Fiduciary Responsibility Refresher - IFEBP...The opinions expressed in this presentation are those...

159

The opinions expressed in this presentation are those of the speaker. The International Foundation disclaims responsibility for views expressed and statements made by the program speakers. Fiduciary Responsibility Refresher Katherine A. Hesse, CEBS Partner Murphy, Hesse, Toomey & Lehane, LLP Boston, Massachusetts © 2016 Murphy, Hesse, Toomey & Lehane LLP. All Rights Reserved. F08-1

Transcript of Fiduciary Responsibility Refresher - IFEBP...The opinions expressed in this presentation are those...

The opinions expressed in this presentation are those of the speaker. The International Foundationdisclaims responsibility for views expressed and statements made by the program speakers.

Fiduciary ResponsibilityRefresher

Katherine A. Hesse, CEBSPartnerMurphy, Hesse, Toomey & Lehane, LLPBoston, Massachusetts

© 2016 Murphy, Hesse, Toomey & Lehane LLP. All Rights Reserved.

F08-1

Purpose of Today’s Session

• To give you some basic tools to allow you to be prudent fiduciaries of your pension and health funds.

• To ensure you understand the legal framework within which you operate. See how key cases illustrate this.

• To refresh your knowledge of best practices for trustees and administrators in providing benefits to covered employees.

• To leave you with a checklist of key takeaways.

F08-2

Overview

• Part 1—Maintaining Tax-exempt Status • Part 2—Key Documents Every Trust Should

Have • Part 3—What It Means to Be a Fiduciary

– The New DOL Fiduciary Rules

• Part 4—Selecting and Monitoring Providers• Part 5—Guiding Principles

– Spotlight: Communications and Disclosure

• Part 6—Key Takeaways

F08-3

Part 1. Tax-Advantaged Status

• We will be focusing mostly on the “fiduciary” standards the DOL enforces (Part VI).

• However, first, it is important to remember that all plans, even governmental plans, are also subject to certain IRS rules.

F08-4

Plan Qualification

• The requirements for tax-advantaged status vary according to the type of plan.

• Some of these requirements include: – Written document– Exclusive benefit rule– Minimum vesting and participation requirements– Non-assignment or alienation– Communication of plan– Nondiscrimination requirements

F08-5

Taking Care of Your Trust

• Trustees should establish practices and procedures to ensure the plan is operated in accordance with the plan document so participants and beneficiaries receive their proper benefits.– As you will see, this is also a fiduciary

requirement.• Be aware that the law and regulations in this

area frequently changes, especially post-ACA or MPRA.

F08-6

Plan Amendments

• The terms of the plan may be amended.• Be very wary of eliminating or cutting back

benefits retroactively. • Even where not required by law, best practice

is to provide sufficient advance notice of the change under the circumstances.

F08-7

Part 2. Key Plan Documents

• Trust Document• Plan• IRS letter• Collective bargaining agreement(s)• Annual Audited Financial Statements• Policies of Insurance

F08-8

Part 2. Key Plan Documents (continued)

• Summary plan description/certificates of insurance/wrap around document

• Policies and Procedures• Minutes of meetings• Written contracts with all vendors• Tip: Make sure to keep copies in the fund

office of all of these documents. Some of them will need to be kept at other locations as well.

F08-9

Key Plan Documents—The Trust

• What are some key provisions it should cover?– Sets forth the plan sponsors

– States the purpose of the trust

– Defines terms

– Provides for the composition of the Board of Trustees and how Trustees are appointed and removed

– Sets forth the duties and powers of the Trustees (general, investment, collection, audit, hiring staff, leasing space, etc.)

– Determines how and when meetings can be called and the voting process

– Provides the Trustees with discretion to interpret the plan and resolve ambiguities

– Governs how the Trustees will vote , including a provision for arbitration

– Determines how amendments to the Trust may be made and how the Trust may be terminated.

F08-10

Other Key Plan Documents

• The Plan– Provides what the plan of benefits is– Sets forth eligibility rules, waiting periods, etc. – Provides procedure for participants to apply for

benefits– Sets out appeal process for those denied benefits

• IRS letter• Collective bargaining agreement(s)

– Provides for the establishment of a trust and its purpose

– Determines the contribution requirement

F08-11

Key Plan Documents

• Annual Audited Financial Statements• Policies of Insurance• Summary plan description/certificates of

insurance• Minutes of meetings• Written contracts with all vendors

F08-12

Key Plan Documents—Policies

• Policies and Procedures– Collection– Investment – Trustee Education and Expenses– Code of Conduct/Ethics– HIPAA/ Privacy Protections/Security– Employee Handbook– Harassment/Non-Discrimination– Social Media/Electronic Communication/Use of I.T.

F08-13

Part 3. Fiduciary Standards

• Who is a fiduciary?• What is the standard of care for fiduciaries?• What are the penalties for breaching your

fiduciary duties?• Can you delegate fiduciary duties and how? • When might one fiduciary be liable for the

breach by another?

F08-14

Who is a Fiduciary?

• ERISA requires that plans name one or more fiduciaries in their written documents.

• Named fiduciaries are generally the plan administrator and plan trustees.

• Others may be functional fiduciaries to the plan if their function or conduct falls within the definition of fiduciary.

F08-15

Definition of a Fiduciary, ERISA, Section 3(21)A

“ . . . a person is a fiduciary with respect to a plan to the extent (i) he exercises any discretionary authority or discretionary control respecting management of such plan or exercises any authority or control respecting management or disposition of its assets;

F08-16

Definition of a Fiduciary, ERISA, Section 3(21)A (Continued)

(ii) he renders investment advice for a fee or other compensation, direct or indirect, with respect to any moneys or other property of such plan, or has any authority or responsibility to do so,

or

F08-17

(iii) he has any discretionary authority or discretionary responsibility in the administration of such plan.”

Definition of a Fiduciary, ERISA, Section 3(21)A (Continued)

F08-18

Two Hats

• Fiduciaries may wear two hats, e.g., may be employer or union representatives.

• When acting as Trustees, you must act for the exclusive benefit of plan participants, not in your own interest or in the interest of your employer or your union.

F08-19

McCaffree Financial Corp. v. Principal Life Ins. Co., 2016 WL 98332,—F.3d—(8th Cir. Jan. 8, 2016).

• Eighth Circuit held that financial advisor for employee retirement benefit plan could not be liable for breach of fiduciary duties for excessive investment management fees because fee structure that was alleged to be excessive was agreed to in contract between financial advisor and plan sponsor.– An outside party is not a fiduciary of a plan simply by

negotiating terms for providing services to that plan– After entering into the agreement, the advisor could

be a fiduciary

F08-20

• In this case, the allegation was based on the advisor charging an “account” fee on top of mutual fund fees that it also charged.– Because the plan sponsor agreed to this layering of

fees, and the layering was the sole basis for the claim, the financial advisor was not liable as a fiduciary for this fee structure.

McCaffree Financial Corp. v. Principal Life Ins. Co., 2016 WL 98332,—F.3d—(8th Cir. Jan. 8, 2016).

F08-21

Think About

• Are you a named fiduciary?• Are you a functional fiduciary?• Are you both?• Why?• How about your professional advisors? Are they

fiduciaries? Some of them? All of them?• What about the collective bargaining parties?

– Is the union a fiduciary?– Is the employer a fiduciary?

F08-22

Examples

• Trustees, the Plan Administrator, and Investment Managers are generally fiduciaries.

• Those who are generally not fiduciaries:– Accountants– Actuaries– Attorneys– Health Providers

• The decision as to who is and who is not a fiduciary is quite fact specific. Note: The New DOL Fiduciary Rule will be discussed later.

F08-23

What is the Fiduciary Standard of Care?

