FilsEvlER - University at Buffalo

38

FilsEvlER Journal of Financial Economics 4.5 (1997) 97 134 Do institutions receive comparable execution in the NYSE and Nasdaq markets? A transaction study of block trades Michele LaPlante”, Chris J. Muscaretia**b Received August 1995: tinjl version received May 1996 The trading structure differences between the !4YSE and the Nasdaq market could produce different levels of trading liquidity. Several studies have attempted to measure these differences by comparing bid-ask spreads. This paper uses an alternative approach to compare liquidity. We analyze three issues: (I) the frc+encies of the sizes and types of block trades found in the two markets, (2) the immediate price effects of the block transactions, and (3) the temporary and permanent price effects of the blocks. We find evidence that the NYSE sys:em provides more liquidity for block transactions. Kqwords: Nasdaq. NYSE. Block transactions. Market structue JEL c.lu.s.s$cution: G 14; D23; L22 *Corresponding author. We thank Robert Rartalio. Jcx B&7, Hank Ressimbindw. Ananth Madhavan. I vrn Mclnish. Harold Mulhcrin. JelT Netter. Paul Schultz. Paul Segum. Duane Seppi. Dennis Shwhun. George Sotianos, Michael Vetsuypens. Rob Wood. an anonymous rckrec add seminar partcipants at tlniverscty of Mrsmi. Santa Clara Univcnity. Penn State. University of Georgra. Virginia Tech. the IW5 European Finance Association Meetings. the 1995 Asran-Pacific Finance Association Meet- ings. the I995 Financial Management Association Meetings. 2nd the 1995 Southern Fmance Associarion Meetings for helpful comments. 0304-405X 97 Sl7.00 r‘ 1997 Elsevier Science S.A. All right; wervcd PII SO;‘-:-405Xt96t00891-4

Transcript of FilsEvlER - University at Buffalo

FilsEvlER Journal of Financial Economics 4.5 (1997) 97 134

Do institutions receive comparable execution in the NYSE and Nasdaq markets?

A transaction study of block trades Michele LaPlante”, Chris J. Muscaretia**b

Received August 1995: tinjl version received May 1996

The trading structure differences between the !4YSE and the Nasdaq market could produce different levels of trading liquidity. Several studies have attempted to measure these differences by comparing bid-ask spreads. This paper uses an alternative approach to compare liquidity. We analyze three issues: (I) the frc+encies of the sizes and types of block trades found in the two markets, (2) the immediate price effects of the block transactions, and (3) the temporary and permanent price effects of the blocks. We find evidence that the NYSE sys:em provides more liquidity for block transactions.

Kqwords: Nasdaq. NYSE. Block transactions. Market structue

JEL c.lu.s.s$cution: G 14; D23; L22

*Corresponding author.

We thank Robert Rartalio. Jcx B&7, Hank Ressimbindw. Ananth Madhavan. I vrn Mclnish. Harold Mulhcrin. JelT Netter. Paul Schultz. Paul Segum. Duane Seppi. Dennis Shwhun. George Sotianos, Michael Vetsuypens. Rob Wood. an anonymous rckrec add seminar partcipants at tlniverscty of Mrsmi. Santa Clara Univcnity. Penn State. University of Georgra. Virginia Tech. the IW5 European Finance Association Meetings. the 1995 Asran-Pacific Finance Association Meet- ings. the I995 Financial Management Association Meetings. 2nd the 1995 Southern Fmance Associarion Meetings for helpful comments.

0304-405X 97 Sl7.00 r‘ 1997 Elsevier Science S.A. All right; wervcd PII SO;‘-:-405Xt96t00891-4

1. Introduction

The different trading structures of the NYSE. which uses a centralized public limit order book and assigns each stock to a single specialist. and the Nasdaq market, which allows many dealers to compete for order flow in each stock, could result in varying levels of market liquidity. It is often thought that the benefits of liquidity accrue mostly to traders of large volumes, typically institu- tional traders, rather than to small retail traders. The purpose of this paper is to SI:I*I~ whether the two principal tradQ?g I’ ,rkets provide Gmilar liquidity when l~~~;~~tci~~~g o~uck traocs of 1u.uo0 or more shares.

Whether institutions receive comparable execution on Nasdaq and the NYSE for their block trades has become increasmgly important. Institutional trading and institutional ownership levels in public firms have increased over the past several years (Kothare and Laux. 1995; Schwartz and Shapiro. 1992). Addition- ally, the NYSE has begun actively courting institutional investors in an effort to obtain new listings (Wall Srreer Journal. I l/1/95). While many Nasdaq-traded firms eventually choose to list on the NYSE. other exchange-eligible firms, including Apple Computers, Intel, and Microsoft. remain on Nasdaq.

Even though block brokers are available to negotiate the placement of large trades in both NYSE and Nasdaq-traded stocks. the two market structures could affect the price impact of the block trades differently.’ The National Association of Securities Dealers (NASD) offers several reasons why the Nasdaq market can provide high levels of liquidity for block trades (Groth and Dubofsky, 1987). First, the competitive nature of the multidealer system should force spreads to be narrower than those quoted by a ‘monopolist’ specialist. Second. dealers offer larger minimum depths so that even if the spread is larger it is good for many more shares than if offered by a specialist. Third, dealers can more readily make a market since they can diversify their positions and spread risk among themselves. Fourth, each dealer competes for and generates informa- tion, in contrast to a specialist who must act alone and is restricted by NYSE Rule 98. Finally. a specialist who adjusts inventory will affect the quoted price whereas Nasdaq offers a computerized system for dealers to contact each other when adjusting inventories so that prices are maintained.

On the other hand, Cochrane (1993) lists several reasons why the NYSE should olTs& superior liquidity. First, there is investor-supplied liquidity from rhe

‘It is noteworthy that despite the dilTercnces in trading mechanisms. block activity is roughly simdar across the two markets. During I990 1993, ratios of block volume to total volume for the NYSE(Nasdaq-NMS)were49.6%(42.7%).49.6%(40.2%k 50.7%(44.5%j.and 53.7%(48b%kand the number of block trades per day averaged 3,333 (2.241). 3.878 (2.81 I), 4,468 (3.884). and 5.841 (5.745). See the NYSE Fact Book 1991 1993 and the I991 1994 Nasdaq Fact Book 81 Company Directory.

limit order book. In contrast. Nasdaq does not have a formal process to expose. public limit orders and discourages them in many ways. Not until July 1994 did the NASD adopt a proposal to ban dealers from trading ahead of customer limit orders. However. the practice is still allowed if dealers ‘pass-off’ the limit orders to another dealer. The NYSE banned such practices several years ago (Wall Street Journal, 6/33/94). Second, Cochrane cites evidence of better prices and lower execution costs, again because of the limit orders which represent commit- ments to future prices. Third, designated market makers are committed to taking offsetting position< since each stock is assigned to a single specialist. Fourth, there is strong adherence to last-sale reporting as required by the SEC’s 90-second rule and. hence. ht=h levels of transparency. Finally, there is not only the opportunity to seek counterparties OK the floor in the ‘upstairs market’ before bringing a large trade t3 the floor, but these trades are then offered potential price improvement thrcugh exposure to floor traders and limit orders before final execution.’

Prior research provides no conctrsive answer as to which trading location offers greater liquidity. The pioneering work of Demsetz (1968) spawned the debate over which type of trading system provides liquidity at lower cost. He compares the advantages from economic< of scale in centralized trading activity to the disadvantages from a lack of competitive market making. Ho and Stall (1983) and Ho and Macris (1985) show that the multidealer market could offer more depth as trading volume increases. although at the cost of wider spreads.-’ Reinganum (1990) conducts an empirical investigation of liquidity premiums and concludes that neither the NYSE nor Nasdaq dominates in providing liquidity but that the Nasdaq system may provide greater liquidity than the NYSE for smaller firms. However, he finds no such advantage for larger firms, and his work cannot explain why Apple and others remain on Nasdaq. More recently. Keim and Madhavan (1995a. 1995b) use proprietary trading information for 21 institutions and find that transaction costs are higher in the Nasdaq marke! for all but the largest firms. WTerences in trading

’ Kcim and Madhavan (1996) and Madhavan and Cheng (1996) find a thr&old trade size above whuh negotiated block trades cause smaller price impacts than cquivalentlv sized blocks that originate on the floor. However. they find that a majority of block trades on the NYSE strll origtnate on the floor rather than in the upstairs market. This is supporttxl by Hasbrc.uck. Sofi.tnos, and Sosebee(1993) who report that on Jan. I 2. 1993.73% oftotal NYSE block volume originated on the floor of the exchange. Ninety percent of trades bctwccn 10.000 25.((K) shams. 6X% cl trades between 25.000 ltXUWO shares, and 43% of trades over IOO.o(K) shares originated in the dou .rstairs market. Also. MadhavanandChcng(l996)ti;rd for twomonths(Dec. 199.1 and Jan. 1994)that 8Je.b of NYSE

block volume originated on the tloor and 72 5, nT blocks for more than W(w)0 &rt!! originatd in

the downstairs market.

‘Other papers that model the influence o(altemative trading mechanisms on prim include Easley and O’Hara (1987). Burdett and O’Hara (1987). Scppi (1990). Kyle (1985). Admati and Pflciderer (1988). Grossman (1992). and Madhavan (1992).

loo M. LuPhntr. C.J. Musc~urcNu !Jnumol of Finunciol Economicc 45 (I9971 97 134

mechanismsgained national attention due to the wide publicity surrounding the research of Christie and Schultz (1994) and Christie et al. (1994) who find that Nasdaq market makers refrain from using odd-eighth quotes for many of the actively traded Nasdaq securities, raising the ques!ion of whether Nasdaq dealers implicitly collude to maintain wide spreads.

This paper adds to the debate over market structure and liquidity in a unique way by investigating which trading location offers greater liquidity for block trades. While much research has been conducted on block trades, nearly all of the studies have focused on Hocks traded on the NYSE.4 We focus our attention 1111 ~0.w !irms tha. >hoL ..! be especially interested in the effects of market structure on block trades, i.e., firms whose shares are often traded in blocks and can switch trading mechanisms if they so choose. Perhaps. as Amihud and Mendelson (1988) suggest, these highly liquid stocks on Nasdaq would realize little gain in liquidity from listing on the organized exchanges Large Nasdaq firms eligible to list are not remaining in the over-the-counter market because of prohibitively high listing costs; Sanger and McConnell (1986) find that the present value of initial and continual listing fees is 0.29% of equity for the average stock.

