FCE Bank plc ANNUAL REPORT AND ACCOUNTS...FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 7 The...

100

FCE Bank plc ANNUAL REPORT AND ACCOUNTS for the year ended December 31, 2006

Transcript of FCE Bank plc ANNUAL REPORT AND ACCOUNTS...FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 7 The...

FCE Bank plcANNUAL REPORTAND ACCOUNTSfor the year ended December 31, 2006

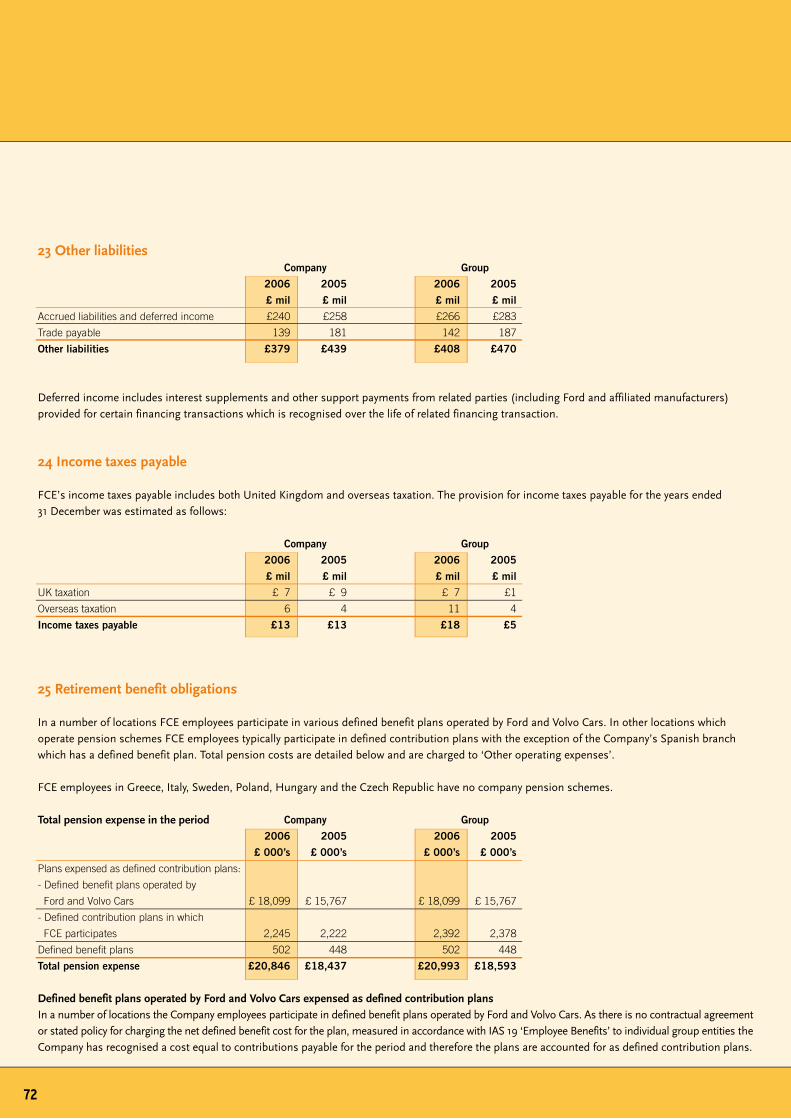

FCE Bank plc is an indirect wholly owned subsidiary of Ford. The Company and its subsidiaries are the automotive financial services arm of Ford in Europe and employ around 2,800 people who provide automotive finance and services to dealers, retail and fleet customers in

19 European countries. Our mission is to support the sales of Ford automotive brands in Europe (Ford, Jaguar, Land Rover, Mazda, and Volvo) while returning value to our shareholder. The Company typically operates as a secured lender in the financing products provided.

Contents

www.fcebank.com

FCE Bank plc. Central Office, Eagle Way, Brentwood, Essex CM13 3AR. Registered in England and Wales no 772784

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006

Current Directors 4

Definitions 4

Ten year financial highlights 5

The Chairman’s statement 6

Annual report of the Directors 8

Directors’ responsibilities for financial statements 13

Strategy and performance summary 14

Risk management 18

Corporate governance 21

Independent auditors’ report to the members of FCE Bank plc 26

Consolidated income statement 27

Statement of total recognised income and expense 27

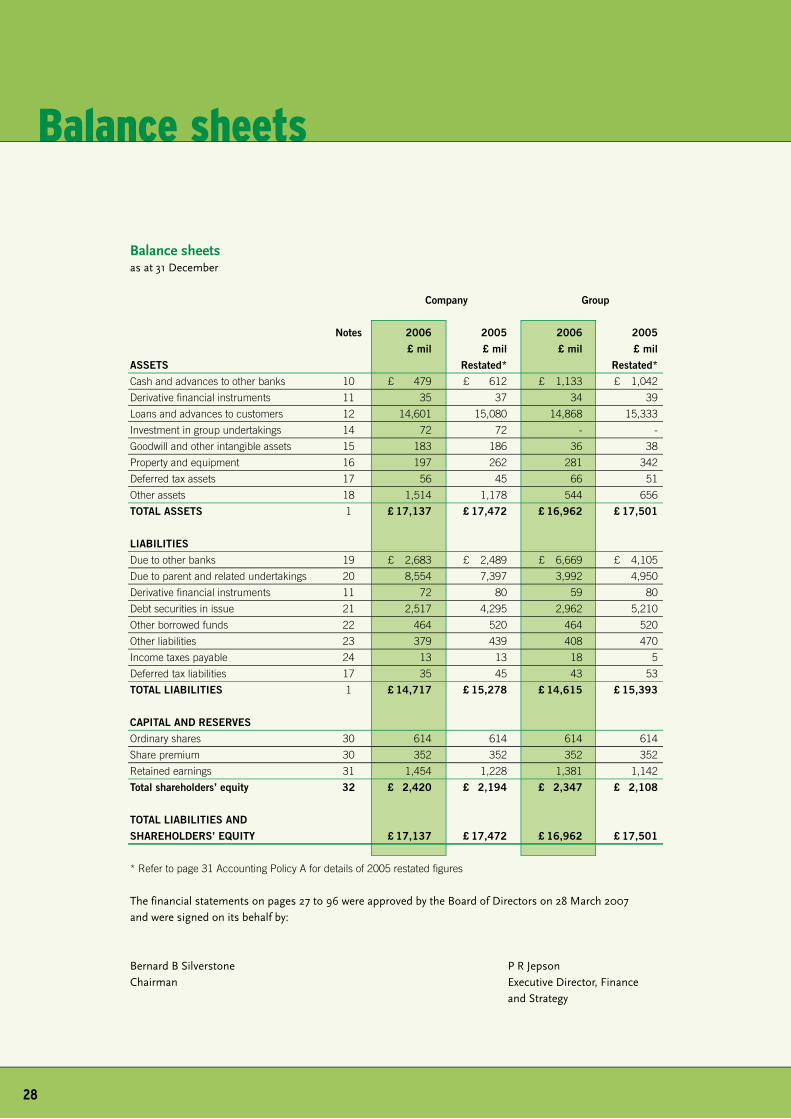

Balance sheets 28

Cash flow statements 29

Accounting policies 30

Notes to the financial statements 43

Web site addresses 97

European operating locations 97

3

Current Directors

Chairman B B Silverstone

Managing Director, Britain J Coffey

Executive Director, Global Operations and Technology N J Falotico

Executive Director, Finance and Strategy P R Jepson

Executive Director, European Sales Operations M E Ribits

Managing Director, Germany R N Rothwell

Director J Noone

Director A Vandenplas

Non-Executive Director C A Bogdanowicz-Bindert

Non-Executive Director R A Corbello

Non-Executive Director M F Robinson

Non-Executive Director A K Romer-Lee

Non-Executive Director C Toner

Secretary C V Rogoff

Registered office Central Office

Eagle Way

Brentwood

Essex CM13 3AR

United Kingdom

Auditors PricewaterhouseCoopers LLP

Chartered Accountants

and Registered Auditors

Southwark Towers

32 London Bridge Street

London SE1 9SY

DefinitionsFor the purpose of this report (with the exception of the Independent Auditors’ report) the term(i) ‘Company’ means FCE Bank plc. and its European branches(ii) ‘Group’, ‘FCE’, ‘we’, ‘us’ or ‘our’ means the Company, its European branches and subsidiaries(iii) ‘FMCC’ means Ford Motor Credit Company, an indirect wholly owned subsidiary of Ford(iv) ‘Ford’ means Ford Motor Company, the Companys ultimate parent company(v) ‘FCI’ means Ford Credit International, Inc. a subsidiary of FMCC and the Company’s immediate shareholder

�

Current Directors / Definitions

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006

Profit before Tax £ Millions

370

323

229216

172178

264

245226222

0

50

100

150

200

250

300

350

400

1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5

UK GAAP IF RS

0

50

100

150

200

250

300

350

400

02468

101214161820

0200400600800

100012001400160018002000

0

50

100

150

200

250

300

350

400Profit before Tax £ Millions

370

323

229216

172178

264

245226222

0

50

100

150

200

250

300

350

400

1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5

UK GAAP IF RS

0

50

100

150

200

250

300

350

400

02468

101214161820

0200400600800

100012001400160018002000

0

50

100

150

200

250

300

350

400Profit before Tax £ Millions

370

323

229216

172178

264

245226222

0

50

100

150

200

250

300

350

400

1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5

UK GAAP IF RS

0

50

100

150

200

250

300

350

400

02468

101214161820

0200400600800

100012001400160018002000

0

50

100

150

200

250

300

350

400

400

350

300

250

200

150

100

50

0

226245

264

178 172

216229

329

356

UK GAAP

IFRS

UK GAAP

IFRS

Profit before Tax £ Millions

Total Assets£ Billions

Retail and Lease Contracts Outstanding000's

20

16

14

10

8

6

4

2

0

18

12

10.9

12.4 12.413.7

16.317.6

19.3 18.617.5

1,4031,487

1,5711,635

1,701 1,7371,659

1,522

1,359

2,000

1,600

1,400

1,000

800

600

400

200

0

1,800

1,200

329

200520042003200220012000199919981997 2006

200520042003200220012000199919981997 2006

200520042003200220012000199919981997 2006

17.0

1,245

5

Ten year financial highlights

6

The Chairman’s statement

I am pleased to announce that FCE achieved pre-tax profits of

£329 million in 2006. Although this is down £27 million from the

prior year it represents strong performance in a highly competitive

market. Exceptional items represented a £8 million decrease to

profits compared to a £34 million increase to profits in 2005 as

detailed in Note 8 to the accounts, ‘Profit before tax’

Overall FCE’s asset levels were at approximately the same level as

2005 and were well diversified by both market and automotive brand.

