Aracely Rosales - Helping diverse consumers navigate health insurance exchanges

Final report

Helping Consumers Reduce Food

Waste – A Retail Survey 2011

In 2009, WRAP undertook a survey across UK retailers, and a selection of food products, of a range of factors believed to influence household food waste. To provide an updated picture, and gauge progress against the recommendations in the 2009 report, the work was repeated in 2011 and this report summarises the findings.

Project code: RHF523-002 Research date: February 2011-March 2012 Date: June 2012

WRAP’s vision is a world without waste, where resources are used sustainably. We work with businesses, individuals and communities to help them reap the benefits of reducing waste, developing sustainable products and using resources in an efficient way. Find out more at www.wrap.org.uk

Written by: Brook Lyndhurst & WRAP

Front cover photography: Shop aisle (Fotofolia)

While we have tried to make sure this report is accurate, we cannot accept responsibility or be held legally responsible for any loss or damage arising out of or in

connection with this information being inaccurate, incomplete or misleading. This material is copyrighted. You can copy it free of charge as long as the material is

accurate and not used in a misleading context. You must identify the source of the material and acknowledge our copyright. You must not use material to endorse or

suggest we have endorsed a commercial product or service. For more details please see our terms and conditions on our website at www.wrap.org.uk

Suggested citation for this report:

Helping Consumers Reduce Food Waste – A Retail Survey 2011. Brook Lyndhurst & WRAP, June 2012.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 1

Executive summary

In 2009, WRAP undertook a survey across UK retailers, and a selection of food products, of a range of factors believed to influence household food waste1. Data on, for example, pack size, price, functionality, labelling and point of sale communications, were reviewed for approximately 10,000 separate products from 19 product categories. The data collected through that research constituted an important resource for WRAP and the food industry to identify good practice that could be implemented more widely, and areas where inconsistency or lack of clarity could be addressed to help consumers get more out of what they buy and waste less. One of the recommendations from the 2009 research was to repeat the project in 2011 to determine what had changed in the previous two years. This report summarises the findings from the 2011 research, creating a new baseline from which changes in the UK retail environment may be measured. Where comparable data existed, this report documents change, or lack of change, since 2009. Data were collected on 12,000 separate products from 20 product categories. In some cases, there may well be genuine reasons why guidance given to consumers differs between products that are, from a consumer perspective, similar. These could relate to differences in product formulation, use of preservatives, differences in packaging materials and design and so on. However, in many cases, differences may have arisen for historical reasons or as a result of decisions taken in isolation by individuals or organisations. It is hoped that this report will encourage a review of the products and information provided to consumers, and WRAP will be working with retailers, food manufacturers, trade associations, governments and the Food Standards Agency to continue to facilitate changes to the retail environment that will help reduce food waste. As in 2009, the project involved collecting a range of data on key product types thought to be representative of their category. Categories were chosen to reflect those where food wastage is highest. Full definitions of each product type, and how they compare to 2009, are found in Appendix 1. In summary, the 2011 products were: 1 Sliced white bread. 2 Plain white rolls. 3 World breads (plain white pittas, plain tortilla wraps, garlic or garlic and herb naans). 4 Standard tomato/original or tomato and herb pasta sauce. 5 Sliced ham. 6 Unsmoked back bacon. 7 Whole, skinless chicken breast fillets (chilled and frozen). 8 Fresh potatoes. 9 Braeburn apples. 10 Fresh carrots. 11 Bagged salad; iceberg/mixed salad. 12 Standard long-grain rice; dry and microwaveable variants. 13 Dry fusili pasta. 14 Chilled and frozen cottage pie ready meals. 15 Standard yoghurts. 16 Hen eggs. 17 Mature cheddar cheese. 18 Standard mayonnaise.

1 Helping Consumers Reduce Food Waste: A Retail Survey, WRAP, 2010

Helping Consumers Reduce Food Waste – A Retail Survey 2011 2

19 Semi-skimmed milk. 20 Chilled orange juice (added in 2011). Delivering the WRAP recommendations from the 2009 survey In addition to repeating the Retail Survey in 2011, and extending it to include a product from the drinks category (orange juice), WRAP committed to several other actions in the 2009 report. Firstly, to undertake research into how promotional strategies are deployed. In late 2011, WRAP published its review of how different promotional mechanics are used by the UK grocery sector (covering the period between 2007-2010), and a survey to investigate the link between promotions and food waste in the UK2. Secondly, to undertake research into how consumers understand and use date labels and storage guidance. A consumer insight report into this was published by WRAP in May 20113. There were several key findings from this research, most relevant to this work were:

The presence of a ‘display until’ date reduced understanding of both ‘best before’ and ‘use by’ dates – the proportion of people interpreting ‘use by’ as a quality mark rose from 25% to 32% when a ‘display until’ date was present and the proportion interpreting ‘best before’ as a safety date increased from 14% to 20% when a ‘display until’ date was present.

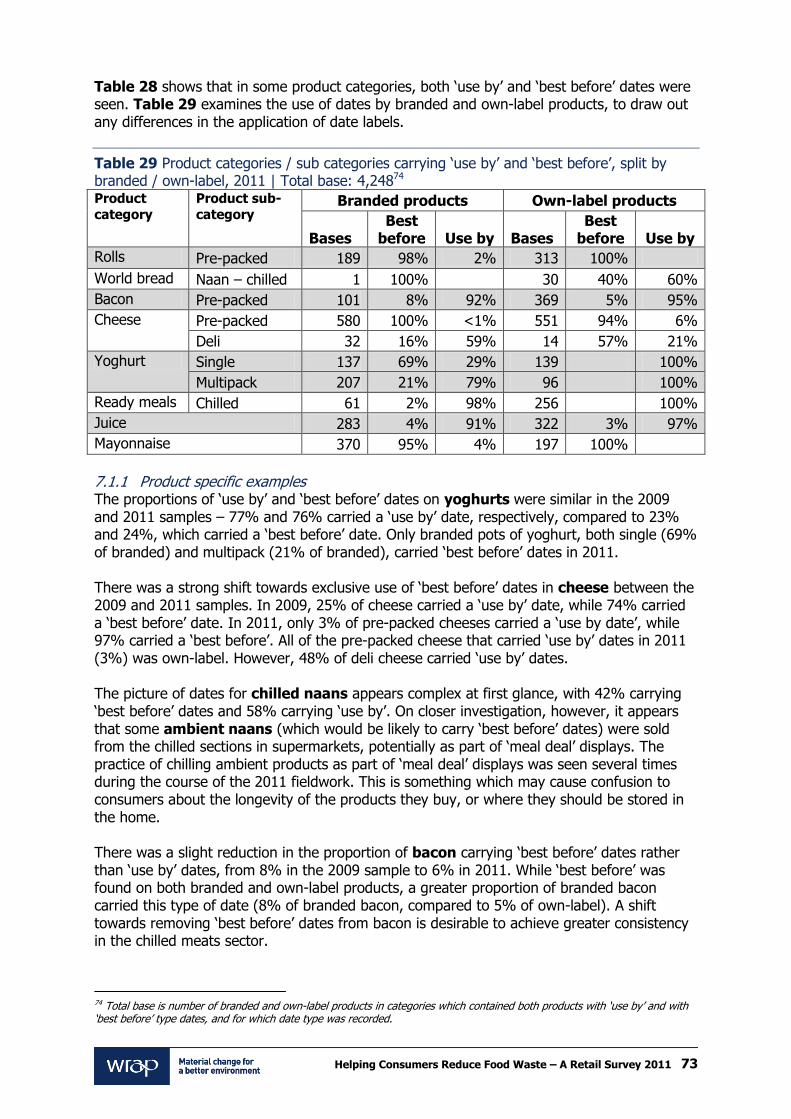

Although interpretation and use of date labels is driven principally by product type, the report revealed that the type of date label present on the pack does have an effect on behaviour, albeit to a lesser extent than product type. Swapping the ‘best before’ for a ‘use by’ on yoghurt caused the proportion of people who said they ‘would eat it up until the date on the label’ to rise, from 32% for yoghurt with ‘best before’ to 42% for yoghurt with ‘use by’. For cheese, those saying they ‘would eat it after the date label’ reduced from 75% for cheese with ‘best before’ to 69% for cheese with ‘use by’.

The majority of respondents selected that they would prefer to buy the product with a longer specified period to use the product after opening (‘use within x days’). For ham the increase was around 50% points preferring the longer date, for milk around 45% points and for ambient cooking sauce around 30% points.

Thirdly, to work with the food industry to investigate alternatives to ‘freeze on the day of purchase’ labelling. WRAP research4 showed that 90% of respondents regularly bought fresh or refrigerated food to freeze at home, with fresh meat, fish and bakery being the most common. 59% stated that they thought they had to freeze the product on the day they buy it, with half of these thinking that this is for food safety reasons. This behaviour is in-line with the majority of current on-pack guidance. WRAP’s research5 showed that on-pack guidance has a very strong influence on respondents’ willingness to freeze food. The proportion saying they would freeze it after the day they bought it greatly increased where a ‘freeze before/date mark’ was shown. For example, for bacon, the proportion indicating that they would freeze it ‘any time before the date on the label’ increased from 25% to 44% when the ‘freeze before / use by’ label was shown. For bread rolls the proportions increased from 13% to 29%. This indicates that many consumers (ca.35%) will make use of the flexibility alternative labelling gives them.

2 Investigation into the Possible Impact of Promotions on Food Waste, WRAP, 2011 3 Consumer Insight: Date Labels and Storage Guidance, WRAP, 2011 4 Understanding Consumer Use of the Freezer, WRAP, 2010 5 Consumer Insight: Date Labels and Storage Guidance, WRAP, 2011

Helping Consumers Reduce Food Waste – A Retail Survey 2011 3

Fourthly, WRAP committed to develop consumer-facing messaging demonstrating the benefits of packaging in helping to prevent household food waste. WRAP is currently working with Incpen, the Packaging Federation, BRC, FDF, together with Courtauld Commitment signatories to develop an approach to demonstrate to consumers the benefits of well-designed packaging in helping to prevent household food waste. The Love Food Hate Waste website also now includes consumer-focused case studies of how the food industry is helping customers waste less food, including some examples of packaging functionality6. Finally, it was recommended WRAP explore consumer perceptions of price gradients. It was thought that consumers may believe that all smaller packs come at a premium for products where this is not in fact the case, such as chicken (where a relatively gentle and unpronounced price gradient between the smallest and largest packs was seen). Price was investigated through WRAP’s earlier research7 in terms of consumers’ willingness to buy smaller packs. This suggested that consumers are not necessarily averse to paying a little more per unit of volume/weight to avoid being left with unnecessary surplus. Having said this, there was considerable variation in how much more respondents were willing to pay between products, and there were doubts as to how well ‘stated’ willingness to pay more would translate into actual purchase decisions. When interviewees who said they would not consider buying packs in alternative sizes were asked why, price was listed as a significant factor. Given the difficulties in accurately investigating consumers’ perceptions of price, and other areas of research being prioritised in discussions with industry, WRAP has not undertaken any further work on this. The 2011 Retail Survey suggests that price gradients remain an aspect of food retailing that could encourage consumers to buy more than they need (Section 3.3). For example, a steep, linear price gradient results in a strong incentive to buy bigger packs e.g. potatoes, orange juice, bacon and world breads. There was a high premium for the smallest examples of some packs e.g. carrots and bagged salad. As in 2009, both chilled and frozen chicken showed non-linear price gradients, indicating that consumers would be wrong to think that buying a larger pack always represents better value for this product, whilst bread showed pronounced price gradients between smaller and larger packs. Key developments since 2009 The 2011 Retail Survey reveals several major developments since 2009 that are in line with recommendations in the 2009 Retail Survey report and subsequent WRAP research (summarised above). This section details these key developments since 2009 as well as any significant developments that have taken place since the fieldwork. As summarised above, WRAP research8 found that consumers are better able to understand the ‘use by’ and ‘best before’ dates in the absence of ‘display until’ dates. The extent to which ‘display until’ dates are used has declined between 2009 and 2011, with 39% of products for which dates were recorded carrying a ‘display until’ date in the 2009 sample, and 29% carrying a ‘display until’ date in the 2011 sample9. It is worth stating that no instances of ‘sell by’ dates were found in 2011 (3 were found in 2009). For all retailers, there were categories in which no products were found with ‘display until’ dates at all (Section 7.2). As in 2009, continued use of ‘display until’ dates is driven by own-label products.

