Federal Home Loan Bank Topeka Annual Management …

14

Federal Home Loan Bank Topeka Annual Management Conference April 25, 2013 Presented by: David L. Kemp Bankers Management, Inc.

Transcript of Federal Home Loan Bank Topeka Annual Management …

Federal Home Loan Bank Topeka Annual Management Conference

April 25, 2013Presented by: David L. Kemp

Bankers Management, Inc.

1

Bankers Management, Inc.

What ________ or __________, by management, has caused the number on the financial statement to be what it is, and as a result, what does this mean to the bank.

The analyst must ask the RIGHT questions

Bankers Management, Inc.

Risk Assets (Loans & Leases) make up the largest asset on the bank’s balance sheet, while the net interest margin and loan fees make up most of the bank’s revenue stream.

No one can predict all potential risk that can impact a credit◦ “Murphy’s Law”◦ Does policy define an acceptable level of risk??

2

Bankers Management, Inc.

Have a healthy skepticism for your customers financial statements. Remember the golden rule “ He who has the gold rules”

The use of financial statements◦ _____________________________________◦ Structuring credit facilities◦ What caused the need for cash ?? What action or lack of action caused the need for $$

Used to Identify the major Sources & Uses of Cash

To identify the underling business reasons that require the need for cash

_______________________________________ _______________________________________ Allows the loan officer to become a

consultant for their customer Meets regulatory requirements

Bankers Management, Inc.

3

Stress Variables

_______________________

_______________________

_______________________

Bankers Management, Inc.

Bankers Management, Inc.

50,000 sq./ft.: Strip shopping center - 2,500 sq./ft.: 5% Utility 47,500 sq./ft.: Rentable Space $902,500: Maximum gross rent @ $19 sq./ft. - 135,375: Vacancy 15% $767,125: Gross rental income - 35,000: Insurance - 30,000: Maintenance

4

Bankers Management, Inc.