The retail portfolio continues to perform in line with the risk profiles

established for origination activities and is reflected in the near to

historically low loss levels being experienced. We are continuing to

invest in improving the data foundations and in enhancing risk

modelling capabilities. By maintaining a disciplined cycle of refresh

to our risk models we can be confident of continued dependable and

predictable portfolio performance.

The Company’s credit rating is linked to those of our parent company,

FMCC, which were lowered during 2006. However in July 2006,

Standard & Poor’s, a leading provider of independent credit ratings,

assigned to the Company a rating one notch higher than FMCC. The

Company has continued its European Medium Term Note programme

and resumed issuance under the programme at the beginning of

2007. To date in 2007 we have completed two large unsecured debt

transactions for Euro 1 billion and £750 million respectively. While

continuing to access the unsecured debt market, FCE has also increased

its use of securitisation and other asset-backed sources of funding

as these channels are presently more cost effective than unsecured

funding and provide access to a broad investor base. In 2006 FCE

launched a record number and value of securitisation transactions.

New Jaguar XKFord Transit Van Of The Year 2007 New Volvo C30 at 2006 Paris Motor Show

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 7

The completion of the five year programme to outsource FCE’s

full-service lease business in 12 markets in Europe is an example of

an alternative business model which also reduces FCE’s funding

requirements. FCE’s leasing product is now consistently branded as

“Business Partner” and is a fee-based, non-equity model that supports

Ford’s vehicle sales. FCE also has a well established automotive

insurance business through which we are able to provide a valuable

customer offering by partnering with leading insurance providers

and receive fees without exposure to the insurance risk.

Common IT applications and business processes are at the centre of

FCE’s drive to minimise its operating costs ensuring consistency in

the quality of service provided to our customers throughout Europe.

The wholesale financing system, which enables FCE to manage a

dealer’s inventory financing was introduced into our German operations

in 2006 and is now used by every FCE location in Europe. Our principal

platform for retail financing is operated in 17 of our 19 locations.

While in Britain and Germany we leverage a shared technology

platform with our US parent that provides appropriate scale and

economics for our two largest operations.

Thanks to the hard work and dedication of our employees we

accomplished a great deal in 2006 delivering strong profits while

supporting the sales of vehicles by our automotive partners. Our

close working relationship with both the automotive marketing and

sales organisations and the dealer network remains key to our

success. We continue to focus on new and innovative ways to support

vehicle sales through targeted offers that provide funding and

services to our customers at the time when they are in market. We

were particularly pleased to be able to support the launch of the

new Transit and the all new S-MAX, which were awarded 2007 Van

Of The Year and 2007 Car Of The Year respectively. The coming

year will no doubt be another challenging one, but with exciting new

products from our automotive partners such as the Ford Mondeo,

Volvo C30, Land Rover Freelander 2, and Mazda CX7, we are well

placed to achieve our goals.

Bernard B Silverstone

Chairman, FCE Bank plc.

28 March 2007

New Ford Mondeo New Land Rover Freelander 2 New Mazda CX7

Ford S-MAX Car Of The Year 2007

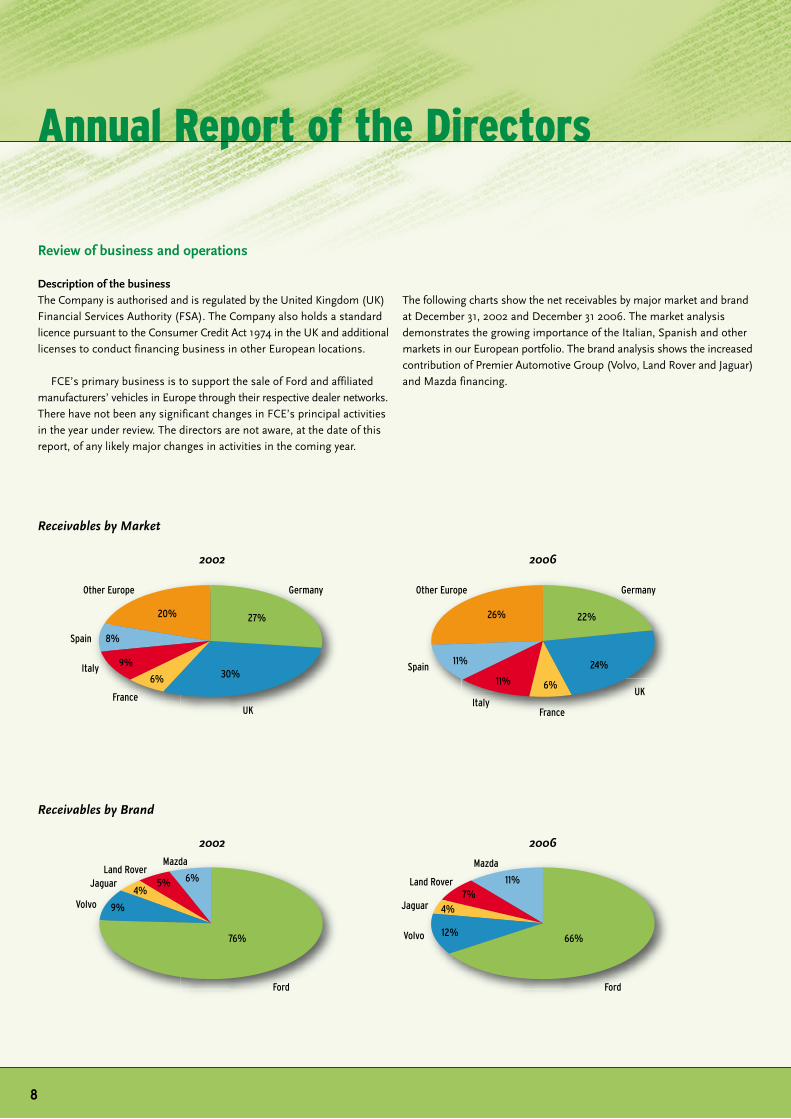

Germany

UKFrance

Italy

Spain

Other Europe

27%

30%6%

9%

8%

20%

Receivables by Market

UK

Germany

FranceItaly

Spain

Other Europe

22%

66%

6%11%

11%

26%

2002 2006

2002 2006

Receivables by Brand

Review of business and operations

Description of the businessThe Company is authorised and is regulated by the United Kingdom (UK) Financial Services Authority (FSA). The Company also holds a standard licence pursuant to the Consumer Credit Act 1974 in the UK and additional licenses to conduct financing business in other European locations.

FCE’s primary business is to support the sale of Ford and affiliated manufacturers’ vehicles in Europe through their respective dealer networks. There have not been any significant changes in FCE’s principal activities in the year under review. The directors are not aware, at the date of this report, of any likely major changes in activities in the coming year.

The following charts show the net receivables by major market and brand at December 31, 2002 and December 31 2006. The market analysis demonstrates the growing importance of the Italian, Spanish and other markets in our European portfolio. The brand analysis shows the increased contribution of Premier Automotive Group (Volvo, Land Rover and Jaguar) and Mazda financing.

Ford

Jaguar

Volvo

Land Rover

Mazda

12%

11%7%

4%

76%

Ford

Volvo 9%

24%

JaguarLand Rover

Mazda

6%5%4%

Annual Report of the Directors

�

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 �

FCE provides a variety of retail, leasing and wholesale finance plans in the markets in which they operate. Retail financing is provided predominately through a number of title retention plans, including conditional sale, hire purchase and instalment credit loans. Operating and finance leases are provided to individual, corporate and other institutional customers, covering single vehicles as well as large and small fleets. In most markets operating leases are provided by business partners to whom FCE has outsourced certain functions whilst retaining responsibility for marketing and sales in return for fee income (see opposite under Full Service Leasing). FCE provides a variety of vehicle wholesale plans to dealers and in addition, loans for working capital and property acquisitions.

FCE also offers distinctive branded insurance products in partnership with local insurance providers. It distributes these products primarily through Ford, Jaguar, Land Rover, Mazda and Volvo dealerships in many European markets. Insurance is a fee-based, non-equity business for FCE. High loyalty rates mean that insurance continues to encourage repair work into franchised dealer body shops, as all policies require original manufacturer parts for repairs. Payment protection policies are sold in many European markets providing additional security to customers.

In addition to operating in the UK, the Company operates branches in 15 other European countries and has subsidiaries in the Czech Republic, Finland (where also it has a branch); Hungary, Poland and the UK (see Note 14 ‘Investment in group undertakings’). Other than the UK the main operations are in the EU focused in France, Germany, Italy and Spain. The European branches and subsidiaries of the Company have established additional finance facilities and associated trading styles primarily for Ford affiliated manufacturers in Europe which are detailed within the European operating locations listing on pages 97 and 98.

The Company’s Worldwide Trade Financing (WTF) division provides finance to distributors and importers in countries where typically there is no established local Ford presence. WTF currently provides finance in over 70 countries. In addition there are private label operations in some European markets.