6 See: http://www.wrap.org.uk/downloads/Retailer_and_Brand_Case_Studies.06c14310.11392.pdf 7 Research into consumer behaviour in relation to food dates and portion sizes, WRAP, 2008 8 Consumer Insight: Date Labels and Storage Guidance, WRAP, 2011 9 This reduction becomes slightly smaller when the 2011 sample is weighted so that the proportion of different retailers in the sample matches that used in 2009. The proportion of products carrying a ‘display until’ date then becomes 32% in the 2011 sample. This still indicates a fairly substantial (7%) decrease in use of this type of date.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 4

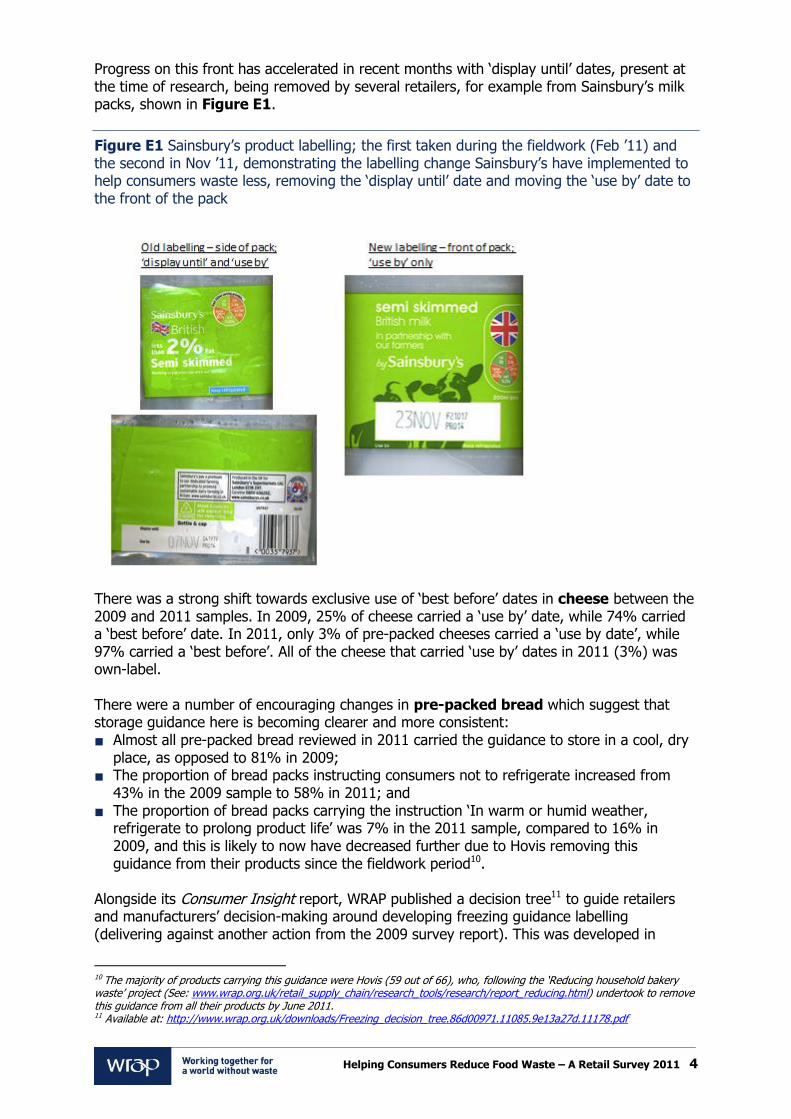

Progress on this front has accelerated in recent months with ‘display until’ dates, present at the time of research, being removed by several retailers, for example from Sainsbury’s milk packs, shown in Figure E1.

Figure E1 Sainsbury’s product labelling; the first taken during the fieldwork (Feb ’11) and the second in Nov ’11, demonstrating the labelling change Sainsbury’s have implemented to help consumers waste less, removing the ‘display until’ date and moving the ‘use by’ date to the front of the pack

There was a strong shift towards exclusive use of ‘best before’ dates in cheese between the 2009 and 2011 samples. In 2009, 25% of cheese carried a ‘use by’ date, while 74% carried a ‘best before’ date. In 2011, only 3% of pre-packed cheeses carried a ‘use by date’, while 97% carried a ‘best before’. All of the cheese that carried ‘use by’ dates in 2011 (3%) was own-label. There were a number of encouraging changes in pre-packed bread which suggest that storage guidance here is becoming clearer and more consistent:

Almost all pre-packed bread reviewed in 2011 carried the guidance to store in a cool, dry place, as opposed to 81% in 2009;

The proportion of bread packs instructing consumers not to refrigerate increased from 43% in the 2009 sample to 58% in 2011; and

The proportion of bread packs carrying the instruction ‘In warm or humid weather, refrigerate to prolong product life’ was 7% in the 2011 sample, compared to 16% in 2009, and this is likely to now have decreased further due to Hovis removing this guidance from their products since the fieldwork period10.

Alongside its Consumer Insight report, WRAP published a decision tree11 to guide retailers and manufacturers’ decision-making around developing freezing guidance labelling (delivering against another action from the 2009 survey report). This was developed in

10 The majority of products carrying this guidance were Hovis (59 out of 66), who, following the ‘Reducing household bakery waste’ project (See: www.wrap.org.uk/retail_supply_chain/research_tools/research/report_reducing.html) undertook to remove this guidance from all their products by June 2011. 11 Available at: http://www.wrap.org.uk/downloads/Freezing_decision_tree.86d00971.11085.9e13a27d.11178.pdf

Helping Consumers Reduce Food Waste – A Retail Survey 2011 5

conjunction with the Food Standards Agency (FSA) and has led to changes in freezing guidance labelling since the 2011 fieldwork was carried out. For example, M&S and Sainsbury’s now label products with a ‘Freeze by date mark shown’ message rather than to ‘Freeze on day of purchase’ (Figure E2).

Figure E2 New product labelling; the first taken during the fieldwork (Feb ’11) and the second in Nov ’11, demonstrating the labelling change implemented to help consumers waste less

WRAP is working with other retailers and manufacturers to embed the freezing decision tree into labelling practice and hopes others will follow M&S’s and Sainsbury’s lead. Other highlights:

Increased proportion of smaller packs for potatoes, milk, cooking sauce, world breads and bread rolls. For example, there was an increase in four packs of rolls to 32% of the sample (from a previous 18%). The proportion of two packs of rolls also increased, from 5% in the 2009 sample to 13% in 2011.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 6

An example of a single breast pack of chilled chicken (none were found in 2009) (see Figure 2, main report).

High availability of loose apples, carrots and potatoes, across most store formats (loose products were found in 53 of 57 stores visited).

47% of all packaged products were re-closable in some way.

35% of cheese came in a re-closable pack, compared to 26% in the 2009 sample.

73% of standard dry rice packs were re-closable, compared to 44% of standard rice in the 2009 sample.

17% of chilled chicken packs reviewed in 2011 were re-closable, compared to only 5% of the sample in 2009.

Continued high proportion of on-pack storage guidance (96% of all packaged products). The introduction of Morrisons’ ‘best kept’ front of pack logo being a key development.

18% of ISB rolls carried storage guidance (n=42), compared to just 3% in the 2009 sample.

All deli ham carried storage guidance (n=33), including guidance to refrigerate.

16 of the 52 stores that sold loose produce (apples, carrots and potatoes) provided plastic bags for these products which carried on-bag storage guidance.

30% of pre-packed cheese carried guidance about using packaging or storage containers to keep the product fresh, which is a significant increase compared to the 6% of pre-packed cheese in the 2009 sample.

19% of pre-packed cheeses carried an on pack ‘flash’ label informing consumers that the pack is re-closable in order to keep the product fresher for longer.

44% of freezable products carried the snowflake logo, with 32% using accompanying text. Chilled naans had a very high prevalence of snowflake/star freezing symbols, with 90% of products carrying a symbol.

The majority (73%) of products which gave freezing guidance recommended how long the product could be kept frozen for. In most cases, this was either one month (81%) or three months (19%).

The proportion of chilled cooking sauces carrying freezing instructions increased between the samples, from 88% of packs in 2009, to 98% in 2011.

82% of products that require cooking, carried cooking guidance.

As in 2009, a number of chicken packs carried guidance on use of leftovers. 8% of packs of chilled chicken (all Waitrose) carried the guidance ‘Cool leftovers to room temperature, refrigerate within 2 hours and consume within 2 days’.

15% of products had a recipe on-pack (compared to just 8% in 2009).

65% of pasta packs carried portioning guidance (compared to 57% in 2009).

During the research, 252 examples of point of sale information that might help prevent food waste were noted including: online links, printed loose produce / deli bags, shelf edge labels and leaflets.

Areas for improvement Very few examples of packs of bagged salad under 100g were found (10% of 2011 sample, down from 14% of the 2009 sample). An increased proportion of branded bagged salad in the 2011 sample (34%, up from 25%) brought with it more larger, rather than smaller, packs with 15% of branded salad now falling in the 201-250g range. Only 2% of branded salads were found in each of the smallest size brackets (100g or less; 101 to 150g). Although the proportion of bagged salad split into smaller sections increased from 2% in 2009 to 9% in 2011. Despite regulatory changes which now allow for pre-packed bread in non-standard sizes, very few packs of bread were found in anything other than 400g or 800g sizes. There was a slight increase in availability of 400g loaves, from 28% to 35% between the two samples.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 7

There were examples of steep, linear price gradients (£/kg), resulting in a strong incentive to buy bigger packs, e.g. for potatoes, orange juice, bacon and world breads. There was a high premium for the smallest packs of carrots and bagged salad. There was a high level of promotion on many products in the survey, for example:

51% of single yoghurts were associated with a promotion in 2011, and 93% of these promotions were multi-buy offers.

40% of multipack yoghurts were associated with a promotion, and 76% of these promotions were multi-buy offers.

38% of pre-packed ham was found to be on offer, a similar level to that found in the 2009 sample (36%). The majority of these were multi-buy within the product category (54%), although a reasonable proportion were cross category promotions (36%). Almost twice the proportion of own-brand pre-packed ham as branded was promoted (41% and 22% respectively).