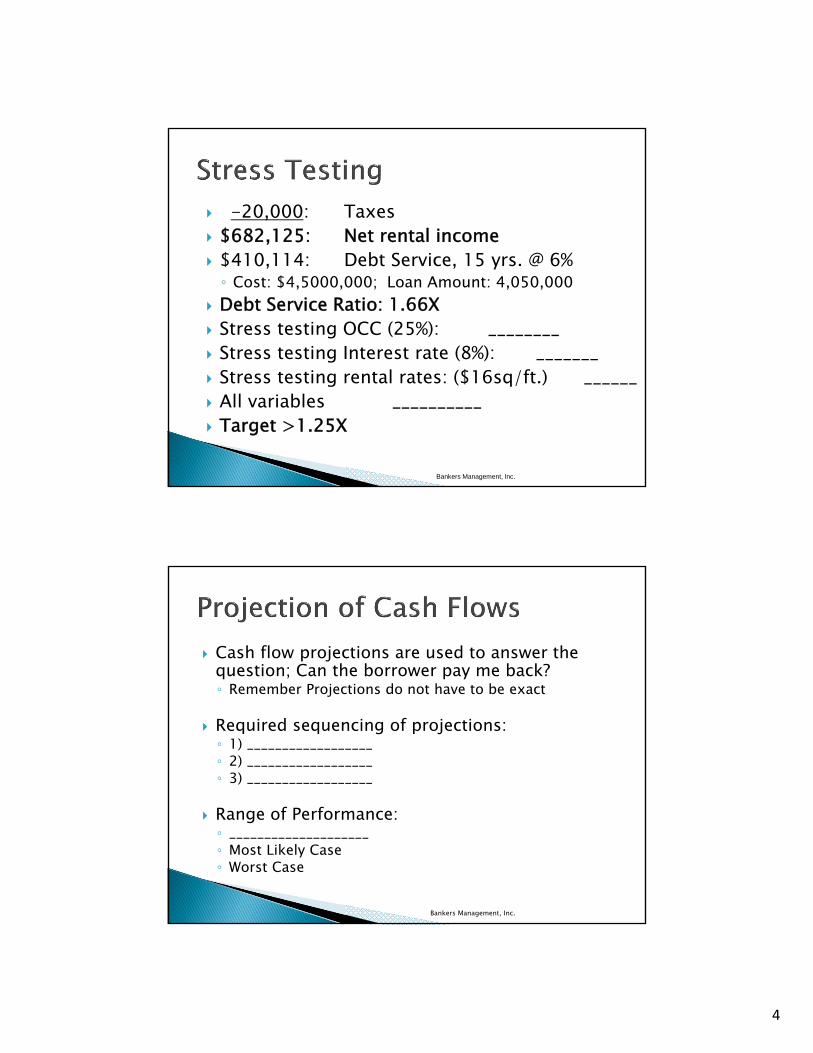

-20,000: Taxes $682,125: Net rental income $410,114: Debt Service, 15 yrs. @ 6%◦ Cost: $4,5000,000; Loan Amount: 4,050,000

Debt Service Ratio: 1.66X Stress testing OCC (25%): ________ Stress testing Interest rate (8%): _______ Stress testing rental rates: ($16sq/ft.) ______ All variables __________ Target >1.25X

Cash flow projections are used to answer the question; Can the borrower pay me back?◦ Remember Projections do not have to be exact

Required sequencing of projections:◦ 1) __________________◦ 2) __________________◦ 3) __________________

Range of Performance:◦ ____________________◦ Most Likely Case◦ Worst Case

Bankers Management, Inc.

5

Sales Gross Profit Margin Operating Expenses as a percentage of Sales Income Tax rate Turnover of Trade Accounts◦ _________________________◦ _________________________◦ _________________________

Fixed Asset Expenditures Anticipated Debt Service◦ Interest Rates

Bankers Management, Inc.

Net Cash Required:◦ If positive; cash available to service debt◦ If negative; additional cash (debt) required

Bankers Management, Inc.

6

Bankers Management, Inc.

