FAIR DEBT COLLECTION PRACTICES TRAINING CONFERENCE · PDF fileFAIR DEBT COLLECTION PRACTICES...

148

FAIR DEBT COLLECTION PRACTICES TRAINING CONFERENCE March 7-8, 2014 San Antonio, TX Introductory Training Sponsored by: The National Consumer Law Center® (NCLC) 7 Winthrop Square, 4th Floor Boston, MA 02110 617-542-8010 www.nclc.org The National Association of Consumer Advocates (NACA) 1730 Rhode Island Avenue, NW, Suite 710 Washington, DC 20036 202-452-1989 www.naca.net Co-sponsored by: LAF Chicago Seniors Project

Transcript of FAIR DEBT COLLECTION PRACTICES TRAINING CONFERENCE · PDF fileFAIR DEBT COLLECTION PRACTICES...

FAIR DEBT COLLECTION PRACTICES TRAINING

CONFERENCE

March 7-8, 2014

San Antonio, TX

Introductory Training

Sponsored by:

The National Consumer Law Center® (NCLC) 7 Winthrop Square, 4th Floor Boston, MA 02110 617-542-8010 www.nclc.org

The National Association of Consumer Advocates (NACA)

1730 Rhode Island Avenue, NW, Suite 710 Washington, DC 20036

202-452-1989 www.naca.net

Co-sponsored by: LAF Chicago Seniors Project

Online Materials:Online Materials:Online Materials:Online Materials:

Introductory Training Materials: http://www.nclc.org/conferences-training/introductory-course-material-2014.html

No Username or Password needed

Fair Debt Collection Practices Fair Debt Collection Practices Fair Debt Collection Practices Fair Debt Collection Practices Introductory TrainingIntroductory TrainingIntroductory TrainingIntroductory Training

Featured Speakers:Featured Speakers:Featured Speakers:Featured Speakers:

Stacy Bardo Peter Barry

Brian L. Bromberg Bernard Brown

Kathy Ann Heibert-Cruz Cary L. Flitter Jean Healey

Robert J. Hobbs Peter Holland

David Humphreys Keith J. Keogh Steve Koval

Robert W. Murphy Michael T. O’Connor David J. Philipps Mary E. Philipps Richard Rubin Luke Wallace

Michelle Weinberg

ACKNOWLEDGMENTSACKNOWLEDGMENTSACKNOWLEDGMENTSACKNOWLEDGMENTS

Thanks to our speakers for volunteering their time and expertise; to NCLC staff Robert J. Hobbs,

Charles M. Delbaum, and Jessica Hiemenz for coordinating the conference, CLEs, and the materials; to Debbie Parziale, Eleanna Cruz, Beverlie Sopiep, and Marina Levy for handling registrations and finalizing

the materials; and to Svetlana Ladan for coordinating the website materials.

© © © © 2014201420142014 National Consumer Law Center® National Consumer Law Center® National Consumer Law Center® National Consumer Law Center® ---- Materials included in this book cannot be copied or reproduced in Materials included in this book cannot be copied or reproduced in Materials included in this book cannot be copied or reproduced in Materials included in this book cannot be copied or reproduced in any way without the express written permission of NCLC®.any way without the express written permission of NCLC®.any way without the express written permission of NCLC®.any way without the express written permission of NCLC®.

Introductory Course Agenda (Tentative agenda 2-21-14)* FAIR DEBT COLLECTION PRACTICES TRAINING CONFERENCE

Sponsored by NCLC, NACA, and LAF Chicago Seniors Project

5:00pm-8:00pm March 6, 2014 (Thursday) Registration

March 7, 2014 (Friday) 7:15 - 8:00am Registration Coffee and pastries

8:00 - 9:00 How Debts Are Collected, Robert Hobbs, Michelle Weinberg

9:00 - 9:10 Break

9:10 - 10:10 Fair Debt Collection Practices Act: Coverage, Violations, & Remedies, Dick Rubin

10:20 - 11:20 Establishing Substantial Damages in a Debt Collection Harassment Suit, Luke Wallace,

David Humphreys

11:20 - 11:30 Break

11:30 - 12:30pm FDCP Fundamentals: The Care and Feeding of Your FDCP Case (Client Intake, Retainers,

Recording Calls, Client Logs, Investigation), Robert Murphy, Bernard Brown

12:30pm - 2:00 Lunch on your own

2:00 - 3:15 Selecting, Developing, Valuing Letter and Overcharge Cases, David J. Philipps, Mary E.

Philipps

3:25 - 4:25 Basic Discovery in a Debt Collection Abuse Case, Michael O’Connor

4:25 - 4:35 Break

4:35 - 5:35 Selecting, Developing, Valuing Phone Harassment Cases, Peter Barry

5:45 - 7:00 Reception

March 8, 2014 (Saturday) 7:15 - 8:00am Coffee and pastries

8:00 - 9:00 Taking and Defending Depositions, Negotiating Settlement Agreements, Peter Barry

9:05 - 10:05 Debt Collectors’ Defensive Strategies, Brian Bromberg, Stacy Bardo

10:05 - 10:15 Break

10:15 - 11:15 Credit Reports: FCRA and FDCPA, Dick Rubin

11:20 - 12:20pm Telephone Consumer Protection Act Basics, Keith Keogh

12:20 - 1:40 Conference Lunch - Jean Healey

1:40 - 2:40 Ethical Issues in Fair Debt Collection Cases, Brian Bromberg

2:50 - 3:50 Developing a Private Fair Debt

Practice, Cary Flitter, Steve

Koval

Bankruptcy Practice and

FDCPA Cases, Kathy

Cruz

Developing a Fair Debt

Legal Services Practice,

Michelle Weinberg

3:50 - 4:00 Break

4:00 - 4:50 Bankruptcies, Debt Collection Suits, and FDCPA Claims, Kathy Cruz

4:55 - 5:45 Defending Consumers in State Court, Peter Holland

FAIR DEBT COLLECTION FAIR DEBT COLLECTION FAIR DEBT COLLECTION FAIR DEBT COLLECTION PRACTICES PRACTICES PRACTICES PRACTICES INTRODUCTORY INTRODUCTORY INTRODUCTORY INTRODUCTORY TRAININGTRAININGTRAININGTRAINING

TABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTS FRIDAYFRIDAYFRIDAYFRIDAY How Debts Are Collected, How Debts Are Collected, How Debts Are Collected, How Debts Are Collected, Michelle WeinbergMichelle WeinbergMichelle WeinbergMichelle Weinberg, Robert Hobbs , Robert Hobbs , Robert Hobbs , Robert Hobbs