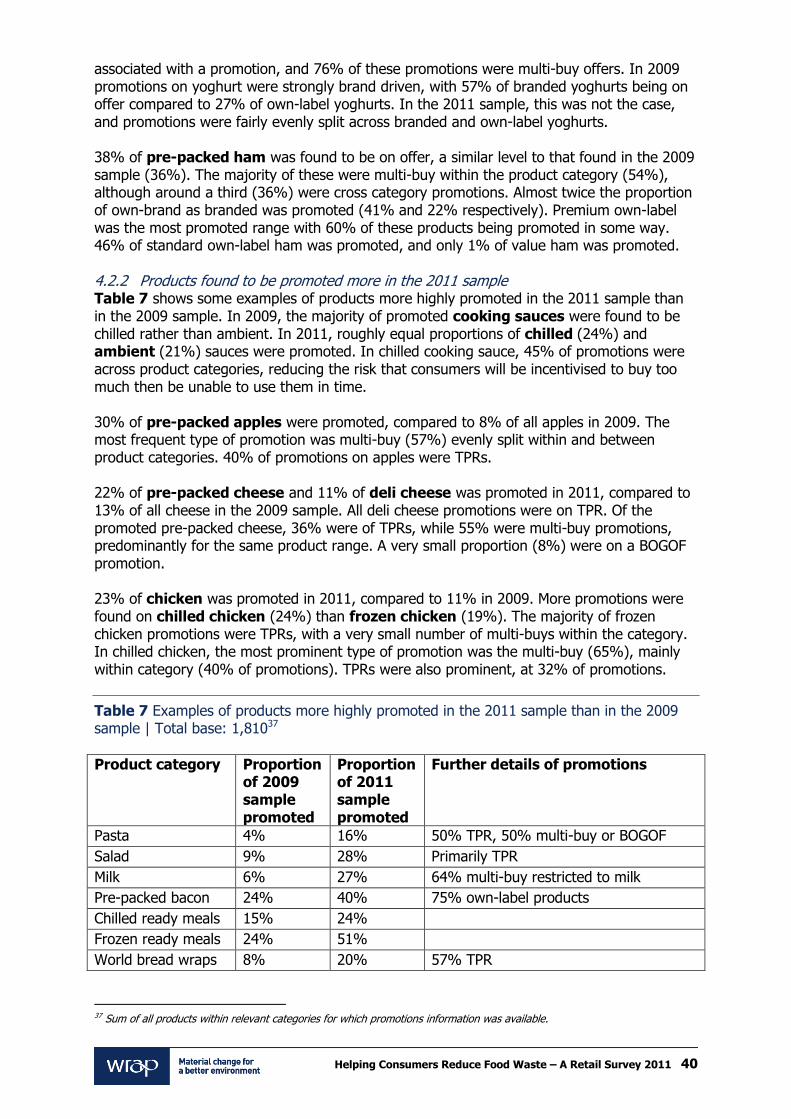

30% of pre-packed apples were promoted, compared to 8% of all apples in 2009. The most frequent type of promotion was multi-buy (57%) evenly split within and between product categories. 40% of promotions on apples were temporary price reductions (TPR).

22% of pre-packed cheese and 11% of deli cheese were promoted in 2011, compared to 13% of all cheese in the 2009 sample.

23% of chicken was promoted in 2011, compared to 11% in 2009. As detailed in WRAP’s research12, retailers should be conscious of the potential for promotions to lead to food waste, their customers’ perception that promotions lead to food waste, and the needs of different types of household, and take this into consideration when planning promotional strategies, especially for perishable, short shelf life products (in terms of which type of promotion, product shelf life, pack sizes chosen etc.). Highlighting what can be frozen on-pack, providing freezing tips at the shelf edge alongside the promotional offer, maximising given shelf life, having clear date labelling, providing flexible meal plans and encouraging batch cooking / freezing (e.g. cook once eat twice) will all help ensure consumers get real value from a promotion rather than food ending up being thrown away. Figure E3 gives a recent example found in Sainsbury’s.

Figure E3 In-store communications to promote freezing extra items, bought on promotion

On packs of pasta, in contrast to rice, there appears to have been a decrease in re-closability, from 73% of the 2009 sample to 56% of the 2011 sample. There was a decrease

12 Investigation into the Possible Impact of Promotions on Food Waste, WRAP, 2011

Helping Consumers Reduce Food Waste – A Retail Survey 2011 8

in the number of packs of ham that were re-closable between 2009 (11%) and 2011. In 2009, 21% of rolls (including ISB rolls sold in packs) came in re-closable packs. In 2011 the proportion of packed rolls (including ISB rolls sold in packs) that were re-closable was 14%. If this functionality is not suitable for packs of pasta, promoting the use of food clips or of guidance advising that the product should be stored in an airtight container once opened is advised. On-pack storage guidance on where to keep potatoes in 2011 was quite varied. 18% said simply store somewhere dark, 17% somewhere cool and dry, 37% somewhere cool and dark, and 28% somewhere cool, dry AND dark. In line with WRAP’s research13 and guidance from the Potato Council, potato packs would ideally be consistently labelled ‘keep in a cool, dark place’. As in 2009, no pre-packed potatoes carried portion guidance. FSA guidance states that where specific temperature guidance is given, for products to be

stored in the fridge, this guidance should be ‘below 5C’. 31% of chilled products specified a temperature or range of temperatures at which the products should be kept. The vast majority (81%) of these products carried guidance conforming to the FSA standard.

30% of instances of this guidance on chilled products stated specifically that the product

should be stored ‘below 5C’.

The remaining 70% gave a range of temperatures, of which 5C was the top of range

value, e.g. ‘store at 0-5C’ or ‘store at between 2 and 5C’.

As in 2009, storage guidance for eggs was quite consistent. 98% of eggs reviewed carried guidance to refrigerate. However, 48 packs of eggs (9%) suggested ‘Store in a cool, dry place OR keep refrigerated’. The presence of storage guidance on ISB bread was a lot lower than that found in the 2009 sample, at 14% compared to 55%. The proportion of ISB bread carrying freezing guidance also fell from 28% to 1% between 2009 and 2011. For ISB rolls, however, this trend was reversed: while none carried freezing guidance in 2009, 7% did so in 2011. This suggests that there is scope to substantially increase the prevalence of freezing guidance on ISB products. The proportion of bread giving freezing guidance had decreased between the two samples from 91% in 2009 to 82% in 2011. For most of the other freezable products, there had been no increase (or decrease) with just 63% of all freezable products carrying freezing guidance and 45% carrying defrosting guidance (i.e. not all freezing guidance was accompanied with defrosting guidance). The number of milk packs carrying snowflake/star freezing symbols doubled from 4% of the 2009 sample to 8% in 2011, despite the proportion of products carrying freezing guidance remaining constant between the two samples (24%) and 12% of milk packs stating that they were not suitable for freezing. Still the most common form of freezing guidance was ‘freeze on day of purchase’ (79%). (Changes such as those detailed in Figure E2 are subsequent to the fieldwork being carried out and so are not reflected in this data.) A higher proportion of bread packs in 2011 stated they needed to be used within just 1 month of freezing than in 2009 (31% and 28%). Nearly all chilled chicken (96%) reviewed in 2011 carried guidance to use within one month of freezing, compared to 76% in 2009.

13 Reducing supply chain and consumer potato waste, WRAP, 2012

Helping Consumers Reduce Food Waste – A Retail Survey 2011 9

The proportion of chilled cooking sauces carrying guidance to use within one month of freezing increased from 87% in 2009 to 97% in the 2011 sample. Where this guidance was given for chicken and chilled cooking sauces, consumers were always given one month to use these products (in 2009 as in 2011). Increases in the prevalence of guidance to ‘use within one month of freezing’ between 2009 and 2011, therefore, reflect an overall increase in use of this type of guidance for these products, rather than a shortening of the amount of time consumers are being given. In 2011, 25% of all yoghurts (both single and multipack) displayed guidance not to freeze. 6% of yoghurts in 2011 employed a crossed out snowflake symbol alongside this guidance. 12% of milk packs stated that they were not suitable for freezing, despite the fact that milk is a freezable product, and 24% of milk packs did carry freezing guidance. 4% of orange juice advised against freezing, again despite being a freezable product, with 19% of packs surveyed carrying freezing guidance. In addition to the snowflake logo, several other, potentially confusing logos were noted e.g.

crossed out snowflake to mean both do not freeze and do not refreeze;

snowflake logos to mean keep refrigerated and keep frozen;

polar bears to highlight defrosting guidance; and

igloos to mean suitable for freezing. In contrast to the increased consistency of date type within cheese, noted above, the proportions of ‘use by’ and ‘best before’ dates on yoghurts were similar in the 2009 and 2011 samples – 77% and 76% carried a ‘use by’ date, respectively, compared to 23% and 24%, which carried a ‘best before’ date. Only branded pots of yoghurt, both single (69% of branded) and multipack (21% of branded), carried ‘best before’ dates in 2011. A worked example, developed by Dairy UK, for yoghurt was included in the Defra decision tree14, to support decision-making around which date type to use on products. Guidance such as ‘Do not exceed the use by date’ is helpful to consumers and reinforces the message that ‘use by’ dates are about safety. It was found on 27% of products which carried a ‘use by’ date in the 2011 sample. Guidance not to exceed the date was also found on some products which carried a ‘best before’ date. This is not helpful to consumers, as it effectively converts a ‘best before’ date into a ‘use by’ date, and is likely to confuse consumers and prompt them to think of ‘best before’ dates as safety dates, when in fact they refer to food quality. This guidance was found on 8% of products which carried a ‘best before’ date in the 2011 sample. One category particularly stands out; it was found on over a quarter (28%) of cheese, which in some ways negates the general shift towards use of ‘best before’ rather than ‘use by’ type dates on this product. Summary of progress since 2009 Table E1 compares progress against the industry recommendations WRAP made in the last survey report.

14 Guidance on the application of date labels to food, Defra, 2011. Available at: http://www.defra.gov.uk/publications/2011/09/15/pb13629-food-labels

Helping Consumers Reduce Food Waste – A Retail Survey 2011 10

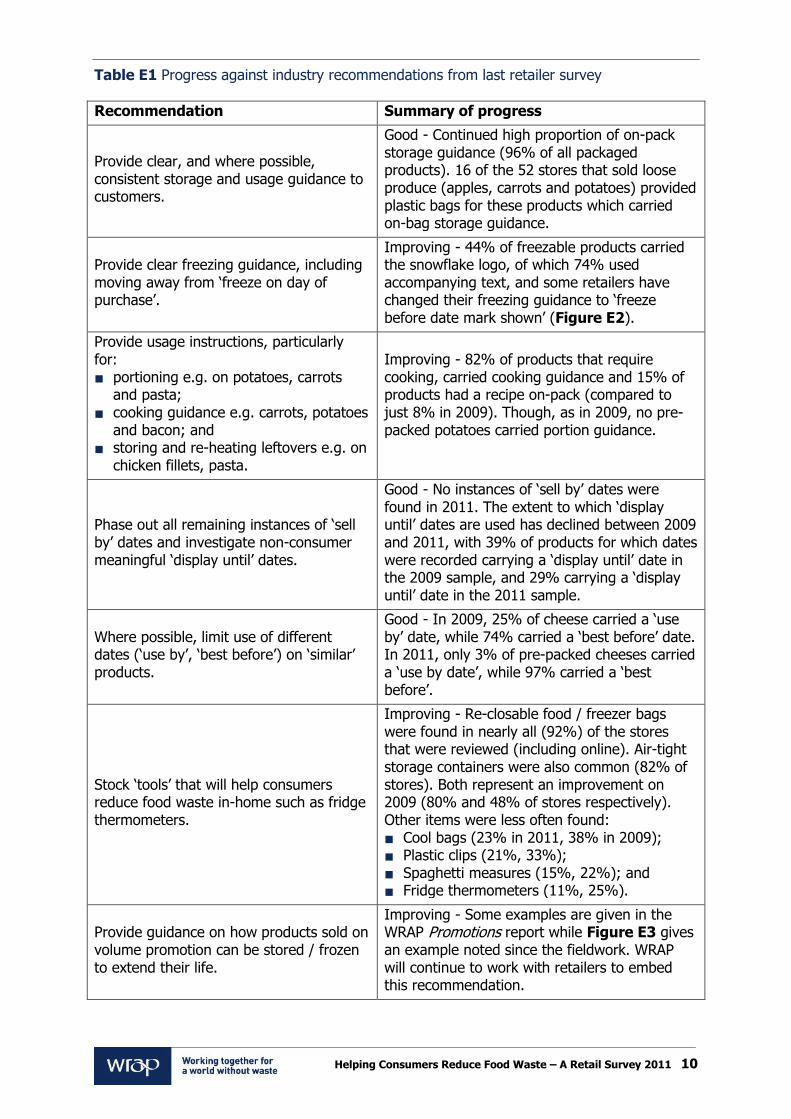

Table E1 Progress against industry recommendations from last retailer survey

Recommendation Summary of progress

Provide clear, and where possible, consistent storage and usage guidance to customers.