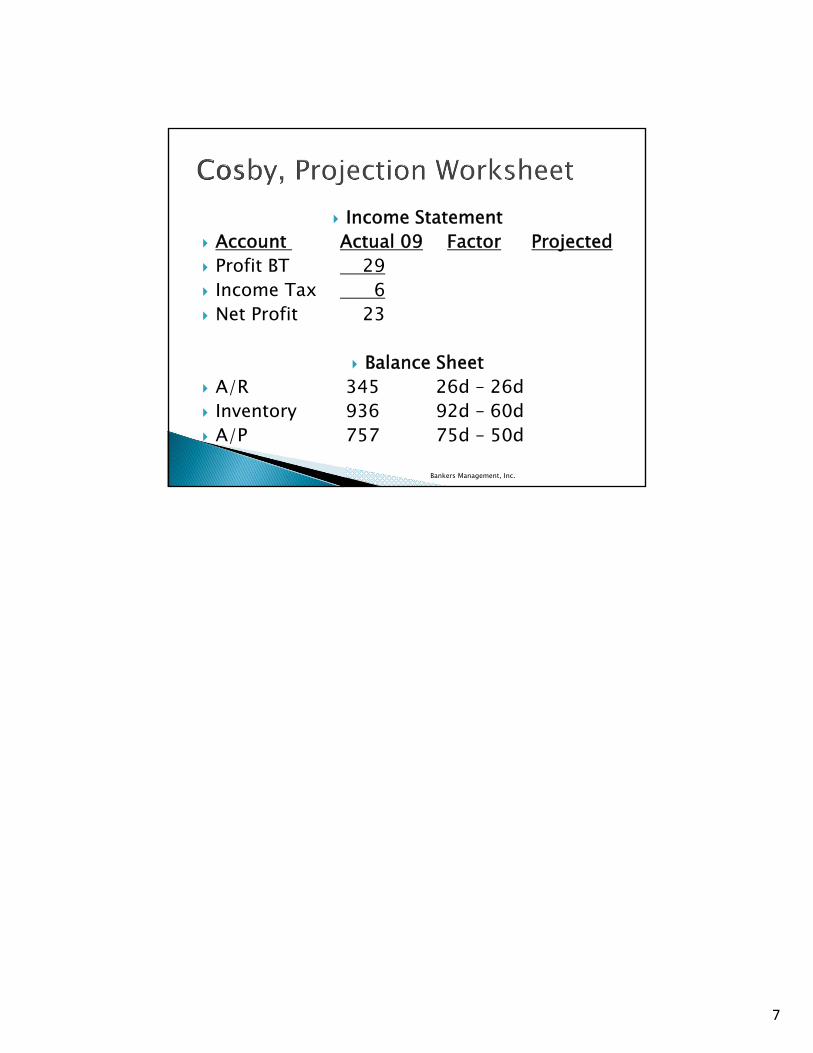

Account Interview# Assumption

Sales 4 15% COGS 5 78% SG&A 7 15% Salary Expense 6 90% Inventory 1 60 days vs. 92D Fixed Assets 8 $17,000 A/P 3 50 days vs. 75D A/R N/A 09 – 26 days

Income Statement Account Actual 09 Factor Projected Sales 4,737 x1.15 COGS 3,695 .78 x Sales Gross Profit 1,042 SG&A 109 x1.15 Depreciation 17 unchanged Total OE 993 OP 49 Interest 20

Bankers Management, Inc.

7

Income Statement Account Actual 09 Factor Projected Profit BT 29 Income Tax 6 Net Profit 23

Balance Sheet A/R 345 26d – 26d Inventory 936 92d – 60d A/P 757 75d – 50d

Bankers Management, Inc.

COSBY’S PHOTO EQUIPMENT & SUPPLIES Bill Cosby, president and sole owner of Cosby’s Photo Equipment & Supplies, has requested a $25,000 increase in his $200,000 line of credit to pay a tax payment that will soon be due. He is concerned that the company’s accounts receivable may not be collected fast enough to cover the upcoming quarterly tax payment. The Cosby family has been in the retail photo business for more than 25 years, since Fat Albert Cosby, Bill’s father and a professional photographer, first opened a store in downtown Las Vegas. The company now operated two additional stores in the Henderson, Nevada area. Ten years ago, Bill assumed the presidency and began to manage daily operations; at that time he also moved the store’s banking business to your bank. Six months later, the national economy went into a recession, and the company found itself struggling to make ends meet. As Bill tells you, “Nobody thinks about buying a camera in a recession.” Cosby’s stocks a full range of cameras, lenses, and printing supplies, and Bill is proud of this fact. He claims he carries every quality camera now on the market and says this is what has made his business successful. “If they can’t get it here, they won’t wait for me to order. They’ll just drive to Los Angeles and get it there. Photographers who have money don’t want to wait.” Most customers are experienced photographers or, as Bill says, “They want to believe they are.” According to Bill, the store services almost all the professional photographers in the area. Your discussions with some photographers you know generally confirm his story. They also tell you that you will never get a great deal there, but the price will be fair and Cosby’s will never sell you something you do not need. The sales approach is very low key. Bill hires his salespeople carefully. He looks for budding professional photographers who have to make a living while they pursue their art. Most of them work three or four days a week and do their own photography the rest of the time. Although these people may be a bit eccentric, they certainly are knowledgeable. Bill tells you the main problem with his sales staff is that they are not always patient enough with novice photographers, particularly novices who try to act like professionals.

8

Page Two When you ask Bill about how the business is run on a day-to-day basis, he replies that it generally runs itself. The sales staff can do everything on the sales floor (the new ones learn from the old), and they even set up window displays. Bill himself does all the hiring and inventory purchasing-and beyond that there is not much to do. A bookkeeper prepares monthly financial statements. The company has two loan facilities currently available. The first is the $200,000 line of credit for which the increase has been requested. The line of credit is to be used to finance accounts receivable and inventory and is renewed annually. The second facility is a term loan with annual amortization requirements of $30,000 and with $120,000 currently outstanding. The term loan was extended to provide financing for permanent working capital needs and capital expenditures.