Although spreads are commonly used to measure liquidity, investors (parti- cularly institutional investors) could be concerned with other measures of trading costs, such as obtaining the best price for the transactions. Schwartz and Shapiro (1992) argue that institutions would rather have an accurate price that reflects the true value of the firm than a narrow spread, because mistiming or mispricing can hurt their returns more than paying the bid-ask spread.

Typically, spreads have been interpreted as reflecting the costs of market making and transacting (Huang and Stall. 1996). However, recent work by Demsetz (1995) shows that while Nasdaq spreads reflect the cost of market making to dealers, NYSE spreads do not. NYSE spreads are most often set by the limit order book which is driven by public interest so that NYSE spreads do not represent transaction and market-making costs for specialists. Furthermore, Nasdaq quotes often do not reflect the cost of trading for institutional traders. Preferencing agreements create no incentives for dealers to post competitive quotes since large order flows will automatically go to them. Keim and Mad- havan (199Sb) and Chan and Lakonishok (1995) provide evidence that posted quotes do not reflect the cost of trading with institutions due to their bargaining power, different investment styles, and trader reputations. Lastly, Madhavan

‘The reaction of bid ask spreads to block trades has been studied by Glosten and Harris (1988). Hasbrouck (1988.1991), Stall (19891. and George et al. (1991). Other papers have studied the impact ol block trades on transaction priczs. inclurling Schoks (1972). Kraus and Stall (1972). Dann et al. (1977). Mikkelwn and Partch (1985). Holthausen et &I. (1987.1990). Ball and Finn (1989). Madhavan and Smidt (Wl).Chan and Lakonishok(l993). Choeet al.(l992.l994).and Madhavan andCheng (19%

(1995) shows that the midquote is not the expected value for an asset when there is serial correlation in order flows. This suggests that the midquote may not reflect the ‘true price’. In this study, we use changes in transaction prices instead of changes in spreads as an alternative measure of liquidity. We recognize that this method fail: to measure the influence of preferencing arrangements and &dollar payments, but such proprietary information is difficult to obtain.

This paper investigates the block trades of the ten largest Nasdaq firms (based on 1990 year-end equity capitalization) eligible to list on the NYSE during 1988- 1990. Various criteria are used to create seven samples of ten NY SE firms matched to the ten Nasdaq firms. We analyze three issues: (1) the frequencies of the sizes and types of block trades found in the two markets, (2) the immediate price effects of the block transactions, and (3) the temporary and pennanent price effects of the blocks. Wc find that the overall price impact of block trading is smaller for the NYSE-tra&led issues than the Nasdaq-traded issues: this finding is robust for all matched samples. The findings are similar for several alternative measures of block impact. Expanded samples and alternative methodologies provide addttional supportive evidence.

This paper is organized as follows. Section 2 presents the data and explains the matching procedures. The results for various measures of price impact and permanent and temporary price etfects are provided in Section 3. which is followed by conclusions and a discussion in Section 4.

2 Data ami methodology

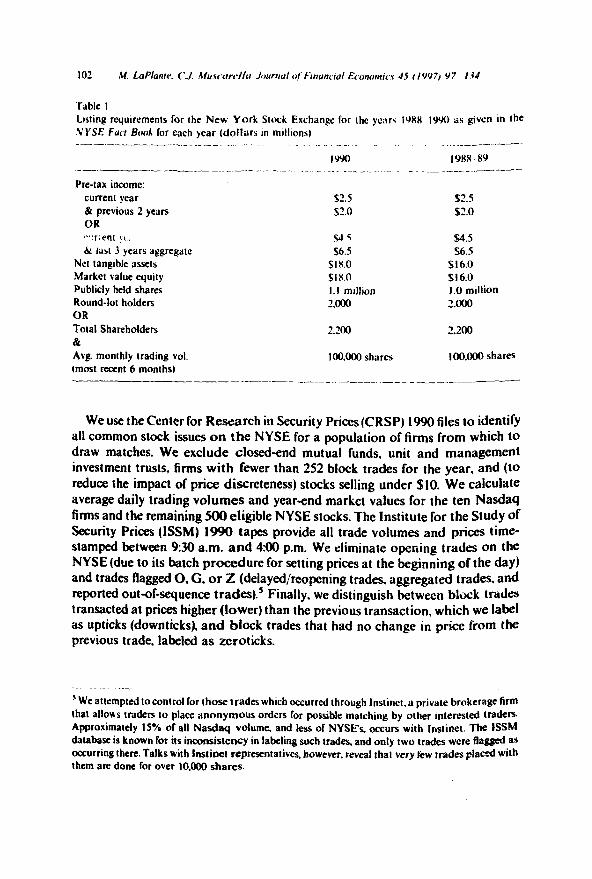

We study and compare the price impact of btxk trades on the NYSE and in the Nasdaq market during 1990 to contrast the liquidity otTered by the two trading structures to large trades. Table 1 presents NYSE listing requirements as found in the NYSE Fact Book. issues 1989--1991. We use COMPUSTATfiles to find Nasdaq firms that met these listing requirements from 1988- 1990, yet remained on Nasdaq through 1992. These criteria reduce the noise in our sample since they eliminate companies that qualified to list on the NYSE but either did not have time to move or moved immediately after our sample period. We exclude any firms that delisted from the NYSE to Nasdaq from 19861990. A total of 186 firms were eligible to list for three consecutive years. tut eight firms had data inconsistencies and 1 I more were not straight common stock issues.

We then focus on the ten largest remaini.tg Nasdaq firms ( lased on 1990 year-end market values) to allow comparisons of highly liquid firms under two different market structures. While Nasdaq-NMS firms have an average of 11 dealers assigned to their stocks, these ten firms each have over 26 deafers making markets in their stocks (1991 Nadaq Fact Book). The large number of dealers should, in theory, result in a highly hquid market for these securities.

Table I Listing requirements for the New Yorh Stock Exchange for the yc;\rc i9XX IWO as given in the .VYSE Focr Book for each year (dollars in millions)

Pre-tax income: current year & previous 2 years OR ~“:rBenl !“. & hl 3 years aggregate

Net tangible assets Market value equity Publicly held shares Round-lot holders OR Total Shareholders & Avg. monthly trading vol. (most reant 6 months)

2.5 s1.0

s4q s4.5 56.5 S6.5

SIR.0 Sl6.0 SIX.0 Sl6.0 I. I million I .O million 2sKm 2.ooo

2.200

lOO.000 shares

52.5 22.0

2.200

IO&O@ shares

We use the Center for R-arch in Security Prices(CRSP) 1990 files to identify all common stock issues on the NYSE for a population of firms from which to draw matches. We exclude closed-end mutual funds, unit and management investment trusts, firms with fewer than 252 block trades for the year, and (to reduce the impact of price discreteness) stocks selling under $10. We calculate average daily trading volumes and year-end market values for the ten Nasdaq firms and the remaining 500 eligible NYSE stocks. The Institute for the Study of’ Security Prices (ISSM) 1990 tapes provide all trade volumes and prices time- stamped between 930 a.m. and 4AXl p.m. We eliminate opening trades on the NYSE (due to its batch procedure for setting prices at the beginning of the day) and trades flagged 0, G, or 2 (delayed/reopening trades, aggregated trades. and reported out-of-sequence trades).’ Finally, we distinguish between block trdda transacted at prices higher (lower) than the previous transaction, which we label as upticks (downticks), and block trades that had no change in price from the previous trade, labeled as zeroticks.

‘We atlempted IO control for those trades which occurred through Instinct. a private brokerage !irt~~ that allows traders IO place anonymous orders for possible matching by other Interested I&Hs. Approximately 1% of all Nasdaq volume. and less of NYSE’s, occurs with f&net. The ISSM database is known fbr its inconsistency in labeling such trades, and only IWO trades were Aa& as occurring there. Talks with Instinct rcpresenratives. however. reveal that very few trades placed with them are done for over 10,000 shares.

As reported by Atkins and Dyl (1993) and Gould and Kieidon (l994), any comparison of trading volumes between Nasdaq and an organized exchange must take rota account the dealer effect on reported volume in the over-the- counter market. Suggestions for percentages by which to reduce reported Nasdaq volume vary from 50% to 65%. We mitigate this problem in our matching procedures described below.

Our objective is to isolate the impact of market structure on liquidity. To do so, we need to control for nonmarket determinants of liquidity, such as firm size and flow of information. Prior research suggests that market value and trading volume are proxies for these determinants (see Amihud and Mendelson. 1986;

Grossman and Miller. :988; Baker and Edelman, 1990; Reinganum. 1990, for work in this area). We must also control for any effects caused by the difference in volume reporting procedures. Since there is no single dimension of matching that obviously dominates all others, we create seven matched samples with ten NYSE firms in each sample. These firms are picked without replacement and matched to a particular Nasdaq firm according to one of the following criteria: (1) 1990 year-end market value oiequity, (2) annual total trading volume using one-half the Nasdaq annual total trading volume, (3) the minimum combined difierence of one-half the annual Nasdaq trading volume and the 1990 yearend market value of equity, (4) 1990 year-end ratio of market value of equity to book value of equity, (5) annual number of block trades, (6) annual number of block trades using one-half the annual number of Nasdaq block trades, and (7) annual block trading volume using one-half the Nlsdaq annual block trading volume.6

Table 2 lists the firms in each sample and. in parentheses the percentage difference in the primary matching variable between each pair. Of the 70 matches, almost 70% (49) are matched to within 1% of ihe Nasdaq variable. There are 59 matches within 5% and 64 are within 10%. Only two matches exceed differences of 20%. The sample created by matching to the annual number of block trades contains three of the four highest percentage ditfetences. No NYSE common stocks had more than 82% of the annual number of block trades reported for Nasdaq-traded Intel, Apple. or MCI. Since this may be due to the inflated volume figures reported by Nasdaq. we create the sample matched to one-half the Nasdaq firms’ annual number of block trades.

Mean and median values of descriptive variables are shown in Table 3. The mean market values of the NYSE firms matched according to one-half

“We originally created a match based on \hrce-dlglt SIC codes and market value in an attempt lo control for potential di&rences in the degree of asymmetric information. A more comprehensive measure of this and firm-specilic growth opportunities is the ratio of market ralue of equity to book value of equity. We thank Hersh Shefrin and Meir Statman for this suggestion. WC also created a match based on the ratio of annual block volume to total volume. but because five of the ten matches exceeded dilTerences of 30%. we dropped this sampie.

Table

2

NYSE

firm

s wh

ich

comp

ose

seve

n sa

mples

ma

tched

to

the

ten

large

st Na

sdaq

firm

s eli

gible

to lis

t on

the

NY

SE

durin

19

8X-

1990

All

samp

les

are

base

d on

19

90

data.

