where it is today.

A present competitive analysis of the grocery retail industry further enhances understanding of the

industry. To do this I will use Porter’s five forces framework as my tool of analysis. Porter (2008)

set out to explain two things with this framework. Firstly, why profitability in one industry

differed to that of another. We know this to be the result of the ‘risk and return’ phenomenon.

Whereby, margins in the oil extraction industry are much greater than that in the grocery industry

due to the challenges and risks involved. Ultimately, grocery retailers take on very little risk when

disseminating commodities around the world, therefore, the margins for the incumbents come out

to about 2%. Secondly, Porter (2008) tries to explain using his framework, where the industry is

likely to go in the future. Competitive rivalry within the grocery retail industry is high and there is

nothing on the horizon to say that the industry is going to become any less competitive in the

future. In fact, it could get worse as those few companies that dominate in each economy become

even more entrenched in battle. The purpose of these two chapters is to gain greater understanding

of the grocery retail industry, how it has evolved and its competitive nature. The literature also

indicates what we might expect from an analysis of the industry’s financial performance such as

tight margins, high asset turnover etc.

1.3 Methodology, measures and analysis

Within the methodology section, I will present a brief introduction to each of the nine companies

chosen for my research as well as a brief outline of the steps taken during the quantitative

exploration of the grocery retail industry’s financial performance. I have limited the sample to

three companies from each of the three main economies, the EU, US, UK. The top three chosen

are representative of between 45%-55% of the total grocery market and in the top four in terms of

sales in their respective jurisdictions and therefore, are considered to be representative of the

industry as a whole. My method of investigation used for this dissertation is primary research.

Data gathered from the annual reports of the sample group from the period between 2011 and

2015 were presented in excel under the three main financial statements. From this it was possible

to put together a range of financial metrics and industry averages. Gathering the information first

hand constituted as a proactive approach that allowed for greater analysis, understanding and

personal development. Initially, a total of eleven financial metrics were chosen for analysis which

included:

3

I. Revenue growth

II. Return on assets

III. Return on equity

IV. Net profit margin

V. Gross profit Percentage

VI. Leverage

VII. Asset turnover

VIII. Borrowing/ Borrowings + Equity

IX. Liabilities/ Liabilities +Equity

X. Cash flow/ Net income

XI. Receivable collection period

From this list, the most meaningful measures were chosen and presented as part of the findings

and analysis section. The high level financial analysis conducted adds depth to the literature, not

only exemplifying an extremely competitive industry, but also how different jurisdictions operate

similarly or differently. The decreasing trends in the industry proved to be an interesting topic to

explore further and thus, a DuPont analysis was chosen to do so. This section offers broad

industry trends that supports the literature, as well as economy-specific findings, and in some

cases, company-specific effects on the overall results. The aim of this paper is to provide an

overview of the grocery retail industry, its performance and and its characteristics that provides

understanding as someone entering the industry and opens up a pathway for further investigation

and analysis.

4

2.0 LITERATURE FOCUS

2.1 The historical development of the multinational grocery and general merchandise

retailers 1912-2016.

Many of the major players in the grocery retail industry today thread the line between department

store and grocery store due to their size and range of goods and services offered wherein, food is

only one segment of their operations. For the purpose of this paper, the focus will be on large

grocery retailers that sell food and other unrelated goods, often referred to as one-stop-shops. This

definition yields a market we refer to as “big-box” grocery retailers consisting of various different

retail formats from traditional supermarkets to supercenters, and the recent introduction of the

German discounters.

The aim of this chapter is to highlight important historical trends that occurred within this

industry and were pivotal in its evolution to the competitive battlefield that it is today. Explosive

growth has been a result of the introduction of different formats and grocery retail concepts which

have altered the basis of competition over the years.

2.1.1 The four major eras in grocery retail format

According to Ellickson (2015), there have been four major eras in the evolution of the grocery

retail industry with the first being the localised chain store revolution led by the Great Atlantic

and Pacific Tea Company (A&P) which introduced the idea of the ‘economy’ grocery store back

in 1912. Prior to major grocery stores, meat was bought from the butchers and bread was bought

from the baker. Time conscious consumers longed for an efficient system that hailed a ‘one-stop-

shop’. When A&P set up the first economy store format, the features of standardisation and scale

came into play in the industry. A more straight forward logistics and supply chain system meant

cost savings from the company which was then passed on to the consumers. Furthermore, they

pioneered the idea of backward integration in the industry by owning their own network of

5

warehouses and delivery trucks, which is a feature of most the major supermarkets today. The

main economies were at the level of the supply chain and innovations in delivery of products,

rather than at the store-format level. Kroger was one of the major American stores to adopt this

‘cash and carry’ business model in its early stages. By the 1930’s, the profits of these chains

began to diminish as competition between them stiffened and an anti-chain ethos began to cripple

their ability to prosper (Ellickson, 2015). The anti-chain ethos was initiated by a wealthy

businessman, W.K. Henderson, who owned a radio station through which he popularised the anti-

chain store revolution (Mattera, 2005). A myriad of newspapers and radio stations followed suit

throughout the world and anti-chain groups turned to government in order to battle these large

chains (Mattera, 2005). The characteristics of the industry now pushed for a move from a

localised outlook to a regional one.

Then came the next major wave in the industry with the birth of the supermarket format which

gave way to economies of scale and scope unheard of 50 years earlier. A traditional supermarket

is defined as a self-service retailer selling a full line of food products, including grocery, meat,

and produce (Alexander et al, 2008). The major difference between these super stores and the

chain stores was the reliance on heavy advertising. This new breed of store was proposed by a

Kroger employee named Michael Cullen who envisioned a strategy based on low margins and

low expenses that would be made up by the difference in volume. Even A&P converted format in

order to target the less price conscious consumer and in keeping with this new breed of

consumers, services were added (Basker, 2016). Scale and scope economies were happening at

the store level as opposed to the distribution level (Ellickson, 2015). Up until the 1970’s,

supermarkets dominated the retail landscape in all the major economies notably the US, EU and

the UK. The post-war period was a period of boom for these supermarkets however, after some

time, again, the markets became saturated leaving these supermarkets in search of new avenues

for growth - namely, acquisition-led growth (Basker, 2016).

