FastClose_EN

16

Fast Close Management Challenges and outlook Benoit LASCOLS - Oct 2014

-

Upload

lascols-benoit -

Category

Documents

-

view

177 -

download

0

Transcript of FastClose_EN

1

Fast Close Management

Challenges and outlook

Benoit LASCOLS - Oct 2014

2

About...

The Company

WM-Up, a company founded in 2013 by Benoit LASCOLS and Nadir AID, promotes and

provides innovative solutions to the financial departments in order to speed up report-

ing cycles and decision making (Fast Close).

Our main line of development is to design tools to optimize finance process by enabling

and pushing accounting information entered by subsidiary (into the ERP) at the group

level and in a homogeneous format. The innovative nature of the approach and the

gains lie in the simplification, auditability, and speed of information feedback.

The Author

Benoit LASCOLS has over 10 years’ experience in consulting with financial departments,

but also as an finance SI manager in a CAC 40 group. He was thus able to develop ex-

pertise in the implementation of tools for consolidation and reporting as well as develop-

ment service activities for financial departments.

Today and in addition to his role of Director General, he manages the Front Office part

(marketing, partnership, support, and testing). Benoit is personally involved in the bal-

ance between business need and development projects of our tools. In parallel, he con-

tinues to provide his expertise to advise the finance departments on the implementation

of Fast Close projects and the optimization of the reporting process.

He holds an engineering degree and a Masters of Business Administration (obtained at

IAE in Aix-en-Provence).

The White Paper

This white paper is the result of a survey conducted with large listed groups. It lists all pos-

sible actions to fasten the financial reporting process, presents a current state of art of

financial reporting, and will project a few years into the future by introducing you the in-

novations proposed to date by few niche publishers, that will help revolutionize the fi-

nance reporting tomorrow.

3

What is it ?

Fast Close encompasses all elements implemented

to accelerate financial closures while ensuring data

quality.

Fast Close thinks through a thorough review of processes,

tools, and a rationalization of these to reduce the number of steps and potential bot-

tlenecks. In some cases, Fast Close can be seen as an approach:

Quality and continuous improvement: the implemented actions are

preventative and consider over the long term. The ISO 9000 standards

provide a methodology suited to this type of approach

Project: corrective actions and re-engineering must be conducted and

organized around a transverse approach, with a strong interaction be-

tween finance and information systems.

Why ?

Fast Close is an objective that returns to the financial departments' issues. Status quo

technology (weak developments over the last 10 years, mainly related to technical

limitations and a duopoly situation in the market), and the ever-increasing need to re-

duce costs and the duration of closing lead to new initiatives.

The objectives are to produce financial and operational information, as quickly as

possible. Early reporting production allows for (non-exhaustive list):

Facilitating management decision-making

Reducing inertia in the decision cycle

Improving company image (external communication)