Th

e pe

rcenta

ge

differ

ence

in

the

prim

ary

match

ing

vana

hle

betw

een

each

Na

sdaq

pa

renth

eses

. --

_.__

__._

_ -_

__.

--- _..

_ --

-.___

.--.

--- .-..

-

Marke

t va

lue

& 1

Trad

ing

f Tr

ading

Ma

rket

value

’ Nu

mber

of

Nasd

aq

Marke

t va

lue’

volum

e’ vo

lume’

Book

va

lue’

bluck

tra

des’

_-_---

-.-

--- .-.

_ --.

._---.

- __

.. -

Micro

soft

Corp

. Sc

ars

Roeb

uck

NCNB

Co

rp.

South

ern

Co.

Merck

Co

Co

ca-C

ola

co.

(1.07

) (0

.15)

(X.49

. I.7

41

( -

2.89

1 ( -

0.2

9)

Inte

l Co

rp.

Hewl

ett

Pack

ard

Peps

ico

Texa

s Ut

ilities

W

estin

ghou

se

Elec

. AT

&T

10.5

4 (

- 1.9

2)

( --

8.88,

- 6.1

3)

( -

0.47)

(

.- 29

.41)

Apple

Co

mpute

r Am

erica

n El

ectric

Po

wer

(0.3

I)

MCI

Comm

. Un

ited

Telec

omm

( -

0.22

1

Food

Lio

n,

Inc.

Wisc

onsin

En

ergy

(

- 0.1

0)

Sun

Merri

ll Ly

nch

Micro

syste

ms

(0.25

)

GTE

Corp

. (0

.31)

Comp

aq

Comp

uter

Free

port

t -

1.38.

- 6.0

1)

McMo

han

( -

0.56)

Citic

orp

( --

19.9

11

Gene

ral

Motor

s Un

ited

Telec

omm

Flowe

rs Ind

ustrie

s Pu

ilip

Morri

s Co

. (0

.67)

( -

23.90

. -

0.22,

(0.47

) (

- 18

.86)

Ediso

n Br

other

s Kn

ight-R

idder

(

- 0.5

X)

(5.18

. 5.2

8)

Sara

Le

e Co

rp.

mm

Motor

ola

( -

1.36)

Un

ion

Carb

ide

Boein

g Co

. (

- 12

.28.

-- 1.8

7)

10.00

)

Time

W

arner

(0.00

)

Fede

ral

Nat.1

Mo

rtg.

Asso

c. ( -

6.1

7)

rm

:nrd

its m

atche

d tir

m IS

sho

wn

in

I Nu

mber

of

block

tra

des’

! Bl

ock

volum

r* _-

. ._-

---.-.-

-. __

.

Koch

well

Int’l

CMS

Ener

gy

n.48)

(

- 0.9

9)

Bocii

tg

Boein

g I

- 1.4

5)

(3.33

)

Brist

ol Me

yers

GTE

Carp

Sq

uibb

(0.18

) (

- 0.0

3)

Imer

ican

Fede

ral

Xat’l

Expre

ss

Mortg

age

Asso

c (

- 2.4

1)

( -

0.50)

Nice

r Am

erica

n St

ores

mm

(0

.11)

Chas

e Ma

nhat

tan

to.51

1

DuPo

nt

de

Nemo

urs

E.1

( -

0.47)

SAFE

CO

Corp

. Ge

rber

Prod

ucts

DPL

Holdi

ng

Clor

ox

Co.

Willi

ams

Cos.

Mario

n Me

rrill

Rite

Ai

d Co

rp.

(0.11

1 co

. (2

.36.

- 2.1

4)

NJ.00

) DO

W

(0.11

) I -

0.0

3)

(0.21

)

Nord

strom

Inc

. Co

ca-C

ola

Ctcu

it Ci

tv Ni

agrd

Mo

hawk

US

X Co

rp.

Hallib

urto

n Co

. ITT

Co

rp.

Enter

prise

s St

ores

Po

wer

( -

0.46)

I

- 0.0

4)

( -

0.07)

( -

0.0

7)

( -

0.01)

( -

- ‘.Y

’ -

1.68)

-

-.

Core

State

s Fin

. Ea

ton

Corp

. Cy

press

Su

per

Value

St

ores

Te

ktron

ix Inc

. Te

xas

Utihl

ies

<‘ray

Re

xarch

(0

.37)

Semi

cond

uctor

(

- 2.9

11.2.

57)

(0.w

to.

121

(0.42

) I -

0.

321

costc

o Av

on

Prod

ucts

Digit

al Co

mm.

Lubr

izol

Corp

. Na

lco

Chem

ical

McDe

rmott

In

t’l W

illiam

s Co

s. W

holes

ale

( --

0.02)

(0

.16)

(3.06

. -

XX)

( -

0.47)

(0

.X)

( -

0.51

1

Ecola

b Inc

. (0

.35)

Fund

Am

enca

n C-

OS.

(-Ott,

fextro

n Inc

. of

Delaw

are

mY)

Capit

al Ho

lding

(

-- 0.3

4)

’ Matc

hed

on

year

-end

ma

rket

value

s of

equit

y b M

atche

d on

an

nual

tradin

g vo

lume

using

on

e-ha

lf Na

sdaq

vo

lume.

‘Matc

hed

on

minim

izing

the

Join

t dif

leren

cc

in on

e-ha

lf an

nual

Nasd

aq

tradin

g vo

lume

and

year

-end

ma

rket

value

of

equit

y. *M

atche

d on

clo

sest

ratio

of

year

-end

ma

rket

value

of

equit

y IO

boo

k va

lue

of cq

uitv.

e Matc

hed

on

the

annu

al nu

mber

(II

block

tr;

tdes

of Na

sdaq

firm

s. ’ M

atche

d on

on

e-ha

lf the

an

nual

numb

er

ol blo

ck

trade

s of

Nasd

aq

Iirms

* Fldt

ched

on

on

e-ha

lf the

an

nual

block

vo

lume

of N:

tulaq

tirm

s.

a

Table

3

Mean

(m

edian

) sa

mple

value

s of

selec

ted

desc

ripttv

e va

riable

s for

the

ten

lar

gest

Nasd

aq

firms

eligib

le to

list

on

the

NY <

;E d

&wing

19

88-1

~0

and

seve

n 2

samp

les

of ma

tched

NY

SE

firms

(See

Tab

le 2

for

a de

scrip

tion

of ma

tching

me

thods

) 2 a 0

_.._.

__---

--._

--.-..-

--_

-.--__

.__

_-..-_

-.----

--.

-. -~_

.--.--

-

._

Marke

t va

lue

$

f Tr

ading

&

3 Tr

ading

5

Marke

t va

lue

Numb

er

I j

Numb

erof

j Bl

ock

5 Na

sdaq

Ma

rket

value

’ vo

lume

volum

e Bo

ok

value

blo

ck

trade

s blo

ck

trade

s vo

lume

‘- : -

----.-.

-- --.

-.. ..-

--.----

.-.-

- -- -

--.--.

... . .

. .

- .-

.-__._

_. __

_ 5

Marke

t va

lue

{in

8 mi

llions

)

Shar

e pr

ice

(8)

Daily

tra

ding

volum

e (0

0’S)

Bloc

k vo

lume)

To

tal

volum

e (U

/O)

Numb

er

of blo

ck

trade

s

Daily

blo

ck

volum

e (O

W

Numb

er

of al

l tra

des

3.78

9 (2

.105)

34

(32) 8.

728

(6.28

6)

41.6

2 W

UO)

s.515

(2

.987)

4.15

4 (1

.831)

107.

795

(116

.180)

3.x04

(2

.106)

30

(29) 3.

1’2

(2,49

9)

48.3

9 (5

0.28)

I .66

5 (1

.136)

1.56

9 t 1

.268)

43.6

02

(38.8

1 I)

7.29

2 ( I

.829

)

27

(24) 4.34

7 (3

.14Ol

48.6

4 (4

8.45)

2.31

4 (1

.895)

2.00

8 t I

.7861

67.0

07

(38.0

76)

3.72

7 (2

.141)

32

(32) 3.

970

(3.27

6)

SO.16

(5

0.31)

1.80

7 t 1

.338)

2.18

3 t 1

,394)

52.8

62

(48.4

27)

7,97

5 (4

.674)

39

(33) 4.

038

(3.26

6)

44.4

8 (4

4.99)

2.02

5 (1

.649)

1.73

7 (1

.421)

66.2

74

(53.1

671

IZ.?2

X t7.

u.w

40

(36) 9.03

5 (7

.737)

so.47

(5

2.56)

4.64

7 (2

.991

I

4.88

8 (4

.307)

121.

844

(89.5

68)

7.89

5 (?

.656)

36

(331

5.17

7 (2

.839)

47.8

5 (4

4.74)

2.73

2 (1

.48’

3 2.6

3 I

(1.17

5)

70.9

I 8

(43.5

81

J

7.84

1 P

(2.27

8)

2. 4 29

3

(26)

i 5 4.

420

s. (1

.482)

;

47.2

7 ‘n 2

(46.3

7)

F

2.50

2 2

(940

) I=

2.08

7 s

1’)08

)

60.4

81

(21.1

61)

Numb

er

block

tra

des

5.10

3.82

3.45

3.42

Numb

er

all

trade

s t%

t (2

.57)

(2.Y

3)

(4.98

) (2

.93)

Relat

ive

trade

siz

e (O

/b)*

16.8-

b 23

.52

21.2

0 31

.82

(18.6

9)

t I7.4

(1)

t 10.9

Y)

(17.7

5)

Shar

es

outst

andin

g I 1

7.96

7 14

0.12

6 24

7.34

7 12

9.45

8 @

OO

kl (1

07.O

YO)

( 108

.297)

(8

5.607

) (1

05.6R

4)

tnsti

tutio

nal

owne

rship

48 8

H 47

.8O

54.3

4 54

.91

WI

(56.1

0)

(46.4

9)

152.4

6)

I58.94

)

Numb

er

of ins

titutio

ns

210

237

274

23H

(I731

(2

lOl

(175

) (IY

8)

Offic

er &

direc

tor

15.0

6 IO

.?7

4.90

6.72

owne

rship

(%I

(4.98

) (IL

SY)

(3.55

) (0

.45)

------

-.--.

.---...

--.--

. . ._.

. __

..__..

-_--

._ .__

_._

- __.

__ -_-

_ .- .

_.___

..