Life of a Debt Chart……………………………………………………………………………………………22

How Debts are Collected (PowerPoint)…………………………………………………………………23 Fair Debt Collection Practices Act: Coverage, Violations, & Remedies, Fair Debt Collection Practices Act: Coverage, Violations, & Remedies, Fair Debt Collection Practices Act: Coverage, Violations, & Remedies, Fair Debt Collection Practices Act: Coverage, Violations, & Remedies, Dick RubinDick RubinDick RubinDick Rubin Fair Debt Collection Practices Act…………………………………………………………………………34 Establishing Substantial Damages in a Debt Collection Harassment Suit, Establishing Substantial Damages in a Debt Collection Harassment Suit, Establishing Substantial Damages in a Debt Collection Harassment Suit, Establishing Substantial Damages in a Debt Collection Harassment Suit, Luke WaLuke WaLuke WaLuke Wallace, llace, llace, llace, David HumphreysDavid HumphreysDavid HumphreysDavid Humphreys

Fighting for the Forgotten…………………………………………………………………………………41 Selecting, Developing, Valuing Letter and Overcharge Cases, David J. Philipps, Mary E. Selecting, Developing, Valuing Letter and Overcharge Cases, David J. Philipps, Mary E. Selecting, Developing, Valuing Letter and Overcharge Cases, David J. Philipps, Mary E. Selecting, Developing, Valuing Letter and Overcharge Cases, David J. Philipps, Mary E. PhilippsPhilippsPhilippsPhilipps Outline: Selecting, Valuing, Developing Letter and Overcharge Case……………………45

Letters for Slides 7-43 Enlarged…………………………………………………………………………61 Basic Discovery in a Debt Collection Abuse CaseBasic Discovery in a Debt Collection Abuse CaseBasic Discovery in a Debt Collection Abuse CaseBasic Discovery in a Debt Collection Abuse Case, , , , Michael O’ConnorMichael O’ConnorMichael O’ConnorMichael O’Connor Sample Discovery Documents……………………………………………………………………………90 SATURDAYSATURDAYSATURDAYSATURDAY Debt Collectors’ Defensive StrategiesDebt Collectors’ Defensive StrategiesDebt Collectors’ Defensive StrategiesDebt Collectors’ Defensive Strategies,,,, Brian Bromberg, Stacy BardoBrian Bromberg, Stacy BardoBrian Bromberg, Stacy BardoBrian Bromberg, Stacy Bardo

Common Debt Collector Defenses (PowerPoint)…………………………………………………98 Telephone Consumer Protection Act BasicsTelephone Consumer Protection Act BasicsTelephone Consumer Protection Act BasicsTelephone Consumer Protection Act Basics, , , , Keith KeoghKeith KeoghKeith KeoghKeith Keogh Telephone Consumer Protection Act Basics (PowerPoint)……………………………………108 Ethical Issues in Fair Debt ColEthical Issues in Fair Debt ColEthical Issues in Fair Debt ColEthical Issues in Fair Debt Collection Caseslection Caseslection Caseslection Cases, , , , Brian BrombergBrian BrombergBrian BrombergBrian Bromberg Legal Ethics and Fair Debt Collection Litigation…………………………………………………116

B. B. B. B. Bankruptcy Practice and FDCPA CasesBankruptcy Practice and FDCPA CasesBankruptcy Practice and FDCPA CasesBankruptcy Practice and FDCPA Cases, , , , Kathy Kathy Kathy Kathy Ann HeibertAnn HeibertAnn HeibertAnn Heibert----CruzCruzCruzCruz (Online Only Materials) Barbara V. Evans v. JP Mortgan Chase Bank, N.A.; et al. Memorandum Opinion C. C. C. C. Developing a Fair Debt Legal Services PracticeDeveloping a Fair Debt Legal Services PracticeDeveloping a Fair Debt Legal Services PracticeDeveloping a Fair Debt Legal Services Practice, , , , Michelle WeinbergMichelle WeinbergMichelle WeinbergMichelle Weinberg Legal Services Corp., Fee Generating Cases………………………………………………………136

Update on Attorney Fees……………………………………………………………………………………139

FTC, Telemarketing Sales Rule Debt Relief Rule…………………………………………………145

Bankruptcies, Debt Collection Suits, and FDCPA ClaimsBankruptcies, Debt Collection Suits, and FDCPA ClaimsBankruptcies, Debt Collection Suits, and FDCPA ClaimsBankruptcies, Debt Collection Suits, and FDCPA Claims,,,, Kathy Kathy Kathy Kathy Ann Heibert Ann Heibert Ann Heibert Ann Heibert CruzCruzCruzCruz (Online Only Materials) Shawn Michael Humes v. LVNV Funding, L.L.C. and Hosto. Buchan, Prater & Lawrence, P.L.L.C., Order from District Court adopting Bank Court Findings of Fact Order from District Court awarding Fees in Full Memorandum Opinion as to Core Claims and Proposed Findings of Fact and Conclusions of Law as to Noncore Claims Proposed Order Granting Plaintiffs’s Appplication for Attorney Fees and Costs

Fair Debt Collection Practices Fair Debt Collection Practices Fair Debt Collection Practices Fair Debt Collection Practices Introductory Introductory Introductory Introductory TrainingTrainingTrainingTraining Speaker Speaker Speaker Speaker BioBioBioBio’’’’ssss

