FEDERAL INCENTIVES FOR INDUSTRIAL ... INCENTIVES FOR INDUSTRIAL MODERNIZATION: HISTORICAL REVIEW AND...

37

il b. b . . L FEDERAL INCENTIVES FOR INDUSTRIAL MODERNIZATION: HISTORICAL REVIEW AND FUTURE OPPORTUNITIES Sandra C. Coleman AST Technical Manager NASA, Marshall Space Flight Center 1/ m* -4 - .. ?7 Industrial Engineering Department 0 Robert G. Batson Associate Professor -. -- , i r L; The University of Alabama a -. .. r.) --I P. 0. Box 6316 Tuscaloosa, AL 35487 . August 1987 Prepared for Submission to the IIE Journal The Engineering Economist https://ntrs.nasa.gov/search.jsp?R=19890016393 2018-06-14T07:56:01+00:00Z

Transcript of FEDERAL INCENTIVES FOR INDUSTRIAL ... INCENTIVES FOR INDUSTRIAL MODERNIZATION: HISTORICAL REVIEW AND...

i l b. b .

. L

FEDERAL INCENTIVES FOR INDUSTRIAL MODERNIZATION:

HISTORICAL REVIEW AND FUTURE OPPORTUNITIES

Sandra C. Coleman AST Technical Manager

NASA, Marshall Space Flight Center 1/

m* -4

-

. . ?7

Industrial Engineering Department 0

Robert G. Batson Associate Professor

-.

-- , i r L; The University of Alabama a -. . . r.) --I

P. 0. Box 6316 Tuscaloosa, AL 35487

.

August 1987 Prepared for Submission to the IIE Journal

The Engineering Economist

https://ntrs.nasa.gov/search.jsp?R=19890016393 2018-06-14T07:56:01+00:00Z

ABSTRACT

Concerns over the aging of the U . S . aerospace industrial base led DOD to introduce first its Technology Modernization (Tech Mod) Program, and

more recently the Industrial Modernization Incentive Program (IMIP).

incentives include productivity shared savings rewards, contractor invest-

ment protection to allow for amortization of plant and equipment, and

subcontractor/vendor participation. The purpose of this paper is to review DOD IMIP and to evaluate whether a similar program is feasible for NASA and

other non-DOD agencies. engineers because it provides a structured, disciplined approach to identi-

fying productivity improvement opportunities and documenting their expected

benefit.

dating cost avoidance is needed.

These

The IMIP methodology is of interest to industrial

. However, it is shown that more research on predicting and vali-

i

LIST OF FIGURES

Figure 1

Figure 2

Figure 3

Figure 4 Figure 5

Figure 6 Figure 7

Figure 8

Figure 9

Figure 10 Figure 11

Figure 12 Figure 13

Comparison of Five Commonly Used Contract Types Cost-Fee Relationships for Five Contract Types IMIP and Baseline Adjustments to Programs Cost Reduction Example Cost-Benefit Methodology Imposed on F-16 Subcontractors by General Dynamics F-16 IMIP Program Savings Forecast and Validation Discounted Cash Flow (DCF) Model Description of Discounted Cash Flow (DCF) Model by Line Item DOD IMIP Benefit Analysis Reporting Format DCF Model Logic DCF Input Screen for Example Application DCF Output for Example Application NASA/MSFC Major Program History

. .

I . INTRODUCTION

Industrial productivity has been defined as the ratio of valuable output to input, i.e., the efficiency and effectiveness with which re- sources -- personnel, machines, materials, facilities, capital and time -- are utilized to produce a valuable output [ l o ] . A recent article [21] in Industrial Engineering cites that high among the reasons for lagging productivity in the U.S. are outdated, outmoded production methods being used in places where capital investment has been minimal. Almost 70% of equipment used in aerospace production is more than twenty years old [ 2 1 ] .

The aerospace industrial base as utilized by the Department of Defense (DOD) and the National Aeronautics and Space Administration (NASA) func- tions under a variety of inherent difficulties which impede productivity gains: (1) complexity of the product; (2) relatively low build rates; (3 )

frequent changes in the basic product; and (4) substantial use of exotic materials and specialized subsystems, components, and parts. These dif- ficulties are further exacerbated by exterior forces on the government contractor by such things as (1) production re-scheduling and stretch-outs, (2 ) funding availabilities, (3 ) short-term contracting and financing, and (4) economic and environmental regulations.

.

To modernize a plant and improve productivity, the industrial engineer must ensure effective use of resources, integrate a unified and efficient effort, provide a baseline for performance evaluation, and prepare for future opportunities and r i s k s . This planning must encompass long range

markets and rate of growth, medium range demand for product and capital facilities and short range sales, personnel space needs, and cash flow. Major capital investments must be planned, designed, and installed in advance of need. profit reasons of using the available but worn-out or unproductive capital equipment or facilities. Often in the aerospace industry, these facilities are government-owned.

DOD capital expenditures to improve defense industry productivity

Too often the decision on investment has been delayed for

growth are described in [2 ] by "policy solutions to incentivize corporate

capital investments have been promulgated in two specific areas: changes to contractual policies relative to negotiated profit objectives and progress payment rates to increase the cash flow of defense contrac- tors; and (2) the provision of government "seed money'' as direct

(1)

1

, . . .

performance incentive payments to specific contractors to bring high technology industrial modernization to the factory floor." in this area by the U.S. Air Force were called Tech Mod (technology modern- ization). This concept matured into the DOD'B Industrial Modernization Incentive Program (IMIP), authorized on 2 November 1982 and referred to as "the cornerstone of DOD efforts to improve defense contractor productivity [12 ] . "

Technology programs that preceded IMIP [81, in fact 132 projects were selected for detailed review. The purpose of this paper is to review IMIP as a DOD-funded program of quite recent origin and evaluate whether a similar program can be used by NASA and other non-DOD agencies.

Early efforts

The GAO has published an extensive review of DOD Manufacturing

Historically, NASA and other non-DOD agencies have incentivized cost reduction through contracting modes that led to various rewards and sharing of cost-savings, based on performance. For this reason, a review of Federal government procurement practices is provided in Section 11. The DOD now has a track-record in applying IMIP, which we describe in Section 111. Industrial Modernization Incentive Program (IMIP) on non-defense Federal government-funded prime and subcontractors projects will be assessed. The decision factors for implementation of IMIP will be identified and applied in an example. NASA IMIP explorations will be reviewed.

In Section IV the feasibility of discrete application of a formal

11. GOVERNMENT PROCUREMENT PRACTICES

Government contacts are of two forms: (1) completion-end-product delivery in a specific time, and (2) tern-specified effort over designated time. tion, or lack of obligation to deliver specified end-products. ified work under a cost-reimbursement contract is not completed by the contractor within estimated cost, the contractor is nonetheless obligated

The form of contract used reflects the contractor's legal obliga- "If spec-

to continue his efforts to complete the work as long as the government is willing to fund the additional efforts [15 ] . "

pletion arrangement, any funding required beyond the ceiling price rests

Under a fixed-price com-

entirely on the contractor. Term contracts are often used

outcomes are difficult to forecast in early R&D efforts where technical and assurance of success is lacking.

2

Irrespective of actual accomplishment, the specified delivery of the level-of-effort completes the contract. Under term contracts, the govern-

ment bears the risk of the contractor not wishing to continue; while under

the completion form, the contractor must continue work till it is deemed

complete." These two forms are often called "mission" type and "best- II

efforts" type. are factors associated with determination of proper contracting form.

Risk assessment and guidelines for profit/fee motivation

The two family groups of contracts are (1) cost reimbursement and (2) fixed price. allocable, and reasonable costs including any overruns or growth. The

government's procurement regulations stipulate the measures of cost allow-

ability, allocability, and reasonableness. These cost type contracts allow

the government great flexibility in contract direction within the contracts

scope of work (SOW). government and less risk to the contractor.

In cost reimbursement, the government must pay all allowable,

This flexibility equates to additional cost to

Fixed-price contracts establish a firm fixed price (ceiling) beyond

which it is legally impossible to fund cost overruns or growth. Converse-

ly, if the contractor underruns his cost estimates he pockets all the

savings. Thus, a strong cost incentive is placed on the contractor and

less on quality or on-time deliveries. are considered for procurements where design is firm, cost estimates are

reliably certain, and schedules are easily attainable.