9

Cosby’s Photo Equipment & Sales Income Statements

Years Ended October 31:

2007 (%) 2008 (%) 2009 (%) Sales $2,211,028 100.0 $3,678,613 100.0 $4,737,405 100.0 Cost of goods sold 1,729,652 2,941,281 3,695,176 Gross Profit 481,376 21.8 737,332 20.0 1,042,229 22.0 Direct Costs Salaries 307,332 529,720 772,788 Payroll taxes 26,532 45,731 66,715 Employee benefits 11,055 19,054 27,793 Total direct cost 344,919 15.6 594,505 16.2 867,296 18.3 Operating Expenses Rent 19,193 24,110 36,207 Telephone 8,121 7,999 9,632 Utilities 3,202 3,941 6,212 Insurance 13,639 17,212 18,663 Taxes and licenses 8,144 9,534 11,028 Advertising 9,541 4,117 8,627 Travel and entertainment 4,007 5,267 4,663 Auto and truck 3,488 4,214 4,737 Depreciation 3,504 5,725 16,720 Services and supplies 5,662 5,414 7,365 Interest 8,994 8,321 19,915 Other operating expenses 8,225 6,100 2,001 Total operating expenses 95,720 4.3 101,954 2.8 145,770 3.1 Income before taxes 40,737 1.8 40,873 1.1 29,163 0.6 Provision for taxes 8,435 0.4 16,223 0.4 6,500 0.1 Net Income $ 32,302 1.5 $ 24,650 0.7 $ 22,663 0.5