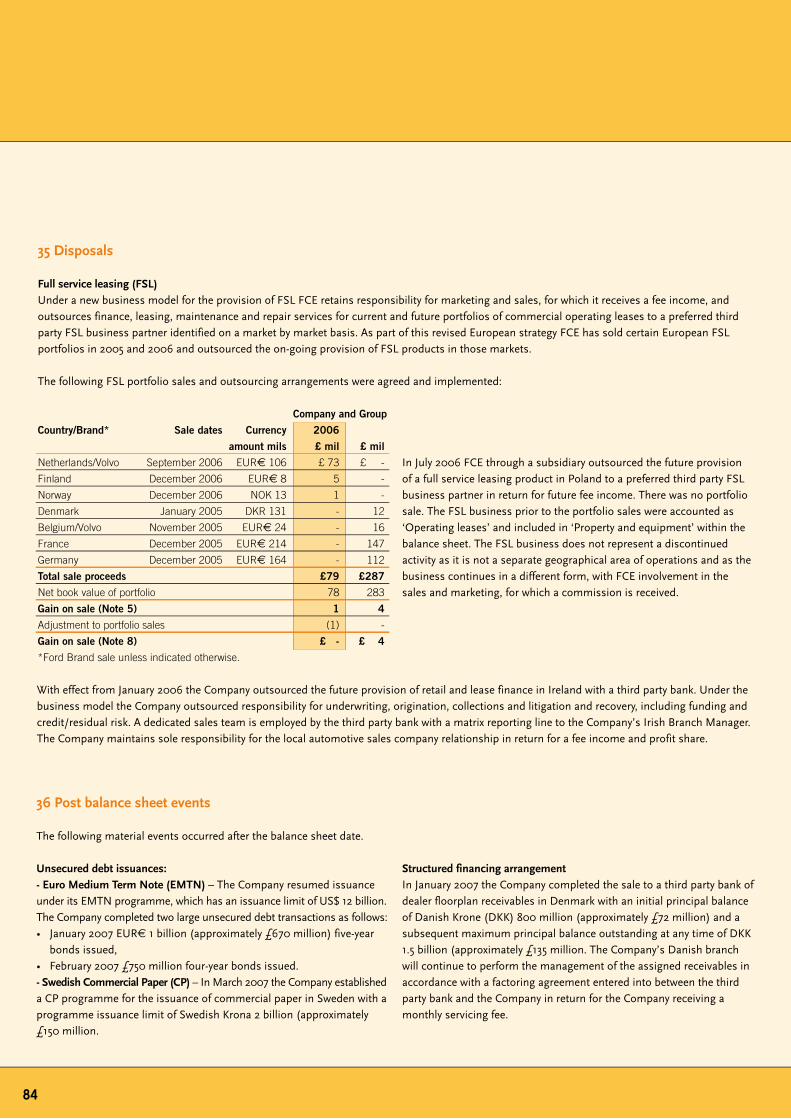

Disposals

Full service leasingUnder our business model for the provision of full service leasing products (FSL) FCE retains responsibility for marketing and sales, for which it receives a fee income, and outsources finance, leasing, maintenance and repair services for current and future portfolios of commercial operating leases to a preferred FSL business partner identified on a market by market basis. This business model ensures that the outsourced operations will deliver a more competitive product and will continue marketing support for Ford and affiliated manufacturers. In line with this strategy, FCE has sold certain European FSL portfolios and outsourced the on-going provision of FSL products in those markets in the future. For further information on transactions completed in 2006 please see Note 35 ‘Disposals’ on page 84.

IrelandOn 23 December 2005 FCE agreed, with effect 3 January 2006, to outsource future provision of retail and lease finance in Ireland to a third party bank. For further information please see Note 35 ‘Disposals’ on page 84.

FCE continues to review its operations to identify alternative business structures and other opportunities to generate non-equity business.

Funding

During 2006 FCE continued to meet a significant portion of its funding requirements through sales of receivables taking advantage of the stability of the market for asset-backed securities. Asset-backed funding has lower relative costs compared to unsecured debt and provides further diversity of funding. In doing so we utilised a variety of both amortising and revolving structures as well as other forms of structured financing and factoring. For further information see Note 13: ‘Sales of Receivables and Related Financing’. Accordingly, we raised GBP 752 million of funding through the sale of wholesale automotive receivables in Belgium, the Netherlands and Germany. Also during the year, we raised GBP 1,122 million through the sale of retail automotive receivables in Belgium, Germany, the Netherlands and Spain, and approximately GBP 1,198 million through the sale of retail automotive receivables in the UK. Further securitisation transactions are planned during 2007.

In addition, FCE raises funds through local bank borrowing, private and public debt offerings and the issuance of commercial paper.

Share Capital

There was no change to the issued share capital of the Group during the year.

In December 2006 the Company received a capital contribution of US$ 75 million (2005 US$ 49 million) from its shareholder to be used solely to make a payment to Jaguar Cars Limited in return for use of group tax relief. For further information see Note 31 ‘Retained earnings and other reserves’.

Post balance sheet events

Refer to Note 36 ‘Post balance sheet events’.

Results and dividends

The directors did not declare any dividends during 2006 and do not recommend the payment of a final dividend (2005: none). The profit for the year of £231 million will be transferred to the Group’s reserves.

Future Outlook

For future prospects and key performance indicators please see the Strategy and Performance section starting on page 14.

Principal risks and uncertainties

The Risk Management section which starts on page 18 details the risks that FCE is exposed to during the normal course of business and the processes in place to manage those risks. The principal external business risks and uncertainties facing FCE which are not already included in the Risk Management section are itemised below:

FCE’s business is substantially dependent upon the sale of Ford and affiliated manufacturers’ vehicles in Europe and its ability to offer competitive financing on those vehicles. The automotive industry is highly competitive. Sales of Ford and affiliated manufacturers’ vehicles could decline if Ford is unable to respond to price pressure in the industry.

The provision of finance in Europe is highly competitive, and FCE must compete effectively with other providers of finance. Ford in Europe currently provides a number of marketing programmes that employ financing incentives to generate increased sales of vehicles. These financing incentives generate significant business for FCE. If Ford chose to shift the emphasis from such financing incentives, this could impact FCE’s share of financing related to Ford vehicles.

The credit ratings of FCE and FMCC have been closely associated with the rating agencies’ assessments of Ford. The lower credit ratings assigned to FCE and FMCC over the past several years are primarily a reflection of the rating agencies’ concerns regarding Ford’s automotive cash flow, profitability, market share, and health care and post-retirement benefit plan costs, as well as the potential impact on Ford of market factors such as excess industry capacity and industry pricing pressure. Lower credit ratings generally result in higher borrowing costs and reduced access to capital markets.

A future inability to access debt or securitisation markets at competitive rates or in sufficient amounts due to additional credit rating downgrades or other reasons or the withdrawal of existing liquidity facilities (such as bank committed lines of credit) or Ford intra-group lending may reduce the amount of receivables FCE could purchase and adversely affect profitability and volume.

10

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006

Annual Report of the Directors

11

Directors

The full list of present directors is shown on page 4. Mr. Corbello resigned as Chairman of the Board effective 1 June 2006 upon his retirement from the Ford organisation. Mr. Silverstone was appointed as Chairman of the Board with effect the same date. Mr. J Moynes resigned as a director with effect 1 July 2006. Ms. Falotico and Mr. Ribits were appointed as directors effective 21 July 2006. Mr. Corbello and Mr. Romer-Lee were appointed as additional Non-Executive Directors effective 1 August 2006 and 1 October 2006 respectively. Mr. Thomson resigned as a Non-Executive Director and Chairman of the Audit Committee effective 31 December 2006. Mr. A Vandenplas was appointed as a director effective 28 March 2007. For details on the attendance record of Non-Executive Directors please see the section entitled Corporate Governance on page 21.

With the exception of Mr. Noone, Mr. Vandenplas and the five current Non-Executive Directors, Mrs. C A Bogdanowicz-Bindert, Mr. Corbello, Mr. M Robinson, Mr. Romer-Lee and Mr. C Toner, all directors are employees of the Company. Mr. Noone is employed elsewhere within Ford.

Mrs. C A Bogdanowicz-Bindert is a Non-Executive Director of McBride plc. She was previously a Non-Executive Director of BPH Bank, PBK Bank and Bank Gdanski before which she worked in various senior positions at Lehman Brothers and the International Monetary Fund.

Mr. Corbello is former Chairman of FCE up until June 2006, former Vice President of FMCC and Executive Vice President Ford Credit International, Inc and previously held various other senior posts with FMCC.

Mr. Robinson is a former Regional Managing Director at National Westminster Bank plc with whom previously he had held various other senior management posts including being Head of Streamline Merchant Services and Head of Card Services.

Mr. Romer-Lee is a Non-Executive Director of Sonali Bank (UK) Limited and was formerly a partner of PricewaterhouseCoopers LLP, where he was Head of Financial Services, Central & Eastern Europe and with whom he previously held various other senior management posts.

Mr. Toner has been Non-Executive Chairman of Barratt Developments plc since October 2002, having previously been Non-Executive Vice Chairman, former Deputy Group Chief Executive of Abbey National plc and former Deputy Chairman of NHBC.

In accordance with the Articles of Association all directors will seek re-appointment at the Annual General Meeting to be held on 28 March 2007.

None of the directors have a beneficial interest in the share capital of the Company. The executive directors hold shares in and/or options over shares in Ford – for further details please refer to Note 6 ‘Other operating expenses’.

Going concern

The Directors are confident in making the formal going concern statement that they have a reasonable expectation that the Company has adequate resources to continue in existence for the foreseeable future. For this reason the directors believe it is appropriate to continue to adopt the going concern basis in preparing these accounts.

Payments to suppliers

FCE does not operate a standard payment policy as each location is responsible for agreeing terms of payment in accordance with the conditions of the order. We seek to abide by the payment terms agreed with suppliers whenever it is satisfied that the supplier has provided the goods or services in accordance with the agreed terms and conditions.

The ratio, expressed in days, between the amounts owed by FCE to trade creditors at the end of the year and the amounts invoiced by suppliers in the year ended 31 December 2006 is 45 days (2005: 45 days).

Changes in fixed assets

Movements in fixed assets are as disclosed in Note 15 ‘Goodwill and other intangible assets’ and Note 16 ‘Property and equipment’ on pages 64 and 65 respectively.