Easing communication between the management and the subsidiaries

Reducing costs related to reporting production

Improving analysis that can be done and giving more time to decision-

making

Fast Close

90% Of CFO want to reduce re-

porting deadlines and repor-

ting workload

4

Fast Close

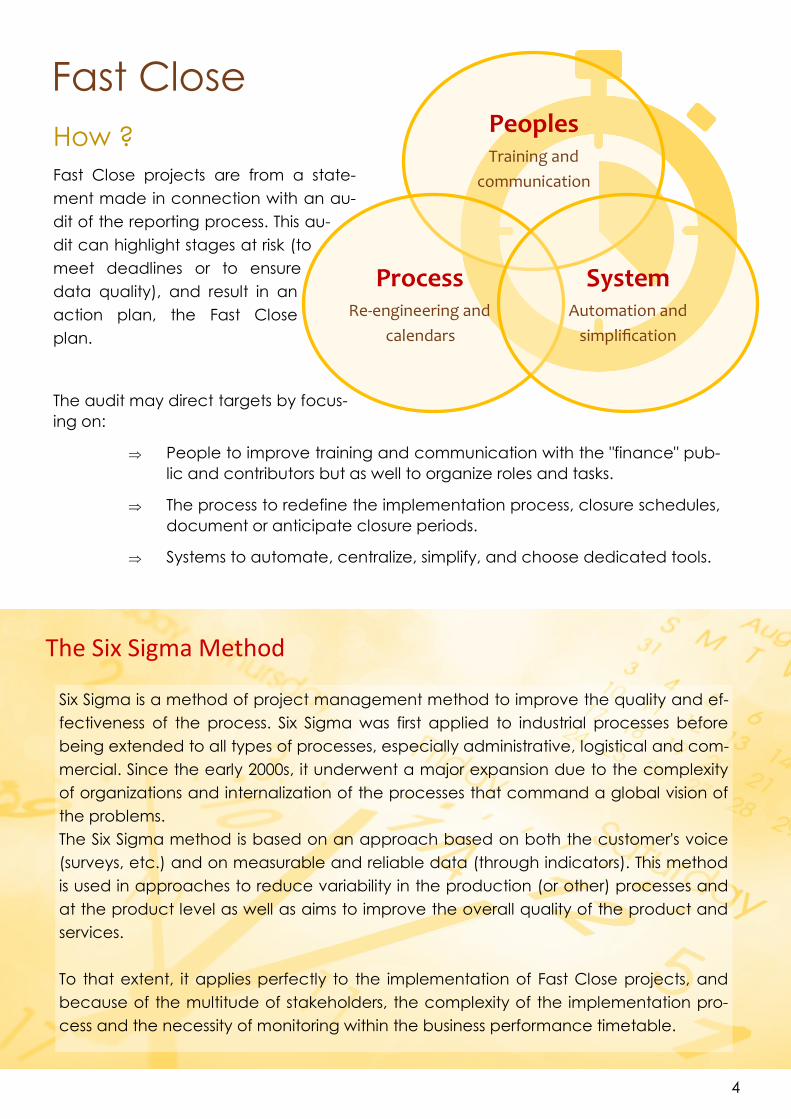

How ?

Fast Close projects are from a state-

ment made in connection with an au-

dit of the reporting process. This au-

dit can highlight stages at risk (to

meet deadlines or to ensure

data quality), and result in an

action plan, the Fast Close

plan.

The audit may direct targets by focus-

ing on:

People to improve training and communication with the "finance" pub-

lic and contributors but as well to organize roles and tasks.

The process to redefine the implementation process, closure schedules,

document or anticipate closure periods.

Systems to automate, centralize, simplify, and choose dedicated tools.

Peoples Training and

communication

Process Re-engineering and

calendars

System Automation and

simplification

The Six Sigma Method

Six Sigma is a method of project management method to improve the quality and ef-

fectiveness of the process. Six Sigma was first applied to industrial processes before

being extended to all types of processes, especially administrative, logistical and com-

mercial. Since the early 2000s, it underwent a major expansion due to the complexity

of organizations and internalization of the processes that command a global vision of

the problems.

The Six Sigma method is based on an approach based on both the customer's voice

(surveys, etc.) and on measurable and reliable data (through indicators). This method

is used in approaches to reduce variability in the production (or other) processes and

at the product level as well as aims to improve the overall quality of the product and

services.

To that extent, it applies perfectly to the implementation of Fast Close projects, and

because of the multitude of stakeholders, the complexity of the implementation pro-

cess and the necessity of monitoring within the business performance timetable.

5

Contributor and their objectives

Define available roles and support

Closures and reporting process involve a multitude of

organizations on different tools. These contribu-

tors may have:

Different objectives and con-

straints.

Various skills.

A level of information about the

processes, tools, and variable data.

These differences impact the process and closure deadlines by :

Lack of user training

Too complex systems and processes.

Excessive turnover of the "finance" population.

Correlation of these impact that can degrade the situation.

A lack of communication between the group and (local) subsidiaries whose origin can

be:

Vague or poorly formulated "group" rules.

Lake of communication or difficulties to access "group" rules.

A lack of visibility on the application of

"group" rules by the subsidiaries.

Organization problems whose origin can be:

Roles and objectives not

clearly defined.

Diffusion of responsibilities or on

the contrary too concentrated.

Internal audit deficit.

Training and communication are integrated into a continuous improvement approach

with an initialization project if necessary.

70% Of IS Manager think that systems

are not correctly used by users

80% Of contributors esteem that the

corporate rules are not clear or

not accessible

6

Implementation

Actions that can be considered in the context of a Fast Close approach (with an objec-

tive of handling users better) can be the following:

Case study - Training and documentation review

State of process

The consolidation group was faced with 50% of

entities submissions made after the deadline.

as well as consistency problems figures at

group level.

Project

The steps of the project were a rewrite of trai-

ning documents (from word format to power-

point in a more accessible format), the esta-

blishment of a sharepoint site for finance and a

tool with educational links and Frequently As-

ked Questions (help forms) and finally the trai-

ning of users.