Therefore, the fixed price contract

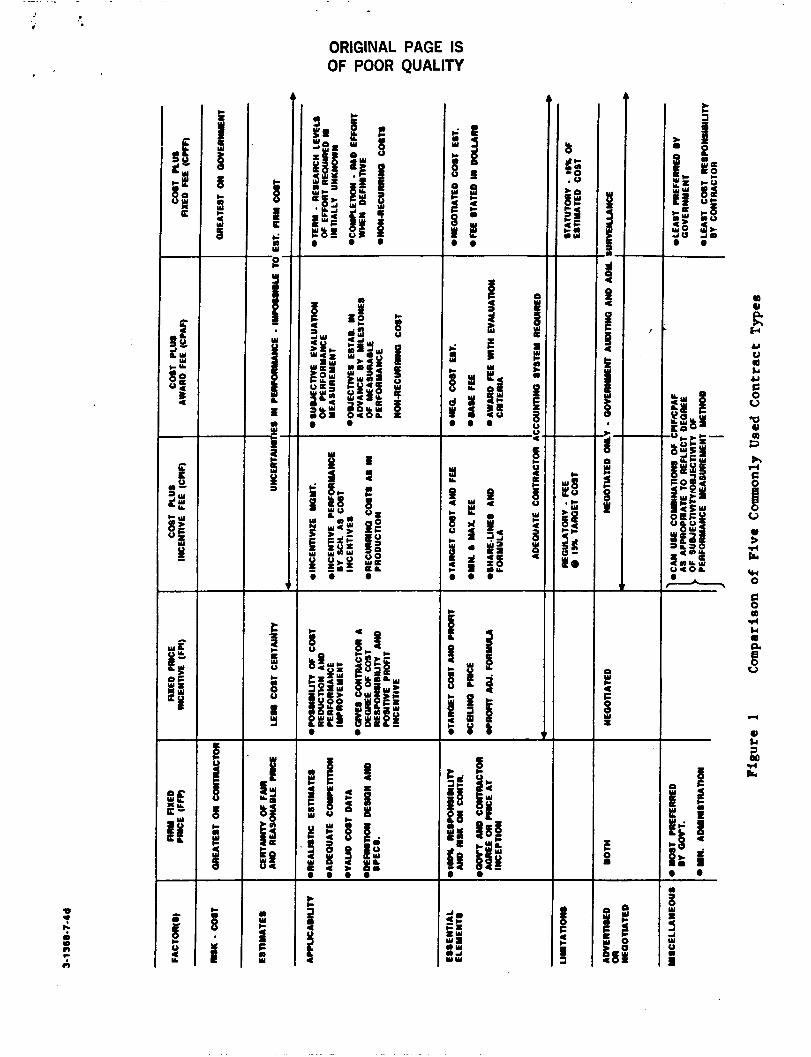

A. Contractor Risk The two families (cost and fixed price) of contracts are further

divided into specific types of contracts which delineate the government's responsibility to pay the costs incurred by the contractor. At one end of

the responsibility/risk spectrum is the firm fixed price which provides a

ceiling price that is not subject to adjustment for actual cost variances

experienced by the contractor. (profit) is a fixed amount and costs are reimbursed at actual.

these extremes, the contract types provide for responsibilities/risks

depending on degree of technical uncertainties. Figure 1 contrasts and

illustrates the factors used in selection of the appropriate contract.

At the other end the contractor's fee Within

This figure contrasts only the major selections of contract arrange-

ments which are commonly used between the government and its aerospace

industry contractors, subcontractors, and vendors. The customary

3

. . - .

contractual use of the profitlfee concept illustrates the strongest dis-

tinction between costs-reimbursement contracts (CPFF, CPIF, & CPAF) Involve

a fee, whereas fixed-price contracts (FPI & FFP) involve a profit.

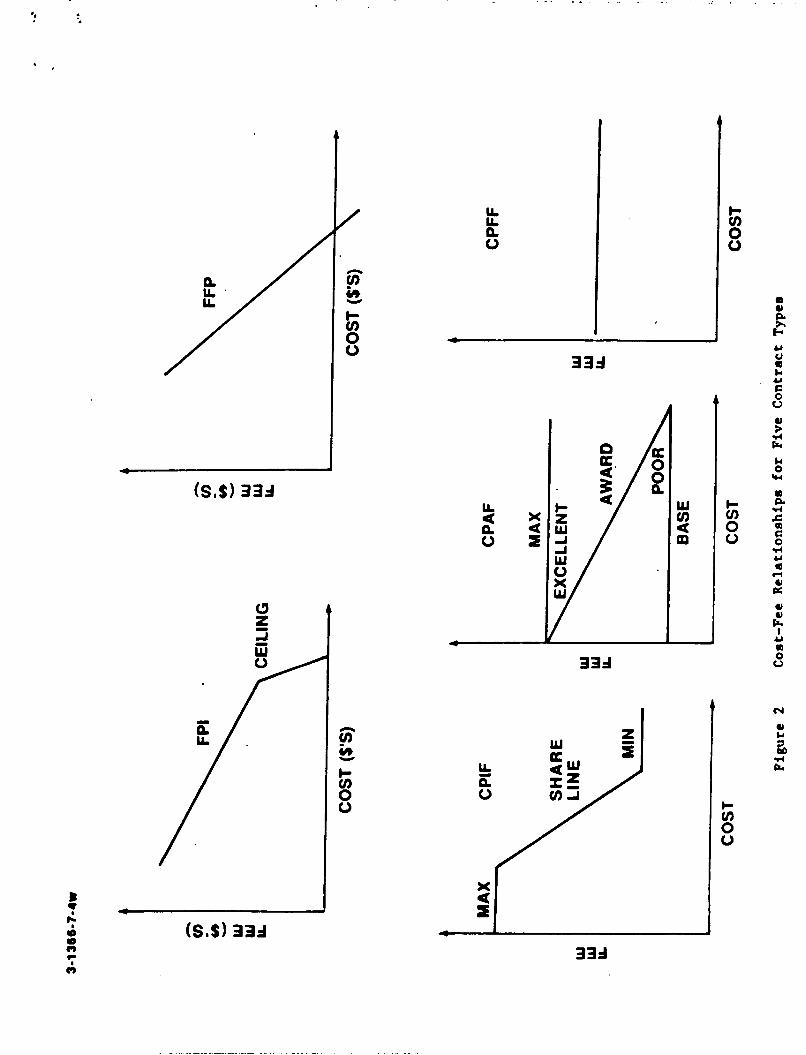

illustrate the relationship of contract cost outcome and the profit/fee Impact of each basic contract, the graphs of Figure 2 are provided.

To

B. Contractor Motivation to Modernize Several economic factors are considered by any contractor who is

Under CPFF contemplating a productivity improvement in his facility.

contracts, the contractor may feel incentivized t o underrun cost and affect

a higher fee relationship (rate) for his fixed fee. The CPFF arrangement

might encourage a contractor to "load up" on non-essential or idle facil-

ities to give stability to his work force. Another problem is the possi-

bility of a contractor overrunning direct cost to absorb fixed charges and

overhead.

The CPAF contract provides greater flexibility in deferral of cost of

performance objectives specification but is often criticized for the

arbitrary subjective evaluation of a contractor's efforts.

the award fee evaluation criteria, the distinction between a contractor's

inputs (such as personnel attrition, training, neatness, and administrative

practices) and delivered outputs (such as test data, facilities construct-

ed, and test completed) is often overlooked. The contractor may be overly

motivated to respond to acceptable "inputs" rather than accomplish the c o n t r a c t scope output o b j e c t i v e s .

In designing

Under CPIF contracts, the risk associated with cost, schedule, and performance objectives are systematically shared between parties of the

contract. Multiple incentive arrangements are encompassed in most "share-

lines" of fee.

emphasis on the penalty-reward considerations for cost, performance, and

schedule, Thus, these sharing structures communicate the optimal trade-

offs among these objectives.

These arrangements are so structured to place appropriate

In Stimson and Reeve's February 1984 Industrial Engineering article

[18] "Industrial Engineering Challenges in the Defense Industries," one of several problems cited in the incentivization for factory modernizations

was the inhibiting effect on progress on productivity by the cost-based

profit policy of DOD. productivity in that when DOD negotiates cost and profits, fee is typically

This policy in certain circumstances penalizes

4

permitted based on a cost relationship.

see profits reduced as a result of efforts to improve productivity and accordingly reduce cost.

Thus, a contractor may actually

The fixed price contracting environment is for those contracts when there is little or no uncertainties associated with cost, performance, or

schedule. incentive effectiveness is structured around cost outcomes which will vary

little from the negotiated cost estimates.

contractor, a higher target profit is provided. Under FFP contract, the

contractors reduction of cost reverts to increase in profit while the government does not share in savings.

The FPI arrangement applies a ceiling price and the range of

Due to higher risk on the

.C. Subcontractors and Vendors When a prime deals with its subcontractors, these second and third

tiers of vendors and suppliers are typically contracted on a firm fixed price basis. These FFP contracts provide the components, assemblies, and

parts that the prime aerospace contractor will modify, combine, assemble,

and test as an end-product. Often these parts and components will be

off-the-shelf hardware or "modified" standard catalog items. In this

arena, price may be a market response, a competitive bid, or a standard

quote with very little relationship to operations unit cost -- essentially "what the market will bear."

