Feedstock Push hits the Demand Wall

37

www.icis.com 1 Feedstock Push hits the Demand Wall John Richardson David Hughes ICIS International eChem GPCA Dubai, November 2018

Transcript of Feedstock Push hits the Demand Wall

www.icis.com 1

Feedstock Push hits the Demand Wall

John Richardson David Hughes

ICIS International eChem

GPCA

Dubai, November 2018

www.icis.com 2

Feedstock Push hits the Demand Wall

• Feedstock push will support integrated players

• Demand patterns are changing as the demographics change

• The circular economy will massively impact our markets

• Globalisation is already coming to an end

www.icis.com 3

The Energy Transformation will up-end the oil markets

• Renewable wind / solar are now the cheapest forms of energy in the world

• Coal and then gas will be the losers in this transition

• Falling battery costs will support and accelerate the move

Source: Lazard Levelized cost of Energy

www.icis.com 4

The Energy Transformation will up-end the oil markets

Source: Prof Ray Wills, Univ. West Australia

www.icis.com 5

Shale boom will continue into the future

www.icis.com 6

Self sufficiency & return to naphtha adds 25 M te

ethylene by 2030

Chemicals used as diversification and hedge

against oil sales

Chemicals used as route to economic growth inside

BRIShale feedstock push adds

6.5 M te in wave 22020-22

Chemicals capacity growth driven by external factors

www.icis.com 7

CompanyCapacity (kt/year)

Downstream (kt/year) Location Start-up Status

Total/Borealis/NOVA 1,000Borstar PE (625) + existing PE

(400)Port Arthur, Texas End 2020

Cracker underconstruction, FID pending

for PE

Shell 1,500HDPE/LLDPE (2x 550), HDPE

(500)Monaca, Pennsylvania Early 2020s

Underconstruction

SABIC/ExxonMobil

1,800 PE (2 units), MEG Corpus Christi, Texas H2 2022Under

construction

PTTGC/Daelim 1,000HDPE (700), MEG (500), EO

(100)Belmont County, Ohio 2021 Evaluation

Formosa Petrochemicals

1,200LLDPE (400), HDPE (400), EG

(900)St James Parish,

Louisiana2022 Permitting, Evaluation

No breathing space before “Wave Two” crackers in US

ICIS Supply & Demand Database

www.icis.com 8

What’s the outlook for demand?

www.icis.com 9

Rich Western consumers are disappearing as they age

International eChem analysis

www.icis.com 10

Since last year, plastic waste has now moved to the top of the agenda

www.icis.com 11

Brands are now driving the circular economy agenda

Company Targeted

▪ Plastics

▪ All packaging

▪ Plastics

▪ All packaging

▪ All packaging

▪ All packaging

Initiative/commitment

“We are planning that all bottles will be made from 100% recycled plastic and trial non-plastic, biodegradable materials by 2020

“Use 100% recycled plastic in 65% of the entire annual bottle volume by 2020, aiming to go up to 100% for all our consumer goods packaging by 2025”

“100% of plastic packaging will be fully reusable, recyclable or compostable by 2025”

“Aiming to make all its consumer packaging 100% recyclable by 2025 and to have 50% recycled content in its packaging by 2030, ultimately help collect and recycle 100% of the packaging it cells”

“M&S announced that all its plastic packaging in the UK will not only be 100% recyclable, but also 'widely recycled' in the UK by 2022”

“Double recycled resin in plastic packaging (2020 vs. 2010), reduce packaging by 20%, ensure 90% of packaging is recyclable”

▪ All packaging “100% of packaging will be recyclable, compostable or biodegradable, increase recycled materials in its plastic packaging by 2025”

www.icis.com 12

A line in the sand … newplasticseconomy.org

• Elimination of problematic or unnecessary plastic packaging through redesign, innovation, and new delivery models is a priority

• Reuse models are applied where relevant, reducing the need for single-use packaging

• All plastic packaging is 100% reusable, recyclable, or compostable

• All plastic packaging is reused, recycled, or composted in practice

• The use of plastic is fully decoupled from the consumption of finite resources

• All plastic packaging is free of hazardous chemicals, and the health, safety, and rights of all people involved are respected.