Donations

FCE made no charitable or political donations during the year under review.

Pensions

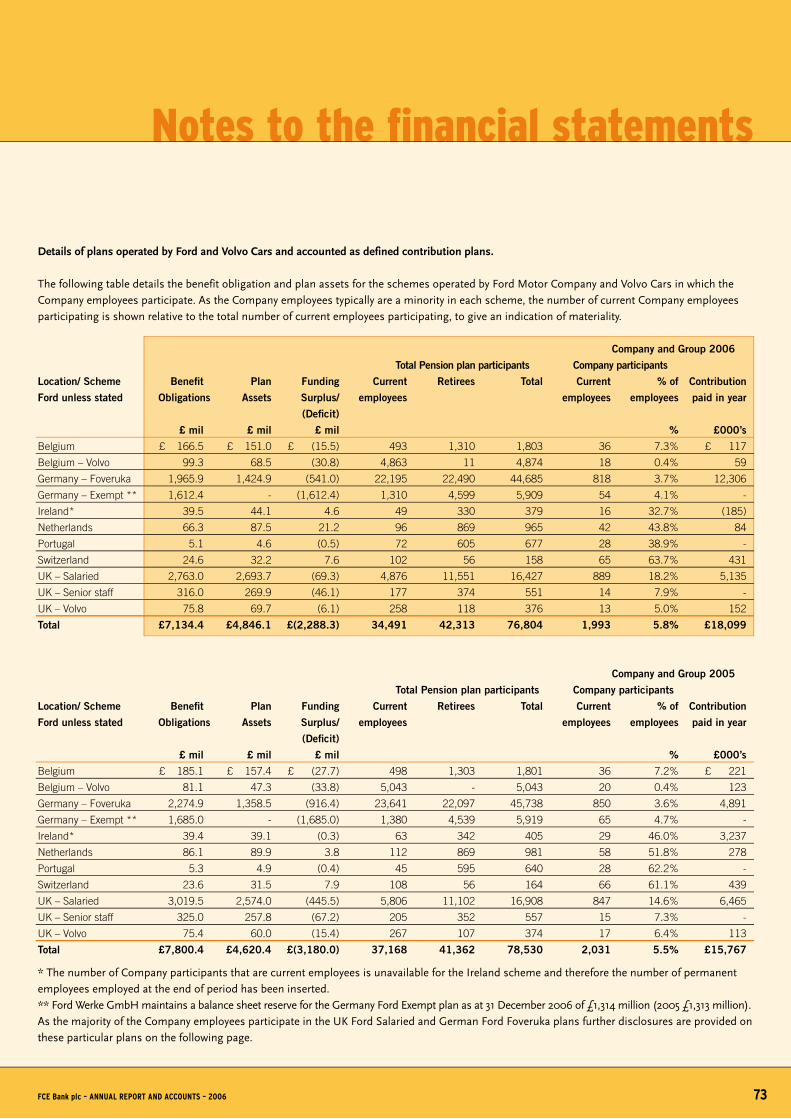

The executive directors and the majority of employees of FCE are accruing benefits as members of various retirement plans administered by Ford affiliated companies. For further information see Note 25 ‘Retirement benefit obligations’ which commences on page 72

Employees

Details of the number of employees and related costs can be found in Note 6 ‘Other operating expenses’ which commences on page 50.

Employee communication

FCE keeps all employees informed of its activities on a national, pan-European and global level by means of in-house publications, intranet and the annual publication of its reports and financial statements. FCE conducts an annual employee satisfaction survey (Pulse) with a feedback and action-planning process aimed at continued dialogue between management and staff to achieve appropriate levels of employee satisfaction. In addition senior management conducts regular cascade meetings throughout the year with employees. These allow management to communicate key business information whilst allowing two-way dialogue via question and answer sessions on business matters. FCE also fully complies with relevant European and national legislation on information and consultation procedures.

Employment practices

FCE complies fully with relevant legislation enacted by both European and national parliaments and any impact the requirements of the FSA has on Human Resources (HR) policy and process. The Company is also committed to ‘best practice’ HR policies and processes in support of the business objectives and in line with its ‘Employer of Choice’ strategy.

As part of being an ‘Employer of Choice’ FCE has a retention strategy to ensure that the required skills and experience required to support business objectives are retained. This strategy includes the use of Personnel Development Committees to support the development of employees and ensure effective succession planning for key roles, a compensation and benefits philosophy targeted at achieving overall competitiveness with the external market, rewarding performing and retaining key skills, and completion of annual individual development plans for all employees which identify their training and development needs.

Diversity

FCE is committed to diversity in the workplace. This values differences provided by culture, ethnicity, race, gender, disability, nationality, age, religion/beliefs, education, experience and sexual orientation. FCE uses the views of employees to improve processes and to foster a culture based on honesty and respect.

Applications for employment by disabled persons are always fully considered, bearing in mind the aptitudes of the applicant concerned. In the event of members of staff becoming disabled every effort is made to ensure that their employment with FCE continues and that appropriate training is arranged. It is FCE’s policy that the training, career development and promotion of disabled persons should, as far as possible, be identical with that of other employees.

Consistent with the principle of diversity FCE also operates a Dignity at Work policy which promotes a business environment where employees, customers and suppliers are valued for themselves and their contribution to the business. FCE is committed to conducting its business with integrity and utilising the talents of everyone through providing an environment free from unlawful discrimination, harassment, bullying and victimisation.

FCE encourages its employees to give something back to their local community. Our policy in this area is that all employees can have up to 16 normal paid work hours per annum (equivalent to two paid work days) to invest in community projects.

12

Annual Report of the Directors / Directors’ responsibilities

for financial statements

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 13

Basel II revised international capital framework

Basel II provides a more robust and risk-sensitive framework for determining the capital requirements of financial institutions than the Basel I Accord it replaces. A thorough review of the implications of the adoption of Basel II has been carried out and the required changes to ensure compliance with BASEL II from January 2008 have been identified.

The Company’s Basel II project is being overseen by a Steering Committee with Executive level sponsorship and regular reporting to the Regulatory Compliance Committee.

FCE’s Basel II project has core aims of:• Demonstrating robust internal capital adequacy assessment processes,• Implementing credit risk reporting processes based on management

information systems,• Deploying comprehensive operational risk tracking, measurement

and management processes,• Developing compliant and informative market disclosures.

Disclosure of Information to Auditors

This confirmation is given and should be interpreted in accordance with the provisions of Section 234ZA of the Companies Act 1985. Each person who is a director at the date of approval of this report confirms that:• So far as the director is aware, there is no relevant audit information

of which FCE’s auditors are unaware; and• Each director has taken all the steps that he/she ought reasonably be

expected to have taken as a director to make himself/herself aware of any relevant audit information and to establish that FCE’s auditors are aware of that information.

Directors' responsibilities for financial statements

The directors are required by UK company law to prepare financial statements for each financial year that give a true and fair view of the state of affairs of the Company and the Group of which it forms a part as at the end of the financial year and of the profit or loss of the Group for that period.

The directors confirm that suitable accounting policies have been used and applied consistently, and reasonable and prudent judgements and estimates have been made in the preparation of the financial statements for the year ended 31 December 2006 and that they comply with International Financial Reporting Standards. The directors also confirm that applicable accounting standards have been followed and that the financial statements have been prepared on the going concern basis.

The directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the Company and the Group and enable them to ensure that the financial statements comply with the Companies Act 1985. They are also responsible for safeguarding the assets of the Company and the Group, and for taking reasonable steps for the prevention and detection of fraud and other irregularities.

Auditors

In accordance with Section 384 of the Companies Act 1985, a resolution proposing the re-appointment of PricewaterhouseCoopers LLP as auditors will be submitted to the Annual General Meeting to be held on 28 March 2007.

BY ORDER OF THE BOARDCarol V RogoffCompany Secretary28 March 2007

Strategy and performance summary

FCE’s objective is to support the sales of our automotive partners while returning value to the shareholder.

Our business model goes beyond simply providing the means for customers to finance the purchase of a motor vehicle. It is to develop customer loyalty which is a critical success factor for the automotive dealer-based distribution system. Market research over time and over different markets and sectors consistently shows that customers who finance their vehicle purchase through FCE are significantly more likely to purchase their next vehicle from the same dealer and the same automotive brand.

The customer benefits from convenience of arranging finance and insurance at the vehicle point of sale and from the service provided by an organisation dedicated to support the customer right through the ownership experience. The dealer benefits from increased customer satisfaction and loyalty, from the support of a bank that supports dealers across the risk range, and that works closely and consistently with the vehicle manufacturer. The automotive company benefits from increased customer satisfaction and loyalty, consistent support for the dealer distribution model, and the efficiency of marketing with the aid of a consistent pan-European finance provider. FCE benefits from increased vehicle sales as this increases our own sales opportunity, through presence at the dealer point of sale, and through manufacturer support for finance-based marketing programs.

Strategies

Origination: Buy it Right, Price it Right We will continue to work closely with our brand partners to create value for our dealers and customers by seeking opportunities to go into the market place together, maximising our unique position as Ford’s financing company. Risk management is also key to our continued value and profitability. We have extensive risk management experience and our focus is on leveraging and strengthening global risk skills internally. Through these efforts, we will continue to optimise profitability as well as generate incremental vehicle sales for Ford.

Servicing:Operate Efficiently, Collect Effectively, Enhance Owner Loyalty FCE has continued to drive efficiencies by increasing the commonality of business processes and information technology platforms. This program has enabled us to reduce the number of unique market/brand systems in core activities. Our two major service centres in Germany and Britain combine with the US service centres of FMCC to drive efficiencies globally by sharing best practices. We remain focused on driving cost reductions in proportion to the overall size of our business while improving customer service and owner loyalty.