Stacy Bardo is a partner at the Consumer Advocacy Center, P.C. in Chicago, Illinois. Stacy litigates cases involving unlawful debt collection practices, consumer fraud, predatory lending, automobile fraud, wrongful repossessions, mortgage foreclosures, credit reporting disputes, identity theft, and electronic fund transfer issues, and has successfully defeated several binding mandatory arbitration clauses. She has been appointed class counsel in numerous national and statewide class actions certified in Illinois, New York, California, Michigan, Minnesota, and Washington and is licensed to practice in the State of Illinois, the U.S. District Courts for the Northern District of Illinois, the Eastern District of Wisconsin, and the Northern District of Indiana, and the U.S. Court of Appeals for the Seventh Circuit. Stacy is a former Vice-Chair of the Chicago Bar Association’s Consumer Law Committee. As a Board Member of the National Association of Consumer Advocates (“NACA”), Stacy has also served on the Steering Committee for several Association conferences and is a member of NACA’s Nominating Committee. She is a member of the Illinois State Bar Association and volunteers her time as Vice President for the Associate Board of CARPLS, Chicago’s Coordinated Advice and Referral Program for Legal Services. Stacy is a graduate of Northwestern University and Loyola University Chicago School of Law. Peter Barry has been a consumer rights lawyer admitted in the State and Federal courts of Minnesota. He is admitted in numerous other courts including the United States Supreme Court. His national practice protects consumers against illegal debt collection practices under the FDCPA. In 2005, he was named Consumer Lawyer of the Year by the National Association of Consumer Advocates. In 2010, he was hired by the Attorney General for the State of Texas and appeared as an expert witness in a consumer fraud case resulting in a nearly $14 million dollar verdict. State of Texas v. Jubilee Financial Solutions, L.P. His three-day FDCPA Boot Camps have trained nearly 1,000 consumer lawyers in all 50 states, Washington, D.C. and Puerto Rico. Pete frequently appears in local and national media discussing consumer rights issues. He volunteers as an ethics investigator, pro bono attorney through the Federal Pro Se Project, and a law student mentor. Since 2003, Pete has been an adjunct Professor of Consumer Law at William Mitchell College of Law where he teaches federal consumer rights litigation. Brian L. Bromberg is the owner of the Bromberg Law Office, P.C. in New York City. Mr. Bromberg is admitted to practice law in New York and California. He graduated from Oberlin College, with a B.A. in Philosophy in 1987, and earned his J.D. from Brooklyn Law School in 1991. Mr. Bromberg is an active member of the National Association of Consumer Advocates (NACA), the Association of the Bar of the City of New York, and many other professional organizations. He has lectured attorney groups and the public on consumer-law issues, and helped revise NACA's Class Action Guidelines. Since 1999, Mr. Bromberg has concentrated his practice on consumer-protection litigation, including violations of the Fair Debt Collection practices Act (FDCPA), the Fair Credit Reporting Act (FCRA), the Equal Credit Opportunity Act (ECOA), the Truth in Lending Act (TILA), the Home Ownership and Equity Protection Act (HOEPA), the Fair Labor Standards Act (FLSA), the Telephone Consumer Protection Act (TCPA), and various state and federal unfair and deceptive acts and practices statutes. Mr. Bromberg has prosecuted numerous consumer-protection and fraud cases against debt-collectors, banks, credit-card companies, and automobile dealers. He has filed cases both individually and on a class basis, and has been appointed class counsel by state and federal courts across the country. Bernard Brown studied as an undergraduate at St. John’s College in Annapolis, Maryland (a “Great Books” school), before obtaining his undergraduate degree from the University of Toronto (in Toronto, Ontario) and his law degree from the University of Kansas. He has been in private practice in Kansas City since 1980. Between 1984 and 1996 his office was focused on representing victims of car fraud -- such as the fraudulent sale of rebuilt wrecks and cars with odometer rollbacks. More recently he also has worked on class actions relating to vehicle sales and financing, on mortgage fraud cases (in

conjunction with Legal Aid in Kansas City), and on “no title” car cases against finance companies. His cases have resulted in many notable jury verdicts and settlements, and a sizable number of his cases have resulted in published court decisions of significance in these areas of the law. Mr. Brown began doing public interest work when he was in college, starting with volunteer work at the headquarters of Common Cause in Washington, D.C. He has worked regularly with the National Consumer Law Center, the country’s leading consumer law think tank, for many years, and has written or contributed to many items relating to consumer law. He also has served as an adjunct law school professor teaching consumer protection law. Mr. Brown is a founding member of the National Association of Consumer Advocates (“NACA”), was one of its two original Co-chairs, has twice served on the NACA board, and currently serves as chair of its Ethics Committee. He has also worked closely for many years on a number of issues with other leading consumer groups (such as Consumers for Auto Reliability and Safety, Consumers Union, Consumer Federation of America, Public Citizen, and others), and has drafted proposed legislation and testified for these groups and on his own before Congress and state legislatures. He is involved in networking, idea-sharing, and direct advocacy efforts of consumer advocates across the country, and regularly gives presentations on various consumer law issues for other attorneys, consumer advocates, law enforcement personnel, and law students. He often is consulted by members of local and national media regarding car industry consumer issues, and appeared in a 60 Minutes piece in 1993 called “Totalled”, about rebuilt salvage cars. He has been serving on a Department of Justice Advisory Committee that is dedicated to building the “National Motor Vehicle Title Information System” (“NMVTIS”) since early 2010. In 2008 he received the “Countryman” award from the National Consumer Law Center. Kathy Ann Heibert-Cruz was born in Gary, Indiana where she attended both public and private schools until graduation from high school. She received her Bachelor=s degree Magna Cum Laude from Bradley University in 1977. She then attended law school at the Northwestern School of Law of Lewis and Clark College in Portland, Oregon in 1981. She has also obtained a Masters of Science degree in forensic studies from Indiana University in 1984. Ms. Cruz was licensed to practice law in Indiana in 1984, and later moved to Arkansas where she obtained her Arkansas law license in 1987. Before opening her own private practice, Ms. Cruz was the Deputy Public Defender for Garland County, and later also served as the Deputy Prosecuting Attorney for Garland County. Ms Cruz also previously worked for several Garland County law firms where she handled numerous civil and criminal cases, both at the trial and appellate level, including trials by jury. Ms. Cruz opened The Cruz Law Firm in 1997, and has focused her practice on bankruptcy. She has filed over 5,000 bankruptcy petitions, has practiced before both the 8th Circuit Bankruptcy Appellate Panel (BAP) and the 8th Circuit on bankruptcy appeals. Currently she serves as co-counsel on several class actions stemming from proofs of claims for pre-petition foreclosure fees. Ms. Cruz joined NACBA in 1998, and served as the Arkansas state chair until last year. Ms. Cruz is a member of many legal organizations, and currently serves at the Arkansas state chair for the National Association of Consumer Advocates. Jean Healey is the Senior Counsel for Enforcement Policy and Strategy Team at the Consumer Financial Protection Bureau (CFPB). She facilitates the implementation of the CFPB's enforcement strategies regarding mortgage servicing and debt collection. Prior to joining the CFPB she was an Assistant Attorney General in Massachusetts. Cary L. Flitter practices consumer law in suburban Philadelphia, Pennsylvania, New Jersey and in Courts around the United States. Flitter litigates principally consumer credit, fair debt and auto repossession cases, both individual cases and class actions. Cary serves on the adjunct faculty at Widener University School of Law in Wilmington, Delaware and at Temple University’s Beasley School of Law in Philadelphia, where he teaches Consumer Law and Litigation including Fair Debt Collection Practices and class action. From 1991 to 1998, Flitter served on the adjunct faculty at Philadelphia