www.icis.com 13

Where recycling is technically easy, expect big rise in production from recycled material

ICIS Supply & Demand Database

-

10000

20000

30000

40000

50000

60000

70000

80000

‘00

0 t

on

es

Global HDPE recycled production grows to 7% by 2030

Production Ex VIRGIN RESIN Production Ex RECYCLE

-

10000

20000

30000

40000

50000

60000

70000

80000

'00

00

to

nn

es

Global HDPE recycled production at 33.5%* in 2030

Production Ex VIRGIN RESIN Production Ex RECYCLE

*50% of today’s average global recycling rate for aluminium, steel and glass

www.icis.com 14ICIS Supply & Demand Database

Disappearing demand where recycling does not happen

-

10000

20000

30000

40000

50000

60000

70000

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

'00

0 t

on

nes

LLDPE: 118m tonnes of lost cumulative global demand

Base case: Growth averages 4.6% per annumm Growth averages 1%

55% of LLDPE consumption is into single-use applications

www.icis.com 15ICIS Supply & Demand Database

Circular Economy threatens cracker operating rates

80%

82%

84%

86%

88%

90%

92%

-

50000

100000

150000

200000

250000

300000

Op

erat

ing

rate

s

'00

0 t

on

nes

/yea

r

Global ethylene capacity

Operating rates under LLDPE base case

Operating rates under LLDPE downside

• Current cracker plans seem to ignore the demand reduction from Circular Economy

• Margins on non-integrated crackers will be squeezed and will see no relief

www.icis.com 16

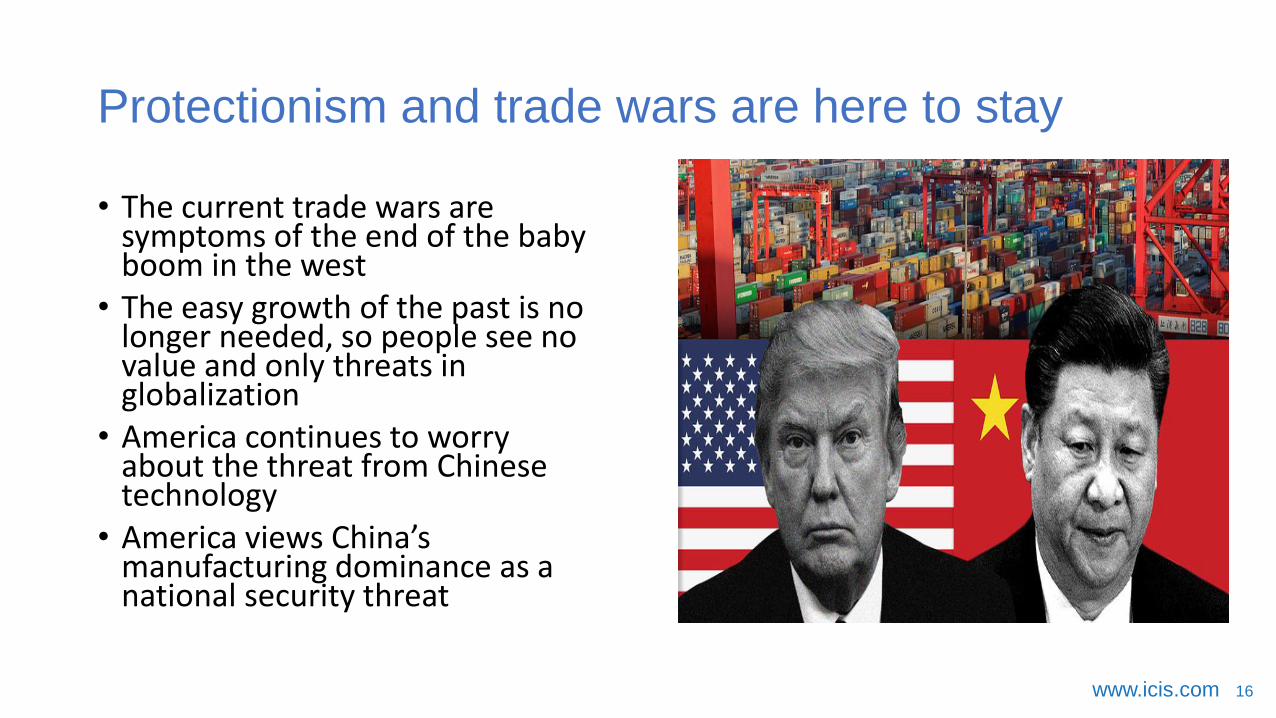

Protectionism and trade wars are here to stay

• The current trade wars are symptoms of the end of the baby boom in the west

• The easy growth of the past is no longer needed, so people see no value and only threats in globalization