Good - Continued high proportion of on-pack storage guidance (96% of all packaged products). 16 of the 52 stores that sold loose produce (apples, carrots and potatoes) provided plastic bags for these products which carried on-bag storage guidance.

Provide clear freezing guidance, including moving away from ‘freeze on day of purchase’.

Improving - 44% of freezable products carried the snowflake logo, of which 74% used accompanying text, and some retailers have changed their freezing guidance to ‘freeze before date mark shown’ (Figure E2).

Provide usage instructions, particularly for:

portioning e.g. on potatoes, carrots and pasta;

cooking guidance e.g. carrots, potatoes and bacon; and

storing and re-heating leftovers e.g. on chicken fillets, pasta.

Improving - 82% of products that require cooking, carried cooking guidance and 15% of products had a recipe on-pack (compared to just 8% in 2009). Though, as in 2009, no pre-packed potatoes carried portion guidance.

Phase out all remaining instances of ‘sell by’ dates and investigate non-consumer meaningful ‘display until’ dates.

Good - No instances of ‘sell by’ dates were found in 2011. The extent to which ‘display until’ dates are used has declined between 2009 and 2011, with 39% of products for which dates were recorded carrying a ‘display until’ date in the 2009 sample, and 29% carrying a ‘display until’ date in the 2011 sample.

Where possible, limit use of different dates (‘use by’, ‘best before’) on ‘similar’ products.

Good - In 2009, 25% of cheese carried a ‘use by’ date, while 74% carried a ‘best before’ date. In 2011, only 3% of pre-packed cheeses carried a ‘use by date’, while 97% carried a ‘best before’.

Stock ‘tools’ that will help consumers reduce food waste in-home such as fridge thermometers.

Improving - Re-closable food / freezer bags were found in nearly all (92%) of the stores that were reviewed (including online). Air-tight storage containers were also common (82% of stores). Both represent an improvement on 2009 (80% and 48% of stores respectively). Other items were less often found:

Cool bags (23% in 2011, 38% in 2009);

Plastic clips (21%, 33%);

Spaghetti measures (15%, 22%); and

Fridge thermometers (11%, 25%).

Provide guidance on how products sold on volume promotion can be stored / frozen to extend their life.

Improving - Some examples are given in the WRAP Promotions report while Figure E3 gives an example noted since the fieldwork. WRAP will continue to work with retailers to embed this recommendation.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 11

Recommendations from 2011 survey On the basis of the insights from this 2011 data collection exercise, WRAP is keen to work with the food industry to:

Continue the excellent progress to remove ‘display until’ dates, and to increase consistency of ‘use by’ or ‘best before’ date type use within a product category, where appropriate.

Increase use of storage guidance that reinforces what the ‘use by’ date means e.g. ‘Do not exceed use by date’ and decrease similar advice for ‘best before’ date products.

Increase proportion of freezable products that carry freezing and defrosting guidance. Highlight this on the front of pack where possible using the snowflake logo, and consider how to amplify this type of guidance during a volume promotion.

Increase use of alternative freezing guidance, and communicate these changes to customers e.g. using the ‘Freeze before / date mark’ label rather than stating to ‘Freeze on day of purchase’.

Reduce use of the snowflake logo to indicate anything other than ‘suitable for home freezing’. Reduce use of other logos to indicate products can be frozen.

Continue to provide clear storage guidance that is consistent within a product category, where appropriate, for both packed and loose formats.

Follow FSA recommended ‘keep refrigerated below 5oC’ where fridge temperature guidance is stated on-pack.

Extend shelf life where possible (without reducing quality or increasing food safety risks):

Extend the ‘best before’ or ‘use by’ date.

Extend ‘Use within x days of opening’.

Extend ‘Use within x months of freezing’.

Continue to provide cooking and portioning information on-pack, and develop pack functionality that aids portioning and extends open shelf life e.g. by being re-closable.

Continue improvements in availability of smaller pack sizes / loose variants, where appropriate. Where it is not possible to provide smaller packs, investigate how to provide guidance on optimising storage, freezing and using leftovers.

Increase the provision and accessibility of tools that help prevent food waste in the home e.g. air-tight storage containers and bag clips, for example, signposting to them from the relevant fixtures.

Use Love Food Hate Waste materials to raise awareness of the benefits of reducing food waste and engaging consumers to act. Continue to use existing communication channels to raise awareness of the benefits (both financial and environmental) of reducing food waste, and provide tips / guidance to optimise in-home storage and food use e.g. through recipes.

WRAP will continue to provide updated guidance documents and support to industry to help implement recommendations. Suggested further research / next steps 1. Investigate the optimum approach to date labelling for fresh produce - In 2011, 10% of pre-packed apples, 16% of pre-packed potatoes and 18% of pre-packed carrots carried a ‘display until’ date only (i.e. no ‘best before’ date) while 4% of carrots and potatoes and 36% of apples carried no date at all. WRAP investigated consumer preference with regards date type on fresh produce through its Consumer Insight project but the findings were not conclusive. In the short-term, the food industry is encouraged to simplify the approach to labelling fruit & vegetables in line with the main recommendations from that study. They are also encouraged to extend shelf life where possible (particularly in line with seasonality), and reinforce optimum storage guidance and the meaning of the date labels. It is suggested that

Helping Consumers Reduce Food Waste – A Retail Survey 2011 12

further in-store trials are conducted to determine the optimum approach to date labelling for fresh fruit and vegetables, and any impact on wastage in-store and at home. 2. Discuss initial findings (Box E1) relating to which factors influence given life15 and open life16 with the food industry to determine where the greatest potential to safely extend shelf life to reduce food waste exists and how this would be best approached.

Box E1 – Initial findings (discussed in Section 8) suggest there can be substantial variation in given lives within a particular product category. Variables which seemed to be most important in differences in given life were:

The supermarket/retailer selling the product;

The particular brand;

The range of own label products (e.g. premium, standard, value); and

Whether a product was on promotion. Regarding open shelf life, there appeared to be a trend, on average across the products, towards an increased proportion of products having ‘once opened’ guidance, and towards shorter recommended open lives. Again, in most cases, open life was longer for branded

than for own-label products.

3. Continue to develop relevant messages and materials through Love Food Hate Waste that can be used by industry to communicate to customers.

4. Continue to recognise progress, good practice and areas for improvement by repeating the Retail Survey in early 2013 to review changes to the retail environment since 2011.

15 The number of days between the date a product is audited (purchased in store or received from an online order) and the ‘use-by’ or ‘best before’ date (or ‘display until’ date where that is the only date present). 16 The number of days given to the consumer to eat the product once it has been opened, as according to instructions on the packaging: ‘use within x days’.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 13

Contents

1.0 Introduction ............................................................................................... 17 1.1 Background to this study .......................................................................... 17 1.2 What data were collected? ........................................................................ 17 1.3 How to use this report .............................................................................. 21

2.0 Methods ...................................................................................................... 22 2.1 Key data collected .................................................................................... 22 2.2 Changes to what data were collected since 2009 ........................................ 22 2.3 A note on comparisons between 2009 and 2011 ......................................... 23 2.4 Where were the data collected? ................................................................ 23 2.5 How were the data collected? ................................................................... 25 2.6 Analysis ................................................................................................... 25

3.0 Pack size range, availability, pack features and price ................................ 26 3.1 Pack size range ........................................................................................ 26

3.1.1 A note about the interplay of pack size and food management........... 26 3.1.2 Products for which consumers had a limited choice of pack size ......... 26 3.1.3 Products for which pack size is less of an issue ................................. 27 3.1.4 Apparent improvements in availability of pack size ............................ 29 3.1.5 New pack sizes appearing in the sample .......................................... 29 3.1.6 Products where there is an opportunity to develop smaller pack sizes . 30

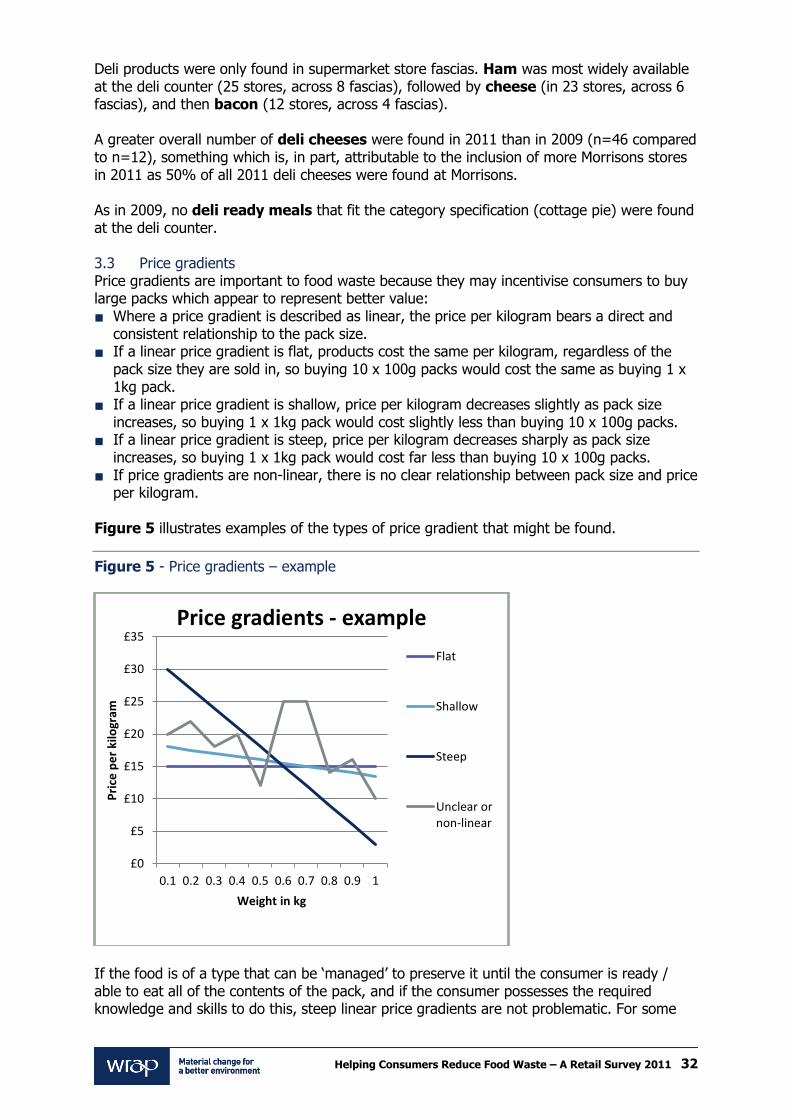

3.2 Availability of deli / loose products ............................................................. 31 3.3 Price gradients ......................................................................................... 32

3.3.1 Steep linear price gradients............................................................. 33 3.3.2 High premium for smallest pack ...................................................... 33 3.3.3 Unclear or non-linear price gradients ............................................... 34

3.4 Pack functionality ..................................................................................... 34 3.4.1 Some excellent examples of pack functionality.................................. 34 3.4.2 Potential to improve product life through pack functionality ............... 38