University where he taught commercial law. Flitter has guest lectured on consumer law issues at Harvard Law School, The University of Pennsylvania Law School, The University of Houston’s Center for Consumer Law, and other venues. He is a graduate of the National Institute for Trial Advocacy and the Delaware Law School of Widener University, where he was named Alumnus of the Year in 2011. Mr. Flitter is a contributing author to Pennsylvania Consumer Law by Bisel Publishing Co. This is the leading treatise in Pennsylvania on consumer law. He is also a contributor to Consumer Class Actions 5th Ed. by the National Consumer Law Center. Flitter has written articles for the National Law Journal, the Legal Intelligencer and other publications. He is a frequent lecturer around the country and consultant for the media in matters of consumer credit, fair credit reporting, fair debt collection practices, auto finance and repossession, and class action. Cary was invited by the Federal Trade Commission to participate in its 2007 workshop Collecting Consumer Debts: The Challenges of Change, the FTC 2009 Roundtable, Consumer Debt Litigation, and the FTC 2011 Roundtable, Collecting Consumer Debt 2.0 in Washington, D.C. In the Court of Appeals, Cary successfully argued Brown v. Card Service Center, 464 F.3d 450 (3d Cir. 2006), Rosenau v. Unifund, 539 F.3d 218 (3d Cir. 2008) and other cases. Brown set broad standards for deception under the Fair Debt Collection Practices Act and became featured in a Time Magazine story Sue Up or Shut Up, October 19, 2006 - www.time.com/time/nation/printout/0,8816,1548158,00.html. Rosenau represented a case of first impression in the Circuit, in which the Court held it may be deceptive to the consumer to send dunning letters from a “legal department” where no attorney is involved. Flitter is the recipient of pro bono awards for Legal Services to Low Income Consumers from the President of the Pennsylvania Bar Association in 2006 and again in 2011. Flitter also serves as the year 2012 Co-Chair of the Federal Courts committee of the Montgomery (County, Pennsylvania) Bar Association, and has served on the Board of the National Associates of Consumer Advocates. Robert J. Hobbs has specialized in consumer credit issues, with particular attention to fair debt collection practices, in his more than 30 years at the National Consumer Law Center, Inc. (NCLC). He writes NCLC’s popular treatise Fair Debt Collection (7th Ed.); the bimonthly newsletter, NCLC REPORTS, now NCLC eReports on fair debt collection and repossession; The Practice of Consumer Law (2nd Ed. 2006); and he edits NCLC’s annual volume Consumer Law Pleadings on the Web. He testified on and proposed amendments adopted as part of the Fair Debt Collection Practices Act and the Truth in Lending Act, and participated in the drafting of NCLC's Model Consumer Credit Code (1974). He was the designated consumer representative in Federal Trade Commission rulemakings to regulate creditor remedies and to preserve consumers' claims and defenses. He started and helps run NCLC’s annual Consumer Rights Litigation and Fair Debt Collection Practices Conferences. He is a Deputy Director of NCLC; a former member of the Consumer Advisory Council to the Federal Reserve Board; a founder, former Director and Treasurer of the National Association of Consumer Advocates, Inc.; and a graduate of Vanderbilt University and of the Vanderbilt School of Law. Peter Holland is the Clinical Instructor, Consumer Protection Clinic, at the University of Maryland Law School. Peter is the author of two articles about debt buyer litigation: The One Hundred Billion Dollar Problem in Small Claims Court: Robo-Signing and Lack of Proof in Debt Buyer Cases; and Defending Junk Debt Buyer Lawsuits. Prior to teaching, he practiced in Annapolis, where he represented consumers in cases involving a broad array of consumer financial protection claims. Since 2009 he has run the Consumer Protection Clinic at Maryland, where he has trained law students and pro bono lawyers how to defend lawsuits filed by debt buyers. He is a frequent lecturer on the subject of debt buyer litigation. He is a member of the National Association of Consumer Advocates. David Humphreys has been practicing law since 1987. He was a member of the first class (1994) of the Gerry Spence Trial Lawyers College, Dubois, Wyoming. He was recognized in 2004 by the college, along with his partner, Luke Wallace, for his trial work and currently serves as a member of the teaching

staff. He and his partner, Luke Wallace, have participated in dozens of trials and settlements resulting in many million-dollar recoveries for their consumer law clients. His areas of special interest include debt collection abuse, predatory mortgage servicing and representing mentally challenged or vulnerable persons who have been trapped into debt by installment lenders. David has provided CLE and pro bono representation across the country and is grateful for his membership in NACA and close friendships that have resulted from his association with NCLC and NACA. He is most proud of his twenty-five-year partnership with his wife Tanya and their three children—a law student, a theatre artist, and a budding scientist. Keith J. Keogh is a partner at Keogh Law, Ltd. in Chicago, Il. Keith has been litigating TCPA class actions since early 2002 many of which have resulted in class wide settlements. He was selected as an Illinois Super Lawyer in 2014 and an Illinois Super Lawyer Rising Star each year from 2008 through 2013. In addition to litigating TCPA cases, Keith has spoken at numerous sessions on the TCPA. For example, he was a panelist for the December 2013 Strafford CLE Webinar titled Class Actions for Telephone and Fax Solicitation and Advertising Post‐Mims. Leveraging TCPA Developments in Federal Jurisdiction, Class Suitability, and New Technology; he was the sole presented for the National Association of Consumer Advocates November 2013 webinar titled Current Telephone Consumer Protection Act Issues Regarding Cell Phones; presenter for the November 2013 Chicago Bar Association Class Action Committee presentation titled Future of TCPA Class Actions; panelists for the March 20, 2013 Strafford CLE webinar titled “Class Actions for Telephone and Fax Solicitation and Advertising Post‐Mims. Leveraging TCPA Developments in Federal Jurisdiction, Class Suitability, and New Technology.” He has also spoken at several NCLC Conference for sessions on the TCPA. Steve Koval graduated summa cum laude from Emory University in Atlanta with a B.A. and M.A. in political science, and served as president of Emory's student body. He earned his law degree from American University's Washington College of Law in 1986, and returned to Atlanta to practice law. Steve has held numerous leadership positions in the legal community. He is a former chairman of the Family Law Section of the Atlanta Bar Association, and co-founder and former president of the Stonewall Bar Association. Steve attended his first NACA conference in 2004 and found it to be a life-changing experience. After the conference he shifted his practice from exclusively domestic relations to consumer law. FDCPA cases now account for approximately 90% of his law firm’s caseload, and Steve has never been happier practicing law. Robert W. Murphy is in private practice in Fort Lauderdale, Florida, focusing on consumer class action litigation. He presently serves as an adjunct professor of law at the University of Florida College of Law in Gainesville Florida. He is a past chair of the Consumer Protection Law Committee of The Florida Bar and is a Board Member, Secretary and Florida State Chairperson for the National Association of Consumer Advocates. He has spoken at many seminars and conferences hosted by a variety of state and national organizations, including The Florida Bar, The Academy of Florida Trial Lawyers, the National Consumer Law Center, the National Association of Legal Aid and Public Defenders, and the United States Military Judge Advocate Corps as well as college and law schools. In October, 2007 and April, 2011, the Federal Trade Commission designated Mr. Murphy to be panel member for the Fair Debt Collection Practices Act Symposium in Washington, DC, which addressed the rising abuses in the consumer debt collection industry. Mr. Murphy has been lead counsel in a wide variety of state-wide, regional and national consumer class actions throughout the United States . In 2003, Mr. Murphy obtained the first contested certified class under the Florida Retail Installment Sales Act as reported in Brown v. SCI Funeral Services of Florida, 212 F.R.D.602 (S.D. Fla. 2003), which was described in the South Florida Business Review as one of the most significant cases in South Florida in 2003. More recently, Mr. Murphy was lead counsel in a 2009 nationwide class action which provided over $50 million in relief to over 8,000 consumers whose vehicles had been wrongfully repossessed. To

