Final Dissertation

77

Dissertation Student Name Ja Htu Aung Degree BA (Hons) Accounting Dissertation Supervisor Wendy Mason Burdon Dissertation Title An Analysis of Changes on Segmental Reporting after IFRS 8 Has Become

-

Upload

kristina-aung -

Category

Documents

-

view

50 -

download

0

Transcript of Final Dissertation

Dissertation Student Name Ja Htu Aung

Degree BA (Hons) Accounting

Dissertation Supervisor Wendy Mason Burdon

Dissertation Title An Analysis of Changes on Segmental

Reporting after IFRS 8 Has Become

Effective

Date April 2015

Keywords IFRS 8, IAS 14, FRS 108, FRS 14,

Segmental Reporting

Declarations

I declare the following:-

(1) that the material contained in this dissertation is the end result of my own work and that due acknowledgement has been given in the bibliography and references to ALL sources be they printed, electronic or personal.

(2) the Word Count of this Dissertation is ...................................

(3) that unless this dissertation has been confirmed as confidential, I agree to an entire electronic copy or sections of the dissertation to being placed on Blackboard, if deemed appropriate, to allow future students the opportunity to see examples of past dissertations. I understand that if displayed on Blackboard it would be made available for no longer than five years and that students would be able to print off copies or download. The authorship would remain anonymous.

(4) I agree to my dissertation being submitted to a plagiarism detection service, where it will be stored in a database and compared against work submitted from this or any other School or from other institutions using the service. In the event of the service detecting a high degree of similarity between content within the service this will be reported back to my supervisor and second marker, who may decide to undertake further investigation which may ultimately lead to disciplinary actions, should instances of plagiarism be detected.

(5) I have read the University Policy Statement on Ethics in Research and Consultancy and the Policy for Informed Consent in Research and Consultancy and I declare that ethical issues have been considered and taken into account in this research.

(6) I have read the University Policy Statement on Data Protection in Research and Consultancy and I declare that the data collected for use in this dissertation has been properly safeguarded and will be destroyed once the dissertation or subsequent research activity has been concluded. I acknowledge that it is my responsibility to destroy the information with due regard to confidentiality.

SIGNED: ..........................................................

DATE: ................................................................

i

AbstractStudent Name JA HTU AUNG

Degree BA (HONS) ACCOUNTING

Dissertation Supervisor WENDY MASON BURDON

Dissertation Title AN ANALYSIS OF CHANGES ON

SEGMENTAL REPORTING AFTER IFRS 8

HAS BECOME EFFECTIVE

Date APRIL 2015

Keywords IFRS 8, IAS 14, FRS 108, FRS 14,

SEGMENTAL REPORTING

The study gave emphasis to the International Financial Reporting Standard

IFRS 8(Operating Segments) and the former standard IAS 14, which was

superseded by the IFRS 8. The purpose of the study is to analyse the changes

on disclosures in segmental reporting after the new standard IFRS 8 has

become effective. Some of the issues developed from applying IFRS 8 will also

be further analysed.

According to the personal interest, sample companies are collected from

Singapore Stock Exchange (SGX). IFRS is applied as a local version which is

known as Singapore Financial Reporting Standard (SFRS) by SGX listed

companies (PricewaterhouseCoopers, 2014). Hence, the IFRS 8 published by

the IASB in converging with US GAAP is established as FRS 108 and the

preceding standard IAS 14 is recognised as FRS 14 locally.

Despite the local implementation, the material(s) of both the FRS 14 and its

superseded standard FRS 108 are identical to IAS 14 and IFRS 8 in overall

aspects (PricewaterhouseCoopers, 2012). For the above stated facts, the study

on pre and post implementation review of IFRS 8 has been approached by

examining on SGX 60 companies which are in full consistency with IFRS.

The key findings are that under IFRS 8, Singapore companies have less

disclosed their business segments and geographic segments due to one of the

ii

mandatory stages of IFRS 8 called aggregation of segments which allows

companies to combine the segments if they meet the specified requirements.

However, the decreasing changes are not sizeable amount while comparing to

the decline on the line items disclosed per segments under IFRS 8.

Considerably, number of companies reporting segment assets, liabilities and

capital expenditures has dropped dramatically in 2010 when IFRS has become

effective. Last but not least, the Chief Operating Decision Maker (CODM) has

been voluntarily identified by many of the SGX companies.

Keywords: IFRS 8, IAS 14, FRS 108, FRS 14, Segmental Reporting

iii

Acknowledgements

Firstly, I would like to thank my supervisor Wendy Mason Burdon for her

excellent guidance and kindness throughout the research procedure. Without

her support, guidance and useful feedbacks, this dissertation would never get to

be done.

Furthermore, I would also like to thank my friend, Emily Ramsden, who has

always helped me whenever I found difficulties and encouraged me. Last but

not least, I am thankful for the excellent service within the Library where I

always worked for my dissertation.

iv

Contents

Dissertation..................................................................................................................................1

Declarations.................................................................................................................................. i

Abstract........................................................................................................................................ ii

Acknowledgements..................................................................................................................... iv

Contents.......................................................................................................................................v

Chapter 1 Introduction.................................................................................................................1

1.1 IFRS 8 (Operating Segments)........................................................................................1

1.2 Research Objective.......................................................................................................2

1.3 Explanation on the Subject Choice...............................................................................2

1.4 Explanation on the approach to the chosen objective.................................................3

1.5 Limitations of the study................................................................................................4

1.6 Structure of the paper..................................................................................................4

Chapter 2 Literature Review........................................................................................................6

2.1 Introduction.......................................................................................................................6

2.2 Agency Theory....................................................................................................................6

2.3 Review on IFRS 8................................................................................................................7

2.4 Review on IFRS 8 in Earlier 2013........................................................................................9

2.5 Review on Segmental Reporting.......................................................................................10

2.6 Review on the Number of Segments and Line Items per Segment...................................12

2.7 Review on Aggregation of segments................................................................................13

2.8 Review on Identification of the CODM.............................................................................14

Chapter 3 Methodology.............................................................................................................15

3.1 Introduction.........................................................................................................................15

3.2 Research objectives..........................................................................................................15

3.3 Data Collection.................................................................................................................16

3.4 Limitations........................................................................................................................16

Figure 1 Sample Companies...............................................................................................17

3.5 Data Extraction and Analysing the Results.......................................................................18

3.7 Ethical Concerns...............................................................................................................19

Chapter 4 Analysis and Findings.................................................................................................20

4.1 Analysis on the Number of Reportable Segments............................................................20

Figure 2 Number of segments comparison........................................................................22

4.2 Items Disclosed per Segment...........................................................................................23

4.2 Items Disclosed per Segment (continued)........................................................................24v

Figure 3 (continued)...........................................................................................................25

4.2 Items Disclosed per Segment (continued)........................................................................25

Figure 3 (continued)...........................................................................................................26

4.2 Items Disclosed per Segment (continued)........................................................................26

Figure 4 Items disclosed under Secondary Reporting Format............................................27

4.3 Average Number of Line Items per Segment................................................................28

Figure 5 Average number of line items per segment.........................................................29

4.4 Analysis on Chief Operating Decision Maker of SGX 60................................................29

Figure 5 Chief Operating Decision Maker of SGX 60...........................................................30

Chapter 5 Conclusion.................................................................................................................31

5.1 Results Overview..............................................................................................................31

5.2 The Current Findings in Consideration of Previous Literatures and Applied Theory........31

5.3 The Current Findings in Consideration of Previous Literatures and Applied Theory........33

5.3 Limitations and Future Research......................................................................................33

References.................................................................................................................................35

Reflective statement..................................................................................................................42

Acronyms...................................................................................................................................44

Appendices.................................................................................................................................45

Appendix 1.........................................................................................................................45

Appendix 2.........................................................................................................................46

vi

Chapter 1 Introduction

1.1 IFRS 8 (Operating Segments)Segmental reporting is mandatory for company whose securities are traded

publicly or those which are in the procedure to be publicised (IASPlus, 2007).

The segmental reporting disclosed within the annual report of an enterprise

must provide users of financial statements with the nature of the economic

background in which that company operates and the fiscal effects of business

transactions where it has engaged/involved (UNIT, 2009).

IFRS 8, operating segments was issued by the International Accounting

Standards Board (IASB) in conjunction with the US Financial Accounting

Standards Board (FASB) in 2006, November (Veron, 2007). The standard has

substituted its former standard IAS 14 for the purpose of better harmonisation

between IFRSs and US generally accepted accounting principles (GAAP)

(PricewaterhouseCoopers, 2008).This new standard IFRS 8 is defined as one

of entity’s constituents, which comprises trade activities such as incurring

revenues and expenses. The transactions of Income and expenditure incurred

within one entity but different components are also recognised as operating

segments (Ernst and Young, 2013).