A. Duty of Loyalty and its corollary, the Exclusive Benefit Rule

B. Duty of Care/PrudenceC. Duty to Diversify Plan InvestmentsD. Duty to Act in Accordance with Plan

DocumentsE. Duty to Avoid Prohibited TransactionsF. Duty With Regard to Co-Fiduciaries

F08-24

General Fiduciary Obligations, ERISA, Section 404(a)(1)

“(a) Prudent Man Standard of Care.—

(1) . . . A fiduciary shall discharge his duties with respect to a plan solely in the interest of the participants and beneficiaries and—

F08-25

General Fiduciary Obligations, ERISA, Section 404(a)(1) (Continued)

(A) for the exclusive purpose of:

(i) providing benefits to participants and their beneficiaries; and

(ii) defraying reasonable expenses of administering the plan;

F08-26

General Fiduciary Obligations, ERISA, Section 404(a)(1) (Continued)

(B) with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims;

F08-27

General Fiduciary Obligations, ERISA, Section 404(a)(1) (Continued)

(C) by diversifying the investments of the plan so as to minimize the risk of large losses, unless under the circumstances it is clearly prudent not to do so; and

F08-28

General Fiduciary Obligations, ERISA, Section 404(a)(1) (Continued)

(D) in accordance with the documents and instruments governing the plan insofar as such documents and instruments are consistent with the provisions of this title and title IV.”

F08-29

Enhanced Prudent Man Role

• If you don’t have the expertise, seek it.• Fail to do so at your own peril!

F08-30

Prohibited Transactions—ERISA § 406

• In addition to breaches of fiduciary duties, fiduciaries are prohibited from engaging in certain transactions known as “prohibited transactions.” Engaging in these transactions would also be a breach of fiduciary duty as well as a prohibited transaction subjecting the fiduciary not only to the remedies described above, but also to excise taxes. Prohibited transactions can be basically broken down into two categories:1. Party in interest transactions

2. Self-dealing transactions

F08-31

Prohibited Transactions—Party in Interest

• Party in interest includes:– Plan fiduciary, counsel or employee– Service provider – Contributing employer– Employee organization whose members are covered

(i.e., union)– Employee, officer, director or 10% shareholder of a

fiduciary, the union or a contributing employer– Certain other relative, owners or entities owned by a

party in interest

F08-32

Party in Interest Transactions—ERISA §406(a)

• A fiduciary cannot cause the plan to engage in a transaction if he knows or should know that it is a direct or indirect:– Sale or exchange, or leasing, of any property between the

plan and a party in interest;– Lending of money or other extension of credit between the

plan and a party in interest;– Furnishing of goods, services, or facilities between the plan

and a party in interest;– Transfer to, or use by or for the benefit of a party in interest,

of any assets of the plan; or– Acquisition by the plan of employer securities or real property

F08-33

Self Dealing TransactionsERISA § 406(b)

• A fiduciary cannot:– Deal with the assets of the plan for his own interest

or for his own account;

– Act in any transaction involving the plan on behalf of a party whose interests are adverse to the interests of the plan or the interests of its participants or beneficiaries; and

– Receive any consideration for his own personal account from any party dealing with such plan in connection with a transaction involving the assets of the plan.

F08-34

Prohibited Transaction Exemptions (PTEs)

• There are certain transactions that are exempted from the prohibited transaction sections of ERISA. These exemptions are provided by:– Statute– Class exemptions– Individual exemptions

F08-35

PTEs—Delinquent Contributions

• Prohibited Transaction Class Exemption 76-1– Arrangement to delay receipt of contribution

is allowed if:• Plan made an effort to collect• Terms of extension are in writing• Arrangement to extend collection time is for

the exclusive purpose of facilitating collection

F08-36

PTEs—Delinquent Contributions

• Plan can agree to accept less than the whole contribution if:– Plan made reasonable, diligent and systematic

efforts to collect the contribution– Terms of agreement are in writing– Terms of agreement are reasonable under the

circumstances based upon the likelihood of collecting the contribution or the expense that would be incurred if the Plan continued to attempt to collect the contribution

F08-37

PTEs—Delinquent Contributions

• Plan can deem contributions uncollectible if:– Prior to the determination, plan made

reasonable, diligent and systematic efforts as are appropriate under the circumstances to collect

– Determination is in writing– Determination is reasonable and appropriate

based on the likelihood of collecting the contribution or the approximate expenses if the plan continued to collection efforts

F08-38

PTEs—Delinquent Contributions

• Takeaways– Adopt a written policy covering audits– Adhere to the policy– Review the policy periodically to ensure that it

remains reasonable– Document decisions to make changes to the policy—

How do we justify the level of effort– In specific cases, ensure that there is a reasoned,

independent decision made in each case about how to proceed, when to settle and when to write off

– Document the efforts to collect, decisions and reasons in those cases!

F08-39

PTEs—Service Providers

• Section 408(b)(2) allows contracts or arrangements with a party in interest to provide services (or ancillary goods) or office space to the plan if:– Necessary for the establishment or operation of the

plan– No more than reasonable compensation is paid– Contract or arrangement is reasonable

• Must be terminable by the plan on reasonably short notice under the circumstances

• Certain covered service providers of covered (pension) plans must disclose compensation-related information to a responsible plan fiduciary if the covered service provider reasonably expects over $1,000 in compensation

F08-40

PTEs—Service Providers

• Takeaways– Make sure you document why you are hiring a service

provider so it is clear that the service is necessary– Review compensation when you hire the provider and

on an ongoing basis to ensure that it is reasonable• If the provider makes disclosures, review those disclosures• Note: plan does not have to accept the lowest bid!—DOL

Informal Letter to SEIU regarding selection of health care providers (2/19/98)

– Never enter into an arrangement until you are sure that no disclosure is required or that you received full disclosure

F08-41

PTEs—Service Providers

– Make sure the contract is terminable on reasonably short notice without penalty

– Make sure the other terms of the arrangement are reasonable

• DOL Adv. Opinion #2002-08A addresses attempts of service providers to limit liability and the process for selection of service providers.

– Review service providers on an ongoing basis • DOL Regulations § 2509.75-8, Q&A FR-17—The

performance of service providers should be reviewed at reasonable intervals

F08-42

Office Space

• Two common prohibited transactions– Leasing between a plan and a PII (union,

related plan, employer association)• Another plan may or may not be a PII (e.g., is it a contributing

employer to the other plan, does it provide services to the other plan?)

– Conflicts of interest for trustees• Same group of trustees decides the rent that one

plan pays to another

• Trustees is also head of the union or association to which space is leased

• Multiple PTEs depending on the particular parties, type of space, and who is leasing to whom

F08-43

Office Space

• Takeaways:– Make sure that there is an exemption for the particular

transaction and understand what it covers• Consider recusals where needed

– Make sure reasonable compensation requirements are met

• Out of date appraisals are a big problem area

– Be able to demonstrate that the terms were at least as favorable to the plan as an arm’s length transaction with an unrelated party or are reasonable

– Document it—Have a written lease, maintain records, document above determinations.

– Note similar issues with shared employees.

F08-44

What are the Penalties for Breaching Your Fiduciary Duty?

Personal Liability for Breach, ERISA, Section 409(a)

“(a) Any person who is a fiduciary with respect to a plan who breaches any of the responsibilities, obligations, or duties imposed upon fiduciaries by this title shall be personally liable to make good to such plan any losses to the plan resulting from each such breach,

F08-45

Personal Liability for Breach, ERISA, Section 409(a) (Continued)

and to restore to such plan any profits of such fiduciary which have been made through the use of assets of the plan by the fiduciary, and shall be subject to such other equitable or remedial relief as the court may deem appropriate, including removal of such fiduciary.”

F08-46

Can Fiduciary Duties Be Delegated?

• A qualified yes, but – Plan document must allow for such

delegation or allocation of fiduciary duties (other than trustee responsibilities.)

