FASB’s Proposed Model for Insurance Contracts - BKD · CONTRACT BOUNDARY – RECOGNITION ......

32

FASB’s Proposed Model for Insurance Contracts

Transcript of FASB’s Proposed Model for Insurance Contracts - BKD · CONTRACT BOUNDARY – RECOGNITION ......

FASB’s Proposed Model for Insurance Contracts

FASB’s Proposed Model for Insurance Contracts

2

Table of Contents BACKGROUND & OVERVIEW .................................................................................................................................. 4

SCOPE .................................................................................................................................................................... 5

GUARANTEES ................................................................................................................................................................ 6

UNIT OF ACCOUNT ................................................................................................................................................. 8

CONTRACT BOUNDARY – RECOGNITION & DERECOGNITION ................................................................................. 8

MEASUREMENT MODELS ....................................................................................................................................... 9

BUILDING BLOCK APPROACH (BBA) .................................................................................................................................. 9 BBA Model Components ..................................................................................................................................... 10 BBA Recognition & Measurement ....................................................................................................................... 13

PREMIUM ALLOCATION APPROACH (PAA) ........................................................................................................................ 14 PAA Initial Recognition ........................................................................................................................................ 14 PAA Subsequent Measurement ........................................................................................................................... 15

OTHER ITEMS ....................................................................................................................................................... 18

ACQUISITION COSTS ..................................................................................................................................................... 18 Recognition ......................................................................................................................................................... 18 Qualifying Direct Acquisition Costs ..................................................................................................................... 18 Direct Response Advertising ................................................................................................................................ 19

PARTICIPATING CONTRACTS, CONTRACTS WITH PARTICIPATION FEATURES & SEGREGATED FUNDS ............................................... 20 Participating Contracts ....................................................................................................................................... 20 Participation Features ......................................................................................................................................... 21 Segregated Fund Arrangements ......................................................................................................................... 21

UNBUNDLING – SEPARATING COMPONENTS OF AN INSURANCE CONTRACT ............................................................................. 23 Embedded Derivatives ........................................................................................................................................ 23 Investment Components ..................................................................................................................................... 23 Performance Obligations .................................................................................................................................... 24 Cash Flow Allocations ......................................................................................................................................... 24

REINSURANCE .............................................................................................................................................................. 25 Ceding Commissions ........................................................................................................................................... 26 Loss-Sensitive Features ....................................................................................................................................... 26

CONTRACT MODIFICATIONS ........................................................................................................................................... 27 BUSINESS COMBINATIONS & PORTFOLIO TRANSFERS .......................................................................................................... 27

Business Combination ......................................................................................................................................... 27 Portfolio Transfers............................................................................................................................................... 28 Acquisition Through Combination of Entities or Businesses Under Common Control ......................................... 28

FOREIGN CURRENCY ..................................................................................................................................................... 28

FASB’s Proposed Model for Insurance Contracts

3

PRESENTATION & DISCLOSURE ............................................................................................................................ 28

PRESENTATION ............................................................................................................................................................ 28 Statement of Financial Position .......................................................................................................................... 28 Statement of Comprehensive Income ................................................................................................................. 29

DISCLOSURES............................................................................................................................................................... 30 Insurance Contract Liabilities & Liabilities for Incurred Claims ........................................................................... 31 Margin ................................................................................................................................................................ 31 Insurance Contract Revenue & Premiums ........................................................................................................... 31

TRANSITION ......................................................................................................................................................... 32

CONTACT US ........................................................................................................................................................ 32

CONTRIBUTORS ................................................................................................................................................... 32

FASB’s Proposed Model for Insurance Contracts

4

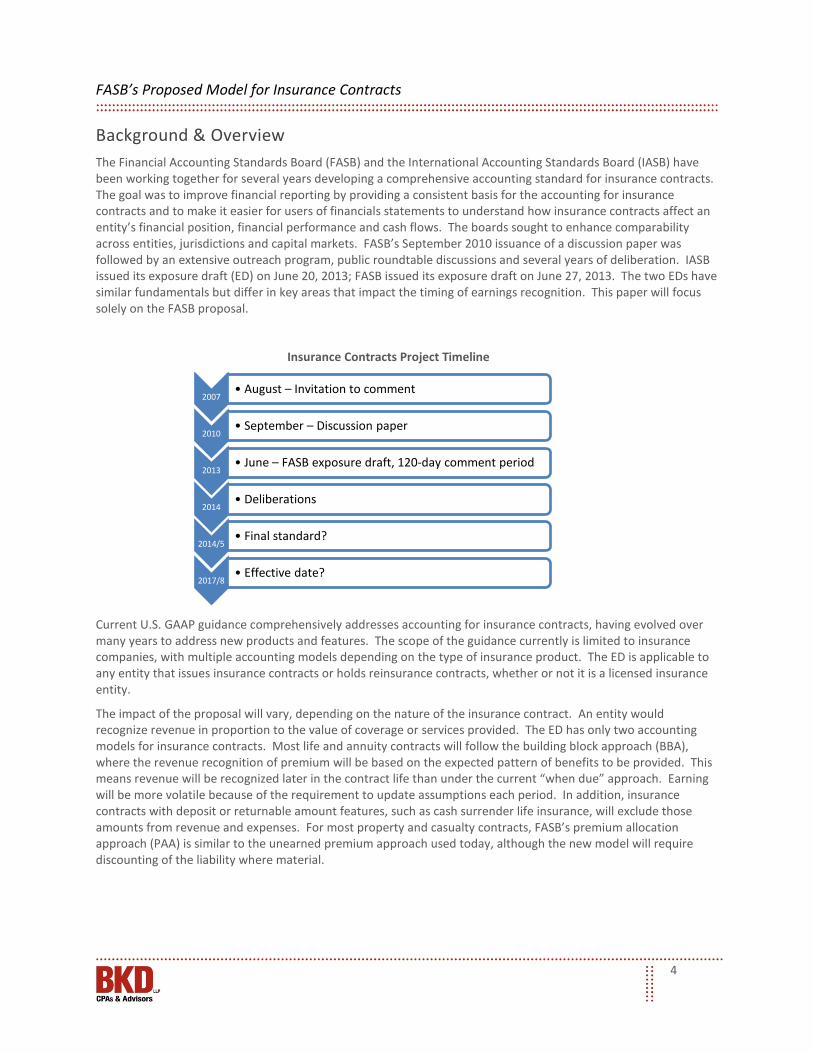

Background & Overview The Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) have been working together for several years developing a comprehensive accounting standard for insurance contracts. The goal was to improve financial reporting by providing a consistent basis for the accounting for insurance contracts and to make it easier for users of financials statements to understand how insurance contracts affect an entity’s financial position, financial performance and cash flows. The boards sought to enhance comparability across entities, jurisdictions and capital markets. FASB’s September 2010 issuance of a discussion paper was followed by an extensive outreach program, public roundtable discussions and several years of deliberation. IASB issued its exposure draft (ED) on June 20, 2013; FASB issued its exposure draft on June 27, 2013. The two EDs have similar fundamentals but differ in key areas that impact the timing of earnings recognition. This paper will focus solely on the FASB proposal.

Insurance Contracts Project Timeline

Current U.S. GAAP guidance comprehensively addresses accounting for insurance contracts, having evolved over many years to address new products and features. The scope of the guidance currently is limited to insurance companies, with multiple accounting models depending on the type of insurance product. The ED is applicable to any entity that issues insurance contracts or holds reinsurance contracts, whether or not it is a licensed insurance entity.

The impact of the proposal will vary, depending on the nature of the insurance contract. An entity would recognize revenue in proportion to the value of coverage or services provided. The ED has only two accounting models for insurance contracts. Most life and annuity contracts will follow the building block approach (BBA), where the revenue recognition of premium will be based on the expected pattern of benefits to be provided. This means revenue will be recognized later in the contract life than under the current “when due” approach. Earning will be more volatile because of the requirement to update assumptions each period. In addition, insurance contracts with deposit or returnable amount features, such as cash surrender life insurance, will exclude those amounts from revenue and expenses. For most property and casualty contracts, FASB’s premium allocation approach (PAA) is similar to the unearned premium approach used today, although the new model will require discounting of the liability where material.

2007 • August – Invitation to comment

2010 • September – Discussion paper

2013 • June – FASB exposure draft, 120-day comment period

2014 • Deliberations

2014/5 • Final standard?

2017/8 • Effective date?

FASB’s Proposed Model for Insurance Contracts

5

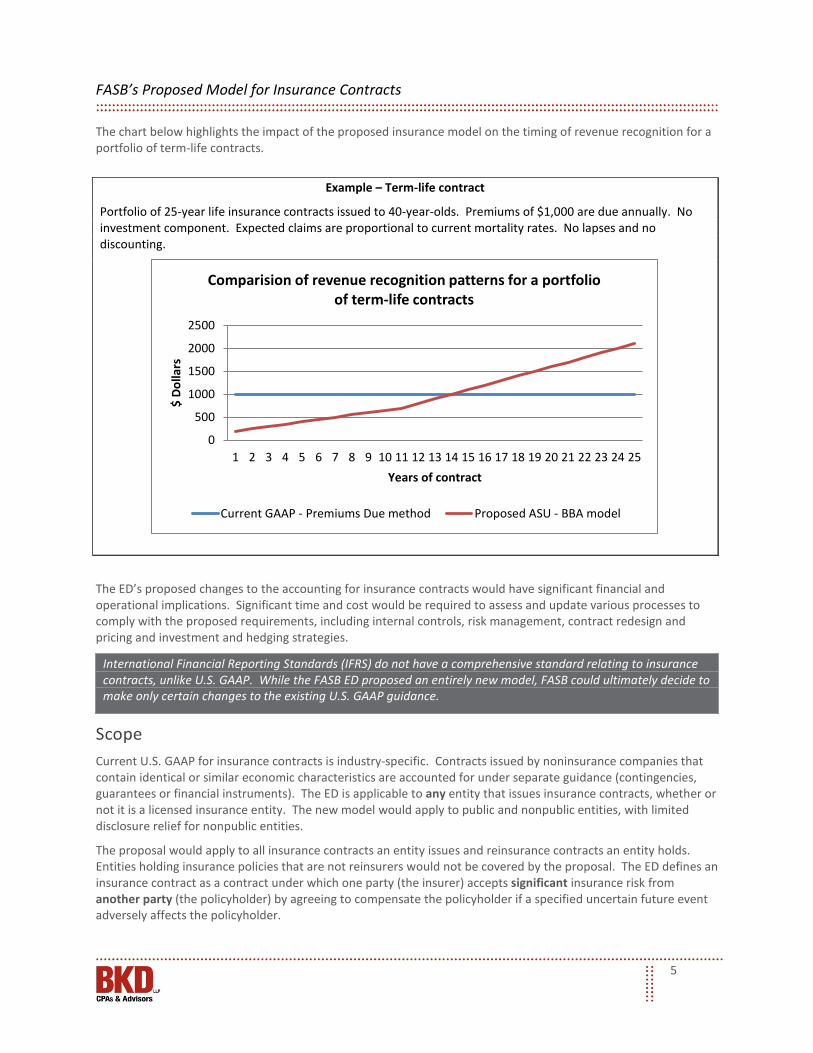

The chart below highlights the impact of the proposed insurance model on the timing of revenue recognition for a portfolio of term-life contracts.

The ED’s proposed changes to the accounting for insurance contracts would have significant financial and operational implications. Significant time and cost would be required to assess and update various processes to comply with the proposed requirements, including internal controls, risk management, contract redesign and pricing and investment and hedging strategies.

Scope Current U.S. GAAP for insurance contracts is industry-specific. Contracts issued by noninsurance companies that contain identical or similar economic characteristics are accounted for under separate guidance (contingencies, guarantees or financial instruments). The ED is applicable to any entity that issues insurance contracts, whether or not it is a licensed insurance entity. The new model would apply to public and nonpublic entities, with limited disclosure relief for nonpublic entities.

The proposal would apply to all insurance contracts an entity issues and reinsurance contracts an entity holds. Entities holding insurance policies that are not reinsurers would not be covered by the proposal. The ED defines an insurance contract as a contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event adversely affects the policyholder.

Example – Term-life contract

Portfolio of 25-year life insurance contracts issued to 40-year-olds. Premiums of $1,000 are due annually. No investment component. Expected claims are proportional to current mortality rates. No lapses and no discounting.

International Financial Reporting Standards (IFRS) do not have a comprehensive standard relating to insurance contracts, unlike U.S. GAAP. While the FASB ED proposed an entirely new model, FASB could ultimately decide to make only certain changes to the existing U.S. GAAP guidance.

0

500

1000

1500

2000

2500

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

$ Do

llars

Years of contract

Comparision of revenue recognition patterns for a portfolio of term-life contracts

Current GAAP - Premiums Due method Proposed ASU - BBA model

FASB’s Proposed Model for Insurance Contracts

6

Entities that self-insure are not in scope since there is no agreement with a third party. For captive entities that only issue insurance contracts to other entities within a group, the parent would not be required to account for those contracts as insurance contracts in the consolidated financial statements; however, the captive’s standalone financial statements would reflect the contracts as insurance. An insurer would assess the significance of insurance risk at the individual contract level. Contracts entered into simultaneously with a single party for the same risk, or otherwise interdependant contracts that are entered into with the same or related party, would be considered a single contract for the purpose of determining risk transfer. A contract exposing the issuer to financial risk without significant insurance risk is not an insurance contract. For example, investment contracts with discretionary participation features would not be covered by the insurance proposal but rather by the financial instruments standard. Credit-related contracts that pay out regardless of whether the counterparty holds the underlying debt instrument or that pay out on a change in credit rating or credit index would continue to be accounted for as derivatives. A life insurance contract with a guaranteed minimum rate of return has financial risk but also has significant mortality risk and therefore is considered an insurance contract.

The table below highlights the more explicit guidance on assessing contracts for significant insurance risk than exists under current U.S. GAAP, which is limited to reinsurance contracts only.

