Final Results Q1-3 2017 - HolidayCheck Group€¦ · Final Results Q1-3 2017 2 1. Overview Q1-3 /...

28

Final Results Q1-3 2017 Georg Hesse (CEO) Nate Glissmeyer (CPO) Markus Scheuermann (CFO) 8 th November 2017

Transcript of Final Results Q1-3 2017 - HolidayCheck Group€¦ · Final Results Q1-3 2017 2 1. Overview Q1-3 /...

Final Results Q1-3 2017Georg Hesse (CEO)

Nate Glissmeyer (CPO)Markus Scheuermann (CFO)

8th November 2017

Final Results Q1-3 2017 2

1. Overview Q1-3 / Q3 2017: Strong booking seasonMarket development• Central-European package travel industry with strong booking season in Q1-3• OTA growth outperformed other revenue streams

Financials• HolidayCheck Group revenue up 10% in Q1-3 2017 and 8% in Q3 2017• Operating EBITDA of EUR 1.3m in Q1-3 2017; operating EBITDA of EUR -1.5m

in Q3 2017 due cost of EUR 1.3m, esp. for LTI and RSP • Well on track to grow in upper third of FY revenue and op. EBITDA guidance

corridor

2. Financials Q1-3 & Q3 2017

2. Financials Q1-3 2017: Invest in brand marketing and newhires

Final Results Q1-3 2017 4

In EUR million Q1-3 2017 Q1-3 2016 Change Q3 2017 Q3 2016 Change

Revenue 93.2 84.6 +10% / +8.6 32.0 29.6 +8% / +2.4

Marketing expenses -48.2 -45.3 +7% / +2.9 -18.7 -15.3 +22% / +3.4

Personnel expenses -28.5 -24.4 +17% / +4.1 -9.1 -9.4 -3% / -0.3

EBITDAEBITDA margin

-0.1-0.1%

3.44.0%

-3.5 -1.5-4.7%

2.48.1%

-3.9

Operating EBITDAOperating EBITDA margin

1.21.3%

2.93.4%

-56% / -1.6 -1.5-4.7%

2.79.1%

-4.2

Depreciation -4.5 -4.1 +8% / +0.4 -1.5 -1.4 +10% / +0.1

EBITEBIT margin

-4.5-4.8%

-0.7-0.8%

>100% / -3.8 -3.0-9.4%

1.0+3.4%

-4.0

Financial result -0.1 0.1 -0.2 0.0 0.1 -0.1

EBTEBT margin

-4.6-5.0%

-0.6-0.7%

-4.0 -3.1-9.5%

1.13.7%

-4.2

Consolidated net result of continued operations -4.9 -0.8 >100% / -4.1 -2.8 0.9 -3.7

Consolidated net result -4.6 -0.8 >100% / -3.8 -2.8 0.8 -3.6

EPS of continued operations (in EUR) -0.08 -0.01 -0.07 -0.05 0.02 -0.07

3. Investment areas 2017

Final Results Q1-3 2017 6

3. Investment areas 2017 – a status report

Invest in brand marketing:‘Book your thing!’ campaign is a encouraging success to improve future brand awareness

Invest in customer service:Well on track to differentiate ourselves from offline and online travel agencies

Invest in data intelligence:Accelerated investment in real-time and self-learning systems to increase value to customers

Invest in product development:Incremental investment in new businesses and new experiences for our Urlauber

