Final report - Review of access pricing on the NSW grain ... · Review of access pricing on the NSW...

120

Independent Pricing and Regulatory Tribunal Review of access pricing on the NSW grain line network Transport — Final Report April 2012

-

Upload

phungquynh -

Category

Documents

-

view

213 -

download

0

Transcript of Final report - Review of access pricing on the NSW grain ... · Review of access pricing on the NSW...

Independent Pricing and Regulatory Tribunal

Review of access pricing on the

NSW grain line network

Transport — Final ReportApril 2012

Review of access pricing on the NSW grain line network

Transport — Final Report April 2012

ii IPART Review of access pricing on the NSW grain line network

© Independent Pricing and Regulatory Tribunal of New South Wales 2012

This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism and review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgement of the source is included.

ISBN 978-1-921929-79-3 S9-77

The Tribunal members for this review are:

Dr Peter J Boxall AO, Chairman

Mr James Cox PSM, Chief Executive Officer and Full Time Member

Ms Sibylle Krieger, Part Time Member

Inquiries regarding this document should be directed to a staff member:

Melanie Mitchell (02) 9113 7743

Brett Everett (02) 9290 8423

Independent Pricing and Regulatory Tribunal of New South Wales PO Box Q290, QVB Post Office NSW 1230 Level 8, 1 Market Street, Sydney NSW 2000

T (02) 9290 8400 F (02) 9290 2061

www.ipart.nsw.gov.au

Contents

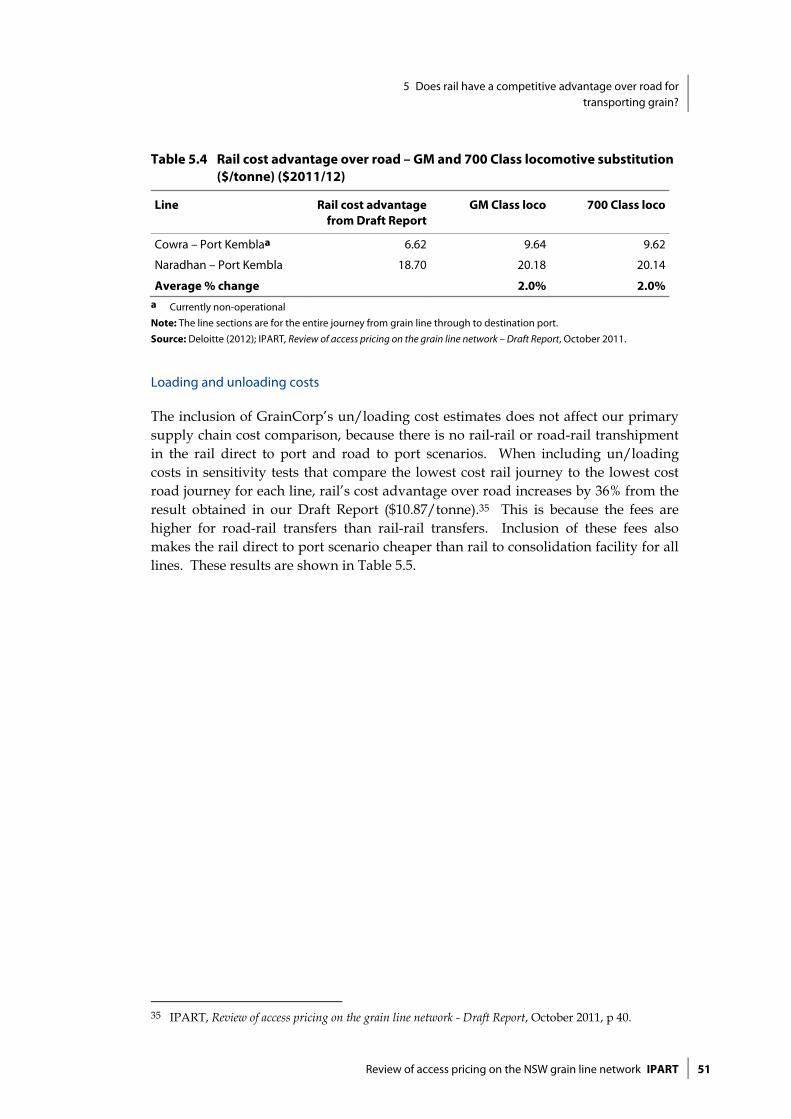

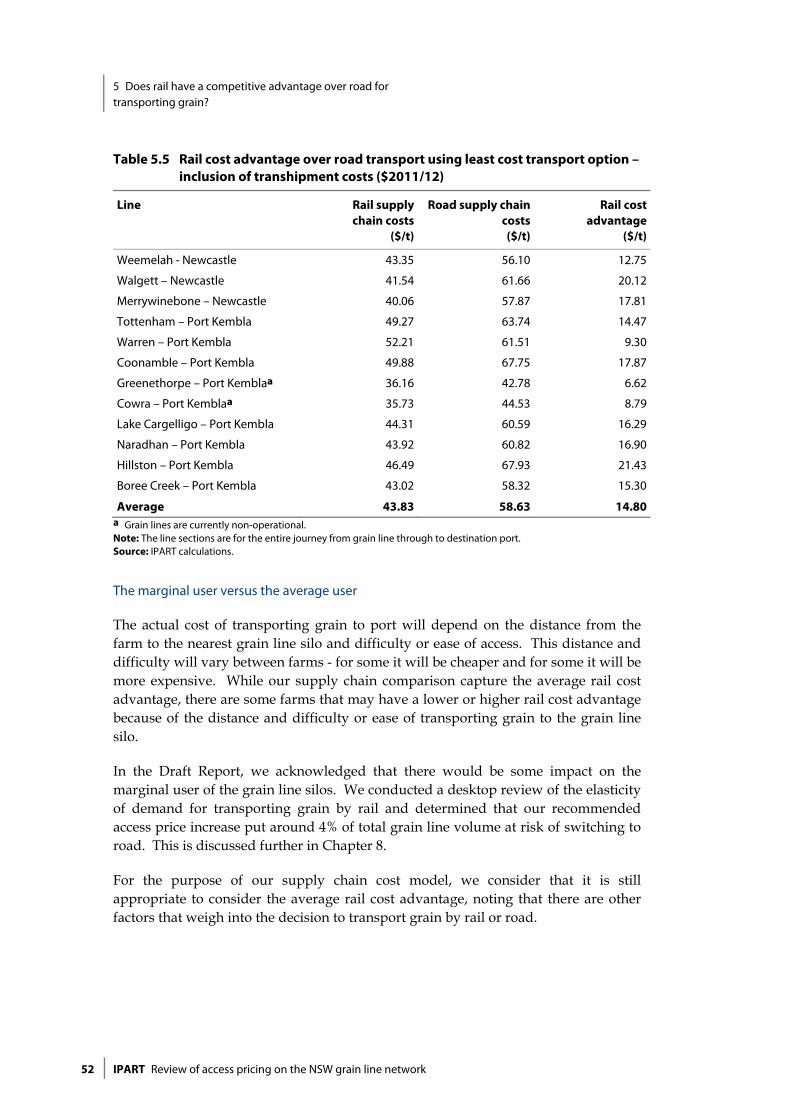

Review of access pricing on the NSW grain line network IPART iii

Contents

1 Executive Summary 1 1.1 What have we been asked to do? 2 1.2 How have we approached the task? 2 1.3 What are our key recommendations? 4 1.4 Overview of other complementary recommendations 12 1.5 What is the structure of this report? 12 1.6 A complete list of our recommendations. 13

2 Context for this review 15 2.1 What is the grain line network? 15 2.2 Who are the key stakeholders? 17 2.3 What are the key problems facing the grain line network? 17 2.4 What were the outcomes of previous reviews of the grain line network? 20

3 What are the costs of maintaining the network and what proportion is recovered from users? 21 3.1 Final Findings 21 3.2 What are the efficient below-rail costs of the network? 21 3.3 What is the level of cost recovery? 27

4 Are the current access prices and government subsidy appropriate? 32 4.1 Final Findings 32 4.2 What are the external benefits of the network? 33 4.3 What level of government subsidy is justified by the external benefits of the

network? 35

5 Does rail have a competitive advantage over road for transporting grain? 42 5.1 Final Findings 42 5.2 Supply chain costs of transporting grain to port by rail and road 43 5.3 Total supply chain cost of transporting grain to port by rail and road 48

6 Are there any non-price solutions that would improve cost recovery? 54 6.1 Final Findings 54 6.2 Can cost recovery be improved without increasing access prices? 55 6.3 Stakeholder submissions 55 6.4 IPART findings 56

Contents

iv IPART Review of access pricing on the NSW grain line network

7 What is an appropriate access price level and arrangement? 59 7.1 Final Findings 59 7.2 What is an appropriate increase in access prices? 60 7.3 What is an appropriate access price structure? 62 7.4 How should the access price be implemented? 66

8 What is the impact of our recommended access price on stakeholders? 69 8.1 Final Findings 70 8.2 What is the impact of our recommended access price increase on rail users? 70 8.3 What is the impact on government? 76

9 Complementary measures to promote sustainability on the grain line network 81 9.1 Final Findings 81 9.2 Do the regulatory arrangements governing the CRN warrant change? 82 9.3 Does the government subsidise heavy vehicle road use? 87 9.4 How could the government undertake a more integrated approach to

funding rail and road projects? 92

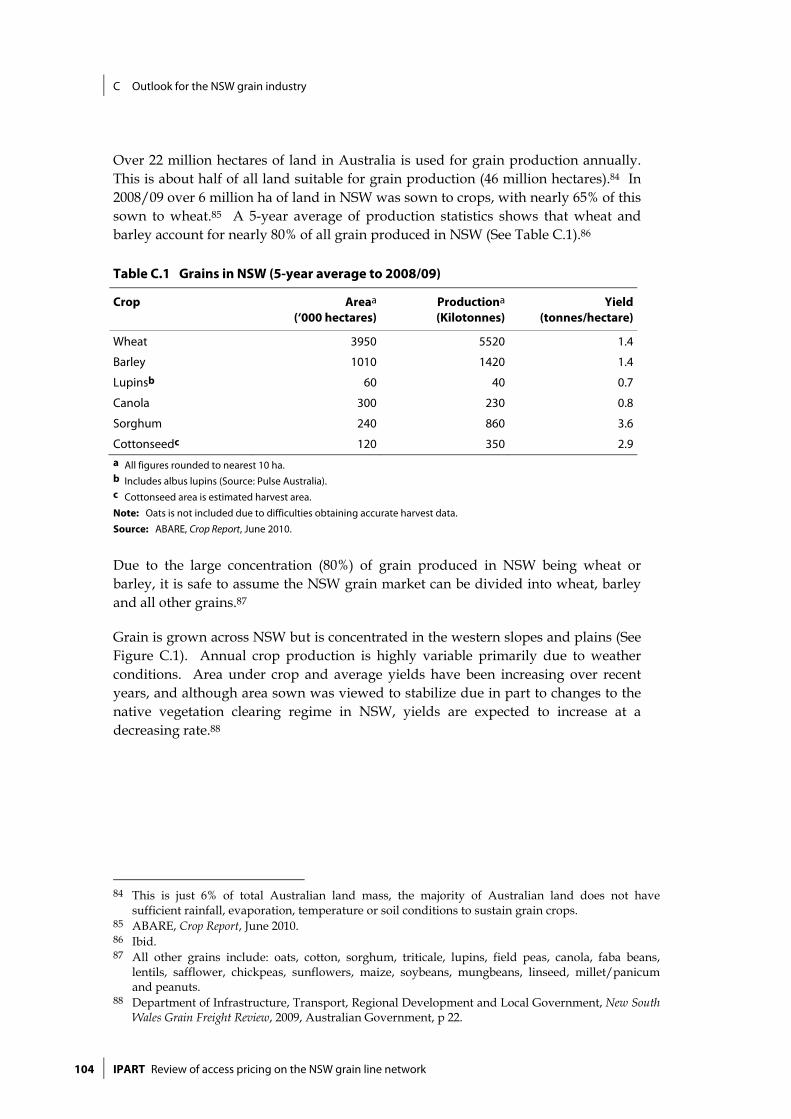

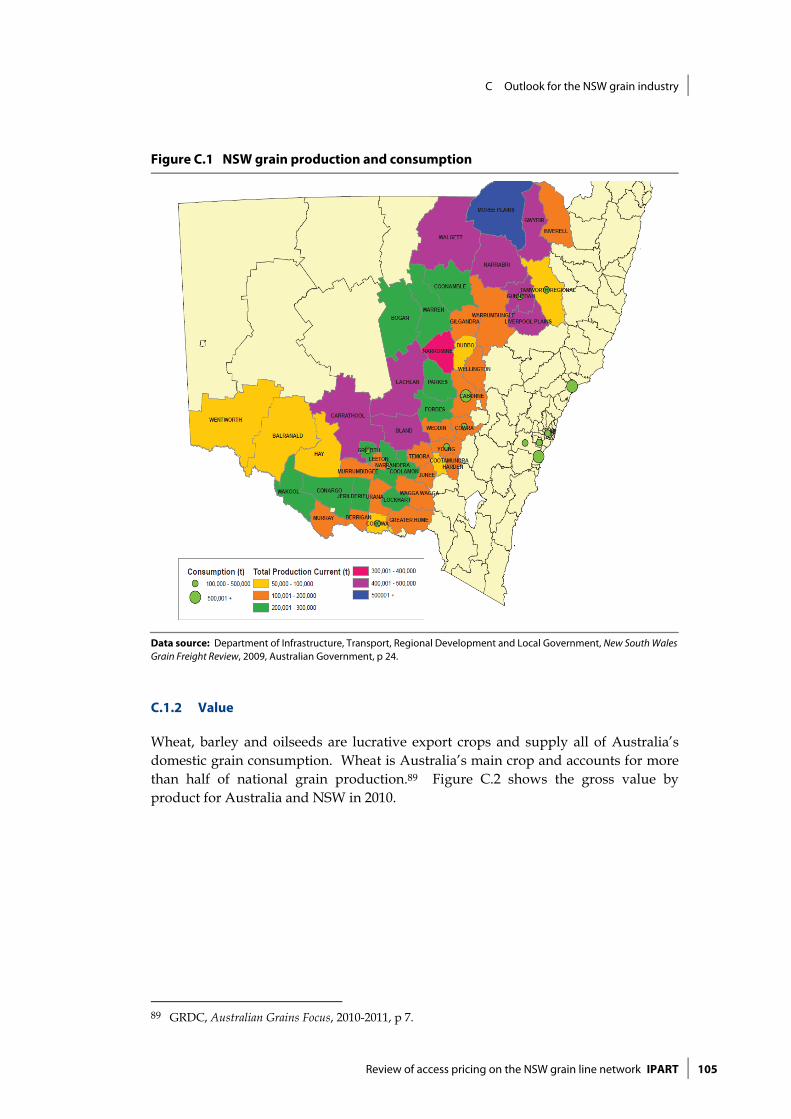

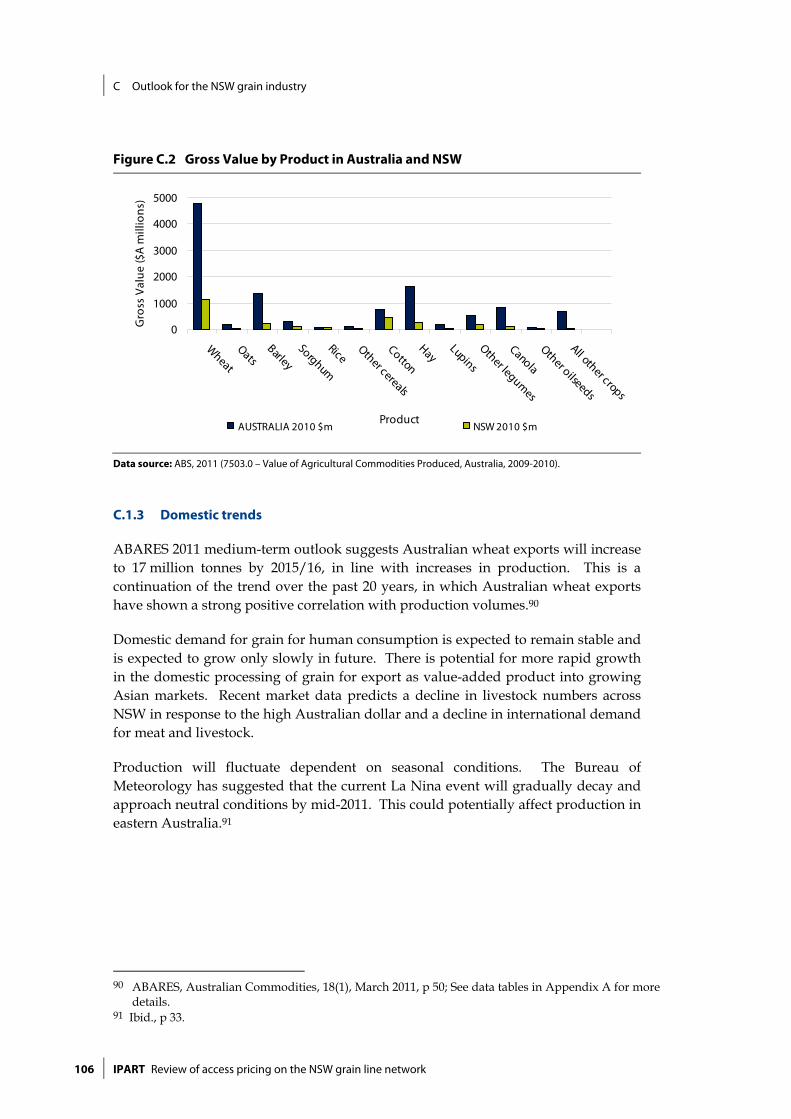

Appendices 96 A Terms of Reference 99 B Map of NSW Country Regional Network 102 C Outlook for the NSW grain industry 103 D Cost-benefit assessment of line upgrades 109 E Glossary 111

1 Executive Summary

Review of access pricing on the NSW grain line network IPART 1

1 Executive Summary

Grain is one of the State’s major commodities. In 2011/12, the export value of wheat is expected to exceed $1.5 billion, making it the most valuable non-mineral export commodity.1 The grain line network plays an important role in transporting grain from grain growing regions in the far north, west and south of the State to port and to large domestic users. In the absence of the grain line network, over 1.5 million tonnes of grain would need to be transported to a main line consolidation facility or to a port/large domestic user by road. This would increase the number of trucks on rural and regional roads and the costs to communities of maintaining these roads.

