Fap Course01sept14

50

description

thj

Transcript of Fap Course01sept14

The Financial Analysis of Projects course provides a set of analytical theory and practical tools needed to evaluate the financial feasibility of some investments in Building sector. Thisincludes urban planning, commercial and residential rehabilitationand development for all property types. Accounting, risk management,

taxation, capital cost, externalities and organizational issues influencing the financial viability of projects will also be analyzed and evaluated.

Time line - Points and periods:• Base Year / Year zero: A base

year is the year used for comparison for the level of a particular economic index ( Westopedia)

• Investment Year - Year in which the actual investment occurs.

• Analysis Period - Period of time for which an evaluation is conducted

- Depreciation Period - Period of time over which an investment isamortized

- Levelization Period - Period of time used when calculating a

levelized cash flow stream

- Discount rate: The discount rate also refers to the interest rate used in discounted cash flow analysis to

determine the present value of future cash flows ( Westopedia)

A timeline provides a tool for visualizing cash flow and time

Two Cash Flows : An Initial TD20000 Outflow and

27209,78 Inflow at the end of the 4th year

What is the difference between simple interest andcompound interest?

Simple i nterest : Interest is earned only on the principal amount.Compound i n terest : Interest is earned on both the principal and accumulated interest of prior periods.

Example : Suppose that you deposit TD 1000 in your savings

account that earns 5% annual interest. How much will you have in your account after two years using (a) simple interest and (b)

compound interest?

Si m ple I n t e r e s t

Interest earned = 5% of TD 1000 = .05×1000 = TD50 per yearTotal interest earned = TD50×2 = TD100

Balance in your savings account:= Principal + accumulated

interest= 1000 + 100 = TD 1100

Compound i n t e r e s t

Interest earned in Year 1 = 5% of TD 1000 = TD50Interest earned in Year 2 = 5% of (100 + accumulated interest)

= 5% of (TD1000 + 50) = .05×1050 = TD 52,5

Balance in your savings account:= Principal +

interest earned

= TD1000 + TD50 + TD52,5 = TD 1102,5

Future Value = Initial Value ( P) +Accumulated Interest

PV = P + r x PInitial value + Accumulated Interest

Future Value Factor

Year Cash Flow Years to end n Future Value

0 0 3 0

1 C 2 C(1+r)2

2 C 1 C(1+r)1

3 C 0 C(1+r)0

FV3 = C [(1+r)2 +(1+r)1+1]

FVn = C [(1+r)n +(1+r)n-1 + …………+1]

When a future payment or series of payments are

discounted at the given rate of interest up to the present

date to reflect the time value of money, the

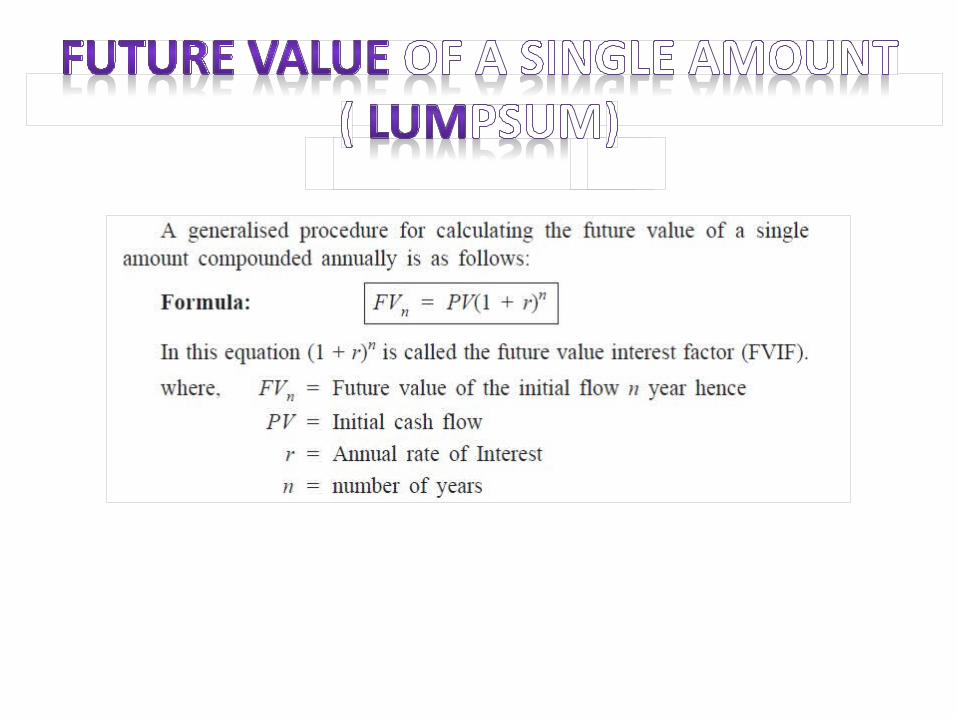

resulting value is called present value.