*Rela

tive

trade

siz

e :=

Aver

age

block

tra

de

airc

Avcra

ge

nonb

lock

trade

sir

e.

3.06

(3.10

)

26.4

6 (2

4.63)

179,

414

(144

.867)

54.5

3 (5

2.55)

302

(267

) 3.36

(2.21

)

3.81

(3.34

)

25.6

6 tl3

.40)

394.

574

(257

.93

I )

53.7

5 ( 5

6.94)

3x1

(377

) 2.7x

W.77

) -

_ --

. ..-

3.85

(3.42

)

22.1

5 (I

5.05)

195.

695

(124

.817)

57.4

0 (5

7.91)

305

(223

3.06

(1.03

)

4.14

t4.44

)

17.8

6 (1

2.26)

22 I

.220

(83.0

45)

60 4

0 ijY

.76)

283

(201

) 3.91

(0.79

)

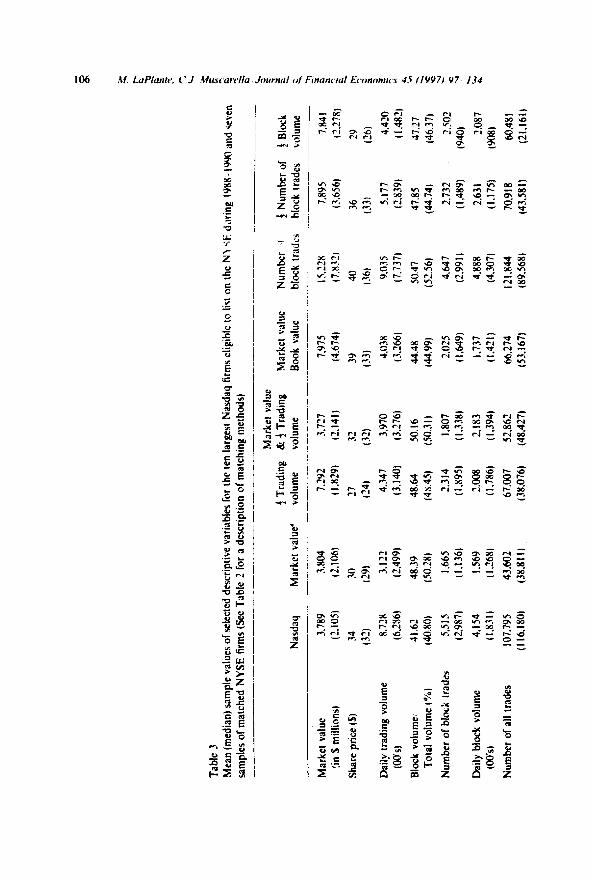

Nasdaq trading volume, market value-to-book value, one-half number of block trades, and one-half annual block volume are twice that of the mean Nasdaq market value, and NYSE firms matched to the average annual number of Nasdaq block trades are nearly five times larger in market value. This is consistent with the notion that reported Nasdaq volume is inflated by at least 500,/o. Average share prices are very equivalent, however. indicating that for a given block trade site, dollar-volume traded is also equivalent. The mean and median ratios of block volume to total volume are roughly the same across all s;liqde\. .,wragirs- -IO? II ?"1. Tr-<c .,rdgnltudcs suggest that block trade execution should be a concern to both firms and traders. Interestingly. even though on average the Nasdaq sample has two to three times more block trades per year (5.515) than the NYSE samples. the mean number of block trades relative to all trades is 5.10% for the Nasdaq sample. This is only slightly higher than the 3%-4% proportion of block trades found on the NYSE. In addition, while the average Nasdaq block trade is almost 17 times greater than the average nonblock trade, the average NYSE block trade is 18 to 32 times greater. Thus, Nasdaq has higher block volume and more frequent block trading, but the average Nasdaq block trade size relative to nonblock trade size is smaller than that for the NYSE.

We collect several ownership statistics from Compact Disclosure. The Nasdaq sample has on average fewer shares outstanding, but the level of institutional ownership and the number of institutional shareholders are roughly equivalent to that of the NYSE samples. We find consider- able overlap of institutions holding shares of both our Nasdaq and NYSE firms. On average, 77% of the institutions that have investments in our sample of ten Nasdaq firms also invest in the NYSE sample firms. Thus, any differences in the impact of block trades are unlikely to be the result of differences in institutional ownership. Finally. the mean percentage ownership of officers and directors is highest for the Nasdaq sample (I 5.06%). This is the result of high inside ownership for Microsoft (59%) and Costco Wholesale (40%).

3. Re&ts

3.1. Block trades compared to preuious trades

We begin our analysis by comparing the price of the block transaction to the price of the previous transaction for that stock. We then expand the analysis to check for potential information leakage by comparing the block price to trans- action prices occurring up to one hour prior to the block transaction. Finally, we use an alternative sample and methodology to provide additional evidence on the price impact of block transactions.

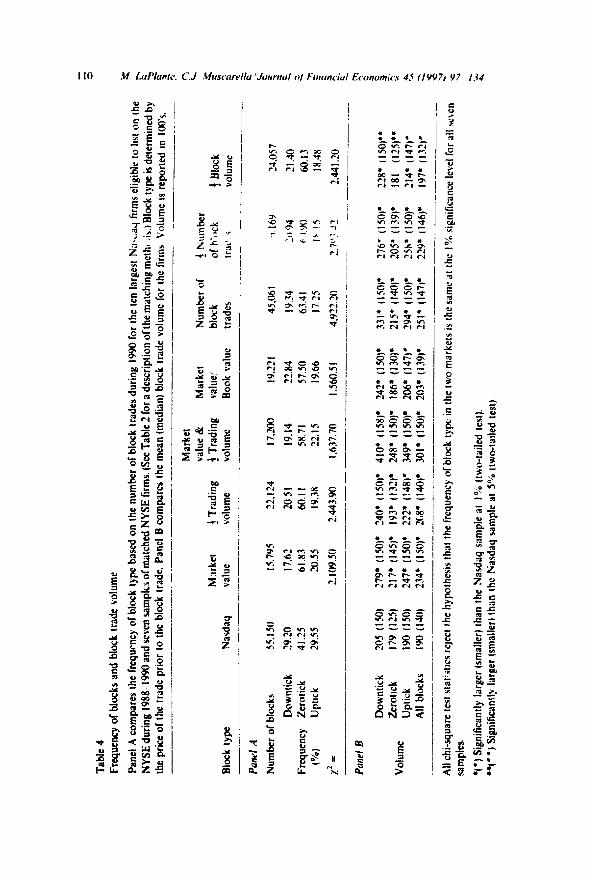

3.1.1. Bloch trade price compared to previous trade pric” Panel A of Table 4 shows the frequency of block type (uptick. downtick, or

zerotick) determined by the previous trade price for the ten Nasdaq firms and seven samples of matched NYSE firms. Nasdaq stocks experience uptick and downtick block trades ;n roughly the same proportion (29.20% and 29.55%, respectively), while zerotick block trades occur more frequently (41.25%). Sim- ilar to the Nasdaq sample, the NYSE samples experience uptick and dowutick block trades in roughly equivalent, but smaller. proportions (about 20%). All seven NYSE samples trade bhocks as zeroticks about 50% more often than the Nasdaq sample. averaging about 61% zerotick block trades. Chi-square tests reject the hypothesis that the freL:uency of block type in the two markets is the same for all seven matched samples.

Panel B of Table 4 shows that the mean block trade volun~es are significantly smaller on the Nasdaq for all seven matched samples and median volumes are significantly smaller for six of seven samples. The mean block size for all Nasdaq blocks is 19,000 shares, while NYSE blocks matched to market value average 23,400 shares. The medians are 14,000 and 15,000. respectively. The block voiumcs-for all three types of block trades !downtick. zerotick. and uptick) are usually significantly smaller for Nasdaq block trades compared to NYSE block trades for all seven matched samples.

To better understand the relative sizes of individual block trades in the two markets, Table 5 presents a frequency distribution by block trade size and block type for all samples of matched firms. For Nasdkq firms, 42.10% of all block trades occur at the minimum block trade volume of lO.ooO shares. About 3 1% of all Nasdaq block trades involve 10,OOl to 20,ooO shares. The frequency of Nasdaq block trades continues to decline as block volume increases, with only 2.52% of the blocks involving more than 50,000 shares.

NYSE block trades occur less frequently at the minimum block size than Nasdaq block trades, averaging only about 33% of block dctivity. NYSE block trades happen more often at 10,001 to 20.000 shares than at any other block size and represent about 40% of the blocks. The frequency of NYSE block trades also declines as block volume increases. However, blocks of more than 50,000 shares occur about twice as often on the NYSE than on Nasdaq. The demand for block trades by institutional traders cannot explain this findmg since the number of institutional owners, the percentage of institutional ownership, and the identity of institutional owners are very similar for the biasdaq and NYdt samples. Apparently. the NYSE trading mechanisms are capable of handling much larger blocks than the Na.sdaq multidealer system.

It is also interesting that the distribution of block types changes with different block volumes. The frequency of zerotick block trades declines with higher block volumes in both markets. However, the NYSE has a higher incidence of zerotick block trades than the Nasdaq for all categories of block volumes. That is, while large block trades ate more likely to cause price movements, they

Table

4

Freq

uenc

y of

block

s an

d blo

ck

trade

vo

lume

Pane

) A

comp

ares

the

fre

qurnc

y of

block

typ

e ba

sed

on

the

numb

er

of

block

tra

des

durin

g 19

90

for

the

ten

large

st Na

~.a.)

firms

eligib

le to

list

on

the

NYSE

du

ring

1988

19

90 a

nd

seve

n sa

mpks

of

match

ed

NYSE

firm

s. (S

ee

Table

2

for

a de

scrip

tion

ofthe

ma

tching

me

thI

sis.l

Bloc

k typ

e is

dete

rmine

d by

the

pr

ice

of the

tra

de

prior

IO

the

blo

ck

trade

. Pa

nel

B co

mpar

es

the

mean

(m

edian

) blo

ck

trade

vo

lume

for

the

firms

Volum

e is

repo

rted

in I(w

)‘s.

__---

. ~~

-

-_-.

- .-.

.

Marke

t va

lue

& Ma

rket

Numb

er

of 4

Numb

er

Mxrke

t !

Trad

ing

i Tr

ading

va

lue,

block

of

h’clck

4

Bloc

k Bl

ock

type

Nasd

aq

value

vo

lume

volum

e Bo

ok

value

tra

des

triu’

\ vo

lume

------

--.-

----

------

.------

-- -.