The third major milestone came in the 70’s wherein supermarkets considered new formats as the

market became saturated and recession influenced buying patterns (Basker, 2016). Thus, club

stores were born, which were retail stores that sold a variety of merchandise, and not exclusively

food items. This format of store was pioneered by Price Club in 1976 (Datamonitor, 2010).

Groceries is the most competitive segment of the retailing market, hence, why many decide to

expand their offerings to make up for the very tight margins afforded in the grocery market

(Steffy, 2016). A key characteristic of these stores is that they sold in bulk. At this time, we were

6

witnessing computerisation, otherwise known as the ‘information age’ and scanning registers

were introduced in stores (Ellickson, 2015). Stores became larger as it became possible to hold

more products and therefore, inventory management systems and logistics gained greater traction

and became a point of differentiation for many (Basker, 2016).

From 1988 onwards, we saw the introduction of the supercenters which were an important and

rapidly growing big-box grocery retail format. Supercenters are typically larger than 180,000

square feet, combining both a large supermarket and a large mass-merchandiser within the same

store (Hanner et al, 2015). There was a supercentre boom between 2000 and 2014. In the US

alone, between 1992 and 2013, supercenters saw a 10.5-fold increase in sales, while traditional

department stores revenues fell by roughly 20% (Hortacsu & Syverson, 2015).. Therefore, the

industry has seen a major shift in the way that stores selling multiple varieties of merchandise

operate, with a shift from the traditional service-oriented department store toward a lower-cost

model that in some ways borrows the logistics techniques of the wholesale sector (Hortacsu &

Syverson, 2015). According to Hanner et al’s (2015) research, during the period between 2004

and 2009, the number of supercenters increased by 53%, while during that same period, the

revenue of supermarkets declined by almost 10%. This is exemplary of the change in composition

of grocery retail outlets.

The fourth and final stage according to Ellickson (2015) came when firms like Walmart formed

the first truly multinational chain stores, in light of the globalisation era. The common thread

throughout the industry’s evolution is the push for greater variety at the lowest possible prices.

Expansion, expansion, expansion. The expansion of variety and store size was the trend for many

years, however, we began to see geographic expansion at an unprecedented rate in the 1990’s

which has continued today to form grocery retailers that operate globally (Dries et al, 2004). We

now see a highly competitive, concentrated and dynamic industry characterised by scale and

constant price reductions (Smith, 2006). Important to note here is that the sequence of

development is the same in Europe and the UK however, they happened slightly later. Another

important point to make is that these stages are characterised by a dominant model but does not

mean that previous models become extinct.

7

2.1.2 The consolidation wave

Competition in the food retail market is intense and due to the evolution of different store formats,

traditional grocery retailers are feeling the pressure. Due to this competition and changing

consumer preferences, many firms in the industry are considering their strategic moves with

M&A being a popular strategy adopted for a myriad of purposes including entry into new

markets, leveraging sourcing capabilities and in order to manufacture greater earnings growth.

Thus, there has been a wave of consolidation in the industry over the past 10+ years that has

changed the industry forever (Duff & Phelps, 2016). As the industry faced a more value-

conscious consumer post-recession, cost reduction was on the fore-front of all the leading grocers’

mindset and subsequently led to increased consolidation. According to Aufreiter et al (1999)

much of the consolidation was infact driven by a need to ‘nourish the corporate ego’ and

following the mantra of ‘bigger means better’. The leading players in the industry had an appetite

for scale, and M&A was the avenue through which to achieve economies of scale for these cost-

focused firms in a hugely competitive industry (Blackbook, 2009). Although M&A activity may

seem attractive to many firms, this activity leaves the industry exposed to antitrust enforcement as

the Federal Trade commision and the European Commision address any anti-competitive

behaviour. The industry has become increasingly concentrated over the years and various

enforcement agencies must monitor collusion and the formation of superpowers that will put

smaller retailers and consumers at a disadvantage (Corstjens & Vanderheyden, 2010). In mature

markets such as the US, Europe and the UK, where the grocery retail market is highly centralised,

M&A transactions are likely to face limitations and restrictions (Blackbook, 2009). We are now

experiencing a complete turnaround whereby firms are scaling back from the trend of the mega

mergers that existed from the late 1990’s onwards largely due to more stringent authority

oversight as well as the emergence of a new store format (McTaggart, 2012).

2.1.3 A fifth era? - The destructive entry of the German discounters

It is no surprise that the global economic crisis that occurred in the late 2000’s impacted retail

commerce, and grocery retail was no exception. Buying behaviour changed as consumers sought

good quality, ethical business practises, simplicity and fair prices (Stefanska & Bilinska-

Reformat, 2015). The aggressive discount grocery store concept or format was formed in the 60’s

in Germany but flourished in Europe at a time when disposable income eroded considerably

(Wortmann, 2004). The discount, no frills approach adopted by German retailers was popularised

8

by firms such as Aldi and Lidl who became vastly popular in Western countries as they ramped

up store openings and saw double digit sales growth at the time of the recession (Shah, 2014). The

destructive arrival of these hard-discounters altered the dynamics of the industry significantly.

The success of this new format has become a major source of concern for traditional supermarkets

and supercentres, leading to reduced sales increases and in some cases, the demise of the entire

business. The German discounters offer a simple store format, with minimum product variations

and average quality products at rock-bottom prices which suited the position of their target

consumers who are now rejecting the ‘big weekly shop’ model that was popular for many years

(Wortmann, 2004). In Ireland, German retailers are increasing their market share faster than any

of the other major competitors. According to figures released by retail analysts, Kantar

WorldPanel, the German retailers have a combined market share in Ireland of 22%, in touching

distance of the market leader Supervalu which has a market share of 23% (Pope, 2016). Lidl and

Aldi are a ‘market share-grabbing nightmare’ for grocery retailers in Europe as a whole. In 2014,

the two combined managed to command 10% of the very competitive grocery market in the UK

(Souza, 2016), while in the same period, the UK’s biggest supermarket, Tesco, saw its market

share fall to a 10-year low (Salmon, 2015). The US market are also under threat with Aldi already

breaking into the market and a well-publicised large scale expansion happening for Lidl in the

next few years (Souza, 2016). For many years we saw the rise of supercenters and greater product

variety, now we are seeing a drawback from that. The on-going internationalisation plans set out

by these firms indicates that they remain confident that this new format will play a major role in

the industry for the foreseeable future (mass grocery retail, 2009). What is interesting to note is

that speculators find that these German discounters are likely to absorb the rise in food prices and

inflation post-brexit decision because they have the leanest supply chain in retail and sufficient

economies of scale (Williem de Jongste, 2016).

