February 2018 JLL Research Report€¦ · 8 JLL Southeast Asia 2018 Outlook 9 In Malaysia, the...

15

JLL Research Report Southeast Asia 2018 Outlook February 2018

Transcript of February 2018 JLL Research Report€¦ · 8 JLL Southeast Asia 2018 Outlook 9 In Malaysia, the...

JLL Research Report

Southeast Asia 2018 Outlook

February 2018

2 JLL Southeast Asia 2018 Outlook 3

1. Economic growth accelerates, appreciatingcurrencies: The Malaysian and Indonesian economies grew faster than expected in 2017 and we expect more positive surprises from these countries in 2018. Expectations for their currencies have also improved, with most economists expecting a turnaround for MYR and IDR over the next four years.

2. We expect a strong recovery in office markets inSingapore, Jakarta: Rents fell 20-30% over last threeyears, but expected to increase 10-25% over next three years. The oversupply situation in Kuala Lumpur is being addressed, which could aid rent recovery. Technology and coworking tenants continue to expand across the region.

3. Residential prices could surprise on the upside inSingapore, Kuala Lumpur and Ho Chi Minh City.In particular, Kuala Lumpur prime residential prices are now the lowest in USD-terms in Southeast Asia, pavingthe way for recovery.

4. Infrastructure spending accelerates in Malaysiaand Indonesia: We expect the infrastructure projects, some of which are part of China’s Belt and Road Initiative, to support employment and growth. Within several Southeast Asia cities, investments in mass rapid transit are bearing fruit, with new lines and networks beingcompleted in 2016-2020, transforming the way city dwellers live, work and play.

This note highlights the key investment themes for 2018:

5. Monetary policies expected to stay neutral-to-accommodative, supportive of growth: While advanced economies are wound down monetary easing in 2017, Southeast Asian governments surprised the markets by cutting policy rates amid inflation in 2017 to boost growth. We expect real policy rates to continue to trend down marginally in 2018. Household debt to GDP in Malaysia and Thailand are also moderating.

6. REIT changes to expand capital sources in SoutheastAsia: We expect ten new REITs and potentially the first independent REIT in Thailand over the next two years. New REITs could emerge in Indonesia and Philippines subject to policy enhancements. Singapore and Malaysia REITs continue to thrive. REITs could enhance market transparency and expand capital sources for owners, potentially resulting in lower cap rates.

7. Intra-regional capital flows likely to step up:There is rising interest from Japan, China and Koreainvestors for Southeast Asia assets; while Philippines,Thai and Malaysian groups are seeking to invest within Southeast Asia.

8. Malaysia, Indonesia and Vietnam likely to continueto attract strongest capital inflow: In 2017, Malaysiawas the top receiver of capital in Southeast Asia, withUS$421million in foreign investment, followed by Vietnam and Thailand. Based on initial investigations by investors, we expect intra-regional capital flows to increase inSoutheast Asia in the coming two years.

Economic growth across the region accelerates, while expectations on currencies improve

Dec 2017 forecast Jan 2017 forecast

MYR

/USD

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.8

5.0

2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E

Fig 2: MYR/USD forecast

Source: Oxford Economics

Dec 2017 forecast Jan 2017 forecast

2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021EID

R/US

D

9,500

10,500

11,500

12,500

13,500

14,500

15,500

16,500

17,500

Fig 3: IDR/USD forecast

Source: Oxford Economics

Dec 2017 forecast June 2017 forecast

1.0

0.0

2.0

3.0

4.0

5.0 4.8

4.4

5.65.4

2.92.7

6.3 6.3

4.0 4.1

6.0

6.4

6.0

7.0

Malaysia Indonesia Singapore Vietnam Thailand Phillippines

Real

GDP

Gro

wth

%

Global growth is expected to hit 3.9% in 2018, with synchronised recovery in both advanced and emerging economies. China has stabilised its growth and has returned as a commodity buyer, which is positive for emerging markets. In Southeast Asia, the outlook for 2018 has progressively been upgraded over 2017.

Fig 1: Southeast Asia GDP growth forecast for 2018 (%)

Source: IMA Asia

Expectations for Southeast Asian currencies have also improved in the last year. Economists now expect the MYR/USD to appreciate about 10% to 3.9 by 2021, and a very mild depreciation of IDR/USD.