The government relies on competition and an "open" marketplace to assure a favorable and reasonable price. The interrelationship of the

subcontractor and the prime contractor under FFP is generally the same circumstances described earlier of the relationship of the prime with the government. The government will usually maintain some degree of control of

subcontracting by the approval process under the prime's declared and

approved "make or buy" policy. Individual major subcontracts must go

through an award approval process between the prime contractor and the

government. In the FFP environment, little if any government surveillance or administration is available on operations cost and performance measure-

ment. This factor complicates any assessment of operation for shared

shavings in the IMIP program parameters. The General Accounting Office

(GAO) has cited this as "needed guidance" to improve DOD efforts to imple- ment IMIP at subcontractors and vendors, stating that mechanisms are needed

for analyzing benefits and investments at these contractual levels [19] .

5

111. IMIP PROGRAM HISTORY

A. Background

In an October 1984 IMIP Technical Review, RADM J. S. Sansone, Deputy Chief of Naval Material, presented "The Challenge: trial Advantage Through Productivity and Technology [16]. "This review

gives a broad overview of the issues, concerns, and results of the IMIP Program to date. the following disturbing conditions: an eroding defense industrial base,

limited surge mobilization capability, capital investment in defense

segment low, productivity growth very limited, Defense Acquisition Regu-

lation (76-23)/profit policy not motivating contractors to make substantial

capital investments, and general misunderstanding of DOD finance policy and

cost principles.

Requiring the Indus-

According to this review, research studies have verified

At the same time, industry's concerns have grown in the areas of high

overhead costs, excess capacity, low labor productivity, high inventory and

material costs, quality assurance, poor sales forecasts, delivering new

products on time, and yield problems. If these concerns are not solved a company cannot compete and may choose to abandon the government market-

place. All of these concerns affect a company's productivity. According

to [16], influences which act contrary to modernization efforts in the DOD

marketplace have been: government provided plant and equipment, much of

which is outdated; cyclical nature of defense demand; annual fundings of contracts; short term-thinking; and cost based profit policy.

B. IMIP Definition and Procedures

In Figure 3, the IMIP influence and baseline adjustments on a program are charted. The profit strategy of IMIP incorporates good profit margin

management with management of asset turnover improvements to facilitate a

sound percentage return on assets and investments. The IMIP promises to

make quality, reliable hardware systems more affordable, while continually

motivating industry through shared savings rewards to be more productive.

Admiral Sansone [16] estimates the DOD results to date with projected new contractor productivity enhancing capital investments at $1.3 billion and

projected savings to be shared at $4.0 billion.

In the 1984 DOD Guide, "Industrial Modernization Incentives Program

(IMIP)" [4], two problems have been cited most frequently as inhibiting

6

- . .

productivity modernization progress. hinder investment amortization and inhibit long-term planning.

is cost-based-profit policy. eliminated long-term benefits of investment in modernization. The problem

is that profits (cost savings/avoidances) do not increase in the short-run

while costs (capital invested) increase significantly because capital must

be invested "up-front" of expected benefits. Figure 4 (from [SI) displays the nature of this "up-front" example of cost reduction.

First is program uncertainties which The other

The low price negotiation concept may have

The IMIP is a very targeted and controlled method of encouraging capital investment in productivity. negotiated under the IMIP, the DOD must be able to recognize the prospect

of reduced costs and other benefits which have cost reduction potential. Baseman [ l ] emphasizes "when more than one DOD Component is doing business with an IMIP contractor, one DOD Component will be assigned the lead and

will consolidate the other DOD Component requirements."

Prior to any business arrangement

C. Strategy and Assessment of Benefit

Other authors [e.g., 171 have recognized that government and industry

approach modernization incentives/programs from different perspectives.

From the government's perspective, three prerequisites for an effective

IMIP application are multi-year procurement, economic production rates, and

encouragement of competition. Program stability is vital to program

efficiency and productivity improvements. Production rate economies are essential to efficient utilization of facilities. A contractor must not

receive an unfair competitive advantage via incentives to modernize and maintain his manufacturing facility.

Other factors relating to the government's comprehensive program

acquisition strategy, which should influence the government's decision to

begin IMIP project planning, are listed below [from [SI): 1. Realistic budgeting

2. Improved support and readiness 3. Termination protection for purposes other than IMIP

4. Second-sourcing plans

5, 6, Spare parts acquisition

7, Profit policies

Manufacturing and producibility engineering planning

7

8. Interaction with other incentives, such as:

a. Incentive-type contracts

b. Value engineering

c. Design-to-cost d. Reliability and maintainability incentives

These considerations must be made to assure plans and techniques are

compatible with project strategy and goals and relationships with IMIP

incentives are well defined. IMIP should not be confused with efforts to

upgrade a manufacturing process in a contractor's facility with direct

costing against available government funding. Such efforts have been

criticized [I71 as promoting "piecemeal, bottoms up" modernization result-

ing in "islands of technology," with "little consideration for their

integration into total or parallel systems."

application with contractor investment,

IMIP is usually a plant-wide

Companies with aggressive productivity programs will gain the most

from IMIP as it overcomes many of DOD's contracting barriers to productiv-

ity enhancement. If IMIP is incorporated into a company's internal produc-

tivity program, only a minimum additional effort is required to effectively

use the IMIP. Furthermore, IMIP methodology [4] forces the industrial engineer assigned to identify productivity improvements to follow a dis-

ciplined approach for: 1. Factory analysis - Identifying productivity enhancement oppor-

tunities. 2. Benefit prediction - Benefits on opportunities to be exploited. 3. Benefit verification - Verifying actual benefits received versus

predictions.

In examining its productivity enhancement activities, a company must

look to those activities of the overall business objectives and its current

capital investment plans, For IMIP purposes, there are two classifications of capital investment; those made without the influence of IMIP incentives

and those with. The first class encompasses investments made to remain

currently competitive, to achieve baseline program objectives, to enter new

markets and to earn an attractive return on investment (ROI). IMIP is not

meant to subsidize, substitute, or replace these outlays,

The second class of investments with IMIP shared savings incentives are for those where an attractive return is not present and where risk due

to program uncertainties is at an unacceptable level. According to the DOD

8

IMIP Guide [4], "The contractor's share of the savings is that share necessary to make the investment an attractive business opportunity and is

calculated using the discounted cash flow model . . . for capital invest- ments and a percentage share of savings when the implemented improvements are not capital intensive.'' reduced to a computer program which is defined and utilized later in this section.

The discounted cash flow (DCF) model has been

The level of capital investment with IMIP incentives will be a strate- gic financial decision for the company. provide acceptable rate of return and investment recovery and make a commitment of the increased level of capital expenditure. commitment, the company should initiate discussions with the DOD and provide broad plans with simple estimates of cost and benefits. Each cognizant service in DOD, as well as NASA, will probably vary in approach and application. A contractor must recognize these distinctions and differences in policy, resolution, and implementation by these agencies.

It must decide that IMIP can

After such a

For early understandings with the DOD, a memorandum, which satisfies IMIP guidelines but is not a contractual commitment, should provide:

1. The contractor's past, present, and future productivity enhance- ment program (both content and dollars) without the IMIP incen- t ives . The contractor's increases in productivity enhancement effort if IMIP incentives are provided.

2.

3 . The expected benefits of the enhancement effort. 4. The company's projected sales base over the proposed IMIP par-

ticipation period, including the major DOD programs. A formal contract arrangement with the company will include approval

of productivity projects, contract incentives, IMIP statement of work, and obligation of direct funding, if any, for the government.

D. Prime/Subcontractor Relationships Under IMIP The subcontractor/vendor base represents a substantial part of most

major aerospace program costs, often 50% t o 60% of cost. At this tier of subcontractors, the DOD's "multi-services" and NASA are often interlinked. As such, this subtier base offers potential, significant benefits for IMIP

initiatives. The subcontractor IMIP involvement may be (1) direct govern- ment administered or (2) prime contractor administered under a government

9

contract. "programmatic" approach. of the industrial base. the subtler base of a given major system program.

The IMIP strategy In this case may be an "industry" approach or The "industry" approach targets a specif ic sector The "programmatic" approach attempts to modernize

The prime contractor may administer the subtler program for the government by formal program office management. provide management, control, financial incentives, and technology assis- tance necessary to stimulate vendors implementation of capital equipment investment. direct government program. and ensures the best interest of the government are being upheld. actions taken are still subject to the review and final approval of the

government.

Its objectives would be to

Basic management of a subcontract is handled the same way as a The prime contractor represents the government

All

In the financial investment analysis of the "costs" and "benefits" of an IMIP proposal, several steps are involved:

1. Define the baseline for comparison and expected savings. Analy- sis requires identification of cost and price if IMIP project was not adopted. There must be agreement on production quantities

and schedules. 2. Identify the necessary investment. Specific items, installation,

engineering, and time-phased acquisition costs must be developed. 3 . Develop a cost and pricing schedule for the proposal. The

realistic time-phased expectation of the implementation will influence the depreciation, the imputed cost of capital, and facilities-related profit.