10

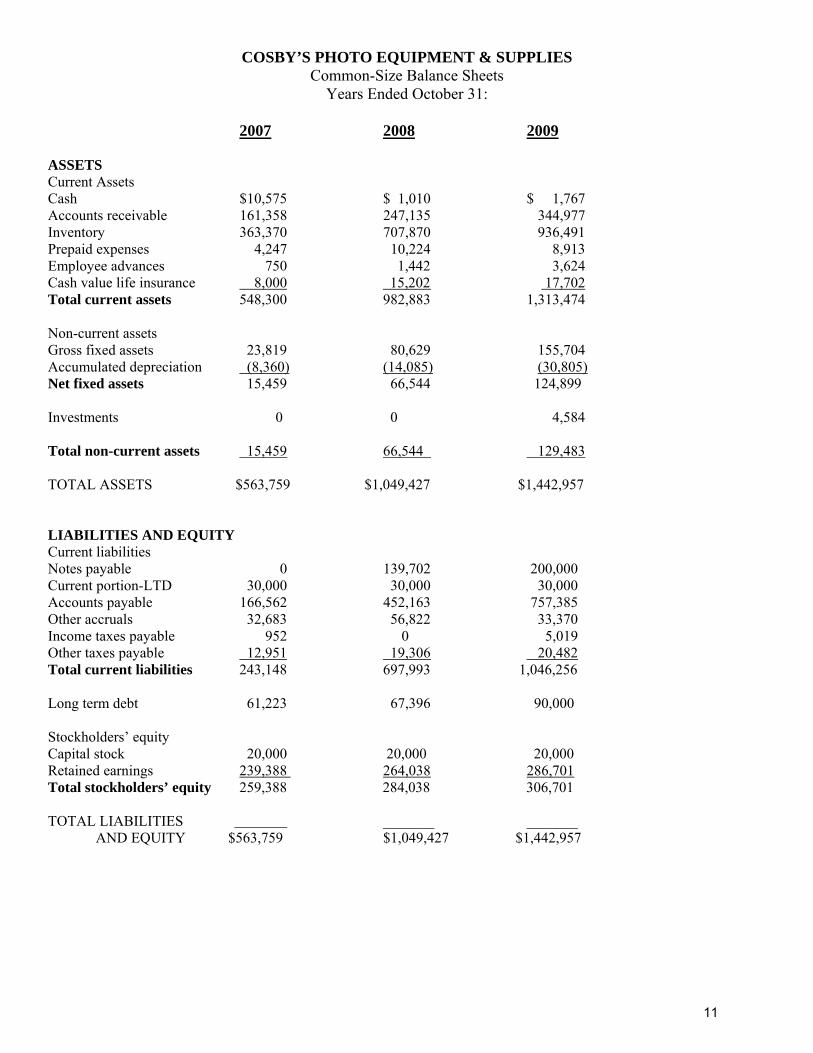

COSBY’S PHOTO EQUIPMENT & SUPPLIES Common-Size Balance Sheets

Years Ended October 31: 2007 2008 2009 ASSETS Current Assets Cash $10,575 $ 1,010 $ 1,767 Accounts receivable 161,358 247,135 344,977 Inventory 363,370 707,870 936,491 Prepaid expenses 4,247 10,224 8,913 Employee advances 750 1,442 3,624 Cash value life insurance 8,000 15,202 17,702 Total current assets 548,300 982,883 1,313,474 Non-current assets Gross fixed assets 23,819 80,629 155,704 Accumulated depreciation (8,360) (14,085) (30,805) Net fixed assets 15,459 66,544 124,899 Investments 0 0 4,584 Total non-current assets 15,459 66,544 129,483 TOTAL ASSETS $563,759 $1,049,427 $1,442,957 LIABILITIES AND EQUITY Current liabilities Notes payable 0 139,702 200,000 Current portion-LTD 30,000 30,000 30,000 Accounts payable 166,562 452,163 757,385 Other accruals 32,683 56,822 33,370 Income taxes payable 952 0 5,019 Other taxes payable 12,951 19,306 20,482 Total current liabilities 243,148 697,993 1,046,256 Long term debt 61,223 67,396 90,000 Stockholders’ equity Capital stock 20,000 20,000 20,000 Retained earnings 239,388 264,038 286,701 Total stockholders’ equity 259,388 284,038 306,701 TOTAL LIABILITIES _______ _______

AND EQUITY $563,759 $1,049,427 $1,442,957

11

COSBY’S PHOTO EQUIPMENT & SALES PROJECTION CASE

Here are the following notes you made during your meeting:

1. Bill thinks that the company can reduce inventory DOH to 60 days by the end of 2010.

2. Bill is planning to eliminate the slower-selling product lines to focus his sales efforts and inventory management on the better selling lines. He is also planning to add a small computer (costing between $5,000.00 and $10,000) to handle inventory control. The information the computer tracks will enable Cosby’s to transfer products from store to store as needed, which will reduce the necessity for full inventories at each store.

3. Bill would like to get his payables down to 50 days on hand by the end of 2010.

4. Bill thinks sales growth will slow to around 15 percent. Sales growth in the last few years has come primarily through opening new locations and the aggressive addition of new product lines. Bill plans no new store openings in 2004 but expects sales to be brisk as the local economy improves and major camera manufactures bring out highly promoted next-generation products.

5. Cost of goods sold should improve slightly, from 78 percent of sales in 2009 to 77 percent in 2010.

6. Salary expense (which is a direct cost on the income statement) should decline in 2010 to between 85 and 90 percent of 2009 levels.

7. Operating expenses, net of interest and depreciation expenses, should rise at the same rate as sales, about 15 percent annually.

8. The majority of Cosby’s fixed assets are leasehold improvements; they increased significantly in the past year because of the increase in number of locations and some new carpeting, painting, and general remodeling in the company’s retail outlets. Bill plans no major additions in the future and expects that depreciation expense will be approximately equal to new additions to fixed assets. As a consequence, net fixed assets should remain at $125,000 over the next few years.

At the end of the meeting, you tell Bill Cosby that you will call him in a few days with any follow-up questions you have after you have analyzed his needs.