The strongest improvements in outlook are in Malaysia, Indonesia and Singapore. For Malaysia, the solid outlook comes from strong consumer spending on improving labour market conditions and wages. Indonesia is expected to grow faster in 2018 as the economy benefits from infrastructure investments and an accommodative monetary policy. If commodity prices recover faster than expected, it will be positive for both Malaysia and Indonesia as well.

Southeast Asia 2018 Outlook 54 JLL

Pri

me

o�

ice

re

nta

l C

AG

R

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Singapore Jakarta Kuala Lumpur Bangkok Manila

2015-2017 2018-2020

Southeast Asia 2018 Outlook 76 JLL

Our top preference is for office assets in Singapore and Jakarta for investment. Rents in these cities have fallen significantly over the last three years. Singapore rents recovered from 2Q17 and we expect office rents in Jakarta to start increasing after 2018. JLL forecast rents in Singapore’s Marina Bay to rise 23% in 2018-2020 while rents in Jakarta could rise 5-10% in 2019-2021.

We also expect capital values in Singapore and Jakarta to surprise on the upside over the next 4 years, while Kuala Lumpur and Manila capital values are expected to grow slower over the next 4 years.

Fig 4: Southeast Asia prime office rental growth

Source: JLL estimates

Strong recovery in office markets in Singapore, Jakarta for 2018-2021

Fig 5: Southeast Asia office capital values growth

Source: JLL estimates

2015-2017 2018-2020

Capi

tal v

alue

CAG

R

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Singapore Jakarta Kuala Lumpur Bangkok Manila

Office oversupply issues have been addressed across Southeast Asia In Singapore, Malaysia and Indonesia, the oversupply of office space in 2015-2017 is being addressed, providing strong foundation for rental recovery.

In Singapore, we expect office supply in the CBD to be lower from 2018, as the government is refocusing on building scale in the decentralised office hubs. In 2H17 and 1H18, there have been no CBD office sites in the government land sales programme’s confirmed or reserved lists, for the first time since 2003. We expect CBD office supply to increase by 0.6 million sq ft per annum in 2018-2023, compared to 1.4 million sq ft per annum on average in 2010-2017.

In Jakarta, the office supply glut is adding more than 600,000 sqm of grade A office space in 2017 but annual grade A supply between 2018 is and 2021 is expected to halve to average just over 270,000 sqm.

Southeast Asia 2018 Outlook 98 JLL

In Malaysia, the Cabinet has directed Kuala Lumpur City Council (DBKL) to stop issuing planning approvals of retail malls, office buildings and luxury residential projects priced over RM1 million in Kuala Lumpur, effective 1 November 2017. The moratorium could last for one to three years but the freeze on luxury condominiums could be indefinite until there is a rise in demand for luxury properties according to some Ministers. These changes were made following

concerns about an oversupply by Malaysia’s central bank. We view this as positive, since a better regulated market with policy makers that empathise with landlords and takes active steps to moderate supply imbalances would be more attractive to investors. As new initiations slow down, it is likely to boost rents and capital value expectations given healthy expected demand.

Fig 6: CBD office supply in Singapore 2010-2023E

Source: JLL estimates

0

1.00

1.50

2.00

2.50

3.00

2010 2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E 2021E 2022E 2023E

CBD

o�ic

e ne

t let

tabl

e ar

ea m

sf

2010-2017 average: 1.38

2018-2023 average: 0.63

0.50

Technology

Other

Resources/ Oil & Gas

Insurance

Financial services

Manufacturing

Pharmaceutical & FMCG

Professional services

Real estate

21%

2%

3%

6%

7%7%

32%

9%

2015-2017

47%

7%

4%

5%5% 3%

10%

8%

11%

2004-2014

13%

10 JLL Southeast Asia 2018 Outlook 11

Across Southeast Asia, financial institutions have taken up less office space in the last three years and technology firms have increased their footprint. In Singapore, financial institutions used to comprise of 50% new office take-up, but, in the last two years, they now make up 20% of new office demand while technology companies and professional services firm make up about 30% and 15% respectively.