– Delegation should be in writing– Remember ongoing duty to monitor

F08-47

Duty of Prudence

• The use of professional advisors does not relieve the fiduciary from exercising prudence in decision-making.

• On a day-to-day basis, this obligation requires ongoing attention to the business of the fund; regular attendance at meetings; careful reading of correspondence from the administrator and fund professionals; and review of meeting minutes and other plan documents.

F08-48

Duty of Prudence (Continued)

• In Schoenholtz v. Doniger, 628 F.Supp. 1420 (S.D.N.Y. 1986), the court concluded that a trustee violated his fiduciary duties by failing to attend trustee meetings.

• Fiduciaries cannot simply “rubber stamp” the decisions of other trustees or rely blindly on the advice of professionals. “A pure heart and an empty head are not enough” to satisfy the Duty of Prudence. Donovan v. Cunningham, 716 F.2d 1455, 1467 (5th Cir. 1983).

F08-49

When Might One Fiduciary Be Liable for the Breach by Another?

• A fiduciary . . . shall be liable for a breach of fiduciary responsibility of another fiduciary . . .– He participates knowingly in, or

knowingly undertakes to conceal, an act or omission of such other fiduciary, knowing such act or omission is a breach;

F08-50

Co-Fiduciary Liability (Continued)

– If by his failure to comply with the specific responsibilities which give rise to his status as fiduciary, he has enabled such other fiduciary to commit a breach; or

– If he has knowledge of a breach by such other fiduciary, unless he makes reasonable efforts under the circumstances to remedy the breach.

F08-51

Hypothetical—Co-Fiduciary Liability

• Assume that you become aware that a fellow trustee has entered into a business venture with the plan’s investment consultant.

• The trustee routinely votes on the consultant’s contract and whether to bid out consulting services, but he never reveals his business relationship with the provider.

• What should you do? Do you have any liability?

F08-52

Co-Fiduciary Liability (Continued)

• A plan fiduciary is not relieved of responsibility for the fiduciary breaches of another fiduciary simply because he or she is not committing the breach.

• The fiduciary who discovers the breach of another must take affirmative action to remedy the problem, or she/he could face liability for the fiduciary breach himself.

F08-53

Co-Fiduciary Liability (Continued)

• This action may include reporting the matter to the full board and demanding remedial action.

• If no action is taken by the board, the fiduciary then must consider whether the matter should be reported to the appropriate authority.

• Resignation from the board without taking any remedial action is generally not enough to shield the fiduciary from liability for the breaches of other board members.

F08-54

Recap: Fiduciary Standards

A. Duty of Loyalty and its corollary, the Exclusive Benefit Rule

B. Duty of Care C. Duty to Diversify Plan InvestmentsD. Duty to Act in Accordance with Plan

DocumentsE. Duty to Avoid Prohibited Transactions

(conflicts of interest)F. Duty With Regard to Co-Fiduciaries

And, of course, comply with applicable law!

F08-55

DOL’s New Fiduciary Rules

• April 6, 2016: DOL issued the final “Conflict of Interest” regulations – Redefines and expands who is classified as an

“investment fiduciary” under ERISA as a result of giving investment advice to a plan or its participants or beneficiaries.

– Significance of new rule:» If investment fiduciary, the person must act in

participant’s best interest, avoid engaging in prohibited transactions and charge only reasonable fees.

F08-56

DOL’s New Fiduciary Rules

• Replaces regulations originally issued in 1975.– DOL viewed old rule requiring that advice be made

“on a regular basis” and be “the primary basis for a decision” to be too narrow.

– Many investment advisors could avoid fiduciary responsibility under old rule.

• Reflects evolution from DB plans to DC plans where individual participants are investing their own retirement assets.

• Phased-in implementation begins April 2017 and full effect by January 1, 2018.

F08-57

DOL’s New Fiduciary Rules

• Classified as an investment fiduciary if the person provides covered investment advice in the form of a recommendation:

• Recommendation: Communication reasonably viewed as suggesting specific action. – The more tailored the suggestion, the more likely it

will be viewed as a recommendation.

• Person providing the recommendation must receive a fee or other compensation for it.

F08-58

DOL’s New Fiduciary Rules

• Covered Investment Advice: Recommendation consists of “covered investment advice.”– Buying, holding, selling or exchanging securities or

other investment property.– How securities should be invested after rollover to an

IRA.– Management of securities, including investment

policies or selection of investment providers. – Whether to take a rollover, transfer or distribution

from a plan or IRA.

F08-59

DOL’s New Fiduciary Rules

• Fiduciary Relationships: Recommender has relationship with the plan, a plan fiduciary, or a plan participant. – Provides specific advice about specific investment

with respect to plan assets. – Pursuant to agreement that advice is based on

particular needs of recipient.– Represents or acknowledges himself as fiduciary

under ERISA or Internal Revenue Code.

F08-60

DOL’s New Fiduciary Rules

• Communications that are notrecommendations.– Making available a platform of investment

alternatives.– Responding to RFPs.– Providing objective financial data comparisons

with independent benchmarks.– General communications, e.g., newsletters,

commentaries, general retirement and financial planning.

F08-61

DOL’s New Fiduciary Rules

• Investment education.– Does not reference appropriateness of individual

investment alternative, individual benefit distribution options.

– Does not address specific plan investments, products, alternatives, options or services.

• Takeaway: – Some investment advisors who were not plan fiduciaries

may now be classified as investment advice fiduciaries.– Trustees may have recourse against third parties who will

now be deemed to be investment advice fiduciaries.

F08-62

Part 4. Service Providers

A. AttorneyB. AccountantC. Consulting/Actuarial FirmD. Administrator/TPAE. Insurer(s)F. Bank/CustodianG. Investment Consultant and ManagersH. IT Consultants and Others

F08-63

Selecting and Monitoring Service Providers

The DOL has published tips for selecting and monitoring service providers:• Consider what services the plan needs.• Ask for relevant information from the service providers being

considered (scope of services, experience, fees, references, etc. )

• Provide all prospective service providers identical and complete information about the needs of the plan. Consider formal bids from those best suited to the plan’s needs.

• Consider “bundled services”.• Require each prospective provider to specify which services are

covered for the estimated fees and which are not. Compare all the information received including that on fees and expenses.

F08-64

Selecting and Monitoring Service Providers

• Ensure that any provider handling plan assets has a fidelity bond.

• Check with state or federal licensing authorities to confirm the provider has an up-to-date license (if required) and whether there are any complaints pending against the provider.

• Make sure you understand the fees and expenses and the other terms of any agreements you sign with service providers and that such fees and other terms are reasonable.

F08-65

Selecting and Monitoring Service Providers

• Document in writing the process followed and the reasons for selecting the provider.

• Require the provider to provide regular information or other reports about the services provided.

• Periodically review the provider’s performance for quality and at a cost consistent with the arrangement.

• Review participant comments and complaints and periodically ask for verification that information received is still valid.

F08-66

Tibble v. Edison International,135 S. Ct. 1823 (5/18/15).

• U.S. Supreme Court ruled in unanimous statute of limitations decision that pension plan fiduciaries can be liable for continuing to include a particular investment option for a 401(k) plan, and not simply for the initial decision to include the investment option.

• Fiduciaries have a duty to monitor the continued prudence of earlier decisions.

F08-67

Part 5. Guiding Principles—The D’s

D’s to Remember:– Dignity– Discretion– Diversity– Disclosure– Due Diligence– Due Process– Documentation

D’s to Avoid:– Delay– Discrimination– Deceit

F08-68

Dignity

F08-69

Dignity

• Treat employees with courtesy and respect.

• Listen carefully. • Be as responsive as possible.• Practice the Golden Rule.• Example this year? Montanile (which we

will discuss under “Delay”)

F08-70

Discretion

• Retain Discretion, • But Exercise It • Consistently!