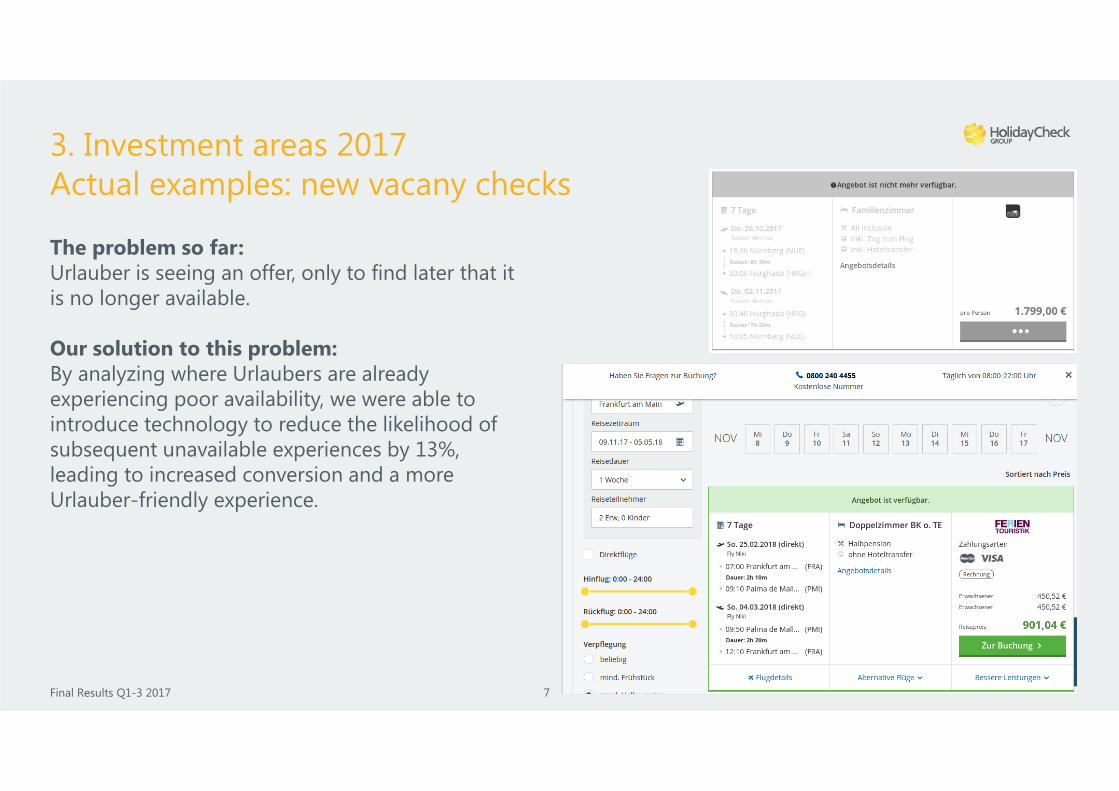

3. Investment areas 2017Actual examples: new vacany checks

Final Results Q1-3 2017 7

The problem so far:Urlauber is seeing an offer, only to find later that it is no longer available.

Our solution to this problem:By analyzing where Urlaubers are already experiencing poor availability, we were able to introduce technology to reduce the likelihood of subsequent unavailable experiences by 13%, leading to increased conversion and a more Urlauber-friendly experience.

3. Investment areas 2017Actual examples: new direct flight filters

Final Results Q1-3 2017 8

The problem so far:Urlaubers struggled to find the best flights due to huge number of possible flight combinations;

The consequences so far:Urlaubers did not manage to book a direct flight or to chose a flight within their a certain time frame

Our solution to this problem:Newly released filters for “direct flights” and “specific flight times” simplifie the search for the best flights and are already used by more than 10% of our customers

4. Outlook 2017

Final Results Q1-3 2017 10

4. Outlook 2017:We stick to our vision & mission

Our vision:

We are the most Urlauber*-friendly company in the world

Our mission:

We make our Urlauber’s experience better every day!

* Urlauber [uːɐlaʊbɐ] is the German term for vacationer, holiday-maker

Final Results Q1-3 2017 11

4. Outlook 2017:Brick and mortar travel agencies are our source of business

Our source of business:

2/3 of all package holidays in Germany are still booked offline.

We aim to change that!

Final Results Q1-3 2017 12

4. Outlook 2017:Our invest areas

Our invest areas in Q4 2017:

• Package: core product experience• Hotel only: continue to grow• Scale travel center by hiring further

employees• Final preparations to launch totally new

cruise experience• Build where we can, buy where we need

Final Results Q1-3 2017 13

4. Outlook 2017:We stick to our guidance

Guidance 2017:

• October well on track• Revenue guidance of +7 – 11% yoy• Q4 2017: We will continue to invest in people,

tech and esp. in brand marketing• Op. EBITDA guidance remains at EUR -5 to 0m• Well on track to grow in upper third of FY

revenue and op. EBITDA guidance corridor• We are hunting the big game!

Our long-term ambition:• Sustainable double-digit growth

• Invest now to gain leverage on personnel and marketing costs in out years

THANK YOUFOR YOUR ATTENTION!