In Kuala Lumpur, technology and consumer goods leased more office space while oil and gas leasing firms’ requirements declined. Technology firms which form only 6.9% of total leasing activities in 2013 rose to 26% in 2016-2017. In recent times, technology companies such as Huawei and Arvarto System moved into the CBD. Areas outside of CBD attracted companies such as Silverlake, Accenture, Agoda, Aecom and Google. The biggest activities were by Huawei and Google in Integra Tower and Menara 1 Sentrum respectively.

Changing office tenant profile across Southeast Asia

In Jakarta, online marketplaces, travel booking websites, fintech companies and online gaming firms remain extremely active to the extent that such firms were responsible for around 50% the space leased in 3Q17.

In Bangkok, measured in percentage terms, tech firms have grown the most rapidly over the last several years, with big names like Google, Facebook, LINE, Lazada, Huawei and JD.com all expanding, albeit from very low bases. Domestic financial institutions have also been expanding but most of them prefer to own their real estate.

ManufacturingTransport & Logistics Pharmaceutical

Oil / Petrochemicals Hi TechFinancial Services

Consumer GoodsBusiness Services

0%10%20%30%40%50%60%70%80%90%

100%

2013 2014 2015 2016 2017

Trends of New Tenants

Fig 8: New tenants in Kuala Lumpur office space 2013-2017

Source: JLL estimates

Fig 7: New tenants in Singapore office space

Source: JLL estimates

12 JLL Southeast Asia 2018 Outlook 13

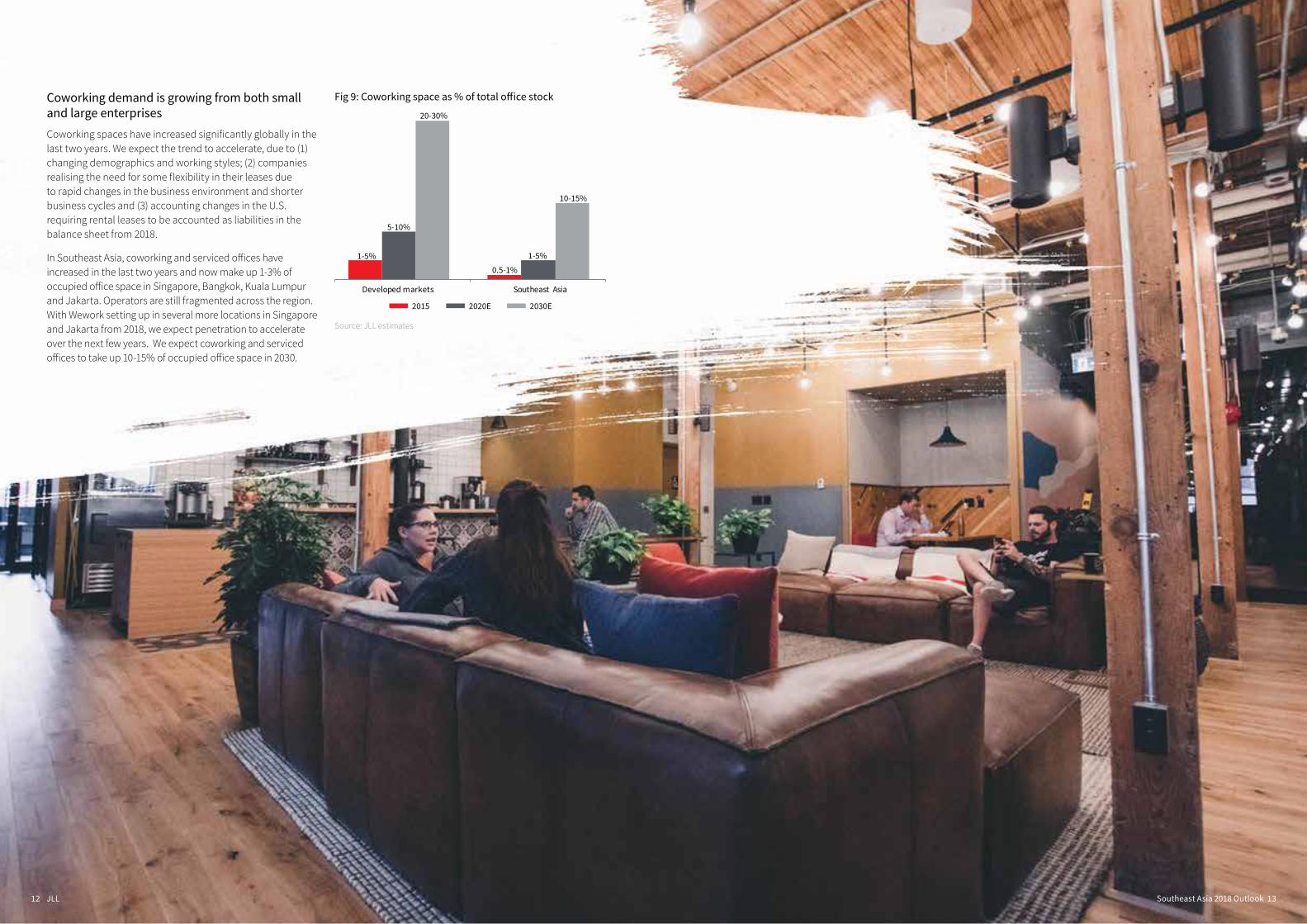

Coworking demand is growing from both small and large enterprises Coworking spaces have increased significantly globally in the last two years. We expect the trend to accelerate, due to (1) changing demographics and working styles; (2) companies realising the need for some flexibility in their leases due to rapid changes in the business environment and shorter business cycles and (3) accounting changes in the U.S. requiring rental leases to be accounted as liabilities in the balance sheet from 2018.