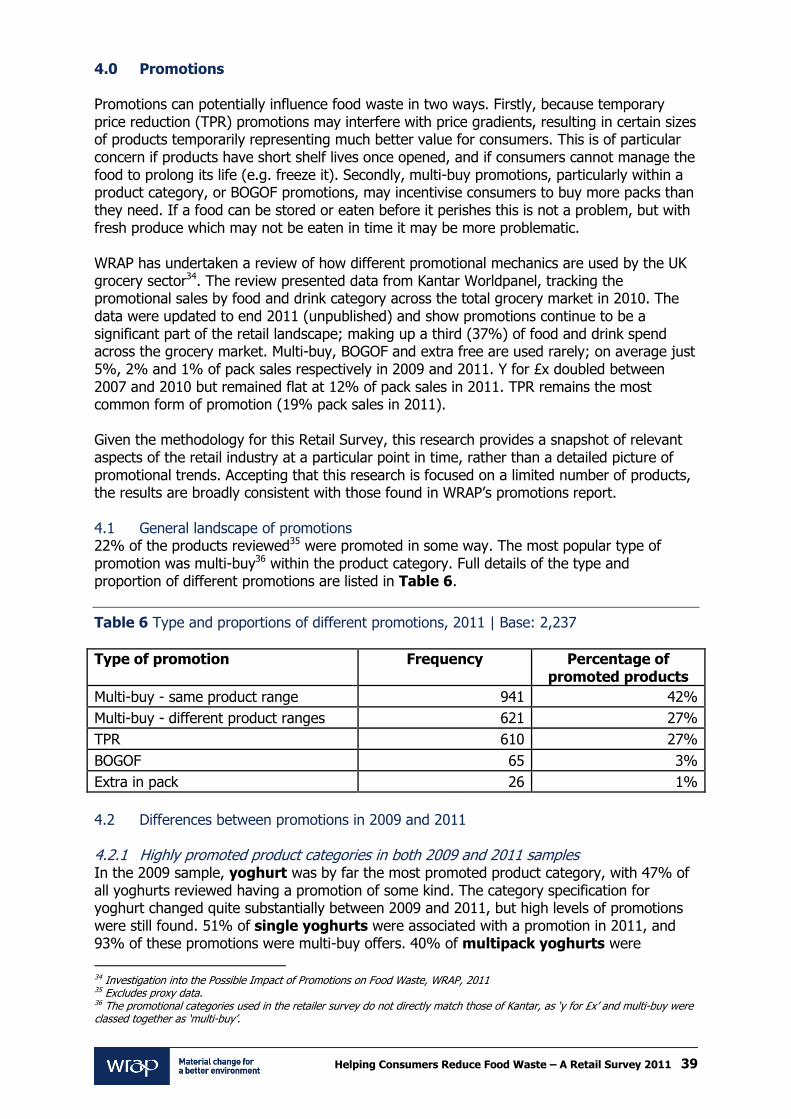

4.0 Promotions ................................................................................................. 39 4.1 General landscape of promotions ............................................................... 39 4.2 Differences between promotions in 2009 and 2011 ..................................... 39

4.2.1 Highly promoted product categories in both 2009 and 2011 samples .. 39 4.2.2 Products found to be promoted more in the 2011 sample .................. 40 4.2.3 Products less promoted than in 2009 ............................................... 41

4.3 Influence of pack volume on promotions .................................................... 41 5.0 Storage guidance ........................................................................................ 42

5.1 Presence of guidance and guidance given .................................................. 42 5.1.1 Headline examples of good or improved guidance............................. 42 5.1.2 Guidance which could be improved .................................................. 43 5.1.3 Encouraging consumers to re-close the pack .................................... 44 5.1.4 Guidance on deli / loose / ISB products ........................................... 44

5.2 Fridge temperature guidance .................................................................... 45 5.2.1 Product categories found to carry specific temperature guidance ....... 46 5.2.2 Temperature values given............................................................... 46 5.2.3 Product categories largely in line with FSA temperature guidelines ..... 47 5.2.4 Product categories with guidance varying from FSA guidelines ........... 48

5.3 Use of on pack ‘flash’ – storage guidance ................................................... 48 5.4 Retail environment in which products are stored ......................................... 50

6.0 Freezing and defrosting guidance .............................................................. 51 6.1 Freezability of products ............................................................................. 51 6.2 Presence of guidance ............................................................................... 51

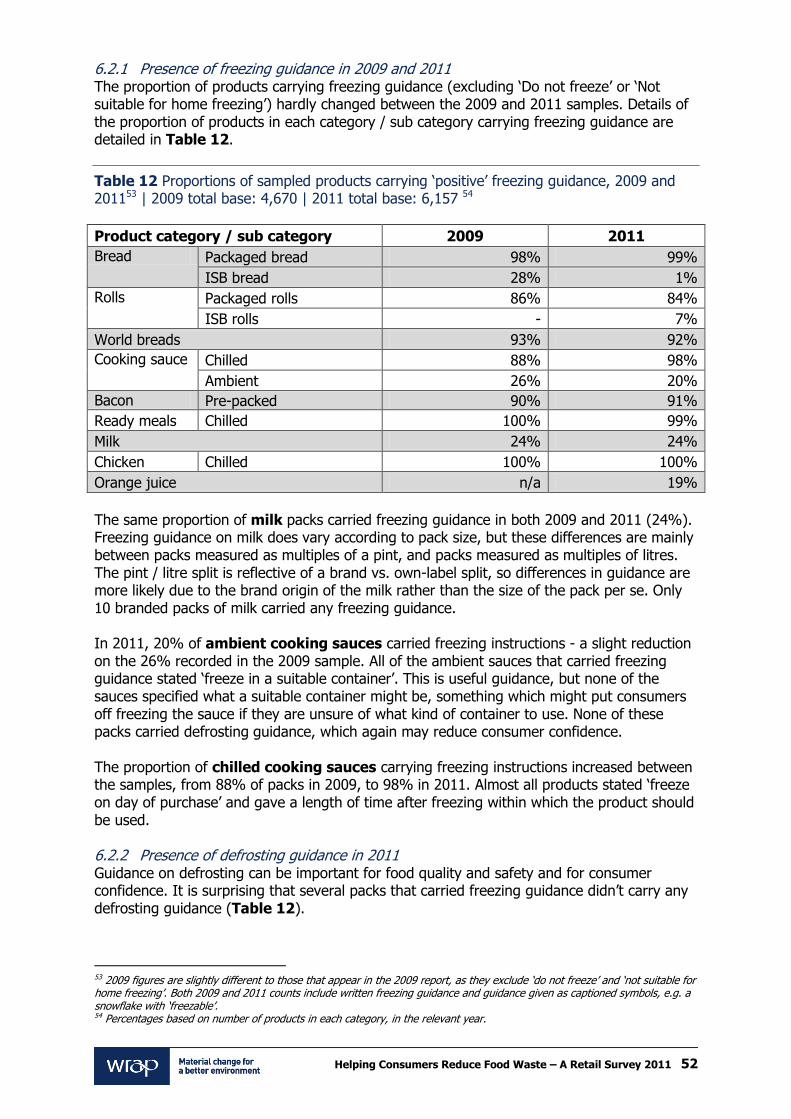

6.2.1 Presence of freezing guidance in 2009 and 2011 .............................. 52

Helping Consumers Reduce Food Waste – A Retail Survey 2011 14

6.2.2 Presence of defrosting guidance in 2011 .......................................... 52 6.2.3 Presence of guidance on loose / deli products .................................. 53

6.3 Freezing guidance given in 2011 ............................................................... 54 6.3.1 Guidance on when to freeze ........................................................... 54 6.3.2 Guidance on how long to freeze ...................................................... 55 6.3.3 Freezer star marking guidance ........................................................ 58

6.4 Use of on pack ‘flash’ – freezing guidance .................................................. 59 6.5 Freezing symbols ..................................................................................... 59

6.5.1 Use of snowflake logo .................................................................... 59 6.5.2 Use of snowflake logo to denote refrigeration guidance ..................... 62 6.5.3 Other freezing symbols found ......................................................... 63 6.5.4 Use of symbols on frozen products .................................................. 65

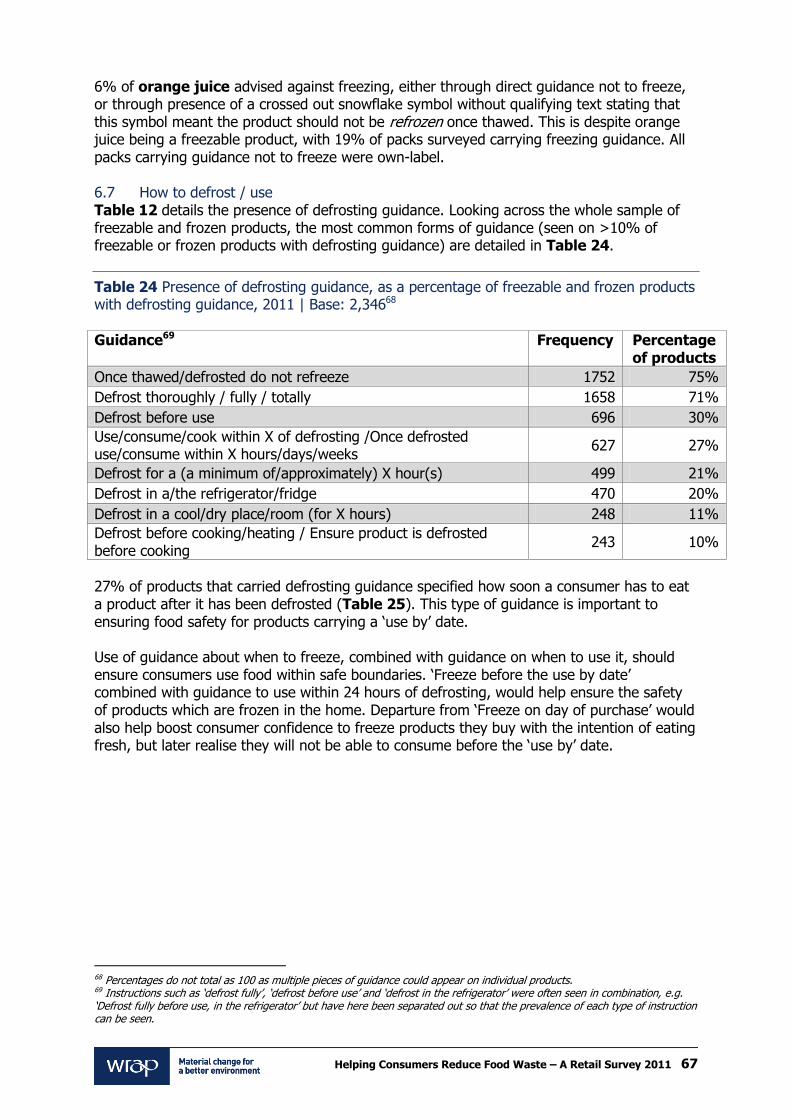

6.6 Warning not to freeze ............................................................................... 65 6.7 How to defrost / use ................................................................................ 67 6.8 Guidance not to refreeze .......................................................................... 69

7.0 Date labels .................................................................................................. 70 7.1 Use of ‘best before’ and ‘use by’ ................................................................ 70

7.1.1 Product specific examples ............................................................... 73 7.1.2 ‘Other’ types of date ....................................................................... 74