• America continues to worry about the threat from Chinese technology

• America views China’s manufacturing dominance as a national security threat

www.icis.com 17

Four themes will drive our future

• Feedstock push will support integrated players

• Demand patterns are changing as the demographics change

• The circular economy will massively impact our markets

• Globalisation is already coming to an end

www.icis.com 18

US-China trade war – the context

www.icis.com 19www.icis.com 19

Why China is so important

ICIS Supply & Demand Database

-

20000

40000

60000

80000

100000

120000

140000

160000

1800002

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

‘00

0 t

on

nes

Global polyethylene consumption

NORTH AMERICA SOUTH & CENTRAL AMERICA EUROPE

FORMER USSR AFRICA MIDDLE EAST

NORTH EAST ASIA EX-CHINA CHINA ASIA AND PACIFIC

Since 2008 China has become the biggest consumer as well as biggest growth market. Result of post-crisis stimulus and wealth growth

Will remain at around 30% of global consumption –largest of all countries and regions

www.icis.com 20www.icis.com 20

…when it is in a race against time to move up the manufacturing value chain as its populations ages

Meanwhile, it still faces the challenge of 500m of its population who live on less than $5.50 a day

So it cannot possibly agree to stop state subsides for manufacturing

US also closing the door on technology transfers

US is demanding China scrap its economic growth model….

www.icis.com 21www.icis.com 21

Largely overlooked key moment last November when, for the first time, the US National Security Strategy identified China as a geopolitical threat

Mike Pence: China now spends as much on its military as the rest of Asia combined. Beijing has prioritisedcapabilities to erode America’s military advantages. But they will fail.

Democrat support for Trump’s China policies

The threat of a new Cold War

www.icis.com 22www.icis.com 22

Speculative shadow lending down by $698nn year-on-year in January-October 2018

Total social financing, which is lending via the shadow and state-owned banks, $246bn lower

Financial easing measures taken to help with credit shortages

But on a net basis, credit will be lower in 2018 than last year

China’s environmental clean-up will continue

China debt reduction was already dampening growth

www.icis.com 23

US new capacity: major market disruptions if trade war continues

www.icis.com 24www.icis.com 24

Overreliance on China as US PE surpluses rise

ICIS Supply & Demand Database

All grades of HDPE and 93% of grades of LLDPE US exports to China affected by duties

But evidence traders are avoiding all cargoes

US needs China more than China needs US – e.g. only 5% of Chinese 2017 PE imports from US, but 11% of US exports-

5000

10000

15000

20000

25000

2019 PE global net imports without China 2019 PE global net imports with China

‘00

0 t

on

nes US would need 36% share of

remaining market based on its net exports

16% US market share

www.icis.com 25www.icis.com 25

Biggest impact on LLDPE

ICIS Supply & Demand Database

My forecast is for US total exports to reach 3.7m tonnes next year, up from 2.2m tonnes in 2017