Funding:Fund it Efficiently, Manage Risk Our funding strategy is to maintain liquidity and access to diverse funding sources that are cost effective. In recent years, lower credit ratings generally have resulted in higher borrowing costs and reduced access to capital markets. Our credit ratings are closely associated with the credit ratings of Ford, which have been lowered in the last several years. This is mainly a reflection of concerns regarding Ford’s automotive cash flow and profitability, declining share of the US market, excess industry capacity, industry pricing pressure and rising US health care costs. In July 2006, Standard & Poor’s assigned a one notch positive differential credit rating to the Company versus FMCC. Asset-backed funding programs are more cost-effective compared with unsecured funding programs, and allow us access to a broader investor base. We plan to meet a significant portion of our funding requirements through securitisation transactions in 2007.

1�

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 15

Key Financial Ratios 2006 2005

Restated

Return on Equity 10.4% 11.8%

Margin (Net Income/Receivables) 3.8% 3.8%

Cost Effi ciency Ratio (Cost/Receivables) 1.5% 1.6%

Cost Affordability Ratio (Cost/Income) 40% 42%

Credit Loss Ratio (Losses/Receivables) 39 bpts 37 bpts

ACE*/ Risk Weighted Receivables* 14.7% 13.3%

ATE*/ Risk Weighted Receivables* 15.9% 14.6%

*(Refer to page 17 for defi nitions)

The Company is holding significantly more capital than is required by either our regulatory minimum or our internal risk-based capital policy. This supplements our funding program and is a source of further reassurance for our unsecured fixed income investors.

Sales Results 2006 2005

Automotive Brand share of Western Europe

Passenger Car Market* 12.4% 12.5%

FCE New Contracts as a percentage of Vehicle Sales 27.6% 28.5%

FCE Sales of New Retail/Lease Contracts (000’s) 711 734

*(Source: ACEA – European Automobile Manufacturers Association)

Ford, Jaguar, Land Rover, Mazda, and Volvo’s combined share of the Western European passenger car market was 12.4% in 2006, compared with a share of 12.5% in 2005 and 12.0% at the start of the decade. This reflects a highly competitive automotive market where manufacturers are balancing profits and volume.

Consistent with the funding strategy, FCE’s sales efforts are focused on supporting Ford’s automotive brands and our core products which are inherently low risk. Although new contract sales reduced, this partly reflects our decision to withdraw from marginal areas outside our core brands and products. This withdrawal together with our partnering strategy for the FSL business largely accounts for the reduction in managed assets since 2003. For further information in regard to the FSL partnering strategy refer to the ‘Disposals’ section, contained on page 9 of the Annual Report of the Directors.

Satisfaction Indices 2006 2005

Customer Satisfaction Index (CSI)

- Completely and Very Satisfied 86% 85%

- Completely Satisfied 41% 41%

Dealer Satisfaction Index (DSI)

- Completely and Very Satisfied 81% 80%

- Completely Satisfi ed 44% 45%

We monitor customer satisfaction through sample market research covering a range of questions. The CSI and DSI metrics we use internally reflect the percentage of those customers who are completely satisfied with their experience in dealing with us. Customers have different expectations by country and by automotive brand and these metrics are used internally to drive improvements in our service as a key contributor to further improving customer loyalty.

The credit loss ratio has reduced from a peak in 2002/2003 which reflected the economic cycle across Europe and difficult trading conditions for dealers particularly in Germany. FCE’s performance in 2006 on consumer credit losses reflects continued improvements in the deployment of risk management tools and improved economic conditions across most of Europe. Dealer losses are stable following a low in 2004 when there were significant recoveries from prior periods. There have been further enhancements to dealer risk models and risk monitoring in 2006.

The credit loss ratio has increased in 2006 to 39 basis points from 37 basis points in 2005. We would normally expect an average credit loss ratio of around 45 to 50 basis points. Almost all our lending is secured, normally against the motor vehicle, and FCE derives strong benefits from the risk management expertise that has been developed by FMCC in the US market.

FCE’s capitalisation has been strengthened as a result of both the increase in equity and the reduction in the balance sheet size in the year to December 2006.

The ratio for Adjusted Common Equity (ACE) as a percentage of risk weighted assets has increased to 14.7% at December 31, 2006 from 13.3% from a year ago.

• Adjusted Common Equity (ACE) = End of period shareholders’ equity less goodwill and other intangible assets,

• Adjusted Total Equity (ATE) = ACE plus perpetual subordinated debt (see Note 22 ‘Other borrowed funds’),

• Risk Weighted Assets = Assets multiplied by the appropriate percentage risk weighting utilised for capital adequacy ratio purposes.

Profitability – Profit before tax (PBT) and ‘Adjusted PBT’ for the periods below was as follows.

Adjusted PBT excluding exceptional items 2006 2005

and derivative fair value adjustments £ mil £ mil

PBT including exceptional items £ 329 £ 356

Deduct exceptional items as detailed in Note 8 (8) 34

PBT excluding exceptional items 337 322

Deduct fair value adjustments to derivative

financial instruments 35 17

Adjusted PBT £ 302 £ 305

The cost ratios shown exclude exceptional items in order to show underlying or ‘normalised’ performance as explained in the table on the next page. The cost efficiency ratio has improved from approximately 2% at the beginning of the decade to 1.5% in 2006. A key contributor to this improvement has been the implementation of common pan-European systems platforms across the business, in turn driving process harmonisation and economies of scale. As we operate with a smaller balance sheet these ratios will be difficult to sustain. We have therefore accelerated our cost efficiency programs which include seeking global process efficiencies and the continued application of our customer-driven Six Sigma program. As part of this effort to accelerate future cost efficiency programs, we have included a £16 million reserve in our 2006 accounts to support restructuring in our German operations – for further details refer to Note 8 ‘Profit before tax’.

16

Strategy and performance summary

Memo: Key Financial data 2006 2005

£ mil £ mil

Restated

A [i] Average Year Net Receivables (*) £ 15,166 £ 15,643

A [ii] Risk Weighted Assets 15,681 15,524

B [i] Average Year Equity 2,228 1,982

B [ii] End of period Adjusted Common Equity (ACE) 2,311 2,070

B [iii] End of period Adjusted Total Equity (ATE) 2,494 2,271

INCOME:

- Operating income £ 722 £ 827

- Deduct exceptional items (Note 8) (8) (21)

- Depreciation of Operating lease vehicles (132) (211)

- Deduct exceptional items (Note 8) - (4)

C Normalised Income (Margin) £ 582 £ 591

OPERATING COSTS:

- Other Operating expenses £ (246) £ (248)

- Office equipment and leasehold amortisation (2) (1)

- Deduct exceptional items (Note 8) 16 (1)

D Normalised Operating costs £ (232) £ (250)

E Net losses (Note 12) (59) (58)

F Profit after tax £ 231 £ 234

KEY FINANCIAL RATIOS:

Return on Equity (F/B[i]) 10.4% 11.8%

Margin (C/A[i]) 3.8% 3.8%

Cost Efficiency Ratio (D/A[i]) 1.5% 1.6%

Cost Affordability Ratio (D/C) 40% 42%

Credit loss Ratio (E/A[i]) 0.39% 0.37%

ACE/Risk weighted assets (B[ii]/A[ii]) 14.7% 13.3%

ATE/Risk weighted assets (B[iii]/A[ii]) 15.9% 14.6%

(*) Includes ‘Loans and advances to customers’

(Note 12) and ‘Wholesale consignment vehicles’

(Note 18)

Excluding exceptional items and derivative fair value adjustments, adjusted PBT for 2006 was £302 million, reflecting similar earnings to the previous year.

FCE uses derivatives to manage interest rate and currency risks and, as a matter of policy, does not use derivatives for speculative purposes. For interest rate risk management, FCE uses primarily interest rate receive-float swaps which change the interest characteristics of debt from floating to fixed rate. Consequently, the fair value of derivatives increases in periods of rising forward interest rates and decreases in periods of falling forward interest rates. The fair value adjustment to derivatives for the periods disclosed result primarily from changes in forward interest rates during the same periods. As the derivative fair value adjustment does not reflect accruals accounting for the underlying assets and liabilities. This adjustment has been excluded in the calculation of ‘Adjusted PBT’.

Future prospectsIn 2007 FCE expects the ‘Adjusted PBT’, which excludes exceptional items and derivative fair value adjustments to be similar to 2006. Higher interest rates will increase margin pressure and potentially increase FCE’s credit losses from their current historically low level, but we are planning on accelerated operating cost efficiencies to partially mitigate this effect. Our sustained focus will be on operational effectiveness, increasing customer satisfaction and supporting Ford vehicles sales.

The future prospects statement is based on current expectations, forecasts and assumptions and involves a number of risks, uncertainties, and other factors that could cause actual results to differ. FCE cannot be certain that any expectations, forecasts and assumptions will prove accurate or that any projections will be realised. Our future prospects statement is based on the best available data at the time of issuance and will be updated upon publication of the FCE’s 2007 Interim Report and Accounts. Other than the FCE 2007 interim results FCE does not undertake to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 17

In the normal course of business, FCE is exposed to several types of risk. These risks include primarily credit, vehicle residual value, financial market (including interest rate, currency, counterparty and liquidity risks) and operational risk. Each form of risk is uniquely managed in the context of its contribution to overall risk. Business decisions are evaluated on a risk-adjusted basis and products are priced to be consistent with these risks.

FCE continuously reviews and improves its risk management practices.

Credit risk management

Credit risk is the possibility of loss from a customer’s or dealer’s failure to make payments according to contract terms. Whilst credit risk has a significant impact on our business, it is mitigated by the majority of FCE retail, leasing and wholesale financing having the benefit of a security interest in the finance vehicle or similar title retention plans. In the case of customer default the value of the re-possessed collateral provides a source of protection. FCE actively manages the credit risk on retail and commercial portfolios to balance the levels of risk and return.

Retail products (vehicle instalment sale, hire purchase, conditional sale and lease contracts) are classified by risk ranking, term and whether the vehicle financed is new or used. This segmented data is used to assist with product pricing to ensure risk factors are appropriately considered. In our two largest markets, Germany and UK data segmentation is also used in contract servicing to ensure contracts receive collection attention appropriate to their risk level. In these markets centralised servicing in the respective Customer Service Centres includes the application of enhanced risk management techniques and controls, e.g. harmonised originations and collections practices plus the realisation of economies of scale through the introduction and use of the latest servicing technology.