4. Analyze the financial effects -- This step needs a Discounted Cash Flow (DCF) analysis of relevant financial forces.

E. Difficulty in Validating Cost Savings Cost and benefits of an IMIP application should be reviewed a minimum

of three times: economic analysis stage, pre-implementation, and post- implementation. A detailed analysis, usually involving a work breakdown analysis of the process for producing an item, must be performed in order

t o calculate the cost savings at a level which clearly segregates the effects of the change in the manufacturing environment [ 5 ] . The GAO [ Z O ]

has criticized the DOD and recommended "Better estimates of the savings resulting from IMIP efforts are needed in order to establish program

10

', . . i'

cost-effectivenese." techniques was true for prime contractors as well as administration of

subcontractors.

This comment on estimates and on better validation

F. F-16 Early Results, Trade, and Projections On the F-16 program, 60% of the cost represents procurement dollars

with subcontractors. In 1984, twenty subcontractors have started moderni-

zation programs and have yielded real results -- more than $550 million in DOD savings committed. According to General Dynamics (GD), ninety subcon-

tractors/suppliers are planned for involvement.

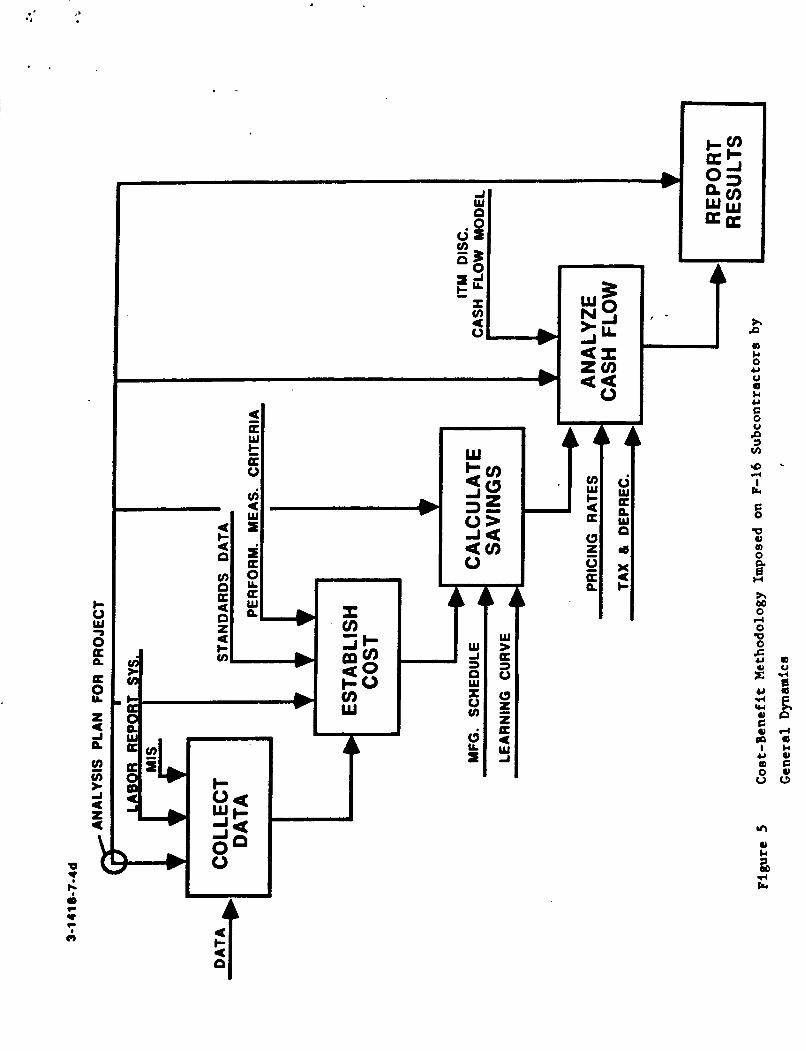

use an authorized cost-benefit approach and methodology which assumes a preliminary cost savings analysis in Phase I, a refined analysis in Phase 11, and implementation in Phase 111. A typical analysis plan and activ-

ities in this methodology is displaying in Figure 5 from [9].

The subcontractors must

The savings on the in-plant GD Tech Mod (IMIP) have been very drama-

tic. ment at $11M and development effort at $14M) in early 1977 was the fore-

runner to the Tech Mod program where GD agreed to invest $100M in new

facilities to affect 1388 F-16 aircraft. With follow-on contracts, the

total F-16 flight units anticipated are 2144 USAF and 75 Peace Marble aircraft. thirty-eight In-plant projects and productivity improvements which have

been Implemented [22].

The initial USAF commitment of $25M (contractor research and develop-

This extremely long production run will have benefited from the

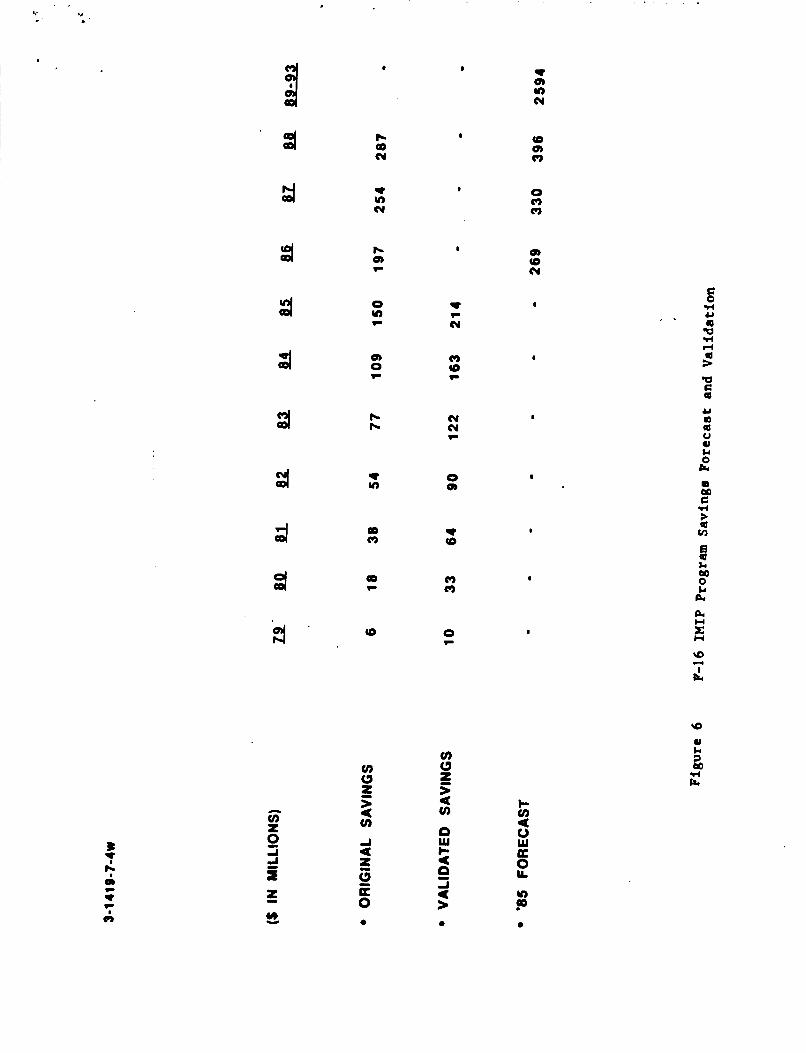

For a dramatic comparison, the original savings, the validated savings and 1985 savings forecast by GD are shown in Figure 6. It shows saving

validated to be 50% greater than estimates in the first seven years.

G. F-16 Goals Attained and New Horizons

The vehicle learning curve experience has been 78% on manufacturing

direct labor hours [22]. aircraft production over this extended period. This fact correlates with a

drop in hours per unit frhn 110,000 in 1977 to 26,000 hours today. savings relate to lead-time reduction from months to days.

basics of IMIP, the ROI at GD is averaging 12-182 [ l l ] .

The USAF considers this a phenomenal rate for

These Inherent to the

As reported by USAF and GD, the current initiatives include:

1. Program expansion to %on-touch," non-factory labor efficiencies

at the GD plant.

11

2.

3.

4.

5 .

Increase participants and lower tiers of subcontractors. Additional technical support to assist subcontractors in their initial efforts. Cost management projects at prime and subcontractor to tailor current cost accounting system to meet automation of the manufac- turing environment. Creation of computer data bases for enhanced collection, analy- sis, and dissemination of programmatic, financial, and technical data to government and industry.