Exports as a percentage of production at record high so far in 2018

US production to rise 12% in 2019 with local demand up just 2%

-

1000

2000

3000

4000

5000

6000

7000

8000

9000

Global net imports including China Global net imports excluding China

,00

0 t

on

nes

LLDPE in 2019

US would need 27% global market share

US would need 53%

www.icis.com 26www.icis.com 26

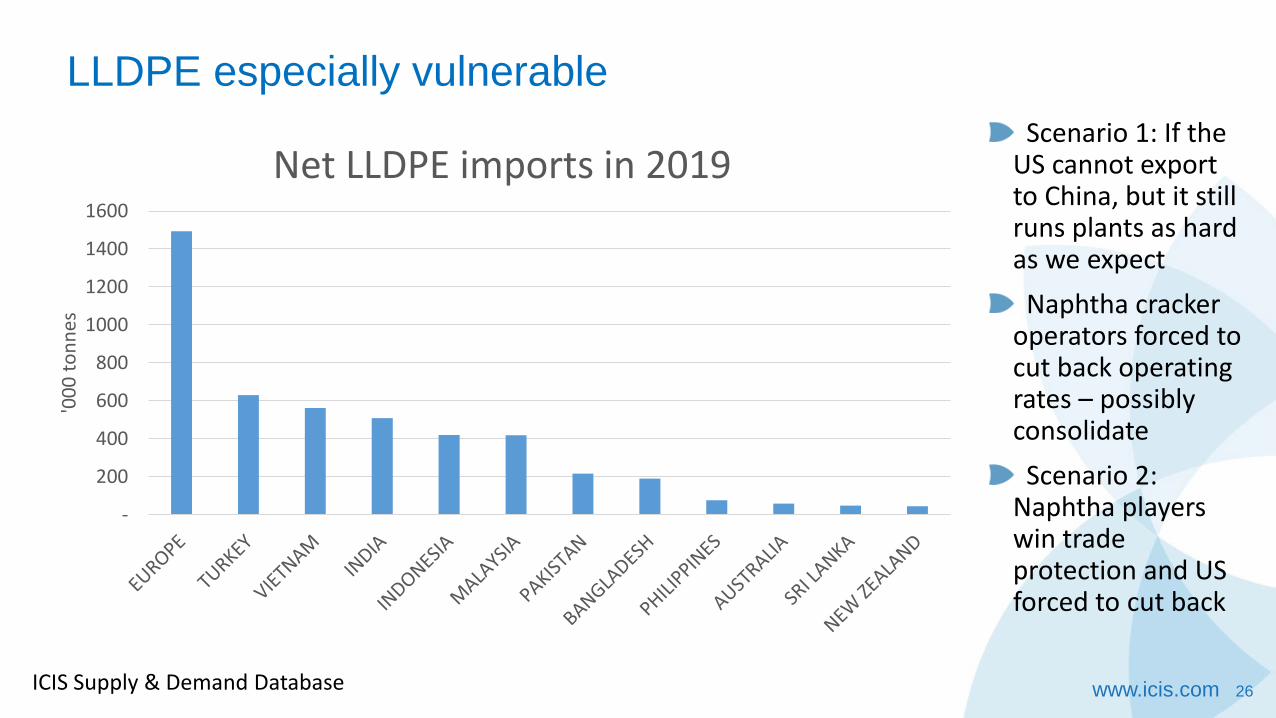

LLDPE especially vulnerable

ICIS Supply & Demand Database

Scenario 1: If the US cannot export to China, but it still runs plants as hard as we expect

Naphtha cracker operators forced to cut back operating rates – possibly consolidate

Scenario 2: Naphtha players win trade protection and US forced to cut back

-

200

400

600

800

1000

1200

1400

1600

'00

0 t

on

nes

Net LLDPE imports in 2019

www.icis.com 27www.icis.com 27

China will account for 84% of global net imports between 2018 and 2025

US will swing from net imports of 4m tonnes in 2008-2017 to net exports of 8.3m tonnes in 2018-2025 (big surpluses after 2020)

This is what could happen if US has no access to China!

Big impact on ethylene glycols longer term

- 20,000 40,000 60,000 80,000 100,000 120,000

Global net imports excludling China

Global net imports including China

Ethylene glycols in 2018-2025

US would need 53% share of this market

9% US marketshare

ICIS Supply & Demand Database

www.icis.com 28

China thought it had more time to make this multi-generational project work

But risk of losing US export markets has made the project more urgent

It has also created major geopolitical and economic opportunity for China to replace the US

In its largest definition, the Belt and Road Initiative would include 78 countries, 4.4 billion people and about 40% of global GDP – the World Bank

China is accelerating BRI because of the US

www.icis.com 29www.icis.com 29

One centred on China and its trading and geopolitical partners. This could comprise most of the developing world –and most consumption and growth

The other trading bloc centred on the US and its partners

Where does this leave the Middle East?

