Falch Henten Skouby Tadayoni

24

1 Innovations in Telecommunications: The Case of Denmark Morten Falch Anders Henten Knud Erik Skouby Reza Tadayoni Center for Tele-Information Technical University of Denmark ITS 14 th European Regional Conference August 23-24, Helsinki, Finland

-

Upload

alifatehitqm -

Category

Documents

-

view

215 -

download

0

Transcript of Falch Henten Skouby Tadayoni

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 1/24

1

Innovations in Telecommunications:The Case of Denmark

Morten FalchAnders Henten

Knud Erik SkoubyReza Tadayoni

Center for Tele-InformationTechnical University of Denmark

ITS14th European Regional Conference

August 23-24, Helsinki, Finland

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 2/24

2

Innovations in Telecommunications: The Case of Denmark 1

1. Introduction

1.1 Definitions and delimitations

The paper examines innovation activities on the Danish telecom market and discussesa number of market based factors affecting innovations, i.e., competition, demand,and strategies of market players. The paper does not include an analysis of policyfactors and does not either contain a more technology specific discussion of servicedelivery platforms, etc. It concentrates on market based factors.

In the paper, the term telecom sector means the telecom operators and other playerson the telecom transport market. Equipment manufacturers and content producers arenot included. However, the interfaces between the operators and the equipmentmanufacturers and content producers are part of the examination.

Based on the works of Joseph Schumpeter on innovation and business development inthe first half of the 20th century, a differentiation has been made in economic theory

between invention, innovation and diffusion2. An invention is a new idea or a prototype of a product, a model of a new production process, etc., which may, for instance, result in a patent. An innovation is the introduction on the market of such aninvention. And, diffusions of innovations deal with the broader market penetration of new products and processes.

The borderlines between the three concepts and phases are fluid and an innovation

study can, in principle, deal with all three aspects. In this paper, however, we willfocus on the two last phases, innovation and diffusion. The reason is the character of the most common innovations in the telecom operator area, i.e. service developments,which seldom can be considered as genuine inventions. Genuine invention activitiesare primarily the ‘turf’ of the equipment manufacturers, in the present situation.

For an individual company, the implementation of a new technology or method of production can be an innovation even if this new technology or production methodhas already been implemented by other companies. Such a perspective on technologyinnovation is relevant, for instance, in analyses of the innovativeness on one nationalmarket in comparison with other national markets. If focus, on the other hand, is on

the competition between individual operators on a national market and the role of innovations in this context, it is more relevant to reserve the innovation notion to thefirst operator(s) introducing the new technologies or methods. It does not have to benew in an international context. The innovative operator is the one which is the first tointroduce a new product or process on the national market – e.g. the first to implementADSL even if ADSL technology has not been developed in the country in question. In

1 The paper is based on a report written for the Danish IT and telecom agency in relation to aGovernment telecom competition report issued in the spring of 2003. The innovation report ‘Innovationog konkurrence, en analyse af det danske telemarked’ is written by Morten Falch, Anders Henten,Knud Erik Skouby and Reza Tadayoni. This report is partly based on interviews with representatives of

the most important market players on the Danish telecom market.2 See Joseph Schumpeter: ’The Theory of Economic Development’ from 1912 and ’Business Cycles’from 1939.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 3/24

3

the present paper, there is focus on both issues, i.e. the general innovativeness on theDanish market and on the role of innovations in relation to competition on the Danishmarket.

The innovation concept, in principle, includes product, process, billing, and marketing

innovations, etc. However, a large part of the innovations, which in the daily activitiesactually affect the market shares of operators, is related to billing methods and smaller

product and service improvements. A known example of such innovations is the pre- paid card on the mobile market in the late 1990s. These kinds of innovations are amixture of business models and technological improvements and they are includedwithin the boundaries of this paper. Only sheer marketing innovations as, for instance,advertisement campaigns and branding initiatives are considered outside the scope of this investigation.

A special issue in the telecom area is concerned with the borderlines between productand process innovations. The borderlines cannot be sharp, as the products – the

communication services – are delivered simultaneously with the process of production, so to say. Product and process can, consequently, not be clearly separated.However, not all process innovations become visible to the end user in the shape of new products/services. And, it is possible to differentiate between network and serviceinnovations, i.e. the innovation which the end users experience (services) and theinnovations which end users do not necessarily notice (network).

An additional angle on the character of innovations deals with their more or lessradical character. In a historical perspective, it can be useful to differentiate betweentechnological innovations, which are within or beyond the existing technological

paradigm3. However, in this paper regarding the innovations inside a giventechnological paradigm, the most relevant thing is to differentiate betweenincremental (step-wise) and more radical innovations. An incremental innovation is,for example, a new service developed on the basis of an IN product development

platform. A radical innovation is, for instance, the implementation of 3G systems inthe mobile area. The transition from a 2G to a 3G system can be made more or lesssmoothly. However, a fully developed 3G system will lead to radically newcommunication possibilities.

1.2 The main issues of the paper

There are two main questions to be examined in the paper. The first one is related tothe general innovativeness of the Danish telecom market as compared with other comparable markets. It has often been mentioned in the public debate in Denmark ontelecommunications that the Danish market has benefited from the fact that largeinternational operators have been able to use the Danish market as a kind of test bed

because of its limited – however large enough – size and because of the generalwealth and advanced demand on this market. The question, however, is whether thisis true, i.e. whether innovations are implemented more quickly on the Danish marketcompared with other national market in Europe. Furthermore, in relation to this issue,it will be examined how the ‘innovation system’ develops in Denmark. This question

3 See, for instance, Giovanni Dosi: ‘Technological Paradigms and Technological Trajectories’,Research Policy 11, 1982.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 4/24

4

is, e.g., concerned with the relationships and interfaces between equipment andhardware manufacturers, telecom operators and content producers and aggregators,and it, furthermore, deals with the cooperative relationships between telecomcompanies and universities. (In the paper, we will concentrate on the relationships

between operators and equipment manufacturers).

The second main question in the paper deals with the relationships betweeninnovation and competition, including the influence of innovations on thedevelopment of competition, but also the influence of competition on innovativeness.It’s obvious that there are mutual influences between innovation and competition,where competition can increase the innovation activities of companies, as innovationscan lead to general market developments and increasing market shares. Innovationactivities can, therefore, also contribute to a sharpened competition – which does notnecessarily lead to more competitors and more equal competition between operatorsof comparable sizes. A sharpened competition, resulting from the innovation activitiesfrom one or a number of operators, can also result in a more skewed development in

market shares.

In relation to this, it should be mentioned that the theories on the positive correlation between competition and innovation does not flow from the traditional Schumpeter- based theories. They, actually, predict a negative correlation, so that an increasedcompetition may lead to less innovation activity, as competition will diminish themonopoly rent shared by successful innovators4. Newer economic analyses, however,indicate positive relationships between competition and innovation5. The telecom areaseems to be a clear example of a sector, where competition has led to greater innovation activity. If the period before the liberalization of the sector is comparedwith the present situation, it is obvious that there are more innovation initiatives in the

present situation. But there is an analogy between Schumpeter’s theory and thecomparison between innovation activities of the dominant operator and the smaller operators on the market. Is it primarily the smaller operators or the big one which arein the lead with respect to innovation activities?