The grain line network is old, and many parts of it have fallen below a standard considered fit for the purpose of transporting grain. Currently, the government funds over 95% of ongoing maintenance costs and has engaged John Holland to provide maintenance and operations services on the network for the next 10 years in a contract worth around $1.5 billion.

While use of the grain lines instead of the road network generates positive external benefits for the wider community, at current levels of usage and access prices, rail users contribute less to maintenance costs than the value of benefits they gain privately from using the network. However, increasing levels of competition from a competitive and innovative road supply chain constrain the price that rail users can be charged for use.

Historically, limited government funding and competing budget priorities have resulted in lengthy periods of uncertainty about the sustainability of many lines and discouraged industry investment in the rail supply chain. Governments have long been aware of this issue and have reviewed the grain line network several times.

In 2009, the NSW Grain Freight Review commissioned by the Australian Government examined the efficiency of the grain supply chain in NSW and the ongoing viability of the grain line network. It recommended that most grain lines should remain open, because the total costs of increased grain traffic on the road network would outweigh the costs of keeping the lines open.2

1 ABS, Value of Agricultural Commodities Produced, 7503.0, 2009-2010. 2 Department of Infrastructure, Transport, Regional Development and Local Government, NSW

Grain Freight Review, 2009.

1 Executive Summary

2 IPART Review of access pricing on the NSW grain line network

In light of this, the NSW Grain Freight Review recommended that most lines be stabilised at a minimum ‘fit-for-purpose’ standard through a non-recoverable NSW government grant, contingent on industry investment in other supply chain improvements. It recommended that the NSW Government review future access charges to determine an appropriate user contribution to the cost of ongoing maintenance of the lines.

Our Final Report recommends a grain line access price increase from $2.61 to $5.22 per thousand gross tonne kilometres over a period of 2 years. While the impact of this increase is expected to be small for users (around 1.4% of the total rail transportation cost to port) it is an important move towards improving cost recovery on some lines and increasing user contribution to the share of benefits they receive from using the lines.

1.1 What have we been asked to do?

In December 2010, the former NSW Government asked the Independent Pricing and Regulatory Tribunal of NSW (IPART) to investigate and recommend future access pricing arrangements to promote the sustainability of the network, taking into account:

the efficient costs of providing grain freight services over the next 5 years

the impact of recommended prices on the road network and requirements for government funding of the grain line network, and

the ability and willingness of the grain industry to pay the recommended access prices (see Appendix A for the full terms of reference).

We have completed our review and formulated our final recommendations on access pricing and arrangements, as well as complementary reforms to improve the sustainability of some of the lines. The purpose of this report is to explain our final recommendations to the NSW Government and the key findings that support them.

1.2 How have we approached the task?

Throughout this review, stakeholders argued strongly and unanimously that to promote the sustainability of the network, any changes in access prices should not remove rail’s competitive advantage over road for grain haulage. They argued that it would encourage current rail users to shift to road transport, which would further reduce the sustainability of the network and may lead to the closure of some or all lines. This would increase heavy vehicle traffic on rural and regional roads, which in turn would increase road maintenance and other costs that this traffic imposes on the community.

1 Executive Summary

Review of access pricing on the NSW grain line network IPART 3

We undertook our own analysis to estimate the cost of transporting grain by rail or road to port. We also determined the efficient costs of maintaining the network and the external benefits that it generates for the wider community by displacing grain trucks from the road network.

To do this, we obtained expert advice from Mr Mike Smart from Sapere Research Group Limited (Sapere) and Deloitte Touché Tohmatsu (Deloitte). Reports by Deloitte and Sapere are summarised in our Draft Report and in the following chapters of our Final Report and are also available on our website.3

We consulted stakeholders by inviting submissions on our Issues Paper, Draft Report and participation at a public roundtable hearing. We have considered all information and views from stakeholders and incorporated them into our decision-making on Final Recommendations.

The key steps in our approach to making our Final Findings and Recommendations were to:

1. Determine the efficient costs of maintaining the network, including capital investment required to stabilise lines at their current operating standard and expected future ongoing maintenance costs.

2. Examine whether users are paying an appropriate contribution towards the costs of maintaining the network, taking into account the net external benefits generated by the network compared to transporting grain by road.

3. Estimate the cost to users of transporting grain from farm to port by rail and road for each grain line route and compare the 2 supply chains to quantify rail’s cost advantage over road at current access prices.

4. Consider whether there are other options to improve cost recovery without increasing access prices. Other options include:

a) reducing below-rail maintenance costs

b) increasing the amount of traffic on the lines

c) track upgrades as a mechanism to reduce operating costs and attract additional demand.

5. Having determined in step 4 that non-price solutions were unlikely to improve cost recovery levels, we revisited the results of the supply chain cost analysis in step 3 and determined how much access prices could be increased without eroding rail’s cost advantage over road.

6. Decide on appropriate access pricing arrangements and implementation.

7. Evaluate the impact of our recommended access price on rail users’ willingness to pay, government funding and other stakeholders.

3 www.ipart.nsw.gov.au

1 Executive Summary

4 IPART Review of access pricing on the NSW grain line network

8. Consider the need for complementary measures to promote the sustainability of the network, including any changes to the current regulatory regime, heavy vehicle user charging and government funding of rail and road infrastructure projects.

1.3 What are our key recommendations?

Following consideration of stakeholder submissions to the Draft Report and further analysis of our own, our Final Recommendations are largely unchanged from the Draft Recommendations. We recommend that:

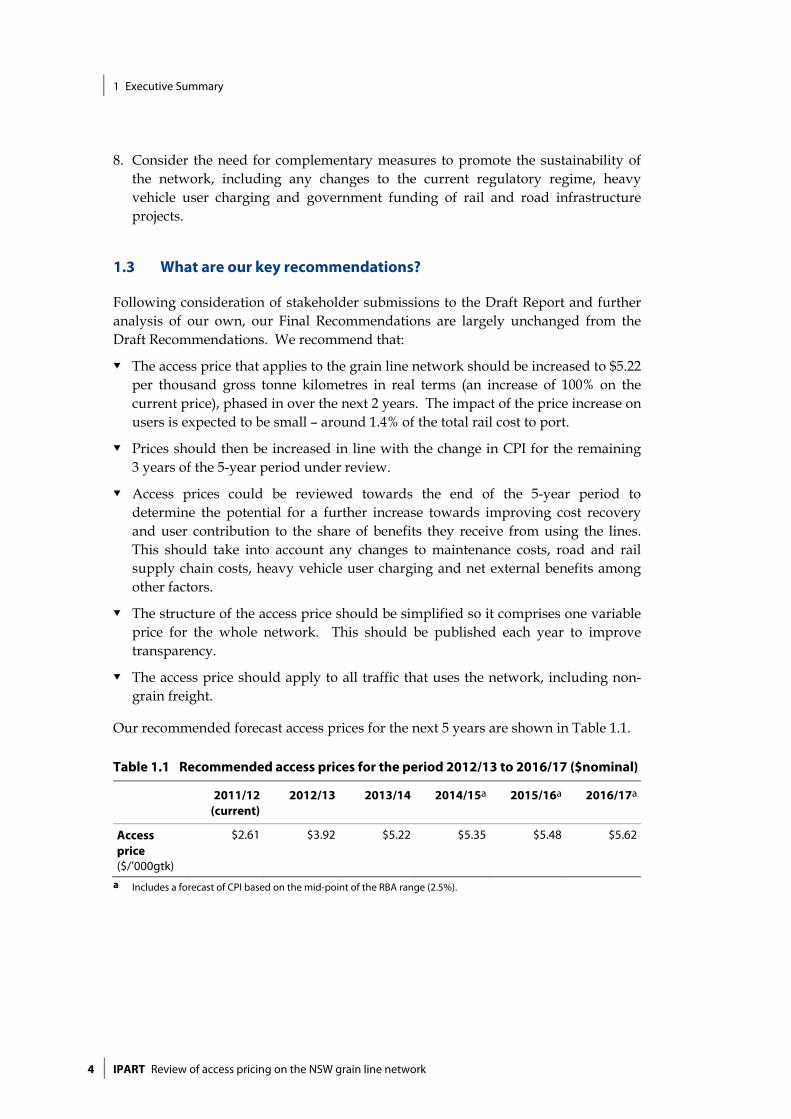

The access price that applies to the grain line network should be increased to $5.22 per thousand gross tonne kilometres in real terms (an increase of 100% on the current price), phased in over the next 2 years. The impact of the price increase on users is expected to be small – around 1.4% of the total rail cost to port.

Prices should then be increased in line with the change in CPI for the remaining 3 years of the 5-year period under review.

Access prices could be reviewed towards the end of the 5-year period to determine the potential for a further increase towards improving cost recovery and user contribution to the share of benefits they receive from using the lines. This should take into account any changes to maintenance costs, road and rail supply chain costs, heavy vehicle user charging and net external benefits among other factors.

The structure of the access price should be simplified so it comprises one variable price for the whole network. This should be published each year to improve transparency.

The access price should apply to all traffic that uses the network, including non-grain freight.

Our recommended forecast access prices for the next 5 years are shown in Table 1.1.

Table 1.1 Recommended access prices for the period 2012/13 to 2016/17 ($nominal)

2011/12 (current)

2012/13 2013/14 2014/15a 2015/16a 2016/17a

Access price ($/’000gtk)

$2.61 $3.92 $5.22 $5.35 $5.48 $5.62

a Includes a forecast of CPI based on the mid-point of the RBA range (2.5%).

1 Executive Summary

Review of access pricing on the NSW grain line network IPART 5

1.3.1 Why should grain line access prices increase?

Unsustainable level of cost recovery

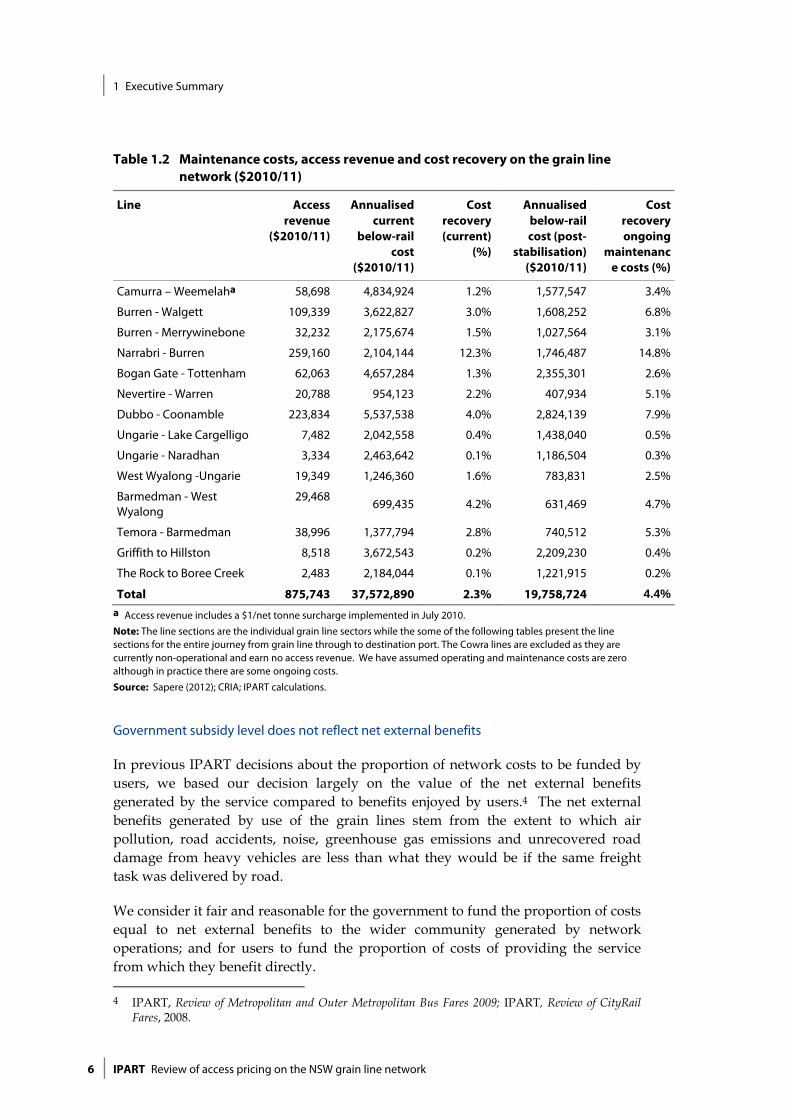

The owner and operator of the grain line network – the Country Rail Infrastructure Authority (CRIA), an agency within Transport for NSW – recovers about 2.3% of the current costs it incurs in operating and maintaining the network through access revenue. It relies on government subsidies to fund the remaining 97.7% of these costs (see Table 1.2), including a substantial capital investment of around $145 million ($2011/12) to 2020 to stabilise the lines at their current operating standard. This is on top of the annual investment of $20.4 million ($2011/12) for ongoing maintenance.

Post-stabilisation in 2020, we calculate that the government will recover 4.4% of ongoing maintenance costs at current access prices. In particular, some lines will recover less than 1% of ongoing maintenance costs. This low level of cost recovery is not sustainable and in the past, has led to lengthy periods of poor service levels, uncertainty and underinvestment in the rail supply chain.

1 Executive Summary

6 IPART Review of access pricing on the NSW grain line network

Table 1.2 Maintenance costs, access revenue and cost recovery on the grain line network ($2010/11)

Line Access revenue

($2010/11)

Annualised current

below-rail cost

($2010/11)

Cost recovery (current)

(%)

Annualised below-rail cost (post-

stabilisation) ($2010/11)

Cost recovery ongoing

maintenance costs (%)

Camurra – Weemelaha 58,698 4,834,924 1.2% 1,577,547 3.4%

Burren - Walgett 109,339 3,622,827 3.0% 1,608,252 6.8%

Burren - Merrywinebone 32,232 2,175,674 1.5% 1,027,564 3.1%

Narrabri - Burren 259,160 2,104,144 12.3% 1,746,487 14.8%

Bogan Gate - Tottenham 62,063 4,657,284 1.3% 2,355,301 2.6%

Nevertire - Warren 20,788 954,123 2.2% 407,934 5.1%

Dubbo - Coonamble 223,834 5,537,538 4.0% 2,824,139 7.9%

Ungarie - Lake Cargelligo 7,482 2,042,558 0.4% 1,438,040 0.5%

Ungarie - Naradhan 3,334 2,463,642 0.1% 1,186,504 0.3%

West Wyalong -Ungarie 19,349 1,246,360 1.6% 783,831 2.5%

Barmedman - West Wyalong

29,468 699,435 4.2% 631,469 4.7%

Temora - Barmedman 38,996 1,377,794 2.8% 740,512 5.3%

Griffith to Hillston 8,518 3,672,543 0.2% 2,209,230 0.4%

The Rock to Boree Creek 2,483 2,184,044 0.1% 1,221,915 0.2%

Total 875,743 37,572,890 2.3% 19,758,724 4.4%

a Access revenue includes a $1/net tonne surcharge implemented in July 2010.

Note: The line sections are the individual grain line sectors while the some of the following tables present the line sections for the entire journey from grain line through to destination port. The Cowra lines are excluded as they are currently non-operational and earn no access revenue. We have assumed operating and maintenance costs are zero although in practice there are some ongoing costs.

Source: Sapere (2012); CRIA; IPART calculations.

Government subsidy level does not reflect net external benefits

In previous IPART decisions about the proportion of network costs to be funded by users, we based our decision largely on the value of the net external benefits generated by the service compared to benefits enjoyed by users.4 The net external benefits generated by use of the grain lines stem from the extent to which air pollution, road accidents, noise, greenhouse gas emissions and unrecovered road damage from heavy vehicles are less than what they would be if the same freight task was delivered by road.

We consider it fair and reasonable for the government to fund the proportion of costs equal to net external benefits to the wider community generated by network operations; and for users to fund the proportion of costs of providing the service from which they benefit directly. 4 IPART, Review of Metropolitan and Outer Metropolitan Bus Fares 2009; IPART, Review of CityRail

Fares, 2008.