In Southeast Asia, coworking and serviced offices have increased in the last two years and now make up 1-3% of occupied office space in Singapore, Bangkok, Kuala Lumpur and Jakarta. Operators are still fragmented across the region. With Wework setting up in several more locations in Singapore and Jakarta from 2018, we expect penetration to accelerate over the next few years. We expect coworking and serviced offices to take up 10-15% of occupied office space in 2030.

2015 2020E 2030E

1-5%

0.5-1%

5-10%

1-5%

20-30%

10-15%

Developed markets Southeast Asia

Fig 9: Coworking space as % of total office stock

Source: JLL estimates

Southeast Asia 2018 Outlook 1514 JLL

In 2017, Kuala Lumpur residential prices surprised on the upside by rising in 3Q17. We believe the price increase is attributable to pent up demand and unsold units in the pipeline falling to a six-quarter low. Pricing could continue to rise, as they now seem very compelling against other Southeast Asian cities. The moratorium on planning approvals of luxury residential projects by DBKL is also positive for capital values outlook as supply is being constrained amid growing demand.

Singapore prime residential prices have inched up 4% over the last four quarters and rents are expected to recover in 2018 after falling for over six years. In 2017, both primary and secondary private residential sale volumes rose c. 50% yoy. As primary sales now exceed land supply from the government, developers bid aggressively for private sites to replenish their landbank and are pricing in 10-20% increase in unit prices over the next

Residential prices expected to surprise on the upside in Singapore and Kuala Lumpur

12 months in their land purchases. We expect the S$8 billion spent by developers to buy redevelopment sites to be partially recycled into the residential market in 2018, which is significant compared to the approximate S$ 16 billion in developers’ primary sales in 2017. We expect prime residential prices to rise 22% over the next four years.

Residential price growth in Manila and Bangkok fell below expectations in 2H17. We see some downside risks in our price forecasts for 2018 and 2019 given slightly lower expectations for economic growth, supply concerns and full pricing compared to incomes and other Southeast Asian cities.