2.1.4 On the cusp of a new development - A move towards an online-only grocery market

While different store formats and the internationalisation of grocery retailers have impacted the

industry, so too have major trends such as access to technology. Technology has always, and will

always continue to be a force shaping the structure of the grocery retail industry from the

beginning of the barcode, to self-service checkouts and now the emergence of online shopping.

With many of the former giants and winners in the industry struggling to continue business and

some experiencing fatal blows, some commentators argue that the decline of these former giants

is due to the prediction that sales will move fully online and physical stores will become

9

completely outdated. E-commerce has been given considerable attention since the boom and

subsequent bust of the ‘dotcom bubble’ (Hortacsu & Syverson, 2015) and the idea of online-only

shopping has created a buzz within the industry (Duff & Phelps, 2016). Digital is considered the

best way to communicate effectively with consumers. The ‘death of retail’ has yet to be fully

realised in the grocery retail industry but is a constant point of conversation and worry for the

stores themselves as they try to expand and create an effective online platform. E-commerce will

continue to be a force shaping the industry well into the future as consumer demand for online

grocery sales has increased drastically over the last number of years. A handful of firms have

entered the online-only grocery business including Groceryworks.com and Instacart (Duff &

Phelps, 2016). According to Hortacsu & Syverson (2015), grocery retailers are unlikely to meet

their demise any time soon but will rather evolve into a hybrid organisation that combines

physical stores with an online platform. All of the major grocery retailers in the sample chosen for

this dissertation have made considerable investments in developing their online presence and

continue to do so as they see its future in the industry to be of paramount importance. To this date,

the changes in format over the years has had a bigger impact on the makeup of the industry than

e-commerce has. Shopping tends to be a social process and therefore, the demise of physical

formats is uncertain (Hortacsu & Syverson, 2015).

A summary of the grocery retail industry’s evolution is presented in figure 1 below.

10

(Figure 2.1 The evolution of the grocery retail industry)

Through an understanding of the evolution and expansion of the industry over the past 100 years,

it is possible to see how the industry has grown to what it is today which is an intensely

competitive sector. A review of the industry shows how fast paced the industry is and unforgiving

to those unwilling to change with shopper preferences. Incumbents in the industry try to anticipate

the next step and change in the structure of the industry in order to stay one step ahead of

competitors, hence why data analytics and reward schemes have been beneficial to these retailers.

As such, it is important to present a competitive analysis of the industry.

2.2 A competitive analysis of the grocery retail industry

To conduct a competitive analysis of the grocery retail industry, I have chosen to use Porter's five

forces framework. This industry analysis model allows us to analyse the profitability of the

industry and where it is likely to go in the future (Porter, 2008).

2.2.1 Threat of new entrants

The threat of new entrants into the grocery retail industry is low due to the fact that the industry

has transformed over the years into a concentrated, supercentre-dominated business. One trend

that has become abundantly clear through the decades of evolution in the industry is the

decreasing number of independent retailers. The large incumbents have established an intricate

supply chain system, they have invested heavily in marketing and have large scale operations in

place that are not easily replicated by new, much smaller entrants. It is clear that the entry and exit

of firms into a specific industry plays an important role in stimulating economic growth, as well

as influencing the competitive process of that industry in the long run (Hanner et al, 2015).

Hanner et al (2015) found that new firm entrants into the industry are unlikely to gain substantial

market share despite the fact that it is relatively easy to enter this market. The fierce competition

and dominance of the major players make it extremely difficult for these firms to do well.

Between their sample period, 2004-2009, they found that new entrants capture less that 5% of the

US market's revenue share (Hanner et al, 2015). What is more, due to the fierce competition and

the never ending price cutting, margins in this industry are low and unattractive for new entrants.

11

Market growth is put down to market expansion by incumbent brands rather than the entry of new

ones (Igami, 2011). Due to stiff competition, incumbents are increasingly looking to further

geographic markets in search of growth. According to IGD’s 2016 forecasts the value of the

global grocery market is likely to see an increase of about a third over the next five years. This is

in large part due to the increasing prosperity of lower-middle income markets. Since 2010,

grocery sales in low income economies have grown by 70%, and are expected to double by 2020

(IGD.com, 2016). The expected growth in these markets is why threat of entry from these mature

market giants into emerging and low income economies is likely to be high. According to the

world bank, countries such as India, China and the US, are likely to contribute considerably to

grocery sales over the next few years (Figure 2). Tesco and Wal mart have both failed to

successfully launch their stores in China, a market that clearly represents huge potential, and

companies domiciled in the EU and UK have found it difficult to penetrate the US market due to

intense competition from incumbent players. Therefore, although entry is desired due to the size

and future potential of the market, it is not without difficulty and entry modes will need to be

reconsidered.

From the point of view of the handful of large retailers that dominate certain mature markets, as

they enter into untapped territory, evidence shows that they impact significantly on the survival of

these smaller retailers, forcing price reductions and improved efficiency. Anti-competition

regulators are under pressure to protect these smaller firms as many criticise that the big stores are

driving out the smaller ones (Igami, 2011). Borraz et al (2014) had similar findings through the

various empirical studies that they conducted, stating that the introduction of supercenters in a

particular area drastically increases the likelihood of the smaller retailers going out of business in

that area. If independent retailers manage to spot a niche in the market, it is likely that they will

only be granted a short time to flourish until the conventional giants overshadow their vision

using their robust supply chain capabilities (Duff & Phelps, 2016).

12

(Figure 2.2: The Largest Contributors to Grocery Sales Growth 2015-2020. The World Bank, IGD

Research, 2015)

In conclusion, for independent, small-scale retailers, entering the market is relatively easy

however, scale poses as a major barrier and the structure of the industry makes it unattractive for

any firms hoping to enter, thus, profitability is likely to be high in the industry.