Under the new standard, companies must report its business or geographic

unique segments which are qualified to disclose in annual reports by giving

descriptive details such as financial information of those segments or

aggregated segments operated within their firms (Iasplus, n.d.).

Business segments are related to products and services of companies while the

geographic segments are the segments of different regions in which they

operate and their major customers are located (Iasplus, n.d.).

The results of those operating segments of an entity are evaluated

systematically by its Chief Operating Decision Maker (CODM) for the purpose of

deciding the allocation of the resources toward the segments and evaluating the

functioning of those segments. Separate financial reporting is also presented

within entity’s operating segments (Deloitte , n.d.).

1

The constraints and specifications of segmental reporting according to the US

Statement of Financial Accounting Standards (SFAS 131) is largely equivalent

to the IFRS 8 with only slight dissimilarities (IFRS , 2006).

A number of criticisms have been derived over the new standard. According to

the review studied by the staffs of IASB in 2013, the major issues upon IFRS 8

are that relying on the management perception before identifying the operating

segments, the usage of measurement which are not within the IFRS 8 standard

and last but not least the absence of providing information about the CODM

who make decision about the line items to disclosed within the segmental

reporting.

1.2 Research ObjectiveThe main purpose of the study is to examine on how the replacement of IFRS 8

over IAS 14 has impacted on the disclosures of companies registered on

Singapore Stock Exchange (SGX). This present research targets in achieving a

better understanding on the nature of segmental reporting and how the new

standard have affected on the disclosures which provide useful information to

users.

1.3 Explanation on the Subject Choice A few considerations have been taken into account before collecting data from

the SGX listed companies. The previous research papers on IFRS 8 in

particular have tested mostly on European companies including UK FTSE

companies which adopted IFRS. Hence, the limitation issue has arisen while

selecting companies to examine at first as the rest of the companies world-wide

have adopted different standards such as US GAAP etc. in preparing their

annual reports.

Therefore, the current research will be assessing on Singapore firms, one of the

Asian companies which applied IFRS locally for some favourable reasons.

Firstly, in addition to the personal interest, the Singapore annual reports have

found to be very efficient in approaching the purpose of this study because the

publicly established reports are written in full English for the understanding of

users worldwide. Secondly, the Singapore reports are also rewarded annually

for their excellent accounting statements in order to motivate the preparers for a

better performance in presenting the annual report (Singapore Corporate

Awards , 2014). Therefore, the disclosures are professionally well-established 2

with full detailed information and broader scope which will benefit the users

such as investors and stakeholders.

In Singapore, financial reports are prepared according to its own local version

called SFRS. Thus, the IFRS 8 is known as FRS 108 and the former standard,

IAS 14 is adopted as FRS 14 (PricewaterhouseCoopers, 2008). However, the

SFRS is largely aligned with IFRS in many aspects and thus the material

features of FRS 108 and the early standard FRS 14 in particular are considered

to be fully consistent with IFRS 8 and IAS 14 respectively

( PricewaterhouseCoopers, 2012).

Last but not least, the topic and SGX listed companies are chosen as there is

no such research that has been studied on this particular area of segmental

reporting previously except from Wilkins and Khoo (2012). Although the paper

was on segmental reporting the research goals were different (see IFRS, 2013).

For above stated reasons, the study on pre and post implementation review of

IFRS 8 has been approached by examining on SGX companies which are in full

consistency with the IFRS

1.4 Explanation on the approach to the chosen objectiveAccording to the (Deloitte , n.d.) , the IFRS 8 was established by November

2006 after its Exposure Draft has been delivered; effective for annual

accounting periods beginning on 1 January 2009 and onwards. Under these

circumstances, the main objective will be obtained by comparing the annual

reports of SGX companies as at 31st December 2010 against those stated

before the effective date; 31st December 2008.

Based on the main objective, three research questions have been derived in

order to know the impact of IFRS 8 on segment disclosures. Numerical data on

the segment numbers, items disclosed under each segments such as business

and geographic segments and the CODM identification by SGX chosen

companies will be collected to compare and analyse the annual reports under

the two different years to answer the three research questions. The final

objective of the study will be attained from these numerical data analysis.

Furthermore, issues arisen in IAS 14 and IFRS 8 will be further examined.

3

1.5 Limitations of the studyInitially, the study obtained 100 SGX companies as others researchers such as

Crawford et al. have also studied approximately 100 companies. Due to a

number of limitations the final companies which will be testing are 60 and

further explanations of limitations upon the selections of companies will be

discussed in the next section, methodology.

1.6 Structure of the paperThe dissertation is structured in the following way. In the first chapter, the

overview of IFRS 8 will be discovered by giving detail information on the

background of it and highlighting on the purposes of the study and how will the

research aims will be achieved.

Followed by the introduction chapter, the literature review on IFRS 8 and

segmental reporting will be explored in order to support the research questions.

Theory associating with the segmental reporting will be also explained in terms

of its relevance to research topic. Last but not least, the current literature has

also reviewed on the issues arising on IFRS 8. However, this literature has not

revised upon the local standard FRS 108 particularly due to the standard being

identical to the original standard IFRS 8 in overall standard’s perspectives as

stated earlier (PricewaterhouseCoopers, 2008).

Next chapter will be presenting on the methods which have been used to collect

and analyse the data to answer the research questions. Prior to explaining the

data collection methods, where the raw data have been obtained from, have

stated with providing limitations experienced throughout the procedure.

Consequently, the final step of the methodology which is the explanation of how

the data will be analysed and derived to the results will be explained in details.

Ethical concerns upon the current research have also included verifying the

study follows the university ethic guidelines.

The last chapter is about the analysis and findings which has derived from the

previous work. The statistics results such as the number of segments disclosed

and items per segments disclosed etc. will be explored by linking between each

variable. The relevant theory as stated above in the literature section will be

linked back to the final complete results.

4

Last but not least, the partial of this research paper will be summarised by

bringing key aspects of the literature which have been discussed in the above

section in comparison with the complete research findings. This piece of

summarising will bring a connection to the methods that have applied to analyse

the research questions. Self-recommendation has been made on the previous

authors’ work by justifying their limitations within their studies and further

contradictions against them have also been made by the current findings.

Therefore, this present reflective understanding on IFRS 8 has developed the

study area with further information and the connection between the current

dissertation and the former studies has also been clearly identified.

5

Chapter 2 Literature Review

2.1 Introduction The purpose of this chapter is to review the areas in alignment with the

research goal of the current study which is whether the companies’ segmental

disclosures listed on SGX (Singapore Stock Exchange) have reformed after the

new standard IFRS 8 (adopted as FRS 108 locally) has taken place.

2.2 Agency Theory The supporting and underpinning theory behind the segmental reporting will be

also explained in details. Based on the conception of agency theory, there is

always asymmetric information between the principal and agent. The

asymmetric information derived from the knowledge gap between the perfectly

exposed company’s information which give reliable data or facts and that of

information which are not completely reliable (Eisenhardt, 1989).

In this study of segmental reporting, the principals are investors or shareholders

and the agents are those people in charge for management such as companies’

managers. Managers operate within the business and hence also known as

internal users while the shareholders are the external users who do not have

direct access to the information relating to the business they are invested in

(Quinn and Jones, 1995).

Therefore, one question has derived over the relationship between the principal-

agent: how the shareholders can assure that the decisions made by

management are in line with their interests?

Because the two individuals have their own different strategies in pursuing the

business target. For example, the stakeholders focus on raising profits for high

returns while the management’s goal is to add value on the companies along

with the wealth maximisation for their own. The value managers have created

may not be parallel to the value that the shareholders are expecting for (Douma

and Schreuder, 2008; Eisenhardt, 1989; Jensen and Meckling, 1994).

The answer to the above question is the financial reporting which is an essential

and compulsory tool for all the shareholders and investors.

According to Aitken et al. (1997), Consolidated information which is a

component of financial reporting alone does not help the investors much to see

6

the risks and the return or the information about the business components,

especially when the profits obtained from business segments are not consistent

to each other. Therefore segment reporting is used to reduce the asymmetric

information between the investors and the company management by providing

detail financial statement of each segment (Yoo & Semenenko, 2012).

Essentially the sole purpose of segment reporting is to help the investors to

understand the company as a whole by breaking down the information to the

level where it is easy to access and understand (Troberg et al. 2010).

Therefore, segment reporting can be seen as a way to solve principal-agent

problem.

2.3 Review on IFRS 8Regarding the study objective, analysis such as the issues and usefulness of

the new IFRS 8 will be presented in this section of literature review. Firstly, one

of the key components of the new standard called the management approach

will be critically examined as there are many judgements made upon the

potential issues which can derive from it (IFRS, 2013).