F08-71

Discretion

• Make sure CBAs/policies/handbook/plans provides discretion to the employer/administrator – To construe, interpret and apply terms and to

resolve ambiguities; – To amend or change those

policies/handbooks/plans at any time.

• Employee communications such as handbooks should also include both discretionary language and right to amend.

F08-72

Discretion

• Exercise discretion reasonably and consistently.

• Provide adequate notice/avoid retroactive amendments whenever possible.

• Still must comply with the law, the CBA, and your own policies. Stephanie C.

F08-73

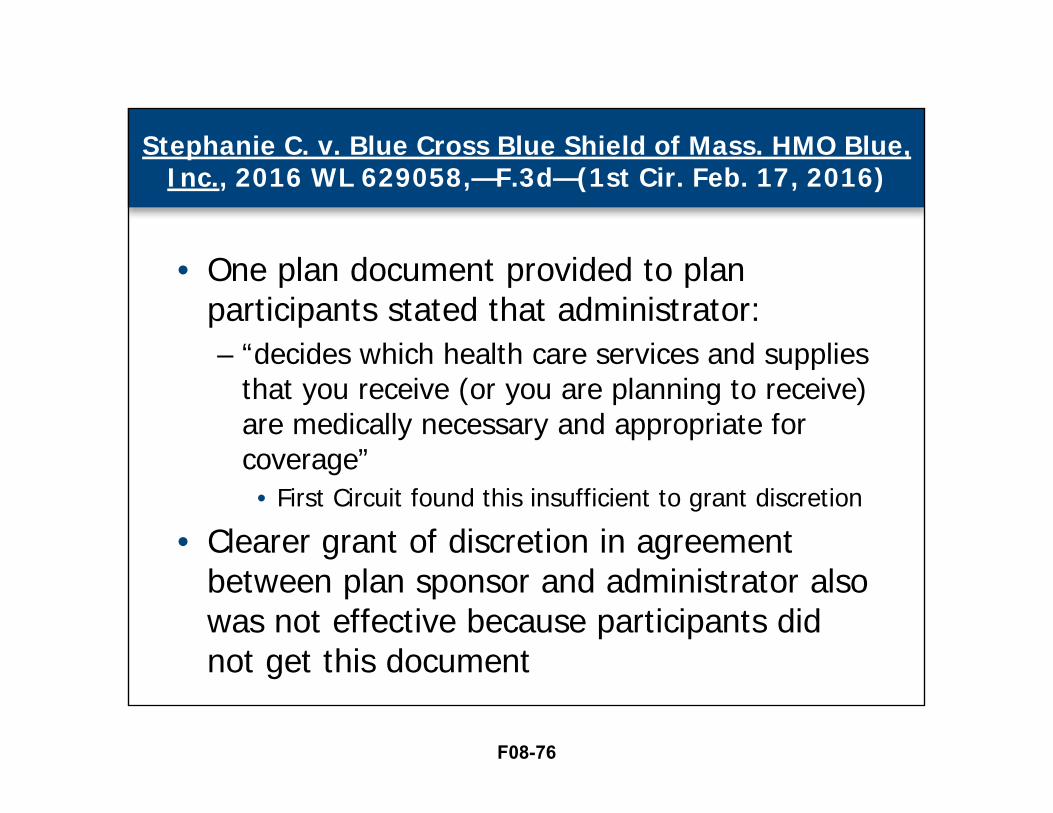

Stephanie C. v. Blue Cross Blue Shield of Mass. HMO Blue, Inc., 2016 WL 629058,—F.3d—(1st Cir. Feb. 17, 2016)

• Claim determinations—The First Circuit recently held that a plan followed proper process and sufficiently communicated with the claimant in denying claim for health benefits, but that plan had not granted discretion to plan administrator by placing discretionary clause in plan document that was not provided to claimant.

F08-74

• Stephanie filed a claim for residential care services for her son, who had severe mental health and behavioral problems.

• The plan administrator denied the claim, finding, based on review by psychiatrist-evaluator, that the treatment was not medically necessary as required by the plan.

• On Stephanie’s internal review, the plan again denied the claim, based on review by second psychiatrist-evaluator of all relevant documents.

Stephanie C. v. Blue Cross Blue Shield of Mass. HMO Blue, Inc., 2016 WL 629058,—F.3d—(1st Cir. Feb. 17, 2016)

F08-75

• One plan document provided to plan participants stated that administrator: – “decides which health care services and supplies

that you receive (or you are planning to receive) are medically necessary and appropriate for coverage”

• First Circuit found this insufficient to grant discretion

• Clearer grant of discretion in agreement between plan sponsor and administrator also was not effective because participants did not get this document

Stephanie C. v. Blue Cross Blue Shield of Mass. HMO Blue, Inc., 2016 WL 629058,—F.3d—(1st Cir. Feb. 17, 2016)

F08-76

• Lessons learned:– Draft discretionary clauses carefully– Include them not only in the plan document,

but also in the summary plan description, and in other documents provided to participants.

Stephanie C. v. Blue Cross Blue Shield of Mass. HMO Blue, Inc., 2016 WL 629058,—F.3d—(1st Cir. Feb. 17, 2016)

F08-77

Disclosure/Loose Lips Sink Ships

F08-78

Disclosure/Loose Lips

• Use all available communications opportunities and frame communications so that they will be most likely to be understood by all.

• Avoid legal or highly technical language.• And always remember: Loose lips sink

ships!• This year? Santana-Diaz, Yafei

F08-79

Santana-Diaz v. Metropolitan Life Ins. Co., 816 F.3d 172 (1st Cir. 3/14/2016)

• Generally, under ERISA, a plan can establish its own statute of limitations for lawsuits over plan-related disputes, so long as the limitations period is reasonable. – Including a limitations period that begins to run

before the claimant receives a final denial.

• If the plan declines to do so, state-law statutes of limitations applicable to similar claims will apply.

F08-80

• ERISA regulations require that “any adverse benefit determination” include:– [a] description of the plan’s review

procedures and the time limits applicable to such procedures, including a statement of the claimant’s right to bring a civil action under section 502(a) of the Act following an adverse benefit determination on review; . . . .

• 29 CFR 2560.503-1

Santana-Diaz v. Metropolitan Life Ins. Co., 816 F.3d 172 (1st Cir. 3/14/2016)

F08-81

• In this case, a disability-benefits claimant, Santana-Diaz, appealed his benefits termination under a 24-month mental-health-disability limitation.

• The plan had specified a 3-year statute of limitations, but failed to make any mention of this internal statute of limitations in several claim denial notices to the claimant

Santana-Diaz v. Metropolitan Life Ins. Co. (continued)

F08-82

• The First Circuit ruled: – (1) the regulatory requirement that an

adverse determination include “a statement of the claimant’s right to bring a civil action” required notifying claimants of a plan’s specific internal statute of limitations for filing suit, and

– (2) failure to do so rendered the plan’s internal deadline inapplicable.

• Even when the claimant has other documents communicating these time limits.

Santana-Diaz v. Metropolitan Life Ins. Co. (continued)

F08-83

• Lessons learned:– Include as much information as possible in

denial notices and other participant/beneficiary communications.

– Follow ERISA regulations, erring on the side of providing more detail where the regulations appear unclear as to what is required.