Expansion of “Significant” Insurance Risk

Current U.S. GAAP Proposed Model

There must be a significant chance of significant loss (currently applicable only to reinsurance contracts )

Only one of the estimated cash flow outcomes must have a significant loss (applicable to insurance and reinsurance contracts)

Guarantees The proposed standard would apply to guarantee contracts within the scope of insurance guidance, such as mortgage insurance and financial guarantee insurance contracts, but not to guarantee contracts currently accounted for as derivatives. Entities regularly issuing guarantees to third parties that are accounted for under ASC 460-10 (formerly FIN 45) will be subject to the new insurance requirements. Guarantees specifically addressed by other accounting guidance, such as leasing guidance, will not be in the scope of the proposal. An exception also is provided for guarantees that are both unusual or nonrecurring and unrelated to the type of risk that is the subject of other guarantees issued by the entity. For example, a seller’s indemnification relating to a nonrecurring transaction—such as the sale of a business or an asset—will be considered a “one-off” transaction excluded from the scope. Guarantees between related parties or entities under common control will be exempt from the proposal if they are typically transacted only with those parties and the entity has no similar guarantee transactions issued to third parties. However, the standard will be applicable to intercompany guarantees issued by entities that also issue guarantees to third parties.

FASB’s Proposed Model for Insurance Contracts

7

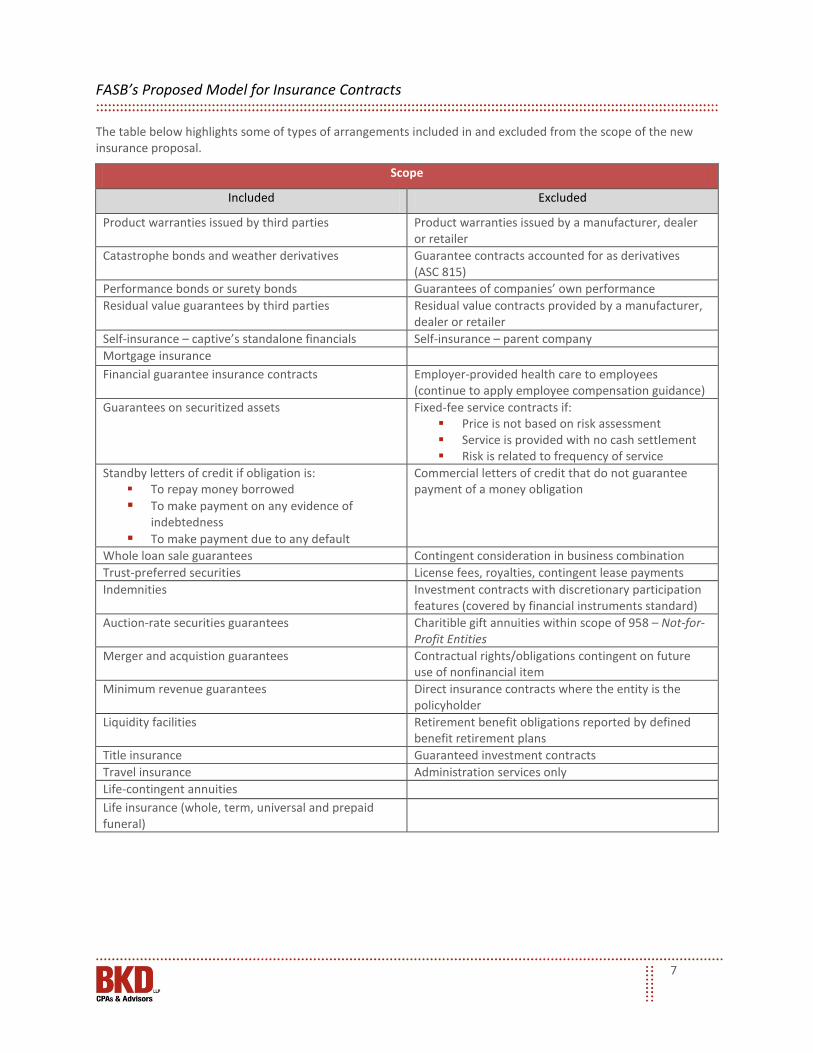

The table below highlights some of types of arrangements included in and excluded from the scope of the new insurance proposal.

Scope

Included Excluded

Product warranties issued by third parties Product warranties issued by a manufacturer, dealer or retailer

Catastrophe bonds and weather derivatives Guarantee contracts accounted for as derivatives (ASC 815)

Performance bonds or surety bonds Guarantees of companies’ own performance Residual value guarantees by third parties Residual value contracts provided by a manufacturer,

dealer or retailer Self-insurance – captive’s standalone financials Self-insurance – parent company Mortgage insurance Financial guarantee insurance contracts Employer-provided health care to employees

(continue to apply employee compensation guidance) Guarantees on securitized assets Fixed-fee service contracts if:

Price is not based on risk assessment Service is provided with no cash settlement Risk is related to frequency of service

Standby letters of credit if obligation is: To repay money borrowed To make payment on any evidence of

indebtedness To make payment due to any default

Commercial letters of credit that do not guarantee payment of a money obligation

Whole loan sale guarantees Contingent consideration in business combination Trust-preferred securities License fees, royalties, contingent lease payments Indemnities Investment contracts with discretionary participation

features (covered by financial instruments standard) Auction-rate securities guarantees Charitible gift annuities within scope of 958 – Not-for-

Profit Entities Merger and acquistion guarantees Contractual rights/obligations contingent on future

use of nonfinancial item Minimum revenue guarantees Direct insurance contracts where the entity is the

policyholder Liquidity facilities Retirement benefit obligations reported by defined

benefit retirement plans Title insurance Guaranteed investment contracts Travel insurance Administration services only Life-contingent annuities Life insurance (whole, term, universal and prepaid funeral)

FASB’s Proposed Model for Insurance Contracts

8

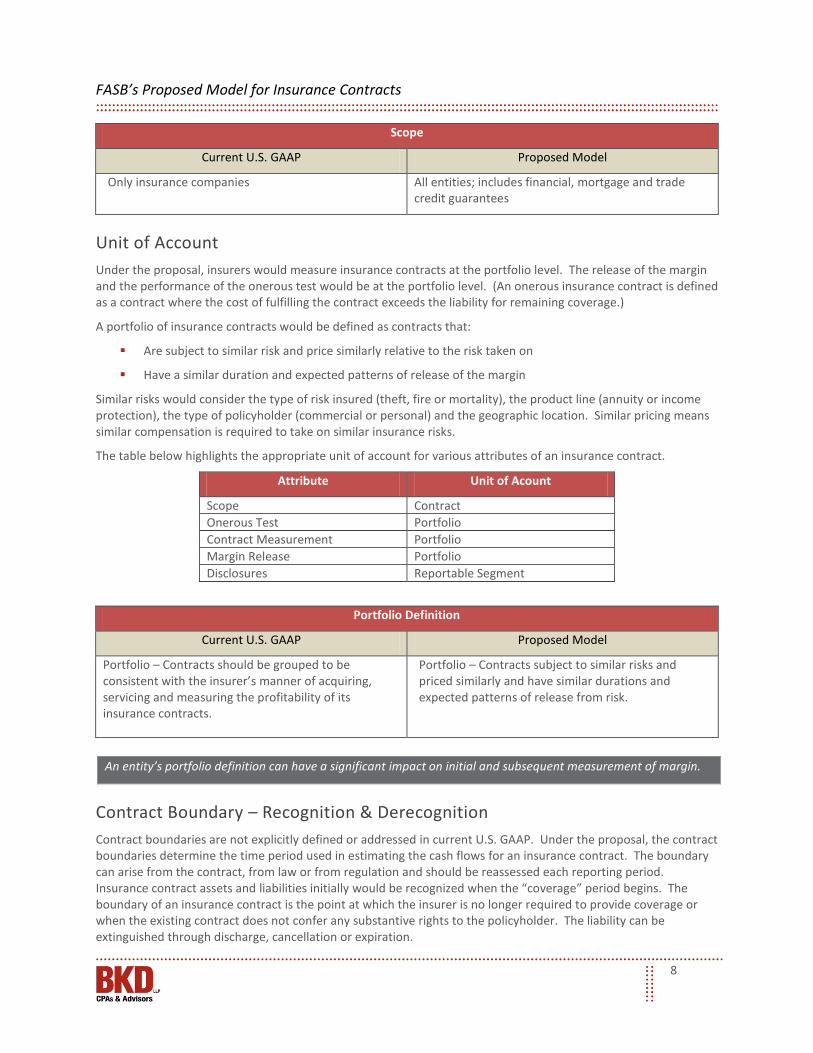

Scope

Current U.S. GAAP Proposed Model

Only insurance companies All entities; includes financial, mortgage and trade credit guarantees

Unit of Account Under the proposal, insurers would measure insurance contracts at the portfolio level. The release of the margin and the performance of the onerous test would be at the portfolio level. (An onerous insurance contract is defined as a contract where the cost of fulfilling the contract exceeds the liability for remaining coverage.)

A portfolio of insurance contracts would be defined as contracts that:

Are subject to similar risk and price similarly relative to the risk taken on

Have a similar duration and expected patterns of release of the margin

Similar risks would consider the type of risk insured (theft, fire or mortality), the product line (annuity or income protection), the type of policyholder (commercial or personal) and the geographic location. Similar pricing means similar compensation is required to take on similar insurance risks.

The table below highlights the appropriate unit of account for various attributes of an insurance contract.

Attribute Unit of Acount

Scope Contract Onerous Test Portfolio Contract Measurement Portfolio Margin Release Portfolio Disclosures Reportable Segment

Portfolio Definition

Current U.S. GAAP Proposed Model

Portfolio – Contracts should be grouped to be consistent with the insurer’s manner of acquiring, servicing and measuring the profitability of its insurance contracts.

Portfolio – Contracts subject to similar risks and priced similarly and have similar durations and expected patterns of release from risk.

Contract Boundary – Recognition & Derecognition Contract boundaries are not explicitly defined or addressed in current U.S. GAAP. Under the proposal, the contract boundaries determine the time period used in estimating the cash flows for an insurance contract. The boundary can arise from the contract, from law or from regulation and should be reassessed each reporting period. Insurance contract assets and liabilities initially would be recognized when the “coverage” period begins. The boundary of an insurance contract is the point at which the insurer is no longer required to provide coverage or when the existing contract does not confer any substantive rights to the policyholder. The liability can be extinguished through discharge, cancellation or expiration.

An entity’s portfolio definition can have a significant impact on initial and subsequent measurement of margin.

FASB’s Proposed Model for Insurance Contracts

9

A contract renewal would be treated as a new contract when the insurer is no longer required to provide coverage or when the existing contract does not confer any substantive rights on the policyholder.

Measurement Models Insurance contract revenue would reflect the amount to which an entity expects to be entitled and recognized in proportion to the value of coverage or services provided. The measurement model is based on a fulfillment objective that reflects the fact that an insurer generally expects to fulfill its liabilities over time by paying benefits and claims to policyholders as they become due, rather than transferring the liabilities to third parties.

The proposal contains two approaches to measure insurance liabilities:

Building Block Approach (BBA) – Fulfillment value method using probability-weighted, expected cash flows

Premium Allocation Approach (PAA) – Similar to the current unearned premium approach for short duration contracts in the preclaims period

The table below highlights the multiple models currently available for recognizing revenue on insurance contracts compared to the single principal-based approach in the proposed standard.

Recognition & Measurement

Current U.S. GAAP Proposed Model

Traditional life insurance – Revenue is recognized on policy’s contractual due dates (premium due method).

Universal life, deferred annuities, variable and equity-based life and annuity products – Revenues are based on actual amounts assessed against the policyholder account balance.

Limited-payment contracts – A portion of the premium is deferred and recognized in a constant relationship with insurance in force.

Revenue shall reflect the transfer of promised services arising from the insurance contract in an amount that reflects the consideration to which the entity expects to be entitled.

Building Block Approach (BBA) The model uses a building block approach to measure the insurance contract liability, including:

Projection of future cash flows, discounted to reflect the time value of money

Application of margin

The proposed model minimizes the number of models for measuring insurance contracts and better aligns with the soon to be issued Accounting Standard Update – Revenue Recognition (Topic 606).

FASB’s Proposed Model for Insurance Contracts

10

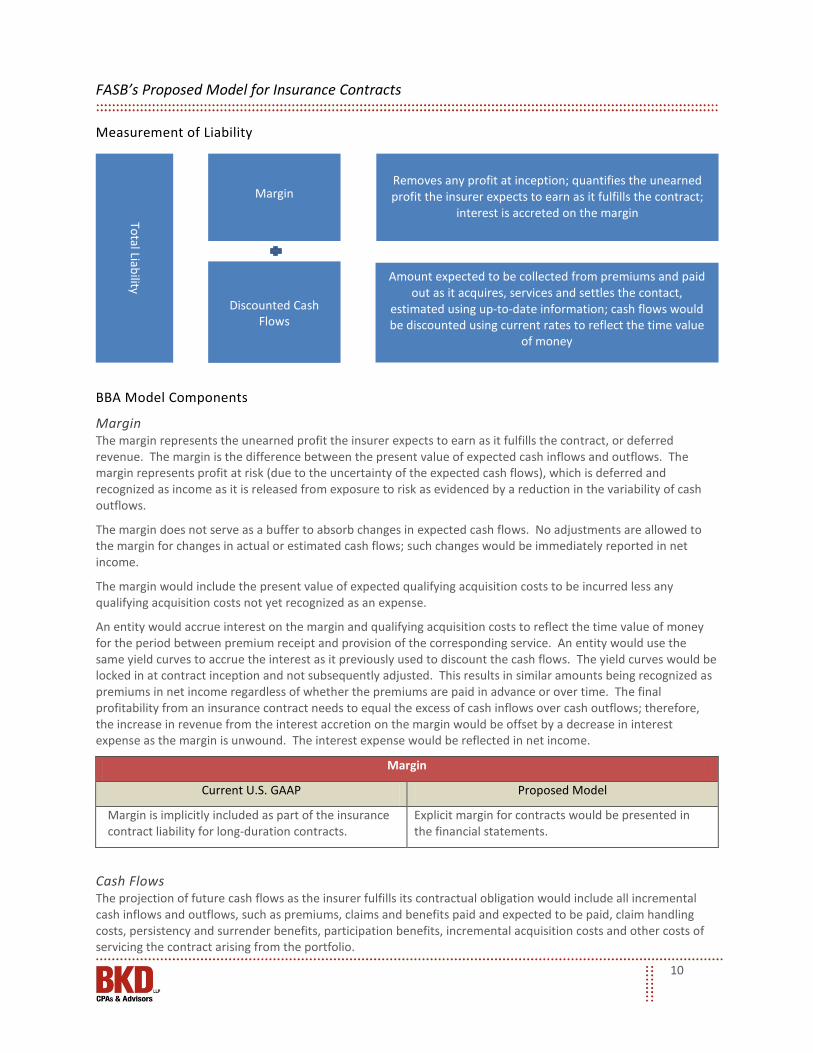

Measurement of Liability

BBA Model Components

Margin The margin represents the unearned profit the insurer expects to earn as it fulfills the contract, or deferred revenue. The margin is the difference between the present value of expected cash inflows and outflows. The margin represents profit at risk (due to the uncertainty of the expected cash flows), which is deferred and recognized as income as it is released from exposure to risk as evidenced by a reduction in the variability of cash outflows.