It is obligatory under IFRS 8 that companies report its segments related

information on business and geographic sectors if they meet specified criteria

(Deloitte , n.d.). Consequently, a company’s segmental reporting regarding the

business operations must be measured and identified through the

“management approach”. Thus, segmental reports are required to describe in

alignment with the internal management scheme revised frequently by the Chief

Operating Decision Maker (CODM) according to IFRS 8

(PricewaterhouseCoopers, 2008; Farías & Rodríguez, 2014).

Numerous criticisms have derived over the approach through management’s

insight and (Sukhraj, 2007b; Veron, 2007a) mentioned that the new innovated

approach could be a failure and inefficient (as cited in Crawford et al. 2013).

Report prepared by the PricewaterhouseCoopers (2008) have further pointed

the pitfall of management approach by stating that information which are

prepared thoroughly by CODM or management team will not be supported by

external audit or some robust processes.

In addition, the two papers prepared by Crawford et al. 2010 and Crawford et al.

2012 have also done much research on the problematic issues of the segment

disclosures under IFRS 8. However, this judgement on management approach

7

could be argued by the result findings of interview prepared by Crawford et al.

(2012). Because 20 participants out of 11 assumed that the recent

management approach of IFRS 8 is considerably more beneficial with extra

reliable information than the former approach of IAS 14 which measured the

segment reporting by using IFRS- compliant business information.

Moreover, the survey work done by CFA UK, 2012 also have in common with

the Crawford’s survey outcome which states that IFRS 8 has equipped the

analysts and users with greater knowledge about companies. However, from

the self-perspective view, this empirical result seems to solely rely on the

preparers’ judgment but not on the users’ point of view (as cited in Tarca &

Pitman, 2013). Correspondingly, the further analysis enhanced from the

continuing comment letters by the European Commission, 2007 has proven that

the exposure draft (ED) 8 of FRS 8 has supported predominantly by the

preparers (Crawford et al. 2010).

Along with the management control, the results of the entity’s operating

segments are evaluated systematically by its Chief Operating Decision Maker

(CODM) for the purpose of deciding the allocation of the resources toward the

segments and evaluating its functioning (PricewaterhouseCoopers, 2007).

Separate financial reporting is presented within entity’s operating segment

(Deloitte, n.d.).

Previous reports by ESMA, 2011 and AASB, 2013 have reviewed on particular

area such as CODM identification, which is one of the stages in applying IFRS

8; the CODM must revise the results of the operating segments within the lines

called product and geographic on a regular basis(Ernst & Young, 2009).

The disclosing number of segments and further proper information could be

reduced for applying this step. As a result, the purposes targeted within the

principle could not be fully achieved. Furthermore, the outdated approach

through management could be complicated and difficult to apply in reality as it is

based on the rules set by the CODM rather than principal-based (Herrmann &

Thomas, 2000).

However, this Herrmann and Thomas’s study seems to have a gap within their

literature as there are two inconsistent statements made upon the management

approach strategy. Because they have also concluded by stating the segmental

reporting has become more reliable and efficient due to its consistency and 8

better accurateness under the CODM’s management (as cited in Crawford et al.

2010).

Sukhraj (2007a) has also criticised on the CODM for not being allocated and

recognised specifically but selecting from the range of random directors such as

financial directors and board directors. However, the shortcoming of CODM

information is likely to be included in future annual reports due to several

criticisms raised over it.

All of the above authors have commented that in the real world, the criticisms

have arisen on the identity of CODM who are making decisions over segment

reporting.

Despite the growing condemnations, the post-implementation review by (IASB,

2013) have drawn conclusion by giving credit on the new standard, IFRS 8 that

the advantages obtained from adopting the IFRS 8 has a greater impact on

disclosures (Deloitte, n.d.).

2.4 Review on IFRS 8 in Earlier 2013In earlier 2013, the comment and review on IFRS 8 have been limited due to

the standard havig been revised only after it is adopted globally. Hence, only a

short-time frame was available to criticise the complete standard before 2013 as

the IFRS 8 has become effective on 1 January 2009 (see Crawford et al. 2012;

H. Mardini, 2012; Mardini, Crawford, & Power, 2012).So with just around 2

years straight after the IFRS 8 has been applied by entities worldwide, a few

responses on the impact of implementing the new standard have been made by

some organisations and authors such as European Securities and Markets

Authority (2011), Veron (2007), Crawford et al. (2010) and European

Commission (2007). Most of the authors who did their research before 2013

have also judged on the similar issues such as the management approach and

the recognition of CODM which derived under the implementation of IFRS 8

regardless of the time frame of reviewing.

Although most of the authors have focused on the identical areas, a few of the

literatures of IFRS 8 were published prior the standard becoming effective, for

example: Veron (2007); European Commission (2007). As a result, those past

studies’ findings seem to have made little comment on overcoming with the

controversial problems and lack of proof based on empirical data. Therefore,

9

regardless of the contents that have covered relevant and useful areas, they

have concluded only on particular aspect among the several potential issues of

the standard and thus incomplete in nature. Noticeably, Veron (2007) has given

a bold definite statement by summarising due to the downsides of the IFRS 8; it

should not be adopted urgently by the European companies.

2.5 Review on Segmental ReportingSecondly, the literature will be reviewing on all the standards of segmental

reporting from the past to the current respectively in specific with the standards’

issues.

Segmental reporting is one of the most important compulsory financial

disclosures for the users of annual reports (Brown, 1997). The rationale behind

segmental reporting is that the mandatory consolidated statements disclosed

within the entities’ annual reports are not abundantly adequate as it lacks in

providing complete useful financial information to the external and internal

users. Therefore, business related information has been separated into

individual segments and hence called segmental reporting (Roberts, 2010).

A number of benefits and drawbacks have arisen upon segmental reporting due

to different judgments made by previous researchers. Numerous authors have

studied on how the data of segment plays a significant role for decisions over

investment and stock market (see Hope et. al., 2008; Epstein and Palepu, 1999;

Berger & Hann, 2003; McKinnon & Dalimunthe, 1993; Herrmann & Thomas,

2000; ESMA, 2011).

However, different evidences have been presented concerning the above

statement. Such as previous study of Epstein and Palepu, 1999 showed by the

results obtained from the contemplation of 140 financial experts such as “sell-

side analysts” (as cited in Berger & Hann, 2003) and the other authors,

McKinnon & Dalimunthe, 1993 have given a bold argumentative statement of

that the history of the company performance can be recognised under the

segment reporting sector and thus users must view them for future predictions

of the enterprise. For example, a large-cap bank normally issues the segments

report on its discrete financial services such as retail banking, corporate

banking, etc. Essentially, the discrete fiscal information has much influence on

the liquidity of a large-cap company as they are essential for the users of annual

10

reports to acknowledge whether they should invest in that particular company or

not (Berger & Hann, 2003).

In addition to those indications, (Berger & Hann, 2003; Balakrishnan et al. 1990)

have also further analysed on whether the improvement in accuracy of

predictions on an enterprise’s income and trades history has associated with

the accessibility of segmental reporting. The result obtained by them appear to

be consistent with those of above authors’, which is segment reporting matters

for a variety of users and analysts to some major extent. Though these authors

have done much research on the benefits of segmental reporting, they seem to

have ignored the downsides.

Nichols et al. 2013; Emmanuel et al. 1999; Parker and Sauer 2009; Edwards

and Smith, 1996 have largely centred on the issue about segmental reporting

being contentious. Such as, concerns have derived from the criticisms of the

new standard, IFRS 8 including the application of management control scheme

and the non-IFRS measurement usage, the possibility in reducing number of

reported segments on the geographic sector, and elimination of disclosing the

line items such as segment liabilities (Crawford et al. 2012; Crawford et al.

2010; Nichols et al. 2012).

Not only is the current standard of segmental reporting IFRS 8 problematic but

also the very original standard of segment reporting, Statement of Standard

Accounting Practice (SSAP) 25 had certain issues regarding to its disclosures

which are mandatory for companies Edwards & Smith (1996) (as cited in

Crawford, Helliar & Power, n.d.). Further concerns derived under SSAP 25 were

about not complying with segment disclosures geographically (Edwards &

Smith, 1996; Rennie & Emmanuel, 1992).

On the other hand, (Jermakowicz & Gornik-Tomaszewski, 2006; Crawford et al.

2010) stated concerns derived from the issues within companies’ disclosures

under the previous standard IAS 14. Further critics are made on the segments

aggregation (Nichols and Street, 2007); and the segment disclosures’ quality

and quantity (Street and Nichols, 2002).

However, these above concerns appear to be momentary as the ground-

breaking standard IFRS 8 has evolved in 2009.

11

2.6 Review on the Number of Segments and Line Items per Segment Last but not least, the literature on how the IFRS 8 has affected the primary and

secondary disclosures of segmental reporting such as business and geographic

segments reporting will be reviewed. Business segment is a unique part of the

whole business that has a distinct product or service. It also has unique risks

and returns. Geographical segment is based on unique economic environment

that produces products or services. Different geographical segment has

different risks and returns (Iasplus, n.d.).