Appendix

Our eco system: A unique combination of a platform & pipeline business

Final Results Q1-3 2017

Hotel

HOTELS

REVIEWERS

HOLIDAYCHECK GROUP

TOUR OPERATORS

INVENTORY

DATA & PERSONAL SERVICE

URLAUBERS*

ADVERTISERS

ADVERTISING

PAYMENT

CONTRACT

*German term for holidaymaker, vacationer

SHARE

DECIDE

BOOK

PLATFORM BUSINESS:User Generated Content

(UCG)

PIPELINE BUSINESS:Online Travel Agency

(OTA)

16

0

10

20

30

40

50

60

70

80

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Strong economic fundamentalsThere is significant headroom for online travel agencies

17

Overall demand remains relatively healthy, despite adverseexternal events

Still a lot of growth potential for package holidays online

Package is key segment for HolidayCheck

Today still offline dominated

72%44%

33%

28%56%

67%

Offline

HotelFlight / Train

Online

*Package

*All privately booked trips with a duration of at least 2 days and one pre-paid element, at leastSource: Own estimate based on the GfK Travelscope 2.0 survey

Total size of German travel market 2016: € ~55 bn;

Thereof package:€ ~16 bn

Impact on the overall travel behaviour (revenue HC)

Overall

Greece

Spain

Military coup in Egypt

Arab revolutions

Military coup attempt in Turkey

Final Results Q1-3 2017

EgyptGreece

Spain

Turkey

Proportional breakdown of travel bookings in Germany (2016)