In the General Dynamics brochure [23] on the F-16 (1985), the USAF F-16 Industrial Modernization Program Office Manager is quoted, "For every dollar of savings generated, 80 cents flow to other products and programs. For every government dollar of seed funding provided, industry has commit- ted six additional dollars of capital investment and ten dollars of savings to government." He expects to save $1 billion by 1993 in the total produc- tion of the F-16 fighter [ l l ] . By any standard of measure, the F-16 IMIP initiative has been highly successful.

.

IV. EVALUATION OF FEASIBILITY OF NON-DOD IMIP APPLICATIONS

We now describe a methodology [ 1 4 ] that could be utilized by program managers in the Federal government or industrial engineering management at

a contractor to evaluate the feasibility of a particular IMIP application, assuming groundrules identical to those used by DOD. The financial attrac- tiveness of a proposal is determined by comparing cost required with the

benefit expected. The contractor's net cash flow for an analysis of an investment proposal consists of:

1. Outflows a. Contractor facilities investment expenditures. b. Contractor income taxes from higher income less investment

tax credit per current Internal Revenue Service (IRS) guidelines.

12

2. Inflows

a. Imputed cost of money -- based on net book value of incentivized facility investment.

Depreciation on the proposed investment. b. c. Net change in profit (increase or decrease) -- represents

the net effect on profit/fee component of price, i.e., profit on depreciation, profit on facilities capital consideration, and any "lost profit" due to reduced

contractor effort.

d. Productivity Saving Reward (PSR) -- formal shared savings which is the incentive of IMIP to produce an adequate

contractor IRR on investment.

A. Analytical Model Analysis of this type is straightforward when a computer program does

the computation and keeps track of the agreed-upon items.

timates to be developed are these: The cost es-

1. The year-by-year investment-related costs (outlays, depreciation

accounting practice, relevant profit rates).

2. Other effects of productivity-enhancing investment (lower labor costs, out-of-pocket cost of production).

A "business as usual" case with no IMIP-related agreement (ini-

tial expected return for contractor and benefit to government without any sharings).

Alternative evaluations of "varied" saving shares and shares

timing .

3.

4.

5. If disagreements arise, the rate of return may be computed with

alternative inputs to highlight the disagreement variances.

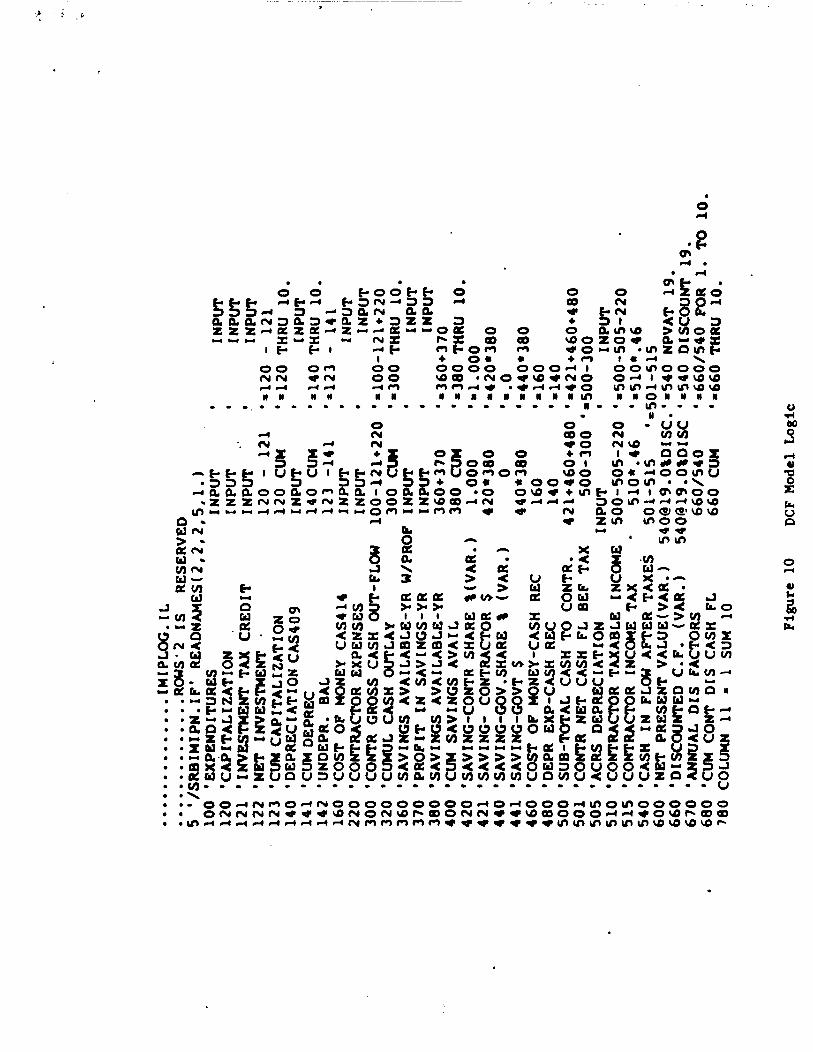

The DOD IMIP Steering Group approved [3] the Discounted Cash Flow (DCF) Model, developed and maintained by the Logistics Management Insti-

tute, for use as a tool in negotiating IMIP Tech Mod business agreements.

Figure 7 is taken from the USAF policy issued pursuant to the DOD IMIP

Guide and outlines the steps and items in the computer model. Figure 8

gives a line by line description of each line in the DCF Model [24]. A spread-sheet financial analysis program can handle a return on

investment (ROI) model and calculate the internal rates of return (IRR) for

a stream of year-by-year net cash flows. In the following sub-section of

13

L . . . .

this paper, a DCF model is developed and employed to evaluate a potential NASA initiative.

An IMIP proposal is based on the expectation of reduced costs and

The validation of the effects of IMIP effort is important

It shared savings. to the assurance and long term credibility of the program application.

is necessary early in the IMIP process to focus on the benefits analysis

and verification of the validated process requirements. The system may vary from minimal (evident reduction) to extensive and is dependent on the types of incentives used. The DOD Benefit Analysis is charted on Figure 9

from [24].

B. Example Application

A cash flow computer program, as shown in Figure 10, addresses all the

elements of the DOD IMIP program model. tions are made as follows, reflected in the model input screen (Figure 11).

A tooling complex costing $40 million is assumed for capital venture. Cost

Accounting Standard (CAS) 409 depreciation is computed on a 5-year sum-of- the-years digits method with an assumption of acquisition by mid-year.

Investment tax credit (ITC) and accelerated cost recovery system (ACRS)

depreciation assumes the pre-1987 tax regulations. CAS 414 cost of money utilizes the current Treasury Department interest rate on borrowed money.

Savings and profit are variable inputs and assumptions based on a forecast of savings inherent in the tooling installation.

In this example, several assump-

With these set of inputs, the DCF model computes a net savings of

$48.062M to NASA and $36.938M to the contractor, as shown in Figure 12.

This is based on an assumed total savings of $85.OM which is a direct

input. the contractor due to a lower base. Therefore, the true savings to the

contractor is $26.738M ($36.938M - $10.200M). on a 19% return on investment, which is a negotiating criteria. Share line

percents would be adjusted as negotiation strategy dictates.