Both IAS 14 and IFRS 8 require a business to report relevant information such

as business and geographic segments separated from their business as a

whole. The formats of reporting those two segments are divided into segments

disclosing of primary and secondary (Ernst and Young, 2009).

Numerous researchers have studied over the changes upon the number of

segments and line items per segments reported within the primary and

secondary disclosures when IFRS 8 has become effective by collecting data

and preparing survey (see Crawford et al. 2012; Mardini et al. 2012; Nichols et

al. 2012; Kang and Gray, 2012; Bugeja et al. 2012; He, He and Evans, 2012;

Heem and Valenza, 2012).

Based on those previous findings of (Mardini et al. 2012; Nichols et al. 2012), it

is likely to be that the segment numbers of business and geographic sectors

disclosed have not changed since IAS 14 although separate segments can be

merged together if they meet the specified requirements under IFRS 8

(Pricewaterhousecoopers, 2008). The study of (Bugeja et al. 2012) upon the

1,617 Australian listed firms also has similar outcomes with them, resulting in

79% of segments quantities remaining constant.

On the other hand, numerous companies have also experienced an upturn on

the segment numbers according to the post implementation review prepared by

the (IFRS, 2013; Moldovan, 2014; IASB, 2013a; ESMA, 2011; AASB, 2013).

Parallel to these findings on the review of implementing IFRS 8 is the Crawford

et al. 2012 as 150 sample companies taken from FTSE 100 and 250 disclosed

increase segment amounts, resulting an average growth of 0.26 under IFRS 8.

12

Although most researchers analysed the number of segments changes based

on the secondary sources, primary data method seems to be used by only a

few researchers including Crawford et al. 2012. Moreover, there is absence of

supporting reasons behind the increase segment numbers by most of the

studies comprising Crawford et al. 2012.

In fact, a decline in the mean numbers of business or geographic segments

reported is considered to be relatively small comparing to the increase overall

(Tarca & Pitman, 2013). However, the results can still be varied based on the

individual companies disclosing them.

While there is an escalating result on segment numbers under IFRS 8, the line

items disclosed for each segment called business and geographic reporting has

decreased comparing to those disclosed under IAS 14 (Weissenberger and

Franzen, 2012a; Crawford et al. 2012; He et al. 2012; Nicholas et al.2012).

Mardini et al. 2012 have an opposing result to them although the difference

within the increase and decrease is not sizeable or significant.

Despite the total line items disclosed under both reporting formats have

undergone a decline, He et al, 2012 has stated that companies disclose more

items such as intersegment revenue, interest expense and revenue and

income tax rather than segment assets, liabilities and capital expenditure(as

cited in IASB, 2013).

Furthermore, in accordance with the review prepared by the member of IASB in

2013, the declining line items under each segment reporting is likely to be

caused by the management approach which is to report to the CODM in

advance before disclosing those line items.

2.7 Review on Aggregation of segments IFRS 8 has allowed the combination of segments to form into one category if

they have met certain specified criteria (IASB, 2012).

Based on this action, (ESMA, 2011; Backhuis and Camfferman, 2012) have

discussed about the segments aggregating process under IFRS 8 (as cited in

IFRS, 2013). According to the review on several study papers prepared by

(ESMA, 2011), the opinion of those researchers who analyse upon the

segment aggregation can be observed that minimising the segments into one

group can result in the absence of providing essential information to users. 13

However, these are just a prediction made by those forecasters who seem to

have ignored proof to the statement. The finding by the (CFA UK, 2012) also

have a common to the ESMA report as most of the analysts tend to favour the

disaggregation rather than aggregation of segments as they personally think to

be more efficient. Last but not least, (KPMG, 2010) have also judged upon the

absence of explanation details about the aggregated segments by companies’

disclosure.

2.8 Review on Identification of the CODMStemming from the issues arisen upon the absence of providing who the CODM

is, a number of analysts have carried out by taking sample companies to

examine how many companies have been identifying the identity behind the

CODM (see Nicholas et al. 2012; ESMA, 2011; KPMG, 2010; Kang and Gary,

2012; Crawford et al. 2012).

Among those analyses, the sample companies performed by the (Crawford et

al. 2012; Kang and Gray, 2012) have the most number of companies which

identified the person who is in charge as CODM, resulting 69% and 82%

respectively.

Followed by this, the 36% European sample companies analysed by Nicholas

et al. in 2012 have also identified the CODM. Furthermore, it has been

observed by (KPMG, 2010) that 33% of chosen firms have given the detail

information about the CODM. Undoubtedly, CODM duty is given the most to the

management team followed by it are the CEO (Kang and Gary, 2012; Nicholas

et al. 2012).

14

Chapter 3 Methodology

3.1 IntroductionThis chapter justifies how and where the relevant data have been collected to

examine the research objectives.

As mentioned in the earlier chapters, IFRS 8 superseded the former standard

IAS 14R and hence the segmental reporting has been adjusted and changed

under the new principles of IFRS 8 (Deloitte, n.d.). Through the segmental

reporting, the changes on structure within the company and the past

performance are measurable (Botosan and Harris, 2000). Therefore, the

alteration of this essential segmental reporting can be a very sensitive case

because of its importance in making decisions for investing to stakeholders.

Stemming from the literature studied in earlier sections on the new

management approach of IFRS 8, (Nichols et al. 2013; Crawford et al. 2012;

Parker and Sauer, 2009; Pricewaterhosuecoopers, 2007) stated that the

business or geographic segments reported is expected to develop under the

control of management by the CODM. However, the CODM is not always

identified and therefore concerns have been arisen.

Although the impact of IFRS 8 on disclosures for UK has been investigated as it

plays a major role (Crawford et al. 2012), none of the research paper has

completed on how the Singapore companies have affected from the IFRS 8.

3.2 Research objectivesSubsequently, the following four questions will be analysed:

RQ 1: Have the numbers of reported segments changed after IFRS has

become effective?

RQ 2: How many SGX listed companies have changed their reportable number

of segments after the new standard is introduced?

RQ 3: Have the line items within the segmental disclosures changed after IFRS

8 has taken place over IAS 14?

RQ 4: Have the CODM been recognised under the segmental reporting?

These objectives have been chosen based on the completed present literatures

for the following reasons. Firstly, there is lack of evidences from world-wide

companies on the implementation of IFRS 8, especially from Singapore which

implemented IFRS locally (Section 1.2). Secondly, are expectations and

15

statements made by various authors about the changes on the quantities of

segments and line items as the management approach occupied also

applicable to Singapore companies (Section 2.4)? The last reason is to see

whether the controversial issues of not identifying who is the CODM that is

making the decisions about segment reporting has been cleared to Singapore

companies (Section 2.6).

3.3 Data CollectionIn order to answer the above research questions, numerical or quantitative data

such as number of business and geographic segments, number of companies

disclosing the line items which are compulsory under IAS 14 for each of the

primary and secondary reporting format. Last but not least the data of number

of companies identifying the CODM will also be collected. All of these raw data

have hand-collected from secondary sources such as annual reports published

within the SGX for two different years of 2008 and 2010 which are the years

that IAS 14 was still in use and IFRS 8 has become active respectively.

The reason for favouring the quantitative approach is because the key research

areas are the number of segments and number of line items per segment which

can be simply and effectively analysed by the measurement of statistics (Horn,

2009).From the stage of analysing the raw data, a precise statistics research

answers will be obtained.

3.4 LimitationsThe SGX has divided its listing into two different sections known as the

mainboard and catalist listings. The previous authors (Kajuter and Nienhaus ,

2012; Pisano and Landriana, 2012; Mardini et al. 2012 ; Crawford et al. 2012)

have selected approximately 100-150 companies whilst analysing the IFRS 8

versus IAS 14R. Therefore, this current study has also chosen the top 100

companies from a mixture of diverse listings established publicly on SGX.

However, according to (Walliman, 2004), the further limitations can be

encountered while collecting data using secondary sources. Firstly, as it is a

tough job to research and access relevant data which have been recorded in

the past, these 100 companies have to be selected again from the various

sectors as some categories of businesses are inconsistent with other remaining

types of firms. For example, the companies under banking sector will not be

considered due to more complex additional information reported on segment

disclosures (e.g. Prather-Kinsey & Meek, 2004; Street et al. 2000). 16

Consequently, collecting segmental info from the banking firms has been limited

by lack of harmonisation. Numerous reliable sectors such as food products; oil,

gas and consumable fuels; hotels, restaurants and leisure sectors; technology

products etc. have selected to analyse.