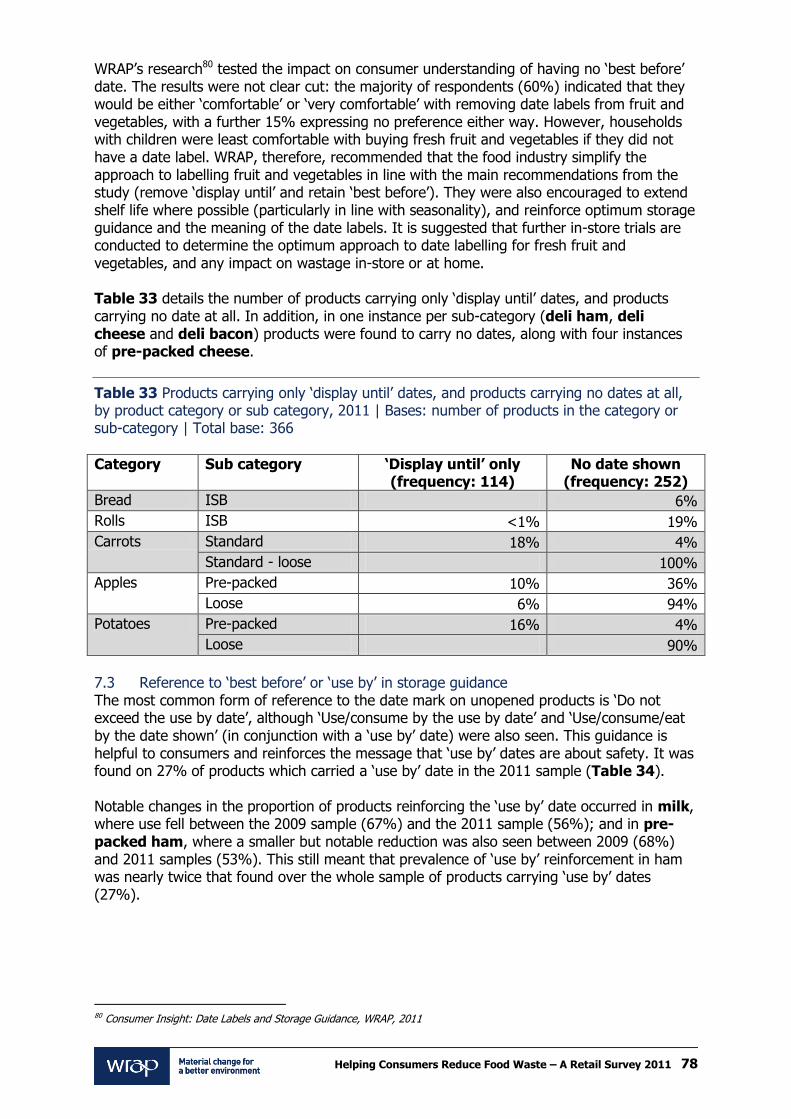

7.2 Use of ‘display until’ ................................................................................. 74 7.2.1 Use of only ‘display until’ date, or no date ........................................ 77

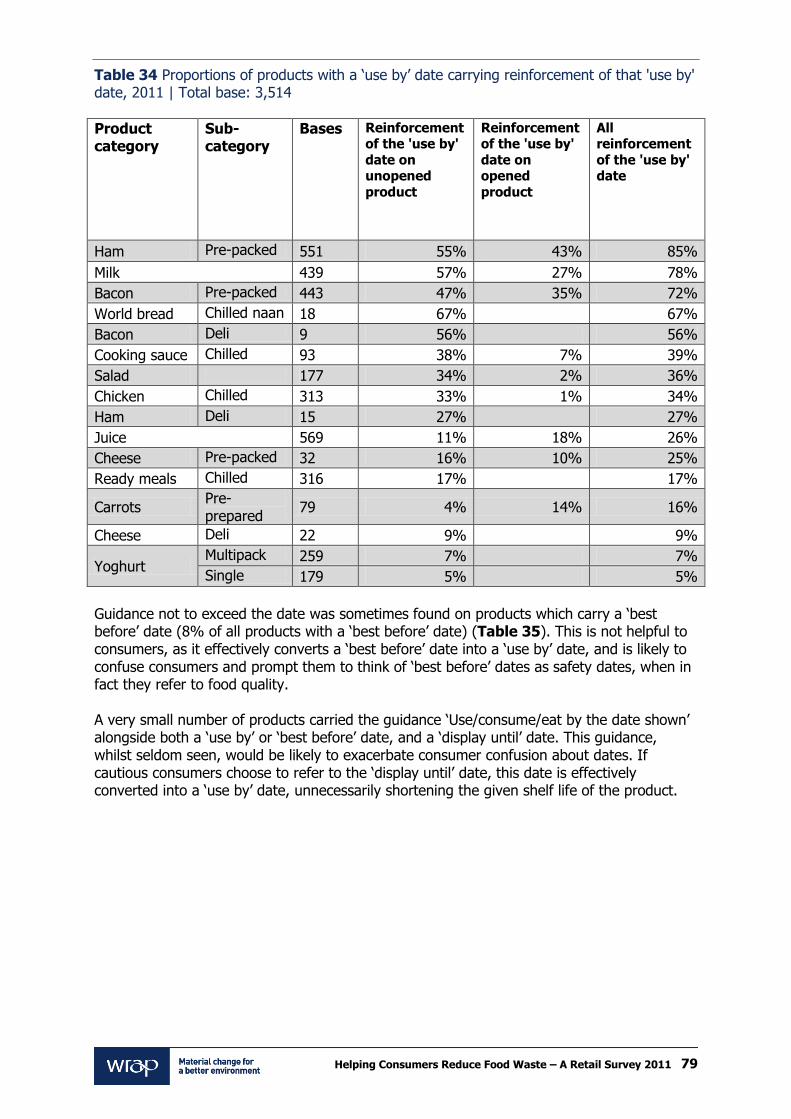

7.3 Reference to ‘best before’ or ‘use by’ in storage guidance ............................ 78 8.0 Shelf life ..................................................................................................... 81

8.1 Given life ................................................................................................. 83 8.1.1 Comparison of branded and own-label products ............................... 86 8.1.2 Impact of date type ....................................................................... 88 8.1.3 Other factors influencing given life .................................................. 89

8.2 Open life ................................................................................................. 90 8.2.1 Changes in open life since 2009 ...................................................... 91 8.2.2 Comparison of branded and own-label products ............................... 91 8.2.3 Other factors of influence on open life ............................................. 92

8.3 Given shelf life according to the ‘display until’ date ..................................... 92 9.0 Cooking and portioning guidance ............................................................... 94

9.1 Presence of cooking guidance ................................................................... 94 9.2 Presence of recipes .................................................................................. 94 9.3 Presence of portioning guidance ................................................................ 95 9.4 Tips ........................................................................................................ 99

10.0 Point of sale information .......................................................................... 100 10.1 Online links ............................................................................................ 100 10.2 Extra information on loose bags .............................................................. 100 10.3 Shelf edge labels .................................................................................... 101 10.4 Leaflets, e.g. recipe cards ....................................................................... 101 10.5 Banners ................................................................................................ 102 10.6 Availability of tools to help prevent consumer food waste .......................... 102

11.0 Closing remarks ........................................................................................ 104 11.1 Key developments since 2009 ................................................................. 104 11.2 Recommendations for industry ................................................................ 105

Appendix 1 – Product category scope 2009 - 2011 ............................................ 106 Appendix 2 - Data collection methodology ......................................................... 109

Helping Consumers Reduce Food Waste – A Retail Survey 2011 15

Glossary

BAH – bake at home – part baked bread or bread rolls for consumers to finish cooking in the home.

‘Best before’ dates – the date of minimum durability of a food, until which the foodstuff retains its specific properties when properly stored. Refers to quality rather than food safety. When the date is passed, the food won’t be unsafe but might begin to lose its flavour and texture.

BOGOF – buy one get one free promotion – applies to identical items only.

Freezable – products which commonly carry freezing guidance, and which can be home frozen and defrosted without quality change.

FODOP – freeze on day of purchase – an abbreviation of the common freezing guidance.

Given shelf life – the number of days between the date a product is audited (purchased in store or received from an online order) and the ‘use-by’ or ‘best before’ date (or ‘display until’ date where that is the only date present).

ISB – in-store bakery – products baked in-store and packaged or sold loose.

MAP - modified atmosphere packaging e.g. pack states ‘packed in protective atmosphere’.

Multi-buy – promotion where more than one of a product is within the promotion either another of the same product or another within the category (e.g. buy any two from the sliced meat range for £x).

On pack ‘flash’ – prominent logo or consumer instruction (e.g. to freeze the product).

Open shelf life – the number of days given to the consumer to eat the product once it has been opened, as according to instructions on the packaging: ‘use within x days’.

Packed product – any product sold in a pack which determines the amount of product a consumer can buy. Includes packaged ISB goods, but excludes loose or deli products.

Pre-packed product – used here in reference to bread and rolls to distinguish them from ISB, deli or loose goods.

Price gradient – describes the correlation between pack price and pack size.

POS – point of sale – communication material displayed at the point of sale e.g. shelf edge labels, recipe cards.

Product category – description of each product type reviewed in this research, see Appendix 1 for details.

Shelf life – the period of time for which a product remains safe and meets its quality specifications under expected storage and use. The shelf life determines the durability date and is expressed as a ‘use by’ or ‘best before’ date on a product17.

SKU – stock keeping unit – a unique product.

Store fascia – type of store e.g. supermarket, convenience / local store or online.

TPR – temporary price reduction promotion.

‘Use by’ dates – In the case of food which, from the microbiological point of view, are highly perishable and are therefore likely after a short period to constitute an immediate danger to human health, the date of minimum durability (‘best before’ date) is replaced by the ‘use by’ date. Food can be eaten up to the end of the ‘use by’ date, but not after even if it looks and smells fine.

17 As described in Articles 9 and 10 of Directive 2000/13/EC. (Source: EC guidance on Listeria monocytogenes shelf life studies for ready-to-eat foods, under Regulation (EC) No 2073/2005).

Helping Consumers Reduce Food Waste – A Retail Survey 2011 16

A note about use of ‘base’ and ‘n’ in this document Throughout this report, the terms ‘base’ and ‘n’ are used to quantify figures in tables. These terms are not interchangeable, and in this report they are used as follows:

Base - the number of relevant samples from which percentages are drawn; and

Frequency (expressed in shorthand as 'n=') or the number of occurrences.

So if the base is 100, and a feature is found on 30% of packs, n=30. The term 'Total base' is used where row percentages (individually ‘based’ figures) are nested within a larger table (e.g. 30% of pre-packed bread carried x feature, while 10% of ISB bread did, etc.). The total base is used to express the overall number of relevant samples which the information in the table is drawn from.