The margin does not serve as a buffer to absorb changes in expected cash flows. No adjustments are allowed to the margin for changes in actual or estimated cash flows; such changes would be immediately reported in net income.

The margin would include the present value of expected qualifying acquisition costs to be incurred less any qualifying acquisition costs not yet recognized as an expense.

An entity would accrue interest on the margin and qualifying acquisition costs to reflect the time value of money for the period between premium receipt and provision of the corresponding service. An entity would use the same yield curves to accrue the interest as it previously used to discount the cash flows. The yield curves would be locked in at contract inception and not subsequently adjusted. This results in similar amounts being recognized as premiums in net income regardless of whether the premiums are paid in advance or over time. The final profitability from an insurance contract needs to equal the excess of cash inflows over cash outflows; therefore, the increase in revenue from the interest accretion on the margin would be offset by a decrease in interest expense as the margin is unwound. The interest expense would be reflected in net income.

Margin

Current U.S. GAAP Proposed Model

Margin is implicitly included as part of the insurance contract liability for long-duration contracts.

Explicit margin for contracts would be presented in the financial statements.

Cash Flows The projection of future cash flows as the insurer fulfills its contractual obligation would include all incremental cash inflows and outflows, such as premiums, claims and benefits paid and expected to be paid, claim handling costs, persistency and surrender benefits, participation benefits, incremental acquisition costs and other costs of servicing the contract arising from the portfolio.

Total Liability

Margin

Discounted Cash Flows

Removes any profit at inception; quantifies the unearned profit the insurer expects to earn as it fulfills the contract;

interest is accreted on the margin

Amount expected to be collected from premiums and paid out as it acquires, services and settles the contact,

estimated using up-to-date information; cash flows would be discounted using current rates to reflect the time value

of money

FASB’s Proposed Model for Insurance Contracts

11

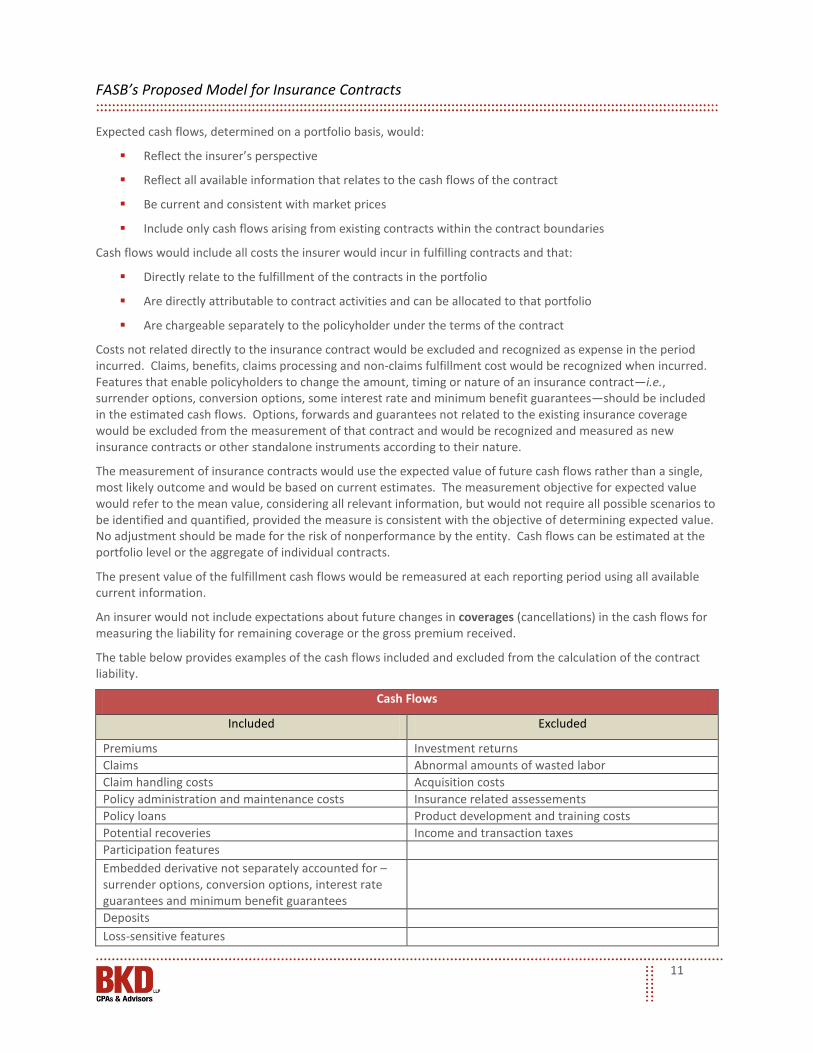

Expected cash flows, determined on a portfolio basis, would:

Reflect the insurer’s perspective

Reflect all available information that relates to the cash flows of the contract

Be current and consistent with market prices

Include only cash flows arising from existing contracts within the contract boundaries

Cash flows would include all costs the insurer would incur in fulfilling contracts and that:

Directly relate to the fulfillment of the contracts in the portfolio

Are directly attributable to contract activities and can be allocated to that portfolio

Are chargeable separately to the policyholder under the terms of the contract

Costs not related directly to the insurance contract would be excluded and recognized as expense in the period incurred. Claims, benefits, claims processing and non-claims fulfillment cost would be recognized when incurred. Features that enable policyholders to change the amount, timing or nature of an insurance contract—i.e., surrender options, conversion options, some interest rate and minimum benefit guarantees—should be included in the estimated cash flows. Options, forwards and guarantees not related to the existing insurance coverage would be excluded from the measurement of that contract and would be recognized and measured as new insurance contracts or other standalone instruments according to their nature.

The measurement of insurance contracts would use the expected value of future cash flows rather than a single, most likely outcome and would be based on current estimates. The measurement objective for expected value would refer to the mean value, considering all relevant information, but would not require all possible scenarios to be identified and quantified, provided the measure is consistent with the objective of determining expected value. No adjustment should be made for the risk of nonperformance by the entity. Cash flows can be estimated at the portfolio level or the aggregate of individual contracts.

The present value of the fulfillment cash flows would be remeasured at each reporting period using all available current information.

An insurer would not include expectations about future changes in coverages (cancellations) in the cash flows for measuring the liability for remaining coverage or the gross premium received.

The table below provides examples of the cash flows included and excluded from the calculation of the contract liability.

Cash Flows

Included Excluded

Premiums Investment returns Claims Abnormal amounts of wasted labor Claim handling costs Acquisition costs Policy administration and maintenance costs Insurance related assessements Policy loans Product development and training costs Potential recoveries Income and transaction taxes Participation features Embedded derivative not separately accounted for – surrender options, conversion options, interest rate guarantees and minimum benefit guarantees

Deposits Loss-sensitive features

FASB’s Proposed Model for Insurance Contracts

12

Cash Flow Assumptions

Current U.S. GAAP Proposed Model

For long-duration contracts, assumptions are locked in at contract inception unless onerous.

Updated each reporting period

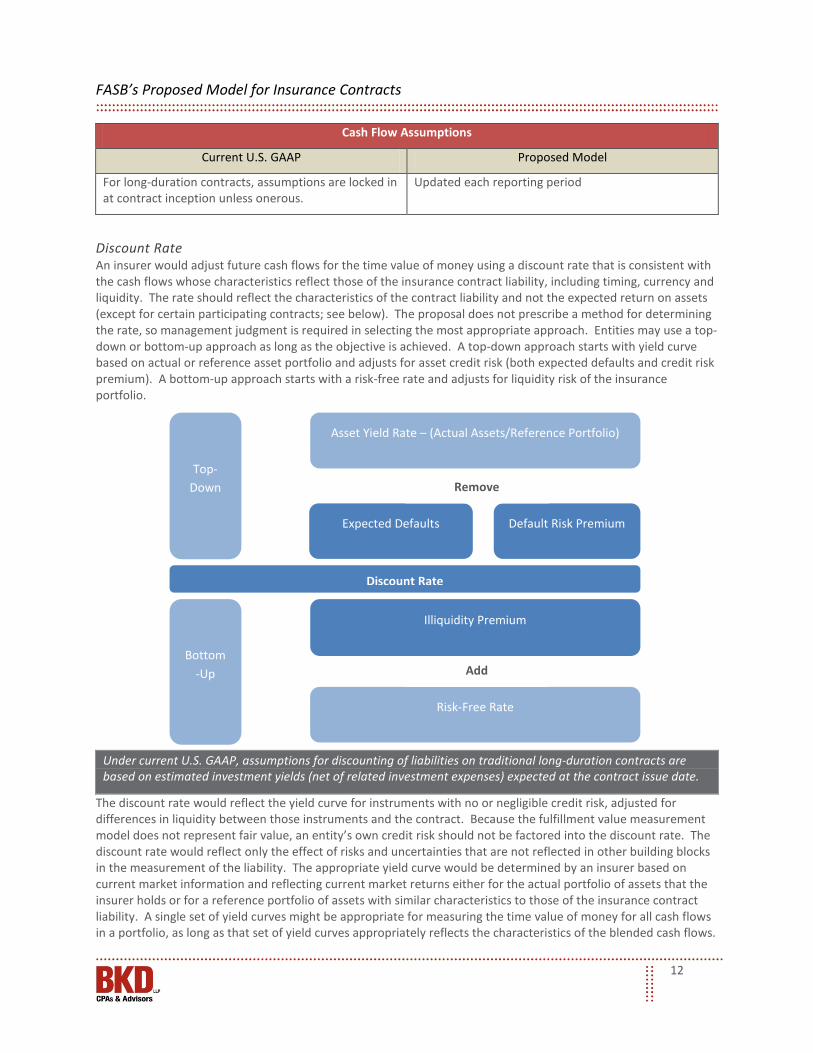

Discount Rate An insurer would adjust future cash flows for the time value of money using a discount rate that is consistent with the cash flows whose characteristics reflect those of the insurance contract liability, including timing, currency and liquidity. The rate should reflect the characteristics of the contract liability and not the expected return on assets (except for certain participating contracts; see below). The proposal does not prescribe a method for determining the rate, so management judgment is required in selecting the most appropriate approach. Entities may use a top-down or bottom-up approach as long as the objective is achieved. A top-down approach starts with yield curve based on actual or reference asset portfolio and adjusts for asset credit risk (both expected defaults and credit risk premium). A bottom-up approach starts with a risk-free rate and adjusts for liquidity risk of the insurance portfolio.

The discount rate would reflect the yield curve for instruments with no or negligible credit risk, adjusted for differences in liquidity between those instruments and the contract. Because the fulfillment value measurement model does not represent fair value, an entity’s own credit risk should not be factored into the discount rate. The discount rate would reflect only the effect of risks and uncertainties that are not reflected in other building blocks in the measurement of the liability. The appropriate yield curve would be determined by an insurer based on current market information and reflecting current market returns either for the actual portfolio of assets that the insurer holds or for a reference portfolio of assets with similar characteristics to those of the insurance contract liability. A single set of yield curves might be appropriate for measuring the time value of money for all cash flows in a portfolio, as long as that set of yield curves appropriately reflects the characteristics of the blended cash flows.

Under current U.S. GAAP, assumptions for discounting of liabilities on traditional long-duration contracts are based on estimated investment yields (net of related investment expenses) expected at the contract issue date.

Top-Down

Discount Rate

Bottom-Up

Asset Yield Rate – (Actual Assets/Reference Portfolio)

Expected Defaults Default Risk Premium

Illiquidity Premium

Risk-Free Rate

Remove

Add

FASB’s Proposed Model for Insurance Contracts

13

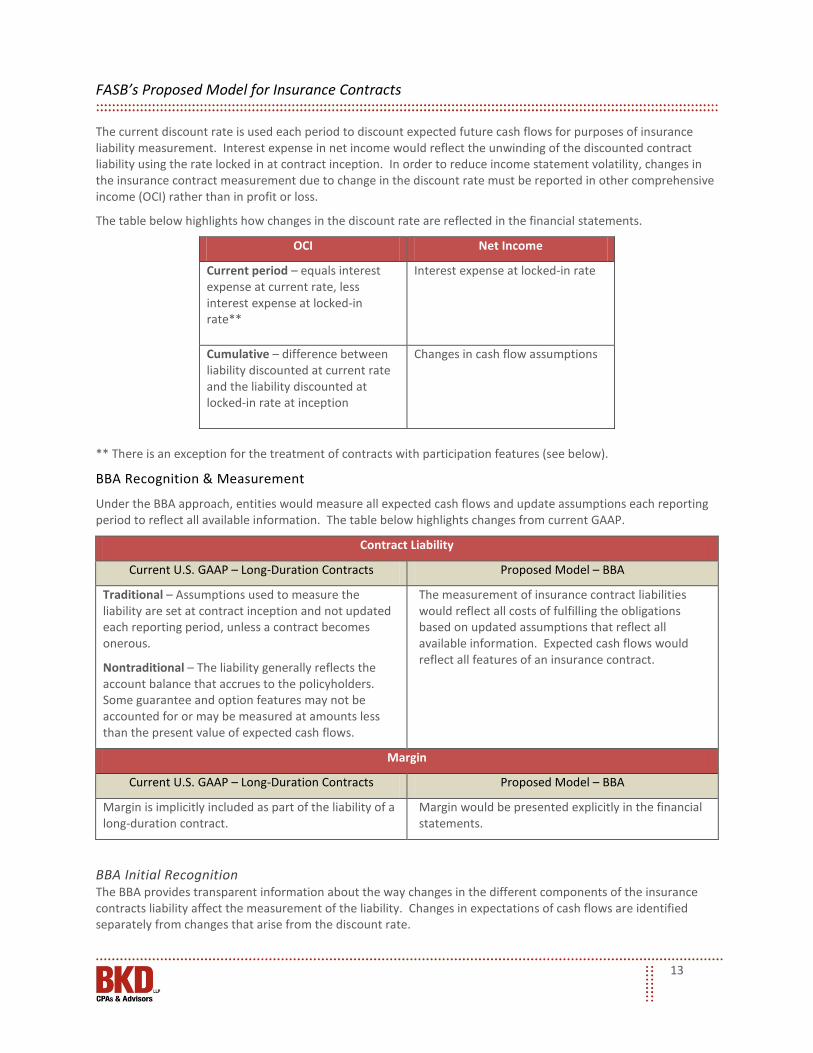

The current discount rate is used each period to discount expected future cash flows for purposes of insurance liability measurement. Interest expense in net income would reflect the unwinding of the discounted contract liability using the rate locked in at contract inception. In order to reduce income statement volatility, changes in the insurance contract measurement due to change in the discount rate must be reported in other comprehensive income (OCI) rather than in profit or loss.