In the paper, there is first a very brief presentation of the Danish telecom market.After this the general innovativeness on the Danish market is examined, which isfollowed by a discussion of the market based factors affecting innovations: Domesticdemand, strategies of operators, competition, and finally cooperative relationships

between operators and equipment manufacturers.

2. The environment for innovation

The Danish market has, in the same manner as the markets in other Nordic countries,a high penetration of most kinds of telecom services. This has been explained by thefact that the major share of the population is able to afford these services. In addition,Danish consumers and enterprises are among the fastest to take up new technology.

4

Philippe Aghion, etc.: ’Competition and Innovation: An Inverted U Relationship’, The Institute for Fiscal Studies, WP02/04, 2002.5 Ibid.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 5/24

5

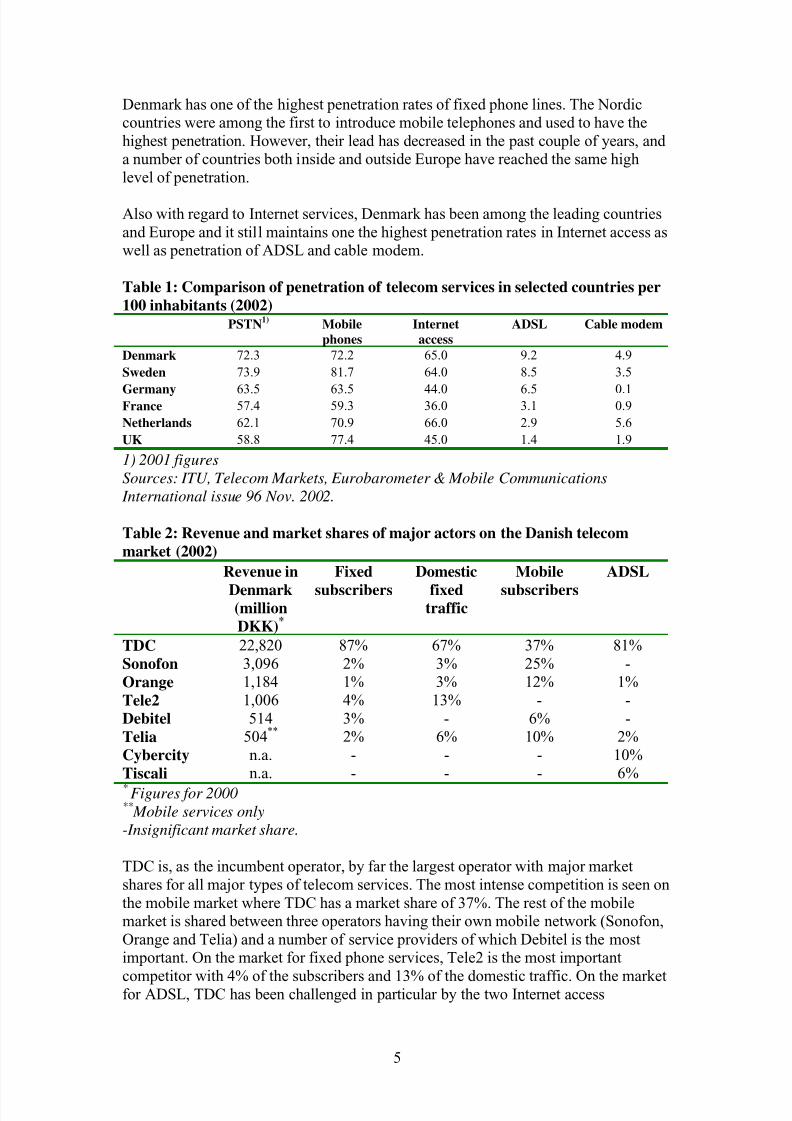

Denmark has one of the highest penetration rates of fixed phone lines. The Nordiccountries were among the first to introduce mobile telephones and used to have thehighest penetration. However, their lead has decreased in the past couple of years, anda number of countries both inside and outside Europe have reached the same highlevel of penetration.

Also with regard to Internet services, Denmark has been among the leading countriesand Europe and it still maintains one the highest penetration rates in Internet access aswell as penetration of ADSL and cable modem.

Table 1: Comparison of penetration of telecom services in selected countries per

100 inhabitants (2002)PSTN1) Mobile

phonesInternetaccess

ADSL Cable modem

Denmark 72.3 72.2 65.0 9.2 4.9Sweden 73.9 81.7 64.0 8.5 3.5

Germany 63.5 63.5 44.0 6.5 0.1France 57.4 59.3 36.0 3.1 0.9Netherlands 62.1 70.9 66.0 2.9 5.6UK 58.8 77.4 45.0 1.4 1.9

1) 2001 figures

Sources: ITU, Telecom Markets, Eurobarometer & Mobile Communications

International issue 96 Nov. 2002.

Table 2: Revenue and market shares of major actors on the Danish telecom

market (2002)

Revenue in

Denmark(million

DKK)*

Fixed

subscribers

Domestic

fixedtraffic

Mobile

subscribers

ADSL

TDC 22,820 87% 67% 37% 81%Sonofon 3,096 2% 3% 25% -Orange 1,184 1% 3% 12% 1%Tele2 1,006 4% 13% - -Debitel 514 3% - 6% -Telia 504** 2% 6% 10% 2%Cybercity n.a. - - - 10%Tiscali n.a. - - - 6%* Figures for 2000** Mobile services only

-Insignificant market share.

TDC is, as the incumbent operator, by far the largest operator with major marketshares for all major types of telecom services. The most intense competition is seen onthe mobile market where TDC has a market share of 37%. The rest of the mobilemarket is shared between three operators having their own mobile network (Sonofon,Orange and Telia) and a number of service providers of which Debitel is the mostimportant. On the market for fixed phone services, Tele2 is the most important

competitor with 4% of the subscribers and 13% of the domestic traffic. On the marketfor ADSL, TDC has been challenged in particular by the two Internet access

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 6/24

6

providers, Cybercity and Tiscali. TDC has, however, increased their market sharefrom 37% in 2000 to 81% in 2002.

Several comparisons position Denmark as an advanced market for ICT products in particular in the mobile areas. According to a benchmarking analysis measuring 26

parameters within infrastructure, applications and market structure, Denmark is themost advanced ICT market next to Hong Kong and ahead of other Scandinavian andEuropean countries6. In a similar benchmark on ‘e-readiness’ made by INSEAD,Denmark ranks as number eight after both Sweden and UK 7.

Table 3: Benchmarking of National ICT-Markets

ITU Mobile/Internet Index 2001 INSEAD Networkedreadiness Index

Index Ranking Index RankingDenmark 65.61 2 5.33 8Sweden 65.42 3 5.58 4Norway 64.67 6 5.00 17UK 63.00 8 5.35 7Netherlands 62.03 9 5.26 11Germany 55.53 17 5.29 10France 52.45 21 4.97 18Sources: ITU: ‘Internet for a Mobile Generation’, Geneva, 2002. Soumitra Dutta and

Amit Jain: ‘The Networked Readiness of Nations’, INSEAD, 2002.

3. Innovation in the Danish telecom sector

Public available R&D figures for the Danish economy do not include innovations intelecom as a separate activity, but include a category on innovations incommunications and media. Within this segment, one third of the R&D expendituresare related product innovations, while the rest mainly is related to process innovations(Table 4).