Santana-Diaz v. Metropolitan Life Ins. Co. (continued)

F08-84

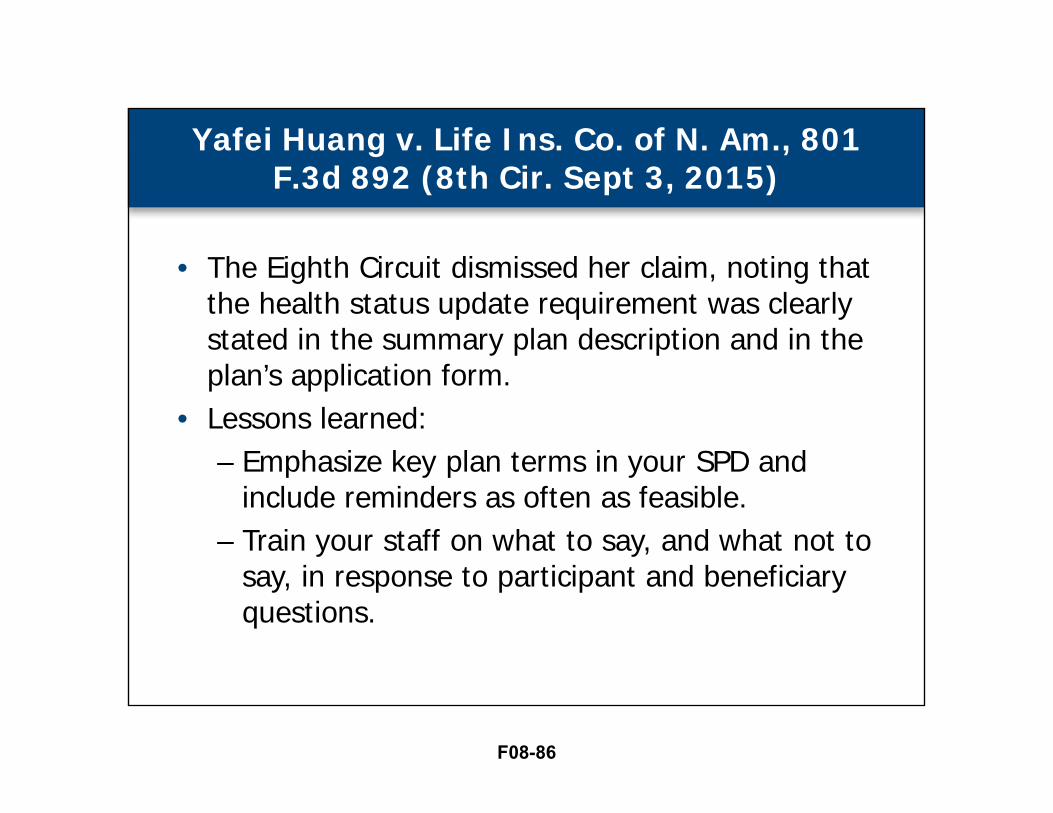

Yafei Huang v. Life Ins. Co. of N. Am., 801 F.3d 892 (8th Cir. Sept 3, 2015)

• Misrepresentation—An insurance company denied life insurance benefits to the wife of a deceased plan participant because the participant failed to notify the plan as to the change in his health status, which was required under the plan terms.

• The wife sued for breach of fiduciary duty (not for wrongful denial of benefits), claiming that someone working for the insurer had told her over the phone that health status was not relevant to coverage.

F08-85

• The Eighth Circuit dismissed her claim, noting that the health status update requirement was clearly stated in the summary plan description and in the plan’s application form.

• Lessons learned:– Emphasize key plan terms in your SPD and

include reminders as often as feasible. – Train your staff on what to say, and what not to

say, in response to participant and beneficiary questions.

Yafei Huang v. Life Ins. Co. of N. Am., 801 F.3d 892 (8th Cir. Sept 3, 2015)

F08-86

Due Diligence

F08-87

Due Diligence

• Due diligence means doing your homework.• Investigate thoroughly: don’t rely on

stereotypes, hearsay, or assumptions.• Due diligence is important in all aspects of

plan administration from development of the SPD and the ensuring of consistent treatment, to the adoption of an investment policy and the careful selection of investments and the regular review and monitoring of same.

F08-88

Due Diligence

• Stay current and get appropriate advice before taking the action– Retain appropriate expertise if you are not adequately

qualified.– Remember to monitor the professionals that you do select;

sift all recommendations with an eye to practicalities, financial and legal ramifications and public perception.

– Document your review process and why you made the decisions you did.

– Examples? – Tibble, Amgen, Montanile, Tyson Foods, Koning– The new DOL Fiduciary Rule

F08-89

Tibble v. Edison International,135 S. Ct. 1823 (5/18/15)

• In 2007, Glenn Tibble and other Edison employees sued under ERISA, which requires fiduciaries of an employee benefit plan to administer the plan prudently and for the exclusive benefit of the participants.

• The Employees alleged, among other claims, that including the retail-class funds was imprudent because there was a materially identical but less expensive alternative available (i.e., institutional-class funds).

F08-90

• The district court dismissed these claims as untimely because the decision to include the retail-class funds occurred outside (earlier than) the applicable six-year limitations period.

• The district court rejected the employees’ argument that continued inclusion of the higher cost funds in the benefit plan was a continuing violation of ERISA, and the 9th Circuit agreed the case should be dismissed.

Tibble v. Edison International,135 S. Ct. 1823 (5/18/15)

F08-91

• According to the Supreme Court, the Ninth Circuit failed to apply traditional trust law principles to the continued offering of the retail-class funds.

• Since plan fiduciaries have a continuing duty to monitor plan investments, any claim falling within the applicable statute of limitations could be considered.

Tibble v. Edison International,135 S. Ct. 1823 (5/18/15)

F08-92

Tibble Takeaways

• Under trust law, a plan fiduciary is obligated to:– Regularly review all investment offerings

• The timing and extent of which will depend on the surrounding circumstances, and

– Dispose of imprudent investments within a reasonable amount of time.

F08-93

• Trustees making investment-related decisions should always document all of their analysis, reasoning, and related efforts to show prudent decision-making processes.

• Valuation is always an issue for privately traded shares. See Perez v. Bruister. For publically-traded securities, it is much easier as the fiduciary can show its publically available market price.

F08-94

Perez v. Bruister, 2016 WL 2343009 (5th Cir. 5/3/2016)

• Federal district court did not err in finding that owner of closely-held corporation acted as a fiduciary of ESOP and breached fiduciary duties by interfering with valuation process and sale of owners stock in the corporation to the ESOP.

F08-95

Takeaways

A. Have a clearly enunciated purpose/mission/set of guidelines

B. Always utilize qualified professional helpC. Follow the basic fiduciary rules of prudence

(see above)D. Follow applicable law and your trust

document

F08-96

Due Process

F08-97

Due Process

• Develop sound policies and procedures and adhere to them.

• Beware of overly complicated processes.• Usually, processes should be in writing or

otherwise clearly published.• Importance of both procedural and

substantive due process. Apply the “smell test”.

• This year? Waskiewicz

F08-98

Waskiewicz v. UniCare Life & Health Ins. Co., 802 F.3d 851 (6th Cir. Oct. 2/Dec. 7, 2015)

• Even with discretionary clauses, courts may still overturn claim determinations.

• This case presents a situation where the court overturned a claim denial that appeared entirely in accordance with plan terms because the court found the denial to be contrary to the “spirit of employer-provided health care benefits generally and with this Plan specifically.”

F08-99

• Here, an employee had an emotional and mental breakdown for several months, and didn’t report the reason for her absence from work until well after the required notification period for purposes of receiving disability benefits.

• She was terminated retroactively effective as of the first day of her absence.

• This termination date made her ineligible for disability benefits because she was not a “covered employee” at the time of disability onset.

Waskiewicz v. UniCare Life & Health Ins. Co., 802 F.3d 851 (6th Cir. Oct. 2/Dec. 7, 2015)

F08-100

• The court ruled in favor of the claimant, explaining:– “An insurance policy can hardly be said to

provide employee disability ‘insurance’ at all if it protects against sudden disability but not if the employer immediately discharges the employee because of the disability before she gets a chance to apply for the benefits.”

• Lesson learned: – Remember fundamental fairness/the “smell” test– Hard facts make bad law.

Waskiewicz v. UniCare Life & Health Ins. Co., 802 F.3d 851 (6th Cir. Oct. 2/Dec. 7, 2015)

F08-101

Documentation

F08-102

Documentation

• The reasons for good documentation are many, not the least of which is that judges, juries, arbitrators, and administrative agencies expect it.