The table below highlights how changes in the discount rate are reflected in the financial statements.

OCI Net Income

Current period – equals interest expense at current rate, less interest expense at locked-in rate**

Interest expense at locked-in rate

Cumulative – difference between liability discounted at current rate and the liability discounted at locked-in rate at inception

Changes in cash flow assumptions

** There is an exception for the treatment of contracts with participation features (see below).

BBA Recognition & Measurement

Under the BBA approach, entities would measure all expected cash flows and update assumptions each reporting period to reflect all available information. The table below highlights changes from current GAAP.

Contract Liability

Current U.S. GAAP – Long-Duration Contracts Proposed Model – BBA

Traditional – Assumptions used to measure the liability are set at contract inception and not updated each reporting period, unless a contract becomes onerous.

Nontraditional – The liability generally reflects the account balance that accrues to the policyholders. Some guarantee and option features may not be accounted for or may be measured at amounts less than the present value of expected cash flows.

The measurement of insurance contract liabilities would reflect all costs of fulfilling the obligations based on updated assumptions that reflect all available information. Expected cash flows would reflect all features of an insurance contract.

Margin

Current U.S. GAAP – Long-Duration Contracts Proposed Model – BBA

Margin is implicitly included as part of the liability of a long-duration contract.

Margin would be presented explicitly in the financial statements.

BBA Initial Recognition The BBA provides transparent information about the way changes in the different components of the insurance contracts liability affect the measurement of the liability. Changes in expectations of cash flows are identified separately from changes that arise from the discount rate.

FASB’s Proposed Model for Insurance Contracts

14

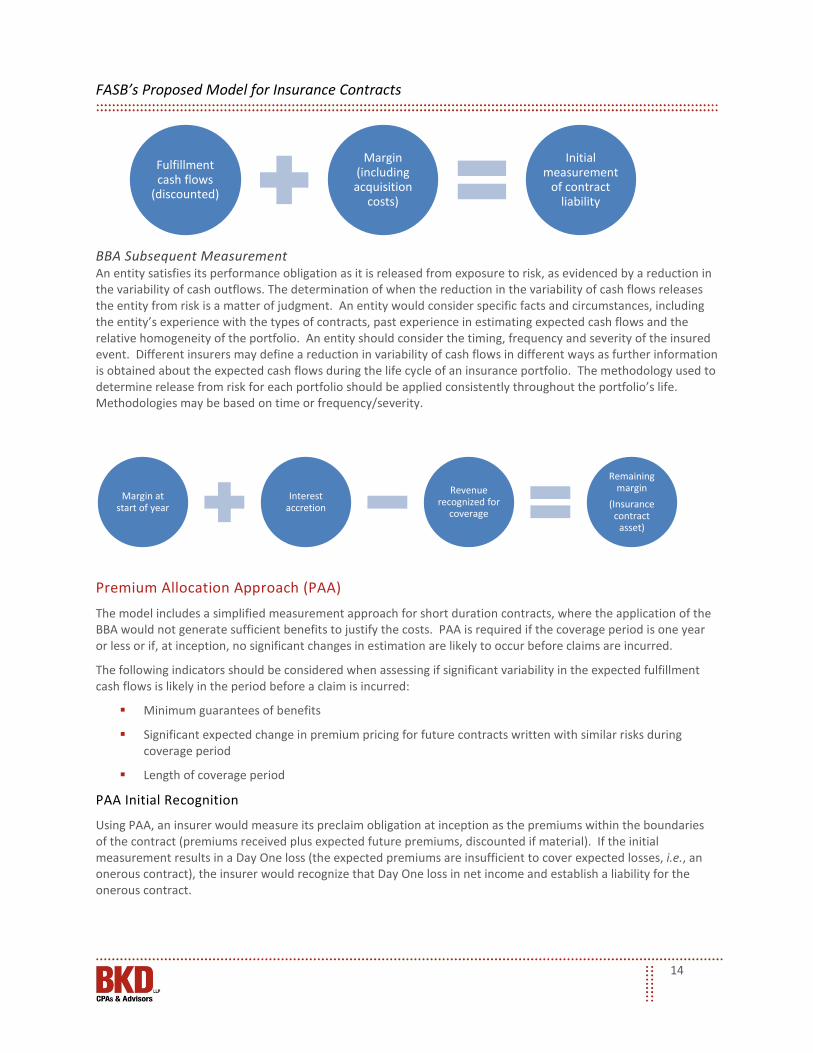

BBA Subsequent Measurement An entity satisfies its performance obligation as it is released from exposure to risk, as evidenced by a reduction in the variability of cash outflows. The determination of when the reduction in the variability of cash flows releases the entity from risk is a matter of judgment. An entity would consider specific facts and circumstances, including the entity’s experience with the types of contracts, past experience in estimating expected cash flows and the relative homogeneity of the portfolio. An entity should consider the timing, frequency and severity of the insured event. Different insurers may define a reduction in variability of cash flows in different ways as further information is obtained about the expected cash flows during the life cycle of an insurance portfolio. The methodology used to determine release from risk for each portfolio should be applied consistently throughout the portfolio’s life. Methodologies may be based on time or frequency/severity.

Premium Allocation Approach (PAA) The model includes a simplified measurement approach for short duration contracts, where the application of the BBA would not generate sufficient benefits to justify the costs. PAA is required if the coverage period is one year or less or if, at inception, no significant changes in estimation are likely to occur before claims are incurred.

The following indicators should be considered when assessing if significant variability in the expected fulfillment cash flows is likely in the period before a claim is incurred:

Minimum guarantees of benefits

Significant expected change in premium pricing for future contracts written with similar risks during coverage period

Length of coverage period

PAA Initial Recognition

Using PAA, an insurer would measure its preclaim obligation at inception as the premiums within the boundaries of the contract (premiums received plus expected future premiums, discounted if material). If the initial measurement results in a Day One loss (the expected premiums are insufficient to cover expected losses, i.e., an onerous contract), the insurer would recognize that Day One loss in net income and establish a liability for the onerous contract.

Fulfillment cash flows

(discounted)

Margin (including acquisition

costs)

Initial measurement

of contract liability

Margin at start of year

Interest accretion

Revenue recognized for

coverage

Remaining margin

(Insurance contract

asset)

FASB’s Proposed Model for Insurance Contracts

15

PAA Subsequent Measurement

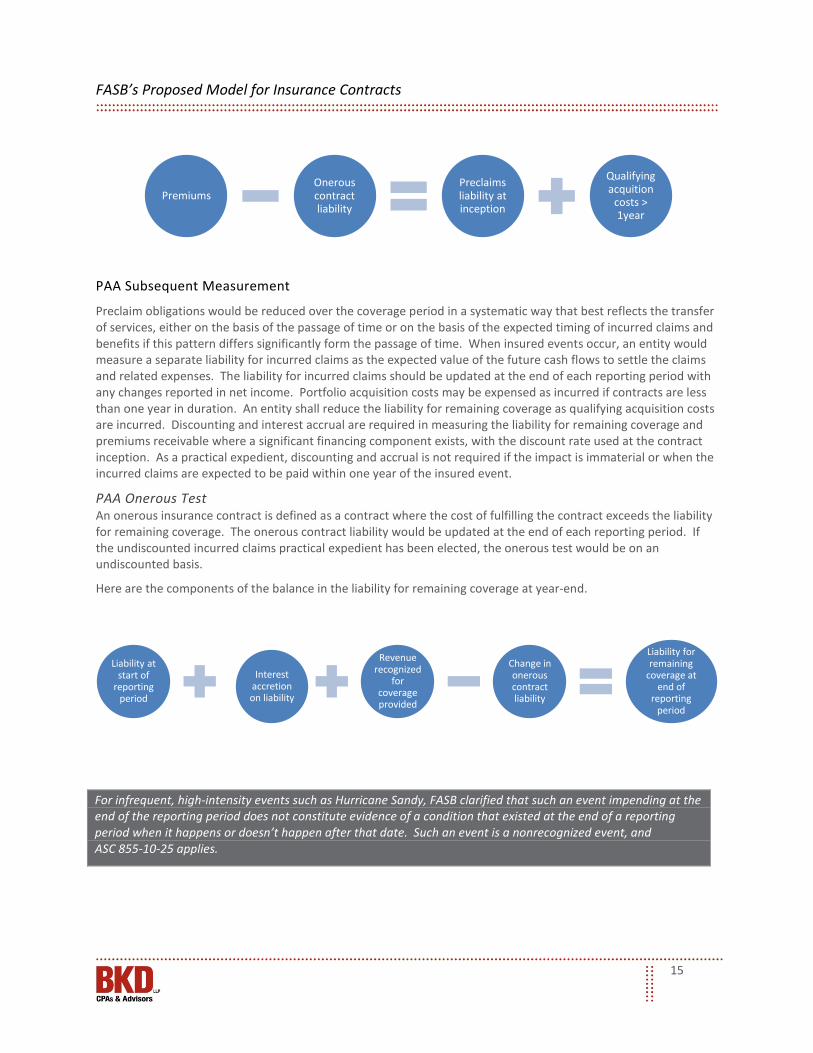

Preclaim obligations would be reduced over the coverage period in a systematic way that best reflects the transfer of services, either on the basis of the passage of time or on the basis of the expected timing of incurred claims and benefits if this pattern differs significantly form the passage of time. When insured events occur, an entity would measure a separate liability for incurred claims as the expected value of the future cash flows to settle the claims and related expenses. The liability for incurred claims should be updated at the end of each reporting period with any changes reported in net income. Portfolio acquisition costs may be expensed as incurred if contracts are less than one year in duration. An entity shall reduce the liability for remaining coverage as qualifying acquisition costs are incurred. Discounting and interest accrual are required in measuring the liability for remaining coverage and premiums receivable where a significant financing component exists, with the discount rate used at the contract inception. As a practical expedient, discounting and accrual is not required if the impact is immaterial or when the incurred claims are expected to be paid within one year of the insured event.

PAA Onerous Test An onerous insurance contract is defined as a contract where the cost of fulfilling the contract exceeds the liability for remaining coverage. The onerous contract liability would be updated at the end of each reporting period. If the undiscounted incurred claims practical expedient has been elected, the onerous test would be on an undiscounted basis.

Here are the components of the balance in the liability for remaining coverage at year-end.

Premiums Onerous contract liability

Preclaims liability at inception

Qualifying acquition

costs > 1year

Liability at start of

reporting period

Interest accretion on liability

Revenue recognized

for coverage provided

Change in onerous contract liability

Liability for remaining

coverage at end of

reporting period

For infrequent, high-intensity events such as Hurricane Sandy, FASB clarified that such an event impending at the end of the reporting period does not constitute evidence of a condition that existed at the end of a reporting period when it happens or doesn’t happen after that date. Such an event is a nonrecognized event, and ASC 855-10-25 applies.

FASB’s Proposed Model for Insurance Contracts

16

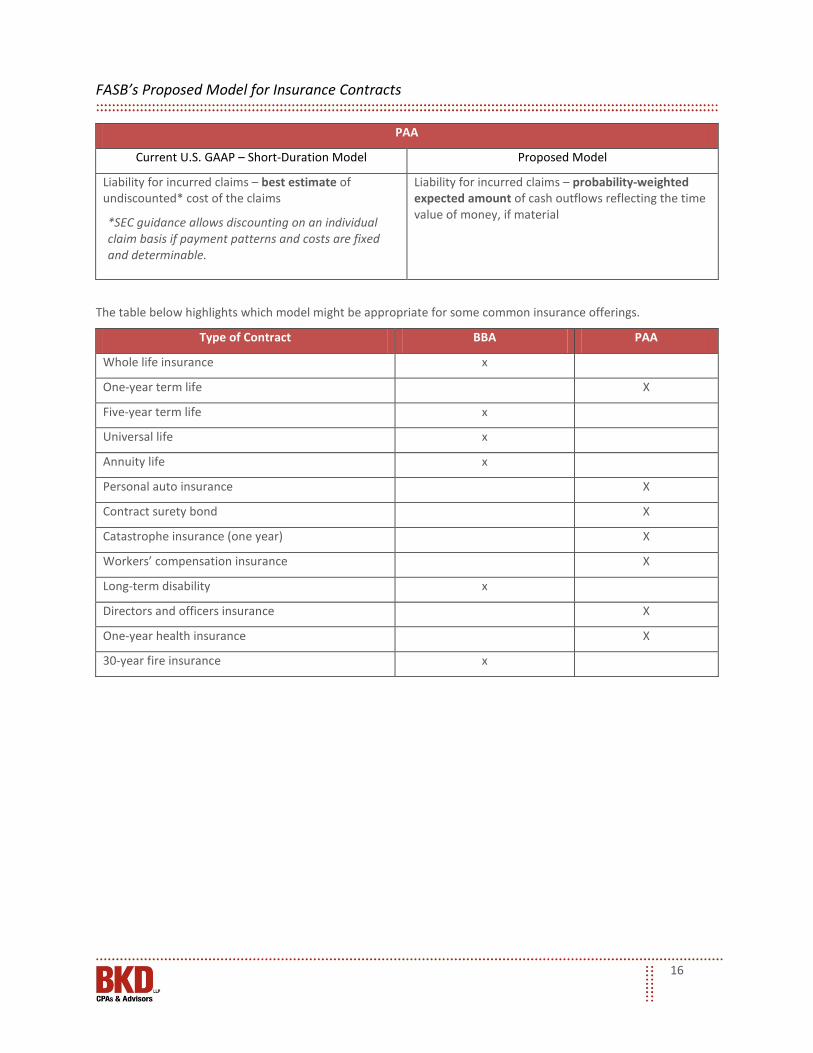

PAA

Current U.S. GAAP – Short-Duration Model Proposed Model

Liability for incurred claims – best estimate of undiscounted* cost of the claims

*SEC guidance allows discounting on an individual claim basis if payment patterns and costs are fixed and determinable.