date, Attorney Murphy has obtained class benefits estimated to be in excess of $500 million with significant cy pres awards to consumer and legal aid organizations. Mr. Murphy attended the U.S. Military Academy, and received his B.A. cum laude from Wake Forest University in 1984 and his J.D. from the University of Florida College of Law in 1987. He is admitted to practice in Florida and Georgia; the United States District Courts for the Middle District of Florida, Southern District of Florida, Northern District of Florida, Western District of Oklahoma, Northern District of Ohio, Middle District of Georgia, Northern District of Georgia; Western District of Michigan; Western District of Tennessee; United States Court of Appeals, Eleventh Circuit and has been admitted pro hac vice in numerous other state and federal courts. A regular contributor to local and national news media on consumer law topics, Mr. Murphy most recently appeared on ABC News Nightline on January 19, 2007 on the topic of consumer debt collection. He has authored and contributed to many articles and papers on consumer litigation issues, including a recent treatise on debt collection Michael T. O'Connor is a trial attorney with the Law Offices of Dean Malone, P.C. Mr. O’Connor earned his law degree from Texas Tech University School of Law, with the highest distinction of summa cum laude. Mr. O'Connor is a member of the Order of the Coif. After law school, Mr. O'Connor was a law clerk to the Honorable Charles Holcomb, Judge, Texas Court of Criminal Appeals. Mr. O’Connor serves as an officer on the Council for the Consumer & Commercial Law Section of the State Bar of Texas. Mr. O’Connor was listed in the May 2009 issue of D Magazine as one of the Best Personal Lawyers in Dallas, Texas. Mr. O’Connor was listed in the April 2011 issue of Texas Monthly as a Rising Star and one of the Top Young Lawyers in Texas. Mr. O’Connor is rated AV Preeminent by the Martindale-Hubbell Peer Review Ratings. Mr. O’Connor has spoken at numerous national and state conferences regarding consumer litigation issues. David J. Philipps and his sister, Mary E. Philipps, are partners in the law firm of Philipps & Philipps, Ltd., in southwest suburban Chicago. David is a graduate of the University of Illinois College of Law and Loyola University of Chicago. He served as law clerk to Justice Benjamin K. Miller of the Illinois Supreme Court from 1987-88. From 1988 to 1999, he practiced with the firm of Beeler, Schad & Diamond, P.C. in Chicago, Illinois, and was a shareholder in that firm from 1995 until leaving in late 1999 to found the firm that is now known as Philipps & Philipps, Ltd. David is a member of the Illinois state bar, and the bars of the U.S. District Courts for the Northern, Central, and Southern Districts of Illinois, the Northern and Southern Districts of Indiana, the United States Courts of Appeal for the Seventh and Ninth Circuits, and the United States Supreme Court. David is a founding member of the National Association of Consumer Advocates (1995), was the Illinois State Chair for NACA (2008-2013), and was elected to its Board of Directors in 2013. In 2011, he was named the NACA Private Attorney of the Year. He has lectured throughout the country at numerous FDCPA and class action seminars for NCLC/NACA and at seminars for his opponents. Their practice consists mainly of litigation for seniors and disabled persons who have been defrauded, or subject to illegal collection activity or improper credit reporting. David and Mary have worked on and/or been appointed class counsel in about 180 cases, which have recovered more than $65,000,000 for defrauded or abused consumers. Notable FDCPA appellate court cases litigated by David and Mary include: Gammon v. G.C. Services Limited Partnership, 27 F.3d 1254 (7th Cir. 1994)(unsophisticated consumer); Newman v. Boehm, Pearlstein & Bright, Ltd., 119 F.3d 477 (7th Cir. 1997)(condo and homeowner’s association dues covered by FDCPA); Turner v. J.V.D.B. & Associates, Inc., 330 F.3d 991 (7th Cir. 2003)(no intent as to false statements); Horkey v. J.V.D.B. & Associates, Inc., 333 F3d 769 (7th Cir. 2003)(calls at work and profanity); Chuway v. NAFS, Inc., 362 F.3d 944 (7th Cir. 2004)(amount of debt); Randolph v. IMBS, Inc., 368 F.3d 726,728-730 (7th Cir. 2004)(bankruptcy code does not preclude FDCPA); McMillan v. Collection Professionals, Inc., 455 F.3d 754 (7th Cir. 2006)(implying consumer was dishonest is actionable); and, Evory v. RJM Acquisitions Funding LLC, 505 F.3d 769 (7th Cir. 2007)(false statements