Retail credit underwriting typically includes a credit bureau review of each applicant together with an internal review and verification process. Retail credit loss management strategy is based on historical experience of many thousands of contracts. Statistically-based retail credit risk rating models are used to determine the creditworthiness of applicants. Portfolio performance is monitored regularly and originations processes and models are reviewed, revalidated and recalibrated as necessary.

FCE has developed retail behavioural models in the UK and Germany to assist in determining optimal collection strategies. Accounts are placed in risk categories for collection follow-up. Every reasonable effort is made to collect on delinquent accounts and keep accounts current.

Repossession is considered a last resort. A repossessed vehicle is sold and proceeds are applied to the amount owing on the receivable. FCE endeavours to realise maximum vehicle sale proceeds by using various resale channels. Collection of the remaining balance continues after repossession until the account is paid in full or is deemed economically uncollectable by FCE.

FCE extends commercial credit primarily to franchised dealers selling Ford’s brands in the form of approved lines of credit to purchase inventories of new and used vehicles. In addition, FCE provides mortgages, working capital and other types of loans to dealers. FCE also provides automotive financing for leasing and daily rental companies, as well as other commercial entities.

Each commercial lending request is evaluated, taking into consideration the borrower’s financial condition, supporting security, debt servicing capacity, and numerous other financial and qualitative factors. All credit exposures are scheduled for review at least annually at the appropriate commercial credit committee.

Financial and judgmental risk evaluation ratings are assigned to each

dealer. Asset verification processes are in place and include the use of physical audits of vehicle inventory with increased audit frequency for higher risk dealers. In addition, inventory-financing payoffs are monitored to detect adverse deviations from typical payoff patterns, in which case appropriate actions are taken.

Vehicle residual value risk management

Vehicle residual value risk is the possibility that the actual proceeds realised by FCE upon the sale of returned vehicles at contract termination will be lower than that forecast at contract initiation. FCE establishes the expected residual values based on input from independent consultants (who forecast residual values), current trade guide valuations and our own proprietary knowledge of historical experience and forward-looking information available to FCE. This information includes new product plans, marketing programmes and quality metrics. Any unfavourable variance between FCE’s forecast and expected residual values for existing contracts results in an adjustment to the carrying value of the asset on the balance sheet. Vehicle residual value provision adequacy is reviewed quarterly to reflect changes in the projected values. At contract end, FCE maximises residual value proceeds by using various resale channels including auctions, trade buyers and dealerships.

For further details see Note 29 ‘Vehicle residual values’.

1�

Risk management

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 1�

Financial market risk management

The objective of financial market risk management is to maximise financing margin while limiting the impact of changes in interest rates and foreign exchange rates. Interest rate and currency exposures are monitored and managed by FCE as an integral part of its overall risk management programme, which recognises the unpredictability of financial markets and seeks to reduce potential adverse effects on FCE’s operating results. Financial market risk is reduced through the use of interest rate and foreign exchange derivatives. FCE’s derivatives strategy is defensive; derivatives are not used for speculative purposes.

For further details on the use of derivatives see Note 11 ‘Derivative Financial Instruments’ and Note 39 ‘Interest rate risk’.

Interest rate riskFCE’s asset base consists primarily of fixed-rate retail instalment sale, hire purchase, conditional sale and lease contracts, with an average life of approximately three years, and floating rate wholesale financing receivables with an average life of about 90 days. Funding sources consist primarily of receivable sales (including securitisation and other structured and financing transactions), term debt (public and inter-company) and short-term commercial paper. To ensure funding availability over a business cycle, FCE often borrows longer-term debt (two to five years). Interest rate swaps are used to change the interest characteristics of the debt to match, within a tolerance range, the interest rate characteristics of FCE’s assets. This matching maintains margins and reduces profit volatility. Since a portion of assets is funded with equity, some income volatility can occur as changes in interest rates impact the repricing of FCE’s assets.

The interest rate sensitivity of FCE’s assets and liabilities, including derivatives, is evaluated each month. The interest rate repricing gap information is shown in Note 39 ‘Interest rate risk’.

Currency riskFCE faces exposure to currency exchange rate fluctuations if a mismatch exists between the currency of receivables and the currency of the debt funding those receivables. Whenever possible, FCE funds receivables with debt in the same currency, minimising exposure to exchange rate movements. When funding is in a different currency, FCE uses foreign currency derivatives to convert substantially all of our foreign currency debt obligations to the currency of the receivables.

For further details see Note 38 ‘Currency Risk’.

Counterparty riskCounterparty risk is the risk that FCE that could incur a loss if the counterparty to an investment, interest rate or foreign currency derivatives with FCE defaults. Counterparty exposure limits are established in order to minimise risk and provide counterparty diversification. Exposures to counterparties, including the mark-to-market on derivatives, are monitored on a regular basis. FCE’s Large Exposure position is reported to the FSA on a quarterly basis.

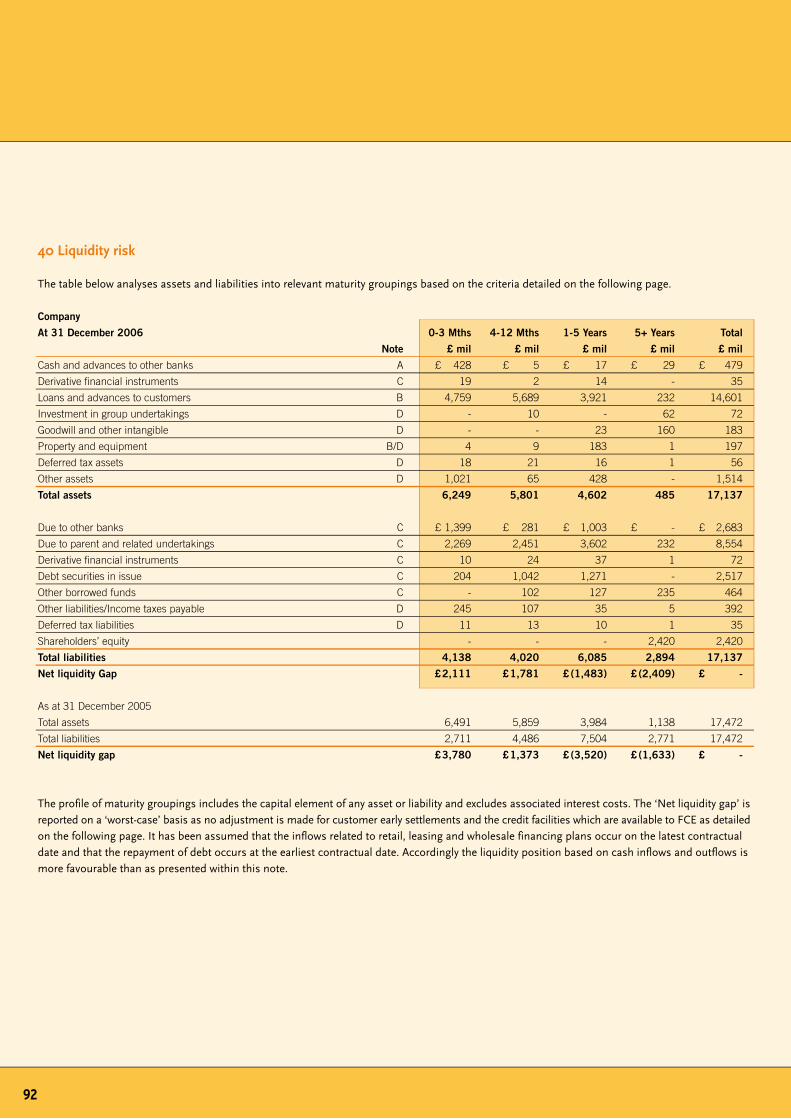

Liquidity riskLiquidity risk is the possibility of being unable to meet all present and future financial obligations as they become due. One of FCE’s major objectives is to maintain funding availability through any economic or business cycle. FCE focuses on developing funding sources to support both growth and refinancing of maturing debt. FCE also issues debt which on average mature later than assets liquidate, further enhancing overall liquidity.

FCE closely monitors the amount and mix of short-term funding to total debt, the overall composition of total debt and the availability of committed credit facilities in relation to the level of outstanding short-term debt.

FCE has the ability to use committed lines of credit from major banks, providing additional levels of liquidity. For further details of these facilities see Note 40 ‘Liquidity Risk’ on page 93. These facilities do not contain restrictive financial covenants (e.g. debt-to-equity limitations) or material adverse change clauses that could preclude borrowing under these facilities. FCE’s liquidity position is reported to the FSA on a quarterly basis.

In the normal course of funding transactions, FCE may generate more proceeds than are necessary for immediate funding needs. These excess amounts are maintained primarily as highly liquid investments, providing liquidity for our short-term funding obligations and flexibility in the use of other funding programs. We monitor our cash levels daily and adjust them as necessary to support our short-term liquidity needs.

Operational risk management

Operational risk is the risk of loss resulting from inadequate or failed internal processes, people or systems, or from external events. This definition of operational risk captures events such as IT problems, human error and shortcomings in the organisational structure, legal changes and lapses in internal controls, fraud or external threats.

FCE takes a pro-active approach to operational risk management, anticipating risks and minimising exposure through risk identification, assessment, monitoring, control and mitigation. FCE seeks to maintain a strong and open operational risk management culture throughout the organisation, embodied within a sound corporate governance structure and supported by company-wide operational risk management processes, policies and procedures.

The Operational Risk Committee (ORC) has responsibility for reviewing and monitoring major operational risks and for promoting the use of sound operational risk management across FCE. Among some of the main areas of focus for the ORC are the implementation of appropriate policies, processes and procedures to control or mitigate material exposure to losses and the maintenance of suitable contingency arrangements for all areas to ensure that FCE can continue to function in the event of an unforeseen interruption.