Liability for incurred claims – probability-weighted expected amount of cash outflows reflecting the time value of money, if material

The table below highlights which model might be appropriate for some common insurance offerings.

Type of Contract BBA PAA

Whole life insurance x

One-year term life X

Five-year term life x

Universal life x

Annuity life x

Personal auto insurance X

Contract surety bond X

Catastrophe insurance (one year) X

Workers’ compensation insurance X

Long-term disability x

Directors and officers insurance X

One-year health insurance X

30-year fire insurance x

FASB’s Proposed Model for Insurance Contracts

17

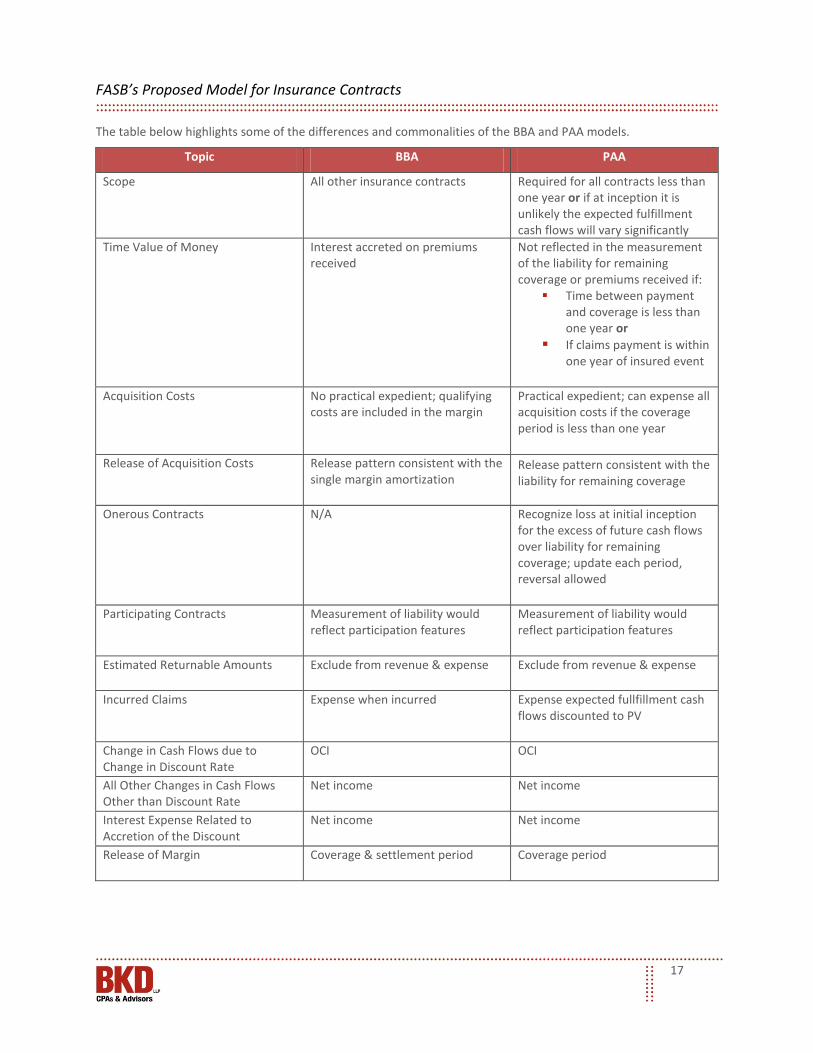

The table below highlights some of the differences and commonalities of the BBA and PAA models.

Topic BBA PAA

Scope All other insurance contracts

Required for all contracts less than one year or if at inception it is unlikely the expected fulfillment cash flows will vary significantly

Time Value of Money Interest accreted on premiums received

Not reflected in the measurement of the liability for remaining coverage or premiums received if:

Time between payment and coverage is less than one year or

If claims payment is within one year of insured event

Acquisition Costs No practical expedient; qualifying

costs are included in the margin Practical expedient; can expense all acquisition costs if the coverage period is less than one year

Release of Acquisition Costs Release pattern consistent with the single margin amortization

Release pattern consistent with the liability for remaining coverage

Onerous Contracts

N/A Recognize loss at initial inception for the excess of future cash flows over liability for remaining coverage; update each period, reversal allowed

Participating Contracts Measurement of liability would reflect participation features

Measurement of liability would reflect participation features

Estimated Returnable Amounts

Exclude from revenue & expense

Exclude from revenue & expense

Incurred Claims Expense when incurred

Expense expected fullfillment cash flows discounted to PV

Change in Cash Flows due to Change in Discount Rate

OCI

OCI

All Other Changes in Cash Flows Other than Discount Rate

Net income

Net income

Interest Expense Related to Accretion of the Discount

Net income

Net income

Release of Margin Coverage & settlement period

Coverage period

FASB’s Proposed Model for Insurance Contracts

18

Other Items

Acquisition Costs

Recognition

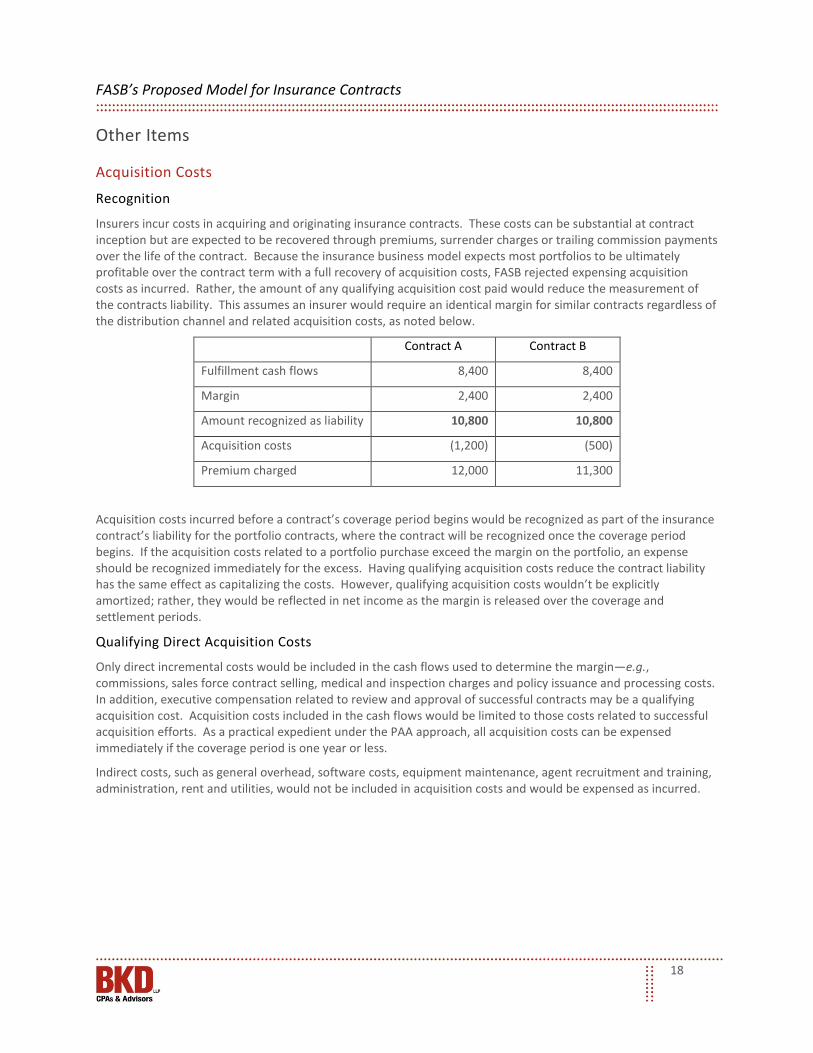

Insurers incur costs in acquiring and originating insurance contracts. These costs can be substantial at contract inception but are expected to be recovered through premiums, surrender charges or trailing commission payments over the life of the contract. Because the insurance business model expects most portfolios to be ultimately profitable over the contract term with a full recovery of acquisition costs, FASB rejected expensing acquisition costs as incurred. Rather, the amount of any qualifying acquisition cost paid would reduce the measurement of the contracts liability. This assumes an insurer would require an identical margin for similar contracts regardless of the distribution channel and related acquisition costs, as noted below.

Contract A Contract B

Fulfillment cash flows 8,400 8,400

Margin 2,400 2,400

Amount recognized as liability 10,800 10,800

Acquisition costs (1,200) (500)

Premium charged 12,000 11,300

Acquisition costs incurred before a contract’s coverage period begins would be recognized as part of the insurance contract’s liability for the portfolio contracts, where the contract will be recognized once the coverage period begins. If the acquisition costs related to a portfolio purchase exceed the margin on the portfolio, an expense should be recognized immediately for the excess. Having qualifying acquisition costs reduce the contract liability has the same effect as capitalizing the costs. However, qualifying acquisition costs wouldn’t be explicitly amortized; rather, they would be reflected in net income as the margin is released over the coverage and settlement periods.

Qualifying Direct Acquisition Costs

Only direct incremental costs would be included in the cash flows used to determine the margin—e.g., commissions, sales force contract selling, medical and inspection charges and policy issuance and processing costs. In addition, executive compensation related to review and approval of successful contracts may be a qualifying acquisition cost. Acquisition costs included in the cash flows would be limited to those costs related to successful acquisition efforts. As a practical expedient under the PAA approach, all acquisition costs can be expensed immediately if the coverage period is one year or less.

Indirect costs, such as general overhead, software costs, equipment maintenance, agent recruitment and training, administration, rent and utilities, would not be included in acquisition costs and would be expensed as incurred.

FASB’s Proposed Model for Insurance Contracts

19

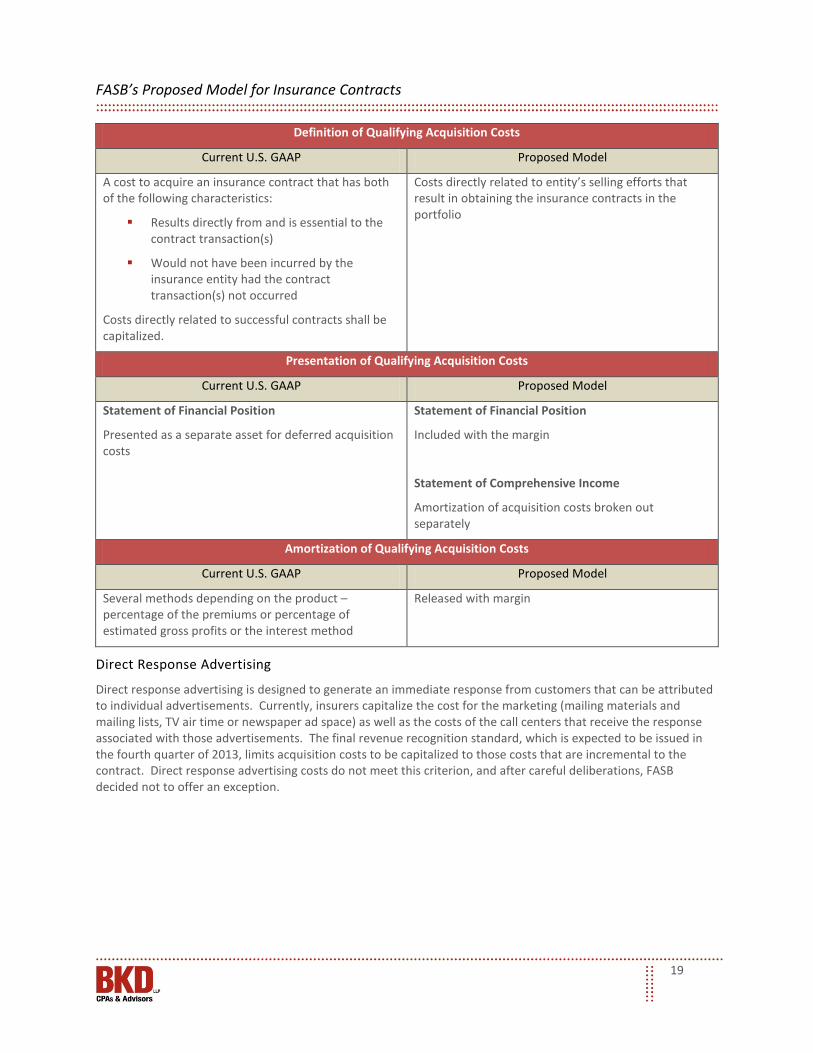

Definition of Qualifying Acquisition Costs

Current U.S. GAAP Proposed Model

A cost to acquire an insurance contract that has both of the following characteristics:

Results directly from and is essential to the contract transaction(s)

Would not have been incurred by the insurance entity had the contract transaction(s) not occurred

Costs directly related to successful contracts shall be capitalized.

Costs directly related to entity’s selling efforts that result in obtaining the insurance contracts in the portfolio

Presentation of Qualifying Acquisition Costs

Current U.S. GAAP Proposed Model

Statement of Financial Position

Presented as a separate asset for deferred acquisition costs

Statement of Financial Position

Included with the margin

Statement of Comprehensive Income

Amortization of acquisition costs broken out separately

Amortization of Qualifying Acquisition Costs

Current U.S. GAAP Proposed Model

Several methods depending on the product – percentage of the premiums or percentage of estimated gross profits or the interest method

Released with margin

Direct Response Advertising

Direct response advertising is designed to generate an immediate response from customers that can be attributed to individual advertisements. Currently, insurers capitalize the cost for the marketing (mailing materials and mailing lists, TV air time or newspaper ad space) as well as the costs of the call centers that receive the response associated with those advertisements. The final revenue recognition standard, which is expected to be issued in the fourth quarter of 2013, limits acquisition costs to be capitalized to those costs that are incremental to the contract. Direct response advertising costs do not meet this criterion, and after careful deliberations, FASB decided not to offer an exception.