1 Executive Summary

Review of access pricing on the NSW grain line network IPART 7

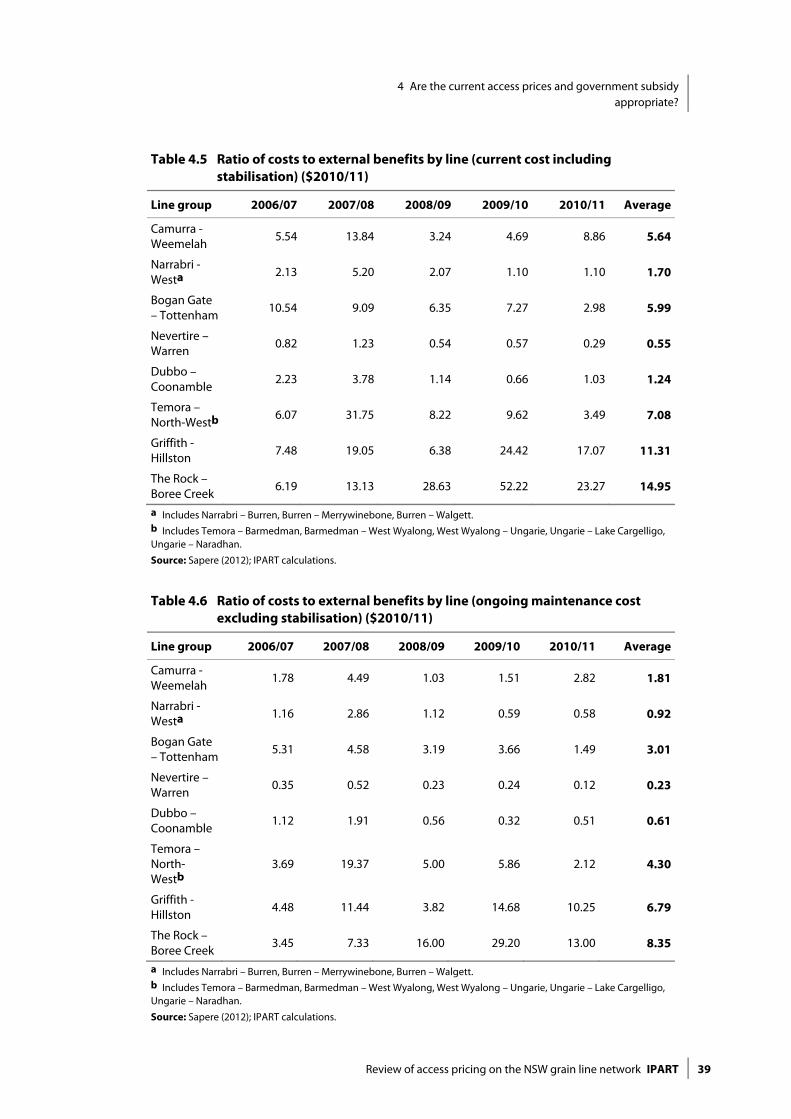

External benefits are not generated by the existence of the network itself, but depend on the degree of use of the network. As such, they vary substantially by harvest (year) and by line. Our analysis shows that using historical volumes of grain and general freight on the network over the last 5 years as a proxy for expected volumes in the next 5 years, costs are 2.7 times higher than the net external benefits generated at current access prices. Expected future ongoing maintenance costs would still be 1.4 times higher than net external benefits.

Our findings indicate that the current government subsidy on the lines is too high. While some level of government subsidy is appropriate; our analysis suggests that the current subsidy is considerably greater than the external benefits to the wider community and that the user contribution to maintenance costs should increase.

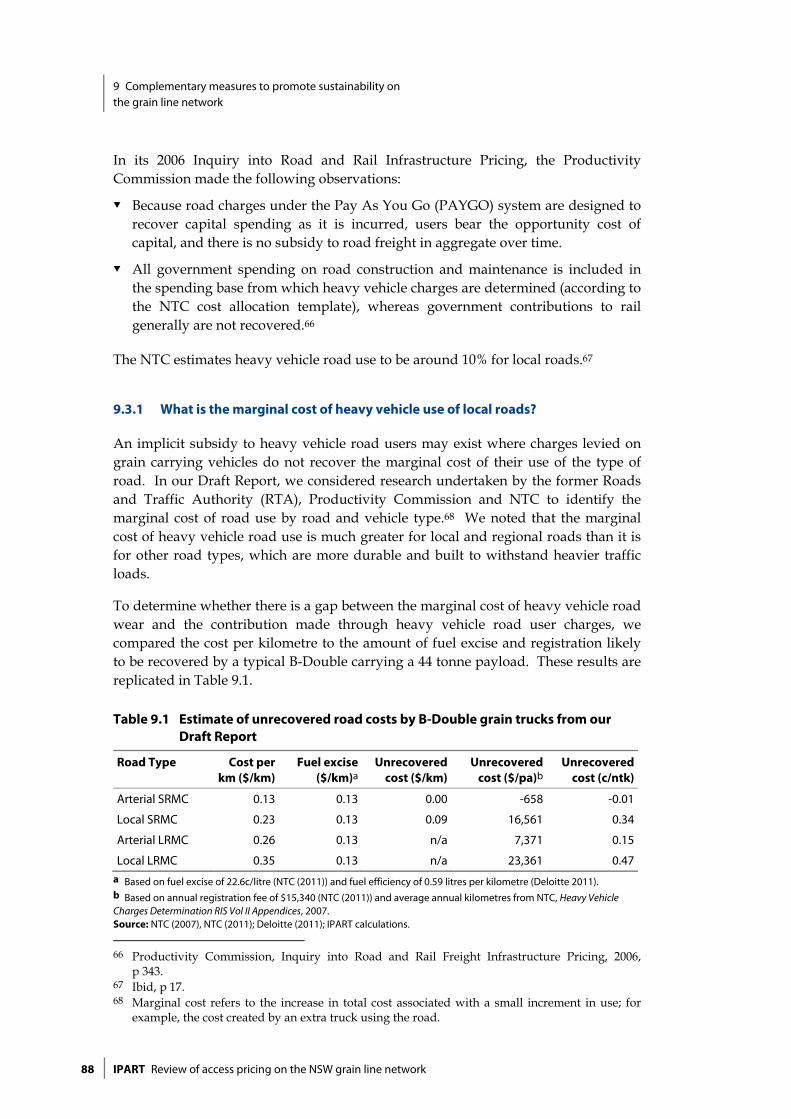

Cost recovery is not likely to be improved through other means

In submissions and at our roundtable, stakeholders suggested that cost recovery could be increased through alternative means including:

reducing below-rail maintenance costs

increasing the amount of traffic on the lines

track upgrades as a mechanism to reduce operating costs and attract additional demand.

We considered the merits of these options and determined that none of them have the potential to increase access revenue by any meaningful amount. Therefore, as a first step towards improving sustainability, we consider that access prices need to increase so that users fund a greater proportion of maintenance costs.

1.3.2 Why have we recommended an increase to $5.22 per thousand gross tonne kilometres?

Unlike public transport services, the grain line network is not a large natural monopoly. It faces direct competition from road for the grain transportation task. Achieving user cost recovery in line with the average proportion of benefits of the network enjoyed by users may force considerable volumes of grain traffic onto roads.

Throughout this review, stakeholders have argued strongly and unanimously that any increase in access prices should not remove rail’s cost advantage over road for transporting grain, so as not to shift current grain traffic from rail to road. We accept that this is a widespread concern and have designed our approach to ensure that the cost advantage of transporting grain on the grain line network is maintained as a result of our recommended access price, noting that this cost advantage is the result of a substantial government subsidy.

1 Executive Summary

8 IPART Review of access pricing on the NSW grain line network

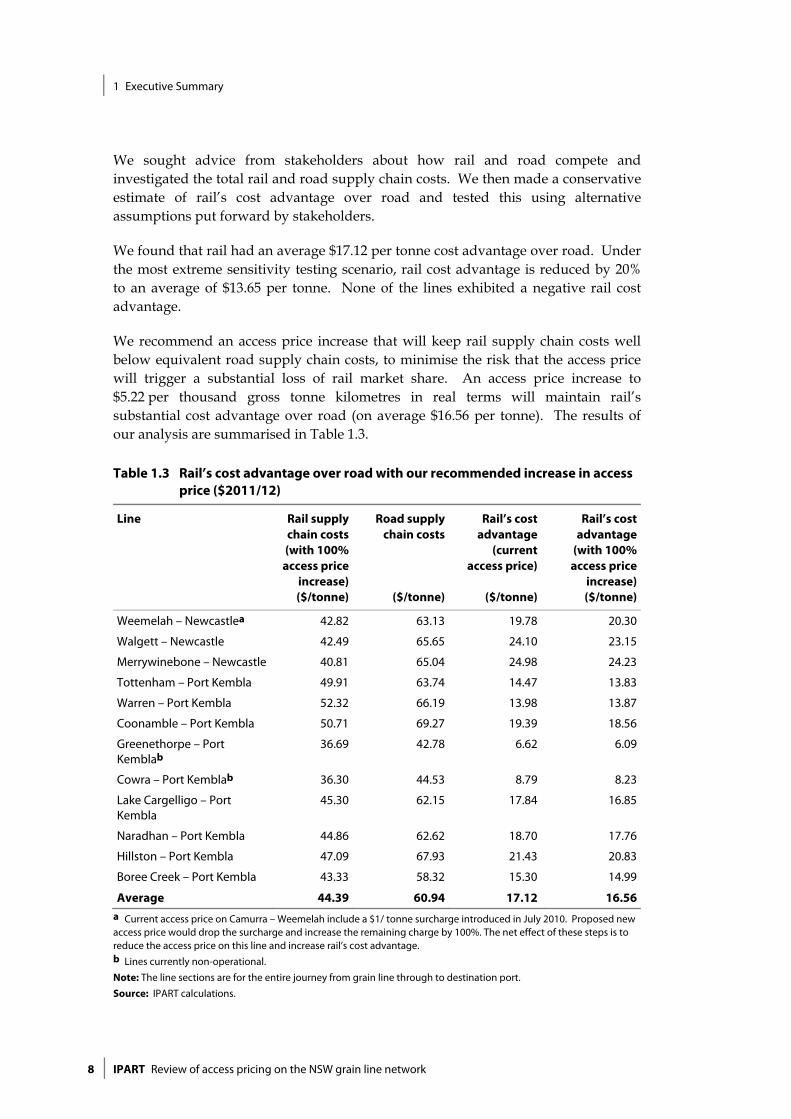

We sought advice from stakeholders about how rail and road compete and investigated the total rail and road supply chain costs. We then made a conservative estimate of rail’s cost advantage over road and tested this using alternative assumptions put forward by stakeholders.

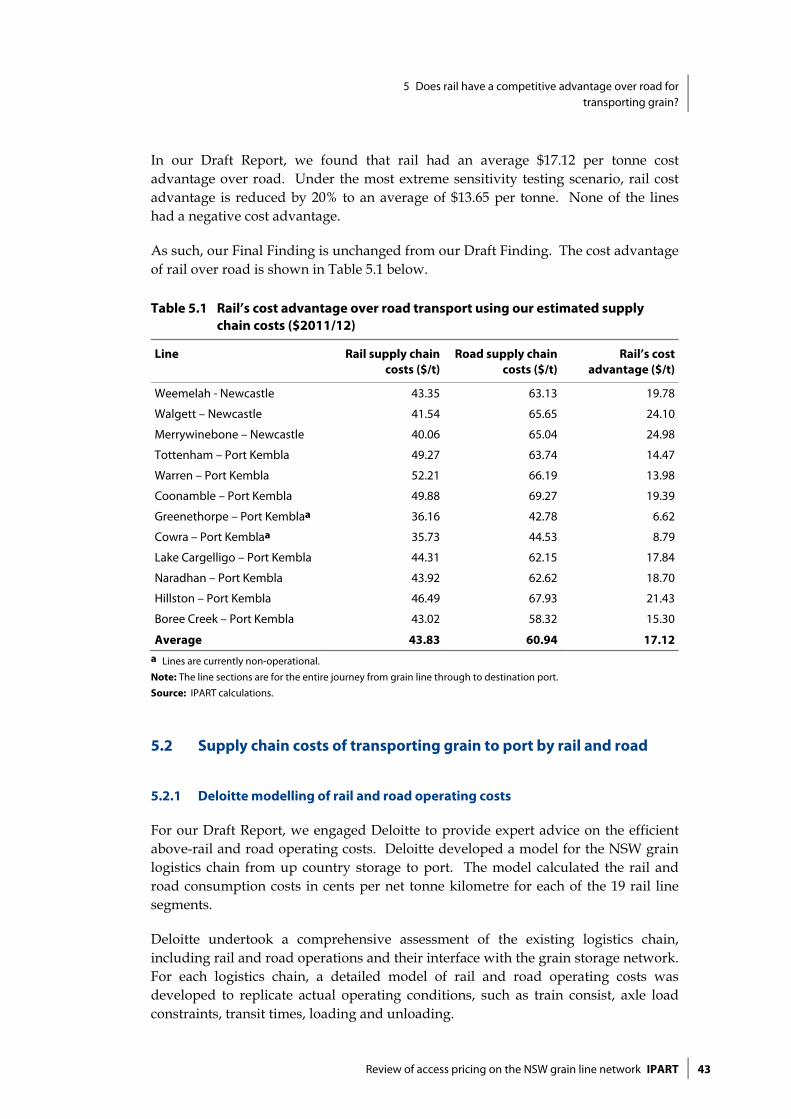

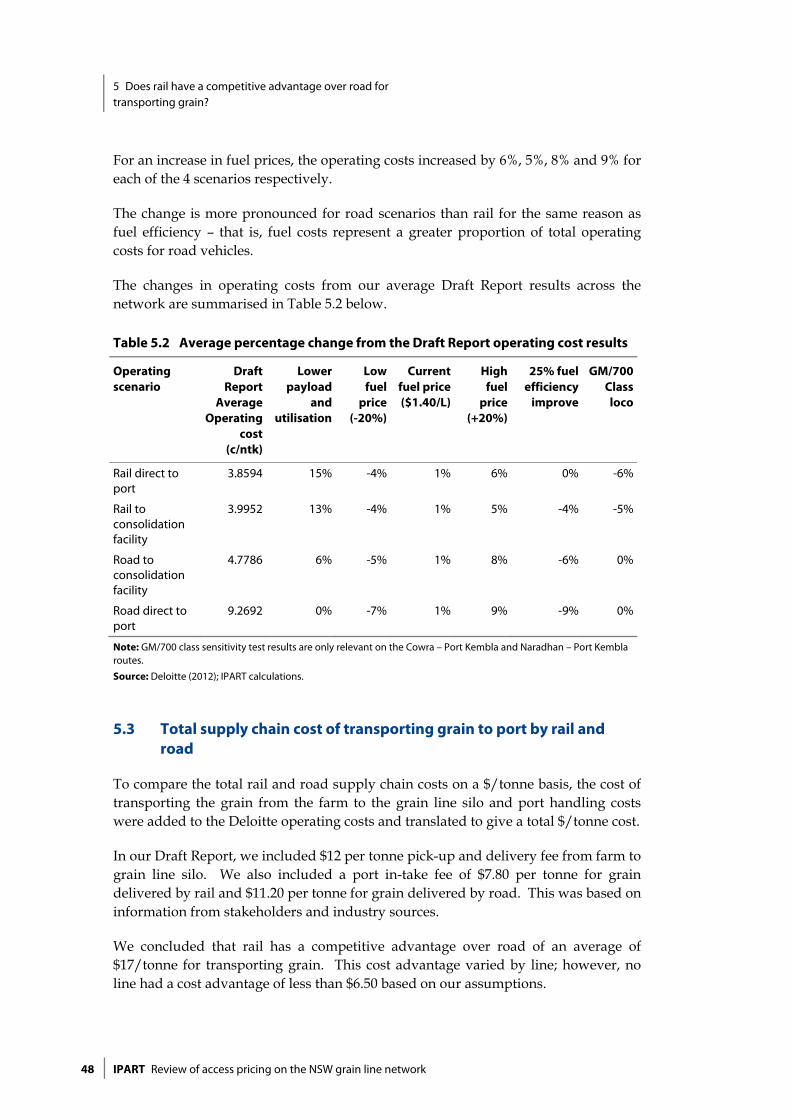

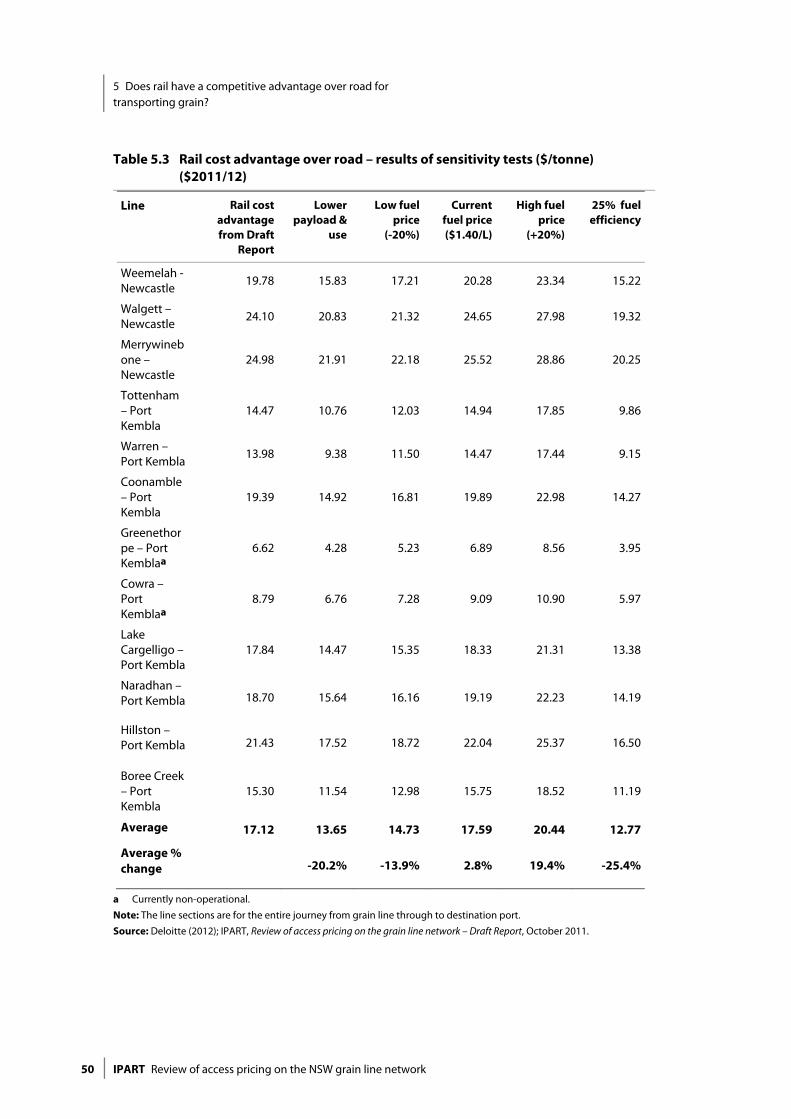

We found that rail had an average $17.12 per tonne cost advantage over road. Under the most extreme sensitivity testing scenario, rail cost advantage is reduced by 20% to an average of $13.65 per tonne. None of the lines exhibited a negative rail cost advantage.