The guiding principle is that management at all levels is responsible for managing operational risks. FCE also maintains a strong internal control culture across the organisation through the Operations Review Program, a self-assessment control process used by the locations, which is reinforced by central controls from the Internal Control Office (ICO) and Ford General Auditors Office (GAO).

20

Risk management

Corporate governance

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 21

General

FCE considers effective corporate governance as a key factor underlying the strategies and operations of the Group. Since only some of the Company’s debt securities are listed on Stock Exchanges there are significantly fewer reporting obligations on the Company compared with a company with listed equity. Nevertheless the Company chooses to comply with many of the provisions of the Combined Code on Corporate Governance applicable to UK listed companies except for those provisions that are not appropriate for a wholly-owned subsidiary. The Company annually undertakes a benchmarking exercise against the latest guidelines on corporate governance making any adjustments as it deems necessary and appropriate. The Company has developed internal standards to ensure that the Group’s business is conducted within a strong and defined control framework. These internal standards are well suited to the evolving demands of corporate governance in highly regulated, multi-national environments.

Board of Directors

The Company is controlled through its Board of Directors. The Board’s main roles are to create value to the shareholder, to provide leadership to the Company, to approve the Company’s strategic objectives and to ensure that the necessary financial and other resources are made available to the management to enable them to meet those objectives. In addition, the Board of Directors has the ultimate responsibility for ensuring that the Company has systems of corporate governance and internal control appropriate to the various business environments in which it operates. The Board regularly evaluates all risks affecting the business and the processes put in place within the business to control them. The process is focused on the key risks, with formal risk mitigation, transfer or acceptance documented. FCE controls are based on Ford standard controls to safeguard assets, check the accuracy and reliability of financial and non-financial data, promote operational efficiency and encourage adherence to prescribed managerial policies. Policy Statements governing credit and treasury risk management are reviewed annually. The Board also reviews the Group’s commercial strategy, business and funding plans, the annual operating budget, capital structure and dividend policy, statutory accounts, financial performance and operation of each of the Company’s businesses, together with receiving other business reports and presentations from senior management, and is responsible for the appropriate constitution of Committees of the Board and to regularly review their activities and terms of reference as part of an annual review of corporate governance.

The composition of the Board is shown on page 4. The Board of Directors met four times during 2006. With the exception of Mr. Corbello and Mr. Noone, who were unable to attend the third meeting held in September 2006, all directors in post at the relevant time attended all the Board meetings. Four Non-Executive Directors were in post for and attended the first two meetings. Five Non-Executive Directors were in post at the time of the third meeting with four attending and six Non-Executives were in post and attended the fourth meeting in November 2006. All directors are equally accountable under the law for the proper stewardship of the Company’s affairs. Throughout the year under review, the Board and its Committees have been supplied with information and papers to ensure that all aspects of the company’s affairs are reviewed on a regular basis in accordance with a rolling agenda of work.

The Non-Executive Directors fulfill a vital additional role in corporate and regulatory accountability. The Board considers that, with the exception of Mr. Corbello, all the other Non-Executive Directors are independent in that they have no material business relationship with the Company (either directly or as a partner, shareholder or officer of an organisation that has a relationship with the Company) and that they neither represent the sole shareholder nor have any involvement in the day to day manage-ment of the Company or its subsidiaries. As such they bring objectivity and independent judgement to the Board, complement the Executive Directors’ skills, experience and detailed knowledge of the business and play a vital role in the governance of the Company through their member-ship of the Audit Committee.

There is no limitation on the term of office for the Non-Executive Directors. Each year the Non-Executive Directors hold a meeting with the Chairman to discuss Executive Director succession planning, corporate governance and any other relevant issues. The Board reviews the number of Executive and Non-Executive Directors periodically to maintain an appropriate balance for effective control and direction of the business.

Within the financial and overall objectives for the Company, the management of the Company is delegated to Directors and management through the Chairman. Each of the six Executive Directors is accountable for the conduct and performance of their particular business within the agreed business strategy. They have full authority to act subject to the reserved powers and sanctioning limits laid down by the Board and Company policies and guidelines.

Selection of Directors

Generally, specialist executive recruitment agencies are employed to find suitable Non-Executive Directors benchmarked against formal competency criteria. Formal interviews are held with senior Company management before a preferred candidate meets other members of the Board including all the current Non-Executive Directors. During the year, to address the imminent retirement of Mr. Thomson as Chairman of the Audit Committee, an additional Non-Executive Director, Mr Romer-Lee, was appointed to the Board to broaden the skills, experience and diversity of the Board and specifically to take Chairmanship of the Audit Committee upon Mr Thomson’s retirement. Five years had elapsed since Mr. Romer-Lee had been a Partner at PricewaterhouseCoopers, FCE’s external auditor, and he had severed all business and pension links with his previous employer and as such he was considered independent in line with current corporate governance best practice. Executive Directors (including the Chairman) are selected through a Ford Financial Personnel Development Committee process. Succession plans for Directors and other senior appointments are reviewed with senior representatives of the Company’s parent and the Non-Executive Directors. Proposals for all new Executive and Non-Executive Director appointments are then submitted for corporate approval both by senior FMCC Management in the US and to the Ford Corporate Governance Committee before being submitted to the Company’s Board of Directors for formal legal approval.

Training of Directors

Consideration is given to the training needs of Directors on their appointment to the Board and Non-Executive Directors benefit from a comprehensive induction to the Company’s business, risk management and regulatory environment. Also there is at least one off-site senior management financial review and strategy meeting held each year to which the Non-Executive Directors are invited and a training day is available as required for the Non-Executives where topical issues and developments can be discussed. From time to time Ford develops training programs for various aspects of Director’s duties and responsibilities, corporate governance and regulatory and general compliance matters.

Evaluation and Compensation of Directors

Each Executive Director is evaluated by FCE’s performance review process and remuneration is determined in line with the global compensation policy of FMCC and Ford. Senior representatives of FMCC evaluate the performance of the Chairman.

Non-Executive Directors receive a flat fee for their services. The level of the fee is reviewed periodically with the last review undertaken in 2005 and the fee level is approved by senior representatives of FMCC. The Non-Executive Directors do not receive any other remuneration or participate in any incentive arrangements.

During 2006 whilst still a Non-Executive Director of the Company Mr. Thomson was in receipt of a pension from Ford Motor Company Limited (‘FMCL’) accrued from completed service with FMCL prior to his appointment to the Company’s Board of Directors. In addition, as a senior management FMCL pensioner Mr. Thomson was entitled to a loan from the Company to purchase a new vehicle from FMCL (see Note 6 ‘Other operating expenses’).

Committees of the Board

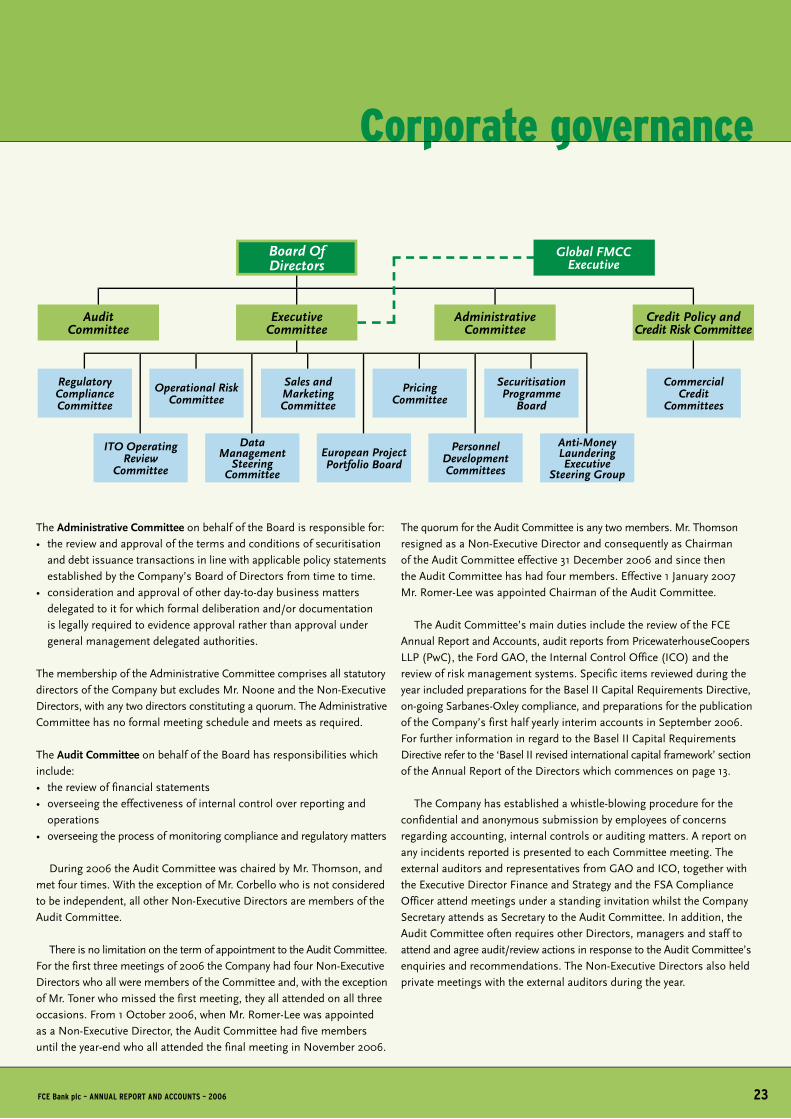

Three Committees reporting directly into the Board were established in 1998 and a fourth, the Administrative Committee, was established on 30 November 2004. Each of the Board Committees has specific delegated authority and detailed terms of reference which is reviewed annually with a report on the activities of each Committee presented to each meeting of the full Board of Directors.