Secondly, authenticating the relevant resources which have been obtained for

current study is very challenging and time consuming. Although top 100

companies are picked from these sectors, (9) enterprises from them are

excluded because they registered on SGX later than 2008, which is the year

that IAS 14R was still in use. Moreover, further (20) companies are also

eliminated because they are incorporated within overseas (SGX, n.d.). Lastly,

(11) more companies are withdrawn at the end after collecting the raw data of

them because the data within those disclosures are listed in contentious and

unclear format and mixed language (see Figure 1).

Due to this fact, about 40 companies are disqualified in approaching to answer

the research questions. Finally, the numbers of companies which have

remained to analyse are 60 (Appendix 1).

Although, there are some limitations experienced from using secondary data

sources, the weighing of limitation for primary sourcing method seems to

exceed the secondary one as it involves man power and more ethical related

issues which can have more boundaries. Hence, although primary method was

in favour of using in the first place, it has been abstained due to lack of

participants in primary survey.

Figure 1 Sample Companies Figure 1 Final Sample

Companies Selection Process No. of companies

Initial selection of Top SGX companies 100Less:Registered on SGX later than 2008 -9Incorporated within other countries -20Usage of inconsistent format and mixed language -11Final Sample 60

Note: This figure shows the sample companies selection process.

3.5 Data Extraction and Analysing the ResultsAs the overall research objectives are abstracted from the outcomes of applying

the cutting-edge standard, IFRS 8 in disclosures, the answers to them will be

17

achieved by comparing the 60 SGX listed companies’ segmental reporting

under IFRS8 and IAS 14. IAS 14 became effective in 1998 and lasted till the

IFRS 8 has replaced it in the 1st January 2009 (Iasplus, n.d.).

Therefore, the data from the SGX 60 annual reports published in the year 2008

and 2009 will be hand-collected each. Although, there are accessible data

sources on its own SGX main website and Bloomberg financial website, the

current data have been selected manually as they are not financial related data

such as dividend and revenue and thus not accessible through those financial

websites.

To answer the first research question (Section 3.2), the data of business and

geographic segments of companies have extracted from segmental information

disclosed within the annual reports of the two different years. Excel software is

used to analyse and test the result by using those obtained data from a total of

142 annual reports. This software has been chosen for several reasons. Firstly,

it is capable of restoring large amount of data collected in a spreadsheet.

Secondly, many useful functions and formulas such as mean (average) etc.

have been provided to present the summarisation of cluttered data.

Lastly, the data analysis of the IFRS 8 versus IAS 14 can be completed without

hassles as it allows flexible filtering and searching tools to find and examine

vast information quickly. The raw data will be keyed in into the excel

spreadsheets. And mostly the Excel by Microsoft has chosen for its easier

accessibility than other software like SPSS.

After transferring the raw data in the chosen Excel spreadsheets, they are

stored securely and analysed. Computations are carried out by using excel

generated formula such as mean formula etc.

For the second research question (see Section 3.2), each of the companies

which made changes to their segments reported are keyed in to the created

excel spreadsheet. In order to obtain the data of increased and decreased total

number of companies, record of the companies which have either inclined or

declined in their segments numbers disclosed have also collected in columns.

The final result for this question has obtained by using the Excel summary

formula to get those total companies affected by IFRS 8. The following two

research questions have also obtained by applying those similar method

routines or formulas to the relevant collected raw data. In these ways, the

analysis stage of the study will be effectively accomplished by the advantages

18

of Excel as the variables which are stored within the tables can be easily linked

together in relationships (Horn, 2009). The final complete results and

comparisons of the numerical data are also presented by creating table by

Excel.

3.6 Reliability of Secondary Data

The whole analysis and results are based on the secondary data obtained from

the original annual reports prepared by the Singapore companies. According to

the SGX, the annual reports are the final and official work disclosed by the

companies registered on the SGX. Therefore, the data currently obtained are

trustworthy and genuine. Although the numerical data are difficult to be precise

and consistent in nature as stated in the (sagepub, 2007), this statement mostly

applies to financial data. As the whole analysis have been relied on the non-

financial data such as the number of segments, and line items disclosed per

segments, the secondary data in this particular research paper is reliable and

reputable.

3.7 Ethical ConcernsThe whole procedures and objectives of the research are carried out and

achieved by obtaining numerical data from annual reports which are publicised

in Singapore Stock Exchange (SGX) and secondary research format.

Therefore, no human participants will be involved in this current study.

According to Singapore Companies Act which has revised in 2006 , further

usage of companies’ annual reports are lawful as the reports are meant for

external users such as investors and shareholders to learn about the company

prior to investing (Singapore Statutes Online, n.d.). A copy of ethical issues

form will be included for future reference (Appendix 2).

Chapter 4 Analysis and Findings

4.1 Analysis on the Number of Reportable SegmentsFigure 2 illustrates the average number of segments. This figure has divided

into two sectors called SGX mainboard and SGX catalist which is also known as

the secondary listing (SGX, n.d.). SGX mainboard involved 38 firms and the 19

catalist listing included 22 firms (see Appendix 1). Firstly, the average number

of business segments for the mainboard has decreased by 0.05 under the

disclosure standard of FRS 1081 (IFRS 8) as it dropped from 2.97 segments in

2008 to 2.92 segments in 2010. However, the average numbers of segments for

the 22 firms under SGX catalist has remained constant since 2008, the year

FRS 142 (IAS 14) was still active. Therefore, the overall 60 SGX companies’

business segments have experienced a slight decrease of 0.03 under FRS 108.

Following the results from the (Section 1 and Section 2), the results for the

number for the number of companies reporting a change in the number of

segments have been derived.

Remarkably, total number of companies which encountered a decrease is 12

out of 60 while 13 companies have experienced an increase number of

segments although the mean number of segments for total 60 firms has

reached a decline of 0.03.

The reason behind these uncommon figures of decreased segments while the

total numbers of companies which have experienced an increase are more than

those companies decrease is because the companies have disclosed lesser

segments of more than one under FRS 108. For example, a company has

disclosed 5 business segments in 2008 and the segments reduced to 2 in 2010

and this cause the total mean number of segments to be declined more.

Furthermore, as mentioned in the earlier literatures, the reason of fewer

segments reporting could be due to the aggregation among them.

Furthermore, both the geographic segments by location of customers and

assets have declined from 2008 to 2010 correspondingly as business segments

(Section 1.2).

The mean number of geographical segments by customers’ locations for both

SGX mainboard and catalist has a slight fall from 4.37 to 4.29 and from 3.73 to

3.41 respectively and a total difference mean number of 0.20 have resulted

from it.

Likewise to the business segments, the number of companies which

encountered an increase in the geographic segments by where the customers

are located is more than a decrease regardless of a decline in the mean 1 FRS 108 is a local version of IFRS 8 which is identical to IFRS 8 in all material aspects (PwC, 2012).2 FRS 14 is a local version of IAS 14 which is identical to IAS 14 in all material aspects (PwC, 2012).

20

number of geographic segments disclosed (Section 2.2). Out of 60 firms 35

firms have not made a change on their geographic segments based on

customer’s regions.

Last but not least, the geographic segments depending on the companies’

assets’ location have the most decline mean number among the other

segments, resulting a difference in the mean of 0.29 (Section 1.3).

Reasonably, there is more decrease number of companies in total than

increase as the mean number of segments has decreased under FRS 108

(Section 2.3). The total number of companies dropping its segments number is

16 while a total of 8 companies have increased their segment numbers. 36

companies do not make a change on their segment disclosures hence both of

the segments reported before and after IFRS 8 remain unchanged since 2008.

As is observed from the above given statistics, the overall segments operated

within the business have reduced under the new standard IFRS 8 (FRS 108).

Therefore, the final outcomes based on the SGX 60 companies for the number

of segments reported have an opposing result figures from those literature

findings stated above as most of the researchers’ have an increased number of

segments disclosed within their chosen companies (Section 2.6). However

(ESMA, 2011; IASB, 2013) have also mentioned about those European

companies experienced a decline in their operating segment numbers. In

addition to this, ESMA has stated the business or geographic segments have

reduced due to the alteration of structure within the business.

For instance, changes involve activities such as acquisitions, withholding or

disposal and organisation structure amendment regarding to internal operating

(ESMA, 2011).

To conclude, the numbers of segments within the segment disclosures have

changed as they decreased under IFRS 8.