FASB’s Proposed Model for Insurance Contracts

20

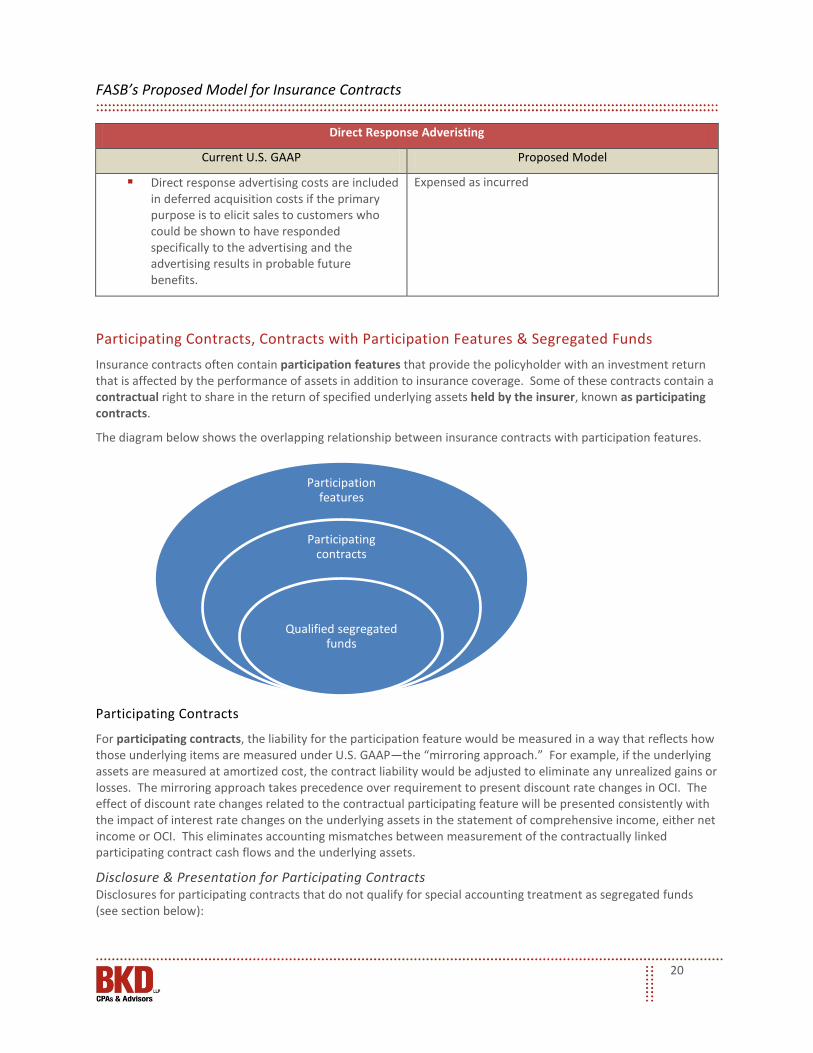

Direct Response Adveristing

Current U.S. GAAP Proposed Model

Direct response advertising costs are included in deferred acquisition costs if the primary purpose is to elicit sales to customers who could be shown to have responded specifically to the advertising and the advertising results in probable future benefits.

Expensed as incurred

Participating Contracts, Contracts with Participation Features & Segregated Funds Insurance contracts often contain participation features that provide the policyholder with an investment return that is affected by the performance of assets in addition to insurance coverage. Some of these contracts contain a contractual right to share in the return of specified underlying assets held by the insurer, known as participating contracts.

The diagram below shows the overlapping relationship between insurance contracts with participation features.

Participating Contracts

For participating contracts, the liability for the participation feature would be measured in a way that reflects how those underlying items are measured under U.S. GAAP—the “mirroring approach.” For example, if the underlying assets are measured at amortized cost, the contract liability would be adjusted to eliminate any unrealized gains or losses. The mirroring approach takes precedence over requirement to present discount rate changes in OCI. The effect of discount rate changes related to the contractual participating feature will be presented consistently with the impact of interest rate changes on the underlying assets in the statement of comprehensive income, either net income or OCI. This eliminates accounting mismatches between measurement of the contractually linked participating contract cash flows and the underlying assets.

Disclosure & Presentation for Participating Contracts Disclosures for participating contracts that do not qualify for special accounting treatment as segregated funds (see section below):

Participation features

Participating contracts

Qualified segregated funds

FASB’s Proposed Model for Insurance Contracts

21

General description of the participation features and the amounts accrued to the benefit of the policyholders in the period

For nondiscretionary obligations:

• How participation features are measured • Amount for which asset or liability was adjusted and whether the amount is included in net

income or OCI

Participation Features

Some contracts have investment returns that are affected by asset performance, but the credited interest is at the insurer’s discretion, i.e., a universal life contract. An index-linked policy provides a contractual right to the performance of specified assets (the index), but the underlying assets are not held by the insurer. While these contracts both contain participating features, they would not be considered participating contracts. For these types of insurance contracts—where the cash flows are not subject to mirroring but are affected by asset returns—the discretionary payments would be included in the expected present value of fulfillment cash flows in measuring an insurance contract; the discount rate should reflect the extent to which the estimated cash flows are affected by the return from those assets.

When there is a change in the insurance contract’s liability caused by an expected change in crediting rate, an insurer should reset the locked-in discount rate to the expected crediting rate to determine the interest expense in net income. Since this expected crediting rate also would be applied to the liability measurement, the effects of changes in discount rates for the participating cash flow portion of contracts would be presented in profit or loss instead of OCI. Using this approach, the interest expense reflects the variable-rate nature of the financing implicit in the insurance contract cash flows.

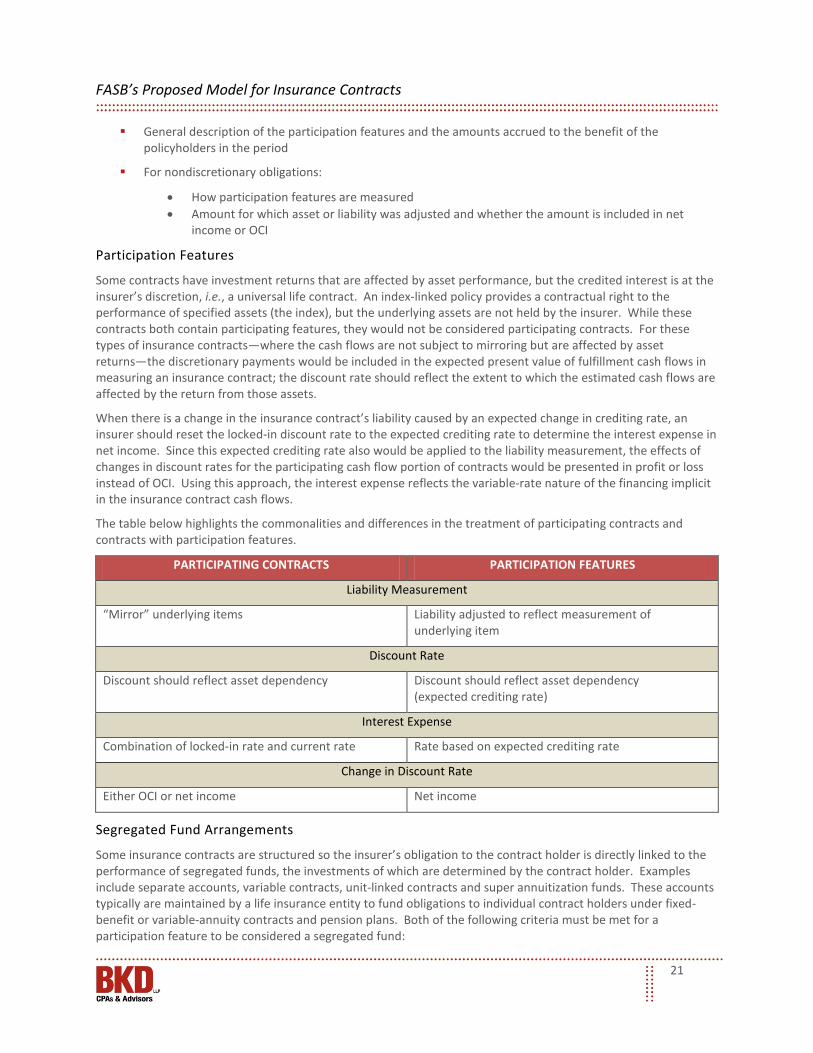

The table below highlights the commonalities and differences in the treatment of participating contracts and contracts with participation features.

PARTICIPATING CONTRACTS PARTICIPATION FEATURES

Liability Measurement

“Mirror” underlying items Liability adjusted to reflect measurement of underlying item

Discount Rate

Discount should reflect asset dependency Discount should reflect asset dependency (expected crediting rate)

Interest Expense

Combination of locked-in rate and current rate Rate based on expected crediting rate

Change in Discount Rate

Either OCI or net income Net income

Segregated Fund Arrangements

Some insurance contracts are structured so the insurer’s obligation to the contract holder is directly linked to the performance of segregated funds, the investments of which are determined by the contract holder. Examples include separate accounts, variable contracts, unit-linked contracts and super annuitization funds. These accounts typically are maintained by a life insurance entity to fund obligations to individual contract holders under fixed-benefit or variable-annuity contracts and pension plans. Both of the following criteria must be met for a participation feature to be considered a segregated fund:

FASB’s Proposed Model for Insurance Contracts

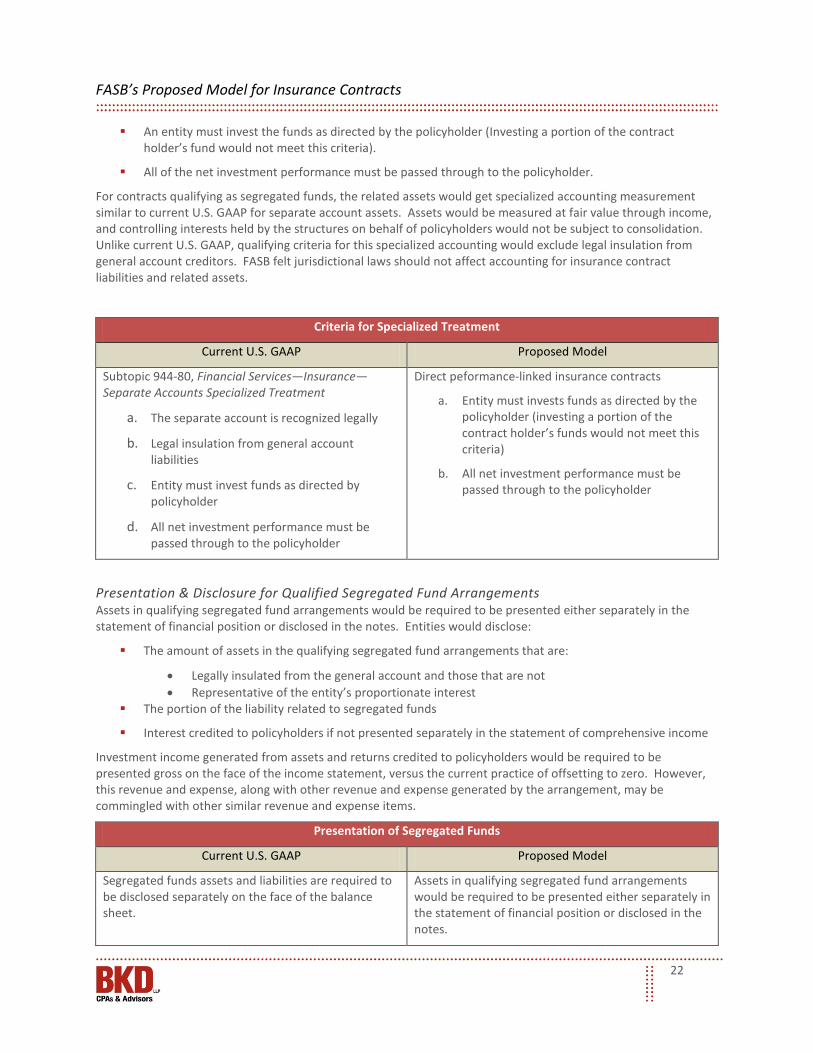

22

An entity must invest the funds as directed by the policyholder (Investing a portion of the contract holder’s fund would not meet this criteria).

All of the net investment performance must be passed through to the policyholder.

For contracts qualifying as segregated funds, the related assets would get specialized accounting measurement similar to current U.S. GAAP for separate account assets. Assets would be measured at fair value through income, and controlling interests held by the structures on behalf of policyholders would not be subject to consolidation. Unlike current U.S. GAAP, qualifying criteria for this specialized accounting would exclude legal insulation from general account creditors. FASB felt jurisdictional laws should not affect accounting for insurance contract liabilities and related assets.

Criteria for Specialized Treatment

Current U.S. GAAP Proposed Model

Subtopic 944-80, Financial Services—Insurance—Separate Accounts Specialized Treatment

a. The separate account is recognized legally

b. Legal insulation from general account liabilities

c. Entity must invest funds as directed by policyholder

d. All net investment performance must be passed through to the policyholder

Direct peformance-linked insurance contracts

a. Entity must invests funds as directed by the policyholder (investing a portion of the contract holder’s funds would not meet this criteria)

b. All net investment performance must be passed through to the policyholder

Presentation & Disclosure for Qualified Segregated Fund Arrangements Assets in qualifying segregated fund arrangements would be required to be presented either separately in the statement of financial position or disclosed in the notes. Entities would disclose:

The amount of assets in the qualifying segregated fund arrangements that are:

• Legally insulated from the general account and those that are not • Representative of the entity’s proportionate interest

The portion of the liability related to segregated funds

Interest credited to policyholders if not presented separately in the statement of comprehensive income

Investment income generated from assets and returns credited to policyholders would be required to be presented gross on the face of the income statement, versus the current practice of offsetting to zero. However, this revenue and expense, along with other revenue and expense generated by the arrangement, may be commingled with other similar revenue and expense items.

