Filing of Income Tax Returns & Advance payment of Tax DAY 3 SESSION 1 & II slide 3.1.

21

Filing of Income Tax Returns & Advance payment of Tax DAY 3 SESSION 1 & II slide 3.1

-

Upload

virginia-monica-riley -

Category

Documents

-

view

222 -

download

3

Transcript of Filing of Income Tax Returns & Advance payment of Tax DAY 3 SESSION 1 & II slide 3.1.

Filing of Income Tax Returns&

Advance payment of Tax

DAY 3

SESSION 1 & II

slide 3.1

INTRODUCTION Persons liable to furnish returns of income Section 139(1) requires every person to furnish return – if his total income or - the total income of any other person in respect of

which he is assessable under the Act during the previous year, exceeds the maximum amount

which is not chargeable to income-tax.

slide 3.1

INTRODUCTION Ignorance of statutory duty provides no excuse

to an assessee who is liable to make return under section 139(1) (Kumar Purnendu Nath Tagore v ITO, (1973)]

slide 3.1

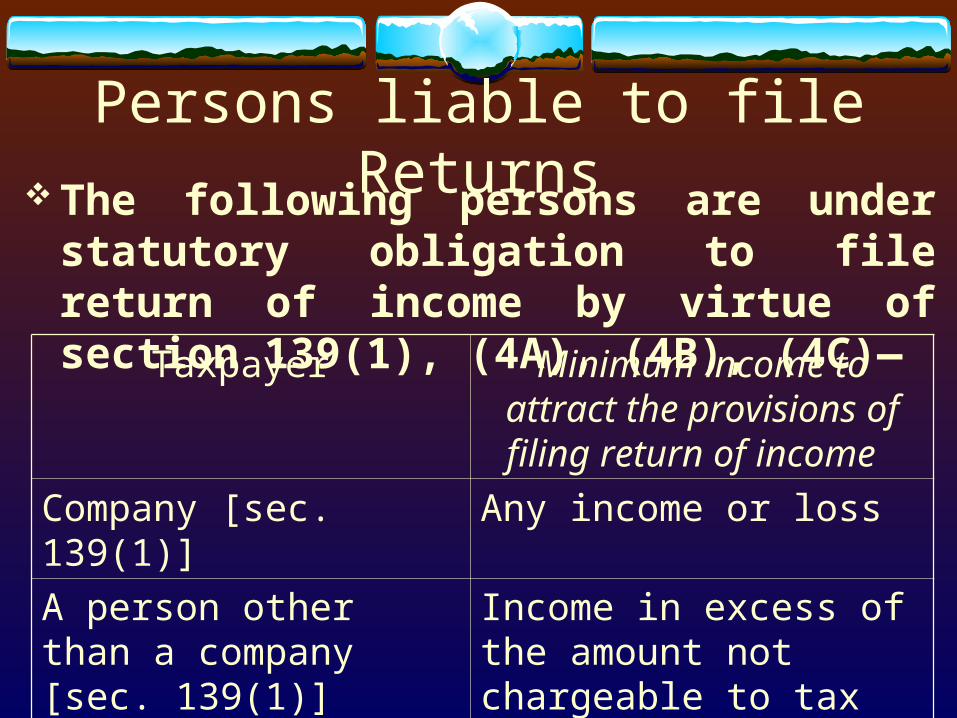

Persons liable to file Returns The following persons are under statutory

obligation to file return of income by virtue of section 139(1), (4A), (4B), (4C)—

Taxpayer Minimum income to attract the provisions of

filing return of income

Company [sec. 139(1)] Any income or loss

A person other than a company [sec. 139(1)]

Income in excess of the amount not chargeable to tax (i.e., the amount of exempted slab) slide 3.1

Persons liable to file Returns

A person in receipt of income derived from property held under a trust for charitable or religious purposes [sec. 139(4A)]

If the income (without giving exemption under section 11 or 12) exceeds the maximum amount† not chargeable to tax

Chief executive officer of every political party [sec. 139(4B)]

Income (without giving exemption under section 13A) exceeds the maximum amount † not chargeable to tax slide 3.1