A generalized procedure for calculating the

present value of a single amount compounded

annually is as follows:

PVn = FV /

(1+r)n

. A cash flow stream is a finite set of

payments that an investor will receive or

invest over time.

.The PV of the cash flow stream is equal to

the sum of the present value of each of the individual cash flows in the stream.

. The PV of a cash flow stream can also be

found by taking the FV of the cash flow stream and discounting the lump sum at the appropriate discount rate for the appropriate

number of periods

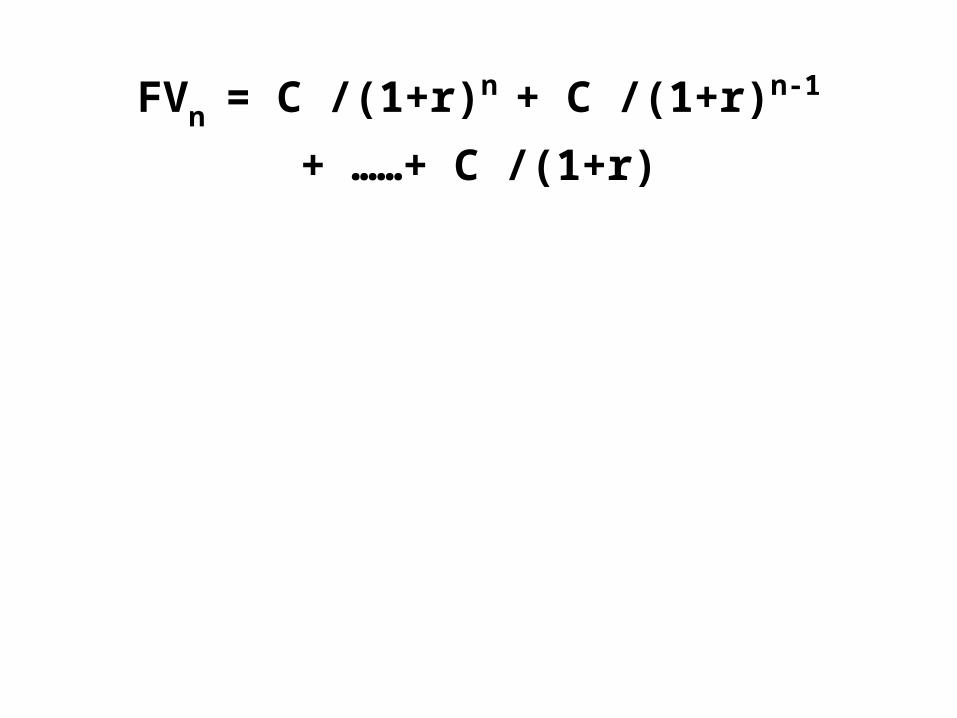

FV4 = CF4/(1+r)4 + CF3 /(1+r)3 + CF2 /(1+r)2 +CF1 /(1+r)

FVn = C /(1+r)n + C /(1+r)n-1 + ……+ C /(1+r)

AnnuityDue = Annuity

Ordinary x (1 + i)

The difference between the ordinary annuity and the annuitydue is one compounding period

Each payment of an ordinary annuity belongs to the payment period preceding its date, while

the payment of an annuity- due refers to a payment period

following its date

00

ExampleYou Plan to attend a French engineering school and you have to take out € 50 000 in a loan at 12%.You want to figure out your yearly payment ; given you will have 5years to pay back the loan

0 1 2 3 4 5

005 00 ? ? ? ? ?

Year Begening Balance Yearly payment Interest PrincipalRepayment

1 50,000TD 13,870TD 6,000TD 7,870TD

2 42,130TD 13,870TD 5,056TD 8,815TD

3 33,315TD 13,870TD 3,998TD 9,873TD

4 23,442TD 13,870TD 2,813TD 11,057TD

5 12,384TD 13,870TD 1,486TD 12,384TD

The annual percentage rate (APR) indicates the amount of interest paid or earned in one year without compounding. APR is also known as the nominal or stat e d inte r est r a t e . This is the rate required by law.We cannot compare two loans based on APR if they do not have thesame compounding period.

To make them comparable, we calculate their equivalent rate using an annual compounding period. We do this by calculating the effective annual rate (EAR) .

APR is the quoted annual rate with a pre-specified compounding frequency. [Let m be the number of compounding periods per year for this APR.]EAR is the effective annual rate at an annual compounding frequency. [One compounding per year]The two should generate the same amount of money in one year:

(1+APR/m)m=(1+EAR) EAR=(1+APR/m)m-1.

Calculating an EAR or Effective Annual Rate

Assume that you just received your first credit card statement and the APR, or annual percentage rate listed on the statement, is 21.7%. When you look closer you notice that the interest is compounded

daily. What is the EAR, or effective annual rate, on your credit card?What is the EAR on a quoted or stated rate of 13% that iscompounded monthly?Verify the answers: 24.23%; 13.80%.