Presentation of Segregated Funds

Current U.S. GAAP Proposed Model

Segregated funds assets and liabilities are required to be disclosed separately on the face of the balance sheet.

Assets in qualifying segregated fund arrangements would be required to be presented either separately in the statement of financial position or disclosed in the notes.

FASB’s Proposed Model for Insurance Contracts

23

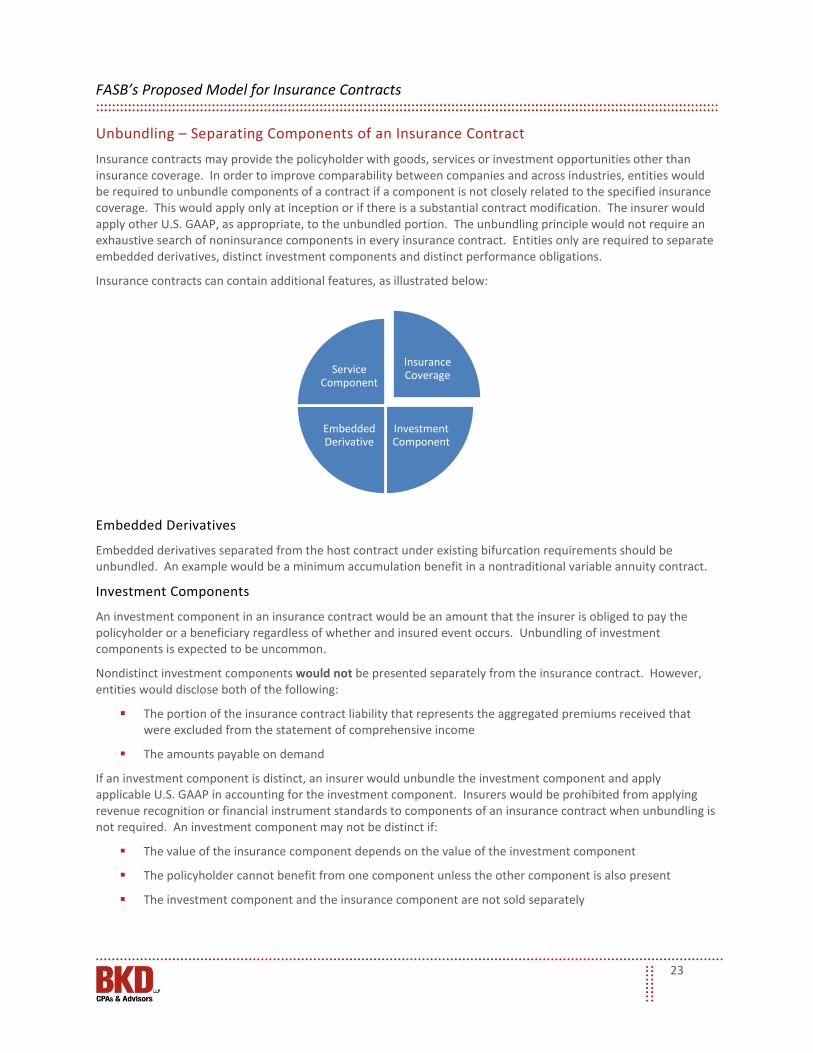

Unbundling – Separating Components of an Insurance Contract Insurance contracts may provide the policyholder with goods, services or investment opportunities other than insurance coverage. In order to improve comparability between companies and across industries, entities would be required to unbundle components of a contract if a component is not closely related to the specified insurance coverage. This would apply only at inception or if there is a substantial contract modification. The insurer would apply other U.S. GAAP, as appropriate, to the unbundled portion. The unbundling principle would not require an exhaustive search of noninsurance components in every insurance contract. Entities only are required to separate embedded derivatives, distinct investment components and distinct performance obligations.

Insurance contracts can contain additional features, as illustrated below:

Embedded Derivatives

Embedded derivatives separated from the host contract under existing bifurcation requirements should be unbundled. An example would be a minimum accumulation benefit in a nontraditional variable annuity contract.

Investment Components

An investment component in an insurance contract would be an amount that the insurer is obliged to pay the policyholder or a beneficiary regardless of whether and insured event occurs. Unbundling of investment components is expected to be uncommon.

Nondistinct investment components would not be presented separately from the insurance contract. However, entities would disclose both of the following:

The portion of the insurance contract liability that represents the aggregated premiums received that were excluded from the statement of comprehensive income

The amounts payable on demand

If an investment component is distinct, an insurer would unbundle the investment component and apply applicable U.S. GAAP in accounting for the investment component. Insurers would be prohibited from applying revenue recognition or financial instrument standards to components of an insurance contract when unbundling is not required. An investment component may not be distinct if:

The value of the insurance component depends on the value of the investment component

The policyholder cannot benefit from one component unless the other component is also present

The investment component and the insurance component are not sold separately

Insurance Coverage

Investment Component

Embedded Derivative

Service Component

FASB’s Proposed Model for Insurance Contracts

24

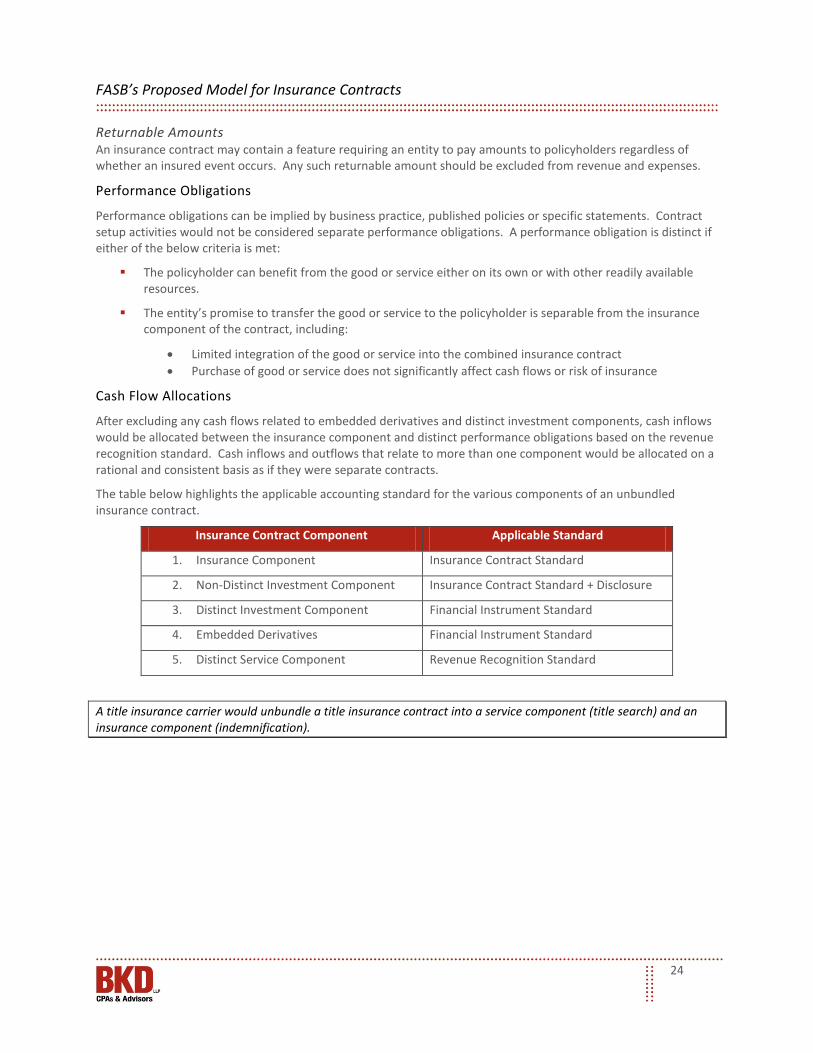

Returnable Amounts An insurance contract may contain a feature requiring an entity to pay amounts to policyholders regardless of whether an insured event occurs. Any such returnable amount should be excluded from revenue and expenses.

Performance Obligations

Performance obligations can be implied by business practice, published policies or specific statements. Contract setup activities would not be considered separate performance obligations. A performance obligation is distinct if either of the below criteria is met:

The policyholder can benefit from the good or service either on its own or with other readily available resources.

The entity’s promise to transfer the good or service to the policyholder is separable from the insurance component of the contract, including:

• Limited integration of the good or service into the combined insurance contract • Purchase of good or service does not significantly affect cash flows or risk of insurance

Cash Flow Allocations

After excluding any cash flows related to embedded derivatives and distinct investment components, cash inflows would be allocated between the insurance component and distinct performance obligations based on the revenue recognition standard. Cash inflows and outflows that relate to more than one component would be allocated on a rational and consistent basis as if they were separate contracts.

The table below highlights the applicable accounting standard for the various components of an unbundled insurance contract.

Insurance Contract Component Applicable Standard

1. Insurance Component Insurance Contract Standard

2. Non-Distinct Investment Component Insurance Contract Standard + Disclosure

3. Distinct Investment Component Financial Instrument Standard

4. Embedded Derivatives Financial Instrument Standard

5. Distinct Service Component Revenue Recognition Standard

A title insurance carrier would unbundle a title insurance contract into a service component (title search) and an insurance component (indemnification).

FASB’s Proposed Model for Insurance Contracts

25

Reinsurance

Example – Whole-life contract

An entity issues a traditional whole-life contract with a death benefit of $5,000 for a premium of $1,000. The policyholder can cancel the contract before death and receive an amount, i.e., cash surrender value, that initially equals $100 and increases by 10 percent a year.

Claims processing and asset management services

The claims processing and asset management services are part of the activities the entity must undertake to fulfill the contract, and the entity cannot transfer a good or service to the policyholder as those activities occur. These performance obligations should not be separated from the insurance contract.

Cash surrender value

The value of the death benefit is the difference between $5,000 and the accumulated cash surrender value. Both the insurance component and the investment component lapse together. The investment component is highly interrelated with the insurance component and is not distinct. The investment component would not be separated from the insurance contract and would be accounted for together.

Example – Life insurance contract with account balance

An entity issues a life insurance contract with an account balance for $1,000 at contract inception. The account balance is increased annually by voluntary amount paid by the policyholder, increased or decreased by amounts calculated using the returns from specified assets and a 1.5 percent asset management fee.

The contract promises to pay the following:

a. Death benefit of $5,000 and the amount equal to the account balance, if the policyholder dies

b. An amount that is equal to the account balance, if the contract is cancelled by the policyholder (no surrender charges)

An investment product that is equivalent to the account balance but without the insurance coverage is sold by another financial institution.

Asset management services

The policyholder can benefit separately from receiving the returns from the specified assets and a death benefit. The risk and value of the death benefit does not depend on the amounts accumulated in the account balance. The asset management services are distinct and would be separated from the insurance contract and accounted for by applying the revenue standard.

Account balance

The existence of a comparable investment product indicates the components may be distinct. However, the right to death benefits lapses or matures at the same time as the account balance, which means that the insurance and investment components are highly interrelated and therefore are not distinct. The account balance would not be separated from the insurance contract.

FASB’s Proposed Model for Insurance Contracts

26

A reinsurance contract is an insurance contract issued by one issuer (the reinsurer) to compensate another insurer (the cedant) for losses on one or more contracts issued by the cedant. Cedants would need to evaluate whether a reinsurance contract meets the definition of an insurance contract and transfers significant insurance risk to reinsurers. Cedants and reinsurers would use the same approach (BAA or PPA) for a reinsurance contract as was used for the underlying contract. Reinsurance contracts that reinsure contracts measured using both approaches would be separated based on the underlying contract measurement model, with each component accounted for using the same approach used to account for the underlying direct insurance contracts.

The reinsurance contract boundary depends on the type of coverage. For direct proportion contracts, coverage begins when the underlying contracts are recognized. For aggregate loss contracts, an entity would recognize a reinsurance asset or liability when the reinsurance coverage period starts. When a cedant enters into a reinsurance contract, it derecognizes the underlying contract only if the obligation to the policyholder is extinguished.

A cedant would measure the reinsurance contract as the sum of the expected present value of future cash inflows less the expected present value of cash outflows. The cedant should consider the risk of nonperformance by the reinsurer on an expected value basis when estimating the present value of cash flows. A cedant would apply the financial instrument impairment model when assessing recoverability of the reinsurance asset and should consider collateral in the analysis. Losses from disputes would be reflected in the measurement of the recoverable asset when current information and events suggest the cedant may be unable to collect amounts due under the terms of the contract.

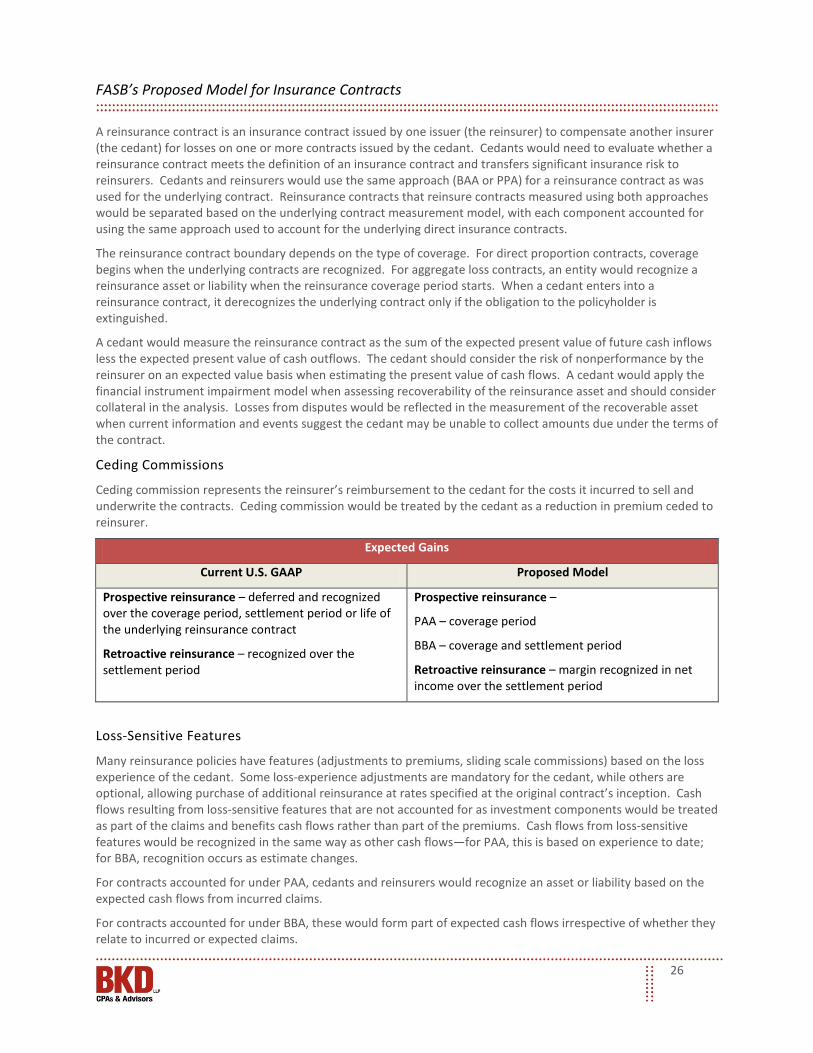

Ceding Commissions

Ceding commission represents the reinsurer’s reimbursement to the cedant for the costs it incurred to sell and underwrite the contracts. Ceding commission would be treated by the cedant as a reduction in premium ceded to reinsurer.