Persons liable to file Returns

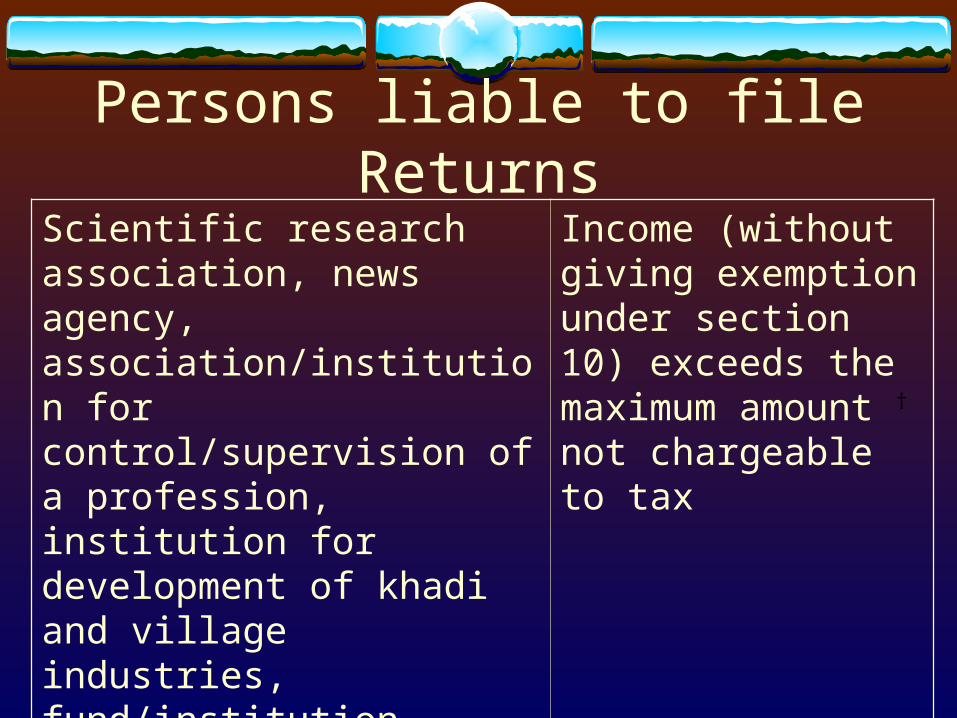

Scientific research association, news agency, association/institution for control/supervision of a profession, institution for development of khadi and village industries, fund/institution referred to in section 10(23C)(iv), (v), educational/medical institution, trade union [sec. 139(4C)]

Income (without giving exemption under section 10) exceeds the maximum amount † not chargeable to tax

slide 3.1

Obligatory filing of return when income is lower than exemption limit

first proviso to section 139(1) A person (other than a company, political party or

charitable trust) [not furnishing return under section 139(1), i.e., when income is less than the exemption limit] and residing in a specified area shall submit his return of income in Form 2C if he fulfils any one of the following conditions at any time during the previous year —

a. ownership/lease of a motor vehicle ; b. occupation of any category or categories of

immovable property as may be specified by the Board by notification whether by way of ownership or tenancy or otherwise ; or