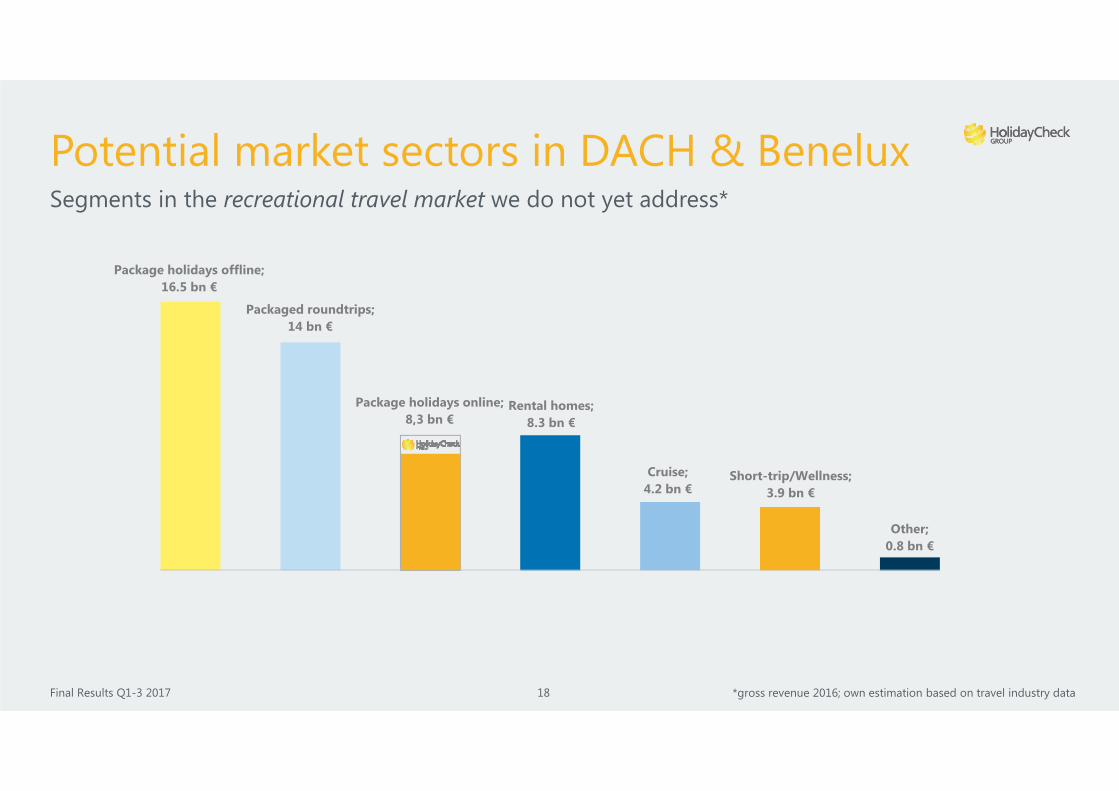

Package holidays offline; 16.5 bn €

Packaged roundtrips; 14 bn €

Package holidays online; 8,3 bn €

Rental homes; 8.3 bn €

Cruise; 4.2 bn €

Short-trip/Wellness; 3.9 bn €

Other; 0.8 bn €

Potential market sectors in DACH & Benelux

Final Results Q1-3 2017 18

Segments in the recreational travel market we do not yet address*

*gross revenue 2016; own estimation based on travel industry data

Drivers of growth

19

User experience We are able to improve user experiencemore easily after our IT migration

CROSS-DEVICE OPTIMISATION• Google Accelerated Mobile Pages (AMP) launched

SIMPLIFICATION• Online booking processes (currently avg. 23 site visits, 400-

600 clicks)• Bulk picture upload for reviews• Integration of Peakwork platform (higher data quality)

PERSONALISATION• With our passion search holidaymakers can search our

reviews by key words, e.g. water park or snorkeling in order to find the hotels that fit their personal interest best

20Final Results Q1-3 2017

Customer service

OUR HEADSTART• We connect people with people• We know what customers want:

#1 review site in DACH and Benelux• That is how we can compete with offline travel agencies

DIFFERENTIATION VIA SERVICE• Regulation fixes retail prices for package holidays

without allowing re-sellers to discount• Only service makes a difference!

SERVICE COSTS• Ticket value high enough to support phone vending• Our service center with 150 skilled travel agents is a sales

channel, not a call center

21Final Results Q1-3 2017

We invest in service to differentiate ourselvesfrom offline travel agencies

Brand marketing We launched our campaign Buch Dein Ding! (Book Your Thing!) in June 2017

GOALS• Strengthen brand awareness and draw particular attention on

booking opportunity

OUTLOOK• Campaign to be continued in H2 2017 and 2018 on a

sustainable basis

TARGETED MEDIA MIX• Selected TV stations, leading news portals (bild.de, focus.de),

YouTube and outdoor advertising

22Final Results Q1-3 2017

ATTRACT BEST TALENTS• One of the most stringent recruiting processes in the industry• New HR-initiative called Talent2020• We hire not from the best travel companies, but from the best

companies, e.g.• 2016 CEO Group: Amazon• 2017 CFO Group: eBay, Mc Kinsey, Burda Group• 2017 CTO, CPO Group: Amazon• 2017 Director HR Group: Amazon• 2017 Director Busines Dev. Group: Mc Kinsey, Deliveroo• 2017 CEO HolidayCheck: Google, Internal

PeopleWe want to be the best team in the travel industry

MOTIVATE TALENTS• Share buyback with purpose of offering shares to employees

INVEST IN TALENT• Continued investment into headcount in customer-facing

service center and web-developers• To be continued in H2 2017 and 2018 on a sustainable basis