2.2.2 Power of suppliers/retailers as buyers

Buyer power of the major supermarket chains over suppliers is substantial leaving the suppliers

with low supplier power. As previously mentioned, the industry is highly concentrated and market

concentration usually equates to market power (Burt & Sparks, 2003). The fear now is that these

retailers have too much power in the market that is being exploited at the expense of the suppliers.

The level of power that these retailers have depends on their relationship with their supplier which

Dobson & Chakraborty (2008) argue is based on bilateral bargaining as opposed to a situation

whereby the retailers would pay their suppliers a ‘market price’ for a product. Important factors

that also need to be considered is relative size and the availability of substitute suppliers. As a

result of the highly concentrated industry in many of the mature markets, the leading retailers

have market share that is significant enough to allow them to dominate their relationships with

their suppliers as they occupy the role of the ‘critical customer’ (Dobson & Chakraborty, 2008).

When suppliers are economically dependent on these retailers whereby a loss of their business

13

could have catastrophic implications for their bottom line, these suppliers are left with very little

bargaining power or they run the risk of having their contracts terminated. These grocery retailers

typically stock a wide variety of product lines, especially since the introduction of supercentres,

thus, the loss of one product line is unlikely to impact them (Smith, 2006). Retailers tend to stay

away from long-term contracts and maintain relationships with a wide range of suppliers to ensure

an agile supply chain and ease of switching (Marketline.com, 2013). Another feature of the

present day grocery market is the rise of private-label goods which extends producer substitution

by devaluing the supplier's particular product and assists these leading retailers in their ability to

exercise considerable buyer power over suppliers (Smith, 2006). If it is a case whereby a

particular supplier offers superior services in terms of efficiency or quality, or customers are

particularly loyal to a particular brand, then the supplier would hold power of their own.

However, this is documented by many as an unlikely scenario in this particular industry.

Furthermore, the pressure that these firms are under due to the level of competitive intensity in the

industry to keep their costs at a minimum means that they will start cutting costs in areas that they

have control over, notably, their suppliers. As part of the consolidation phenomenon, many of

these large retailers participated in backwards integration in order to scale up and capture the

profit being made by these suppliers, as was necessary given the cost structure of the industry

(Smith, 2006). These conditions put the large chains in an advantageous position to negotiate rock

bottom prices and is one way in which they can exercise their buyer power. The substantial power

that rests in the hands of the retailers can be good news for consumers as price reductions are

passed on to them and increased supplier competition is likely to lead to improved quality and

efficiency (Hattersley et al, 2013). However, the pressure placed on suppliers to the grocery retail

industry to keep costs low can also lead to ‘suppression of investment’ whereby shortcuts are

taken so that these suppliers can operate at such a low cost (Dobson & Chakraborty, 2008). Sotgiu

and Gielens (2015) noted that while it is unlikely, retailer-initiated price cuts can benefit certain

supplier brands as demand can increase substantially. This was the case in 2010 when Walmart

initiated a ‘soda war’ by reducing the preferred manufacturer price of various brands such as

Coca-Cola and Pepsi, forcing competitors to follow suit. Demand was so strong for these brands

that the suppliers could barely keep up supply. The power imbalance has shed light on supplier

welfare, as many feel they are being squeezed too far by the large giants (Bloom & Perry, 2015).

The fear going forward and a basis of further contemplation for competition authorities is the

increasing buyer power of these large retailers that dominate the market in the major economies

that leads to further consolidation and a subsequent reduction in smaller retailers (Dobson &

14

Chakraborty, 2008). As a result of exploitation concerns that proliferate the global grocery retail

industry, many governments have been called to bring about more stringent regulatory

frameworks that monitors the supplier-supercentre relationship leading to a myriad of formal

investigations into the abuse of power. This means a move away from self-regulated markets that

assume perfect competition (Burch et al, 2013). Many retailers have a CSR initiative that will

outline how well they treat their suppliers as a way to increase their consumer loyalty and

credibility amongst fierce competition in the face of changing market conditions, as opposed to a

dislike for exerting power over suppliers. Power has inevitably become highly centralised in the

hands of the dominant retailers who have the ability to take advantage of this self-regulatory

environment at the expense of the independent grocery brands (Burch et al, 2013). In this case,

low supplier power enhances profitability for the retailers in the industry.

2.2.3 Power of buyers: end-consumers

Individually, customers that shop in these supermarkets tend to have virtually no bargaining

power. If we focus solely on grocery purchases, the proportion of consumers’ total income that is

spent on them is sizeable. Based on 2014 data, in the US, households spend 6.5% of their total

income on food, while in the UK, 8.7% is spent on food, and in various other countries in Europe

such as Germany, Italy and France grocery expenditure accounts for over 10% of their annual

income (bls.gov.uk, 2015). Presently, just four nationally operating supermarket chains control 75

percent of all sales in the United Kingdom. This is not only the case in the UK, but the US also,

whereby a small number of large firms dominate the entire market (Plumer, 2015). This level of

concentration, in large part as a result of the ‘consolidation wave’, has implications for consumers

as mentioned above. Consumers have low switching costs as they fluidly move from one retailer

to another. Loyalty is a problem area for these large retailers and some try to retain consumers

through reward-schemes and other initiatives. Most of the large retailers will compete on price,

attempting to constantly undercut each other, but finding new points of differentiation becomes

increasingly important to keep consumers shopping with them. Bargaining power in this industry

is low because there is little the customer can do to alter the selling patterns of a grocery store,

and the revenue provided by a particular consumer is minimal for these retailers

(Marketline.com2013). However, it is important to note that while this is the case for an

individual consumer, the consumer base as a whole has the ability to drive trends and demand

higher quality and/or lower prices (Briggs & Goldman, 2006). As customer preferences

amalgamate, retailers must tap into that in order to stay ahead of the competition. This is why

15

access to big data is big business in this industry as failure to notice trends quickly is not tolerated

in this sector. Due to low-moderate buyer power, profitability improves for the incumbent

retailers.