-_-

._.__

_-__

Paw/

A

Numb

er

of blo

cks

Down

tick

Freq

uenc

y Ze

rorick

to4

Up

ttck

$ =

55.1

50

29.2

0 41

.25

2Y.J.

(

I S.?

Y5

Il.62

61

.83

20.5

5

2.10

950

22.

I24

17.2

0 I Y

.22

I 45

.061

20.5

I 19

.14

22.8

4 19

.34

60.1

I 5X

.71

s7.50

63

.41

19.3

8 22

.15

19.6

6 17

.25

2443

.90

1637

.70

1.56

051

4.Y2

2.20

24.0

57

21.4

0 60

.13

I X.4

X

2.441

.20

Pane

l B

Down

tick

Volum

e Ze

rotxk

Up

tick

All

block

s

205

(150

) 27

9. (I

50).

240’

(150

). 41

0. (1

58).

$42.

(I 5O

P 33

10

(150

). 17

9 (1

25)

217,

(145

). 19

3’ (1

32).

248.

(ISO)

* 18

6. (1

30)+

21

5. (1

40)’

IW

(150

) 24

7’ (I

50)’

222;

(!48)

’ 34

9. ( l5

0P

206’

(147

)’ 29

4. (1

50)’

I90

(140

) 23

4. (I

50)’

2(,8*

(M

O)*

301’

(150

)’ 20

3’ (1

39).

251.

(147

).

‘76’

t 150

)’ 22

8; (IM

)**

205’

(I 39

). 18

1 (1

25)+

+ 2S

h*

( I50)

8 21

4’ (1

47)’

229’

(146

)’ 19

7’ (1

32)’

.~--

----

..-

...-

-.--

----

-._

----

--

--.

----

__-_

-. __

All

chi-s

quar

e tes

t rta

t:+uc

s re

ject

the h

ypoth

esis

that

the f

requ

ency

ol

block

typ

e in

the t

wo

marke

ts is

the

same

at

the

lo’ I”

signif

icanc

e lev

el fo

r al

l se

ven

samp

les.

*(‘)

Sign

ilican

tly

large

r (sm

aller

) tha

n the

Na

sdaq

sa

mple

at lob

(tw

o-tai

led

test).

*I(**)

Si

gnific

antly

lar

ger

(small

er)

than

the

Nasd

aq

samp

le at

5%

(two-

tailed

tes

t)

Table

5

Volum

e fre

quen

cy

distri

butio

ns

ol blo

ck

trade

s du

ring

199O

(in

perce

nttfor

the

ten

lar

gest

Nasd

aq

firms

eligib

le to

list

on t

he N

YSE

durin

g 19

88--1

990

and

seve

n sa

mples

of

match

ed

NYSE

firm

s. (se

e Ta

ble

2 for

a

desc

riptio

n of

the

match

ing

metho

ds);

block

typ

e is

dete

rmine

d by

the

pric

e of

the

trade

pr

ior

to the

blo

ck

trade

--

Marke

t va

lue

j Tr

ading

%

4 Tr

ading

Ma

rket

value

Nu

mber

of

f Nu

mber

of

f Bl

ock

Nasd

aq

Marke

t va

lue

volum

e vo

lume

‘Boo

k va

lue

block

tra

des

block

tra

des

volum

e --

___--

--.

-_-..-

._._ -_

---_--

..---

---__

_

-_-__

-...-.-

-...-__

---.-

..-_---

-- -.

Freq

uenc

y wi

thin

Volum

e Bl

ock

type

volum

e -_-

---

_---~

- .--

_

10.0

00

Down

tick

Zerot

ick

Upttc

k AL

L

10.0

01

-20.0

00

Down

tick

Zernt

ick

Uptic

k AL

L

20 &

)I -3

0.000

Do

u-vtic

k Ze

rotick

Lp

tick

ALL

30.0

01

50.0

00

Down

tick

Zero

t ick

Up

tick

ALL

> 5o

.ooo

Do

wntic

k Ze

rotick

L’p

tick

ALL

27.0

7 43

.x9

29.0

4 42

.10

2X.6

3 41

.42

29.9:

30

.78

Jl.SX

.X

.20

30.2

2 Il.5

5

34.5

2 35

.30

10.

I x

7.03

40.2

0 31

4x

x31 2.5

2

Freq

uenc

y Fr

eque

ncy

with

in wi

thin

volum

e vo

lume

15.5

7 64

.25

?O.IH

31

.x9

17.1

X 62

.19

IY.6

2 3Y

U6

19.3

8 59

.65

‘0.98

14

.71

--

17.4

4 63

.96

I x.60

33

.81

20.

I 7

61.5

4 I X

.29

40.

IO

?MO

55.3

0 24

.11

X.69

24.S

I 52

.2’)

$3 ‘

0 e.

.w

4.n4

226H

59

2:

I n.05

I3

.Yh

26.7

6 53

.1x

?0.0

6 7.

Y6

29.2

4 47

.50

23.2

6 4.1

6

Freq

uenc

y wi

thin

volum

e ~--

Il.25

60.8

9 2

I .86

30

.53

17.9

0 61

.11

20.9

9 3R

.40

19.8

3 57

.59

22.5

9 15

.39

21.2

6 53

.61

25.1

3 8.

X8

30.4

5 44

.38

25.1

7 6.7

3

Freq

uenc

y Fr

eque

ncy

wtth

in wi

thin

volum

e vo

lume

_- _ .

.---__

-- --

--

20

.48

17.1

1 17

.95

IS.4

5 60

.40

66.2

6 63

.H9

63.9

0 lY

.II

1 ti.6

3 18

.16

17.6

4 34

.19

33.7

9 32

.21

37.0

3

22.6s

58

.39

18.9

3 40

.70

23.1

6 55

.67

21.1

7 13

.57

27.5

2 49

.w7

22.6

1 7.

85

19.11

) 64

.78

16.1

2 3Y

.22

19.8

2 62

.10

18.0

8 14

.07

20.6

5 21

.36

61.8

1 61

.00

17.5

4 17

.65

40.6

2 39

.07

;11.

-18

56.7

5 20

.7H

7.99

21.9

3 23

.35

60.2

7 56

.32

17.H

I 20

.33

! 4.32

12

.9x

25.7

’ 27

.90

54.8

4 50

.40

19.4

4 21

.70

8.35

7.25

35.4

4 43

.74

20.H

2 3.7

0

30.1

3 47

.54

22.3

2 4.9

3

33.0

8 44

.56

7’) 1

6 ..-

._ 4.50

31.7

8 45

40

22.H

l 3.6

7

Freq

uenc

y Fr

eque

ncy

with

in wi

thtn

vo

lume

volum

e

112 M. LaPlanrc, C.J. M~~s~~arulla,‘Jorrmrrl of Financial Economics 45 (IVY?) 97 I34

are less likely to have price impacts on the NYSE than on the Nasdaq. For example, zerotick Jlock trades are more common on the NYSE for 30,001 to 50,000 share trades (about 54%) than they are for Nasdaq trades (35.30%). Even for the largest block trades on the NYSE, zerotick trades are more likely than either downtick or uptick trades in all seven samples. Chi-square tests reveal that the frequency of block type is statistically different across markets for each volume category in all seven samples. Lastly, uptick and downtick block types are about equally likely for smaller block volumes in both markets. As the size of tl,c* block iTcreases. do\t,ntickF bec.\mc .norc frequent than upticks in both m;rkets.

The raw data in Tables 4 and 5 suggest that there are differences in the nature of block trading between the two markets. The types and sizes of block trades are statistically different. Block trading on the NYSE involves more shares with fewer instances of price changes. To learn more about the impact of block trading on Nasdaq and the NYSE, we conduct statistical tests on the returns for all blocks as well as for the different types of blocks. Results are presented in panel A of Table 6. We measure the return on block trades as the percentage change in stock price from the previous trade to the block trade. Although Porter and Weaver (1995) find evidence that Nasdaq dealers fail to comply with the SEC’s 90-second rule for reporting trades more often than do the specialists of organized exchanges, this finding should introduce no systematic bias to our llMX3SUreS.

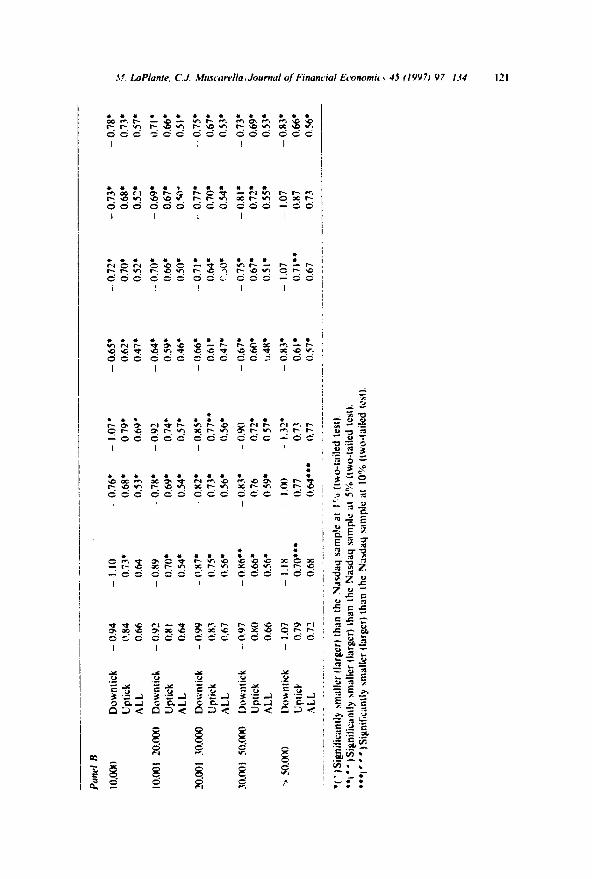

We find that block trades are absorbed with less price movement on the NYSE compared to Nasdaq. Downtick block trades for the Nasdaq firms have a mean return of - 0.55%. Six of the NYSE samples have significantly smaller price impacts, ranging from - 0.39% to - 0.48%. For uptick block trades, the Nasdaq firms have a mean return of 0.53%. All seven NYSE samples have significantly smaller returns.

We calculate the price effect for all types of block trades by averaging the unsigned returns for all trades. This measures the overall impact of block trades on pice movements and reflects the frequency of zerotick blocks. The smaller the absolute return for a firm, the smaller is the overall price movement due to block trading for that firm. Nasdaq blocks have an average absolute price impact of 0.32%. The average absolute price impacts for the seven NYSE samples are all statistically smaller at the 1% level of significance and average 0.18%. The tests for differences in median returns have similar results. In economic terms, this difference results in a potential cost to Nasdaq block traders of approximately $4.7 million per year per firm or a perpetuity value of S1.57 billion for all ten Nasdaq firms using a 3% real discount rate.