• Know the difference between good and bad documentation.

• Don’t promise more documentation then you can deliver.

• Document facts rather than conclusions.• Example: Tyson Foods

F08-103

Diversity

F08-104

Diversity

• Age• Gender• Ethnic background• Race• Religion• National origin• Disability

• Color• Gender identity • Sexual orientation• Military service or

Veteran status• Genetic

Information

F08-105

Diversity

• Cultural competency is the watchword.• Be sensitive to people’s varying backgrounds and

special needs.• Develop a communication style that works for you

and then adapt as needed to each individual’s needs.

• Create an atmosphere of dignity and respect where each person feels that their contributions are valued and where diversity is celebrated.

• Be alert to possible accommodations that may be needed.

F08-106

D’s to Avoid

• Delay• Discrimination• Deceit

F08-107

Delay

F08-108

Delay

• Act/Respond as promptly as possible under the circumstances.

• Always adhere to any time limits set forth in your CBA, policies, employee handbooks, or other relevant source.

• Document agreements to extend timelines. • Investigations should be as prompt as

possible under the circumstances.• Keep employees informed of need for

additional time.

F08-109

Delay

• Be proactive—Try to anticipate potential issues and plan your strategy ahead of time so that you can respond quickly.

• Example this year? Montanile.

F08-110

• Subrogation—Supreme Court held that ERISA-governed employee benefit plan cannot bring a reimbursement claim against the general assets of a beneficiary.– This is only a minor extension of a principle

established by the Supreme Court in 2002 (Great-West Life & Annuity Ins. Co. v. Knudson).

Montanile v. Board of Trustees of Nat. Elevator Industry Health Benefit Plan, _ S. Ct. (2016)

F08-111

Subrogation

• Here, plan beneficiary was insured through employer’s health insurance plan, which reserved the right to third-party payments to beneficiary for medical claims.

• Plan paid out medical claims to beneficiary for injury for which beneficiary later received a settlement from a third party.

• Plan tried to recover reimbursement from beneficiary, but beneficiary’s lawyer challenged.

F08-112

Subrogation

• Beneficiary’s lawyer was holding the settlement funds temporarily during negotiations.

• After negotiations broke down, the lawyer gave notice to the plan that he intended to distribute the funds (minus attorney’s fees) to the beneficiary. The plan did not respond, so the beneficiary received the money.

• Plan waited 6 months before suing for the settlement funds, by which point most of the proceeds had been spent by the beneficiary.

F08-113

Subrogation

• This ERISA section limits plans to “equitable” claims, which the Supreme Court has interpreted to mean that a plan cannot simply recover money owed to it; rather, a plan can only recover a specific, identifiable fund that rightfully belongs to the plan.

• The plan here had tried to argue that because the beneficiary had the money at one point in time, an “equitable lien” attached, allowing the plan to collect what it was owed from the beneficiary’s general assets.

F08-114

Subrogation

• The Court disagreed, ruling for the beneficiary.– Although not helpful to the plan in this case,

the Court noted that a plan may be allowed to recover money from a specific account when settlement funds were “co-mingled” with funds in that account.

• Lesson learned: – Act quickly to collect money owed, before the

money is distributed and/or spent.

F08-115

Discrimination

F08-116

Discrimination

• Avoid illegal discrimination or the appearance of it. – Remember an intent to discriminate is not

necessary if there is an adverse disparate impact on a protected class.

• Consistency is perhaps the single most important guiding principle in ensuring your decisions are not considered “arbitrary”.

F08-117

Discrimination

• This consistency should include:– Consistency with the trust document, CBA,

policy and how each has been previously interpreted and applied to other employees.

F08-118

Deceit

F08-119

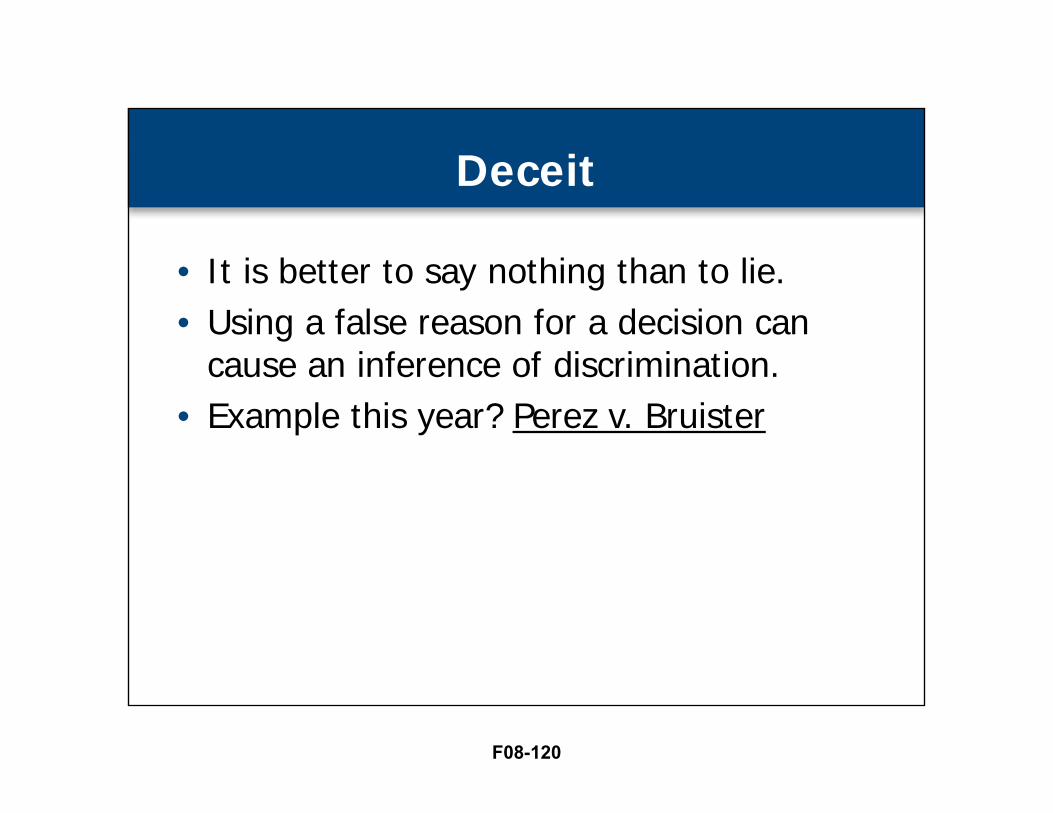

Deceit

• It is better to say nothing than to lie.• Using a false reason for a decision can

cause an inference of discrimination.• Example this year? Perez v. Bruister

F08-120

Take Home Supplement: Focus on Communication

F08-121

Communicate, Communicate, Communicate

• You can never have too much of the right kind of disclosure.

• Plan provisions should clearly spell out eligibility rules:– How to apply for benefits– How to appeal denials, and– Any limitations, exclusions, or time limits.

F08-122

Communicate, Communicate, Communicate

• Use all available communication opportunities.

• Frame communications so that they will be most likely to be understood by all.

• Avoid legal or highly technical language.

F08-123

Communicate, Communicate, Communicate

• Pay attention to legal requirements.– Make all required communications timely and

in the manner required.– In some cases, you may need to look at

providing some information in other languages.

– If you comply electronically, make sure you have met all the proper criteria.

• Remember: Communication is a two-way street.

F08-124

Communication in the Workplace

• All employee benefits communications should be careful, timely and accurate.

• Training fund office staff, employer HR and benefits staff, supervisors and managers, and union stewards and business agents about acceptable statements, comments and actions are also critical steps to avoiding lawsuits.

F08-125

Cigna v. Amara

• In 2011, the U.S. Supreme Court highlighted the importance of careful, timely and accurate participant communication and the avoidance of misleading statements.