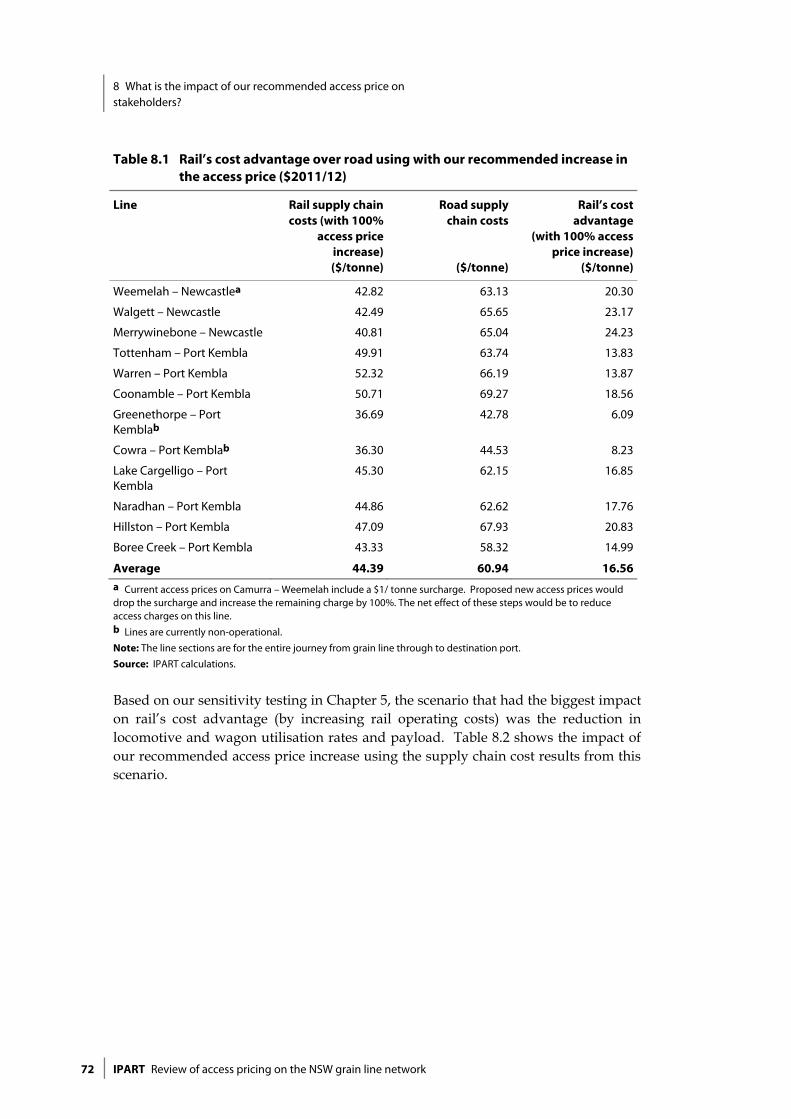

We recommend an access price increase that will keep rail supply chain costs well below equivalent road supply chain costs, to minimise the risk that the access price will trigger a substantial loss of rail market share. An access price increase to $5.22 per thousand gross tonne kilometres in real terms will maintain rail’s substantial cost advantage over road (on average $16.56 per tonne). The results of our analysis are summarised in Table 1.3.

Table 1.3 Rail’s cost advantage over road with our recommended increase in access price ($2011/12)

Line Rail supply chain costs (with 100%

access price increase) ($/tonne)

Road supply chain costs

($/tonne)

Rail’s cost advantage

(current access price)

($/tonne)

Rail’s cost advantage

(with 100% access price

increase) ($/tonne)

Weemelah – Newcastlea 42.82 63.13 19.78 20.30

Walgett – Newcastle 42.49 65.65 24.10 23.15

Merrywinebone – Newcastle 40.81 65.04 24.98 24.23

Tottenham – Port Kembla 49.91 63.74 14.47 13.83

Warren – Port Kembla 52.32 66.19 13.98 13.87

Coonamble – Port Kembla 50.71 69.27 19.39 18.56

Greenethorpe – Port Kemblab

36.69 42.78 6.62 6.09

Cowra – Port Kemblab 36.30 44.53 8.79 8.23

Lake Cargelligo – Port Kembla

45.30 62.15 17.84 16.85

Naradhan – Port Kembla 44.86 62.62 18.70 17.76

Hillston – Port Kembla 47.09 67.93 21.43 20.83

Boree Creek – Port Kembla 43.33 58.32 15.30 14.99

Average 44.39 60.94 17.12 16.56 a Current access price on Camurra – Weemelah include a $1/ tonne surcharge introduced in July 2010. Proposed new access price would drop the surcharge and increase the remaining charge by 100%. The net effect of these steps is to reduce the access price on this line and increase rail’s cost advantage. b Lines currently non-operational.

Note: The line sections are for the entire journey from grain line through to destination port.

Source: IPART calculations.

1 Executive Summary

Review of access pricing on the NSW grain line network IPART 9

Based on stakeholder feedback, we recommend a simplified price structure and publication of prices to provide users with transparency and certainty about the costs of using the network and how these costs will change over time. We recommend that the same access price be charged for grain and non-grain freight using the network.

1.3.3 What is the impact of our recommended access price increase on stakeholders?

Impact on rail users

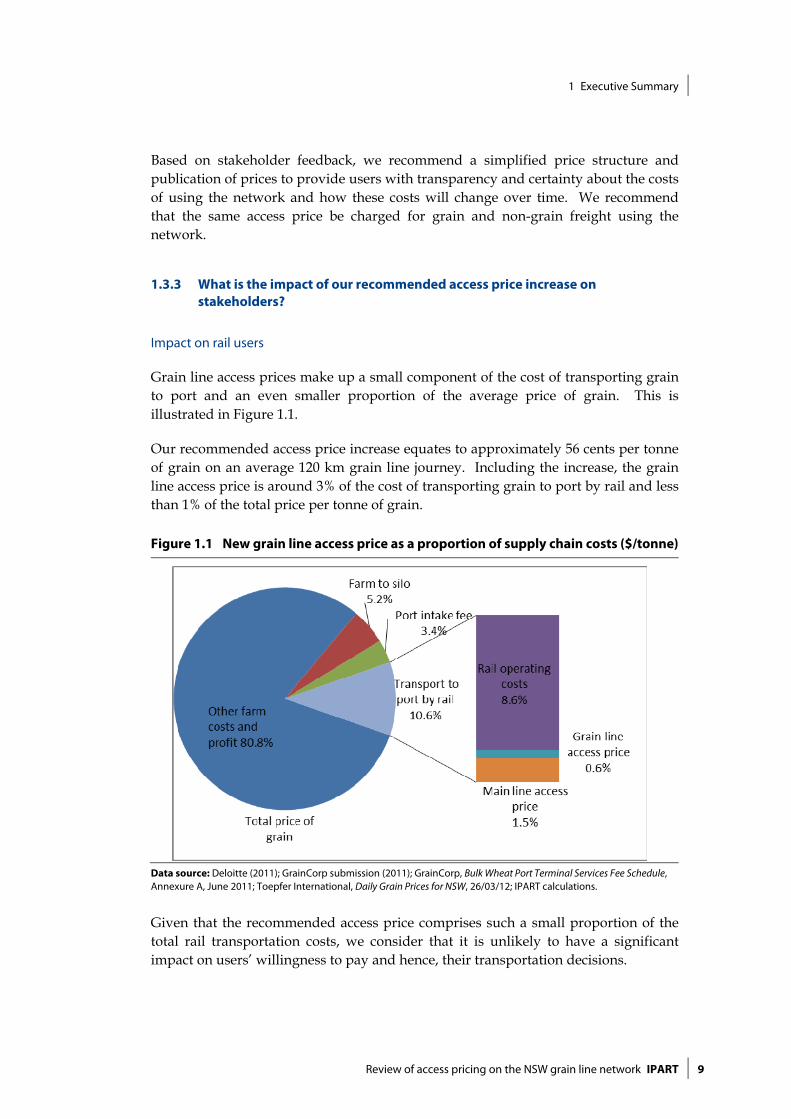

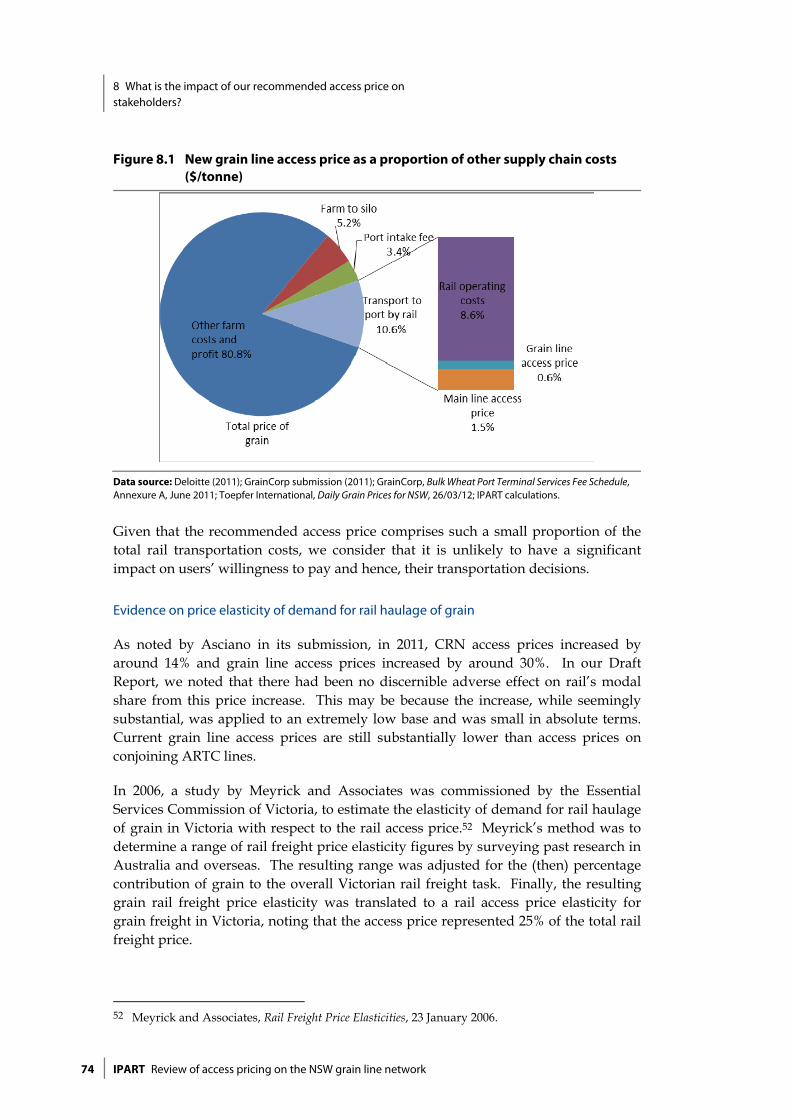

Grain line access prices make up a small component of the cost of transporting grain to port and an even smaller proportion of the average price of grain. This is illustrated in Figure 1.1.

Our recommended access price increase equates to approximately 56 cents per tonne of grain on an average 120 km grain line journey. Including the increase, the grain line access price is around 3% of the cost of transporting grain to port by rail and less than 1% of the total price per tonne of grain.

Figure 1.1 New grain line access price as a proportion of supply chain costs ($/tonne)

Data source: Deloitte (2011); GrainCorp submission (2011); GrainCorp, Bulk Wheat Port Terminal Services Fee Schedule, Annexure A, June 2011; Toepfer International, Daily Grain Prices for NSW, 26/03/12; IPART calculations.

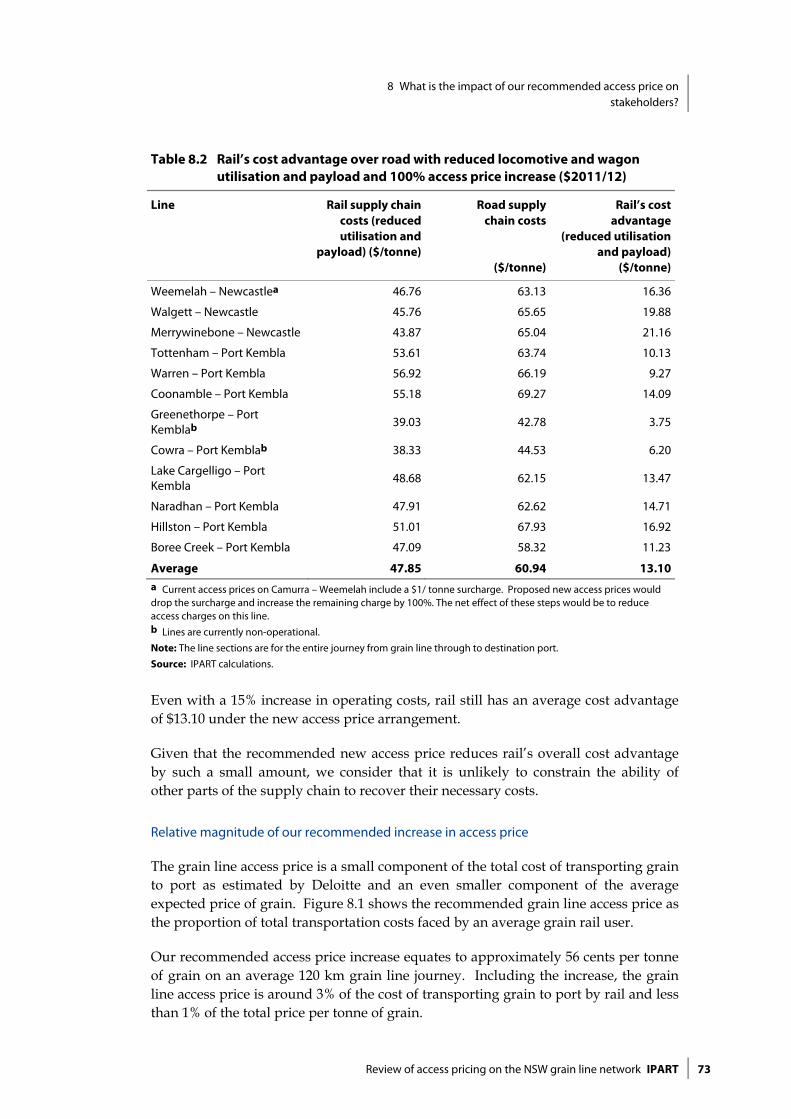

Given that the recommended access price comprises such a small proportion of the total rail transportation costs, we consider that it is unlikely to have a significant impact on users’ willingness to pay and hence, their transportation decisions.