To investigate the impact of different block trade sizes, panel B of Table 6 presents mean returns by block type across volume categories. For all but the largest volume category (over 50,000 shares), the NYSE samples have signifi- cantly smaller price movements for both uptick and downtick trades and

M LaPlanre. C.J. Muscarella ‘Joumul of Financid Econonh JS 11997) Y7 I34 113

statistically AmaIler absolute price changes. (Similar results were found for trades of exactly 1520.25, 30, 3540. and 45 thousand shares.)

For blocks of over 50,000 shares, the results are mixed. This could be explained by the fact that the NYSE blocks in this size category are much larger and mote frequent compared to the Nasdaq blocks. For the Nasdaq sample, only about 0.09% of all block trades involve more than 200,tMO shares versus the NYSE samples, which are about eight times as likely to have blocks of this size. Given the absence of very large block trades on Nasdaq, any conclusions from the results of the comparisons of the mean returns of our samples for the largest size category are unwarranted.

One possible explanation for the large incidence of zerotick block trades found on the NYSE can be that blocks are brokenup on the NYSE but not on Nasdaq. To check this possibttity, we eliminate any blcck trade that has a block trade preceding it within I5 seconds. We repeat all calculations and find results that are qualitatively similar to those in Tables 4 through 6.

3.1.2. Block trade price compared to IS-. 30-, and &I-minute prior trade price Another potential explanation fo; the higher frequency of zerotick block

trades on the NYSE is that information leakage regarding a block trade being shopped in the upstairs market could cause stock prices to move before the block trade is executed. Since both markets have access to block brokers, this could happen with Nasdaq stocks, too. We attempt to control for information leakage by repeating our comparisons between the two markets using transac- tion prices prevailing 15 minutes, 30 minutes, and 60 minutes before each block trade as benchmarks. The results are qualitatively similar, we present the results for only the 30-minute interval.

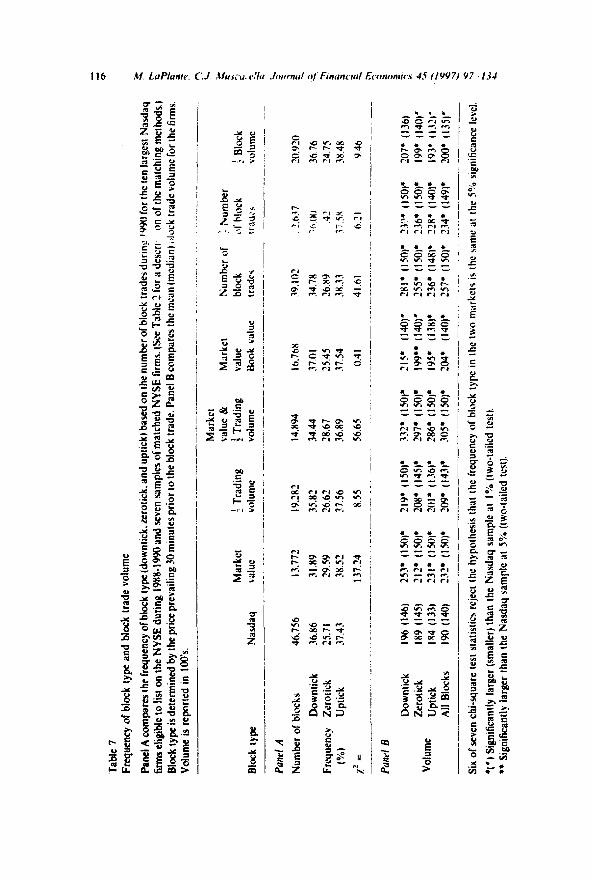

Table 7 shows the revised frequencies of block type by volume category based on the trade occurring at least 30 minutes prior to the block trsde. Blocks that trade during the first 30 minutes of the day are eliminated. Panel A shows that based on prices prevailing 30 minutesearlier, block trades in both markets occur as downticks and upticks more often than as zeroticks (roughly 35%. 38%. and 27%, respectively). Five of the seven NYSE samples continue to have higher frequencies of zeroticks than the Nasdaq firms. Overall, the frequencies ditfer from those based on the prior trade, with the number of zerotick blocks dropping dramatically. This supports the notion that there can be market reaction to an upcoming block trade many minutes before it occurs. Panel B of Table 7 reports mean block trade volumes that are still significantly smaller on Nasdaq for all seven samples and median volumes that are signi;icantly smaller for five of seven matched sampies.

Table 8 reproduces volume frequency distributions according to trade size and block type determined by prices prevailing 30 minutes before the blocks. As found earlier, blocks trade most often as IO,000 shares on Nasdaq and as lO,OOl-20,000 shares on the NYSE. The frequency of blocks over 50,000 shares

Table

6

Retur

ns

acros

s blo

ck

type

and

volum

e ca

tcgori

cs

Pane

l A

show

s me

an

(med

ian)

return

s ac

ross

block

typ

e fo

r blo

ck

trade

s du

ring

1990

for

the

ten

lar

gest

Nasd

aq

firms

cligr

.‘e

to

lrst

on t

he

NYSE

du

rmg

)98$

l99

Oand

se

ven

samp

les

of ma

tched

NY

SE

firms.

(See

Tab

le 2

for

a de

scrip

tion

ofthe

ma

tching

me

thods

.) Pa

nel

B sh

ow

x mea

n ret

urns

for

block

typ

e ac

ross

volum

e ca

tegor

ies.

Retur

ns

are

meas

ured

as

the

per

crnlag

e ch

ange

in

stock

pr

ice

from

the

prev

ious

trade

IO

the

hl&

j, ’

trade

. Th

e AL

L ret

urns

arc

calcu

lated

as

the

av

erag

e of

the

unsig

ned

return

s for

al

l tra

des

and

thus

refle

cts

the f

requ

ency

of

zerot

ick

block

s. Bl

ock

ry)x

s de

term

ined

by

the

pric

e of

the

trade

pr

ior

to the

blo

ck

trade

. __

-___

--_

- ._.

.

_ .-

-.--

..-

Marke

t va

lue

& j

Trad

ing

volum

e Vo

lume

Pmel

.4

Bloc

k typ

e I’a

sdaq

All

volum

es

Down

lick

- 0.5

5 f

- 0.4

5)

Uptic

k 0.5

3 (0

.45)

ALL

0.32

(0.31

)

j Tr

ading

hia

rket

value

vo

lume ..-

- .-.

- 0.4

6, --

n.4u

* -

0.55

( -

0.4-w

I

- 0.4

2)’

( -

0.48)

’

0.46.

0.43

4 0.4

9+

IO.JZ

)* (O

N)*

(0.46

)’

OIlI*

0.1

8. 0.

21*

fO.O

O)*

(0.00

)’ (o

.oo)*

Marke

t va

lue

Numb

er

of j

Numb

er

d j

Bloc

k Bo

ok

value

blo

ck

trade

s blo

ck

trade

s vo

lume

- 0.3

9. f

- 0.3

5).

0.37

9 (0

.36)*

0.16.

(0.00

)’

- 0.4

5. (

-- 0.

34p

0.40

’ (O

N)*

0.16.

(o.oo

)*

- 0.

47’

( -

0.40)

.

0.43.

wol*

0.18.

(0.O

f.V

- 0.

39’

f -

0.35)

.

0.39.

(0.36

)’

O.l6*

fo.

oo)*

I I I ,

‘Tab

le 7

Freq

uenc

y of

block

typ

e an

d blo

ck

trade

vo

lume

Pane

l A

comp

ares

the

frqu

ency

of

block

typ

e (d

ownti

ck.

zerot

ick.

and

uptic

k) ba

sed

on t

he n

umhe

r of

block

tra

des

durtn

g !Y

Ytl

for

the t

en l

arge

st Na

sdaq

firms

e\&M

e to

list

on

the

NYSE

du

ring

1988

-199

0 an

d se

ven

samp

les

of ma

tched

NY

SE

firms.

(See

Tab

le ?

for

a de

scrl

on o

f the

matc

hing

metho

ds.)

Bloc

k typ

e is

dete

rmine

d by

the

pric

e pr

evail

ing

30 m

inutes

pr

ior

to the

blo

ck

trade

. Pa

nel

B co

mpar

es

the m

ean

(med

ian)

,jlock

tra

de

volum

e for

the

firm

s. Vo

lume-

is re

porte

d in

100’s

. -~-

- -

..--

..-

Bloc

k typ

e Na

sdaq

Ma

rket

i Tr

ading

va

lue

volum

e

---._-

----

------

.-

.-.

.-_-

-._

.--.

_-__

_.

Marke

t va

lue

& Ma

rket

Numb

er

of 1

&umb

er

i Tr

ading

va

lue

block

d-

block

;

Bloc

k vo

lume

Book

va

lue

trade

s 1r

ad2c

vo

lume

-_-_

--- .._

_ --.

._ -..-

--

--...-.

-

-.---

.__-_

..-

. ._.

.. _._

Pane

l A

Numb

er

of blo

cks

46.7

56

13.7

7’ 19

,282

Down

tick

36.8

6 31

.89

35.8

2 Fr

eque

ncy

Zerot

ick

25.7

1 ?9

.5Y

26.6

2 (%

I Up

tick

37.4

3 3x

.52

31.5

6

%?

= 13

7.24

x.5

5 __

__._

____

_..

__.

..-

.._...

--.

----

-....

. .--

----

--

Pant

1 B

14.H

94

16.7

68

19.

IO?

2.6.17

20

.9 2

0

34.4

4 37

.01

34.7

8 :h

M

I 36

.76

28.6

7 25

.45

26.8

9 .42

‘4.

75

36.8

9 37

.54

38.3

3 37

.5x

38.4

8

56.6

5 0.4

I 41

.61

6.21

Y.46

Down

tick

196

(146

) 25

3. (1

50)*

219.

(150

). 33

2. ( I

SO)

* 21

5, (1

40)’

181’

(150

). 23

”. (1

50)’

207'

(136

)

Volum

e Ze

rotick

I89

(I4

51

212’

(150

1’ 20

8. (1

45).

297.

(ISO)

* 1Y

9**

1140

) ‘55

. (IS

O)*

236.

(150

)’ 19

9’ (1

40)’

Uptic

k 14

4 (1

33)

2310

(1

501.