The following chart shows the interrelationship of the Company’s

Board and Committees that deal with corporate governance:

22

Board Of Directors

Audit Committee

Credit Policy and Credit Risk Committee

Commercial Credit

Committees

Administrative Committee

Pricing Committee

Sales and Marketing Committee

Operational Risk Committee

Executive Committee

Global FMCC Executive

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 23

Corporate governance

Securitisation Programme

Board

Personnel Development Committees

European Project Portfolio Board

Data Management

Steering Committee

ITO Operating Review

Committee

Anti-Money Laundering Executive

Steering Group

Regulatory Compliance Committee

The Administrative Committee on behalf of the Board is responsible for:• the review and approval of the terms and conditions of securitisation

and debt issuance transactions in line with applicable policy statements established by the Company’s Board of Directors from time to time.

• consideration and approval of other day-to-day business matters delegated to it for which formal deliberation and/or documentation is legally required to evidence approval rather than approval under general management delegated authorities.

The membership of the Administrative Committee comprises all statutory directors of the Company but excludes Mr. Noone and the Non-Executive Directors, with any two directors constituting a quorum. The Administrative Committee has no formal meeting schedule and meets as required.

The Audit Committee on behalf of the Board has responsibilities which include:• the review of financial statements• overseeing the effectiveness of internal control over reporting and

operations• overseeing the process of monitoring compliance and regulatory matters

During 2006 the Audit Committee was chaired by Mr. Thomson, and met four times. With the exception of Mr. Corbello who is not considered to be independent, all other Non-Executive Directors are members of the Audit Committee.

There is no limitation on the term of appointment to the Audit Committee. For the first three meetings of 2006 the Company had four Non-Executive Directors who all were members of the Committee and, with the exception of Mr. Toner who missed the first meeting, they all attended on all three occasions. From 1 October 2006, when Mr. Romer-Lee was appointed as a Non-Executive Director, the Audit Committee had five members until the year-end who all attended the final meeting in November 2006.

The quorum for the Audit Committee is any two members. Mr. Thomson resigned as a Non-Executive Director and consequently as Chairman of the Audit Committee effective 31 December 2006 and since then the Audit Committee has had four members. Effective 1 January 2007 Mr. Romer-Lee was appointed Chairman of the Audit Committee.

The Audit Committee’s main duties include the review of the FCE Annual Report and Accounts, audit reports from PricewaterhouseCoopers LLP (PwC), the Ford GAO, the Internal Control Office (ICO) and the review of risk management systems. Specific items reviewed during the year included preparations for the Basel II Capital Requirements Directive, on-going Sarbanes-Oxley compliance, and preparations for the publication of the Company’s first half yearly interim accounts in September 2006. For further information in regard to the Basel II Capital Requirements Directive refer to the ‘Basel II revised international capital framework’ section of the Annual Report of the Directors which commences on page 13.

The Company has established a whistle-blowing procedure for the confidential and anonymous submission by employees of concerns regarding accounting, internal controls or auditing matters. A report on any incidents reported is presented to each Committee meeting. The external auditors and representatives from GAO and ICO, together with the Executive Director Finance and Strategy and the FSA Compliance Officer attend meetings under a standing invitation whilst the Company Secretary attends as Secretary to the Audit Committee. In addition, the Audit Committee often requires other Directors, managers and staff to attend and agree audit/review actions in response to the Audit Committee’s enquiries and recommendations. The Non-Executive Directors also held private meetings with the external auditors during the year.

Committees of the Board (continued)

The Board is confident that the collective experience of the Audit Committee members enables them, as a group, to act as an effective audit committee. The Committee also has access to the financial expertise of the Group and its auditors, internal and external, and can seek further professional advice at the Company’s expense if required. The Board considers that Mr. Romer-Lee, in particular, qualifies as having recent and relevant financial experience to bring to the deliberations of the Committee as required by the Combined Code on Corporate Governance.

The Credit Policy and Credit Risk Committee (Credit Policy Committee), usually chaired by the FCE Chairman, determines on behalf of the Board, the general credit policy of the Group on a pan-European basis. It oversees and reviews retail and commercial credit risk and vehicle residual value risk. It reports to each full Board meeting held during the year. Six of the ten members of the Credit Policy Committee are members of the Board of Directors. The Credit Policy Committee consists of individuals responsible for the key components of the business; British, German and European markets, brand directors and pan-European and cross-brand functions such as credit policy and credit risk, marketing, sales, and finance.

The quorum for the Credit Policy Committee is five members to include two from either the Chairman, the Executive Director Finance and Strategy, the Executive Director, Marketing, Sales and Strategy and the Director Credit Policy and Risk Management provided one is either the Executive Director Finance and Strategy or the Director Credit Policy and Risk Management. In addition a Business Unit Head is required for the quorum. The Credit Policy Committee meets monthly. During 2006 it held eleven meetings. No more than three members were absent at any of the meetings held during 2006.

The Commercial Credit Committees have been established as sub-committees of the Credit Policy Committee to review and approve commercial lending requests across Europe. The Commercial Credit Committees are constituted and operate at district, country, European and international levels according to delegated approval authorities and risk assessment.

The Executive Committee usually chaired by the FCE Chairman, reviews, on behalf of the Board, the Group’s strategic direction and policy and the enhancement of shareholder and customer value whilst improving growth, efficiency and profitability. The Executive Committee reports to the Board at each of the full Board meetings held during the year. For the first six months of 2006 the Executive Committee had thirteen members and thereafter fourteen members of whom six are members of the Board of Directors.

The Executive Committee consists of individuals responsible for the key components of the business; British, German and European markets and brand directors, as well as pan-European and cross-brand functions such as credit policy and credit risk, information technology, marketing, sales, general counsel, strategy and finance. Either the Chairman or the Executive Director Finance and Strategy are required in attendance as one of seven members needed to constitute a quorum. The Executive Committee meets monthly and held 12 meetings during 2006. With the exception of the August meeting when four members were absent no more than two members were absent from any meeting.

Several sub-committees have been established and meet regularly and cover all areas of the business. These sub-committees report into the Executive Committee:• The Regulatory Compliance Committee informs senior management

and the Audit Committee on regulatory compliance issues. Its responsibilities include monitoring and evaluating regulatory changes and determining the Company’s response or changes needed. The Committee also reviews returns submitted to the FSA.

• The Information Technology Office Operating Review Committee monitors, aligns and resolves plans and priorities across FCE to support key information technology related projects and initiatives.

• The Operational Risk Committee has the overall responsibility for reviewing and monitoring major operational risks and for promoting the use of sound operational risk management across FCE.

• The Data Management Steering Committee provides a co-ordinated input to process and IT application development to meet business requirements through data solutions that are consistent with strategic priorities.

• The Sales and Marketing Committee facilitates regular and timely information exchanges between business units and functional areas covering sales, marketing and operational matters.

• The European Project Portfolio Board oversees the management of FCE’s strategic projects. This sub-committee meets on a monthly basis to review, approve and prioritise large / strategic projects.

• The Pricing Committee reviews and approves pricing strategies and policies on a national, regional and European basis.

• The Personnel Development Committees drive personnel development and career and vacancies planning. The sub-committees are comprised of members of management, who are assisted by Human Resources representatives.

• The Securitisation Programme Board approves and reviews structural and policy matters concerning planned securitisation transactions and securitisation issues raised at other committees and forums may be referred to it for further deliberation.

2�

Corporate governance

• The Anti-Money Laundering Executive Steering Group oversees compliance with the provisions of the relevant European Community Money Laundering and related directives as applied to those markets in which FCE operates.

In addition, the Executive Committee may from time-to-time appoint working groups or steering committees to address specific business risks and opportunities.

Audit and internal control

PricewaterhouseCoopers LLP (PwC) conducts audits of FCE’s financial statements, in accordance with relevant legal and regulatory requirements and International Standards on Auditing (UK and Ireland). PwC provides external audit opinions on FCE’s financial statements.

To help ensure that the auditors’ independence and objectivity are not prejudiced by the provision of non-audit services, the Audit Committee has agreed that the external auditors should be excluded from providing management, strategic or Information Technology consultancy services and all other non-audit related services, unless the firm appointed as external auditor is:- the only provider of the specific expertise/service required; or- the clear leader in the provision of the service and is able to provide

that service on a competitively priced basis.

As auditors, PwC will undertake work that they must or are best placed to complete. This includes tax-related work, formalities related to borrowings, regulatory reports or work in respect of acquisitions and disposals.

Ford’s GAO is fully independent from FCE; its coverage is based on the relative risk assessment of each ‘audit entity’, which is defined as a collection of processes and systems that are closely related. The GAO’s mission is to provide objective assurance and advisory services to Management and the Board of Ford and to the Company’s Audit Committee in order to improve the efficiency and effectiveness of Company operations and assist the Company in achieving its objectives through systemic and disciplined auditing.

ICO is based within FCE to offer control consultancy, audits, process reviews, advice on systems controls and control training across all locations. ICO access to internal reports and operational experience informs the conduct of operational reviews and audits. The department has created and delivered training in ongoing controls as part of formal feedback to reflect learning points derived from the audits and reviews. This matches industry leading-edge practices to assist management in early identification of potential control risks which is an essential element of the process to ensure compliance with the Sarbanes-Oxley Act.

The Operations Review Programme (ORP) has been designed, implemented and revised for the last several years to embed the assessment of risk and opportunity across the Group. The ORP provides the means for the management of each location or activity to continually monitor control integrity throughout their operation by the performance of regular and appropriate checks and embeds sound governance principles in key processes. The ORP facilitates high levels of control self-assessment as part of good business practice. It also embodies the principles established by the UK’s Turnbull Committee on achieving the standards in the Combined Code of Corporate Governance. The ORP was modified for, and provides a key structure in FCE’s compliance with the US Sarbanes-Oxley legislation.

FCE Bank plc – ANNUAL REPORT AND ACCOUNTS – 2006 25

We have audited the group and parent company financial statements (the ‘financial statements’) of FCE Bank Plc for the year ended 31 December 2006 which comprise the Consolidated Income Statement, the Group and Parent Company Balance Sheets, the Group and Parent Company Cash Flow Statements, the Group and Parent Company Statements of Recognised Income and Expense and the related notes. These financial statements have been prepared under the accounting policies set out therein.