1 Executive Summary

10 IPART Review of access pricing on the NSW grain line network

Impact on government cost recovery

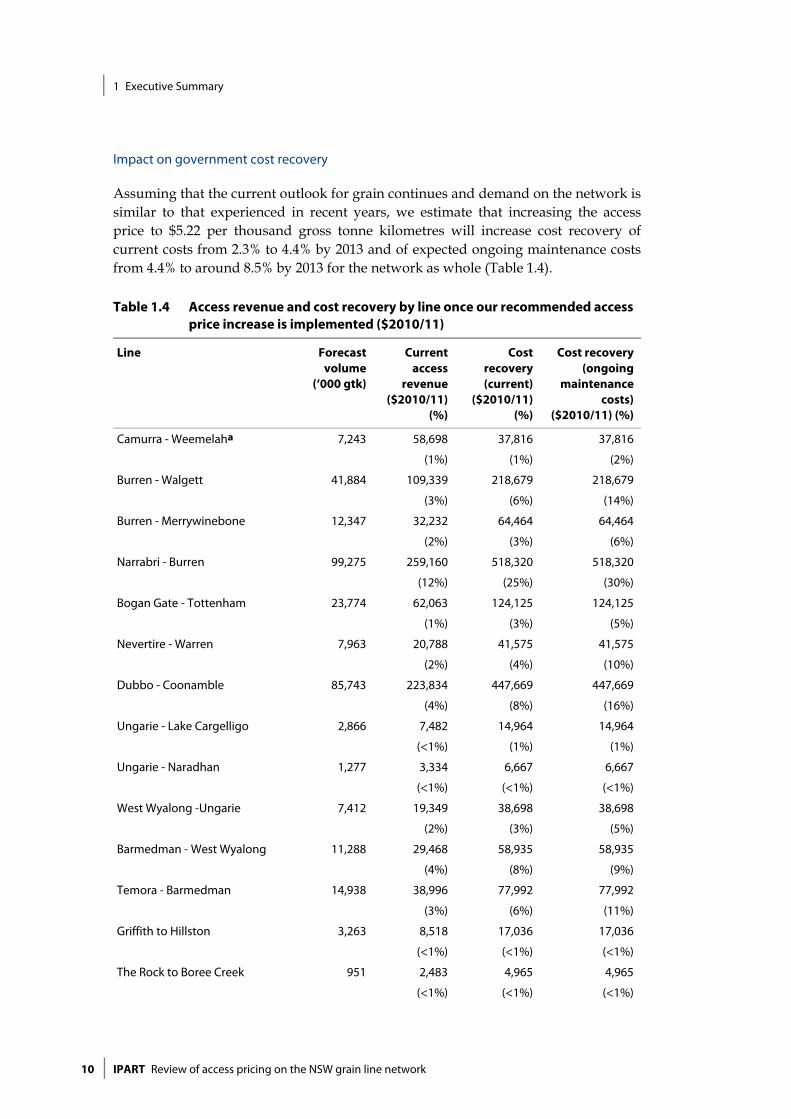

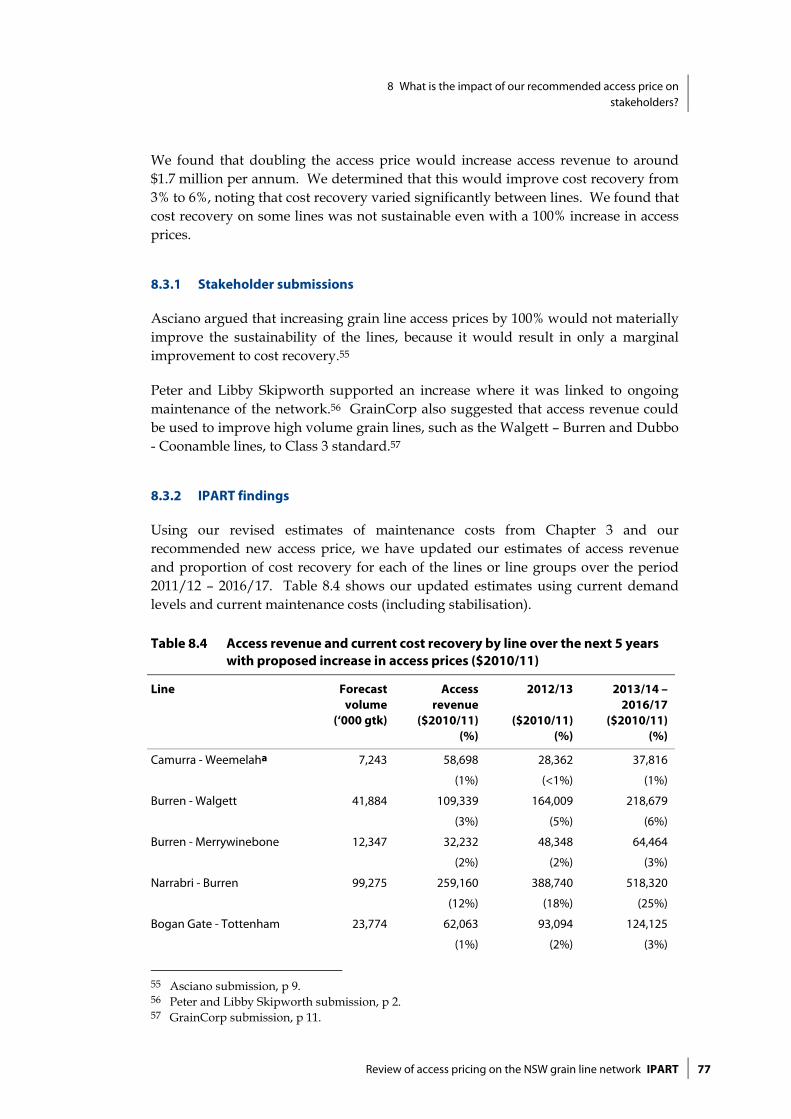

Assuming that the current outlook for grain continues and demand on the network is similar to that experienced in recent years, we estimate that increasing the access price to $5.22 per thousand gross tonne kilometres will increase cost recovery of current costs from 2.3% to 4.4% by 2013 and of expected ongoing maintenance costs from 4.4% to around 8.5% by 2013 for the network as whole (Table 1.4).

Table 1.4 Access revenue and cost recovery by line once our recommended access price increase is implemented ($2010/11)

Line Forecast volume

(‘000 gtk)

Current access

revenue ($2010/11)

(%)

Cost recovery (current)

($2010/11) (%)

Cost recovery (ongoing

maintenance costs)

($2010/11) (%)

Camurra - Weemelaha 7,243 58,698

(1%)

37,816

(1%)

37,816

(2%)

Burren - Walgett 41,884 109,339

(3%)

218,679

(6%)

218,679

(14%)

Burren - Merrywinebone 12,347 32,232

(2%)

64,464

(3%)

64,464

(6%)

Narrabri - Burren 99,275 259,160

(12%)

518,320

(25%)

518,320

(30%)

Bogan Gate - Tottenham 23,774 62,063

(1%)

124,125

(3%)

124,125

(5%)

Nevertire - Warren 7,963 20,788

(2%)

41,575

(4%)

41,575

(10%)

Dubbo - Coonamble 85,743 223,834

(4%)

447,669

(8%)

447,669

(16%)

Ungarie - Lake Cargelligo 2,866 7,482

(<1%)

14,964

(1%)

14,964

(1%)

Ungarie - Naradhan 1,277 3,334

(<1%)

6,667

(<1%)

6,667

(<1%)

West Wyalong -Ungarie 7,412 19,349

(2%)

38,698

(3%)

38,698

(5%)

Barmedman - West Wyalong 11,288 29,468

(4%)

58,935

(8%)

58,935

(9%)

Temora - Barmedman 14,938 38,996

(3%)

77,992

(6%)

77,992

(11%)

Griffith to Hillston 3,263 8,518

(<1%)

17,036

(<1%)

17,036

(<1%)

The Rock to Boree Creek 951 2,483

(<1%)

4,965

(<1%)

4,965

(<1%)

1 Executive Summary

Review of access pricing on the NSW grain line network IPART 11

Line Forecast volume

(‘000 gtk)

Current access

revenue ($2010/11)

(%)

Cost recovery (current)

($2010/11) (%)

Cost recovery (ongoing

maintenance costs)

($2010/11) (%)

Total

320,224 875,743

(2.3%)

1,671,906

(4.4%)

1,671,906

(8.5%)

Line Group

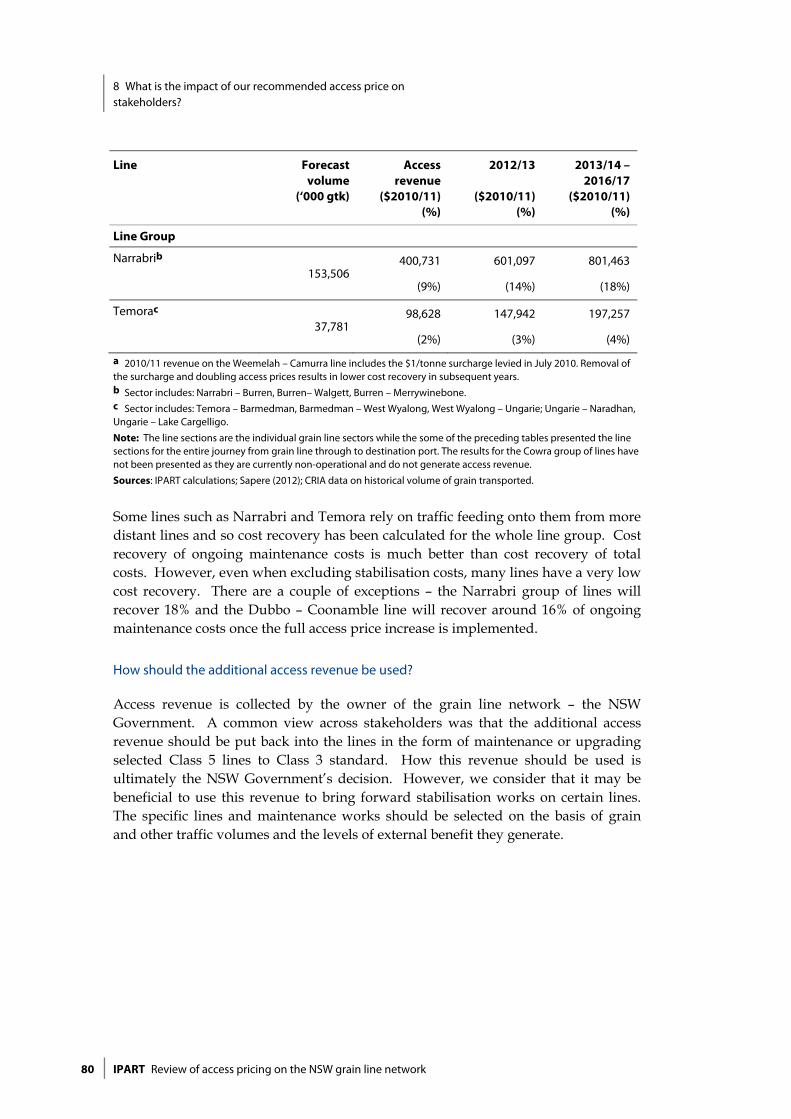

Narrabrib 153,506 400,731

(5%)

801,463

(10%)

801,463

(18%)

Temorac 37,781 98,628

(1%)

197,257

(2%)

197,257

(4%)

a 2010/11 revenue on the Weemelah – Camurra line includes the $1/tonne surcharge levied in July 2010. Removal of the surcharge and doubling access prices results in lower cost recovery in subsequent years. b Sector includes: Narrabri – Burren, Burren– Walgett, Burren – Merrywinebone. c Sector includes: Temora – Barmedman, Barmedman – West Wyalong, West Wyalong – Ungarie; Ungarie – Naradhan, Ungarie – Lake Cargelligo.

Note: The lines are the individual grain line sectors while the some of the following tables present the line sections for the entire journey from grain line through to destination port. The results for the Cowra group of lines have not been presented as they are currently non-operational and do not generate access revenue.

Sources: IPART calculations; CRIA data on historical volume of grain transported.

Cost recovery varies considerably by line and line group with some lines continuing to recover 2% or less of costs. Some lines such as Narrabri and Temora rely on traffic feeding onto them from more distant lines and so cost recovery has been calculated for the whole line group.

1.3.4 Will an access price increase to $5.22 per thousand gross tonne kilometres make the grain line network sustainable?

We consider that our recommended pricing arrangements will help promote the sustainability of some lines. However, lines that barely contribute to operating and maintenance costs after a 100% increase in the access price may not be sustainable in the longer-term and warrant consideration of whether there is a lower cost transport solution. It is a matter for the NSW Government to decide what should be done about these lines. However, we recommend that any decision about future rail subsidies should include an economic cost-benefit analysis that considers the merits of road and rail transport projects on an equitable basis.

For higher volume lines, the recommended increase in access price will enable a greater share of costs to be recovered from users without triggering a significant shift in grain traffic from rail to road. Yet even for these higher volume lines, CRIA will continue to need a substantial government subsidy to fund the ongoing maintenance costs.

1 Executive Summary

12 IPART Review of access pricing on the NSW grain line network

1.4 Overview of other complementary recommendations

We have recommended some other complementary measures to assist in delivering improvements to the sustainability of the network. These measures include:

Industry coordination - through a more structured and collaborative approach to decision making on the network between the below and above-rail operators and industry stakeholders.

Mode-neutral freight strategy - we support the NSW Government’s goal in its NSW 2021 plan to invest in strategic and coordinated infrastructure. We consider that the plan should be mode-neutral and identify the best transport options in selected regional routes, rather than funding competing rail and road infrastructure.

Line viability – for lines that have a low cost recovery and external benefit outlook, the NSW Government should consider the best transport solution via a comprehensive demonstration of the costs and benefits prior to any future capital investment.

Road cost offset – for rail lines that are not the best transport option following the NSW Government’s analysis, the funding earmarked for maintaining these lines could be used to offset any increased road maintenance costs or to bring forward stabilisation works on more viable lines.

Heavy vehicle road user charging - while recognising that heavy vehicles may pay for their use of roads in aggregate, reforms are required to ensure that these charges better reflect the actual costs of use of different types and locations of roads. This will enable more transparent decisions about government subsidies to road and rail.

1.5 What is the structure of this report?

The following chapters and appendices explain our final findings and recommendations in detail:

Chapter 2 discusses the context for the review, including the grain line network, key stakeholders, problems facing the network and outcomes from previous reviews.

Chapter 3 identifies the efficient costs of maintaining the network including stabilisation costs and ongoing maintenance costs post-2020.

Chapter 4 assesses whether the user contribution to current and expected future ongoing maintenance costs are appropriate.

Chapter 5 explains our final findings on how the costs of the rail and road supply chains compare and tests the impact of varying assumptions.

Chapter 6 considers whether there are non-price solutions to increase cost recovery.

1 Executive Summary

Review of access pricing on the NSW grain line network IPART 13

Chapter 7 explains our final findings on the extent to which access prices could be increased without eroding rail’s cost advantage as well as appropriate access pricing arrangements and implementation.

Chapter 8 assesses the impact of our final recommendations on rail users and government cost recovery.

Chapter 9 discusses our final recommendations on complementary reforms to improve the sustainability of the network including the current regulatory arrangements, heavy vehicle user charging and future funding of road and rail transport projects.

Appendices 1-5 provide background information and a glossary of terms.

1.6 A complete list of our recommendations.

We recommend that:

1 Any future upgrades of grain lines to a Class 2 standard or higher should be: 58

– negotiated on the basis of a comprehensive cost benefit analysis that includes consideration of non-grain traffic 58

– funded primarily by the parties to whom the benefits accrue, through an appropriate funding mechanism. 58

2 An increase of the grain line access price to $5.22 per thousand tonne kilometres provides a good balance between improving cost recovery and maintaining rail’s modal share in the short-term. 61

3 At the end of the 5-year period, the NSW Government could review the access price to determine whether there is scope to increase it to a level that is more commensurate with user share of benefits, taking into account constraints from road competition amongst other factors. 62

4 The access price structure should be simplified so that a single variable access price is applied across all lines. 66

5 The access price should be published. 66

6 The access price should apply to all traffic that uses the grain line network, including non-grain freight. 66

7 The access price increase should be phased in over 2 years. 67

8 Should the NSW Government pursue a review of the regulatory arrangements for some or all of the grain lines; it would be prudent to extend that review to incorporate the current regulatory and structural arrangements that apply to the

1 Executive Summary

14 IPART Review of access pricing on the NSW grain line network

NSW Government’s ownership interests in the greater CRN and Hunter Valley rail network. 83

9 The NSW Government should consider the establishment of an industry coordination forum to facilitate greater coordination of operations and investment in the network. The forum could advise on maintenance priorities, investment decisions and funding contributions. 87

10 Further analysis on the long-run marginal costs of road wear caused by heavy vehicles that transport grain is required to understand the overall government subsidy to road and rail freight transport infrastructure. 90

11 The NSW Government should continue to pursue national reforms to national heavy vehicle charging, such that it better reflects the actual costs of heavy vehicle use of regional and local road infrastructure. 91

12 The NSW Government should take a mode-neutral approach to the future provision of subsidies for freight transport infrastructure. This should include a comprehensive demonstration of the costs and benefits for rail and road transport projects on a like basis. 95

13 Should the NSW Government decide to suspend operations on any of the current lines, the funding earmarked for maintenance on those lines could be used to offset any increased road maintenance costs or to bring forward stabilisation works on more viable lines. 95

2 Context for this review

Review of access pricing on the NSW grain line network IPART 15

2 Context for this review

This chapter provides background on the unique characteristics of the grain line network. It explains how the recommendations of previous reviews have led to this review and its scope.