slide 3.1

Obligatory filing of return when income is lower than exemption limit

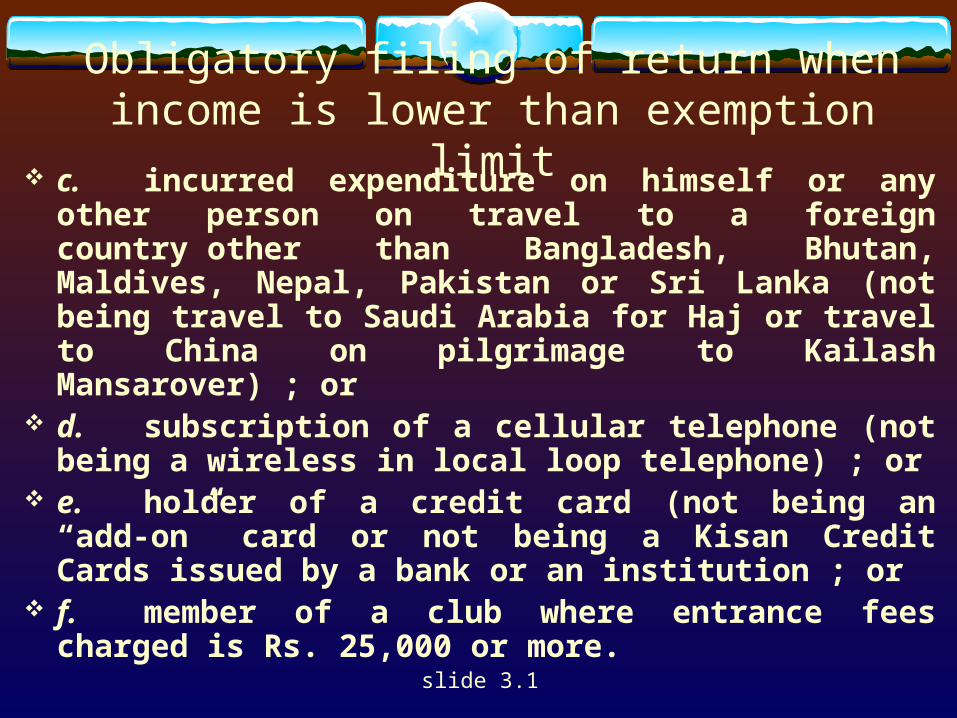

c. incurred expenditure on himself or any other person on travel to a foreign country other than Bangladesh, Bhutan, Maldives, Nepal, Pakistan or Sri Lanka (not being travel to Saudi Arabia for Haj or travel to China on pilgrimage to Kailash Mansarover) ; or

d. subscription of a cellular telephone (not being a wireless in local loop telephone) ; or

e. holder of a credit card (not being an “add-on” card or not being a Kisan Credit Cards issued by a bank or an institution ; or

f. member of a club where entrance fees charged is Rs. 25,000 or more.

slide 3.1

Obligatory filing of return when income is lower than exemption limit

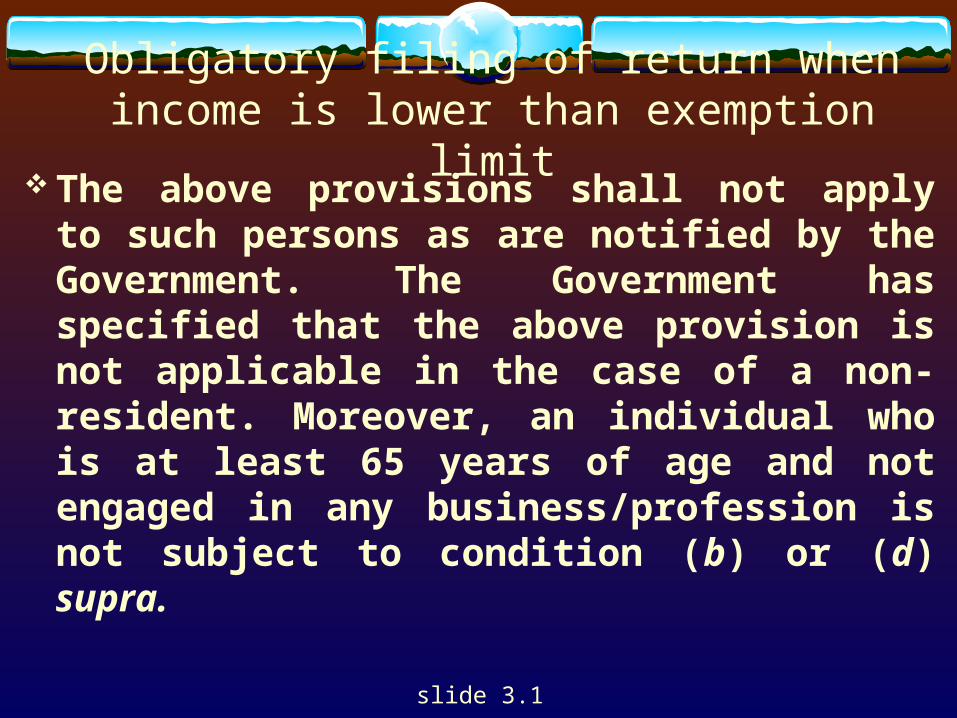

The above provisions shall not apply to such persons as are notified by the Government. The Government has specified that the above provision is not applicable in the case of a non-resident. Moreover, an individual who is at least 65 years of age and not engaged in any business/profession is not subject to condition (b) or (d) supra.