2.2.4 Power of substitutes

If we consider a substitute to be something that is outside the industry, there are very few real

substitutes for grocery stores. As economies have become richer, we have seen a shift towards

eating out in restaurants which acts as a potential substitute for this industry. The 2015 census

bureau report showed that, in the US, consumer spend on eating out in restaurants and bars

overtook grocery sales for the first time ever showing a shift in consumer eating habits (Jamrisko,

2015). Likewise, in the UK and Europe, the casual dining sector is booming as consumers look

for efficiency and affordability. Furthermore, economic conditions and consumer preferences are

likely to be favourable for the restaurant sector into the future according to Ernst & Young’s

Restaurant and Casual Dining Insight Report 2014 (Gerrard & Cartmell, 2014). However, despite

this trend, the threat is quite weak. Restaurants and takeaways tend to be considered as an

accompaniment rather than a total alternative (Marketline.com, 2013).

The superstores we see today are offering a greater variety of goods and services that are not

solely focused on food items. If we consider the fact that you can buy a TV in Tesco, it begs the

question of whether home stores such as Harvey Norman act as substitute stores or just as a niche

version of that. One might argue that smaller convenience stores act as a substitute however, there

are two arguments in the way that would consider this to be a very weak substitute. Firstly, most

of the large supercentre stores have entered the convenience store realm of business. Secondly, it

can also be described as just another segment of the same industry, another format that has

evolved in the evolution process. A possible alternative for this industry that could cause a major

threat in the future is subsistence agriculture whereby individuals farm their own produce.

Currently, this is an uncommon practise in today’s world due to a lack of land space, access to

machinery, and high costs in terms of money and time. However with the ever-growing number

of health conscious consumers, this could pose significant substitution concerns for the future

(Marketline.com, 2013).

16

2.2.5 Competitive rivalry

Grocery retailers face stiff competition with each store fighting intensely for market share. In

order to avoid the cut-throat price competition, they have tried to expand their goods and services

range in order to gain loyalty in an industry that has seen a steady decline in the ability to create a

loyal consumer base.

The patterns of evolution explained above have been accompanied by a number of changes in the

structure of the market. Firstly, scale and scope dynamics have played a major role in driving

competitive structure in this industry. The scale of operations in grocery retail has increased

dramatically over the years, especially since the emergence of supercenters and warehouse clubs

(Ellickson, 2015). Economies of scale and scope in logistics, procurement and other operations is

of paramount importance due to the highly competitive nature of the industry and the pressure to

keep costs at an absolute minimum.

It is a common realisation that the sector is oligopolistic in structure. The ‘circle of growth’ is

driven by scale whereby increased scale leads to greater efficiencies, increased sales and market

share, which leads to greater investment ie expansions and so on and so forth. As this continues it

acts as a serious barrier to entry (Burt & Sparks, 2003). Ellickson (2013) examines the role of

investment in determining the equilibrium structure of the supermarket industry. Rather than

inviting more players into the market, larger markets encourage additional sunk investment by the

players already incumbent in the market, thus, limiting the number of firms that can profitably

enter these large markets. This model is relevant to the grocery competition discussion due to the

fact that geographic markets in the US, UK and Europe are consistently dominated by a small

number of major chains rather than just one chain who has the monopoly advantage, making the

competition in this industry more complicated. He looks at the outcome of this investment as a

way to consistently increase product variety and the one-stop-shop idea, which has become the

strategic focus of the industry and the basis of competition. Ellickson (2013) concludes that the

main incumbents in the industry form a natural oligopoly through increasing the size of their

stores and operations in order to compete head to head with other rivals, thus, making it very

difficult for smaller firms to compete. Dobson, Waterson and Chu (1998) observe essentially the

same pattern. Growth and market concentration at a national level increases organizational scale,

which provides lower unit costs through greater buying power. As a consequence sales and profits

increase, providing the capital and scope to invest in attractive customer facilities or in price

17

reductions. The potential arises for what Dobson, Waterson and Chu (1998) term a 'virtuous

circle' of growth dominated by one or two organizations, whose lower unit costs enable them to

assume market leadership. Smaller retailers find it hard to compete as they have to match prices

but with a higher cost margin thus, causing a huge number of exits from the market and a reduced

number of entrants. Hanner et al (2015) builds on these findings by giving empirical evidence of

how the set of important players in the industry rarely changes over the intermediate run.

As firms have become larger, the industry has become more concentrated, another element of the

change in market structure over the years. This concentration happened at a regional level up until

the 80’s (ellickson, 2015). With this comes questions of market power abuse on the part of the

incumbent grocery retailers (Basker, 2016). The very forces that contributed to the construction of

the oligopolistic market that we see today could lead to a strengthening of one or two

organisations and thus, a duopolistic market if authorities do not take this threat seriously.

Cotterill (1986) found that grocery prices tended to rise with increased retailer concentration. This

concentration of retailers acts as a significant barrier to entry and raises concerns over the

diminishing supplier power in the industry.

Various trends, changes in consumer preferences and shifts in store concepts including the

increasing popularity of the German discounters in recent years has led to increased competition

in the food retail space (Duff & Phelps, 2016). German discount retailers pose a threat for many

of the traditional store formats as they aggressively grab market share and push for greater

operational efficiency and lower prices. Many supermarkets and supercenters try to compete

directly with them by adopting the same format and as such, run the risk of cannibalising their

core business as a conventional supermarket or supercenter (Duff & Phelps, 2016). Although

supermarkets and discounters emphasise different consumer benefits and thus, target different

segments, there is considerable overlap which means the two different store format experience

considerable interformat competition. Not to mention the intraformat competition that occurs

between those following the same business model (Clereen et al, 2010). The fierce competition

between those operating the same format, along with naivety as to the severity of the threat posed

by these German retailers, allowed these discounters to enter various markets in Europe, expand

quickly and eat up market share at an alarming rate (Clereen et al, 2010).

The fierce competition in the market benefits customers in terms of lower prices, higher quality

products, greater selection and a more efficient shopping experience (Stanikunas, 2010). Glandon

18

and Jaremski (2014) focused their research on the prevalence of price reduction and ‘sales’ as a

way to attract consumers in the sector, acting as a testament to the loss-leader strategy and

exemplifying the competitiveness in the industry. The idea of ‘everyday low prices’ came about

with the introduction of Walmart in the US whereby temporary price reductions were superseded

by the idea that high quality produce can be affordable. This was further cemented by the

introduction of the German retailers some years later (Glandon & Jaremski, 2014). According to

Glandon & Jaremski (2014), for those firms not following a low cost strategy, many are forced to

partake in sales promotions in response to competition from these low-cost retailers. From their

study, firms in close proximity to the opening of a Walmart -like store would increase the

frequency of sales on particular products in order to compete, thus showing a strategic response to

the entry of this low-cost retailer (Glandon & Jaremski, 2014).