Of the $85.OM savings, $10,20OM is attributable to profit loss to

This saving split is based

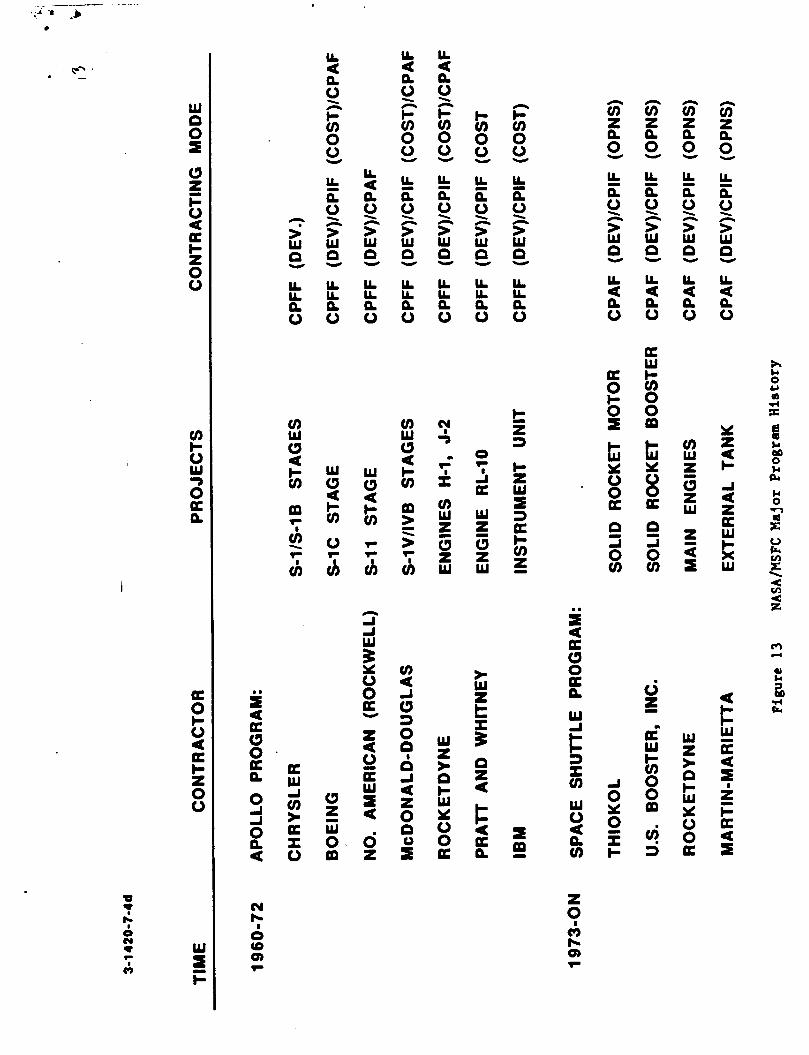

C. NASA IMIP Explorations Since the early 1 9 6 0 ' ~ ~ the role of NASA's George C. Marshall Space

Flight Center (MSFC) has primarily been the design, development, test, and

launch of various multi-project, multi-contractor propulsion systems.

of NASA's aerospace contractors use their own plants with government

Most

14

furnished tooling and have other contracts with one of the DOD tri- services. In some instances, the contractors utilized a government-owned

facility and produced a single project item, i.e. NASA's Michoud Assembly

Facility in New Orleans where Boeing and Chrysler built the Apollo Pro-

gram's S-IC and S-IB stages and where Martin-Marietta builds the Space

Shuttle's External Tank. In most cases, the government has provided

facilities and equipment rent-free, With the onset (1973) of the Space Shuttle Program, the use of expend-

able hardware from short production runs (often one-of-a-kind) gave way to

the repetitive production required of such items as the External Tank and

the Solid Rocket Boosters.

bility for IMIP-like programs at NASA-MSFC.

system contracts that MSFC manages on the Space Shuttle Program are given

at the bottom of Figure 13.

This repetitive production opened the possi-

The four major propulsion

.

These contracts are for ten or more years, valued at $5OOM to $1500M, and utilize incentives for cost control and improvement. Generally, each

of the programs of the Shuttle era have a non-recurring CPAF type of

contract environment with the recurring operational costs in a CPIF mode.

Prior to the Challenger accident, the trend in contracting for the projects

nearing a stable production status was the FPI mode. Due to weaknesses highlighted in the Challenger investigation, the emphasis has reverted to

the development mode of CPAF. This mode enables the NASA management a subjective unilateral use of profit measurement and motivation of a con-

tractor. The effect of this return to development mode and CPAF con-

tracting relegates IMIP opportunities to a secondary priority until the

Shuttle returns to flight status, Nevertheless, it I s likely that with the

return to Shuttle launches in mid-1988 and subsequent increases in the

launch rate to accommodate defense and Space Station projects, that the opportunity for IMIP applications will once again emerge similar to the

explorations reported below. The Solid Rocket Motor (SRM) prime contractor, Morton-Thiokol, Inc.

(MTI), I s the only NASA contractor which has explored IMIP opportunities. MTI IMIP efforts are traced back to March 1984 when a new tactical motor

plant and equipment were formally brought on-line and installed through

IMIP efforts of the U.S. Navy [13]. In November 1984, MTI initiated a complete analysis of all Solid Rocket Motor (SRM) operations at the Wasatch Division. The work breakdown structure was used as the framework for this

15

study. and potential improvement were identified.

Over 200 potential projects were identified and evaluated.

All major cost drivers within the WBS were analyzed, zero-based,

The study and evaluation technique considered feasibility, potential savings, invest- ment cost, lead time for implementation, verification, or qualification

requirements and other factors. subprojects were selected as suitable for near term implementation and were

included in the SRM Buy I11 Proposal (60 flight sets) which was withdrawn after the Challenger accident.

From the potential project list, 71

NASA has encouraged MTI to extend IMIP opportunities to its subcon- tractors. SRM subcontractors to help them understand the concepts and mechanics of

IMIP. Over the next s i x months, seven possible candidate subcontractors

responded with preliminary potential projects or process enhancements.

contractor made site visits and assessed the subcontractor's degree of

commitment and scope of projects.

In March 1985, orientations and presentations were given twenty

. The

Several issues were raised which fortify the early problems inherent

in procurement with government systems contractors.

program instability equate to level of production concerns and commitments.

Industry's concern for confidentiality of its cost information bears on the

very competitive nature of some market places and suppliers. The danger of

favoring one competitive supplier over another risks protests in court.

All of these subcontract candidates were in the very early planning stage

at the time of the Challenger accident, developing their initial capital investment plans and abilities. Significant interests in IMIP exist when program long range stability and production demand are present.

suppliers' concerns are for production rate, technical acceptability and

fair competition, Once these concerns are resolved, the joint NASA-

contractor decision to implement IMIP must be based upon cost recovery,

rate of return and risk protection.

The problems of

The

16

V. CONCLUSIONS

The DOD has been long concerned that the U.S. aerospace industry was not prepared for either short-term surge conditions nor long-term mobili- zation. Furthermore, defense contractors (similar to most heavy industry in the U.S.) are using out-moded facilities and tooling and therefore are not as productive as they could be if they modernized. Capital investment planning for long-range operations has been circumvented at these contrac- tor plants by short-term profit strategies and myopic fiscal planning. IMIP was created by DOD to solicit capital investment commitments from progressive firms for the purpose of providing savings to both parties in defense contracts through productivity improvements. These incentivized improvements have proven especially successful for General Dynamics and its subcontractors on the F-16 program.

It has been a government policy not to put one firm in a more competi- tive posture than another. In fact, competitive forces themselves lead to some modernization efforts. encourage production readiness improvement. has served as the primary motivator for Federal contractors to implement productivity improvements.

Direct cost funding by agencies such as NASA The CPIF mode of contracting

Assuming an ideal opportunity is shown to exist at a prime contractor facility or its vendors, IMIP can be readily employed in the first two phases, i.e., analysis and project plan. A performance measurement base- line, purged of others acquisition factors such as quantity changes, engineering changes, and learning curve effects must be developed [ 7 ] . The major drawback, which has been recognized by GAO, is the process to vali- date savings predicted by contrasting a "before-IMIP baseline" with "after IMIP." level of detail and distinction between learning, changes, and enhance- ments. A system of cost accounting and control to afford this level of substantiation could be complex, ponderous, and extremely costly to manage, unless properly designed. CPIF performance evaluation on an interim (prior t o completion) basis. There is a clear opportunity for engineering economy researchers to con- tribute improved methods to predict and validate cost savings due to modernization, and for contractor industrial engineers t o apply these in the IMIP-type arrangements with the Federal government.

Most firm's accounting systems are unable to reflect this precise

To a lesser degree, this problem is inherent in

17

Unless a contractor is heavily committed to work under Federal con-

tract to the exclusion of other work, modernization efforts will be more

influenced by commercial opportunities. Industry management has been

supportive of the IMIP concept, even though they are unanimous in their preference for an improved tax structure and the stability of multi-year

procurement as better ways to incentivize modernization. IMIP's role is

not to replace these preferred incentives, but rather to provide a justi-

fication for long-term investment in facilities and tooling which out-

weights any consideration of short-term R O I financial criteria. Thus, the

government's desire for productive use of its contract dollars can be

realized by appealing to the "strategic" or long-term profit desires of the

contractors [ l a ] .

18

c ? .

VI. REFERENCES

[l] Baseman, LeRoy T., "Cost Growth in the Acquisition of Weapons Systems: Experience, Causes, Understanding of and Positive Responses Thereto," The Journal of Cost Analysis, Vol. 1, No. 1, Spring 1984, pp. 101-114.

Collins, 0. M., LTC USAF, Planning, Program Manager, May-June 1984, pp. 28-35.

(21 "Getting Serious About Industrial Base

[3] Dever, James C., Jr., GEN USAF, Letter Dated April 18, 1984, Subject: DOD IMIP Discounted Cash Flow (DCF) Model.

[4] DOD, "The IMIP Process," DOD Guide, Industrial Modernization Incen- tives Program (IMIP), October 4, 1984, p. 2-1.

(51 DOD, "Scope and Purpose of IMIP, Background," DOD Guide, Industrial Modernization Incentives Program (IMIP), October 4, 1984, pp. 1-1, 1-3.

[6] DOD, "Investment Analysis, Verification, and Other Aspects," DOD - Guide, Industrial Modernization Incentives Program (IMIP), October 4, 1984, p. 3-2.