Total project costs have reached 120 days

(including days of availability of people trai-

ned).

Gains

Gains after project were a reduction of 60% of

submissions made after the deadline and bet-

ter confidence of the top management in fi-

gures and mastery of reporting risks.

Action Advantages Disadvantages Example

Users training User Training Accountability in

their zone

More restrictive organization

and logistics

Regular training with a sched-

ule and training objectives

(training plan) Identify key users as relays

in the closure process

More flexible and supply sup-

port and communication pro-

cesses

Requires having a minimum

target number of users

FP&A advanced training on

tools and implemented pro-

cesses

Simplify the rules Simplification of communica-

tion to users

Compromise with the data

quality

Removal of some unused or

unreliable account details

Communicate and for-

malize the rules

Accessibility of support Significant responsibility of

initialization. Updating and

maintenance of procedures

Documentation of account-

ing procedures in an accessi-

ble format (powerpoint)

Centralize information Ergonomics for facilitating

research and access to infor-

mation

Establishment of a SharePoint

site

Organize and redefine

objectives in teams

Clarification of roles and ob-

jectives, improvement of the

understanding of manage-

ment expectations

Significant change manage-

ment

Definition of a mapping for

roles and objectives for each

in the closure process

Contributor and their objectives

7

Process

Complexity related to the num-

ber of contributors

Processes are necessary because they help

ensure data quality. However, if the processes

are poorly arranged or performed too late in

the production cycle, they can put at risk, in-

crease time periods, and have in some cases

counter-productive effects (with regard to fixed ob-

jectives). The main processes involved in the financial clos- ing

are:

The contribution of subsidiaries and the rise in numbers (ERP closing, data

entry / loading, data validation)

The consolidation process: inter-company reconciliation, control of

batches and analysis, accounting for the group's operations, internal re-

porting process, analysis of changes

Data control and accounting adjustments

Formatting and presentation of figures / dashboarding

The audit and certification of accounts

The problems encountered may be of different types:

A data quality level too high or useless for quick decision-making

A lack of phasing / structuring the process

Redundant tasks / controls

Validation process that is too hierarchical

70% Of the times is spent on tasks wi-

thout added value from control-

ling point of view

Few records illustrating the reporting issues

« This is not my figures» (Regional CFO)

« My technical expert is in vacation. I cannot close my reporting » (Consolidation manager)

« I prefer to post a journal, than to reload the whole local package » (Accountant)

« I spent more time on reconcilliation than on analysis» (Controler)

« I do not have access to figures, so I cannot justify them» (Controler)

8

Finance process

Process Typology

The reporting process can be considered as two major methods:

Rake: for a centralized and direct process, but leaving very little leeway

for sub-activities or sub-assemblies (BU subgroups, ...). Suitable for matrix

organizations.

In tiers for a decentralized process and delegated responsibility for pro-

duction of the numbers, providing flexibility for stages (often necessitated

by the specific nature of their organizations or businesses) suitable for hier-

archical organizations

The stage method is less suitable for the following reasons:

Not suitable for the majority of matrix organizations

Adds validation levels and sub tasks that can slow down the whole pro-

cess

Necessarily higher overall reporting cost and therefore inadequate in a

logical rationalization of costs

Detailled workload on closing processes

Our survey has been led on company that have to comply with external reporting re-

quirements. The survey was on half-yearly financial processes. 46 company contributes

between March and June 2014. The result present average time to complete on half

yearly closing.

9

Financial process

Implementation

The implementation of efficient processes will be mainly determined in the process type.

In a process by stage, the flexibility and leverage of optimizations are difficult to use by

the group. Conversely, in a matrix organization, optimization options are numerous and

can lead to concrete results.

To date, the most extensive and most extreme method is to achieve an early closure.

We will develop the issues for this method in order to show the limitations of such practic-

es.

Action Advantages Disadvantages Example

Establish an organization

in stages.

Accountability of subgroups

independant.

Well suited to hierarchical or-

ganizations or conglomerates.

Opacity of any analysis at

group level.

Unsuitable for matrix organiza-

tions.

Increased inertia in the closure

phases.

Establish a rake organiza-

tion.

Direct accountability for the

subsidiary accountants.

No intermediate level, direct

communication.

Increase the number of inter-

locutors.

Reduce the number of

controls.

Acceleration of reporting and

the provision of information.

Compromise on data quality

that must be corrected later.

Automate some correc-

tions.

Presentation of specific infor-

mation.