• Cigna had converted its DB pension plan to a cash balance plan

• 25,000 employee class action was filed claiming that the notice of the filing was deficient.

F08-126

Cigna v. Amara (Continued)

• District Court found that Cigna’s descriptions were significantly incomplete and misleading, e.g., co. newsletter said the new plan would:– “Significantly enhance” the “retirement program”.– Produce an overall improvement in . . . retirement

benefits; and– Provide the “same benefit security” with “steadier

benefit growth”.

F08-127

• Employees were also told that– They would “see the growth in (their) total

retirement benefits” every year– That Cigna’s initial deposit “represent(ed) the

full value of the benefit (they) earned for service before 1998” and

– “(O)ne advantage the company will not get from the retirement program change is cost savings.”

Cigna v. Amara (Continued)

F08-128

• The new plan saved the company $10 million annually.

• The plan made a significant number of employees worse off:– The old plan had permitted early retirement at age

55.– The new plan imposed a pre-retirement mortality

charge.– The new plan shifted the risk of a fall in interest rate

from Cigna to its employees.

Cigna v. Amara (Continued)

F08-129

• The Supreme Court, although it remanded, appeared in dicta to approve the ultimate result of the district court, but disagreed with how it got there.

• Let’s look now at some recent cases illustrating the importance of how benefits, and any changes to or restriction on those benefits, are communicated.

Cigna v. Amara (Continued)

F08-130

Osberg v. Foot Locker, Inc. 2015 WL 5786523 (S.D.N.Y. 10/5/15)

• Employees filed a class action against sued employer, claiming that it violated ERISA when it failed to properly inform them of the effect of changing its defined pension benefit plan to a cash balance retirement plan.

• The district court held that the employer had failed to articulate the changes in the summary plan description leading participants to mistakenly believe that their pension benefits were growing.

F08-131

Osberg v. Foot Locker (Continued)

• The district court judge found that the SPD was not written clearly.

• The remedy was determined to be reformation of the plan to provide the participants with the benefits they thought they were receiving based on the misleading SPD.

• The employer has appealed this decision.

F08-132

Osberg and Cigna: Takeaway Tips

• Ensure proper notice is provided to employees about amendments to employee benefit plans.

• The more complete and accurate information you provide, the less likely claims will be brought against you.

• Remember Cigna and resist the impulse to “spin”.

F08-133

Johnson v. Meriter Health Services Employee Ret. Plan, 29 F.Supp.3d 1175 (W.D.Wis. 2014)

• Employee filed class action against the Plan and Employer on behalf of current and former plan participants.

• Defendant allegedly violated ERISA section 502(h) by amending the plan in 2003 without providing sufficient information to allow participants to understand the effect of the amendment.

• The court found on summary judgment that Plan and Employer had provided participants with sufficient notice of the 2003 amendments.

F08-134

What Did the Court Find to Constitute Sufficient Notice?

• A 3 page written notice, issued 2 months before amendment took effect, and included:– Date amendment would take effect – Possible future accrual effects– Changes to the employer's annual credits – Changes to annual interest credits– Forewarning that interest rate changes may result in monthly

annuities that will not increase for several years– Attachments showing how amendments could affect

participants differently, depending on age, years of service and pay level.

F08-135

Johnson v. Meriter: Takeaway Tips

• Be forthcoming with important information about amendments and the actual effect they may have on participants, as the Plan and Employer were here. The more complete and accurate the information provided, the better!

• Even though Defendants were sued, the nature of the notice they issued in 2003 saved them from spending time and money defending the issue at trial.

F08-136

Honey v. Dignity Health, 27 F.Supp.3d 1113 (D.Nev. 2014)

• Plan administrator/employer ordered to pay over $25,000 in penalties for failure to provide COBRA notice, despite paying for the medical bills.

• Employee Regina Honey worked as an RN at Dignity and participated in its group health, vision and dental plans, along with her dependent child, Addison.

F08-137

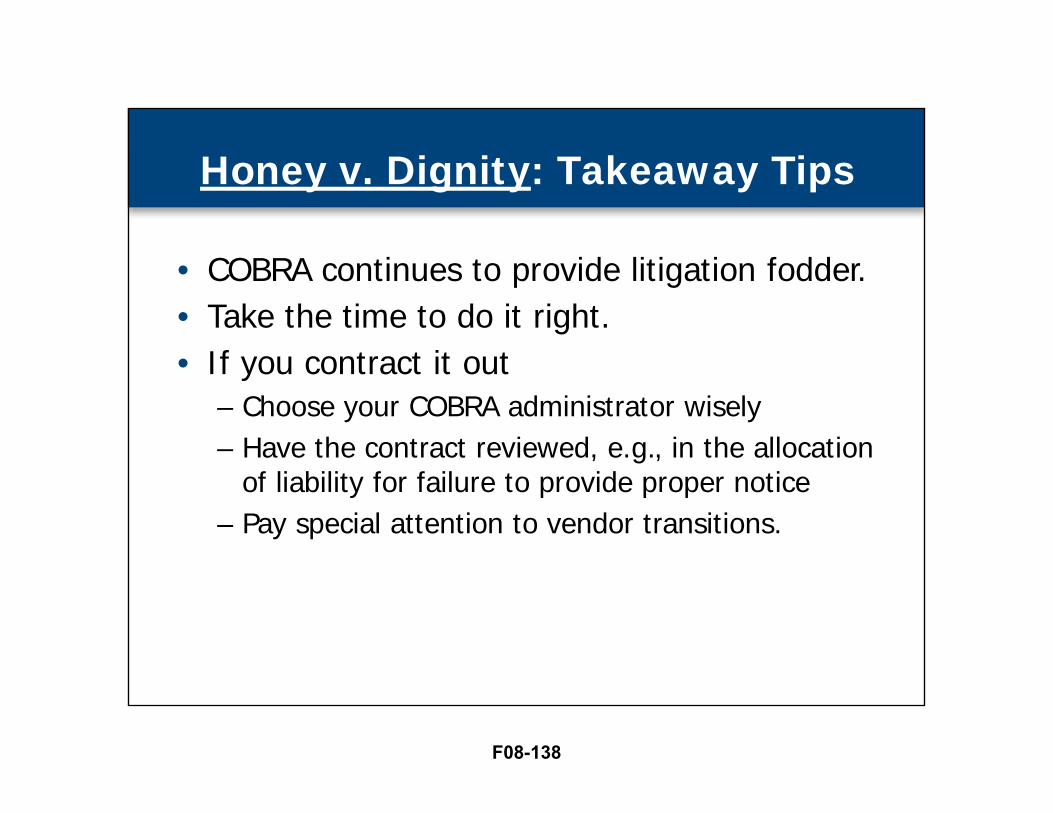

Honey v. Dignity: Takeaway Tips

• COBRA continues to provide litigation fodder.• Take the time to do it right.• If you contract it out

– Choose your COBRA administrator wisely– Have the contract reviewed, e.g., in the allocation

of liability for failure to provide proper notice– Pay special attention to vendor transitions.

F08-138

Honey v. Dignity: Takeaway Tips (Continued)

• Do not allow other concerns, such as processing of a grievance, to interfere with providing timely notice.

• Use updated model notices issued by DOL.

F08-139

Fama v. Design Assistance Corp, 2013 WL1443463 (3rd. Cir. 2013)

• Plaintiff’s resignation triggered right to COBRA notice; continuation of coverage did not negate termination as a qualifying event. Penalty upheld for inadvertent failure to provide timely notice.

• Penalty was appropriate even though court found DAC did not act in bad faith or with malicious intent, given its retroactive reinstatement of the coverage at no cost to her.

F08-140

Takeaways from Fama

• Pay attention to all required notices including COBRA notices.