KL Jakarta Manila Bangkok HCMC

2012 2013 2013 2013 2013 2014 2014 2014 2014 2015 2015 2015 2015 2016 2016 2016 2016 2017 2017 20171,500

2,000

2,500

3,000

3,500

4,000

Prim

e re

siden

tial p

rice

USDp

sm

Fig 10: Prime residential prices in emerging Southeast Asia

Source: JLL estimates

Confirmed List Reserve List New sales incl EC

0

2000

4000

6000

8000

10000

12000

14000

16000

2011 2011 2012 2012 2013 2013 2014 2014 2015 2015 2016 2016 2017 2017 20181H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H

Fig 11: Singapore primary sales vs Govt land supply

Source: JLL estimates

16 JLL Southeast Asia 2018 Outlook 17

In 2017 and 2018, Malaysia and Indonesia are accelerating their fixed capital expenditure with an increase in public infrastructure projects. On the other hand, capital expenditure in Philippines, Thailand and Singapore is slowing. Over the medium term, we expect Malaysia and Indonesia to outperform the region in infrastructure spending.

China’s Belt and Road Initiative, also known as the “One Belt One Road” (OBOR) initiative, is aimed at building the land-based “Silk Road Economic Belt” and the seagoing “21st Century Maritime Silk Road” by promoting trade, financial integration, infrastructure inter-connectivity and people-to-people exchanges among continents. We expect positive impact on industries, businessmen, farmers and even students, as China steps up investments for infrastructure projects and import more food and palm oil.

Infrastructure spending accelerates, especially in Malaysia and Indonesia

Investments in the OBOR in Southeast Asia are focused on Malaysia, Indonesia and Myanmar. China is building Indonesia’s first national high-speed rail link, spanning 150 km and costing US$5.1 billion. Talks are ongoing for a proposed USD20 billion road and railway linking Kyaukphyu, Myanmar and Kuming, China.

In Malaysia, major projects include the Malaysia-China Kuantan Industrial Park in Pahang, Melaka Gateway, East Coast Rail Link (ECRL) and Xiamen University Malaysia. These agreements were mostly trade-based and boasted a total value of US$7.22 billion or RM31.26 billion. China is now Malaysia’s top trading partner and the latter remains China’s biggest import source within the ASEAN bloc. Bilateral trade amounted to $54.3 billion in 2016, up 44.4 % year-on-year, according to the Ministry of Commerce. For the first 9 months of this year, the bilateral trade is reported about RM212.94 billion.

0

5

10

20

25

30

Malaysia Myanmar Indonesia Thailand Philippines LaosAn

noun

ced

BRI C

hina

inve

stm

ents

USD

(bill

ion)

15

Fig 13: Belt and Road Investments

Source: JLL estimates

2015 2016 2017E 2018E

Grow

th in

fixe

d ca

pita

l exp

endi

ture

6.1 6.2

9.5 9.7

-5.4

1.8

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Malaysia Indonesia Vietnam Philippines Singapore Thailand

Fig 12: Growth in fixed capital expenditure

Source: IMA Asia

18 JLL Southeast Asia 2018 Outlook 19

Southeast Asian cities are also investing in mass rapid transit (MRT), which is transformational in the way city dwellers live, work and play.

In Malaysia, the first MRT line was completed in July 2017. The 51 km-route has 31 stations and increased connectivity to the city centre. The line will serve an estimated 2 million people in the Klang Valley and transport 74,000 passengers daily. We expect any positive impact from the MRT will be more pronounced when the two other lines in the network are completed over the next few years.

Mass Rapid Transit networks are getting built across Southeast Asia

In Bangkok, the 21-station MRT Purple line opened in August 2016 and became fully connected to the network early in 2017. Together with the MRT Blue Line, BTS Skytrain network and the SRT Airport Rail Link, Bangkok’s rail-based rapid transit network now carries more than 1.1 million passengers on an average weekday. Seven new lines and extensions to existing lines are presently under construction and due for delivery between late 2018 and 2023. These new routes will add 165 km worth of new connectivity to the existing 108 km-long network. Jakarta’s MRT is under construction and will operate in 2019. Ho Chi Minh City’s first MRT is expected to operate from 2020.

Thailand Malaysia

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

1Q17

3Q17

Hou

seho

ld d

ebt t

o GD

P %

50

55

60

65

70

75

80

85

90

95

0

1

2

3

4

5

6

7

2015 2016 2017E 2018E

1

2

3

4

5

6

7

2015 2016 2017E 2018E-2

-1

0

Financial assets Debts

0

2

4

6

8

10

12

14

2013 2014 2015 2016 3Q17

Southeast Asia 2018 Outlook 2120 JLL

While advanced economies are winding down their monetary easing, Southeast Asian governments have surprised the markets by cutting policy rates to boost growth amid low inflation in 2017. Indonesia and Vietnam cut policy rates by 50bps and 25bps respectively in 2017 when analysts had expected their rates to stay flat. The Philippines and Thailand held their rates flat amid expectations of some tightening.