made to consumer’s attorney are actionable and limited-time settlement offer collection letters are actionable). Mary E. Philipps, and her brother, David J. Philipps are partners in the law firm of Philipps & Philipps, Ltd., in southwest suburban Chicago. Mary is a graduate of the University of Illinois College of Law and Northwestern University, and earned an LL.M. from the Universität Bielefeld in Germany. Mary is a member of the Illinois state bar, and the bars of the U.S. District Courts for the Northern, Central, and Southern Districts of Illinois, the Northern and Southern Districts of Indiana, and the United States Court of Appeal for the Seventh Circuit. Mary has been a member of the NACA since 2005. Their practice consists mainly of litigation for seniors and disabled persons who have been defrauded, or subject to illegal collection activity or improper credit reporting. David and Mary have worked on and/or been appointed class counsel in about 180 cases, which have recovered more than $65,000,000 for defrauded or abused consumers. Notable FDCPA appellate court cases litigated by David and Mary include: Gammon v. G.C. Services Limited Partnership, 27 F.3d 1254 (7th Cir. 1994)(unsophisticated consumer); Newman v. Boehm, Pearlstein & Bright, Ltd., 119 F.3d 477 (7th Cir. 1997)(condo and homeowner’s association dues covered by FDCPA); Turner v. J.V.D.B. & Associates, Inc., 330 F.3d 991 (7th Cir. 2003)(no intent as to false statements); Horkey v. J.V.D.B. & Associates, Inc., 333 F3d 769 (7th Cir. 2003)(calls at work and profanity); Chuway v. NAFS, Inc., 362 F.3d 944 (7th Cir. 2004)(amount of debt); Randolph v. IMBS, Inc., 368 F.3d 726,728-730 (7th Cir. 2004)(bankruptcy code does not preclude FDCPA); McMillan v. Collection Professionals, Inc., 455 F.3d 754 (7th Cir. 2006)(implying consumer was dishonest is actionable); and, Evory v. RJM Acquisitions Funding LLC, 505 F.3d 769 (7th Cir. 2007)(false statements made to consumer’s attorney are actionable and limited-time settlement offer collection letters are actionable). Richard Rubin is a private attorney in Santa Fe, New Mexico, whose federal appellate practice is limited to representing consumers in federal consumer credit protection cases, including credit reporting and debt collection abuse litigation, and to consulting for other consumer rights specialists around the country.The United States Court of Appeals for 33 the Seventh Circuit has acknowledged Mr. Rubin as a "nationally known consumer-rights attorney" (Bass v. Stolper, Koritzinsky, Brewster Neider, S.C., 1997 U.S. App. LEXIS 41397, *5 (June 6, 1997)). He and his solo practice were the subject of a profile published in the January 1993 ABA Journal. Mr. Rubin is the past chair of the National Association of Consumer Advocates and in 2000 was the recipient of NCLC’s Vern Countryman Award.Mr. Rubin has taught consumer law at the University of New Mexico School of Law, is a regular contributor to the Consumer Credit and Sales Legal Practice Series manuals published by NCLC, and presents continuing legal education and attorney-training programs nationally in the areas of consumer credit, warranty law, and debt collection abuse. Luke Wallace is a father, husband and a trial lawyer from Tulsa, Oklahoma. He is a partner in the consumer protection law firm, Humphreys Wallace Humphreys, P.C. Along with his partner, David Humphreys, he has tried consumer protection jury trials across the country. Luke very much enjoys training other lawyers in the areas of trial practice and consumer law. He speaks to national, state and local bar associations on FDCPA, wrongful collection, identity theft, false credit reporting, predatory lending, automobile fraud, wrongful foreclosures, trial skills and maximizing damages in consumer law cases. Luke is a 2001 graduate of the Gerry Spence Trial Lawyers College, Dubois, WY. In 2004, the college recognized him and his partner, David Humphreys, as Co-Warriors of the Year for the 18-state South Central region of the country. He is a member of the teaching staff of the college. Luke has been named an Oklahoma Super Lawyer since 2006. In 2002, The National Association of Consumer Advocates awarded him and his partner, David, the Trial Advocates of the Year Award.

Michelle Weinberg is a Supervisory Attorney at LAF (Legal Assistance Foundation), concentrating in the representation of seniors with consumer issues. She is a 1992 graduate of IIT-Chicago Kent College of Law. Ms. Weinberg began her career as a consumer lawyer in 1993 with the firm of Edelman & Combs, before opening a solo practice on Chicago’s North Side. After two years solo, she practiced with the firm of Horwitz Horwitz & Associates in 1999-2001, and joined LAF in June, 2001. Ms. Weinberg has handled a wide range of consumer cases, including claims under the Truth In Lending Act, the Fair Debt Collection Practices Act, the Illinois Consumer Fraud Act and other consumer protection statutes, including numerous predatory lending, automobile and home improvement fraud cases, and debt collection defense. In May, 2005, Ms. Weinberg received the Excellence in Public Interest Service Award from the United States District Court for the Northern District of Illinois and the Chicago Chapter of the Federal Bar Association. In 2011, she received the NACA Consumer Advocate of the Year for public interest work. Ms. Weinberg is frequently called upon to speak at legal conferences and to comment in the news media on emerging consumer issues. She is a former Chair of the Chicago Bar Association Consumer Law Committee, has been a member of the National Association of Consumer Advocates (“NACA”) since 1997, and is a former member of NACA’s board of directors. She is also a semi-professional musician and singer.

FFFFAIR AIR AIR AIR DDDDEBT EBT EBT EBT CCCCOLLECTION OLLECTION OLLECTION OLLECTION

TTTTRAINING RAINING RAINING RAINING CCCCONFERENCEONFERENCEONFERENCEONFERENCE

March 7March 7March 7March 7----8, 20148, 20148, 20148, 2014

San Antonio, TXSan Antonio, TXSan Antonio, TXSan Antonio, TX

Fair Debt Collection Practices Fair Debt Collection Practices Fair Debt Collection Practices Fair Debt Collection Practices IntroductoryIntroductoryIntroductoryIntroductory TrainingTrainingTrainingTraining

Participant DirectoryParticipant DirectoryParticipant DirectoryParticipant Directory

2014 Participants Directory By Name

Tom Addleman

Addleman Law Firm

255 NW Blue Parkway, Suite 200

Lee's Summit, MO 64063

816-994-6200

Micah Adkins

Burke Harvey LLC

2151 Highland Avenue suite 120

Bitmingham, AL 35205

205-747-1907

Kaitlyn Alavi

PSU Student Legal Services

PO Boc 791

Portland, OR 97207

503-725-4556

Adelaide Anderson

Consumer Law Project Public Counsel 610 South Ardmore Ave

Los Angeles, CA 90005

213-385-2977

Judith Asaad

Castle Law Office

500 N. Broadway Suite 1400

St. Louis, MO 63102

314-446-4657

Jeffrey Basinger

Mid-Missouri Legal Services

1201 West Broadway

Columbia, MO 65203

573-442-0116 206

Barak Berlin

Law Offices of Barak Berlin

41530 Enterprise Circle S Suite 209

Temecula, CA 92590

951-296-6188

Andrea Bopp Stark

Molleur Law Office

419 Alfred Street

Biddeford, ME 4005

207-283-3777

Barbara Boysen

University Student Legal Service

160 West Bank Skyway 219 19th

Avenue South

Minneapolis, MN 55455

612-624-1001

Bernard Brown

Brown Law Firm

1627 Main

Kansas City, MO 64108

816-283-3100

James Brown

Castle Law Office

500 N. Broadway Suite 1400

St. Louis, MO 63102

314-446-4650

Tim Bullock

Bullock Law LLC

827 Good Hope Drive

Castle Rock, CO 80108

888-682-3788

John Burnett

Burnett Law Office

1114 Main

Blue Springs, MO 64015

816-254-0400

Natalie Bush-Lents

California Monitor Program

401 E. Peltason Dr., Law 3800

Irvine, CA 0

949-824-4311

Francisco Cieza

Francisco Cieza, P.A. 2525 Ponce de Leon Blvd Suite 300

Coral Gables, FL 33134

786-423-8144

Jennifer Cohen

Bay Area Legal Services, Inc.