slide 3.1

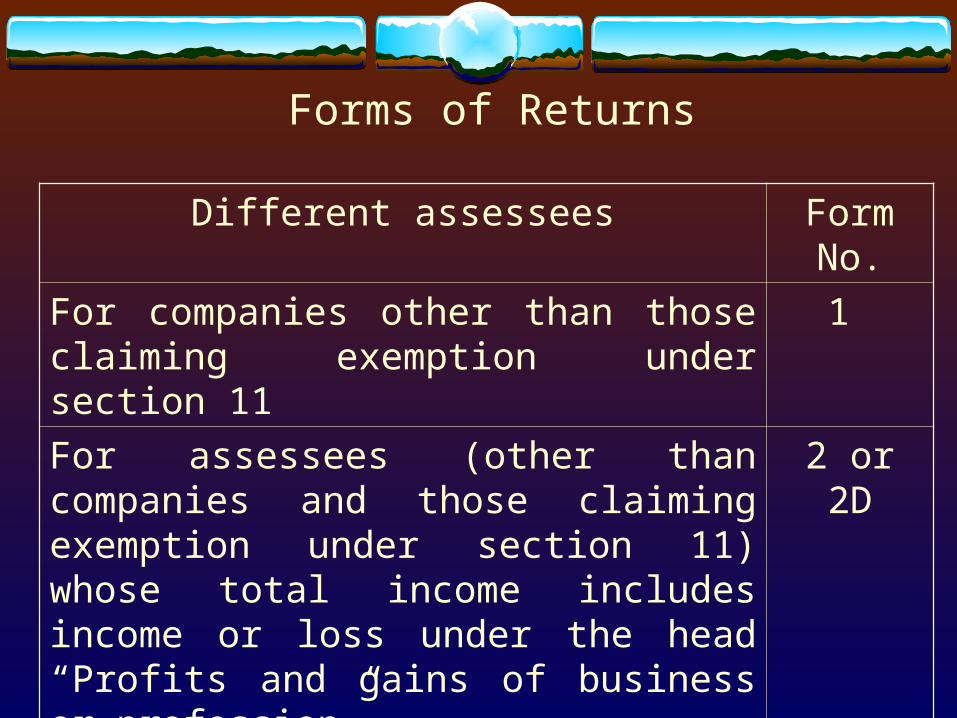

Forms of Returns

Different assessees Form No.

For companies other than those claiming exemption under section 11

1

For assessees (other than companies and those claiming exemption under section 11) whose total income includes income or loss under the head “Profits and gains of business or profession”.

2 or 2D

For a person who is required to file a return under proviso to section 139(1)

2C

Forms of ReturnsDifferent assessees Form No.

For assessees (other than companies and those deriving income

2D or 3

from property held for charitable or religious purposes claiming exemption under section 11) whose total income does not include income or loss under the head “Profits and gains of business or profession”.

For assessees (being resident individuals or HUFs) not having any income/loss from business or profession, or capital gains/loss or agriculture income