Monetary policies expected to stay neutral-to-accommodative to support growth

For 2018, we continue to expect policy rates to be neutral-to-accommodative, even though inflation expectations may be marginally higher. As a result, we see real policy rates trending down in most markets.

The benign interest rate environment is supportive of continued cap rate compression in Southeast Asia.

Fig 14: Policy rates in Southeast Asia (%)

Source: IMA Asia

Fig 15: Real policy rates after accounting for inflation (%)

Source: IMA Asia

Fig 16: Malaysia household assets and debt growth (%)

Source: Bank Negara Malaysia

Fig 17: Household debt to GDP (%)

The Governor of Bank Indonesia has said the central bank has plans to change down payment rules for automotive and home loans to apply differently, by regions. Last year, Bank Indonesia eased the loan-to-value (LTV) ratio requirement, lowering the minimum down payment nationally to between 15-25% from 20-40%. The central bank is also reviewing rules on loan to financing ratios, which could increase lending.

In countries where household debt levels have been high, such as Malaysia and Thailand, these have moderated over the last few years. The Malaysia’s household debt-gross domestic product (GDP) ratio has eased to 84.6% in the first quarter of 2017 from 88.4% in 2016 and the growth in households’ assets finally outstripped growth in household debt in 2017. This provides households with considerable flexibility to adjust to unexpected changes in income or expenditures. This might also lead to more flexibility for relaxations on LTV and loan approvals.

Malaysia Indonesia Philippines Thailand Vietnam

Southeast Asia 2018 Outlook 2322 JLL

REITs to expand capital sources in Southeast Asia

In several countries across Southeast Asia, more assets are being securitised into real estate investment trusts (REITs), driven by policy changes and growing investor interest. This is a positive trend, as it expands capital sources for asset owners beyond banks. As more assets are held in listed REITs, transparency on occupancy, rents, valuation and capitalisation rates are likely to help narrow bid-ask spreads, potentially resulting in more transactions. REITs that trade well should also be able to raise new equity and potentially new debt instruments including bonds and medium term notes, in addition to bank loans. Over the medium term, it could lead to more competitive loan spreads and tighter capitalisation rates for assets.

Since being introduced in 2014, 14 REITs have launched in Thailand with total market capitalisation as at end-November 2017 of USD 2.6 billion. We believe at least ten new REITs are planned for launch over the next 12-18 months as well as several potential REIT conversions (from the previous property fund structure) and planned capital injections. To date, all existing REITs have been developer / owner sponsored. We expect 2018 will herald the arrival of the first independent REITs with no developer / owner sponsorship.

In Indonesia, the release of the government’s eleventh economic policy package in 2016 detailed plans to encourage the formation of locally listed REITs (DIRE) by bringing taxes more in line with established REIT markets such as Singapore. The central government lowered income tax on REITs from 5% to 0.5% and issued a directive to local governments to reduce acquisition duty of rights on land and buildings (BPHTB) from 5% to maximum 1%. The implementation of the latter may vary throughout the archipelago. While no new REIT listings have resulted since the regulations were announced, these could happen gradually as several developers expressing interest in Indonesian REITs.

In 2017, the Philippines government has reopened debates on taxation and free float requirements to facilitate the formation of REITs in the country.

Singapore and Malaysia already have thriving REIT markets. The Singapore REIT market continues to attract assets globally, including the listing of a new US office REIT and a new European commercial REIT in 2017.

expand

24 JLL Southeast Asia 2018 Outlook 25

In 2017, Malaysia was the top receiver of capital in Southeast Asia, with US$421 million in foreign investment, followed by Vietnam and Thailand. The main foreign investors in Southeast Asia came from China, with c.US$465 million of investment in Malaysia, Indonesia and Vietnam. Vietnam is also a key market for foreign capital in 2017, with smaller investment tickets and mainly focused on residential projects.