201

l ( 1

361’

X6*

(150

). 19

5. (13

x)*

236,

(I48)

* 22

U*

(l40)

* 19

3' (IL

?) Al

l Blo

cks

I90

(140

) 23

.2,

(150

)* x9

* (1

43).

305.

(150

)2

ml*

(140

). 25

7*

(Isol*

2.3

4, (1

49).

2cw

((35)'

__

_-

_.

.--.-.

___

----

--

.----_

--

----

.--

-.._.

..-

. _

Six

of se

ven

cm-sq

uare

test

statis

tics

rejec

t the

hy

pothe

sis

that

the

irequ

ency

of

block

typ

e in

the

two

marke

ts is

the

same

at

the

5%

signit

icanc

e lev

d.

*(*)

Sign

ifican

tly

large

r (sm

aller

) tha

n the

Na

sdaq

sa

mple

at I%

(tw

o-tai

led

test).

l *

Sign

ifican

tly

large

r tha

n the

Na

sdaq

sa

mple

at 5%

(tw

o-tai

led

test).

Table

8

Volum

e fre

quen

cy

distri

butio

ns

in pe

rcent

for

block

tra

des

durin

g 19

90 f

or

the t

en

large

st NJ

sdaq

lir

mseli

gible

IO l

ist o

n the

NY

SE

durin

g 19

88.

19W

and

seve

n sa

mples

of

match

ed

NYSE

firm

s (se

e Ta

ble

2 for

a

desc

riptio

n of

the m

atchin

g me

thods

): blo

ck

rype

is de

term

ined

by

the p

rice

prev

ailing

30

minu

tes

prior

to

the

block

tra

de

--

_ .__

._ .-

_-

.__.

- ._

__.-.

__

_-._

----

---

..___

-

.-----

_-

---__

-_-._

_---

Marke

t va

lue

] Tr

ading

&

i Tr

ading

Ma

rket

value

Nu

mber

of

i Nu

mber

of

f Bl

ock

Ndilq

Ma

rket

value

vo

lume

volum

e ,B

ook

value

blo

ck

trade

s blo

ck

trade

.

volum

e ---

-..-.-_

__

.._.

-.- __

.. -_

- .-

. ._

- _-.

-.. _..

._ _

- ._-

_- __

__~

-. __

---

--___

_-.

- ._^

.

Freq

uenc

y Fr

eque

ncy

Freq

uenc

y Fr

eque

ncy

Frcq

ucnc

y Fr

eque

ncy

Trcq

uenc

y Fr

eque

ncy

with

in wi

thin

with

in wi

thin

with

in wi

thin

with

in wi

thin

Volum

e Bl

ock

type

volun

~c

volum

e vo

lume

volum

e vo

lume

vohr

-..c

volum

e vo

lume

-..--

. . .

..-

_ .

.-.---

.---.

. . . .

.----.

...-

.----.

. --

----

-.-

--...-

----.-

-._..

-. 10

.000

Do

wmick

36

.25

30.9

7 33

.33

35.0

7 35

.YY

33.5

2 34

.34

35.9

5 Zc

rotick

25

.27

28.2

3 26

.33

25.2

5 25

.0:

26.5’

) 25

.48

23.7

6 Up

tick

384W

40

.80

40.3

4 39

.68

3KY6

39

.YO

40.1

7 40

.2Y

ALL

41 8

3 31

.18

32.9

5 29

.XH

33.4

9 33

.22

31.4

3 36

.17

10.0

01

20.0

00

Down

tick

Zcrol

ick

Upnc

k AL

L

20.0

01

30.0

00

Dowm

ick

Zerot

ick

Uptic

k AL

L

36.2

0 3l.

Yl

36.8

6 3’.

9l 37

.32

35.1

7 36

.32

37.3

6 26

05

31.2

6 26

.46

30.6

2 25

.81

27.2

4 27

.01

25.2

5 37

.75

36.8

3 36

.7s

35.4

7 36

.87

37.6

0 36

.67

37.3

9 31

.01

40.4

4 JiM

S 38

59

41.0

4 3Y

.32

40.9

2 33

.55

37.0

5 30

.22

35.2

6 32

.25

26.3

7 70

.12

27.9

’ 31

.00

36.5

8 39

.66

fhK

36.7

5 17

SR

I4.7H

14

.27

I6 t-4

34.9

I 26

.31

38.7

8 I.1

87

33.9

1 35

.73

35.1

1 X1

& 26

.07

25.2

6 39

.38

38.2

0 39

64

14.2

1 14

.49

13.1

0

3O.O

OI

5O.W

O Do

wntic

k 1

I .03

34.6

1 JO

.13

33.4

8 3Y

.7Y

35.6

0 37

.84

3u.2

3 Zz

C.bic

k 25

.53

26.3

6 25

.h?

28.9

2 25

.17

28.2

4 27

81

25.5

3 lip

tick

33.4

4 3Y

.03

14.2

5 37

.59

35.0

4 36

.16

34.3

4 36

.23

ALL

6.Y5

87

I

8.12

li.YX

7.

Y I

X.13

85

9 7.4

1

2 50

.01w)

Do

wntic

k 42

.37

37.7

8 38

7Y

40.Y

5 44

.66

4 1.07

41

.93

41.2

4 Ze

rotick

24

.49

28.5

0 27

.96

26.9

5 22

.4Y

26.1

0 26

.09

25.7

6 Up

tick

33.1

4 33

.63

23.2

5 32

.10

32.8

5 32

x3

31.9x

32

.99

ALL

2.52

4.90

4.21.

6.‘)0

3.6

9 5.1

3 4.5

7 3.

7i

: 8 Y F 2 4 5 ..-

-.---_

..^

.__

-.-._

-_--.