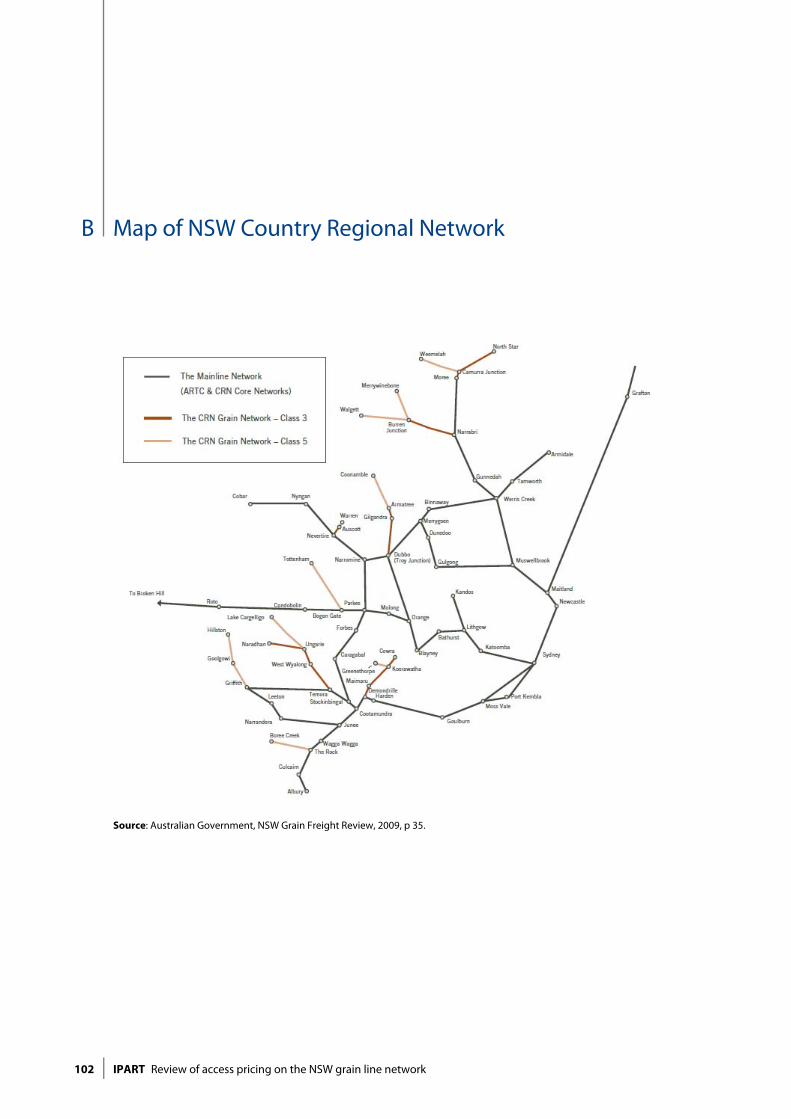

2.1 What is the grain line network?

The NSW grain line network is a collection of lines that connect the grain growing regions in the North-West, Central-West and South-West of the State to the main line rail network. A diagram of the lines is included in Appendix B. Many of the lines are over 100 years old and are mainly Class 5 and Class 3 standard, which enables them to carry only light axle locomotives at low speeds.5

In our Issues Paper, we defined the network as the 19 lines that were assessed as part of the NSW Grain Freight Review (2009). On 1 July 2011, the operation of 2 of these lines was transferred to the Australian Rail Track Corporation (ARTC) – Moree to Camurra and Camurra to North Star. As such, these 2 lines are no longer included in our review.

We also noted that the Cowra lines were no longer operational, but their potential re-opening was subject to a Ministerial Taskforce review. As such, these lines have been considered as part of our review.

CRIA also advised that following the termination of the previous management contract with ARTC, there were some minor boundary changes to the interface points between the ARTC leased network and the CRN for some grain lines. Table 2.1 provides an updated list of the grain lines considered in this review and their current classification. Table 2.2 provides a description of the line classifications.

5 See Table 2.2 for definitions.

2 Context for this review

16 IPART Review of access pricing on the NSW grain line network

Table 2.1 NSW grain line network: sectors included in the scope of our review

Region Sector code

Class Sector Route km

Northern 478 5 Weemelah to Camurra 83.7

480 3/5 Burren to Narrabri (via Wee Waa) 83.5

481 5 Walgett to Burren 88.2

482 5 Merrywinebone to Burren 52.6

Western

732 5 Tottenham to Bogan Gate 112.4

743 3/5 Warren to Nevertire (via Auscott) 20.3

761 3/5 Coonamble to Dubbo (via Gilgandra) 150.2

Southern 645 5 Boree Creek to The Rock 56.6

660 3 Koorawatha to Demondrillea 74.1

661 3 Cowra to Koorawathaa 27.3

663 3 Greenethorpe to Koorawathaa 21.5

672 3 Barmedman to Temora 36.3

673 3 West Wyalong to Barmedman 31.5

674 3 Ungarie to West Wyalong 40.4

675 5 Lake Cargelligo to Ungarie 71.4

678 3 Naradhan to Ungarie 60.4

687 5 Hillston to Griffith 108.1

Total 1,118.5 a Currently non-operational, subject to Ministerial Taskforce review.

Source: CRIA.

Table 2.2 Standard classification of lines

Class Max. axle load

(tonnes)

Max. train operating speed

(freight) (km/h)

Rail section

(km)

Nominal ballast depth (mm)

1 25 80 53/60 270

2 21 80 47 270

3 19 70 40 200

4 19 50 36 150

5 19 40 30 150

Source: Rail Infrastructure Corporation (now CRIA), Standard Classification of Lines, version 4, November 2001.

The network forms a small part of the grain supply chain for grain destined for export or domestic milling. Grain may start its journey on the grain line network, move onto the Country Regional Network (CRN) and complete the journey on the Australian Rail Track Corporation’s (ARTC) interstate network, which may also include movements on the RailCorp network. It may also complete all or part of its journey on the road network. Therefore, any changes to access prices on the grain line network will have an impact on the overall grain supply chain, including road transport operations.

2 Context for this review

Review of access pricing on the NSW grain line network IPART 17

2.2 Who are the key stakeholders?

The lines are owned by the NSW Government. CRIA, an agency within Transport for NSW, is responsible for overseeing the operation and maintenance of the lines and negotiating access arrangements with above-rail operators.

The primary operator on the lines is GrainCorp, which has an agreement with Transport for NSW to provide grain haulage services on the grain lines.

There are many other stakeholders who have an interest in the funding and governance arrangements associated with the grain lines, including: grain growers, grain handlers, above-rail operators, flour and cotton facilities, road agencies and road transport operators.

2.3 What are the key problems facing the grain line network?

The grain line network has a number of significant problems which threaten its sustainability and cause uncertainty for industry. These include:

low and variable freight volumes

low levels of cost recovery

a high reliance on government funding, which puts the maintenance and sustainability of the lines at risk of budget fluctuations and priorities

a high degree of competition with road.

2.3.1 Low and variable freight volumes

The volume of traffic on the grain lines depend primarily on grain production and the market for which grain is destined. This is because grain makes up 95% of all traffic transported on the grain lines. The other 5% of traffic is a combination of general freight (including containerised grain), minerals and some passenger traffic.

Grain is grown across NSW, but is concentrated in the western slopes and plains. Grain production depends on market and climatic conditions and varies considerably from year to year. Demand volatility is also a result of exchange rate fluctuations or global supply issues, which may have impacts on grain production in NSW.

2 Context for this review

18 IPART Review of access pricing on the NSW grain line network

NSW grain is used primarily for domestic consumption, with the remainder serving the export market. Within the domestic market grain is used for human consumption (milling) or feedstock. Each market has its own supply chain characteristics. Grain for feedstock is transported almost entirely by road due to the flexibility of this transport mode and the dispersed nature of the end-use market. The majority of grain supplying the export market and domestic human consumption is transported by rail; however, in the case of exports, this volume can fluctuate considerably as domestic demand is met first.

In response to our Issues Paper, GrainCorp provided the following transportation estimates and characteristics for each market:6

2.2 mega tonnes (Mt) domestic human and industrial market: A stable base that receives most of its grain (wheat) by rail. Major consumers include Manildra Milling, Allied Mills, and Weston Milling.

2.5 Mt animal feed market: Less stable demand, with little or no rail access, served by road transport. Consumers include feedlots, intensive livestock production, dairies and compound stockfeed producers.

0.8 Mt container export market: Stable demand facilitated by export traders, with good rail access, container trains operating from country packing facilities to Port Botany.

>2.5 Mt bulk export market: Variable demand dependent upon grain production with rail and road access into Carrington (Newcastle) and Port Kembla export elevators.

Historically, comparing a ‘drought’ year and a ‘bumper’ harvest, grain volumes transported on the grain line network have varied by as much as 50%. The variation on individual lines is even more unpredictable with volumes changing up to 175% from year to year. More information on the outlook for the NSW grain industry and its structure is in Appendix C.

2.3.2 Low cost recovery and high reliance on government funding

Maintaining the grain lines to a safe operating standard is expensive. The network is maintained at a ‘fit-for-purpose’ standard, which provides a minimum level of service for operators.7 The NSW Government subsidises around 97% of the cost of providing this level of service.

6 GrainCorp submission to Issues Paper, July 2011, p 3. 7 ‘Fit for purpose’ means that lines are able to operate to the specifications of their classification

level. For example, a Class 5 line should be able to run 19 tonne axle load trains at 40 km/h and a Class 3 line should be able to run 19 tonne axle load trains at 70km/h.

2 Context for this review

Review of access pricing on the NSW grain line network IPART 19

The current asset replacement and maintenance regime is driven by stakeholder requirements relative to the available long-term funding. The regime assumes that funding will continue to be available each year for the maintenance and renewal of assets required to maintain the existing level of service.

The extent of network maintenance is therefore subject to government budget priorities and the industry has experienced a lengthy period of uncertainty regarding the ongoing viability of the network. Where funding has not been available, many parts of the network have fallen below the fit-for-purpose standard. This has affected decisions on whether to invest in associated above-rail assets and led to various reviews of the costs and benefits of maintaining lines or optimising the network.

Throughout this review, stakeholders have expressed support for greater certainty and stability on the network and many have argued that the network plays an important role in the transport of grain in NSW. However, while the network continues to rely heavily on the continued availability of government funds, it is likely that current uncertainties about fluctuating track condition and threatened line closures will persist.

2.3.3 Competition with road

The relatively short lengths and low volumes on the grain lines, as well as the dispersed markets for grain, mean that they compete directly with the road network. Around 70% of grain destined for export or domestic milling is transported on the grain line network and the main line to port.8 The remainder is transported by road.

Past reviews of the grain supply chain have assumed that road and rail compete for the export line haul task between a silo and port. The Grain Industry Advisory Committee (GIAC) review (2004) and NSW Grain Freight Review (2009) both assumed that grain is delivered from silo to port, whether it goes by rail or road. However, some stakeholders to our review have argued that competing road movements are direct from farm to port.

A growing trend of on-farm storage, containerisation of grain and higher productivity trucks means that farm-to-port road haulage could become an increasingly competitive option for grain transportation in the future.

8 GrainCorp submission to Issues Paper, July 2011, p 5.

2 Context for this review

20 IPART Review of access pricing on the NSW grain line network

2.4 What were the outcomes of previous reviews of the grain line network?

Over the last decade, there have been a handful of government and industry led reviews to determine the future of the grain lines. In 2004, the GIAC undertook a cost-benefit analysis on the lines to determine which lines were cost-effective in the longer-term and which lines should be closed in favour of road.

The GIAC review found that cost recovery across the 15 grain lines it examined ranged from 0.8% to 6.3%, and was 3% on average. The review identified 3 lines where the cost of maintaining the line was significantly greater than the cost of upgrading the road network and 7 lines where retaining the rail line was marginally cheaper.

The NSW Government responded to these recommendations by suspending services on 4 lines and committing funding of $69 million over 3 years to keep the remaining lines open.

In 2008, it was announced as part of the NSW Government mini-budget that services would be suspended on another 5 lines. However, this decision was delayed pending the outcome of the NSW Grain Freight Review.

In 2009, the Australian Government initiated the NSW Grain Freight Review. This review considered broader issues in the NSW grain supply chain, but also conducted a cost-benefit analysis of the viability of the lines. The review found that cost recovery was around 6% across the network, but recommended that most lines be stabilised at a fit-for-purpose standard. The review recommended that access charges should be reviewed to determine an appropriate level of user contribution to ongoing maintenance.

Since the NSW Grain Freight Review there have been various changes in the grain supply chain; most notably the industry adjustment to the removal of the AWB single-desk marketing monopoly. During the single desk regime, grain for domestic use and export was transported almost entirely by rail. The market now allows for multiple competing grain handlers and grain growers to make strategic decisions about where they sell their grain and the way grain is transported. This has led to a more competitive market for grain transport.

3 What are the costs of maintaining the network and what proportion is recovered from users?

Review of access pricing on the NSW grain line network IPART 21

3 What are the costs of maintaining the network and what proportion is recovered from users?

The first step in determining the cost recovery on the network is identifying the efficient costs of maintaining the network. This chapter examines the expected costs of maintaining the network to 2020 and beyond, including the capital investment required to stabilise the lines.

Based on actual access revenue received in 2010/11, we compute the current level of cost recovery and examine the expected level of cost recovery of ongoing maintenance costs once stabilisation is complete.

3.1 Final Findings

IPART finding

1 The average cost of maintaining the grain line network up until 2020 is $38,911 per track kilometre or $38.5 million per annum. This includes an annual capital investment of $18.1 million for stabilisation ($2011/12).

2 Post-2020, the average cost of ongoing maintenance of the grain line network is $20,608 per track kilometre or $20.4 million per annum ($2011/12).

3 At current access prices and demand levels, 2.3% of current costs and 4.4% of ongoing maintenance costs are recovered from network users with the remainder being funded by government subsidy.

Since the Draft Report, we received detailed data on estimated network maintenance costs from CRIA. From this information and based on feedback from submissions, we estimated the efficient cost of ongoing maintenance and capital investment required for stabilisation. We have updated our estimates of cost recovery on the network based on both estimates of costs.

3.2 What are the efficient below-rail costs of the network?

In our Draft Report, we noted that we had not received detailed information about future maintenance costs from CRIA in time to include them in our analysis.

Instead, we compared a range of publicly available estimates and estimated the below-rail cost of maintaining the network to be around $26,350 per kilometre per

3 What are the costs of maintaining the network and what proportion is recovered from users?

22 IPART Review of access pricing on the NSW grain line network

annum. This estimate was derived from actual historical maintenance expenditure, taking into account likely future efficiency improvements.

3.2.1 Stakeholder submissions

Some stakeholders raised the point that our estimate of below-rail costs in the Draft Report did not take into account the underlying condition of the track. As such, there could be scope for maintenance cost savings going forward.

Peter and Libby Skipworth stated that an increase in maintenance following a period of poor maintenance history and the impacts of natural disaster mean that current costs may be substantially higher than they would be under a regular maintenance schedule.9 Asciano suggested that cost savings could result from the new management contract with John Holland, which was awarded following a competitive tender process.10

NSW Farmers noted that the NSW Grain Freight Review (2009) recommended that a majority of lines should be stabilised at a minimum standard of operation, with these stabilisation costs to be funded by the NSW Government through a non-recoverable grant. The recommendations were subsequently agreed to by the former NSW Government in its preliminary response to the review. NSW Farmers pointed out that the below-rail costs used in the Draft Report did not distinguish between stabilisation and ongoing maintenance costs.11

NSW Farmers also suggested that estimated costs should be tested against those from rail operations in other jurisdictions.12

3.2.2 IPART’s findings

Following the release of the Draft Report, we sought further information from CRIA about the costs of maintaining the grain lines. We sought to identify the component of costs that result from stabilisation works compared to future ongoing maintenance costs post-stabilisation.

CRIA provided IPART with its estimation of projected costs by line based on its long-term Total Asset Management (TAM) plan. The costs are categorised into routine maintenance (RM) and major periodic maintenance (MPM) of structures and track. They include direct costs such as labour, materials and plant as well as a reasonable margin to cover necessary overheads. They do not include project management, depot or transportations costs, although these would also form valid components of service delivery.

9 Peter and Libby Skipworth submission, p 1. 10 Asciano submission, p 9. 11 NSW Farmers submission, p 1. 12 Ibid, p 2.

3 What are the costs of maintaining the network and what proportion is recovered from users?

Review of access pricing on the NSW grain line network IPART 23

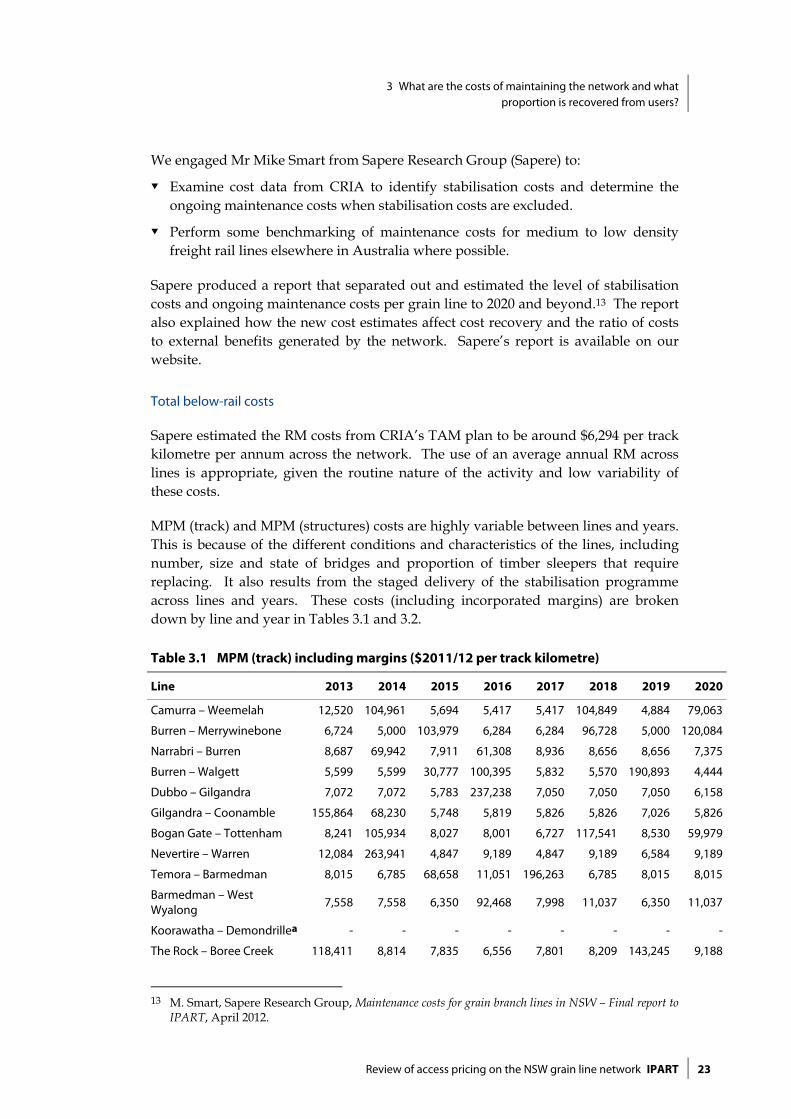

We engaged Mr Mike Smart from Sapere Research Group (Sapere) to:

Examine cost data from CRIA to identify stabilisation costs and determine the ongoing maintenance costs when stabilisation costs are excluded.