[7] Engwall, Richard L., "Methodology for Measuring Contractor Productiv- ity Sought by Defense Groups, Industrial Engineering, Vol. 16, No. 2, February 1984, pp. 62-64.

(81 GAO, "DOD Manufacturing Technology Program -- Management is Improving But Benefits Hard to Measure," Comptroller General, GAO/NSIAD-85-5, November 30, 1984.

[9] Hawk, M. R., F-16 Industrial Modernization Program Brochure, USAF F-16 System Program Office and General Dynamics, pp. 41-49, 59.

[lo] Hughes Aircraft Company, RbD Productivity, Second Edition, Culver City, CAB 1978.

[l l ] Lowndes, Jay C., "Management by Computer Promises Unprecedented Productivity Gains," Aviation Week and Space Technology, December 22, 1986, pp. 50-55.

[12] Mittino, John A,, "Productivity Improvement in the Acquisition En- vironment," IE Aerospace News, Val. XIX, No. 4, Spring 1985.

[13] Morton-Thiokol, Inc., Wasatch and NASA Host Industrial Modernization Workshop Today at MTC for our SRM Subcontractor," IMPULSE, Vol. 3, No. 10, March 7, 1985.

[14] Myers, Myron G., Discounted Cash Flow Analysis for Formulating and Evaluation IMIP Proposals, RE301-1, Logistics Management Institute, January 1984, pp. 1-8.

[15] NASA, "Legal Characteristics of Contract 'Types'," NASA Fundamentals of Incentive Contracts, Harbridge House, Inc., 1982.

19

[la] Sansone, R A D M J. S. , USN, "The Challenge: Requiring the Industrial Advantage Through Productivity and Technology,- IMIP-Technical Review, October 1984, pp. 243-263.

Sokol, Dan Z., "A Contrast of Government and Industry Technology Modernization Perspectives," IE Aerospace News, IIE Aerospace Divi- sion, Vol. XIX, No. 2, Summer 1984.

Stimson, Richard A., and A. Douglas Reeves, "Tri-Service DOD Program Provides Incentives for Factory Modernization," Industrial Engineer- ing, Vol. 16, No, 2, February 1984, pp. 54-61.

The Bureau of National Affairs, Inc.," Guidance Needed for Subs, Vendors," Federal Contracts Report, Vol. 44, No. 11, Sept. 16, 1985, p. 539.

The Bureau of National Affairs, Inc., "GAO Suggests Ways to Improve Implementation of DOD's IMIP Effort," Federal Contracts Report, 44, No. 11, Sept. 16, 1985, p. 538.

Vol.

Tulkoff, Joseph, "MANTECH Program Aims t o Make Factory of Future a Reality in Defense," Industrial Engineering, Vol. 16, No. 2, February 1984, pp.46-53.

USAF, History, F-16 Industrial Modernization Program Brochure, USAF F-16 System Program Office and General Dynamics, pp. 13-17.

USAF, Program Introduction, F-16 Industrial Modernization Program Brochure, USAF F-16 System Program Office and General Dynamics, p. 7.

USAF, "Tech Mod Economic Analysis Approach," IMIP, A Guide to Technol- ogy Modernization and Contracting for Productivity, Revised May 1984, pp. G-12 - G-29.

20

W

c t

ORIGINAL PAGE IS OF POOR QUALITY

0 Y

z c YI t a

IL IL

0 n

IL 4 0 n

333

B 'I

w v) U rn

t cn 0 0

J

8 Y a c Y 0

Id Y C 0 u 0 * rl fr b 0

8 a rl

C 0 r( e, 6 r( 0

pc 0

a

f

f u 8 0 u

8 8 I I I I

W

CI * D a c L <- 8 z

F U -3 0 0 Qc Q w

.

W > W 0

A x c' a Y 2 a 0 0 1E

w

W

m

3 w w 0 w PI 0 Y

m U

E a c, an 3 CI

2-

v) w

3 w 0

\ M 0 z w > 4 M

s

4 w v) 0 0

V u 7 m 0 pc Y

' 4

W > 3 0

Q

z < W J

a

E a

-

. . " . * '

3 a a t Q) Y) hl

b OD hl

a

0 Y) hl

a 0 (3 (3

a 0) co hl

0 ua r

* hl r

a d

4 7) t( rl

, - 4J

d 3 0) 0 r

c) co r

a

7) E 4 Y P Q 3 a

v u Id

a" 0 Q)

a 0 m C d * 4 Lo OD

(3 t 4 0

(3 (3

co 0 r

v) Q

r' a v)

v) (3 z 4 v)

3: c v) 4 z: d

4 z !? K 0

L t ?

-

8 LL r'

E n,

Y) OD

e

Figure 7 Diecounted Caeh Flow (DCP) Model ORIGINAL PAGE IS OF POOR QUALtTY

1984 1985 1986 Yrrr: I 2 3

1 C O . t r r C C O ? 1 D V O a C m r B t 0.0 0.0 0 .0 C u m u l r t i v o t o t a l 0.0 0.0 0.0

2 Comcrrccor t a p r r a r r 0.0 0.0 0.0 Cumulr t i v o T o t a l 0.0 0.0 0.0

3 DoD/Crvrrr~rrc r U B d i D 8 0.0 0.0 0.0 C u ~ u l r t i v r t o t a l 0 :o 0.0 0.0

4 S r v i m 8 r A v r i l r b l o t o D o 0 0.0 0.0 0.0 CUDU Lit i v o Total 0.0 0.0 0.0

---o-o ------ --.ooo S t C T I O S I. C O R E DATA

,/

1981 4

0.0 0.0 0.0 - 0.0 0.0 0.0 0.0 0.0

--..-.

Y O D I L I P I V T S :

C O B t t r C C O ? IBVOOLDOmr ................ ,-. ,-, C O B C r r C C O ? gS)OBO@r ,-, -,

8 r V i B 8 1 A V r i l a b l O t@ DoD ............. ,-,

??.fit I f f o r t ........................ CAS 414 a r t @ ................ s a t .................................... CAS 409 D r p r ~ e i a t i o r : ....................................................

Do prrr i r t i o @ U a t bo4 . .................................... Arrot S r r v i c r L i f e ( y o a t r ) .................................... ?Or? ?l@COd i B C B S O r V i t @ ....................................

A C I S D o p t r t i a t i O B : ....................................................... D i p t r r i r r i m m NrtLo4 .....................................

( ~ : $ t o m d r r d A C I S T r b l r r ; 2 : S t r r i 8 b t time) ........................... A r r r t CIrro ( S o r v i ~ o L i f e ) ....................................

( 3 : 3 - y r ; I: 50yr; 10: lO-yr) ....................................... Yrrr ? l a c o d i ~ r o S r r r i i i ....................................

C ~ ~ t r r c t ~ r T ~ s l r t ~ yy: .................................... I o v ~ r t o r a t t r a C r e d i t l r t r .. 88: .................................... C O D p l O t O d C O @ t ? r C t 0 r r r r r ( 0 i ~ p l i r r BO la81

e .

h D / G o v r r m m o ~ t famdi.8 ............... -. l o t r i m r d Srvi.60 I ~ ~ o m t i v o ........... SrlVr80 TOIBO

( 1 : s t r r i ( b t L i ~ o ; 2:su~-of-trrrr; I : S u m ~ o f ~ t r r r a / Y ~ l f ~ t r . r ; 4:lSOX D r c t i r i B ( B r l r m c r ; ) : l S O X . 08 . 8 r i t e I I O s t L i . 0 )

. . .

.........

0 . 0 .