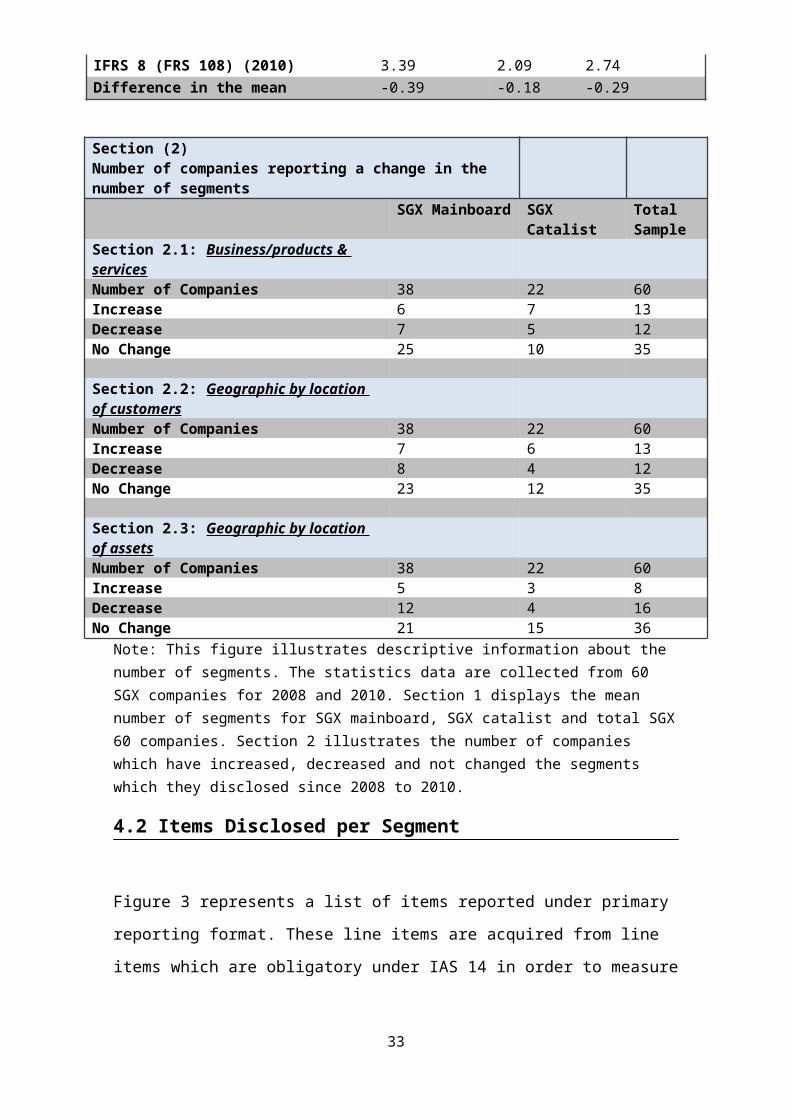

Figure 2 Number of segments comparison Section (1) Comparison of number of segments provided under IAS 14(FRS 14) and IFRS 8(FRS 108)

SGX Mainboard

SGX Catalist

Total Sample

Section 1.1: Business/products & servicesIAS 14(FRS 14) (2008) 2.97 3.36 3.17

21

IFRS 8 (FRS 108) (2010) 2.92 3.36 3.14Difference in the mean -0.05 0.00 -0.03

Section1.2: Geographic by location of customersIAS 14 (FRS 14) (2008) 4.37 3.73 4.05IFRS 8 (FRS 108) (2010) 4.29 3.41 3.85Difference in the mean -0.08 -0.32 -0.20

Section1.3: Geographic by location of assetsIAS 14 (FRS 14) (2008) 3.79 2.27 3.03IFRS 8 (FRS 108) (2010) 3.39 2.09 2.74Difference in the mean -0.39 -0.18 -0.29

Section (2)Number of companies reporting a change in the number of segments

SGX Mainboard SGX Catalist Total Sample

Section 2.1: Business/products & servicesNumber of Companies 38 22 60Increase 6 7 13Decrease 7 5 12No Change 25 10 35

Section 2.2: Geographic by location of customersNumber of Companies 38 22 60Increase 7 6 13Decrease 8 4 12No Change 23 12 35

Section 2.3: Geographic by location of assetsNumber of Companies 38 22 60Increase 5 3 8Decrease 12 4 16No Change 21 15 36

Note: This figure illustrates descriptive information about the number of segments. The statistics data are collected from 60 SGX companies for 2008 and 2010. Section 1 displays the mean number of segments for SGX mainboard, SGX catalist and total SGX 60 companies. Section 2 illustrates the number of companies which have increased, decreased and not changed the segments which they disclosed since 2008 to 2010.

4.2 Items Disclosed per Segment

Figure 3 represents a list of items reported under primary reporting format.

These line items are acquired from line items which are obligatory under IAS 14 22

in order to measure how many line items have been omitted under the new

disclosure standard.

Mostly, business segments information is disclosed as primary reporting.

However, there are also some companies whose geographic segments are

reported by using primary format while the business segments are disclosed

under secondary reporting format (mca.gov, n.d.).

For instance, if the company risks and returns are mostly dependent and based

on what it produces and offers such as products or services, the business

segments information are reported by using primary reporting format while its

geographic segments are reported in secondary disclosure format.

Inversely, if the risks and returns are highly affected by where those products or

services are sold or operated such as geographical regions, those geographic

based segments are reported by using primary reporting format while the

business based segments are reported under the format of secondary reporting

(Altaf, 2014).

Regardless of more than half of the SGX 60 companies disclosed identical

business and geographic segments without making a change since IAS 14 to

IFRS 8 (Figure 2 of Section 2), some of the line items disclosed under business

and geographic segments have changed when IFRS 8 superseded IAS 14 for

SGX 60 companies (See Figure 3; Figure 4).

According to Figure 3 of section 1, it is remarkable that approximately half of 32

SGX mainboard companies (17) which disclosed capital expenditure in 2008

have excluded it from disclosing in 2010, leaving a percentage of 45% from

84%. There is only a slight decrease in the number of SGX mainboard

companies disclosing the depreciation line when IFRS 8 is occupied as it

dropped from 35 to 31 in 2010. Followed by this item, segment results of

continued operations and discontinued operations, total assets and liabilities

have also reduced by a difference in the percentage of 29%, 2%, 20% and 29%

correspondingly.

Last but not least, it can be learnt that all the 38 SGX mainboard sample

companies have disclosed line items such as revenue obtained from customers

and inter-segment revenue in both years despite the standard has changed

from IAS 14 to IFRS 8.

23

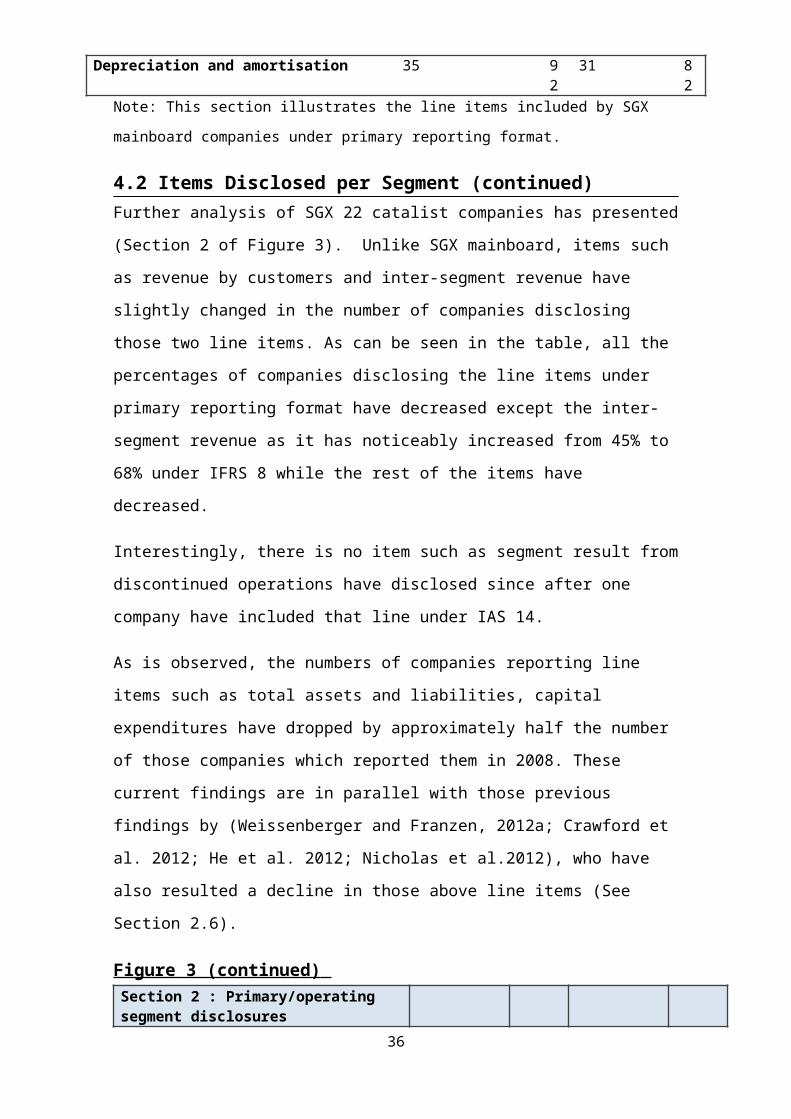

Figure 3 Items disclosed under primary reporting format

Section 1: Primary/operating segment disclosuresSGX Mainboard

Primary/operating segment disclosures (per IAS 14R)

Pre IFRS 8 (FRS 108) Post IFRS 8 (FRS 108)

No. of Companies % No. of Companies

%

Revenue from external customers 31 82 31 82Inter-segment revenue 26 68 26 68Segmental result – continuing operations 32 84 21 55Segmental result – discontinued operations 2 5 1 3Total assets 36 95 28 74Total liabilities 35 92 24 63Capital Expenditure (PPE & intangible Assets) 32 84 17 45Depreciation and amortisation 35 92 31 82

Note: This section illustrates the line items included by SGX mainboard companies

under primary reporting format.