12

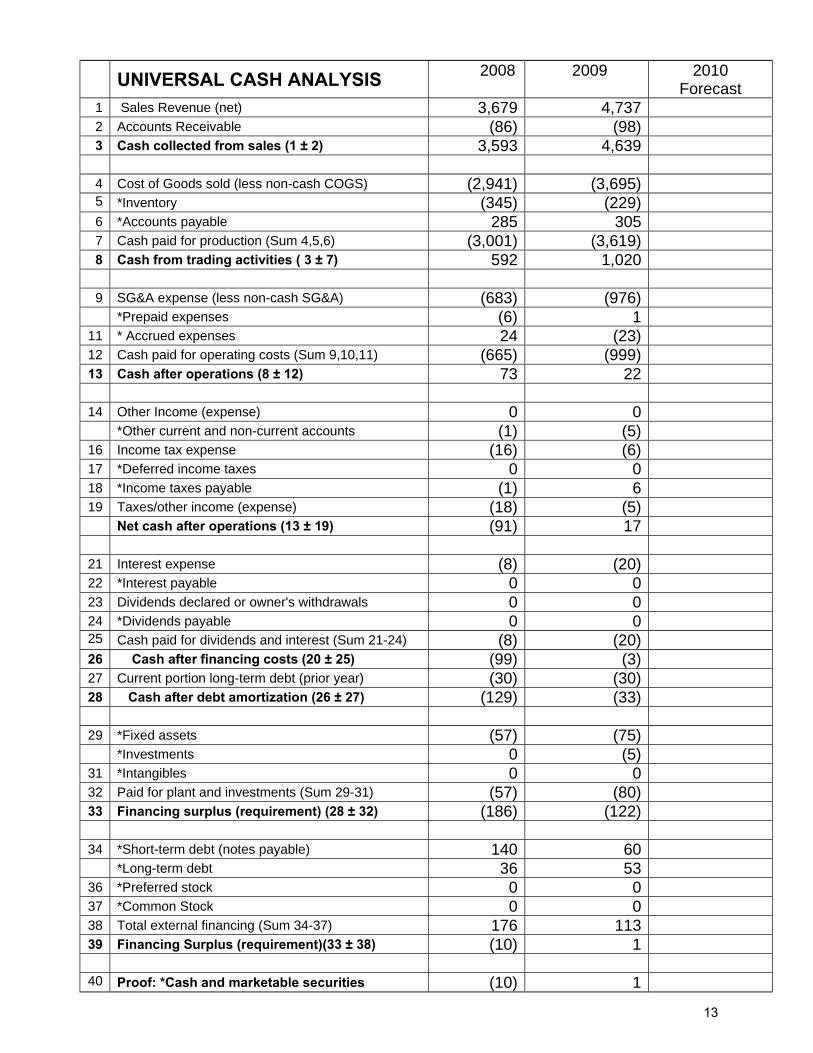

UNIVERSAL CASH ANALYSIS 2008 2009 2010 Forecast

1 Sales Revenue (net) 3,679 4,737 2 Accounts Receivable (86) (98) 3 Cash collected from sales (1 ± 2) 3,593 4,639

4 Cost of Goods sold (less non-cash COGS) (2,941) (3,695) 5 *Inventory (345) (229) 6 *Accounts payable 285 305 7 Cash paid for production (Sum 4,5,6) (3,001) (3,619) 8 Cash from trading activities ( 3 ± 7) 592 1,020

9 SG&A expense (less non-cash SG&A) (683) (976)

*Prepaid expenses (6) 1 11 * Accrued expenses 24 (23) 12 Cash paid for operating costs (Sum 9,10,11) (665) (999) 13 Cash after operations (8 ± 12) 73 22

14 Other Income (expense) 0 0

*Other current and non-current accounts (1) (5) 16 Income tax expense (16) (6) 17 *Deferred income taxes 0 0 18 *Income taxes payable (1) 6 19 Taxes/other income (expense) (18) (5)

Net cash after operations (13 ± 19) (91) 17

21 Interest expense (8) (20) 22 *Interest payable 0 0 23 Dividends declared or owner's withdrawals 0 0 24 *Dividends payable 0 0 25 Cash paid for dividends and interest (Sum 21-24) (8) (20) 26 Cash after financing costs (20 ± 25) (99) (3) 27 Current portion long-term debt (prior year) (30) (30) 28 Cash after debt amortization (26 ± 27) (129) (33)

29 *Fixed assets (57) (75)

*Investments 0 (5) 31 *Intangibles 0 0 32 Paid for plant and investments (Sum 29-31) (57) (80) 33 Financing surplus (requirement) (28 ± 32) (186) (122)

34 *Short-term debt (notes payable) 140 60

*Long-term debt 36 53 36 *Preferred stock 0 0 37 *Common Stock 0 0 38 Total external financing (Sum 34-37) 176 113 39 Financing Surplus (requirement)(33 ± 38) (10) 1

40 Proof: *Cash and marketable securities (10) 1

13