Table 4: Product-and process-related R&D in post, telecom and radio and TVbroadcasting (1999)

Improvement of existing products 12%Development of existing products

but new to the firm1%

Development of entirely new products

20%

Product-related innovations total 33%Of which customer related

product development28%

Process-related activities 62%

Others including basic research 5%

Source: Analyseinstituttet for Forskning: ’Erhvervslivets forsknings- og

udviklingsarbejde’, Forskningsstatistik 1999.

6

ITU, Geneva, 2002.7 Soumitra Dutta and Amit Jain: ‘The Networked readiness of Nations’, INSEAD, 2002.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 7/24

7

It is not possible to document whether innovation activities within the telecom sector follows the same pattern as depicted in table 4. The incumbent operator TDC reportsthat that their R&D activities mainly are focused on product innovations, while the

majority of the other operators seems to concentrate on process related activities.

TDC is, by far, the Danish telecom operator with the highest R&D expenditures.Their expenditures amounted 15 million € in 2002. A major reorganization of TDC’sR&D activities has taken place since the telecom market was liberalized in the 1990s.Before the merger into TDC, the regional monopoly operators financed substantialresearch activities. Basic long term research was conducted by a national researchcentre (Tele-technical Research Laboratory), owned by the operators in cooperation,while short term product development was made in research departments within theregional companies. Following the merger of the regional companies, all researchdepartments and the national research centre were merged into TDC research, and

focus was moved towards more business oriented development activities. In 2000,TDC Research was dissolved, and innovation activities were delegated to the various

business units of TDC.

At the same time, a number of new operators have entered the market. Some of thesehave no tradition for research and their R&D budgets are much smaller than those of the incumbents. The overall trend in the level of innovation activities within thetelecom sector depends on how such activities are defined. Most of the Danishtelecom operators do not carry out their own research. On the other hand, theyconstantly seek to optimize their production, implement new services and create newopportunities for their business.

Development of new products is still important for the telecom operators, but productdevelopment is organised differently than before. The operators are using much morestandardized equipment, and this implies that all operators basically are able to

provide the same types of services. Product innovation is, therefore, focused onadaptation of existing products to the company’s own commercial and technicalenvironment.

The development within TDC is a good example of this. TDC has no separateresearch and development department, but maintains a large number of innovative

activities in all parts of the organization. Some claim even that the overallexpenditures allocated for R&D are rising although they are less visible today.Development projects have become smaller, more commercially oriented, and with ashorter time horizon, but they have also become more numerous. Others claim thatinnovative activities with relation to fixed network operations are decreasing, whileinnovations within mobile networks and services are either stable or increasing.

Cybercity – one the major Internet access providers claims that 20 percent of their staff works with innovation. The innovative activities include development of web-

based customer handling, work-flow and billing systems, development of newservices and network optimization. Tiscali – the other major Internet access provider

competing with TDC - has a much lower level of innovative activities, as Tiscali hasconcentrated most of their R&D in their Italian parent company.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 8/24

8

On the mobile market, the second operator, Sonofon, reports that 200-250 out of atotal staff of 1,300 are engaged in innovative activities. Half of these work with

product development. The third mobile operator Orange (former Mobilix) used todevote substantial resources to R&D and was the most innovative mobile operator on

the Danish market. The recent telecom crisis, however, has forced Orange to makesubstantial cuts in their Danish R&D budget. But the Danish affiliate has managed tomaintain its position as a competence centre for the Orange conglomerate in selectedareas.

4. The role of domestic demand

Domestic demand affects innovations in two different ways: The demand affects thespeed of innovations: A sufficient demand is necessary to create the economic basisfor investments in new innovations. In addition, such investments will becomeeconomic attractive only if the can be expected to result in additional revenue in the

future.

The demand also affects the direction of innovations. The demand for different typesof services is an indicator of the types of innovations that will become the most

profitable. One of the decisive factors for a company’s ability to innovate is its abilitythrough the market to receive the right signals on the future needs of the users.Therefore, the relation between users and producers is important for a description of national systems of innovation8. The role of the demand is also included in MichaelPorter’s theory on competitive advantages9. Here, demand – in particular demandfrom advanced vanguard users – is included as one of the four factors determiningcompetitiveness.

It follows that not only the size but also the type of demand is important for innovations. A large demand limited to a few basic services will not stimulate productinnovations, but may stimulate process innovations which increase capacity andreduce costs. On the other hand, even a limited demand for new services may beimportant for gaining experiences in product innovation. Access to advanced anddemanding customers does not only contribute to the overall revenue, but will alsocontribute to the learning of the company. Advanced telecom users could, for instance, be the financial sector or public institutions.

Another characteristic of demand, impacting on innovations, is price sensitivity. If thedemand is very sensitive to price changes it might be difficult to introduce innovationswhich will improve the level of services but also result in a slight increase in costs.Price sensitivity depends both on consumer preferences and the level of competition.Fierce price competition can, therefore, dampen innovations. But competition alsostimulates innovations which can be used to maintain or even increase market shares.

The most prominent example in Denmark of demand driven innovations within thetelecom sector is the building of the partly optical hybrid cable-TV/data network in

8

Lundvall, B-Å (ed.): ‘National Systems of Innovation – Towards a Theory of Innovation andInteractive Learning’, Pinter, 1992.9 Michael Porter: ‘The Competitive Advantage of Nations’, The Free Press, 1990.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 9/24

9

the 1980s. The building of the network stimulated demand for optical equipment andformed the basis for the current stronghold in this industry. The network did not resultin the expected innovations in broadband services, but it contributed to the creation of technical competence within the area of optical communication.

A more recent example of demand led innovations is that the demand for fast andcheap Internet connections has led to the creation of alternative network infrastructures operated by municipalities, power companies or by local groups of citizens. One example is the municipality of Esbjerg which has upgraded their cable-TV network so that they have become able to offer Internet connections at pricesmuch lower than offered by the telecom operators.

Demand can be stimulated both through private demand and through demand from public institutions. The public sector is a comparatively advanced user of IT productsand has stimulated private use of advanced IT as well, and the public sector has in thisway been able to promote demand for IT- and telecom services.

There are several examples where public use has stimulated innovations in areas,where demand from the private sector alone hardly would justify investments ininnovations. One example is the use of EDI in the health care sector. Earlyimplementation of EDI in public hospitals has initiated development and a widediffusion of EDI not only in the health care sector but in other sectors of the economy.

Another factor in the creation of an advanced demand is the development within areaswith specialized communication needs. One of the drivers on the market for Internetaccess and high-speed connections has been the growth in telework. Telework has

been stimulated through tax deduction schemes for employer financed home PCs.Telework has both stimulated demand for telecom connections and for various typesof office products providing secure and efficient communication between the home-

based work place and the office. This is an area with wide perspectives for thedevelopment of mobile services which can contribute to demand for UMTS, Wi-Fiand other wireless services.

5. Denmark as a test market for telecom products

The concept of test market has played an important role in the Danish debate onindustrial policy. The conce pt is used in the presentation of the Danish industrial IT

policy published in 199810

, and in later reports published by the Ministries of Research and Trade and Industry1112.

The Danish market has, in previous decades, been used as a test market for electronics. IBM has, for instance, used Denmark as a test market for the introductionof personal computers. Companies, who want to be visible on a national market, may

prefer to start their introduction of new products on a small market.