4.2 Items Disclosed per Segment (continued)Further analysis of SGX 22 catalist companies has presented (Section 2 of

Figure 3). Unlike SGX mainboard, items such as revenue by customers and

inter-segment revenue have slightly changed in the number of companies

disclosing those two line items. As can be seen in the table, all the percentages

of companies disclosing the line items under primary reporting format have

decreased except the inter-segment revenue as it has noticeably increased

from 45% to 68% under IFRS 8 while the rest of the items have decreased.

Interestingly, there is no item such as segment result from discontinued

operations have disclosed since after one company have included that line

under IAS 14.

As is observed, the numbers of companies reporting line items such as total

assets and liabilities, capital expenditures have dropped by approximately half

the number of those companies which reported them in 2008. These current

findings are in parallel with those previous findings by (Weissenberger and

Franzen, 2012a; Crawford et al. 2012; He et al. 2012; Nicholas et al.2012), who

have also resulted a decline in those above line items (See Section 2.6).

24

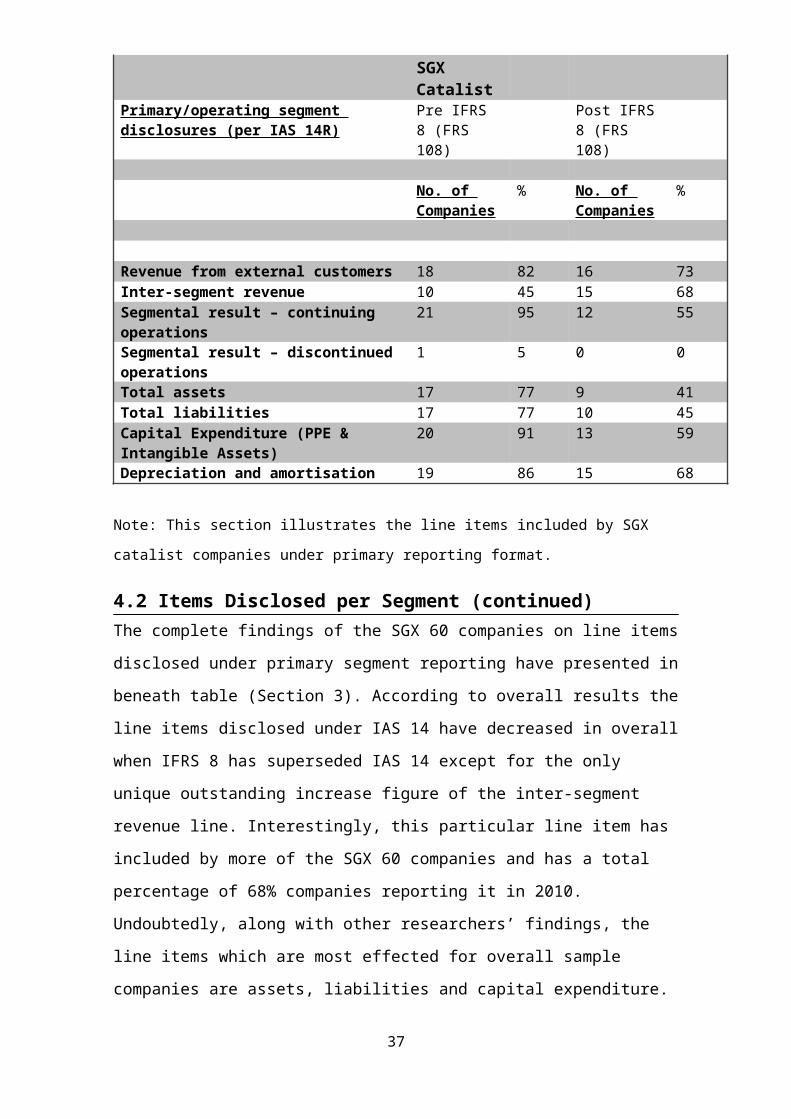

Figure 3 (continued) Section 2 : Primary/operating segment disclosures

SGX CatalistPrimary/operating segment disclosures (per IAS 14R)

Pre IFRS 8 (FRS 108)

Post IFRS 8 (FRS 108)

No. of Companies

% No. of Companies

%

Revenue from external customers 18 82 16 73Inter-segment revenue 10 45 15 68Segmental result – continuing operations 21 95 12 55Segmental result – discontinued operations 1 5 0 0Total assets 17 77 9 41Total liabilities 17 77 10 45Capital Expenditure (PPE & Intangible Assets) 20 91 13 59Depreciation and amortisation 19 86 15 68

Note: This section illustrates the line items included by SGX catalist companies under

primary reporting format.

4.2 Items Disclosed per Segment (continued)The complete findings of the SGX 60 companies on line items disclosed under

primary segment reporting have presented in beneath table (Section 3).

According to overall results the line items disclosed under IAS 14 have

decreased in overall when IFRS 8 has superseded IAS 14 except for the only

unique outstanding increase figure of the inter-segment revenue line.

Interestingly, this particular line item has included by more of the SGX 60

companies and has a total percentage of 68% companies reporting it in 2010.

Undoubtedly, along with other researchers’ findings, the line items which are

most effected for overall sample companies are assets, liabilities and capital

expenditure.

Therefore, according to figure 3 of section 1 to 3, it can be observed that SGX

60 companies have less disclosed the line items which they have included

under FRS 14 in 2010. Inter-segment revenue has the outstanding figure as

more companies are including it in 2010 while the rest items are either no

longer reported or less disclosed.

Figure 3 (continued)Section 3 : Primary/operating segment

25

disclosuresTotal Sample

Primary/operating segment disclosures (per IAS 14R)

Pre IFRS 8 (FRS 108)

Post IFRS 8 (FRS 108)

No. of Companies

% No. of Companies

%

Revenue from external customers 49 82 47 78Inter-segment revenue 36 60 41 68Segmental result – continuing operations 53 88 33 55Segmental result – discontinued operations 3 5 1 2Total assets 53 88 37 62Total liabilities 52 87 34 57Capital Expenditure (PPE & intangible Assets) 52 87 30 50Depreciation and amortisation 54 90 46 77

Note: This section illustrates the line items included by SGX total 60 companies under

primary reporting format.

4.2 Items Disclosed per Segment (continued)This figure is the continuous part of segment information statement called

secondary reporting. It has been discovered that there is a dramatic drop in

disclosing capital expenditure and carrying amount of segment assets

according to the data results of SGX 60 companies. Two-third of the companies

has excluded those items in their secondary reporting format in 2010 after IAS

14 was replaced, leaving a total companies’ percentage of 20% and 18%

respectively in 2010 (Figure 4 of Section 3). As shown in section 3, 78% of

companies have included the item called revenue obtained from external

customers. This figure has decreased for sizeable amount when compare to

those percentage of companies reporting it under IAS 14 in 2008 (93%).

These results are in aligned with the findings of Crawford et al. (2012). Crawford

et al. have further stated that the cause in a decline in those line items may

impact negatively upon the segment disclosures as less information has been

provided for the principals or shareholders.

Figure 4 Items disclosed under Secondary Reporting Format Section 1: Secondary/entity-wide disclosures

SGX Mainboard

Pre IFRS 8 (FRS 108) Post IFRS 8 (FRS 108)

26

Secondary/entity-wide disclosures (per IAS 14R)

No. of Companies % No. of Companies

%

Segment Revenue (external revenue) 36 95 32 84Capital expenditure (location of assets) 27 71 8 21Carrying amount of segment assets 31 82 7 18 Note: This section illustrates the line items included by SGX mainboard companies

under secondary reporting format.

Section 2: Secondary/entity-wide disclosures

SGX CatalistPre IFRS 8 (FRS 108)

Post IFRS 8 (FRS 108)

Secondary/entity-wide disclosures (per IAS 14R)

No. of Companies

% No. of Companies

%

Segment Revenue (external revenue) 20 91 15 68Capital expenditure (location of assets) 14 64 4 18Carrying amount of segment assets 17 77 4 18

Note: This section illustrates the line items included by SGX catalist companies under

secondary reporting format.