1302 N. 19th Street, Suite 400

Tampa, FL 33605

813-232-1222 143

Elliot Conn

Kemnitzer, Barron & Krieg

445 Bush Street, Floor 6

San Francisco, CA 94108

415-632-1900 122

Cory Crawford

Legal Aid of Arkansas

714 South Main Street

Jonesboro, AR 72401

870-972-9224 5305

Kathy Cruz

The Cruz Law Firm

1325 Central Ave

Hot Springs, AR 71901

501-624-3600

Joanna Darcus

Community Legal Services of

Philadelphia, Inc.

1424 Chestnut St

Philadelphia, PA 19102

215-981-3728

Melissa Deutsch

DeutschJacobs, A Law Practice

900 Congress Ave Ste L120

Austin, TX 78701

512-236-1998

Mitchell Dobbs

Legal Services Alabama

224 W. Main St

Dothan, AL 36301

334-793-7932 3758

Robert Doig

Robert James Doig, LLC

2985 Broadmoor Valley Road Suite 4

Colorado Springs, CO 80906

719-227-8787

Michael Eades

John Steinkamp & Associates

5218 S. East Street Suite E1

Indianapolis, IN 46227

317-780-8300

Stefanie Ebbens Kingsley

Legal Aid of the Bluegrass

546 East Main Street

Morehead, KY 40351

606-784-8921 2129

Cassie Fleming

DNA-People's Legal Services

PO Box 116

Crownpoint, NM 87313

505-786-5277

Cyrus Frazier

Louisiana Office of the Attorney

General

1885 North 3rd Street

Baton Rouge, LA 70802

225-326-6428

2014 Participants Directory By Name

Angela Habeebullah

Law Offices

1125 Grand, Suite 1200

Kansas City, MO 64106

816-842-3266

Timothy Harper

Castle Law Office

500 N. Broadway Suite 1400

St. Louis, MO 63102

314-446-4662

Casey Harris

NACA 1730 Rhode Island Ave NW Suite 710

Washington, DC 20036

202-452-1989 202

Jessica Hiemenz

National Consumer Law Center

7 Winthrop Sq., 4th Floor

Boston, MA 2110

617-542-8010

Joshua Hillin

Law Offices of John T. Orcutt

6616-203 Six Forks Rd

Raleigh, NC 27615

919-847-9750

Robin Hood

Robin Hood, Attorney at Law

3020 Bay Brg. Dr.

Flowood, MS 39232

601-862-9489

Calvin Hwang

Land of Lincoln

8787 State Street Suite 101

East Saint Louis, IL 62203

618-398-0958 273

William Jaworski

Law Office of william F. Jaworski

1274 S. Governors Avenue

Dover, DE 19904

302-730-8511

Jeanne Johons

New Mexico Legal Aid

301 Gold Ave SW, Suite 204 PO

Box 25486

Albuquerque, NM 87125

505-768-6112

Robert June

Law Offices of Robert June, P.C.

415 Detroit Street, 2nd Floor

Ann Arbor, MI 0

734-481-1000

Mohahammad Kazerouni

Kazerouni Law Group, APC

245 Fischer Ave Suite D-1

Costa Mesa, CA 92626

800-400-6808 3

Abbas Kazerounian

Kazerouni Law Group, APC

245 Fischer Ave Suite D-1

Costa Mesa, CA 92626

800-400-6808 2

Tashi Lhewa

The Legal Aid Society of New York

120-46 Queens Blvd.

Kew Gardens, NY 11415

718-286-2474

Dave Maxfield

Dave Maxfield, Attorney, LLC

5217 N. Trenholm Road, Suite B

Columbia, SC 29206

803-509-6800

Laureen McCloskey

Law Office of Laureen

McCloskey

848 Ella Street

Pittsburgh, PA 15243

412-706-2681

Jonathan Miller

Bromberg Law Office, P.C.

40 Exchange Place, Suite 2010

New York, NY 10005

212-248-7906

Nelson Mock

Texas RioGrande Legal Aid

4920 N. IH 35

Austin, TX 78751

512-374-2723

Tara Newberry

Connaghan Newberry Law Firm

7854 W Sahara Ave

Las Vegas, NV 89117

702-608-4232

Michelle Newman

Nevada Legal Services

204 Marsh Ave, Suite 101

Reno, NV 89509

775-284-3491 226

Angela Owens

Sices Law

2000 N. Central Expressway Suite 209

Plano, TX 75074

972-360-3253

Michael Pereira

Law Office of Ahmad Keshavarz

16 Court St., 26th Floor

Brooklyn, NY 11241

718-522-7900

Eric Peters

Eric G. Peters, Attorney At Law

710 Court St

Lynchburg, VA 24504

434-846-8737

Jacob Petry

Texas Attorney General's Office

300 W. 15th St

Austin, TX 78701

512-475-4184 [email protected]

Chet Randall

Molleur Law Office

419 Alfred Street

Biddeford, ME 4005

207-283-3777

Jason Rapa

Rapa Law Office, P.C.

141 S. 1st Street

Lehighton, PA 18235

610-377-7730

David Raulerson

Viles & Beckman, L.L.C.

6350 Presidential Ct

Fort Myers, FL 33919

239-334-3933

Cynthia Ravosa

Massachusetts Bankruptcy

Center

One South Avenue

Natick, MA 1760

508-655-3013

2014 Participants Directory By Name

Ira Rheingold

NACA

1730 Rhode Island Ave. NW

Washington, DC 20036

202-452-1989

Angie Robertson

Philipps & Philipps, Ltd.

9760 S. Roberts Road Suite 1

Palos Hills, IL 60465

708-974-2900

R. Lee Roland Law Offices of John T. Orcutt, P.C.

6616-203 Six Forks Road

Raleigh, NC 27615

919-847-9750

John Roper

The Roper Law Firm

5353 Veterans Parkway Suite D

Columbus, GA 31904

706-596-5353

Susan Rotkis

Consumer Litigation Assoc. P.C.