2D or 2E or 3

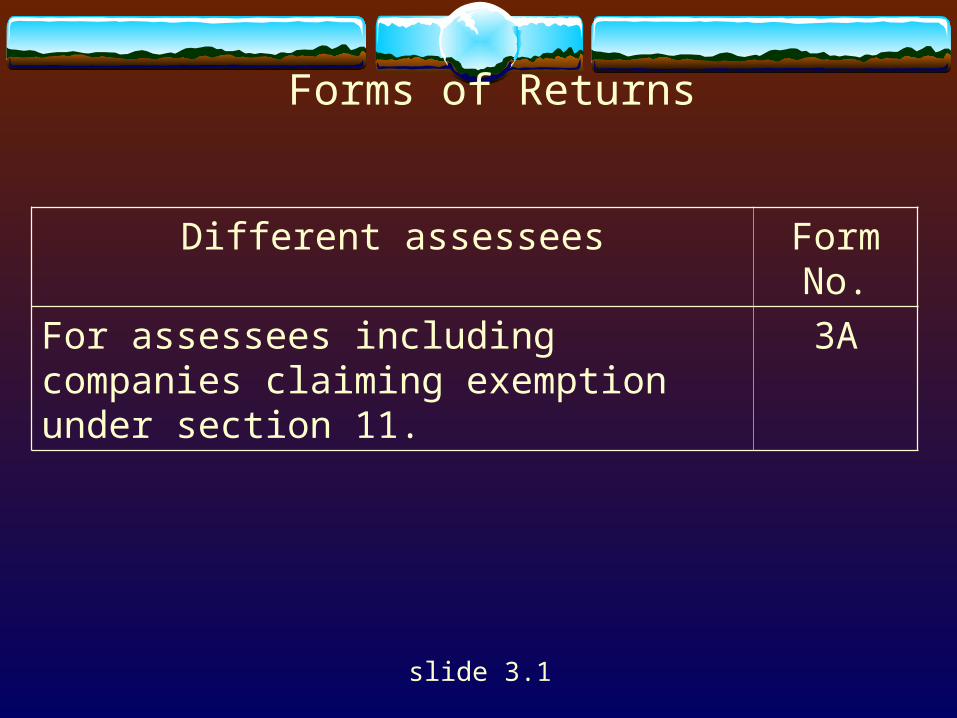

Forms of Returns

slide 3.1

Different assessees Form No.

For assessees including companies claiming exemption under section 11.

3A

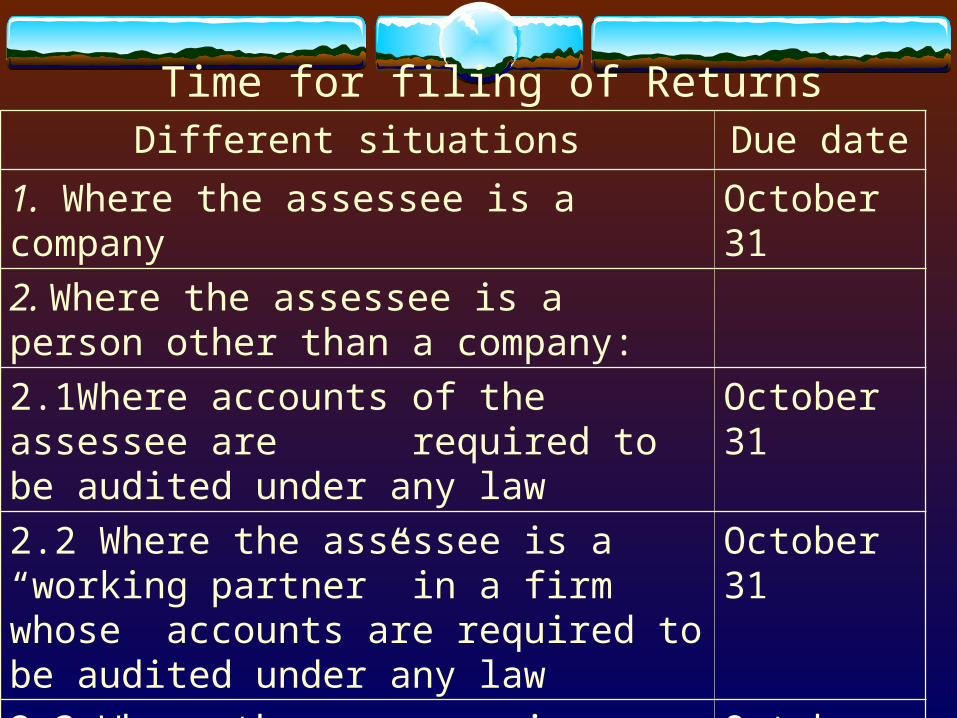

Time for filing of ReturnsDifferent situations Due date

1. Where the assessee is a company October 31

2. Where the assessee is a person other than a company:

2.1Where accounts of the assessee are required to be audited under any law

October 31

2.2 Where the assessee is a “working partner” in a firm whose accounts are required to be audited under any law

October 31

2.3 Where the assessee is covered by the first proviso to section 139(1)

October 31

2.4 In any other case July 31

Action when return of income is not filed

Section 142(1) of the Income Tax Act, 1961, provides for issuance of notice to the assessee for filing of return if the same has not been submitted earlier.