Acknowledgements

With particular thanks the staff of all the major UK retailers who enabled our field workers to undertake in-store survey work and to our field workers who collected all the data for analysis. WRAP also wishes to thank the Brook Lyndhurst research team: David Fell, Michael Fernandez, Sara Giorgi, Ruth Townend, Margot Tong and Susie Stevenson.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 17

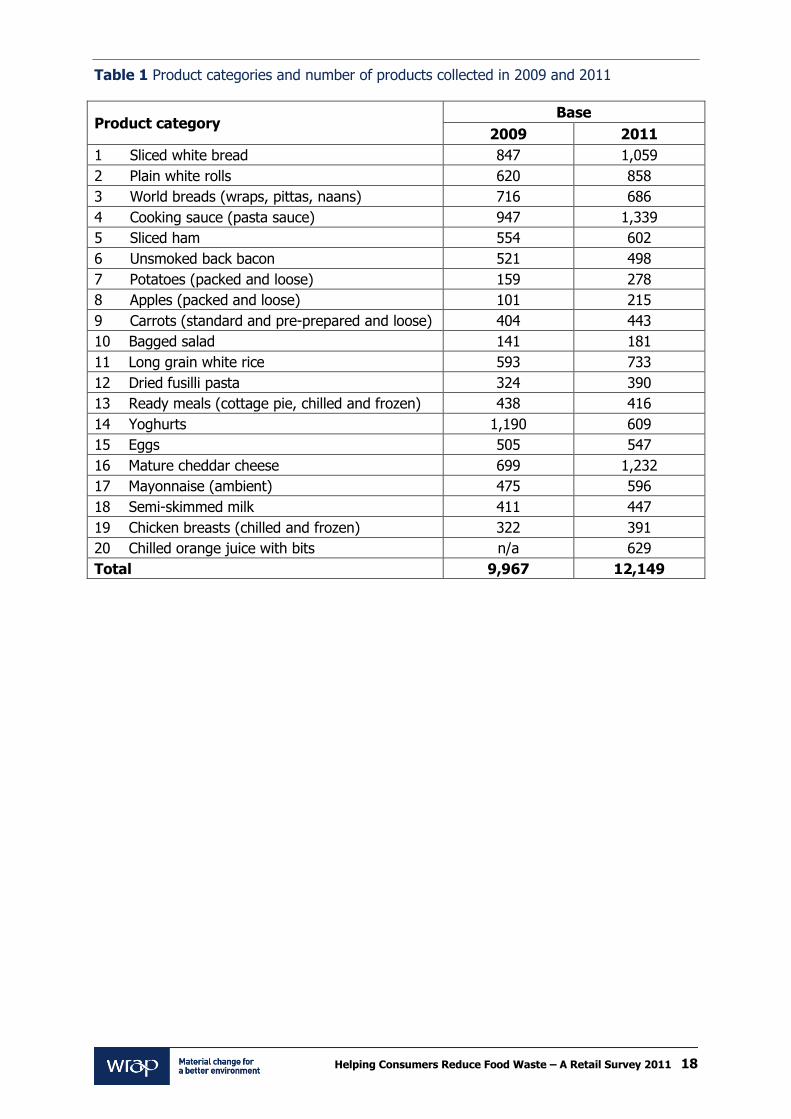

1.0 Introduction 1.1 Background to this study In 2009, WRAP published Household Food and Drink Waste in the UK18. This found that ca. 8.3 million tonnes of food and drink is thrown away each year in the UK (22% of all the food and drink purchased) and 5.3 million tonnes of this could have been eaten. WRAP announced a reduction in total household food and drink waste of 1.1 million tonnes in November 201119. Consumer’s knowledge and understanding of how to store and use foods in the home will influence the amount of food waste. Similarly, availability of, and incentives to buy, appropriately sized packs of food can prevent or lead to wastage. Many decisions about what guidance is available to consumers with respect to storage and use of foods, and decisions about the availability of different pack sizes, are in the hands of retailers and manufacturers. This research provides a snapshot of relevant aspects of the retail industry at a particular point in time. It seeks to inform WRAP’s work with retailers and manufacturers through the Courtauld Commitment20, in order to enable change and widespread adoption of good practice, with the aim of reducing consumer food waste. In early 2011, Brook Lyndhurst set out to review the labelling and packaging of key products in the UK retail sector. Data were collected on some 12,000 products, in twenty product categories, stocked by ten major retailers across the UK. This work was a repeat of a data collection exercise conducted by Brook Lyndhurst and ESA in 2009, which looked at approximately 10,000 products, split into nineteen product categories. This report summarises the key findings from the 2011 research, creating a new baseline from which changes in the UK retail environment may be measured. Where comparable data existed, this report documents change, or lack of change, since 2009. 1.2 What data were collected? Data were collected on twenty key product categories, which are listed below. The product categories in 2011 were broadly consistent with 2009, although minor adjustments were made to reflect WRAP’s areas of interest, as well as lessons learned about the practicalities of the data collection process in the course of the 2009 research. Product categories in 2009 had been selected on the basis that WRAP’s research21 had shown them to be high waste categories, and included an understanding of which food types are most commonly discarded, and in what state (e.g. whole, unopened, opened but uncooked, leftover etc.). An additional category, chilled orange juice, was added to the sample in 2011. This addition reflects the fact that fruit juice is very commonly wasted, and has some of the same challenges (in terms of storage / freezing guidance) as other chilled food products. Full details of all twenty product categories, including a description of the new category and details of the original nineteen categories, as well as any modifications for the 2011 research, can be found in Appendix 1. A summary of the 2011 categories can be found in Table 1.

18 Household Food and Drink Waste in the UK, WRAP, 2009. 19 New estimates for household food and drink waste in the UK, WRAP, 2011. Available at: www.wrap.org.uk/hhfwfacts 20 See: http://www.wrap.org.uk/retail_supply_chain/voluntary_agreements/courtauld_commitment/index.html 21 Household Food and Drink Waste in the UK, WRAP, 2009

Helping Consumers Reduce Food Waste – A Retail Survey 2011 18

Table 1 Product categories and number of products collected in 2009 and 2011

Product category Base

2009 2011

1 Sliced white bread 847 1,059

2 Plain white rolls 620 858

3 World breads (wraps, pittas, naans) 716 686

4 Cooking sauce (pasta sauce) 947 1,339

5 Sliced ham 554 602

6 Unsmoked back bacon 521 498

7 Potatoes (packed and loose) 159 278

8 Apples (packed and loose) 101 215

9 Carrots (standard and pre-prepared and loose) 404 443

10 Bagged salad 141 181

11 Long grain white rice 593 733

12 Dried fusilli pasta 324 390

13 Ready meals (cottage pie, chilled and frozen) 438 416

14 Yoghurts 1,190 609

15 Eggs 505 547

16 Mature cheddar cheese 699 1,232

17 Mayonnaise (ambient) 475 596

18 Semi-skimmed milk 411 447

19 Chicken breasts (chilled and frozen) 322 391

20 Chilled orange juice with bits n/a 629

Total 9,967 12,149

Helping Consumers Reduce Food Waste – A Retail Survey 2011 19

1.2.1 Sub-categories A number of product categories were further split into sub-categories, which sometimes reflect differences in the format of a product, e.g. yoghurts – single and multipack, and sometimes reflect deeper splits in the category, e.g. chicken – chilled or frozen, or world breads – pittas, wraps, naans. Table 2 details the sub-categories into which products were split, and lists the numbers reviewed in each sub-category.

Table 2 Number of products reviewed in each category or sub-category, 2011 | Base: 12,149

Product category Sub-category Base

Bread Pre-packed 882

ISB 177

Rolls Pre-packed 624

ISB 234

World bread Pittas 193

Wraps 290

Naans – ambient 172

Naan – chilled 31

Cooking sauce Chilled 98

Ambient 1,241

Ham Pre-packed 569

Deli 33

Bacon Pre-packed 486

Deli 12

Potatoes Pre-packed 257

Loose 21

Apples Pre-packed 146

Loose 69

Carrots Standard 304

Standard – loose 47

Pre-prepared 92

Rice Standard dry 578

Pre-cooked – microwavable 155

Ready meals Chilled 328

Frozen 88

Yoghurt Single 286

Multipack 323

Cheese Pre-packed 1,186

Deli 46

Chicken Frozen 78

Chilled 313

Total 12,149

In 2011, all retailers surveyed carried both branded and own-label ranges. The proportion of own-label to branded products varied from retailer to retailer and from product category to product category (see Table 3). In the sample of all packed products reviewed, 44% were branded while 56% were own-label.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 20

Table 3 % packed products, by category, by own-label or branded, 2011 | Total base: 11,875

Retailer Product origin

Bre

ad

Rolls

World

bre

ads

Cookin

g

sauce

Ham

Baco

n

Pota

toes

Apple

s

Carr

ots

Sala

d

Ric

e

Past

a

Ready

meals

Yoghurt

s

Eggs

Cheese

Mayonnai

se

Milk

Chic

ken

Ora

nge

juic

e

To

tal

Aldi

Branded 100% 100% 100% 100% 77% 100% 75% 50% 88% 100% 100% 100% 100% 100% 100% 100% 100% 100% 88%

Own-label 23% 100% 100% 25% 50% 13% 12%

Asda

Branded 79% 26% 51% 78% 9% 23% 9% 41% 47% 51% 11% 63% 58% 59% 66% 30% 10% 43% 45%

Own-label 21% 74% 49% 22% 100% 91% 77% 100% 91% 59% 53% 49% 89% 37% 42% 41% 34% 70% 90% 57% 55%

Co-op

Branded 66% 45% 62% 80% 7% 10% 43% 33% 24% 61% 18% 36% 72% 23% 6% 55% 45%

Own-label 34% 55% 38% 20% 93% 90% 100% 100% 100% 100% 57% 67% 76% 39% 82% 64% 28% 77% 94% 45% 55%

Lidl

Branded 100% 100% 100% 100% 100% 100% 100% 50% 100%

88% 100% 100% 100% 33% 100% 100% 100% 100% 100% 93%

Own-label

50%

13%

67%

7%

M&S

Branded

45%

2%

Own-label 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 55% 100% 100% 100% 98%

Morrisons

Branded 55% 19% 55% 75% 10% 24%

2% 34% 55% 32% 22% 63% 39% 55% 66% 35% 11% 49% 43%

Own-label 45% 81% 45% 25% 90% 76% 100% 100% 98% 66% 45% 68% 78% 38% 61% 45% 34% 65% 89% 51% 57%

Ocado

Branded 64% 14% 60% 83% 29% 33% 60% 63% 64% 59% 36% 48% 75% 43% 55% 52%

Own-label 36% 86% 40% 17% 71% 67% 100% 100% 100% 100% 40% 38% 36% 41% 64% 52% 25% 57% 100% 45% 48%

Sainsbury's

Branded 61% 18% 47% 76% 4% 25% 4% 56% 56% 40% 27% 86% 43% 50% 64% 34% 4% 50% 44%

Own-label 39% 82% 53% 24% 96% 75% 96% 100% 100% 44% 44% 60% 73% 14% 57% 50% 36% 66% 96% 50% 56%

Tesco

Branded 53% 31% 42% 72% 19% 27% 3% 62% 53% 54% 28% 58% 42% 52% 62% 17% 13% 48% 44%

Own-label 47% 69% 58% 28% 81% 73% 100% 100% 97% 38% 47% 46% 72% 42% 58% 48% 38% 83% 87% 52% 56%

Waitrose

Branded 48% 36% 55% 76% 12% 16% 7% 56% 48% 31% 61% 37% 49% 69% 37% 58% 45%

Own-label 52% 64% 45% 24% 88% 84% 93% 100% 100% 100% 44% 52% 69% 39% 63% 51% 31% 63% 100% 42% 55%

Total

Branded 60% 26% 48% 75% 12% 22% 9% 1% 5% 34% 52% 46% 24% 61% 42% 51% 65% 28% 10% 47% 44%

Own-label 40% 74% 52% 25% 88% 78% 91% 99% 95% 66% 48% 54% 76% 39% 58% 49% 35% 72% 90% 53% 56%

Helping Consumers Reduce Food Waste – A Retail Survey 2011 21

1.2.2 Range Products were categorised as ‘premium own-label’, ‘standard own-label’, ‘value own-label’ or branded. Figure 1 details the relative proportions of each, found in the 2011 research.

Figure 1 Proportion of packed products in different ranges carried by supermarkets, 2011

1.2.3 Fascia Stores reviewed fell into three store fascias (defined by the project team) supermarket / hypermarket, convenience or online. Table 4 details the split of products collected across the store fascias.