10

Erhvervsministeriet: ’IT/Tele/Elektronik – Danmarks ervhvervspolitiske strategi’, 1998.11 Forskningsministeriet: ’Sund konkurrence og ægte valgfrihed’, 1999.12 Erhvervsfremmestyrelsen: ’IT/Kommunikation – en erhvervsanalyse’, 2001.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 10/24

10

Strategies and products can be tested before they are introduced on a larger scale. Itmay also be an advantage if competition with major international competitors can beavoided in the test phase. Other factors that could make Denmark attractive as a testmarket is that Denmark has a well developed telecom infrastructure and, in general, ahigh penetration of ICT products.

In addition to this, new electronic products penetrate the market much more rapidly inDenmark than in most other European countries13. A survey made in 2000 amongDanish companies within IT and communications confir ms that Denmark in 2000-2005 still may be considered as an important test market14.

It has been argued that Denmark is well suited for a position as a test market becausethe Danish telecom market is one of the most open and competitive market within theEU. This is a result of a deliberate Government policy since 1995, where ’Best andCheapest’ was introduced as the overall objective for Danish telecom policy15. Thestrategy was to maintain a telecom regulation, which was ahead of the rest of the EU

in terms of liberalization and creation of real competition. The early liberalization has been decisive for new operators entering the Danish telecom market, and has been themajor driver f or the large investments made in the Danish telecom infrastructure inthe mid 1990s16. The most obvious example of this is the entry of France Telecomthrough establishment of Mobilix in 1997 (see box 1).

Box 1: Mobilix/Orange

Mobilix was established in Denmark in 1997, and it won one of the four GSM1800licenses which were offered this year. From the beginning, the ambitions went beyondthe Danish borders. Mobilix was one of France Telecom’s first major engagements ina foreign national market in Europe, and Mobilix was planned to cover theScandinavian market, which at that time was the most advanced in the world withrespect to mobile services.

Denmark was seen as a market suitable for development and testing of new services.From the outset, substantial investments were made in marketing, infrastructure anddevelopment of a new organization.

From March 1998, Mobilix offered national coverage for mobile telephony. FromJanuary 1999, Mobilix offered fixed services as well, and in October 1999, Mobilix

became a full scale telecom operator offering all types of telecom services. In these

years, Mobilix was recognized to be one of the most innovative operators on theDanish market, and introduced a number of new services. Mobilix developed in co-operation with a national clearing bank one of the first mobile payment systems usingthe mobile phone as a personal terminal for electronic payments with debit cards.

13 ‘The International Takeoff of New Products: The Role of Economics, Culture, and CountryInnovativeness - Do new products take off at consistently different times in different countries? Why?’,Gerard Tellis, 2003, 22 (2) , pp.188-208. In: Marketing Science.14 Ministry of Trade and Industry.15Ministry of Research and Information Technology: ‘Best and Cheapest by Way of Real Competition’,Copenhagen, 1995.16

See, e.g., Andersen Management International: ’Konkurrencesituationen i telesektoren i Danmark’(The level of Competition in the Danish Telecom Sector), report to Ministry of IT and InformationTechnology, Copenhagen 1999.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 11/24

11

The investments in the Danish market were not matched by the immediate revenueobtained and the Danish affiliate generated a heavy deficit. In December 2000,Mobilix became an affiliate of Orange, and in particular after the internationaltelecom crash, major cuts in the budget were demanded. Innovation activities weresubstantially reduced and, presently, product development is primarily made by the

parent Orange company. The Danish part of Orange has, however, been able tomaintain a R&D department with 20-30 employees doing R&D for the entire Orange.Orange Denmark has acquired special competences in certain areas, and the Danishmarket is still considered to have a strategic importance.Sources: Interviews and press releases from Orange/Mobilix

The Danish telecom market is still among the most advanced in Europe, but Denmark has not been able to maintain its position as a test market. Orange is still testing someof its products in Denmark, but most tests take place in other countries. Sometimes,the same product is tested in a number of countries using different pricing models or marketing strategies in each country, and Denmark has not a unique position in that

respect.

Products introduced by Sonofons are often first tested on the Norwegian market byTelenor (the majority share holder of Sonofon). Nor does TDC see Denmark as a

particular test market. When operators are asked to compare Danish and foreignmarkets, they not see the Danish market as particularly innovative. They rank theinnovativeness of the Danish market for fixed network services to be on the averagelevel of the EU countries, while the mobile market is above average but far from aleading position. In particular, the markets of UK and Norway are more advancedthan the Danish, and also the Swedish market is more advanced in certain areas.

Denmark has not been in front in the development of UMTS, as it was in thedevelopment of GSM and especially NMT. Even though 3G services already have

been available for some time in both Japan and South Korea and in a number of European countries, such services are not offered in Denmark yet. 3 – the newcomer on the Danish 3G market – will as the first operator introduce UMTS services by theend of this year, while TDC will wait until 2004. A reason for this could be thatDenmark was among the last countries within the EU to auction its UMTS licenses.Another reason is that the Danish licenses are stricter with regard to network sharing

between the licensees. This increases the level of investments in network infrastructure needed to offer 3G services and may delay the introduction. On the

other hand, it will in the long term enable more competition in the development of new networks and services.

More serious, however, is that the Danish telecom industry, so far, has been unable tomake the necessary investments in order to build up core competences within 3G at aninternational level. UMTS is a much more complicated technology that GSM and

NMT. It is, therefore, more difficult for small enterprises to afford the investmentneeded to stay competitive - in particular in a situation where the Danish market isless advanced than in a number of other countries.

I-mode is another technology that not has reached the Danish market. When NTT

DoCoMo wanted to test this technology in Europe, they chose to start off in Germany

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 12/24

12

and the Netherlands. The Danish market did not seem to be attractive – maybe because of the fierce competition on prices.

Responses to a questionnaire distributed to national regulatory agencies in selectedcountries reveals that the timing for introduction is very similar on the different

markets. It is not possible to find a clear trend, but Germany has been early in their adoption of all the services included in the questionnaire. None of the services listedseem to have been using Denmark as a test country (maybe apart from GSM, but thatcannot be confirmed by the questionnaire). It is, however, important to note that thetime of introduction is determined by a combination of market and regulatoryconditions, as most of the services demand a license before they can be introduced. Afew services not included in the questionnaire have been introduced in the Danishmarket first, e.g., Multiplan (first developed and marketed by TDC under the nameDuét) and mobile payment (introduced by Orange).

The Danish position as a test market has been lost during the international telecom

crisis. Focus was moved from innovation towards cost reduction and pricecompetition. In addition to this, the markets for mobile communication have matured,and this has led the operators to concentrate on the markets with the largest volume.Finally a delay in auctioning of UMTS licenses has prevented a vanguard position onthe 3G market – at least in the short run.

Table 5: Time of introduction for selected services

GSM GPRS ADSL FWA

Denmark 1992 01/2001 07/1999 12/2000Sweden 1992 10/2001 Spring 1999 12/2001

Norway 1993 1/2001 6/1999 3/2000UK 1992 4/2001 12/1998 9/2000Netherlands 1994 12/2000 11/1999 2002Germany 1992 12/2000 1/1999 8/1999France 1992 5/2002 11/1999 No informationSource: Responses from national regulators

6. The role of competition

This section is concerned with the relations between competition and innovation -

with respect to the implications of competition on innovation activities, on the onehand, and the implications of innovations on the competitive environment, on theother. These two questions are often seen as two sides of the same coin, so thatcompanies innovate to have a stronger stand in the competitive environment and thatcompetition, consequently, increases innovation activities. However, it is not alwaysthat simple, and it is important to examine the two questions more thoroughly.