23Final Results Q1-3 2017

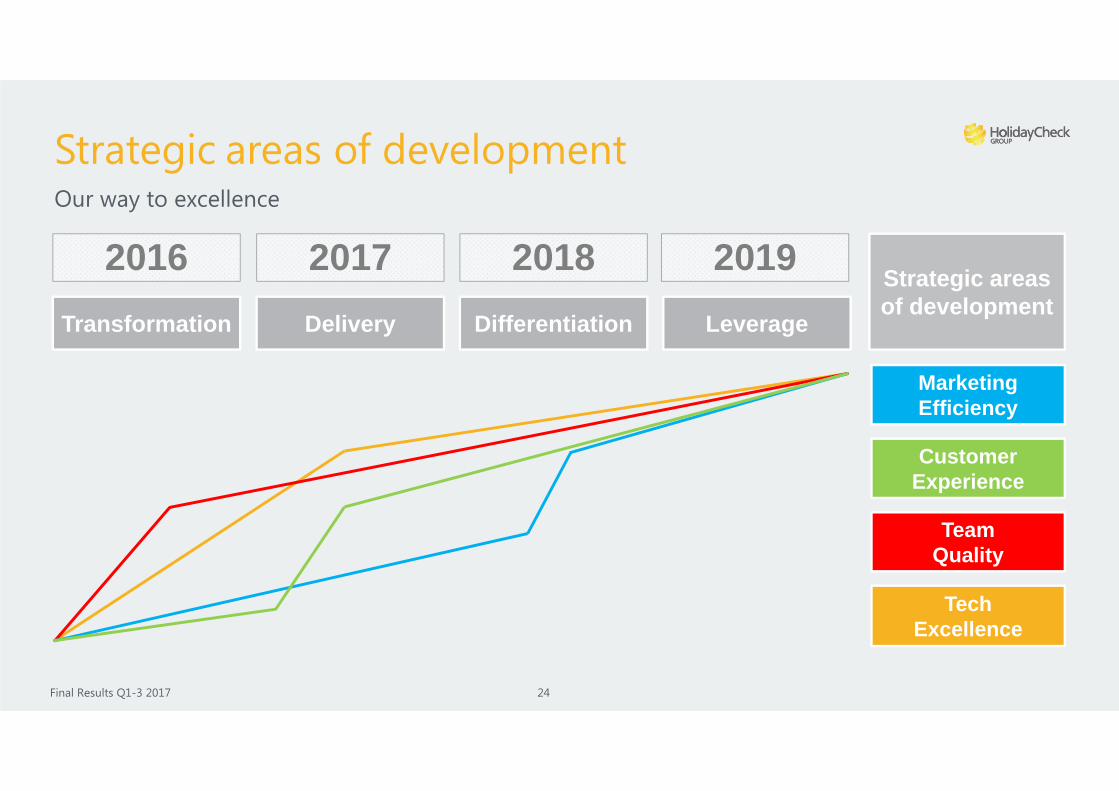

Final Results Q1-3 2017 24

Strategic areas of development

Transformation Delivery Differentiation Leverage

2016 2017 2018 2019

Tech Excellence

Marketing Efficiency

Customer Experience

Team Quality

Strategic areasof development

Our way to excellence

Strategic areas of development

25

Financials

2016 2017 2018 2019

TRANSFORMATION DELIVERY DIFFERENTIATION Leverage

Leverage cost base

underlying revenue growth

Guidance: 7-11%revenue growth

3.5%

EBITDAEUR 2.8m

EBITDAEUR -5m – 0m

Double digit revenue growth

Fix cost dilution effect

Final Results Q1-3 2017

Financial calendar

NOV 2017 NOV 2017 JUN 2018

8 NovemberPublication fo the Interim Statement Q1-3 2017Munich, Germany

27 NovemberGerman Equity Forum 2017Frankfurt/Main, Germany

20 JuneAnnual General MeetingHaus der Bayerischen Wirtschaft, Munich, Germany

* Provisional dates26Final Results Q1-3 2017

www.holidaycheckgroup.com HolidayCheck Group @HolidayCheckGrp

Contact

Georg HesseCEO

+49 89 357 680 [email protected]

27

Nate GlissmeyerCPO/CTO

+49 89 357 680 [email protected]

Armin BlohmannDirector Group Comm. & Investor Relations

+49 89 357 680 [email protected]

Final Results Q1-3 2017

Markus ScheuermannCFO

+49 89 357 680 [email protected]

Disclaimer

Final Results Q1-3 2017 28

This presentation contains 'forward looking statements' regarding HolidayCheck Group AG, including opinions, estimates and projections regarding HolidayCheckGroup AG’s financial position, business strategy, plans and objectives of management and future operations. Such forward looking statements involve known andunknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of HolidayCheck Group AG to bematerially different from future results, performance or achievements expressed or implied by such forward looking statements.These forward looking statements speak only as of the date of this presentation and are based on numerous assumptions which may or may not prove to be correct.No representation or warranty, express or implied, is made by HolidayCheck Group AG with respect to the fairness, completeness, correctness, reasonableness oraccuracy of any information and opinions contained herein.The information in this presentation is subject to change without notice, it may be incomplete or condensed, and it may not contain all material informationconcerning HolidayCheck Group AG.HolidayCheck Group undertakes no obligation to publicly update or revise any forward looking statements or other information stated herein, whether as a result ofnew information, future events or otherwise.