0 0 . 0

f a r I P Y d L

- - * e - -

3 d

ORIGINAL PAW IS OF POOR QUALtTY

s u 4

I I c

Et I e

ORIGINAL PAGE is OF POOR QUALtTY

‘ I

Figure 9 DOD IHIP Benefit Analysis Reporting Format

. ,

. 0 d

0 - W N > - a m

cnm < z u w

irlw J Z

a Y

- I

a * I

> < VI z n

e Y

Y Y U Y Y

is" Y Y

a L O

Er u fr

........................................ 5s R ~ A D ~ 8 6 , 8 6 , 1 0 0 , 1 1 , 1 . 0 ~ . 0 ~ ~ ~ l . ~ FOR 1. TO 10. 56 READ(89,89,120,11,1.01.,0001.) FOR 1. TO 10. 57 R E A D ( 9 O , 9 O , l 2 l , l l , l . , I . , 0 . , 1 . ) FOR 1. TO 10. 58 R & A D ~ ~ l , 9 1 0 1 4 ~ 0 1 1 , 1 . 0 1 . 0 0 . 0 1 ~ ~ FOR 1. TO 10. 59 READ(92,92,160,11,1.01.,0.01.) FOR 1. TO 10. 60 R E ~ D ~ 9 ~ 0 ~ ~ 0 2 ~ ~ 0 1 1 0 1 . 0 1 . 0 0 ~ ~ l . ~ FOR 1. TO 10. 61 R&AD~94,94,360,11,1.01.00D01~~ FOR 1. TO 10. 62 R € A P ( 9 ~ , 9 ~ , ~ ~ o , ~ ~ , ~ . 0 ~ . 0 ~ ~ ~ ~ . ) FOR 1. TO 10. 63, ~~AD~96,96,505,11,1.01.00.01.~ FOR 1. T0.10. 75 - 1.0 .......... 75 76 COLUMN RANGE 76 = 5.0 . 77 = 4S.O , . . . . . . . . . . . . . . . T H I S 1s U S E D AS A LABEL. 78 .I 84. ............... MESSAGE

8 1 FORMSCREEN ( 23 . ) 83 ' F I = LEFT F 5 . m R I G H T F13 * S A V E DATA Fll - EXIT' 84 'YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5 ' 85 'YEAR 6 YEAR 7 YEAR 8 YEAR 9 YEAR 10'

90 INPUT('1NVESTMENT TAX CRE ',' ',9.01r08.01.,25.) FOR 75 TO 76 91 INPUT('DEPREC1ATION CAS409 " ' '~10.~l.08.,l.025.) FOR 7s TO 76 92 INPUT('C0ST OF MONEY CAS414 ',' '011.01.06.01.025.) FOR 75 TO 76 93 INPUT('CONTRACT0R EXPENSES ', ' ' 012.01.08.,1.025.) FOR 75 TO 76 94 INPUT('SAV1NGS AVAIL-YR W/P ' ' ' ' 013001.06.01.025.) FOR 75 TO 76

96 INPUT('ACRS D E P ~ I C I A T I O N ',' '015*01.08.01.,25.) FOR 7s TO 76 110 MESSAGE(83,20.,22.,55.) 111 HESSAG€('78',5.,28.,45.)

115 IF(l13COLl. EQ 11.1 GOTO 132 116 IF(113COLl. EQ 4.O)GOTO 75 117 ZF(ll3COLl'. EQ 5.)(75*6. FOR 1.;76=10. FOR 1.;78=85.;77*50.; GOTO 8 0 ) 118 IF(113COLl. EQ 13.1COTO 121 I19 GOTO '77' 121 PORMSCREEN(0.) ;FORMSCREEN(l8.) 122 MESSAGE('SAVING DATA - PLEASE WAIT - ',4.,20.,40.,9.) '

80 FORMSCREEN(O. 1

0 ~ 7 ~ ~ 1 * ~ 8 * ~ ~ ~ , 2 5 . ) F O R - 7 5 TO 76 0 ',8.01.06.01.,25.) FOR 7s TO 76

0 "

88 INPUT('EXPCND1TURES @ D 89 INPUT('CAPITAL~ZATION

9s INPUWPROPIT I N SAVINGS-YR ~014.01.0e.01.02s.~ FOR 75 TO 76

1 1 3 READSCREEN(I.)

. . . e . . . . . . . . . . . . . . . . ~ ~ ~ ~ o ~ ~ ~ . ~ ~ ~ o ~ ~ ~ ~ ~ ~ ~

123 WRITE~88088,100011,1.,l.00.01.~ FOR 1. TO 10. 124 WR1TE(89,89,120,11,1.~l.00.01.) FOR 1. TO 10. 125 WRITE~90,~0,121,11,1.01.,0~01~~ FOR 1. TO 10. 126 WRITE~91,91,140,11,1.01.,0.,1.~ FOR 1. TO 10.

128 WR1T&~93,93,220,11,1.,1.,0.,1.~ FOR 1. TO 10. 129 WR1T~~94,94,360,11,1.,1.,0.,1.~ FOR 1. TO 10. 130 WRIT&~9509S037001101.01.D~.,l.) FOR 1. TO 10. 131 WRITE(960960S0S011,1.,l.,0.,l~) FOR 1. TO 10.

127 WR1TE(92,92~160,11~1.~1o~O~,lo) FOR 1. TO 10.

............. ........................*.* A32 RETURNPLOGIC us1 /SRBIMIPMENU.IL CALC') A33 'END'

Figure 11 DCF Input Screen for Example Application -

a W e z W V v)

c C A

- 7 0 A O C

W v w a d

3:; u a

a i

n e t m t a a o A x a

a ? f t

A v l W 4 K f vl

~ o o o o o o o o ~ ~ g o o o o o o o o o ~ o ~ ~ o ~ ~ , n m m o o

o o o w o 0 m 0 m o w w m 0 ( 3 W O O m O ) C ) ( 3

< 0 0 0 0 0 0 0 0 O O ? w 0 1 1 0 t N - 0 0 0

c w w (3 * (3 m - W f- w _ N O * Q ( . ) w - - C O O 0 0 0 W 0 O N O f - O m m O m W - Y ) Y ) O

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 m 0 0 OY) .(3

S ? ? 0 0 0 0 0 0 0 0 0 0 w w (3 I- c

0 0 -

o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o m 0 0 S? 9 OY) ' 2

Y) 0 0 0 0 0 0 0

0 0 (0 w - w w (3 f-

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 o o o o o o w o o w 0 m w O N 0 CD O O m N O O N q 0 N O O O W N O m 0 Q, o m 0 2'0 I L"SC'" 222 " N X

O O O O O O O O O O O O O O O O O O O O O O O O O O @ ~ O ~ N ~ (3 O O O N C ) O O O O ~ O O ~ n o m m o m w m ooazn O C D O O N . ~ ~ O I D O ~ N ~ W Q C ) N

O w - m 0 - m w W W m z m z 0 .(3 0

c 0 1 0 * m m N I N W N N N

00000000000000000000oooooooooomw m O w w O m ~ :o-o-m Q 0 0 0 1 N O W a70 N o m m ~ 1 0 o o o o m o ~ o o m w ~ o ~ m r n ---t

o a 0 n w 1 m m o - Q , ( ~ w w m m ~ m m (0 q 0 O O I N.IB N mFl N - N

i . -

O O O O O O O O N O O O O O O O O O O O N O N N O N ~ W O O ~ ( 3 0 O O ~ N O o o o o ~ o o q O O O O O O O N N Q ) N m O O O O - 0 0 - w * w b O O O m m w W o m 0

O N ~ - N O N - o w - o ~ ~ m m m w r - ~ ? . N 0 - - N 0 - 1 - - r N N . - - I

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 o o o o o o O W o W w m

m 0 0 m N O O U O Q N o m 0 0 a 0 O l c O - O O m O Q ml-81 m m N L O O O t D O N L n Q 0 0 0 - 0 N Q V ) O ( D I I z 2 - E N N N 0 0 N O 1 I 1 I N

Q O O O O O ~ ~ N O O O O ~ N N O N O m m m - o - ~ - c ) @ o w

I I l l

00000000000000000000000000000000 0 0 0 0 b 0 b . . 0 !LD o m 0

m 0 0 0 0 0 0 0 0 Q O O N a D O 0 00

N N - O N N 00 - 11 7 * m 11 I

C C -- - - - I

O O o O O O O O O O O O O O O O O O O O o o o o o o o o O o o o 0 0 g ? ? ? f- - m

c

w V

I a a

I

0 s p i z

a a > >

'$ a K bl

c, 3 a

2 R x

z rl .. a

.b

W n 0 t c3 z 0 U I- z 0 0

F a

v) L i> W

0 n U

a 0 I- 0 a U k 2 0 0

s a U (3 0 U P

0 d d 0 P a

m

0 m 0)

?

r

LL

P 0

v) 0 0

5

a

F \

Y

P 0 > W

\ n

n Y

LL LL P 0

W c3 I- v)

0

a

j;

0 z 3 0 m

LL a a 2 s n W Y

LL LL P 0

W Q + v)

a

r z

5 n d d

Y 0 0

I U 0

a Y

iE a 0

i z

LL

P 0

v) 0 0

CL

0 > W n LL LL P 0

a

F \

W

\ n

v

7

7 I: v) W I

I W

3 m

i?

W z * n t; Y 0 0 a

I- v) 0 0 v

k 0 > W n LL LL P 0

\ n

Y

0

U W z I W

r 3

i?

* W z t

n a

a

I 2

r= a

~

3 z P 0

E

Y

LL

0 > W

\ n

n

a Y

LL

P 0

U 0

z

Y

8 t 8 a 0 i 0 v)

d 0 Y 0

k E

G z P 0

E

Y

LL

0 \ n c 0

LL

P 0

U

a

a W

0 0

tii

t m

Y 0 0 U n - 6 v)

3

ae" 2 - W

0 0

$i

4 m

3

~~

3 z P 0

ii:

s n

a

v

LL

0

W

\

v

LL

P 0

v) W z Q I W

2

P

-

z

W z * I- W Y 0 0 a

n