The implications of competition include the following points:

• The extent of innovation activities• The innovators (who)• The character of innovations

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 13/24

13

The implications of innovations include the following points:

• Market shares• The character of competition

6.1 The implications of competition on innovation activities

A comparison of the extent of innovations in the telecom sectors before and after the processes of liberalization speaks in favor of the competitive market situation.However, the supposition that competition leads to increased innovation activitiesdoes not apply as a law of nature in all situations. In the Schumpeter-based innovationtheory, on the contrary, it is argued that competition can hamper innovation, as therewill be less economic room for innovative activities17. But in the telecom sector, it hasclearly been proven that innovation activities have grown considerably with theintroduction of liberalization. This does not imply that the sector formerly was lackinginnovativeness; many of the technologies which, at present, are implemented have

been developed in the monopoly period. But the incremental innovations are currentlyfar more numerous and the degree of variation is considerably bigger, and a radicalinnovation as Internet, which, so to say, comes from outside the traditional telecomsector, would not have developed in the same manner and seen such a wide diffusionwithout a liberalization of alternative operators’ access to the telecom networks.

The question of who the most innovate operators are can be analyzed along the linesof the above discussion on whether competition enhances of limits innovativeness. Isit primarily the big operator, TDC, or is it first and foremost the newcomers whichinnovate? The answer is far from simple and needs clarification. A company like

Cybercity has been and is continuously an innovative force on the Danish telecommarket. The company was, e.g., the first to introduce ADSL in Denmark. Telia waslikewise, in the beginning, very active on the Danish market with considerableinvestments, but has since then had to limit its investment and development activities

because of great financial problems. Telia has in Denmark cut its investment activitiesdown to a level of 20-25% of what it was in 2000, and the development staff has beencut down to one third18. The reason for this downscaling of activities is that, in manymarket segments, Telia has not succeeded in making money on the Danish market. Ina start-up phase, it is possible to ‘invest in the future’, but in the long run it is not

possible to keep on investing if this does not result in a positive economic outcome,says Telia.

TDC – the incumbent on the Danish market – has initiated a number of marketintroductions during the past decade. The most often mentioned innovation is the Duétservice, which integrates mobile and fixed network telephony for the customers, andwhich, for example, won the innovation price in 1999 at the big ITU technologyexposition in Geneva. However, often TDC is not the first to introduce new serviceson the Danish market. In most cases, TDC follows the first innovator but eventuallymanages to become the biggest player in the new market segment. This applies, tosome extent, to Internet access – the so-called ISP area – and it applies, to a large

17

This theory has found some empirical evidence – see, for instance, Luc Soete: ‘Firm Size andInventive Activity: The Evidence Reconsidered’, European Economic Review 12, 1979.18 Information from interview with Ole Krogh Buus, Telia.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 14/24

14

extent, to ADSL. With respect to cable modem, Telia Stofa was the first operator onthe market. However, the market force of TDC is bigger, as TDC has more cable-TVcustomers than Telia Stofa. An overview of different innovations and the innovatingcompanies is provided in table 6.

Table 6: Who was first? Examples of services and technological solutions and thefirst innovators

First innovatorIN-based services TDCInternet access UNI-C (UNI2)Duét TDCPrepaid mobile cards SonofonNational mobile roaming SonofonGPRS SonofonLocation based services OrangeMobile payment OrangeMMS IdeationhouseADSL CybercityCable modem Telia StofaWLAN Non-operators

An often given explanation for the relatively late market introduction by theincumbent operator is that the incumbent has to earn back its considerableinvestments in earlier technological solutions, for instance ISDN in relation to ADSL,or that the incumbent already has technological and economically profitable solutionsin its product portfolio which it does not immediately see any reason to supplement

with other solutions, for example leased lines in relation to SDSL. The explanation isthus that an operator, which already has a large market share on a given market, doesnot want to ‘cannibalize’ its own market – which follows from general business logic.There will, however, continuously be an evaluation of when it pays to offer substituting or supplementing products.

The explanation as to why the big operator often manages to become dominant also innew market segments is – in contrast to the theory predicting that first-comers willwin the market – that the big operators mostly have a solid technology competenceand financial capacity, but also that it is possible for them to build on the existingdominance in complementary markets. New technological solutions mostly build on

the existing infrastructure. ADSL is a much discussed example in this respect. TDCwas not the first with ADSL in Denmark, and Cybercity and Tiscali rapidly acquiredlarge market shares of the – in the beginning – small ADSL market. But after a coupleof years, TDC has come to dominate the market with more than 80% of all ADSLsubscribers. This has resulted in accusations against TDC regarding price dumpingand delays in the procedures with respect to service delivery to customers of other operators. Both accusations have, however, been rejected by the competition authorityand the IT and telecom agency. However, the accusations have not been given up bythe plaintiffs and the complaints continue in the system.

However, no matter what the end result will be, it is not strange from a general

economics point of view that there are transaction procedures and, therefore, costsincurred in relation to interactions between different operators. The operator which

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 15/24

15

owns the network will generally have an advantage over other operators, and the roleof regulation will be to diminish all transaction procedures and costs for alternativeoperators as soon as they arise. The problem, in an innovation context, is that this canlimit some of the incentives for the company owning the network to develop newapplications if equal opportunities are to be given to other operators at once. This,

however, may be necessary in a situation where one operator sits with theoverwhelming part of the access capacity.

The conclusion with respect to innovativeness is that one cannot unequivocallydetermine whether the incumbent operator or the newcomers are the most innovative.If one is talking about products which substitute for existing services (for exampleSDSL in stead of leased lines) and where there may be a certain cannibalization of own products, there will be a tendency for new players to come first to the marketwith new services for the customers. If, on the other hand, we are dealing with

products covering new demands (for instance integration of fixed and mobilenetworks), it can just as well be the old operator as the new ones being the first

innovator. When, furthermore, are added the big financial problems of the newoperators, limiting their innovativeness and pushing them towards building a

profitable business on their existing product portfolio, then the incumbent operator will, to an increasing degree, dominate innovation activities.

This may have implications for the total amount of innovations in the market. If acompetition mainly based on price competition becomes too sharp, it may havenegative effects on the degree of innovativeness. This situation exists in Denmark according to Telia. They believe that there is far too much weight in the Danish telecom policy under the heading of ‘best and cheapest by way of competition’19 oncheapest and too little weight on best – including innovativeness.

With respect to the character of innovations as a consequence of competition, thereare three important issues, which are dealt with here:

1) the increasingly demand driven nature of innovations2) the dominance of service developments as compared with genuine research

activities3) the internationalization of the telecom sector

The two first questions are intimately interrelated. In a competition oriented market,

the players will, to a larger extent than in a monopoly market, follow a logic whereinnovations are guided by demand. In a monopoly situation, the operator canintroduce new services where and when it fits into an overall plan, includingdepreciations of innovation activities. In a more competitive situation, the operatorsare more inclined to follow the logic of the market.

This has led to a situation where the activities of innovation of the operators currentlymust be characterized as service development rather than genuine research activity.This issue is discussed later in the paper in the section on the divisions of labor

between operators and equipment manufacturers. Suffice it to say here that the fact

19

This was the title of the telecom policy of the Danish government published in 1995 and remains themain focus of telecom policy developments. (Forskningsministeriet: ‘Bedst og billigst gennem reelkonkurrence’, 1995).