Expected Gains

Current U.S. GAAP Proposed Model

Prospective reinsurance – deferred and recognized over the coverage period, settlement period or life of the underlying reinsurance contract

Retroactive reinsurance – recognized over the settlement period

Prospective reinsurance –

PAA – coverage period

BBA – coverage and settlement period

Retroactive reinsurance – margin recognized in net income over the settlement period

Loss-Sensitive Features

Many reinsurance policies have features (adjustments to premiums, sliding scale commissions) based on the loss experience of the cedant. Some loss-experience adjustments are mandatory for the cedant, while others are optional, allowing purchase of additional reinsurance at rates specified at the original contract’s inception. Cash flows resulting from loss-sensitive features that are not accounted for as investment components would be treated as part of the claims and benefits cash flows rather than part of the premiums. Cash flows from loss-sensitive features would be recognized in the same way as other cash flows—for PAA, this is based on experience to date; for BBA, recognition occurs as estimate changes.

For contracts accounted for under PAA, cedants and reinsurers would recognize an asset or liability based on the expected cash flows from incurred claims.

For contracts accounted for under BBA, these would form part of expected cash flows irrespective of whether they relate to incurred or expected claims.

FASB’s Proposed Model for Insurance Contracts

27

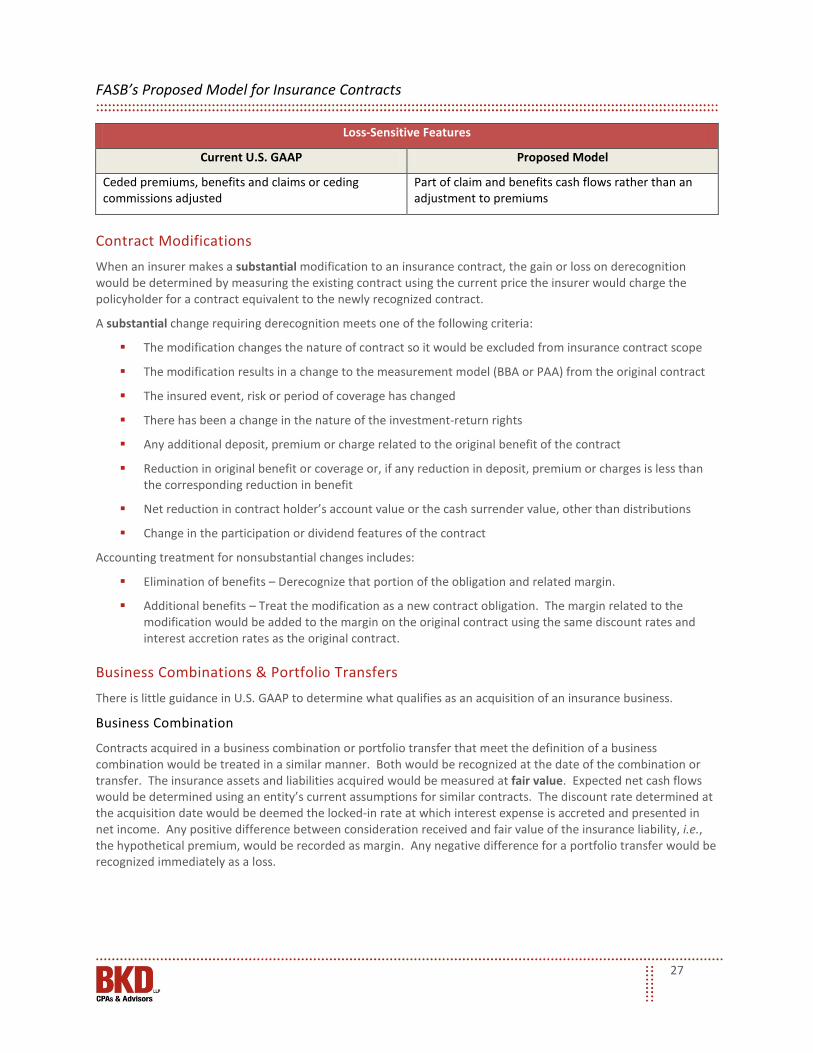

Loss-Sensitive Features

Current U.S. GAAP Proposed Model

Ceded premiums, benefits and claims or ceding commissions adjusted

Part of claim and benefits cash flows rather than an adjustment to premiums

Contract Modifications When an insurer makes a substantial modification to an insurance contract, the gain or loss on derecognition would be determined by measuring the existing contract using the current price the insurer would charge the policyholder for a contract equivalent to the newly recognized contract.

A substantial change requiring derecognition meets one of the following criteria:

The modification changes the nature of contract so it would be excluded from insurance contract scope

The modification results in a change to the measurement model (BBA or PAA) from the original contract

The insured event, risk or period of coverage has changed

There has been a change in the nature of the investment-return rights

Any additional deposit, premium or charge related to the original benefit of the contract

Reduction in original benefit or coverage or, if any reduction in deposit, premium or charges is less than the corresponding reduction in benefit

Net reduction in contract holder’s account value or the cash surrender value, other than distributions

Change in the participation or dividend features of the contract

Accounting treatment for nonsubstantial changes includes:

Elimination of benefits – Derecognize that portion of the obligation and related margin.

Additional benefits – Treat the modification as a new contract obligation. The margin related to the modification would be added to the margin on the original contract using the same discount rates and interest accretion rates as the original contract.

Business Combinations & Portfolio Transfers There is little guidance in U.S. GAAP to determine what qualifies as an acquisition of an insurance business.

Business Combination

Contracts acquired in a business combination or portfolio transfer that meet the definition of a business combination would be treated in a similar manner. Both would be recognized at the date of the combination or transfer. The insurance assets and liabilities acquired would be measured at fair value. Expected net cash flows would be determined using an entity’s current assumptions for similar contracts. The discount rate determined at the acquisition date would be deemed the locked-in rate at which interest expense is accreted and presented in net income. Any positive difference between consideration received and fair value of the insurance liability, i.e., the hypothetical premium, would be recorded as margin. Any negative difference for a portfolio transfer would be recognized immediately as a loss.

FASB’s Proposed Model for Insurance Contracts

28

Portfolio Transfers

Acquisitions of insurance businesses occur in various forms. Portfolio transfer is the transfer of an insurer’s entire liability for in-force policies or outstanding losses, or both, of a segment of an insurer’s business to another entity. An insurer would measure a portfolio of insurance contracts acquired in a portfolio transfer that does not meet the definition of a business combination in accordance with the guidance in the ED. Fulfillment cash flows would be determined using an entity’s current assumptions for similar contracts. The margin would be an excess of cash inflows over cash outflows. Any negative difference would be immediately recognized as a loss in net income.

Acquisition Through Combination of Entities or Businesses Under Common Control

An insurer would account for insurance contracts acquired through a business combination of entities or businesses under common control following the guidance in Subtopic 805-10, Business Combinations.

Foreign Currency When remeasuring foreign currency transactions, all financial statement components related to an insurance contract would be classified as monetary items. This applies both to the BBA and PAA approaches. FASB felt assessing each component of the insurance contract separately (fulfillment cash flows, margin and preclaims liability) would be complex and costly and would not be warranted under cost-benefit considerations.

Foreign Currency

Current U.S. GAAP Proposed Model

Nonmonetary – Unearned premium reserves, deferred acquisition costs (recorded at historical exchange rates)

Monetary – Liability for future policyholder benefits, liability for incurred claims (recorded at current rate)

All financial statement components related to an insurance contract would be classified as monetary.

Presentation & Disclosure

Presentation

Statement of Financial Position

The new insurance model will require more disaggregated information. The statement of financial position would reflect the expected contract profit from the insurance contract and a current estimate of the amount of future cash flows from the insurance contract, adjusted to reflect timing and uncertainty related to those cash flows. Contract balances (liability or assets) will be shown separately on the underlying approach applied (BBA or PAA). Portfolios in an asset position should not be netted with portfolios in a liability position. The obligation related to any unpaid direct acquisition costs should be presented together with the margin, rather than as part of the obligation to policyholders on the face of the financial statements. Reinsurance assets would not be offset against insurance contract liabilities.

BBA Premiums due for which the insurer has an unconditional right would be presented separately as an asset; all other rights and obligations would be presented on a net basis.

PAA Premiums receivable, both conditional and unconditional, and the contact liability would be disaggregated into liability for remaining coverage, liability for incurred claims and gross premium received.

FASB’s Proposed Model for Insurance Contracts

29

Statement of Comprehensive Income

The statement of comprehensive income reports an operating result that reflects underwriting experience, the change in uncertainty and the profit from services in the period. The income statement line items would reflect underwriting margin, reinsurance gains and onerous contract losses at initial recognition, indirect acquisition costs expensed, experience adjustments and changes in estimates, income from unit-linked contracts and interest on insurance liabilities. Breaking out the single margin separately in revenue more clearly shows the link between the deferred profit and the profit earned, increasing transparency for users, and would more closely align the statement of comprehensive income with the related accounts in the statement of financial position. The amount presented as insurance contract revenue represents the present value of the premiums received attributable to the insurance component at the time the coverage is provided.

BBA Summarized margin information in which all cash inflows associated with an insurance contract, i.e., premiums, are treated as deposits received and all cash outflows, i.e., benefits, are treated as repayment. Subsequently, as the insurer is released from risk, the related portion of the margin is recognized as revenue. Premiums and claims should be measured by applying an earned premium presentation, where premiums are allocated to periods in proportion to the value of coverage that the insurer has provided in the period and claims are presented when incurred.

PAA An entity would include the underwriting margin, disaggregated—either in the statement of comprehensive income or in the notes—into premiums, claims and expenses and changes in additional liabilities for onerous contracts.

Statement of Financial Position

Assets Liabilities and Stockholders’ Equity

Cash Liability for remaining coverage (PAA)

Investments Liability for incurred claims (PAA)

Premiums receivable (PAA) Insurance contract liability (BBA)

Premiums receivable (BBA) Margin (BBA)

Reinsurance contract asset (PAA) Total Liabilities

Reinsurance contract asset (PAA)

Insurance contract asset (BBA)

Reinsurance contract asset (PAA)

Accumulated OCI

Reinsurance contract asset (BBA) Retained earnings

Total assets Total liabilities & stockholders’ equity

FASB’s Proposed Model for Insurance Contracts

30

Disclosures The required disclosures are intended to help financial statement users understand the amount, timing and uncertainty of cash flows and include a discussion of the methods, processes and assumptions used. Entities will need to disclose quantitative and qualitative information about the amounts arising from insurance contracts recognized in the financial statements and the nature and extent of risks arising from those insurance contracts. Reportable segments would be the highest level of aggregation allowed for disclosures, but entities are not precluded from going to a greater level of detail.

U.S. GAAP contains limited explicit guidance on presentation but does include extensive examples and illustrations. The presentation requirements primarily are driven by SEC regulation. U.S. GAAP contains explicit disclosure guidance, depending on the type of insurance contract, including:

- The basis for estimating the liabilities for unpaid claims and claims adjustment expenses

- The nature of acquisition cost capitalized and the amount of amortization for the period

- A reconciliation of the beginning and ending balances for the liability of unpaid claims and claims adjustment expenses

- Payments of claims and claims adjustment expenses

STATEMENT OF COMPREHENSIVE INCOME

Margin release

Insurance obligation for benefits and expenses

Insurance contract revenue (premiums earned) (PAA) (including interest accretion)

Ceded reinsurance premium (expenses) (BBA)

Ceded reinsurance premium (expenses) (PAA)

Benefits incurred (BBA)

Claims incurred (PAA)

Adjustment for changes in estimates or future benefits/claims

Amortization of qualifying acquisition costs

Underwriting Margin

Other expenses

Investment income

Interest expenses (including unwind of the discount)

Net Income

Components of other comprehensive income

Effects of changes in discount rate for insurance liabilities

Total Comprehensive Income

FASB’s Proposed Model for Insurance Contracts

31

The new model would apply to public and nonpublic companies with limited disclosure relief for nonpublic entities. Nonpublic entities would be exempt from the requirement to provide specified disclosures at a minimum by reportable segment and would not be required to provide the insurance disclosure required for interim periods.

Insurance Contract Liabilities & Liabilities for Incurred Claims

Separate reconciliation of the opening and closing balance of the insurance liability under BBA and liability for incurred claims for PAA

Explanation of significant drivers of the changes in the insurance liability and liability for incurred claims

Disclosure of asset or liability account balance arising from reinsurance contracts held

Margin

Reconciliation of opening and closing balances for the margin

Amounts of revenue recognized in the period that arose from the margin being released

Qualifying acquisition costs incurred but not yet amortized in the statement of comprehensive income, i.e., embedding in the margin

Reinsurance receivable

Reconciliation of opening and closing balances

Balance of reinsurance receivable related to claims paid

Allowance for reinsurance recoverable