Perform some benchmarking of maintenance costs for medium to low density freight rail lines elsewhere in Australia where possible.

Sapere produced a report that separated out and estimated the level of stabilisation costs and ongoing maintenance costs per grain line to 2020 and beyond.13 The report also explained how the new cost estimates affect cost recovery and the ratio of costs to external benefits generated by the network. Sapere’s report is available on our website.

Total below-rail costs

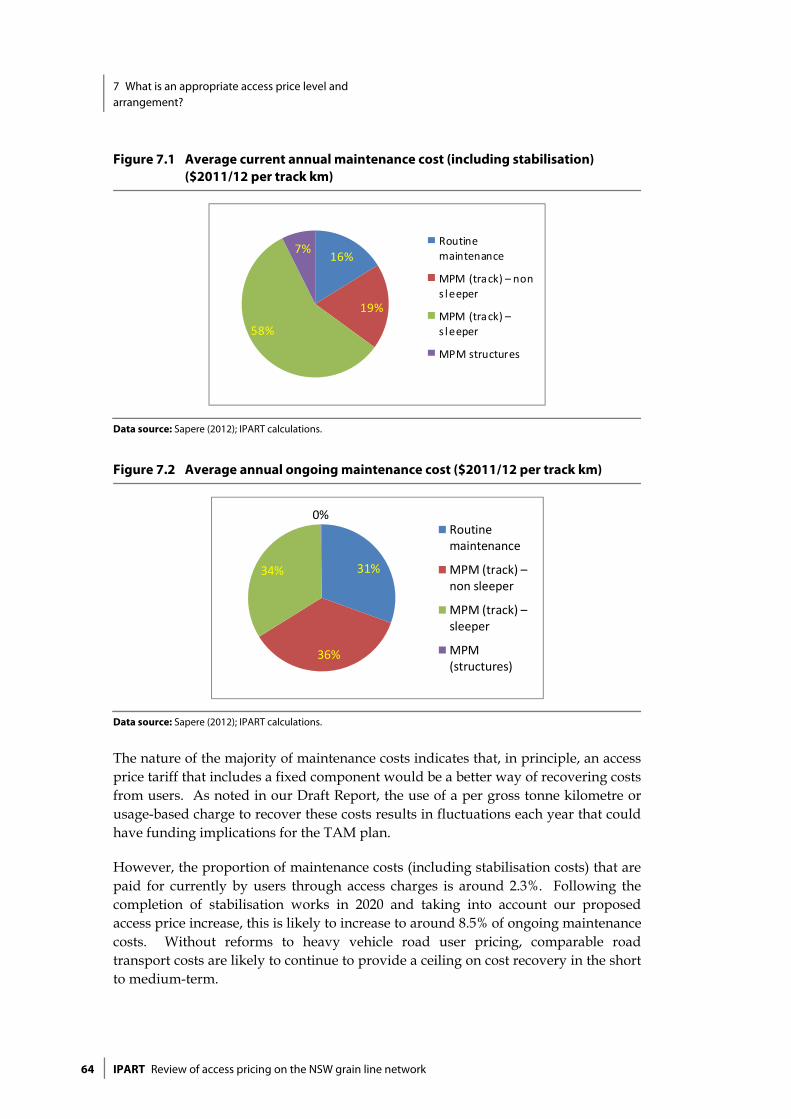

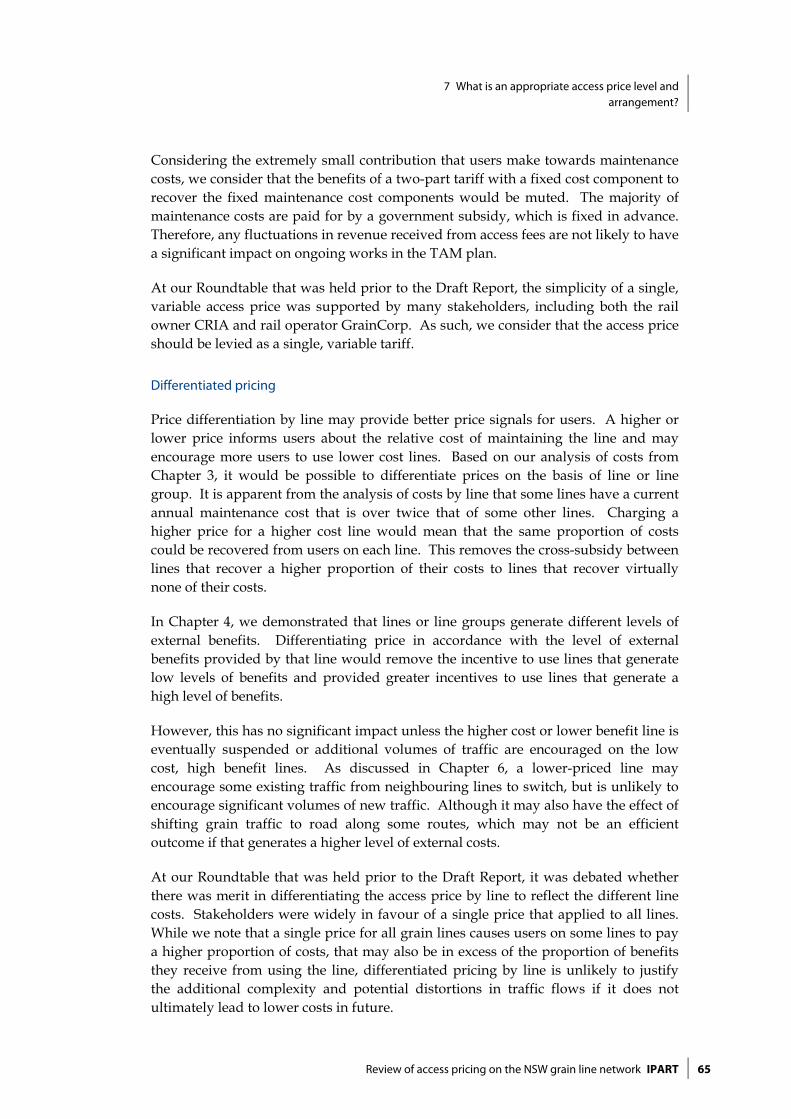

Sapere estimated the RM costs from CRIA’s TAM plan to be around $6,294 per track kilometre per annum across the network. The use of an average annual RM across lines is appropriate, given the routine nature of the activity and low variability of these costs.

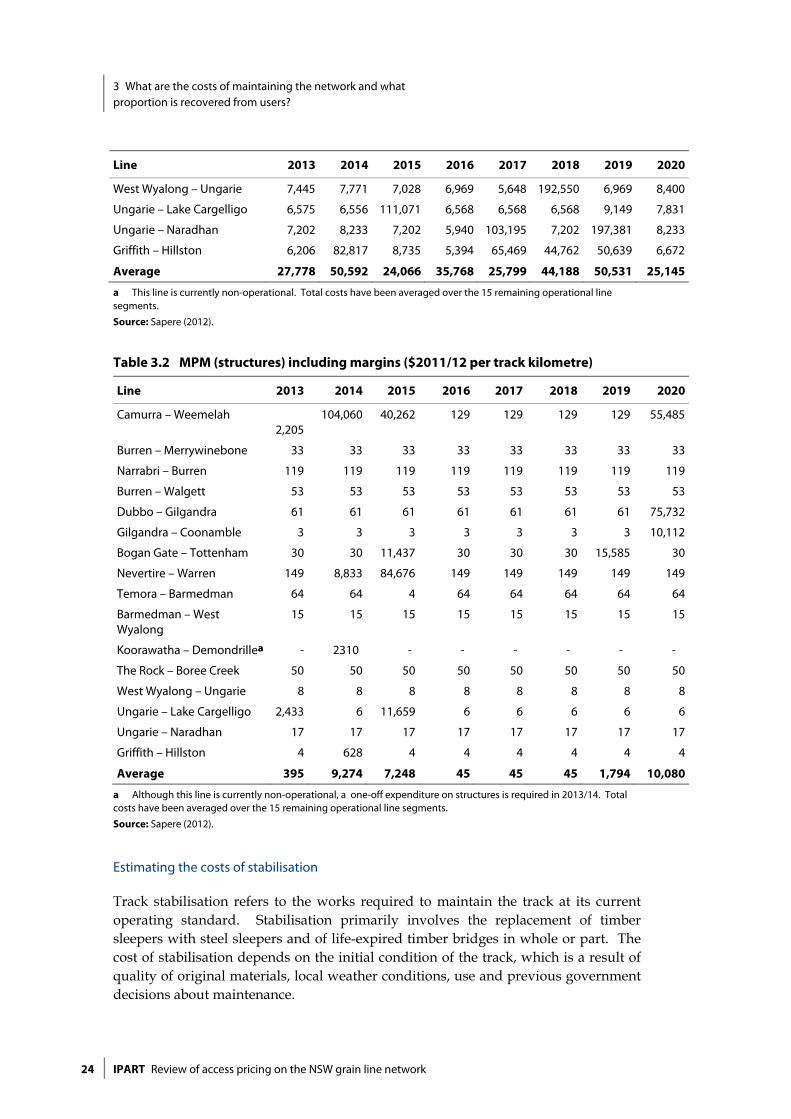

MPM (track) and MPM (structures) costs are highly variable between lines and years. This is because of the different conditions and characteristics of the lines, including number, size and state of bridges and proportion of timber sleepers that require replacing. It also results from the staged delivery of the stabilisation programme across lines and years. These costs (including incorporated margins) are broken down by line and year in Tables 3.1 and 3.2.

Table 3.1 MPM (track) including margins ($2011/12 per track kilometre)

Line 2013 2014 2015 2016 2017 2018 2019 2020

Camurra – Weemelah 12,520 104,961 5,694 5,417 5,417 104,849 4,884 79,063

Burren – Merrywinebone 6,724 5,000 103,979 6,284 6,284 96,728 5,000 120,084

Narrabri – Burren 8,687 69,942 7,911 61,308 8,936 8,656 8,656 7,375

Burren – Walgett 5,599 5,599 30,777 100,395 5,832 5,570 190,893 4,444

Dubbo – Gilgandra 7,072 7,072 5,783 237,238 7,050 7,050 7,050 6,158

Gilgandra – Coonamble 155,864 68,230 5,748 5,819 5,826 5,826 7,026 5,826

Bogan Gate – Tottenham 8,241 105,934 8,027 8,001 6,727 117,541 8,530 59,979

Nevertire – Warren 12,084 263,941 4,847 9,189 4,847 9,189 6,584 9,189

Temora – Barmedman 8,015 6,785 68,658 11,051 196,263 6,785 8,015 8,015

Barmedman – West Wyalong

7,558 7,558 6,350 92,468 7,998 11,037 6,350 11,037

Koorawatha – Demondrillea - - - - - - - -

The Rock – Boree Creek 118,411 8,814 7,835 6,556 7,801 8,209 143,245 9,188

13 M. Smart, Sapere Research Group, Maintenance costs for grain branch lines in NSW – Final report to

IPART, April 2012.

3 What are the costs of maintaining the network and what proportion is recovered from users?

24 IPART Review of access pricing on the NSW grain line network

Line 2013 2014 2015 2016 2017 2018 2019 2020

West Wyalong – Ungarie 7,445 7,771 7,028 6,969 5,648 192,550 6,969 8,400

Ungarie – Lake Cargelligo 6,575 6,556 111,071 6,568 6,568 6,568 9,149 7,831

Ungarie – Naradhan 7,202 8,233 7,202 5,940 103,195 7,202 197,381 8,233

Griffith – Hillston 6,206 82,817 8,735 5,394 65,469 44,762 50,639 6,672

Average 27,778 50,592 24,066 35,768 25,799 44,188 50,531 25,145

a This line is currently non-operational. Total costs have been averaged over the 15 remaining operational line segments.

Source: Sapere (2012).

Table 3.2 MPM (structures) including margins ($2011/12 per track kilometre)

Line 2013 2014 2015 2016 2017 2018 2019 2020

Camurra – Weemelah 2,205

104,060 40,262 129 129 129 129 55,485

Burren – Merrywinebone 33 33 33 33 33 33 33 33

Narrabri – Burren 119 119 119 119 119 119 119 119

Burren – Walgett 53 53 53 53 53 53 53 53

Dubbo – Gilgandra 61 61 61 61 61 61 61 75,732

Gilgandra – Coonamble 3 3 3 3 3 3 3 10,112

Bogan Gate – Tottenham 30 30 11,437 30 30 30 15,585 30

Nevertire – Warren 149 8,833 84,676 149 149 149 149 149

Temora – Barmedman 64 64 4 64 64 64 64 64

Barmedman – West Wyalong

15 15 15 15 15 15 15 15

Koorawatha – Demondrillea - 2310 - - - - - -

The Rock – Boree Creek 50 50 50 50 50 50 50 50

West Wyalong – Ungarie 8 8 8 8 8 8 8 8

Ungarie – Lake Cargelligo 2,433 6 11,659 6 6 6 6 6

Ungarie – Naradhan 17 17 17 17 17 17 17 17

Griffith – Hillston 4 628 4 4 4 4 4 4

Average 395 9,274 7,248 45 45 45 1,794 10,080

a Although this line is currently non-operational, a one-off expenditure on structures is required in 2013/14. Total costs have been averaged over the 15 remaining operational line segments.

Source: Sapere (2012).

Estimating the costs of stabilisation

Track stabilisation refers to the works required to maintain the track at its current operating standard. Stabilisation primarily involves the replacement of timber sleepers with steel sleepers and of life-expired timber bridges in whole or part. The cost of stabilisation depends on the initial condition of the track, which is a result of quality of original materials, local weather conditions, use and previous government decisions about maintenance.

3 What are the costs of maintaining the network and what proportion is recovered from users?

Review of access pricing on the NSW grain line network IPART 25

The inclusion of stabilisation costs in the TAM plan causes a high degree of variability or cost ‘spikes’ in MPM costs between lines and years as illustrated in Tables 3.1 and 3.2. This is caused by programs of sleeper replacement in the case of MPM (track) and bridge works in the case of MPM (structures). The non-sleeper component of MPM (track) is less variable between years as maintenance is more predictable.

To separate out the impact of stabilisation costs from ongoing maintenance costs, Sapere split the MPM (track) costs into sleeper and non-sleeper components. This was done by calculating the median cost of MPM (track) per line per year. The sleeper component is represented by the annual unit cost in a year where cost exceeds the median value, minus the median value. The non-sleeper component is either the annual unit cost or the median value in a year where the annual unit cost exceeds the median.

MPM (structures) unit costs exhibit similar cost spikes in years where there are stabilisation works planned for bridges on a particular line. To isolate stabilisation costs from ongoing MPM (structures) costs, Sapere carried out the same process using the median value.

Sapere then calculated the ongoing maintenance cost for sleepers once major works are completed using the following assumptions:

the average life of a new steel sleeper is 50 years

the average cost of installing a steel sleeper is between $170 - $220 per sleeper

there are approximately 1,667 sleepers per kilometre of track

around 2% of sleepers require replacing each year.

Sapere estimated that the ongoing annual cost of sleeper maintenance would be around $6,931 per track kilometre ($2011/12). The resulting annual maintenance cost per track kilometre for each line is in Table 3.3.