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 16/24

16

that genuine research activities are located mainly with the equipment manufacturers(and the universities) means that the differentiation in the basic network and servicedeliveries, in principle, are rather small among the different operators. The operatorscan buy the same basic elements from the equipment producers. And, the emphasis inthe innovation activities of the players in the telecom transport market will be on

service development, where linking and interoperability between functionalities and billing innovations become crucial. This division of labor, which is increased bycompetition and which pushes the operators towards a concentration on their coreactivities - i.e. to deliver communication and information services to their customersleaving the genuine research activities to the equipment manufacturers – has the effectthat the tendency towards product differentiation which competition induces,

primarily will find an expression on the service front - especially the smaller andincremental service elements. The problem with such incremental innovations is thatthey can relatively easy be copied and that a sharp price competition may be theresult. In the last instance, it may, therefore, turn out that the competitive struggle

primarily will depend on the point of departure of the operators with respect to

network infrastructure and financial capacity with respect to renewal and extension if their network.

Liberalization and internationalization of telecom markets have led tointernationalization and commercialization of innovations made by the operators. Itcould, therefore, be argued that the term ‘national systems of innovation’ is becomingless meaningful, as innovations are made by international companies and not bynational companies. The example of Tiscali could indicate that innovations on theDanish telecom market depend more on the competence in the Italian telecom sector than in the Danish. The creation of more multinational telecom operators may imply aconcentration of innovation activities within countries hosting parent companies,while innovation activities in affiliates are reduced. However, innovation activitiesmay also be concentrated in those markets with the highest level of competence in a

particular field. The Danish market has examples of both trends. The Danish affiliateof Tiscali hosts hardly any research or development, while the Danish affiliate of Orange carry out research and development for the entire Orange in certain areas. Inthe same manner, TDC has spread their innovation activities not only among severallocations in Denmark but also among foreign affiliates. The organization of R&D in

both Orange and TDC thus provides examples where the local availability of competence seems to affects the location of activities.

6.2 The implications of innovation on competition

The question regarding how innovations affect competition – including the questionof whether an innovative company will win market shares from companies with lessinnovation activities – is partly dealt with in the above sections in relation to theADSL development. However, before focusing on market shares it should bementioned that the new services and communication possibilities result in a totalmarket growth, from which all market actors will benefit. It is thus not a static marketsituation with a stable demand to be distributed in different ways between theoperators. This was, to some extent, the case earlier on where the share of the incomeof a family used on telecommunications was very constant. However, this does not

apply any more in a situation where mobile communications and Internet has beenadded on top of the telecommunication consumption of families. And, it does not

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 17/24

17

either apply to the telecom usage of businesses, which has increased considerablyduring the past years.

These issues also have relevance in relation to the interoperability between newinnovative services. The individual operator has an interest in increasing its turnover,

but there can be a trade-off regarding the interests in either a smaller share of a bigmarket or a large share in a small market. The big market can be obtained if there isagreement between the operators on standards and accounting principles, while asmaller market may be the result of a lack of agreement. This problem issue is, e.g.,relevant to MMS, where the operators at present have a hard time agreeing on theaccounting principles – a fact which is holding back market development in the area.The incentive to buy a mobile terminal supporting MMS and to use MMS is limited if MMS messages can only be sent internally among the subscribers of the operatorsseparately.

On the whole, it is difficult unequivocally to conclude that innovativeness leads to

increasing market shares. Many other factors also play a role, first and foremost pricecompetition and marketing campaigns. But the cases mentioned in the followingillustrate that innovative operators in different cases have won considerable marketshares as a consequence of innovation activities. As already mentioned, this does notnecessarily mean that the first innovator will keep its lead. Small innovativecompanies can quickly be overtaken by other telecom companies as the ASDSLexample illustrates.

The DSL technologies were developed for more than 10 years ago but were notintroduced on the Danish market until 1999 with the introduction of ADSL.Cybercity, closely followed by Tiscali (Worldonline), were the first ones on theADSL market, and they quickly acquired large market shares of the initially smallADSL market. In 2000, Cybercity and Worldonline and TDC had each app. one thirdof the market. This does not correspond to the general development in Europe whereit was primarily the old former monopoly operators which already from the beginningdominated this market. However, the ‘raw cupper’ was opened for access for other market actors already in 1998 in Denmark – two years ahead of the EU decision in thearea. This has not only given another distribution of market shares in Denmark butalso a higher penetration. On the basis of the new technological possibilities for offering high-speed access to Internet and because of the competition from Cybercityand Tiscali – and maybe also because of the fact that TDC did not get a FWA license

in 2000 – TDC opted for at speedy extension of the ADSL access availability. At present, almost 97% of TDC’s customers can get access to ADSL. With respect tomarket shares, TDC has become very dominant on the ADSL market and has morethan 80% of the total number of ADSL subscribers, while Cybercity is down to 10%and Tiscali down to 6% (see table 2). It has been difficult for Cybercity and Tiscali toretain their relatively good point of departure because of the complementarity betweenADSL and the physical access network owned by TDC.

Cable modem is an alternative to ADSL in high-speed Internet access. Cable modemwas introduced in 1998/99 in Denmark. StofaNet was the first provider, but since thenTDC has also arrived on the scene. StofaNet has given Telia a good possibility for

offering high-speed access, while for TDC cable modem is more like a supplement toADSL. As a ‘first-mover’, Telia has acquired the biggest market share of the 133,000

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 18/24

18

cable modem customer in 2002. Telia has two thirds of these customers and TDC hasthe last third. However, in a longer term perspective it is very likely that TDC will bethe biggest operator also in this market segment, as TDC cable-TV has app. 800,000customers, while StofaNet only has 350,000. The potential of TDC is thus far the

biggest.

Duét is a service which combines mobile and fixed access for customers. The Duétservice was launched by TDC in 1997/98. Duét was, right from the beginning, metwith complaints from Sonofon regarding cross subsidization (from the fixed network to mobile); however, the complaint was rejected by the competition authority whichreasoned that this was a new service and in itself a profitable service. Since then,Sonofon has marketed its own combination services, DuoFon and later on Multiplan,which however is specifically directed at the business customer segment, while Duéthas a broader customer target. It is difficult to document that Duét meant a jump inadvance in market shares for TDC, as the service was launched in a period wherecompetition with new operators (Mobilix/Orange and Telia) was increased for other

reasons. However, Duét must be considered as a solid success and has contributed toconsolidate TDC’s position on the mobile market.

Prepaid mobile cards are incremental innovations. They were introduced on theDanish market in 1998/99 but cannot be seen as a clear success with respect to thedevelopment of market shares in this period. It was in the same period thatMobilix/Orange and Telia had their entry on the market, and both of these operators – and especially Mobilix/Orange – quickly acquired considerable market shares. Theeffect of the prepaid cards of Sonofon can thus best be measured by the limitations inlosses of market shares. Moreover, prepaid cards are a type of innovation where other operators quickly can offer something similar – which also happened.