Necessary corrections of the

(ERP) source systems after-

wards.

Establish account plan

into ERP Core model.

Information feedback facili-

ties.

Rigid and somewhat flexible

solution, which does not allow

for taking into account fiscal

constraints for example.

Assimilating ERP controls. Faster correction of errors. Need for flexible tools.

Assimilate the inter-

companies into the trans-

action currency.

Simpler reconciliation.

Offset currency effects. No

disruption due to currency

effects.

Risk of discrepancies among

(ERP) sources and batches of

rebounds (consolidation tool).

Anticipate the figures. Suitable for long production

cycles or planned (consulting

& design firm) activities.

Unsuitable for short production

cycles.

Feasible only on operational

data.

Establishment of a process

allowing to raise the margin to

D-5 (anticipated time entry for

a consulting activity).

Establish a hard close (to

simulate a biannual clo-

sure in preparing figures

for the first 5 months).

Anticipating problems related

to the closure.

Reduction remains to be done

on the next closure.

Streamlining responsibility re-

lated to the closure.

Limiting the risk on the actual

closure.

No reduction of the actual

responsibility.

Communication about the

hard close.

10

Financial process

Early Closures

The main limiting factor at the time of closures is the data submission date. To return this

task back to an earlier time in the process, some groups establish early closures.

Early closures consist of anticipating some or all of the figures before the closing date

(with the consolidations re-worked at D+1, to take into account variables external to the

business like exchange rates, or more generally, market factors, which can not be antici-

pated).

This type of closure is conceivable only in the condition of having a predictable activity

and must for example:

Rely on a fixed backlog (building, ....)

Long production cycles (aircraft construction, ...)

A planned activity (consulting activity on the condition of knowing about

their activity in 2/3 weeks)

On the other hand, this type of closure will not be suitable for the following activities:

Short cycle activity (large distribution)

Seasonal activity because of not being an issue (non-calendar closures)

Conglomerates: too many different activities to model, and potentially

too frequent organizational / zone changes

Early closures, allow at best, to promote the numbers and start consolidation audits at

D+1. However they entail difficulties:

Need for a common model to allow for the achievment of a reliable clo-

sure

Need to perform a second closure and to overcome fluctuations, quickly,

to provide adjustments to the audit

Early closures are therefore very quickly limited by business constraints or implementation

difficulties. It is therefore not possible to generalize a Fast Close method.

11

Information systems

Sources of Process Complexity

Information systems must proceed and develop along with the business. The various as-

pects to consider are:

Flexibility: the ability to move with business organization changes.

Their integrability: the ability to integrate with other information systems.

Their auditability: the ability to trace and track changes (SOX require-

ments, external and internal control).

Their simplicity: the ability to be properly handled, and used.

Case—Survey on financial information system

Bellow the result of a studies (survey led between March and June 2014) presenting the

closing deadlines compare to the flexibility of the tools used (mesure from a questionnary

that gaves a note on 10). The bullets size is a evaluation of the TCO (total cost of

ownership) of the financial tools by M€ of revenues.

This study shows that the flexible system close faster, and that the rapidity of the closing is

not obviously linked to the investments realized by IT departement.

12

Information system

Implementation

All of these 4 points seen previously allow for influencing the ability of a system to simplify

use, improve processes, and reduce reporting needs. In consideration of the existing,

and the issues encountered, the strategy will be oriented according to one of the fol-

lowing strategy:

Redesign of interfaces to automate and re-process batches and their

submissions.

SI rationalization by a decrease in the number of bases needed for re-

porting to avoid reconciliations.

Action Advantages Disadvantages Example

Integrate existing systems. Optimal use of existing sys-

tems.

Complexity of flows and inter-

faces.

Inflexibility of systems.

No questioning of the overall

architecture.

Establishment of a corporate

mapping within the ERP sub-

sidiaries

Centralize figures in a da-

ta-mart.

Analysis capabilities and ad-

vanced controls.

Simpler and faster audit and

certification of accounts.

Need for a flexible and dedi-

cated tool.

Establish an electronic

data interchange system.

More than necessary inter-

company reconciliation

(adequate through construc-

tion).

Cumbersome and complex

maintenance.

Inflexible system.

Establishment of a system for

generating internal invoices

(electronic data inter-

change).

Industrialize reporting pro-

duction.

Implement a spider web

architecture

Guarantee scalability of sys-

tems over time.

Flexibility with respect to

changes in the business.

Centralization of all business

financial and operational da-

ta.