3 What are the costs of maintaining the network and what proportion is recovered from users?

26 IPART Review of access pricing on the NSW grain line network

Table 3.3 Annual maintenance cost per line ($2011/12 per track kilometre)

Line Routine Mainten

ance

MPM track MPM structures Total cost

Non-sleeper

Current sleeper

Post-stabilisa

tion sleeper

Current Post-stabilisa

tion

Current Post-stabilisation

Camurra – Weemelah

6,294 6,159 27,074 6,931 20,278 129 59,805 19,513

Burren – Merrywinebone

6,294 6,971 29,533 6,931 33 33 42,831 20,229

Narrabri – Burren 6,294 8,555 11,416 6,931 119 119 26,384 21,900

Burren – Walgett 6,294 5,581 30,554 6,931 53 53 42,481 18,858

Dubbo – Gilgandra 6,294 6,910 23,114 6,931 7,629 61 43,946 20,196

Gilgandra – Coonamble

6,294 5,818 21,455 6,931 1,014 3 34,580 19,046

Bogan Gate – Tottenham

6,294 8,576 25,572 6,931 2,726 30 43,167 21,831

Nevertire – Warren 6,294 7,735 25,874 6,931 9,470 149 49,373 21,109

Temora – Barmedman

6,294 7,864 25,136 6,931 64 64 39,357 21,153

Barmedman – West Wyalong

6,294 7,429 9,156 6,931 15 15 22,894 20,669

Koorawatha – Demondrillea

- - - - 231 - 231 -

The Rock – Boree Creek

6,294 9,002 24,472 6,931 50 50 39,818 22,277

West Wyalong – Ungarie

6,294 6,792 18,748 6,931 8 8 31,841 20,024

Ungarie – Lake Cargelligo

6,294 7,573 14,269 6,931 1,414 6 29,549 20,804

Ungarie – Naradhan

6,294 7,024 28,746 6,931 17 17 42,080 20,266

Griffith – Hillston 6,294 8,020 20,944 6,931 67 4 35,324 21,249

Average 6,294 7,334 22,404 6,931 2,879 49 38,911 20,608

a Although this line is currently non-operational, a one-off expenditure on structures is required in 2013/14. Total costs have been averaged over the 15 remaining operational line segments.

Source: Sapere (2012).

Adding together the RM and MPM components, the average annual cost of maintaining the grain lines up until 2020 is $38,911 per track kilometre ($2011/12). However, this ranges from $22,894 per track kilometre on the Barmedman – West Wyalong line to $59,805 per track kilometre on the Camurra – Weemelah line due to differences in track condition. This equates to an annual stabilisation investment of around $145 million ($2011/12) over the next 8 years.

3 What are the costs of maintaining the network and what proportion is recovered from users?

Review of access pricing on the NSW grain line network IPART 27

After 2020, the total cost of maintaining the grain lines will decrease to around $20,608 per track kilometre ($2011/12) with a much smaller range between lines. This equates to an ongoing annual maintenance investment of $20.4 million ($2011/12).

Comparison to other benchmarks

In its report, Sapere looked at how these unit maintenance costs compare to the unit maintenance costs on the Victorian rail freight network. Adjusting for inflation, Sapere calculated the Victorian unit maintenance costs to be around $21,498 per track kilometre per year for Class 2 and 3 lines and around $14,873 per track kilometre per year for Class 4 and 5 lines.

The post-stabilisation unit maintenance cost for the NSW grain line network falls within this range. The pre-stabilisation unit maintenance cost is much higher than these estimates due to the level of capital investment required to stabilise the lines at their current operating standard and prevent further deterioration. Sapere concluded that there was no evidence that these stabilisation costs could be reduced further other than by delaying the completion date for stabilisation.

3.3 What is the level of cost recovery?

In the Draft Report, we calculated cost recovery per line using our below-rail cost estimate of $26,350 per track kilometre and historical grain traffic volumes from CRIA.

We concluded that cost recovery in 2010/11, which was a good harvest year, was extremely low, averaging only 3% across the network and ranging from 12% to less than 1% between lines. This means that the NSW Government subsidised 97% of the cost of providing and maintaining the grain line infrastructure. By comparison, the proportion of government subsidy provided to CityRail for the provision of public passenger rail services was around 78% in 2010/11.

3.3.1 Stakeholder submissions

Peter and Libby Skipworth suggested that using a maintenance cost estimate that does not take into account increased maintenance costs associated with poor maintenance history and the impact of natural disasters may negatively skew the cost recovery ratio.14

14 Peter and Libby Skipworth submission, p 1.

3 What are the costs of maintaining the network and what proportion is recovered from users?

28 IPART Review of access pricing on the NSW grain line network

3.3.2 IPART’s findings

Current level of cost recovery

The NSW Grain Freight Review (2009) recommended that the cost of stabilising lines should be met through a non-recoverable government grant, with a review of access charges to determine an appropriate level of user contribution to ongoing maintenance. We note that the former NSW Government agreed to these recommendations in its preliminary response to the review.

However, the cost of stabilisation works is an important component of the cost to the NSW Government of maintaining the grain line network. Even if the costs are met by non-recoverable government grant, they are still a significant capital investment that is funded primarily through taxpayer funds. These funds are limited and investing them in the grain line network means that they cannot be invested in other projects.

Therefore, we consider that it is relevant to illustrate the total cost of maintaining the grain line network, including stabilisation costs and to measure the cost recovery on this basis. Table 3.4 shows cost recovery based on the current annualised below-rail cost (including stabilisation costs)15 and actual access revenue received in 2010/11.

15 We deflated $2011/12 costs using the Sydney capital city CPI index in order to compare costs to

access revenue received in 2010/11 and accurately calculate cost recovery.

3 What are the costs of maintaining the network and what proportion is recovered from users?

Review of access pricing on the NSW grain line network IPART 29

Table 3.4 Cost recovery including stabilisation costs ($2010/11)

Line Annualised below-rail cost ($2010/11)

Access revenue ($2010/11)

Cost recovery %

Camurra – Weemelaha 4,834,924 58,698 1.2%

Burren - Walgett 3,622,827 109,339 3.0%

Burren - Merrywinebone 2,175,674 32,232 1.5%

Narrabri - Burren 2,104,144 259,160 12.3%

Bogan Gate - Tottenham 4,657,284 62,063 1.3%

Nevertire - Warren 954,123 20,788 2.2%

Dubbo - Coonamble 5,537,538 223,834 4.0%

Ungarie - Lake Cargelligo 2,042,558 7,482 0.4%

Ungarie - Naradhan 2,463,642 3,334 0.1%

West Wyalong -Ungarie 1,246,360 19,349 1.6%

Barmedman - West Wyalong

699,435 29,468 4.2%

Temora - Barmedman 1,377,794 38,996 2.8%

Griffith to Hillston 3,672,543 8,518 0.2%

The Rock to Boree Creek 2,184,044 2,483 0.1%

Total 37,572,890 875,743 2.3%a Access revenue includes a $1/tonne surcharge implemented in July 2010. Note: The costs have been adjusted by the Sydney CPI December quarterly index in order to compare with access revenue for the same period. Cowra lines have not been included as they are currently non-operational and earn no access revenue.

Source: CRIA; Sapere (2012); IPART calculations.

Based on current annualised below-rail costs, cost recovery is around 2.3% across the network ranging from 12.3% (Narrabri – Burren) to virtually zero (The Rock – Boree Creek, Hillston – Griffith, Ungarie – Naradhan, Ungarie – Lake Cargelligo).

Expected cost recovery based on future ongoing maintenance costs

Once stabilisation works are completed, the annual ongoing maintenance cost is almost halved. Table 3.5 show cost recovery by line, based on the expected ongoing maintenance cost post-2020 and actual access revenue received in 2010/11.

3 What are the costs of maintaining the network and what proportion is recovered from users?

30 IPART Review of access pricing on the NSW grain line network

Table 3.5 Cost recovery excluding stabilisation costs ($2010/11)

Line Annualised below-rail cost (post-

stabilisation)($2010/11)

Access revenue ($2010/11)

Cost recovery %

Camurra – Weemelaha 1,577,547 58,698 3.7%

Burren - Walgett 1,608,252 109,339 6.8%

Burren - Merrywinebone 1,027,564 32,232 3.1%

Narrabri - Burren 1,746,487 259,160 14.8%

Bogan Gate - Tottenham 2,355,301 62,063 2.6%

Nevertire - Warren 407,934 20,788 5.1%

Dubbo - Coonamble 2,824,139 223,834 7.9%

Ungarie - Lake Cargelligo 1,438,040 7,482 0.5%

Ungarie - Naradhan 1,186,504 3,334 0.3%

West Wyalong -Ungarie 783,831 19,349 2.5%

Barmedman - West Wyalong

631,469 29,468 4.7%

Temora - Barmedman 740,512 38,996 5.3%

Griffith to Hillston 2,209,230 8,518 0.4%

The Rock to Boree Creek 1,221,915 2,483 0.2%

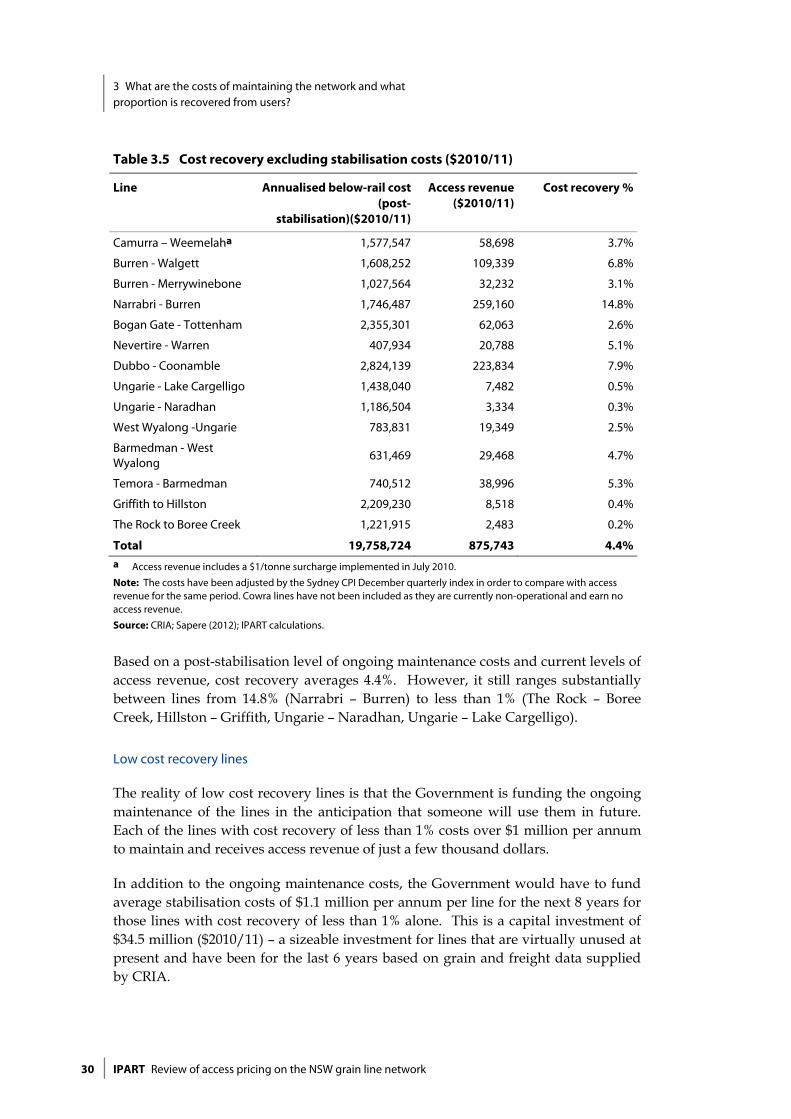

Total 19,758,724 875,743 4.4% a Access revenue includes a $1/tonne surcharge implemented in July 2010. Note: The costs have been adjusted by the Sydney CPI December quarterly index in order to compare with access revenue for the same period. Cowra lines have not been included as they are currently non-operational and earn no access revenue.

Source: CRIA; Sapere (2012); IPART calculations.

Based on a post-stabilisation level of ongoing maintenance costs and current levels of access revenue, cost recovery averages 4.4%. However, it still ranges substantially between lines from 14.8% (Narrabri – Burren) to less than 1% (The Rock – Boree Creek, Hillston – Griffith, Ungarie – Naradhan, Ungarie – Lake Cargelligo).

Low cost recovery lines

The reality of low cost recovery lines is that the Government is funding the ongoing maintenance of the lines in the anticipation that someone will use them in future. Each of the lines with cost recovery of less than 1% costs over $1 million per annum to maintain and receives access revenue of just a few thousand dollars.

In addition to the ongoing maintenance costs, the Government would have to fund average stabilisation costs of $1.1 million per annum per line for the next 8 years for those lines with cost recovery of less than 1% alone. This is a capital investment of $34.5 million ($2010/11) – a sizeable investment for lines that are virtually unused at present and have been for the last 6 years based on grain and freight data supplied by CRIA.

3 What are the costs of maintaining the network and what proportion is recovered from users?

Review of access pricing on the NSW grain line network IPART 31

The next chapter considers whether this level of government funding is justified on the basis of the net external benefits generated by the lines or if there is a case for users to make a greater contribution to costs through higher access prices.

4 Are the current access prices and government subsidy appropriate?

32 IPART Review of access pricing on the NSW grain line network

4 Are the current access prices and government subsidy appropriate?

In previous IPART reviews, such as CityRail, we determined the amount of government subsidy based on the level of external benefits generated by the service. The remainder of costs are assumed to generate private benefits, for which users should pay.

The net external benefits generated by operations on the grain line network include the extent to which air pollution, road accidents, noise, greenhouse gas emissions and unrecovered road damage from heavy vehicles are less than what they would be if the same freight task was delivered by road.

This chapter presents our findings on the comparison between expected future net external benefits generated by operations on the grain lines and expected future government subsidy requirements. This comparison assumes access prices at current levels and 2 maintenance cost scenarios: (1) efficient costs including stabilisation investment, (2) efficient costs after stabilisation has taken place.

4.1 Final Findings

IPART finding

4 The current government subsidy to the grain line network (including capital investment for stabilisation) is almost 3 times greater than the average external benefits generated by use of the network over a typical 5-year period.

5 The expected ongoing government subsidy to the grain line network (excluding capital investment for stabilisation) is 1.4 times greater than the average external benefits generated by use of the network over a typical 5-year period.

From the Draft Report, we updated our calculations of external benefits to take into account our new estimates of maintenance costs (including and excluding stabilisation costs), which affect the estimated level of the implied government subsidy. Based on feedback in submissions to the Draft Report, we included non-grain freight in our total volume of traffic using the network.

4 Are the current access prices and government subsidy appropriate?

Review of access pricing on the NSW grain line network IPART 33

Given that net external benefits depend on the volume of traffic, we included an analysis of the net external benefits by line. This showed that, on average over a typical 5-year period, some lines generate a level of net external benefits that is proportionate to the government subsidy they receive, but other lines cost far more to maintain than the benefits they generate.

4.2 What are the external benefits of the network?

In our Draft Report, we calculated the external costs associated with transporting grain to port by rail and road and looked at the difference between the 2 estimates. We found that rail had a net benefit over road for each of the grain line routes to port.

Our analysis was based on external cost unit rate estimates from 2 difference sources including a Queensland study, which was quoted in a submission by Dr Philip Laird16, and a report by Booz Allen Hamilton17 undertaken for the Ministerial Taskforce considering the case for reopening of the Cowra grain lines in NSW. These external cost unit rates are replicated in Table 4.1 below.

Table 4.1 Externality unit rates used in the Draft Report

Transport mode Location Laird externality unit rates (c/ntk)

Booz externality unit rates (c/ntk)

Road Urban 3.88 2.11

Road Non-urban 2.79 0.31

Rail Urban 0.61 0.75

Rail Non-urban 0.24 0.09

Source: Laird submission (2011); Booz (2011).

The rates proposed by Dr Laird represent a combined value of the external costs of accidents, air pollution, noise pollution, greenhouse gas emissions, congestion, and incremental road damage for urban and non-urban regions. They include an allowance of 1 cent per net tonne kilometre for under-recovered road system costs. That is, the difference between the road user charge component of the diesel excise and the actual pavement damage caused by trucks.

16 Laird submission to Issues Paper, June 2010. 17 Booz Allen Hamilton, Final Report Re-Opening the Cowra Rail Lines: Cost Benefit Analysis and

Policy Options, October 2011.

4 Are the current access prices and government subsidy appropriate?

34 IPART Review of access pricing on the NSW grain line network

The Booz Allen Hamilton estimates take into account air pollution, greenhouse gases, noise, water, nature & landscape and urban separation, but do not include any allowance for unrecovered road costs. While, in aggregate, road costs are assumed to be recovered wholly through heavy vehicle charges, in practice, we considered that it is likely that there is some degree of under-recovery on some road types. As such, we added the same estimate of unrecovered road costs (1 cent per net tonne kilometre) to the Booz externality rates to make them comparable to the Laird estimates.

4.2.1 Stakeholder submissions

The ARTC agreed with IPART’s approach that social benefits should be paid for by the wider community (through government subsidy), whereas private benefits should be paid for by users to whom they accrue.18

However, Mr Lewis Davies argued that IPART had not considered all of the external costs associated with rail and road transport.19

Dr Philip Laird suggested that a breakdown of the external costs from the Booz Allen Hamilton report should be included.20

4.2.2 IPART’s findings

Analysis of external unit costs

In February 2012, the Ministerial Taskforce overseeing the business case for the revival of the Cowra lines produced its final report.21 The report referred to the Booz Allen Hamilton cost benefit analysis report and provided a breakdown of the externality unit costs of rail and road. These costs include air pollution, greenhouse gases, noise, water, nature and landscape and urban separation. Road congestion and road accident costs were calculated separately, as were road maintenance cost savings. Adding in these costs makes the estimates slightly higher than those used in the Draft Report.