The gains from Duét and prepaid cards are thus hidden in the total market growth andin the market shares of the newcomers, but still it can be concluded that there aremarket shares to be gained by being the first innovator on the market. However,whether this gain can be sustained depends on many circumstances, includingstrengths in complementary areas (ADSL), development potentials (cable modem),new substituting products (Duét) and price competition (prepaid cards). Especially

price competition is a serious problem for smaller incremental innovations whichrelatively easily can be copied. This point is emphasized by Sonofon20, where theanalysis is that the advantages offered by product innovations easily can be overtaken

and exposed to price competition, while process innovations often are of a morefundamental character resulting in productivity gains, which can have a more long-lasting effect on competition. Product innovations will, therefore, often give shortmarket advantages, where process innovations can provide more long termcompetitive advantages and increased market shares. The convergence betweenmobile and fixed networks is an area where process innovations may provide morelong-lasting competitive advantages, says Sonofon. And, Next Generation Network developments are also an area where operators can gain more long term marketadvantages.

20 Interview with Kim Wehrs from Sonofon.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 19/24

19

With respect, finally, to the question whether innovation leads to more competition,this depends partly on how increasing or diminishing competition is defined. If increasing competition is defined as a growing number of operators and a more equaldistribution of market shares, it is not given that innovation leads to increasingcompetition. This applies, for instance, if it is the incumbent operator which is the

primary innovator. But if increasing competition is defined as a sharpened struggle between the operators, it can positively be confirmed that innovation leads toincreasing competition. Under all circumstances, it leads to another and more dynamicform of competition as compared to the sheer price competition or a competition

based on marketing campaigns.

7. The division of labor between operators and equipment manufacturers

In the old telecom structure, the operators were the all-dominating users as well as themain actors in the development and innovation activities concerning equipment,network and service. There was, however, a division of labor where the operators

concentrated their activities on network and service development – including basicand long term research – while their equipment manufacturers (typically national)were responsible for the development and production of equipment. As advancedusers and developers of telecom technologies, the operators could continuouslyconsolidate their position as central players – often supported by close contacts totechnical universities. The equipment manufacturers typically went through adevelopment where they, by way of close contacts with the operators, acquiredcompetences for an increasing engagement in research and development activities.

This structure was decisively changed with the introduction of liberalization andcompetition, while it, at the same time, was a decisive precondition for this marketdevelopment. The existence of a number of advanced equipment producers effectivelylowered the entry barrier to a relatively complicated market and was, consequently, animportant condition for the establishment of a number of new operators on the market.This again meant new potentials for the equipment manufacturers to choose a strategy

based on research and development. This development was, moreover, enhanced bythe fact that the old operators loosened their tight relations with their nationalequipment producers and increasingly started buying on the open market – pressed bythe liberalization initiatives taken by the EU Commission and the aggressivecompetitive behavior of the new operators. This had, as a natural consequence, thatthe long term research and development activities were lowered by the operators.

Important parts of the research and development activities in networks and equipmentand partly also in services were, by the middle of the 1990, located and under considerable development among the equipment manufacturers. This development isillustrated by table 7 showing the research and development activities of differentcompanies in respectively 1987 and 1999 – that is to say until the telecom boom. Thetendency shown is accentuated by the fact that the new aggressively competingoperators by and large do not have any R&D activities21. The table also shows that theR&D activities of the equipment producers in 1999 have developed to a levelcomparable with the research intensive pharmaceutical industry, represented here byRoche.

21 The argument is not affected by the fact that some of these operators have disappeared during thecrisis, as this is not related to their R&D activities.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 20/24

20

Table 7: R&D as percentage of turnover

1987*) 1999**)AT&T 9,8 1,6BT 2,1 1,9NTT 3,8 3,7

TDC 2,4***) 1,2***)Ericsson 9,1 14,5Nortel 12,3 13,9Nokia n.a. 10,4Cisco n.a 18,7

WorldCom n.a. ~0Qwest n.a. ~0Global Crossing n.a. ~0

Roche n.a. 15,5Sources:

*) M. Fransmann in G. Pogorel: ‘Global Telecommunications Strategies and

Technological Changes’, Amsterdam 1994, p. 280

**) M. Fransman: ‘Telecoms in the Internet Age’, Oxford 2002, p. 49

***) Interview with Ole Mørk Lauridsen in Ingeniøren, 18.03.1998

This development based on ’stylized facts’ is also found in Denmark, however,modified by the fact that the formerly larger companies in the Danish equipmentindustry, to a large extent, disappeared along the way, while new internationalcompanies arrived.

The new division of labor between operators and equipment manufacturers has led toa situation where the development activities of operators almost entirely are in servicedevelopment. There are no genuine long term research activities among the telecomoperators in Denmark, but there is a service development close to the market. And,there is also a tendency for equipment producers to enter service development, as theydo not see a sufficient development in this field among the operators, or they engagethird-part companies for the service development activities.

The division of labor between operators and equipment producers is, according to TI(Telekommunikationsindustrien i Danmark – the Danish organization for the telecom

operators)22

, a entirely natural and basically positive development, which followsfrom the concentration on core competences of the companies as a consequence of the process of liberalization. The development in the R&D activities of TDC (and its predecessors) is clear illustration of this. It is, however, not everybody withknowledge on the development of the telecom sector, who sees this division of labor as an entirely positive development. The concern is that it can be short sighted to leanentirely on the innovation activities of the equipment manufacturers. The mostcomprehensive innovation activities are established in a cooperative relationship

between different kinds of actors, i.e. operators, equipment manufacturers, content producers, universities, technology consultants etc., is the point of view23.

22 Interview with Ib Tolstrup from Telekommunikationsindustrien.23 Interview with Torben Rune from Netplan.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 21/24

21

In a Danish context, the equipment producers in the traditional telecom area withlarge research and development activities are, first and foremost, Nokia, which hasone of its large development centers in Copenhagen, and the companies which are

built up around the fiber optic industry with its point of departure in NKT Elektronik.However, in addition to this there are the companies from the IT area and companies

with their point of departure in the Internet development. The other large internationalequipment manufacturers as Ericsson and Siemens have downscaled their genuineresearch and development activities in Denmark to a considerably lower level than

before.

Telecommunications is presently very dependent on the IT area based on chipdevelopment and computer technology with hardware/software configurations. One of the most often mentioned companies in this category in Denmark is Giga, which onthe basis of its important competences in chip design for optical communications was

bought by Intel in 2000.

The service development of the operators takes place in a cooperative relationshipwith the equipment manufacturers, and the same thing applies to the implementationof new equipment and solutions, which the operators buy from the equipment

producers. An important reason for having a genuine research activity as the regionaltelecom operators formerly had in Denmark with Teleteknisk Forskningslaboratoriumwas, in addition to the independent research results obtained, that it provided a better

possibility for a qualified cooperation with the equipment manufacturers. And, thefact that the operator side no more maintains such a readiness in knowledgedevelopment changes the balance in the cooperative relationship with the equipment

producers. An example of this is the implementation of Next Generation Networks.Apart from the many good reasons for a transition towards a more modern, fullyintegrated and packet based network, an important reason for the transmission is alsothat equipment manufacturers in a few years will stop servicing the existing networks

based on traditional exchanges. A radical and not unrealistic development possibilityis that the equipment producers to an increasing degree will take over the operation of the networks while leaving the service operation to the operators.