Necessary questioning of exist-

ing information systems

Elimination of unneeded

bricks.

Installing performant applica-

tions and environments.

Implementation of Fast Close

Management (WM-Up).

13

Information system

Simplification and Adaptability

Information systems have become rigid, mainly for the following reasons:

Too many specific developments that have led to black boxes too com-

plex to evolve

Lack of rationalization of application portfolios

No standard for communication among software publishers

Lack of finance process industrialization

The cause of these problems is found in an unstable economic environment that evolves

much faster than information systems. These changes have accelerated with the global-

ization of the economy (merger, acquisition, spin-off, IPO, reorganization, ...) and have it

constantly jumbling, stiffening, and destabilizing information systems.

Simplification (rationalization and ergonomics) and adaptability (standardization and

normalization) are now well-assimilated objectives for information systems departments.

This flexibility of use opens the door to a major change in the reporting process: consoli-

dation in real time.

Fast Close Management and WM-Up innovation

WM-Up, in developing new methods of data processing, has developed tools that can

be quickly adapted to any situation. The added value is summarized in three points:

Simplicity: an integration and logical use and does not require special

technical skills

Adaptability, ensured by a wide range of connectors for ease of use

Auditability of all financial reporting of the issued figure invoice

Innovation: new algorithms for processing data allowing for the processing

of a large volume of information in a very short time (performance gains

multiplied by 30 compared to market standards)

14

Information system

…. To the real-time consolidation

Consolidation in real time allows for submission of figures central to the transaction gen-

eration within the ERP. This will drastically change the methods and financial processes

that until now were bound by timelines and progressive data validation steps. Consoli-

dation will therefore be more constrained by the slowest submissions.

Tomorrow, from user perspectives, real-time consolidation, financial closures will no long-

er entail an intense workload of 5 to 10 days, but will be a responsibility streamlined over

the entire month. This will reduce approximations and start the analysis at D+1 (instead

of D+10, on average, to date).

These changes can only be emphasized if they have flexible and simple systems, allow-

ing for adaption to changes in scope and reorganization.

This technological evolution has major impacts:

The finance public is no longer restricted by short, intense closure phases.

It can streamline the workload throughout the month

Processes are no longer dependent on a specific phasing of reassembled

numbers. They focus more on data quality and their analysis

The governance of information systems can be more flexible and adapt

to group internal changes

Numbers production can be done within a much faster time

The consolidation service can reorder tasks around business analysis

(instead of an organization by milestone, as is the case today)

15

Synthesis

Fast Close can focus on one of three previously identified areas which are: people, pro-

cesses, and / or systems.

A preliminary audit phase allows for emphasizing the possible failures or optimizations.

Risk analysis / efficiency matrices identify the critical points of the closure process.

A feedback on the projects implemented shows that a top management sponsor is

necessary when it strives to change processes and systems. Change management and

enrollment of the various parties are needed to involve stakeholders.

The benefits of such an approach are measurable:

Data quality: reducing the number of local adjustments passed after vali-

dation of the batches.

Reducing the percentage of entities / BU outside of closure deadlines.

Reducing the announced group closure deadline.

The reduction of the subsidiary recorded closure (actual submission date).

All of these measurable gains, are to allow for calculating a ROI (return on investment)

for the projects, and track this ROI in time. Matrices that allow for assessing risk, also pro-

vide an encrypted correspondence of responsibility induced by such risks.

16

This document is the property of SAS WM-Up.

This document, including but not limited to, the general design, content, logo, trademark, are protected by copyright

and laws relating to intellectual property rights. You may not copy, distribute, modify, plagiarize, transmit, display, re-

produce, publish, transfer or sell the contents or part of WM-Up presentation, except with the prior written consent of

WM-Up SAS.

This document contains information in summary form and is contained reference only. It is not intended to be a substi-

tute for detailed research or the exercise of professional judgment. WM-Up disclaims all liability for losses which might

be caused by a partial or complete interpretation or implementation of this publication.

You can refer to the Terms of Use and Online Privacy Policy, for each question and information on the use, content

and data provided in this presentation.

Any controversy or claim arising out of or related to the content, conditions of use or privacy policies are governed by

French law. The Commercial Court of Paris shall have exclusive jurisdiction in the matter.

© 2013-2014 WM-Up. All Copyrights

@Fast_close

@RealTimeReporting

www.wm-up.com

6, rue Henri Marrou

92 290 Chatenay Malabry (France)