In conclusion, the structural characteristics of the grocery industry are conducive to market

concentration and it is often assumed that as a consequence there is a competition problem

(Smith, 2006). This has resulted in price wars, a significant power imbalance between the few

large retailers and the suppliers, reduced buyer power in terms of end consumers, and the

construction of stiff barriers to entry. Hence why the competitive nature of the industry is closely

tracked by government agencies. Governments have a responsibility to ensure fair competition

and possess the power to alter the dynamics of power in the industry. Therefore, understanding

how these firms work and compete is critically important for economic policy (Stanikunas, 2010).

19

(Figure 2.3: A five forces analysis of the grocery retail industry)

The five forces discussed above are summarised in figure 3 and come together to exemplify a

very competitive industry. This is supported by my financial analysis of nine major retailers in

three major economies. The tight and small metrics that I have compiled provide empirical

evidence of the above strategic analysis. We can also understand the metrics better through

understanding the industry as a whole. Decreasing returns in the industry over the past five years

is not surprising considering what we know about the competitive struggles in the industry, as

well as economic circumstances. Therefore, greater depth and understanding of the industry can

be gained by conducting a high-level exploratory analysis of its performance through a range of

metrics.

20

3.0 METHODOLOGY

This section sets out the procedures by which the data for this dissertation will be collected. The

aim of this quantitative research it to give a general overview of the financial performance of the

grocery retail across three of the major economies over a period of five years, through the use of

financial metrics. As identified in the literature and the competitive analysis of the industry, this

industry in unique in terms of its competitive rivalry and therefore, we can expect to see

increasingly tight margins, decreasing performance based on the synopsis’ of each company, and

similarities between the different economies on each of the metrics.

3.1 Method, measures and rationale

The primary source of data for this dissertation is the annual reports of the chosen companies

which have been presented in a coherent format in order to improve understanding and analysis.

Excel sheets were compiled for each company with the three prominent financial statements: the

income statement, the balance sheet and the cash flow statement. The aim was to keep a

consistent format for each economy so as to facilitate comparisons and greater ease of analysis.

Information gathered from financial statements was appropriate for this research as it gives

insight into the financial performance of each company that can be useful in preparing industry

averages and economy specific information. However, financial statement analysis is not without

its limitations such as issues involving classification when considering statements produced in

different economies that operate under different accounting standards, the sole focus on historical

information and the problem of missing non-financial information (Mahboobinijad, 2015) To

analyse the industry, economies and companies, a range of eleven financial measures were put

together that would give a rounded view of the industry. The averages of such are presented in

appendix 2 and represent all nine companies over the five year period chosen. In an excel it was

possible to compile averages per economy, per year, per company, and over the five years.

Graphs were drafted up to improve visual coherence and certain trends could be spotted. From

this, a select few metrics were chosen out of interest and a DuPont analysis was formed to assess

the decline in returns observes. These measures will be discussed in greater detail throughout the

analysis. It was important to compile my own financial statements and metrics into a

comprehensive framework in order to gain a greater understanding of the key performance

indicators of the selected companies over a 5 year period. For developmental and professional

21

purposes, it made sense to conduct a financial analysis from scratch. This quantitative analysis

can be reproduced by another researcher who has the same aims and they will come out with the

same results, landing this research methodology in the realm of positivism according to Saunders

et al., (2007).

3.2 An introduction to the sample companies chosen for analysis

The target groups for my research are grocery retailers from three main economies; the UK, the

US and the EU. I have chosen to analyse and compile data on three companies domiciled in the

three different economies over a period of five years. At least one from the group operates

multinationally, and all of which are of similar scale, format and business model. The companies

chosen make up a substantial proportion of the total market which leads us to believe that it is

representative of that particular economy and the global grocery retail industry. The combined

market share of the three companies make up between 45% and 55% of the total grocery retail

market in their respective countries. Certain players in the industry had to be omitted from the

research due to insufficient financial information.

3.1.1 UK-domiciled companies

(Figure 1: Great Britain Grocery Market Share 2016. Kantarworldpanel.com, 2016)

22

The table above is a snapshot of the UK grocery market in 2016. It is clear from this that the three

companies chosen make up a substantial part of the total market with a combined share of 55.3%

(Kantarworldpanel.com, 2016). This leads us to believe that an analysis of these companies is

representative of the market as a whole. Asda is a Walmart-owned company and therefore, has

been omitted from this research project.

(1) Tesco

Tesco was established in 1919 in East London and operated on a small scale up until 1950 when

its first supermarket was introduced. In the 1960’s it began introducing various household items

and in 1968, in keeping with the periods of evolution outlined in chapter one, Tesco opened its

first superstore. Slightly behind the US in terms of computerisation, Tesco did not introduce

scanning registers until 1982. The 1990’s was a revolutionary decade for the company wherein it

launched its ‘every little helps’ campaign, the first Tesco Express was introduced, and, Tesco’s

international ambitions became a reality as it became a global corporation. In the early 2000’s,

Tesco continued its expansion which included building itsonline presence and buying the UK’s

largest convenience store chain, One Stop (Tescoplc.com, 2016). Today, Tesco is the UK’s

leading grocery retailer with a market share of 28.2% at the end of June 2016 (Kantarworldpanel,

2016). However, the seemingly impregnable brand has encountered some difficulty over the last

number of years. In the financial year ended February 2015, the net loss was £5,741 million,

compared to the net profit of £974 million in 2014. Tesco has been feeling the pressure from

German discounters with revenues falling since 2013, as well as suffering from the bad publicity

after the accounting scandal that transpired in 2014 (marketline, 2016). Some questioned whether

or not the company has been over-ambitious with its expansion as attempts to break the US

market failed and markets such as China and Japan proved less fruitful than it had hoped (Simms,

2014). In response, the company announced a turnaround strategy in order to restore

competitiveness. Tesco’s CEO, Dave Lewis, announced plans to scale back expansion, close

unprofitable stores, reduce the number of product lines held in store, and decrease prices on a

variety of ranges.