Table 4 Store fascia, all products, 2011 | Base: 10,10122

Store fascia Frequency %

Supermarket/hypermarket 7,279 72%

Convenience 1,688 17%

Online 1,134 11%

1.3 How to use this report This report is a summary of extensive sub-category specific analysis of the data collected. It contains what were considered the most interesting outcomes of the research, alongside key comparisons, where possible, to data from the 2009 survey. The information in the report is arranged thematically under eight headings:

Pack size and price incentives, pack features and format;

Promotions;

Storage guidance;

Freezing and defrosting guidance;

Date labels;

Given and open shelf life;

Cooking and portioning guidance; and

Point of sale information.

Where reference is made to a specific product category or sub-category, the name of that category is picked out in bold, so that in skimming the report a reader may pick up on categories they are interested in.

22 Store fascia information was not available for 2,048 products as these were proxy data.

10%

39%

8%

43%

Range, 2011: Base: 11,875

Premium own label(n= 1134)

Standard own label(n= 4588)

Value own label(n= 983)

Branded(n= 5170)

Helping Consumers Reduce Food Waste – A Retail Survey 2011 22

2.0 Methods 2.1 Key data collected The key data collected on each product surveyed, were as follows:

Type and details of dates displayed on packaging;

Storage guidance (both presence of, and detail);

Freezing instructions (both presence of, and detail);

Defrosting instructions (both presence of, and detail);

Pack size, features and format;

Recipes, tips and information;

Portion guidance;

Price and promotions;

Presence of symbols;

Presence of on-pack ‘flash’ labelling; and

Presence of on pack tips on waste avoidance or use of leftovers.

In addition the following contextual information (where relevant) was recorded:

Retailer;

Store type (fascia);

Store location (geographical);

Sub-type of product (if relevant);

Whether branded or own-label, and if own-label, whether ‘premium’, ‘standard’ or ‘value’;

Brand/sub brand;

Variant (e.g. extra strong; Mediterranean; wafer thin);

In store location, whether chilled, ambient, frozen or from the deli counter); and

Any point of sale information. Alongside data about products, data were collected about the availability of tools that might help consumers better store or manage the food they purchased. Data on the following types of tools were collected:

Re-closable food / freezer bags;

Air-tight storage containers;

Cool bags;

Plastic clips;

Spaghetti measures; and

Fridge thermometers.

Throughout this work there has been a keen awareness of the need for longevity in the research. Innovations such as the recording of programming code23 to enable future statistical analysis; the development of identification numbers for unique products (SKUs) as well as for unique records; and the development of a user interface for data collection, will enable similar work to be carried out at greater speed and reduced cost in future years. 2.2 Changes to what data were collected since 2009 The 2011 research involved a number of changes to what data was collected. Most notable were changes in the sample, in terms of the proportions of retailers and store fascias that were reviewed, and changes to the product categories. These changes are described in Sections 2.4 and Appendix 1. In 2011, researchers collected, ‘best before’, ‘use by’ and ‘display until’ dates on products, and recorded the dates on which products were reviewed. This data allowed subsequent calculation of given shelf life – the number of days between the date of review and the ‘best

23 In IBM SPSS statistics package.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 23

before’ or ‘use by’ date of the product, and also allowed calculation of the intervals between ‘best before’ or ‘use by’ dates and ‘display until’ dates. Increased emphasis was placed on collection of data about symbols, for example the ‘snowflake’ freezing symbol, and on ‘on pack ‘flash’ labelling on products. The categories to which products were assigned were further refined in 2011, with separate analysis generally being conducted for all aspects of loose versus packed, factory baked versus in store bakery, and chilled versus ambient or frozen versions of products. A decision was taken not to count 5-a-day information as portion guidance in 2011. Hence guidance such as ‘80g = 1 of your 5 a day’ would be counted as portion guidance in 2009, but not counted in 2011. Examples of guidance judged to be portion guidance in 2011 were ‘This pack contains 2 servings’ and ‘One portion = 80g’. This has led to the appearance of a decrease in the proportion of products carrying portion guidance, but is a more accurate reflection of true guidance around portion sizes. Data on portion guidance in this report should therefore be considered to be a revision to the previous baseline, rather than a comparison with 2009. 2.3 A note on comparisons between 2009 and 2011 It should be noted that a quota sampling approach has been taken in both the 2009 and 2011 research, and that the quotas changed between the two years. Neither the 2009 or the 2011 sample is intended to be representative of the retail environment as a whole, but each gives a snapshot of the retail environment, through a particular lens, at a particular point in time. Where comparisons are made it should be noted that they are between the two samples and are not necessarily representative of changes in the retail environment as a whole. That said, efforts have been made to ensure that reported changes between the samples are of sufficient magnitude to be likely to reflect genuine change. Specific comparisons have been subject to double checking with a 2011 dataset weighted to match the relative proportion of retailers in the 2009 sample. Where such checks have been carried out they are detailed in the footnotes. 2.4 Where were the data collected? In 2009, data collection involved visits to four examples of each type of fascia for nine major retailers. For each store fascia, examples were visited in the following locations:

two in England (one north, one south);

one in Wales; and

one in Scotland.

In 2011, the numbers of stores visited was adjusted in order to bolster the presence of some retailers in the sample and to scale down the presence of others to reflect changes in market share. The locations in which stores were visited also changed in order to allow representation of the midlands as well as North, South, Scotland and Wales in the sample. Data collection in 2011 involved visits to four examples of each of the following store fascias:

M&S department stores;

M&S Simply Food;

Sainsbury’s Local;

Sainsbury’s supermarket;

Tesco Express;

Tesco Extra;

Tesco Metro;

Helping Consumers Reduce Food Waste – A Retail Survey 2011 24

Tesco supermarket;

The Co-operative (convenience store);

The Co-operative (supermarket); and

Waitrose. Two examples of each of the following stores: Aldi and Lidl. Eight Morrisons supermarket stores, which does not have a ‘convenience’ store fascia. Asda was unable to participate in in-store reviews, but was keen to participate in the survey. In-house staff carried out a review of products in one Superstore, and this, in combination with data from an online shop, was used to create proxy data. Proxy data were multiplied by eight in order to represent the four superstores and four supermarkets that would otherwise have been reviewed: Asda supermarket and Asda Wal-Mart Supercentre. Certain data that was likely to vary from store to store was excluded from the proxy data:

Price;

Promotions;

Region;

Date item audited; and

Any ‘use by’, ‘best before’ or ‘display until’ dates.

This means that calculations such as given shelf life could not be made for proxy products. As mentioned above, stores from the Midlands were included in the 2011 sample. This has made the spread of locations in the sample somewhat more complex. Table 5 briefly outlines where stores were located. Data were also collected from five online stores in 2011. Goods were reviewed online and purchased in three of these online shops: Asda; Tesco; and Waitrose. Goods were reviewed online, but not purchased from two further online stores: Ocado and Sainsbury’s due to time and budgetary constraints. The online reviews allowed capture of ‘point of sale’ information that is available to consumers as they shop online. Of particular interest was a high incidence of information about the ‘expected’, or ‘guaranteed’ life of certain products. More details about this information can be found in Section 10.1. Table 5 shows that data was collected from three nations during the research – England, Scotland and Wales. A number of tests were run to investigate potential differences between these nations. Some differences were found in the data, but these differences were attributable to the differences in the sample of retailers taken from each country, rather than reflective of differences in products available to consumers in these nations. For this reason, no further analysis by nation was carried out.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 25

Table 5 Locations of store fascias visited in 2011 | Base: 64 Retailer and store fascia

Location

Midlands North Scotland South

East Wales

Proxy

data

1 Waitrose 1

1 1 1

2 Aldi

1

1

3 Lidl

1

1

4 M&S Department Store 1 1 1

1

5 M&S Simply Food 1

1 1 1

6 Tesco Metro 1 1 1

1

7 Tesco Express 1 1

1 1

8 Tesco Extra

1 1 1 1

9 Tesco Supermarket 1 1 1 1

10 Sainsbury's Local 1 1 1 1

11 Sainsbury's

Supermarket 1 1

1 1

12 Morrisons 2 1 1 2 2

13 Asda Supercentre

1

15 The Co-op (Convenience)

1 1 1 1

16 The Co-op

(Supermarket) 1 1

1 1

Asda proxy

7

Total 12 12 10 12 11 7

2.5 How were the data collected? An initial phase of survey design and piloting was carried out, followed by training of the research field force. Two tranches of fieldwork were then conducted. The fieldwork tranches were punctuated by a two week gap, which allowed the Brook Lyndhurst team to clean the data collected and to refine the data collection process where possible. Full details of this phase of work are given in Appendix 2. 2.6 Analysis Once fieldwork was complete and all databases returned, the data was subjected to further cleaning, and allocation of photographs to records in Excel, before being uploaded to SPSS, where detailed analysis was conducted. A series of category reports were produced, detailing information gathered on each product category or sub-category, according to thematic headings similar to those used in this summary report. These reports were subjected to detailed review by WRAP. A workshop was then held with WRAP and Brook Lyndhurst to examine emergent themes from the product category reports and to agree on the focus of additional analysis.

Helping Consumers Reduce Food Waste – A Retail Survey 2011 26

3.0 Pack size range, availability, pack features and price 3.1 Pack size range Our research generally found a range of pack sizes, or compensating availability of loose or deli products, in most product categories. In some categories, however, pack size options were restricted, either by availability on-shelf, or by the economic accessibility of specific sizes of pack due to price gradients. WRAP’s study24 reported that pack size may be a contributor to food waste where households are unable to find, or are disincentivised to purchase, packs of a suitable size to meet their needs. Large pack sizes can place the onus on households to effectively manage the food they buy in such a way as to prevent waste. Where food skills are lacking, where suitable guidance is not provided (or not noticed) or where products have very short shelf lives once opened, food waste is more likely to result from purchase of large packs. 3.1.1 A note about the interplay of pack size and food management It is important to acknowledge that while availability (both physical and economical) of smaller pack sizes does have a role to play in preventing food waste, there are a range of other factors that will influence whether a product is consumed or thrown away, whole or in part. Consumers can often manage the contents of large packs in such a way as to extend product life and enable them to use all of the contents. Examples of this include freezing loaves of bread and removing slices as needed, and tightly wrapping cheese to keep it airtight and prevent it drying out. The presence of storage guidance, freezing guidance, and innovations to increase open shelf life of products, all play a role in the way larger packs of food are managed, and whether or not a bias towards large packs has an impact on how much food is wasted. In some food categories, for example bagged salad, however, packs cannot be so easily managed, once opened. It is with these types of food that improvements in range and availability of pack sizes have the greatest potential benefits. It should also be borne in mind that the provision of smaller pack sizes has associated environmental impacts, as a result of increased use of packaging materials. For some foods, therefore, the onus is on the provision of guidance on how to manage the contents of packs, as well as on changes to pack sizes. 3.1.2 Products for which consumers had a limited choice of pack size By far the most common size of orange juice pack reviewed was 1 litre (54% of reviewed packs). Smaller packs were less readily available, with little between single serving packs (250-330ml) and 1 litre. Packs in the 500-900ml range made up only 7% of the sample, meaning that consumers who wanted more than a single serving but were unlikely to finish a litre of juice would have limited choice. Pack sizes, were, however, well distributed between store fascia, with a good proportion (26%) of packs found in convenience stores being in the smallest size bracket (250-330ml). As in 2009, packs of ham at first glance come in reasonably small sizes, with 44% between 100g and 150g (this was 50% in the 2009 sample). 15% of packs weighed 100g or less (13% in 2009). However, smaller packs are considerably more expensive per kg of ham than bigger packs, providing a disincentive for consumers to downsize.

24 Research into Consumer Behaviour in Relation to Food Dates and Portion Sizes, WRAP, 2008

Helping Consumers Reduce Food Waste – A Retail Survey 2011 27