-_._

_

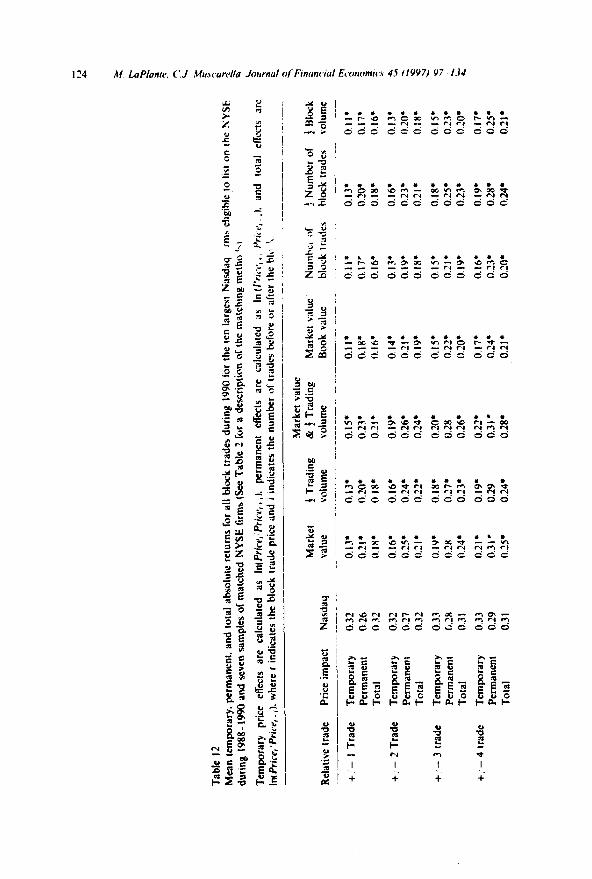

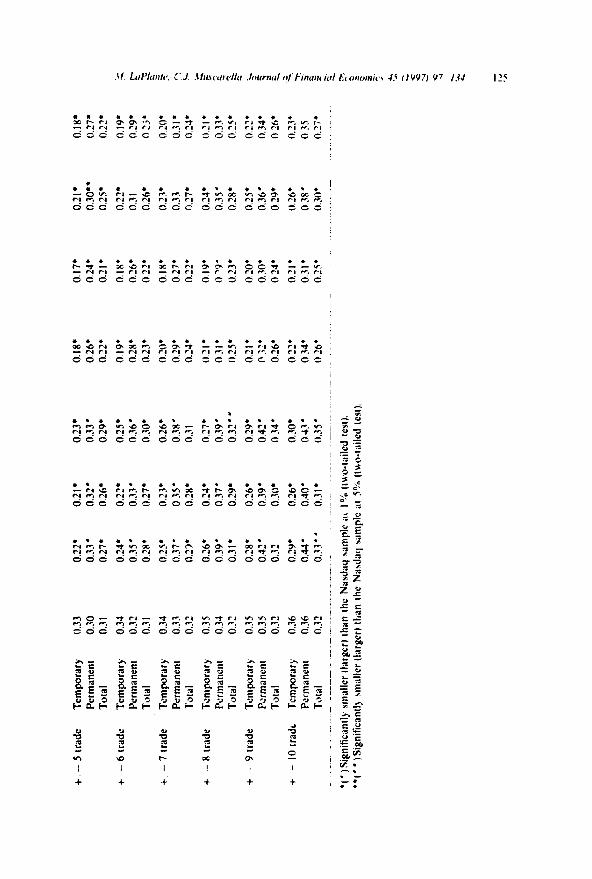

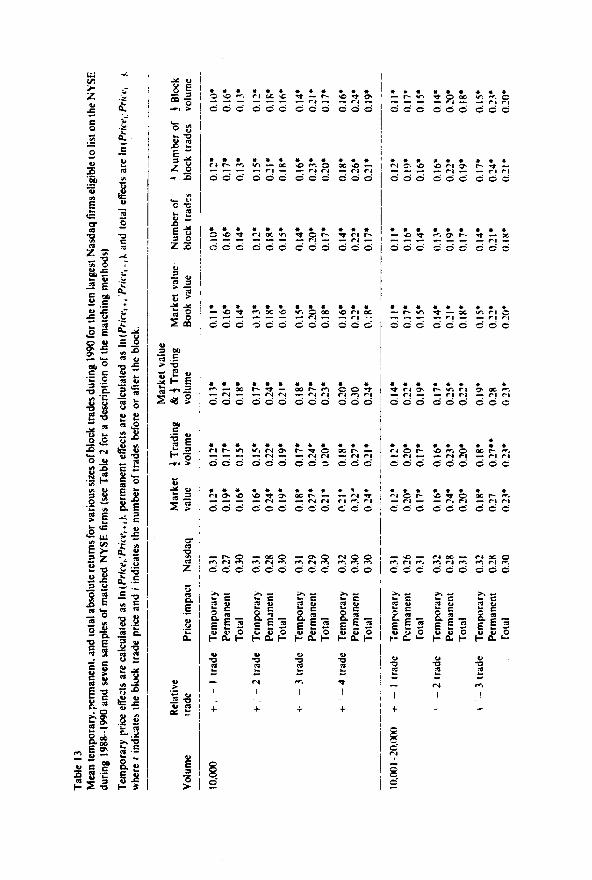

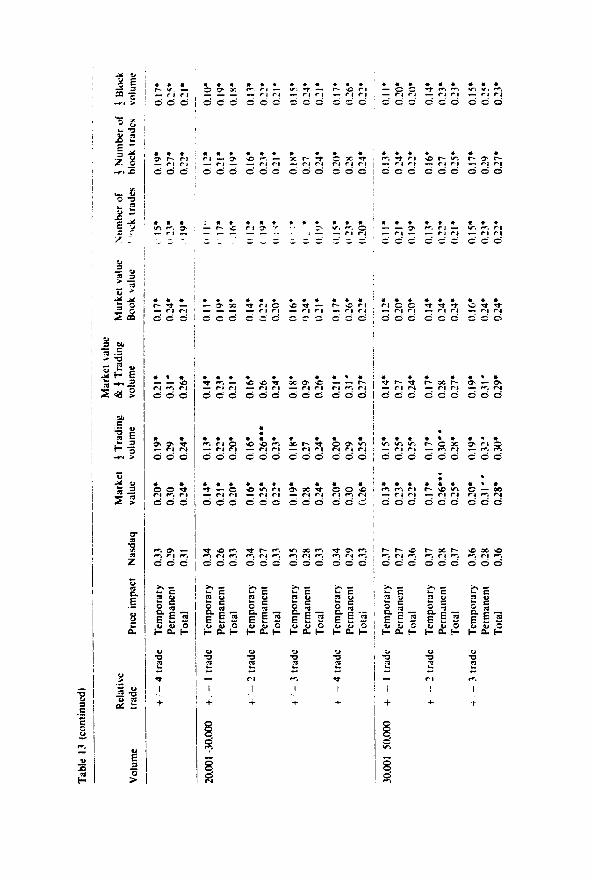

increases slightly in the NYSE samples compared to Table 5. suggesting that very large blocks on the NYSE occur less frequently in the first half-hour of trading. Again. the frequency of zeroticks in the largest size category is higher for the NYSE samples than for the Nasdaq firms.

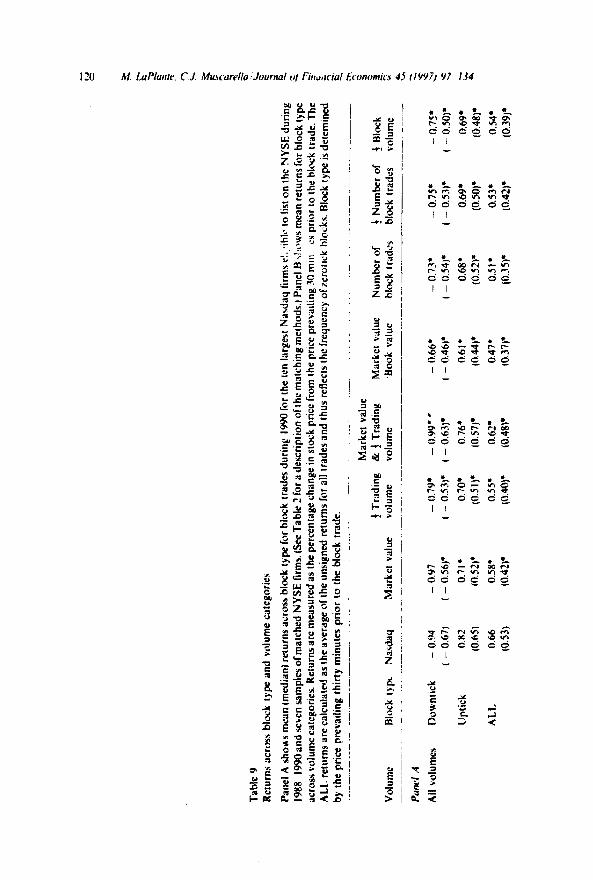

Table 9 presents returns based on the percentage change in stock price from the price prevailing 30 minutes prior to the block trade for the different block types and volume categories. While returns are always larger than the corres- ponding returns in Table 6, the results are consistent with Table 6. Panel A shows that all seven NYSE samples h:bvc : ‘-niticantly smaller block trade +ce ‘rt)ir<*k ‘*orl:i,;:rLd t<) :..&a, ,.OLJ~~Y 0.54 ‘XI versus 0.66%. respectively). Panel B shows return patterns across block types by volume categories that are similar to panel B of Table 6. While there is evidence in both markets of price movements occurring many minutes before a block trade, the NYSE still absorbs block trades with less price movement than Nasdaq.

3.1.3. Expanded sample This study compares levels of liquidity offered to large firms in the

Nasdaq market and the NYSE by focusing on block trade execution for the ten largest and most actively traded firms on Nasdaq. We do not attempt to draw conclusions regarding the general liquidity in the Nasdaq market versus the NYSE. However, as a check on our restricted sample size, we now expand the sample to include all Nasdaq firms that qualified to list during 1988- 1990 and use a sample of NYSE firms matched on market value as a comparison. The original sample contained 167 firms. We drop I8 with prices less than $10 and six more because of data discrepancies. The final sample contains 143 firms which are matched to NYSE firms by closest 1990 year-end market values. Table locontains the results of the comparisons. Panel A shows that the average number of block trades is similar (658 for the Nasdaq sample and 748 for NYSE), but again the mean number of shares traded in a block is smaller for the Nasdaq firms (18,700 shares versus 22.800 shares). It is interesting to note that the pattern of block type frequency is very similar to those found in the smaller sample. For example, the incidence of zeroticks is still higher on the NYSE. 58.52% versus 37.52%. Panel B shows the mean absolute price impacts based on the previous trade and the prices prevailing 15. 30, and 60 minutes earlier. Again, the results with the expanded sample are consistent with the smaller sample in that the price impacts of NYSE blocks are significantly smaller across all size categories for all benchmarks. We conclude that Nasdaq firms eligible to list on the NYSE could have smaller block price impacts if their shares were traded on the NYSE.

3.1.4. Regression analysis To further check our findings we use an alternative methodology and conduct

a pooled regression analysis for the ten Nasdaq firms and seven matched

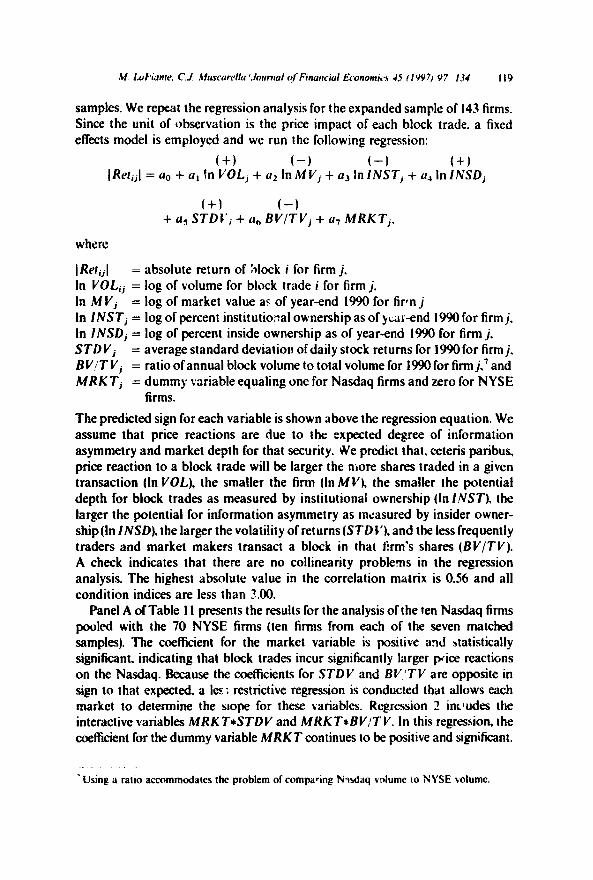

samples. We repeat the regression analysis for the expanded sample of 143 firms. Since the unit of observation is the price impact of each block trade. a fixed effects model is employed and we run the following regression:

(+I l-1 (-1 (+I IRetijl = 00 + ~1 In VOLj + ~2 In MI’, + ~73 In 1NSTj + u4 In INSDj

(+I f-1 + ~5 STDk’i + Uh BV/TVj + UT MRKTj.

where

IRefijI = absolute return of %ck i for firm j. In VOLij = log of volume for block trade i for firm j. In MVj = log of market value as of year-end 1990 for firIn j In 1NSTj = log of percent institutional ownership as of yc,u-end 1990 for firm j. In 1NSDj = log of percent inside ownership as of year-end 1990 for firm j. STDVj = average standard deviation of daiiy stock returns for 1990 for firm j, BV!T Vj = ratio of annual block volume to total volume for 1990 for firm j,’ and MRK Tj = dummy variable equaling one for Nasdaq firms and zero for NYSE

fiflllS.

The predicted sign for each variable is shown above the regression equation. We assume that price reactions are due to the expected degree of information asymmetry and market depth for that security. we predict that, ceteris paribus, price reaction to a block trade will be larger the more shares traded in a given transaction (In VOL), the smaller the firm (In MI’), the smaller the potential depth for block trades as measured by institutional ownership (In INST), the larger the potential for information asymmetry as measured by insider owner- ship(In INSD), the larger the volatility of retums(STDC’), and the less frequently traders and market makers transact a block in that f!rm’s shares (BY/TV). A check indicates that there are no collinearity problems in the regression analysis. The highest absolute value in the correlation matrix is 0.56 and all condition indices are less than ?.oO.

Panel A of Table I I presents the results for the analysis of the ten Nasdaq firms pooled with the 70 NYSE firms (ten firms from each of the seven matched samples). The coefficient for the market variable is positive and statistically significant. indicating that block trades incur significantly larger p&e reactions on the Nasdaq. Because the coefficients for STDV and BV,‘TV are opposite in sign to that expected a ler; restrictive regression is conducted that allows each market to determine the slope for these variables. Regression 2 includes the interactive variables MRKT+STDV and MRKT*BVITV. In this regression, the coefficient for the dummy variable MRKT continues to be positive and significant.

- Using a ratio accommodates rhe problem of comparing Ndaq vnlume io NYSE volume.

A?. LoPkme. C.J. Mu.wcwc&~ I Journd ol’Financiu/ Ecwnomk * 45 II VV71 V7 124 121