(2) Sainsbury’s

Sainsbury’s opened its doors 50 years before Tesco in 1869. Among its competitors, it was the

first in many ways including; the first to introduce fairtrade in its stores, recyclable plastic bags,

23

organic produce, and the use of the traffic light nutritional guidance system. In the 70’s, the store

began introducing non-food items in store, including its own fashion brand (J-Sainsbury.co.uk,

2016). The period between 1992 and 1998 was a rough one for the company as sales declined

considerably (Butler, 2014). Sainsbury’s not only operate the supermarket format. In 1998,

Sainsbury’s introduced its first convenience store, Sainsbury’s Local, which has now expanded to

over 700 stores as the company noticed a change in consumer buying habits away from the ‘one-

stop-shop’ phenomenon (Coles, 2015). Over 100 of these stores are thanks to a joint venture that

the company entered with Shell garages. As was the case for Tesco, acquisition was the main

entry mode into this sector of the industry. Sainsbury's too faced disaster when trying to expand

abroad, exemplified by its catastrophic joint venture with an Egyptian distribution company that

resulted in a first year loss of £10 million and the imprisonment of its Chief Executive, Mike

Coupe (Ruddick, 2015). 2015 was a particularly bad year financially for the company as it saw its

first loss in over a decade (Ruddick, 2015). At the beginning of 2016, the company decided to

expand its non-food range. The company managed to secure a takeover of Argos which it hopes

will guarantee it a position as the ‘leading food and non-food retailer’ in the future (Hutchison,

2016). The first quarter of 2016 has not been kind to the UK’s four major grocery retailers.

However, Sainsbury's has seen the smallest sales declines compared to its four main rivals

(Yeomans, 2016).

(3) Morrisons

Morrisons has its roots in Bradford in 1899. The first supermarket came some 62 years later in

1961 (Morrisons-corporate.com, 2016). As opposed to many of the other retailers in the market,

Morrisons has historically followed an organic-growth strategy rather than an acquisition-led

growth strategy. That was until 2004, when Morrisons acquired Safeway, making it the UK’s

fourth largest grocery retailer (Morrisons-corporate.com, 2016). In 2014, the company announced

its ‘im cheaper’ campaign which meant that the company was to become permanently cheaper

than its major rivals. Today, the chain is the cheapest among its ‘big four’ rivals. Since the

beginning of 2016, the company has consistently seen the second strongest sales declines

compared to its four main rivals in the UK grocery retail industry at roughly 2% (Yeomans, 2016)

However, this is much less severe than the declines suffered by the company in previous years.

For example, in 2015, the company saw a painful 5.9% decline in sales. The company has failed

to expand geographically which means it has heightened exposure to economic, political and

social situations in the UK. Furthermore, the company was slow to adapt to the move away from

24

the one-stop-shop trend and adopt a range of convenience stores like its rivals. It was not until

2011 that Morrisons introduced its chain of convenience stores known as M Local (Morrisons-

corporate.com, 2016). In an effort to improve performance, Morrison’s newly appointed CEO,

David Potts, announced a rebrand at the start of 2015 to turn around the financials of the

company. A number of initiatives were introduced, one of which was to sell of underperforming

stores, which included the whole chain of convenience stores (Smollen, 2015). A new logo has

been introduced, stores are being revamped, prices have been cut considerably to attract new

consumers, and greater efforts have been made to enhance its online presence (Hobbs, 2016). In

February of this year, Morrisons entered a major partnership deal with Amazon to extend its

online platform. Morrisons already have a 25-year supply deal with Ocado but partnering with

Amazon is a low-risk and capital light deal that will open the company up to a new consumer

base. As of 2014 figures, Morrisons held a miniscule 0.9% of the online grocery sector in the UK,

in companrison to the 39.1% share held by Tesco (Roderick, 2016).

3.2.2 US-domiciled companies

The three companies chosen for the analysis of the US retail grocery segment are Wal-mart,

Kroger and Costco, which together make up 49% of the total sales in the US grocery market

according to the Progressive Grocer’s Super 50 report (Korosec, 2015).

(1) Walmart

The company that is now hailed as a mega-corporation that has the power to impact society,

prices, wages and the overall economic situation on a local, national and global scale, began its

operations much later than some of its well-known rivals, in the year 1962. In the early 80’s, the

company opened its first cash and carry-style warehouse club, and a few years later it opened its

first hypermarket which transformed into the supercentres that we know today (Marketline.com,

2016). Today, Walmart operates various different store formats and holds the title as the retailer

that sells more groceries than any other in the entire world (Fishman, 2006). Walmart consistently

strive for lower input prices so that it can pass these savings on to its customers, otherwise known

at ‘the perpetual motion machine of profitability’ (Steffy, 2016). Before Walmart came onto the

scene, incumbents dabbled in sporadic sales, however, Walmart built on this by announcing

‘everyday low prices’ which became its slogan and the basis through which it turned the industry

on its head. The company is considered revolutionary in changing the shopping habits of

25

consumers and the structure of the industry. Essentially, what Walmart did was change our

perception about quality and its affordability. Walmart's expansion nationwide was aggressive,

with there now being a store in all 50 states, and exemplified by the fact that, today, more than

half of Americans are within five miles of a Walmart store (Fishman, 2006). According to

Progressive Grocer’s 2016 issue of the top US grocery retailers, Walmart ranks first in terms of

size, number of employees and total revenue (Progressivegrocer.com, 2016). Not only has its

expansion nationwide been impressive, but the corporation now boasts an international profile of

an additional 26 countries throughout the world, making it a truly global company

(Marketline.com, 2016). However, like others in the industry, Walmart has suffered setbacks. The

company didn’t always get it right when it came to international expansion, among others was the

much-publicised withdrawal from the German market. Furthermore, in tandem with the global

economic downturn and the rise in oil prices, Walmart has suffered sluggish global sales growth

over the last number of years. The company dominates the hypermarket channel however, sales in

such have slowed as cash-strapped consumers opt for the smaller-format dollar stores (O’Keefe,

2015). The company’s commitment to the ‘Always low prices, always’ slogan has afforded it

some unwanted publicity and criticism over its abuse of buyer power (Cascio, 2006). The

company that was once micro-managing the marketplace, now faces the stiffest competition of its

existence. As a result, CEO, Doug McMillion announced the reinvention of the company to win

in the digital age (O’Keefe, 2015). This led to the opening of multiple e-commerce fulfillment

centres throughout the US (Marketline.com, 2016).