Another important aspect of the development is that the actors on the operator side aswell as the manufacturing side increasingly are internationalized. All major operatorson the Danish telecom market (TDC, Sonofon, Telia, Orange, Tele2, etc.) are parts of international companies, and the by far largest equipment manufacturer with

development activities in Denmark is the Finnish company Nokia. The ownershiprelation is not in itself decisive, as a locally owned company also can decide toupgrade or downscale its development activities or establish them in other countries.One of Nokia’s largest development centers outside Finland is, as mentioned, locatedin Copenhagen. But it makes development activities more exposed to uncontrollabledecisions that international actors can close or move development activities to other countries. This has, for instance, happened to the development activities of Ericsson inDenmark, which have been downscaled especially in the Copenhagen area.

This potentially volatile situation also applies to the operator side, where the major part of development activities can be located in other countries. Telia Denmark has,

for example, removed most of its development activities and now has to rely on theactivities of the mother company in Sweden. Tiscali, whose mother company is

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 22/24

22

Italian, is dependent on the development activities in Italy. However, it should benoted that the decreasing level of genuine development activities among operators inDenmark only to a small degree is related to knowledge and experience coming fromthe mother companies abroad. The most important reason is the changing division of labor between operators and equipment manufacturers.

The telecom operators in Denmark have not be able to or wanted to place themselvesin the same central role in relation to the equipment manufacturers and content

providers as, for instance, NTT DoCoMo in Japan. This comparison may seem to beinappropriate, but is illustrates that it is not a given and unequivocal tendency thatequipment manufacturers are the central players in the research and development

processes. In the example of DoCoMo, which has its own large research anddevelopment activities, it is the telecom operators, which is centrally placed andmanages the cooperation with equipment manufacturers and content producers. Thisis among other things related to the size of the market and the relatively large number of equipment producers in Japan, but it is also dependent on the fact that the relations

of strength are affected by company strategies. This shows that the liberalization of the telecom sector does not necessarily lead to a passive technology receiver positionfor telecom operators.

With the technological solutions, which are on their way in both fixed and mobilewith NGN and 3G technologies, there will in the coming years be possibilities for sharper divisions of labor among network provision, virtual network provision andcontent deliverance. This will make demands on the telecom operators with respect toadaptation to the new conditions, where the operators will not to the same extent as

presently hold the whole value chain in the telecom transport area. If the operators, onthe on side, leaves a number of network operation activities to the equipmentmanufacturers and, on the other side, witnesses virtual operators and content providersas active players on the transport market, there is a clear scenario where the survivalof traditional operators does not only require a clear business positioning but also adevelopment cooperation with the other actors in the field.

8. Conclusion

The paper examines innovation activities in the Danish telecom sector. Despite theimportance of innovation (also in this sector), not much has been written on the topicof telecom innovation. Much has been written on the penetration (diffusion) of new

services and on the price developments for telecom services. Much has also been published on the importance of new telecom services for the renewal of processes and products of other sectors, but on the topic of innovations in the telecom sector itself,the amount of published material is rather scanty.

The paper concentrates on the market based factors affecting innovation and on theimplications of innovations on competition. Policy intervention is also important andso are the existing technology platforms with their impact on path dependencies.However, the focus here is on the market related factors, including domestic demand,strategies of operators with respect to test markets, competition in the sector, and thedivisions of labor between telecom operators and equipment manufacturers.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 23/24

23

The paper emphasizes the importance of advanced demand. In Denmark, telecomdemand is relatively advanced and the take-up of new services relatively rapid in aninternational comparison. However, markets in Europe have converged much duringthe past 5-10 years with respect to penetration of services and regulatory conditions,and differences have become more limited. A result of this (in combination with the

changing focus of operators resulting from the telecom crisis) has been that the testmarket status that Denmark clearly had in the end 1990s has, to some extent,evaporated.

The liberalization of the telecom sector has clearly changed the patterns of innovationin the sector. Telecom operators have moved towards service developments, close tothe market, while genuine research and development activities increasingly are takencare of by the equipment manufacturers. This is probably the clearest conclusion thatone can draw from the relationship between competition and innovation in the sector.It is a general trend in the whole telecom sector even though the Japanese exampleillustrates that there are other possible options where operators play a more central

role in innovation activities.

It can also be concluded that competition has unleashed many innovations in thesector. Whether the innovative accomplishments are bigger under a competitionregime than under a monopoly regime cannot be determined from the documentationin the paper. This would require a deeper analysis of the amount and character of innovations under different market conditions. However, there is no doubt thatcompetition has opened the way for many incremental, but also for some more radicalinnovations.

With respect to the implications of innovations on the competitive environment, the paper shows that innovations may contribute to increases in market shares for theinnovative operators. However, there are many other factors to be taken intoconsideration, and often the innovations of smaller newcomers to the market areovertaken by incumbents, basing their market strength on their existing marketdominance.

In crude theories on competition, it is often assumed that competition willautomatically lead to more innovations, as operators will innovate in order to expandor consolidate their market positions. But the reality is more complicated than this

partly tautological argument. Competition may also turn out to limit innovation if

competition becomes overwhelmingly price based and if operators run into fiercefinancial problems. The character of competition is, therefore, important to include inthe analysis and can, furthermore, be dealt with by means of policy interventionfavoring one kind of competition over the other. In Denmark, the debate on this themeis gaining weight, illustrated, e.g., by the inclusion of the innovation question in thelatest competition analysis by the Danish IT and telecom agency24. The innovationtheme will probably gain more prominence in the discussions on the development of the telecom sector in the immediate years to come.

24 See footnote 1 of this paper.

8/22/2019 Falch Henten Skouby Tadayoni

http://slidepdf.com/reader/full/falch-henten-skouby-tadayoni 24/24

9. References

Aghion, Philippe et al: ‘Competition and Innovation: An Inverted U Relationship’,The Institute for Fiscal Studies, WP02/04, 2002.

Andersen Management International: ’Konkurrencesituationen i telesektoren iDanmark’ rapport til Forskningsministeriet, 1999.

Dosi, Giovanni: ’Technological Paradigms and Technological Trajectories’, ResearchPolicy 11, 1982.

Dutta, Soumitra & Amit Jain: ‘The Networked Readiness of Nations’, INSEAD,2002. Erhvervsfremmestyrelsen: ’IT/Kommunikation – en erhvervsanalyse’, 2001.

Erhvervsministeriet: ’IT/Tele/Elektronik – Danmarks ervhvervspolitiske strategi’,1998.

Forskningsministeriet: ’Bedst og billigst gennem reel konkurrence’, 1995.

Forskningsministeriet: ’Sund konkurrence og ægte valgfrihed’, 1999

ITU: ’Internet for a Mobile Generation’, 2002.

Lundvall, Bengt-Åke (ed.): ‘National Systems of Innovation – Towards a Theory of

Innovation and Interactive Learning’, Pinter, 1992.

Porter, Michael: ‘The Competitive Advantage of Nations’, The Free Press, 1990.

Schumpeter, Joseph: ’The Theory of Economic Development’, 1912.

Schumpeter, Joseph: ’Business Cycles’, 1939.

Soete, Luc: ’Firm Size and Inventive Activity: The Evidence Reconsidered’,European Economic Review 12, 1979.

![IPTV Market Development and Regulatory Aspectsorbit.dtu.dk/files/2506559/ITS2006_conference_version[1]… · · 2015-10-20IPTV market development and regulatory aspects Reza Tadayoni](https://static.fdocuments.in/doc/165x107/5ae331097f8b9a495c8ce7d2/iptv-market-development-and-regulatory-12015-10-20iptv-market-development-and.jpg)