Moving forward, we expect Malaysia, Indonesia and Vietnam to continue to be the top 3 target markets for international investors. There is increasing appetite from Japanese, Korean investors in addition to interest from Chinese and Singaporean investors.

Intra-regional capital flows have been low within Southeast Asia over the last decade. Singapore remains the largest cross-border investor in Southeast Asia. In 2017, the only non-Singapore transaction is the sale of the Pullman Hotel by the Indonesian developer Agung Podomoro to the Thai-listed SHREIT. However, based on investor feedback and initial investigations, we expect intra-regional activity to increase, even as investors from Singapore continue to invest in the region.

Intra-regional capital flows likely to step up over the next few years

Fig 18: Foreign Capital Inflows (2017)

Note: no capital inflows data reported in the Philippines as it is mainly a market for domestic investors Source: RCA

Fig 19: Capital Source by Countries (2017) Fig 20: Capital Inflows by Sector 2017

Source: RCA Source: RCA

China Hong Kong Japan South Korea Taiwan The US

50

100

150

200

250

450

300

400

350

The PhilippinesIndonesiaMalaysia Vietnam Thailand

In U

S$ m

illio

n

Total: US$1,476 million

China

Japan

The US

Hong Kong

South Korea

Taiwan

Total:US$1,476 million 31%

29%

3%6%

13%

18%

Total:US$1,476 million

20%

19%

7%

7%

26%

Land plot Residential Retail

21%

O�ice Industrial Hotel

Fig 21: Intra-Regional Capital Flows (2017)

Source: RCA

Singapore Thailand

300

400

500

600

MalaysiaIndonesia Vietnam Thailand

In U

S$ m

illio

n

Total: US$847 million

0

200

100

26 JLL

Australian developer Logos announced their first project in Indonesia earlier in 2017 – the group plans to develop a 155,000 sqm, three tier warehouse in Bekasi, Greater Jakarta and Mega Manunggal Property (MMP), with whom GIC are partnered with, also has several developments in the pipeline. The relatively lack of high specification, modern logistics warehouse space and strong occupier demand is likely to mean that this emerging sector remains very much on the radar for investors and developers in 2018.

In Vietnam, the supply of industrial and logistics assets has not changed much during the last few years. Compared to its regional peers, Vietnam’s current supply is remarkably lower, resulting in good room for growth in this market. Additionally, Vietnam’s high-specification warehouse/factory space is still relatively less competitive compared to the average specification warehouse/factory space in Thailand, China (YDR) and Singapore. As the Vietnam market evolves, specific areas of opportunity are beginning to emerge as it develops a more intermediate product and value added offering. Moving from more labour intensive to more capital intensive and automated resources, JLL anticipates that industrial facilities will become more sophisticated as occupier requirements develop.

Approximately 38,461 ha of additional land is planned for industrial growth until 2020, nearly double the current market size. Given Vietnam’s promising economic prospects, it is expected that Vietnam will witness strong manufacturing growth in the near future particularly as its regional peers tend to shift away from the early stages to more mature industrial development. Thus, huge opportunities exist in the Vietnam market for both existing players and potential new market entrants to access potential land bank and capture market share.

Logistics continues to attract strong investor interest in the region.

Continued strong interest in industrial and logistics assets

Authors

Regina Lim

Head of Capital Markets Research, Southeast [email protected]

With contributions from:

Kieran O’FlynnSoutheast Asia Capital Markets

Veena LohHead of Research JLL Malaysia

James TaylorHead of Research JLL Indonesia

Tay Huey YingHead of Research JLL Singapore

Andrew GulbrandsonHead of Research JLL Thailand

Le TrangHead of Research JLL Vietnam

jll.com© 2018 All rights reserved. The information contained in this document is proprietary to JLL and shall be used solely for the purposes of evaluating this proposal. All such documentation and information remains the property of JLL and shall be kept confidential. Reproduction of any part of this document is authorized only to the extent necessary for its evaluation. It is not to be shown to any third party without the prior written authorization of JLL. All information contained herein is from sources deemed reliable; however, no representation or warranty is made as to the accuracy thereof.