Non-filing of returns can be of two forms: -

1. Non-filing in cases where returns were being filed in the past i.e. stop filers

2. Cases where returns are not filed at all

slide 3.1

Action when return of income is not filed

Cases falling in the first category can be detected from the Blue Book maintained with the assessing officer. In all cases where a return of the assessee is received for the first time as well as cases of transfer of jurisdiction, the name of the assessee concerned is to be entered in the Blue Book maintained by each assessing officer. This register also keeps a track of returns filed every year by the assessee

slide 3.1

Action when return of income is not filed

Cases falling under the second category could be detected by a process of integration of records held with various statutory bodies such as the Central Information Branch of the income tax department, TDS wards, Registering authorities, and banks. Quoting of PAN has now been made compulsory in the case of most of the transactions entered into by all persons

slide 3.1

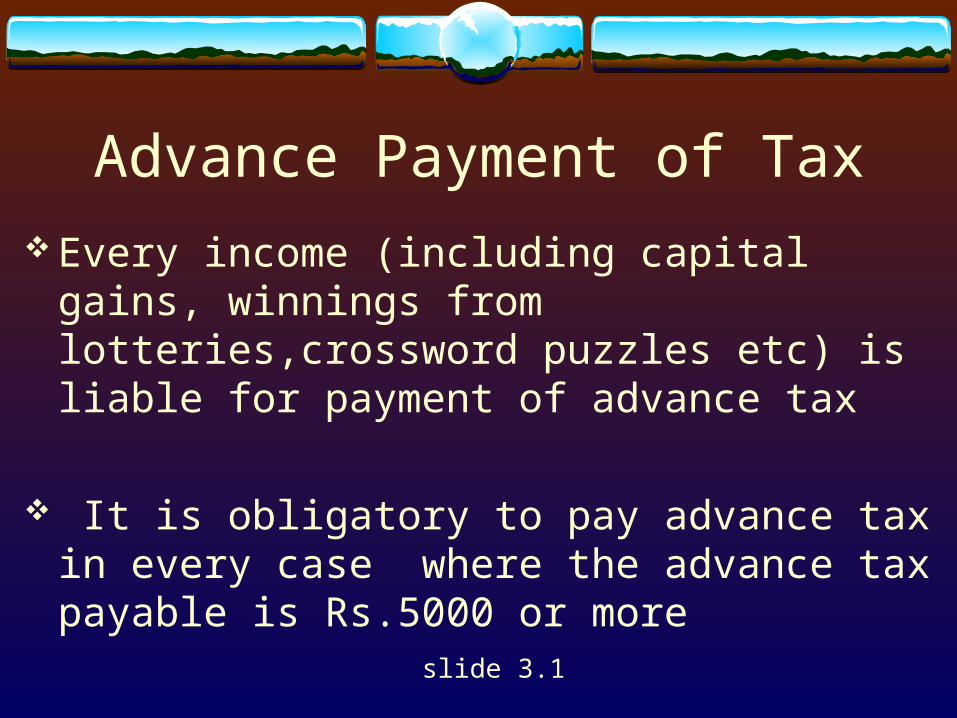

Advance Payment of Tax

Every income (including capital gains, winnings from lotteries,crossword puzzles etc) is liable for payment of advance tax

It is obligatory to pay advance tax in every case where the advance tax payable is Rs.5000 or more

slide 3.1

Due dates of payment of Advance Tax

Corporate assessee Non corporate assessee

On or before June 15 of P.Y.

On or before Sept.

15 of P.Y.

On or before Dec.

15 of P.Y

On or before Mar.

15 of P.Y.

Up to 15% of adv. tax payable

Up to 45% of adv.tax payable

Up to 75% of adv.

Tax payable

Up to 100% of adv. Tax payable

slide 3.1

Up to 30% of adv. Tax payable

Up to 60% of adv.

Tax payable

Up to 100% of adv. Tax payable

Advance Tax liability under different situations

Payment of advance tax by the assessee of his own account (Section 210)

Payment of advance tax in pursuance of order of assessing officer (Section 210)

Payment of advance tax in pursuance of revised order of assessing officer

slide 3.1

Interest payable by the assessee For defaults in furnishing return of income (Sec.234A) For failure to deduct and pay tax at source(Sec.201(1A)) For default in payment of advance tax (Sec.234B) For deferment of advance tax (Sec.234C) Interest on excess refund (Sec.234 D w.e.f.June 1 2003)

slide 3.1

Cont… For making late payment of Income Tax

(Sec.220(2)) Interest payable to assessee Interest payable where any refund arises due to

any excess payment of tax (Sec.244A) Procedure to be followed in calculation of interest

(Rule 119A)slide 3.1