Section 3 : Secondary/entity-wide disclosures

Total SamplePre IFRS 8( FRS 108)

Post IFRS 8 ( FRS 108)

Secondary/entity-wide disclosures (per IAS 14R)

No. of Companies

% No. of Companies

%

Segment Revenue (external revenue) 56 93 47 78Capital expenditure (location of assets) 41 68 12 20Carrying amount of segment assets 48 80 11 18

Note: This section illustrates the line items included by SGX total 60 companies under

secondary reporting format.

4.3 Average Number of Line Items per SegmentThis figure has derived from the results which are obtained from the above

analysis and findings of the line items disclosed per segment. The disclosure of 27

business segments which is mostly disclosed by primary reporting format as the

chosen SGX companies’ business risks and returns are largely based on the

products and services they offered to the customers has more number of line

items reported than those geographic segments for both years ( 352>145;

269>66). Although the total segment line items by business sectors under both

IAS 14 and IFRS 8 have exceeded those disclosed under geographic

segments, the line items for business segments have reduced in 2010 when

IFRS 8 become active. Therefore, the average number of total line items for

business segments under IFRS 8 has reduced to 4.5 from 5.9.

Not only the business segments’ line items disclosed are affected but also those

reported under geographic segments have decreased dramatically from a total

number of 145 to 66, leaving an average number of 1.1 in 2010.

In accordance with the overall measurement results of line items per segments

(Figure 3; Figure 4), it has been very clear that SGX companies’ line items have

changed negatively as it dropped after IFRS 8 has taken place over IAS 14.

Figure 5 Average number of line items per segment 2008 (IAS 14(FRS 14)) 2010 (IFRS 8 (FRS 108))

Business segments

Geographic segments

Businesssegments

Geographic Segments

Total segment line items disclosed

352 145 269 66

Mean (total segment items/60)

5.9 2.4 4.5 1.1

Note: This figure shows the total segment line items disclosed under business segments reporting and geographic segments reporting. The average number of line items per segments has also identified.

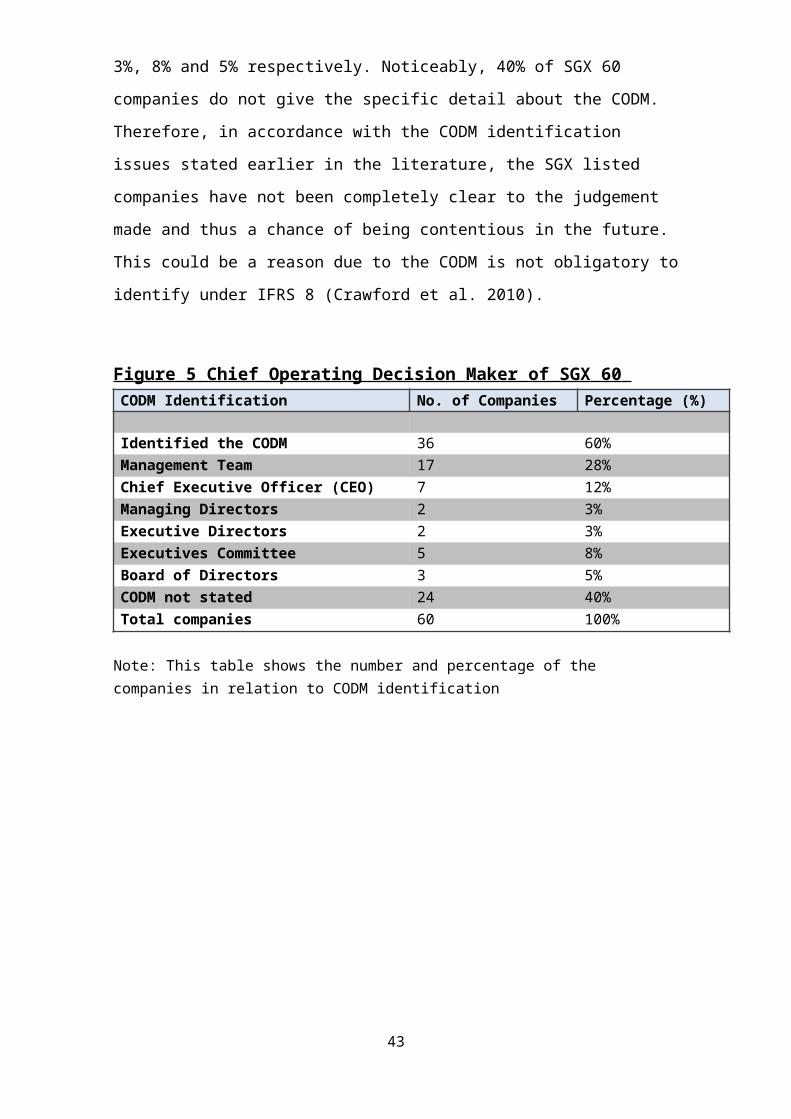

4.4 Analysis on Chief Operating Decision Maker of SGX 60From this figure it can be seen that 36 numbers of companies out of 60 have

voluntarily included about the information of whom is the person making a

decision relating to segment disclosures or who the CODM is. This gives a total

percentage of 60 out of 100%. The current study results of SGX 60 companies

28

are parallel to the findings of (Crawford et al. 2012; Kang and Gray, 2012) as

more than half of the total companies have given detailed information about the

CODM. It has been evidenced that most of the companies’ management team

(17%) have the position of CODM, followed by the CEO (7%). This current

result is parallel to (Kang and Gary, 2013) whose study is based on 189

Australian listed companies. The rest of the roles such as managing and

executive directors, executives committee and board of directors are the least

common CODM resulting 3%, 8% and 5% respectively. Noticeably, 40% of

SGX 60 companies do not give the specific detail about the CODM. Therefore,

in accordance with the CODM identification issues stated earlier in the

literature, the SGX listed companies have not been completely clear to the

judgement made and thus a chance of being contentious in the future. This

could be a reason due to the CODM is not obligatory to identify under IFRS 8

(Crawford et al. 2010).

Figure 5 Chief Operating Decision Maker of SGX 60 CODM Identification No. of Companies Percentage (%)

Identified the CODM 36 60%Management Team 17 28%Chief Executive Officer (CEO) 7 12%Managing Directors 2 3%Executive Directors 2 3%Executives Committee 5 8%Board of Directors 3 5%CODM not stated 24 40%Total companies 60 100%

Note: This table shows the number and percentage of the companies in relation to CODM identification

29

Chapter 5 Conclusion

5.1 Results OverviewFinally, this research paper has accomplished to answer the research questions

which are prepared in earlier to evaluate whether the new IFRS 8 has caused

changes to the segmental disclosures of Singapore firms.

The complete final results as a whole prove that segment disclosures of SGX

companies have changed after IFRS 8 (FRS 108) has superseded the old

standard IAS 14 (FRS 14). Based on the overall findings, IFRS 8 have impact

on the areas such as number of segments and line items per segment. Other

amendments or new steps which applied under the principles of the new IFRS 8

are also reasons supporting segment disclosures to be different from the

previous former version. For instance, applying the new stage of IFRS 8 such

as the management approach has affected those numbers of segments and line

items per segments disclosed under Singapore companies’ segmental

reporting.

Stemming from the management approach, the process with CODM who made

decision or managed about the segment reporting has also been judged by

numerous forecasters and users as the annual reports in general do not give

30

the detail information on it (Nichols et al. 2012). Along with others research on

various sample companies upon the analysis of CODM identification, some of

the Singapore selected firms have also not provided about who the CODM is.

However, there are also some SGX companies which have voluntarily disclosed

the CODM details.

5.2 The Current Findings in Consideration of Previous Literatures and Applied TheoryMost of the current findings are in parallel with the previous research findings.

However, there are also certain results obtained by SGX 60 companies which

are not consistent with those past results. One of the most uncommon findings

on SGX companies is about the decrease in the number of segments after the

introduction of IFRS 8 as many of the previous studies’ findings on it has

increasing results (Crawford et al. 2012; Kang and Gary, 2012; Nichols et al.

2012). Yet, this present findings of decrease in the number of segments by SGX

companies are comparable to the previous results obtained from the study on

Finnish companies by Saariluoma (2013).

Although the number of business and geographic segments of SGX 60

companies have a declining figures, it was found that the number of total

companies which have increased segment figures are more than those

companies which have suffered a decrease. The possible reasons behind this is

that under IFRS 8 segments are allowed to aggregate each other if they met the

segments aggregation requirements (PricewaterhouseCoppers, 2008) and

therefore combining two or more segments can result a decline in the number of

segments. As a result, literatures have stated that principals or shareholders of

segmental reporting will not be able to obtain the complete essential information

of the segments operated within the companies they are investing in (ESMA,

2011).

From the judgment made from the above reviewed literatures, SGX companies

have a slight negative impact by applying the ground-breaking standard IFRS 8