• All qualifying events count, even voluntary quits.• Notice should be sent out even if coverage will be

continued for a period without cost.• Remember that all COBRA beneficiaries are entitled

to notice, for example, dependents living away from home or spouses living separately.

• Pay attention to the details, e.g., addressees.

F08-141

Lupyan v. Corinthian Colleges Inc., 761 F.3d 314 (3rd.Cir. 2014)

• Third Circuit reversed an order granting summary judgment to Corinthian Colleges on a plaintiff’s FMLA interference claim where she denied receiving her FMLA notice in the mail.

• College relied on the “Mailbox Rule”, which creates “presumption of receipt” if one can show a letter was either mailed or given to the postal carrier.

• CCI provided affidavits regarding the timing and method of the ailing the plaintiff claimed to have never received.

F08-142

Lupyan v. Corinthian Colleges Inc. (Continued)

• The Third Circuit determined that the Mailbox Rule does not create a conclusive presumption of receipt, but rather was only a rebuttable “inference of fact.” Her claim that she never received the letter overcame that inference for the purposes of summary judgment.

• The court pointed out that it would have been easy enough for the employer to have obtained proof of receipt. In this case, the letter was sent only “regular mail” with no certified letter receipt, tracking number, or signature.

F08-143

• The court remanded for determination of whether she received the notice and concluded that she had presented sufficient evidence to show that she may have been prejudiced by the employer’s alleged failure to provide the notice.

Lupyan v. Corinthian Colleges Inc. (Continued)

F08-144

• Although this was an FMLA, not an ERISA case, the court’s reasoning would appear equally applicable:In this age of computerized communication and handheld devices, it is certainly not expecting too much to require businesses that wish to avoid a material dispute about the receipt of a letter to use some form of mailing that includes verifiable receipt when mailing something as important as a legally mandated notice. The negligible cost and inconvenience of doing so is dwarfed by the practical consequences and potential unfairness of simply relying on business practices in the sender’s mailroom.

Lupyan v. Corinthian Colleges Inc. (Continued)

F08-145

Lupyan v. Corinthian Colleges Inc.: Lessons Learned

• Be thoughtful about the methods you use to provide important notices.

• Best practice is to be able to document actual delivery and receipt.

• Consider using some form of tracking or certification of delivery, i.e., sending them out in a traceable manner., such as:– Requiring signature (e.g., certified mail, return receipt requested)

– Using a delivery service with tracking numbers (e.g., overnight or two-day delivery services)

– Using electronic messaging with electronic receipt.

F08-146

• Seek confirmation from employee that email is an acceptable method of communication.

• Consider whether multiple methods should be used, e.g., distribution at worksites or union meetings in addition to mailing.

• Remember that in-hand delivery to one beneficiary may not constitute delivery to the other beneficiaries.

Lupyan v. Corinthian Colleges Inc.: Lessons Learned

F08-147

Koning v. United of Omaha Life Ins. Co., 2015 WL 5603094,—Fed. Appx.—(6th Cir. Sept. 24, 2015)

• Claim determinations—An administrator should explain why it makes a decision contrary to the submitted supporting documentation.

• Here, Vicki Koning worked for many years with chronic back pain, until finally reaching a point where she determined her condition prevented her from working.

• She was denied long-term disability benefits under her employer’s plan.

F08-148

• The claim administrator had found no physical change in her condition at the time she claimed benefits, and so denied the claim because she had worked with her condition for many years before.

• The court here sent the claim back to the insurance company for redetermination, finding that it failed to address medical documentation from Ms. Koning’s treating physician providing a credible and well-supported opinion that she was permanently disabled.

Koning v. United of Omaha Life Ins. Co., 2015 WL 5603094,—Fed. Appx.—(6th Cir. Sept. 24, 2015)

F08-149

• Lessons Learned:– The administrator should provide the reason

or reasons for the denial. – Address countervailing evidence of all types

and explain why the decision made is correct notwithstanding the contrary evidence.

– Ignore the treating physician’s evidence at your peril.

Koning v. United of Omaha Life Ins. Co., 2015 WL 5603094,—Fed. Appx.—(6th Cir. Sept. 24, 2015)

F08-150

Other Disclosure Cases

• Kough v. Teamsters Local 301 Pension Plan, 2011 WL 3626689, (7th Cir. 2011). Where benefit denial letter was cursory, it failed to comply with claims regulations and remand necessary.

• Mullins v. AT&T Corp., 2011 U.S. App. LEXIS 9271 WL 1491223 (4th Cir. 2011). Sponsor can be hit with large penalty for failure to provide documents even when underlying claim is dismissed.

F08-151

Disclosure

• Withrow v. Bache Halsey Stuart Shield Inc. Salary Protection Plan, 2011 U.S.App.LEXIS17526 (9th Cir., 2011) Wishy-washy responses to claim for benefits did not begin the accrual period for statute of limitations on appeal of benefits denial.

F08-152

Disclosure

• Kludka v. Qwest Disability Plan, (9th Cir., 2014) LTD denial reversed, because plan failed to explain specifically what information was needed to perfect the claim and why. Plan also failed to request SSA records even though it knew participant was receiving Social Security benefits and failed to explain why it came to a different determination.

F08-153

Disclosure

• Ortega v. Orthobiologics, LLC, (1st Cir. 10/25/11). Plan’s one year limit on filing suit did not bar suit filed 4 years after denial where plan failed to provide adequate notice of the one year limit.

• Novella v. Westchester County, (2d.Cir. 11/3/11) Claim begins only "when there is enough information available to the pensioner to assure that he knows or reasonably should know of the miscalculation.”

F08-154

Disclosure

• Bidwell v. Univ. Med. Ctr., (6th Cir. 6/8/12) Fact that claimants say they did not receive notice was not controlling where plan acted in a way reasonably calculated to ensure actual receipt of the notices by sending them by first class mail.– Query if this would still be sufficient (at least in the

Third Circuit) after Lupyan.

F08-155

Communication: Lessons Learned

• Stay current.• Communicate honestly, clearly,

completely, timely and often.• Do not over-spin or over-promise.• Remember, loose lips sink ships.• Train your staff!

F08-156

Part 6. Key Takeaways

DO PRACTICE: DON’T ENGAGE IN:– Dignity – Delay– Discretion – Discrimination– Disclosure – Deceit– Due Diligence– Due Process– Documentation

F08-157

Website Resourceshttps://www.ifebp.org/Resources/trusteeresourcecenter/Pages/FiduciaryResponsibility.aspx (Members Only)https://www.youtube.com/watch?v=d8HIyNGH3r4

62nd Annual Employee Benefits ConferenceNovember 13-16, 2016Orlando, Florida

• Do Practice:• Dignity• Discretion• Disclosure• Due Diligence• Due Process• Documentation• Don’t Engage In:

– Delay– Discrimination– Deceit

Session #F08

Fiduciary Responsibility Refresher

F08-158

2017 Educational ProgramsFiduciary Responsibility

63rd Annual Employee Benefits Conference October 22-25, 2017 Las Vegas, Nevadawww.ifebp.org/usannual

New Trustees Institute— Level I: Core ConceptsFebruary 20-22, 2017 Lake Buena Vista (Orlando), FloridaOctober 21-22, 2017 Las Vegas, Nevada www.ifebp.org/trusteesadministrators

Trustees and Administrators InstitutesFebruary 20-22, 2017 Lake Buena Vista (Orlando), FloridaJune 26-28, 2017 San Diego, Californiawww.ifebp.org/trusteesadministrators

New Trustees Institute— Level II: Concepts in PracticeOctober 21-22, 2017 Las Vegas, Nevadawww.ifebp.org/trusteesadministrators

Related ReadingVisit one of the on-site Bookstore locations or see www.ifebp.org/bookstore for more books.

Trustee Handbook: A Guide to Labor-Management Employee Benefit Plans, Seventh EditionItem #7068www.ifebp.org/books.asp?7068

816

F08-159