(2) Kroger

The first Kroger was established almost 80 years before Walmart came on the scene. What sets

the company apart is its commitment to providing fresh, quality, organic produce in store and to

ensure this, more than 40% of the produce found in store is made in its own Kroger factories

(krogercorp.usdphosting.com, 2016). The first superstore came about in the early 1970’s, in

tandem with the evolution of the industry. When Walmart began to roll out its supercentres across

the country, Kroger began to invest heavily in a number of things, notably, greater data analytics

to improve the customer shopping experience (Telesca, 2015). Kroger has consistently been ahead

of its competitors with regards to the digital boom. It was the first to introduce scanning registers

at checkouts and, in 2012, it rolled out the first, and currently only technology platform in the US

that uses sensors and predictive analytics that affords managers real-time data (Taylor, 2015).

Kroger’s story has a common thread of acquisitions and mergers running through it which has led

26

it to the scale it operates at today and has been named as one of the top 10 retailers to from in

2016 (Springer & Zwiebach, 2016). Currently, Kroger ranks second in the US grocery market in

terms of sales, operates the third largest filling stations in the US and is the fifth largest drugstore

operator in the nation. The company announced a massive $4 billion expansion plan that is due to

be rolled out this year with a greater focus on high profile acquisitions, upgrading its digital

presence and extending its geographic reach (Coolidge, 2016).

(3) Costco

A key characteristic of the grocery retail industry is the lack of consumer loyalty. Despite efforts

by traditional retailers to increase loyalty through reward schemes, consumer loyalty has

diminished over the years along with the dissolution of the ‘one-stop-shop’ idea. Costco has

managed to hang on the coattails of this trend through the creation of members-only warehouses.

In the intensely competitive environment that it operates in, low-price membership and a bundle

of faithful shoppers sets Costco apart (Kell, 2015). Costco opened its doors for the first time in

1983 and operates the warehouse club format that champions bulk, low-cost products, pioneered

by Price Club (Datamonitor, 2010). Therefore, key to its competitive advantage is a lean

operating cost model whereby inventory levels are kept at a minimum, allowing the company to

make greater sales per square foot compared to its closest rivals (Soni, 2016). Rather than selling

the usual items at discounted prices, there can be high-end goods such as diamond rings for rock-

bottom prices which sends consumers on somewhat of a ‘treasure hunt’ while also changing

consumers perception of ‘discounts’ and quality. This strategy has worked well for the company

throughout the years as they attempt to stave off competition from ‘sensible discounters’ (Branch,

1999). The strategic emphasis for the company is on value rather than price. Thus, its target

market is the more upscale, sophisticated consumer base (Cascio, 2006). The company currently

operates in nine different countries throughout the world (Costco.com, 2016). However, it is

heavily reliant on its home market with almost 75% of its warehouses based in forty states in the

US (Datamonitor, 2010). By the end of 2015, the company ranked as the second-largest retailer in

the world (Carpenter, 2015) and ranked second in terms of sales in its country of origin.

27

3.2.3 EU-domiciled companies

The top European companies chosen for this project are within the top four in terms of sales. The

Schwarz group could not be included as it is privately owned and does not issue financial

statements.

(1) Carrefour

Carrefour is Europe’s largest retailer with over 15,000 stores in four different formats;

hypermarkets, supermarkets, cash and carry and convenience stores (Datamonitor, 2011). In 1959,

this French company pioneered the ‘hypermarket’ format, which, was an extension of

supermarkets in terms of retail space and product variety. In fact, the term ‘hypermarche’ means

“bigger than traditional supermarkets” in French (Yhi-Chearang et al, 2006). Carrefour operates

globally in over thirty countries concentrated on three continents (Carrefour.com, 2016). Despite

its huge success in Europe, the company failed to crack the American market due to stiff

competition, even though it entered into joint ventures with Costco and Office Depot. Hong Kong

also caused trouble for the French giant (Yhi-Chearang et al, 2006). The company is heavily

reliant on sales in France and Western Europe countries which has left it heavily exposed to the

turmoil the has occurred in these economic environments over the last number of years, notably,

the recession and the instability of the Eurozone area. For many years, the company was plagued

by disappointing results, until it announced a turnaround strategy in 2012 that would entail a

drawback from many unprofitable overseas markets in order to concentrate on maintaining a

leadership position in Europe (martin et al, 2016). 2016 will be the year of digitisation for the

company, along with others mentioned above. Carrefour’s CEO, Plassat, agrees with the general

consensus that physical stores will remain important in the industry, however, an online ‘click and

collect’ system is important in terms of evolution and providing time-conscious consumers with

an additional avenue for purchase (Van Looveren, 2016)

(2) Metro AG

Metro began operations in Germany in the year 1964 under the cash and carry format, and began

its internationalisation four years later. The company became Metro AG in 1996 and introduced a

variety of formats to change with the evolution of the industry (Krafft & Mantrala, 2010). It

witnessed the structural decline in large store formats such as supermarkets and hypermarkets

28

with sales falling for a number of years up until 2011. To offset this the company introduced a

‘Shape cost savings’ initiative, turned its international expansion efforts towards emerging

markets and focused on the smaller format stores. Today, Metro operates in 26 countries (Kelly,

2016). The company felt the effects of its native discount rivals Aldi and Lidl before other parts of

the world. In response, Metro added a new format to its list in tandem with the evolution of the

industry - the discount format. Its flexibility in format has been hailed as the main reason why the

company has managed to stay in business. Although, the Cash and Carry arm of the business

remains at the forefront contributing almost half of the group’s total earnings (Kelly, 2016). With

unstable financials over the last number of years, the company faced 2016 with reduced investor

confidence and a need to scale back its expansion plans significantly, and it did just that by selling

off unprofitable operations in both Vietnam and Canada which resulted in a slight growth in sales

and a reduction in its debt (Baja, 2016).

(3) Auchan

Following in Carrefour’s footsteps, French-based company, Auchan opened its first hypermarket

in 1967 (Groupe-Auchan.com, 2016). The 1990’s was an important period for the company in

terms of international expansion as it moved into various markets, notably, China. The company

has remained ‘hypermarket-dominated’ in format despite entering the convenience store,