Two new trading blocs – US petchems face major risk

ICIS Supply & Demand Database

China 36%

Asia P15%

NE Asia Ex china8%

Africa3%

Former USSR2%

Middle East 5%

Europe14%

S&C America4%

North America13%

2018-2025 percentage shares of PE, PP, styrene and ethylene glycols consumption

www.icis.com 30

Sustainability and other risks to Chinese growth

www.icis.com 31www.icis.com 31

But this might lead to lower than expected per capita polymer consumption:

1. The rich, apart from sustainability concerns, don’t want to waste time in traffic jams

2. China government funding for autonomous driving and ride-hailing

3. Focus on improving air quality

4. The time poor, cash rich and the washing machine

China’s booming urban clusters are driving wealth growth

Bloomberg picture, September 2018: Hong Kong surpasses New Yorkin number of super rich (number of people worth at least $30m)

South China Morning Post: Baidu autonomous cars funded byIts Nasdaq-listed Apollo Fund

www.icis.com 32

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Base case in '000 tonnes

Downside in '000 tonnes

Base case per capita consumption in kilograms

Downside per capita consumption in kilograms

ICIS Supply & Demand Database

Base case: China’s per capita PP consumption rising from 19.9 kilograms in 2018 to 32.3 kilograms in 2030.

This would result in PP demand growing from 27.6m tonnes in 2018 to 45.4m tonnes in 2030.

Downside scenario: Only reaches 28.3 kilograms in 2030 with 19m tonnes of lost demand

Quantifying downside for PP

www.icis.com 33www.icis.com 33

Benefit of urbanisation: Beijing per capita consumption at 46 kilograms last year up from 16 kilograms in 2000

Meanwhile, Gansu, poorest region in China, rose to 10 kilograms from 1.5 kilograms

Boost from further more urbanisationand wealth growth

Booming internet sales a further factor?

Jing Daily, IMF and ICIS Supply & Demand Database

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Be

ijin

g

Shan

ghai

Tian

jin

Jian

gsu

Zhe

jian

g

Fuji

an

Inn

er

Mo

ngo

lia

Gu

angd

on

g

Shan

do

ng

Ch

on

gqin

g

Hu

be

i

Shaa

nxi

Jilin

Liao

nin

g

Nin

gxia

Hu

nan

Hai

nan

Heb

ei

Hen

an

Jian

gxi

Xin

jian

g

Sich

uan

Qin

ghai

An

hu

i

Hei

lon

gjia

ng

Gu

angx

i

Shan

xi

Tib

et

Gu

izh

ou

Yu

nn

an

Gan

su

Kilo

gram

s

PE per capita consumption by province and other administrative regions in 2017

Potential for inland wealth growth to accelerate

www.icis.com 34www.icis.com 34

Sustainability issues drive “less is more” focus on plastic packaging as recycling replaces virgin resins

Residents in poorer inland cities lack access to sufficient health care and education

Unless China escapes middle income trap faces major pension, healthcare shortfalls

2030 consumption 10.6m tonnes lower

What if per capita consumption growth disappoints?

0

10000

20000

30000

40000

50000

60000

Scenario 1: Average PE per capitaconsumption at 34.9 Kgs (up from 21.5

kgs in 2018)

Scenario 2: Average PE per capitaconsumption at 28.9 Kgs

'00

0 t

on

nes

China PE consumption in 2030

ICIS Supply & Demand Database

www.icis.com 35

Our concluding thoughts

www.icis.com 36www.icis.com 36

Just two of many scenariosScenario 1 - China/US reach deal and sustainability small effect

• Trump/XI reach a compromise. OR Trump leaves office and

US/China trade war ends

• Petchem world remains fully globalised

• US production and export growth continue

• Producers in other regions continue today’s strong capacity

growth

• Demand big enough to easily absorb new capacities

• Pushback against plastic waste has small effect on demand

Scenario 2 - China/US fail to resolve differences and

sustainability has major effect

• Trade war escalates

• New world of China + friends versus US + friends

• US unable to export to China and so floods Europe and

developing world ex-China with excess supply

• US and other projects are cancelled

• Global investment also slows on demand loss from plastic

rubbish crisis

www.icis.com 37www.icis.com 37

Feedstock push will support integrated players

Demand patterns are changing as the demographics change

The circular economy will massively impact our markets

Globalisation is already coming to an end

Winning in the new world requires focus