763 J. Clyde Morris Blvd Suite 1-A

Newport News, VA 23601

757-930-3660

Michael Salorio

Lenderman & Salorio

Attorneys At Law 303 S. 8th St.

El Centro, CA 92243

760-353-7949

Carla Sanchez-Adams

Texas RioGrande Legal Aid, Inc.

4920 N. IH 35

Austin, TX 78751

512-374-2763

Jordan Sartell

Zamparo Law Group, P.C.

1600 Golf Road Suite 1200

Rolling Meadows, IL 60008

224-875-3202

Virginia Schramm

Texas RioGrande Legal Aid

1111 North Main Ave

San Antonio, TX 78212

210-212-3706

Shelley Slafkes

Levitt and Slafkes

76 South Orange Ave Suite 305

South Orange, NJ 7079

973-313-1200

Jocelyn Smith

Legal Advocacy Center of Central

Florida, Inc.

128 Orange Avenue

Daytona Beach, FL 32114

386-255-6573 2513

Larry Smith

SmithMarco, P.C.

205 N. Michigan Ave. Suite 2940

Chicago, IL 60601

312-324-3532

John Steinkamp

John Steinkamp & Associates

5218 S. East Street #E-1

Indianapolis, IN 46227

317-780-8300

Bo Thomas

Addleman Law Firm

255 NW Blue Parkway, Suite 200

Lee's Summit, MO 64063

816-994-6200

Andrew Thomasson

Thomasson Law, LLC

101 Hudson Street, 21st Floor

Jersey City, NJ 7302

973-665-2056

Linda Tirelli

Garvey, Tirelli & Cushner, Ltd.

Westchester Financial Center 50 Main

St., Ste.390

White Plains, NY 10606

914-946-2200

Scott Ugell

Ugell Law Firm, P.C.

151 North Main Street suite 203

New City, NY 10956

845-639-7011

Marcus Viles

Viles & Beckman, L.L.C.

6350 Presidential Ct

Fort Myers, FL 33919

239-334-3933

Jason Watson

Law Offices of John T. Orcutt

6616-203 Six Forks Rd

Raleigh, NC 27615

919-673-9109

Ronald Weiss

Law Offices of Ronald S. Weiss

7035 Orchard Lake Road Suite 600

West Bloomfield, MI 48322

248-737-8000

Jeremy White

Virginia Legal Aid Society

513 Church Street

Lynchburg, VA 24504

434-846-1326 12

2014 Participants Directory By State

AZ, Phoenix, David McGlothlin, Hyde & Swigart CA, Santa Clara, Ben Dupre, Dupre Law Office CA, San Jose, Ronald Wilcox, Attorney at Law CA, Santa Ana, Abbas Kazerounian, Kazerounian Law Group, APC CA, San Diego, Robert Hyde, Hyde & Swigart CA, Santa Clara, William Kennedy, Consumer Law Office of William E. Kennedy CA, Burbank, Stephanie Tatar, Tatar Law Firm, APC CA, San Diego, Joshau Swigart, Hyde & Swigart CT, Rocky Hill, Dan Blinn, Consumer Law Group LLC CT, Hartford, Sarah Poriss, Sarah Poriss, Attorney at Law, LLC CT, New Haven, Joanne Faulkner, Law Office FL, Fort Lauderdale, Robert Murphy, Law Office of Robert W. Murphy FL, Daytona Beach, Kimberly Derry, Community Legal Services of Mid-Florida, Inc. FL, Lake Mary, Taras Rudnitsky, Rudnitsky Law Firm FL, Jacksonville Beach, Wendell Finner, First Coast Consumer Law FL, Jacksonville Beach, Ryan Moore, First Coast Consumer Law FL, Coral Gables, Leo Bueno, LEO BUENO, ATTORNEY, P.A. FL, Melbourne Beach, Michael Howard, Law Office of Michael G. Howard, P.A. GA, Macon, David Addleton, Addleton Ltd Co GA, Atlanta, Steve Koval, The Koval Firm LLC IL, Palos Hills, Mary Philipps, Philipps & Philipps, Ltd. IL, Chicago, Keith Keogh, Keogh Law, Ltd. IL, Chicago, Stacy Bardo, The Consumer Advocacy Center, P.C. IL, Chicago, Michelle Weinberg, LAF IL, Chicago, Craig Shapiro, Keogh Law, Ltd. IL, Palos Hills, David Philipps, Philipps & Philipps, Ltd. KS, Kansas City, AJ Stecklein, Consumer Legal Clinic LLC MA, Boston, Charles Delbaum, National Consumer Law Center MA, Arlington, Yvonne Rosmarin, Law Office of Yvonne W. Rosmarin MI, Davison, Rex Anderson, Rex Anderson, P.C. MO, Union, Steven White, Purschke, White, Robinson & Becker NC, Chapel Hill, Suzanne Begnoche, Suzanne Begnoche, Attorney at Law NJ, Maplewood, Philip Stern, Philip D. Stern & Associates, LLC NJ, Jersey City, John Ukegbu, Northeast new Jersey Legal Services NY, New York, Evan Denerstein, MFY Legal Services, Inc. NY, New York, Carolyn Coffey, MFY Legal Services NY, New York, Brian Bromberg, Bromberg Law Office, P.C. NY, new york, James Fishman, Fishman & Mallon, LLP NY, Spring Valley, Shmuel Klein, Shmuel Klein NY, New York, Robert Martin, DC 37 AFSCME Municipal Employees Legal Services NY, New York, Daniel Schlanger, Schlanger & Schlanger, LLP NY, West Islip, Joseph Mauro, The Law Office of Joseph Mauro, LLC NY, Brooklyn, Ahmad Keshavarz, Law Office of Ahmad Keshavarz NY, New York, Peter Lane, Schlanger & Schlanger, LLP NY, New York, Michael Litrownik, Bromberg Law Office, P.C. OH, Niles, Philip Zuzolo, Zuzolo law offices llc OK, Tulsa, Luke Wallace, Humphreys Wallace Humphreys P.C. OK, United States of America, David Humphreys, Humphreys Wallace Humphreys, PC PA, Dunmore, Carlo Sabatini, Sabatini Law Firm, LLC PA, Philadelphia, David Pearson, David E. Pearson

2014 Participants Directory By State

PA, Pittsburgh, Clayton Morrow, Morrow & Artim, PC PA, Philadelphia, Mark Mailman, Francis & Mailman PA, Philadelphia, Irv Ackelsberg, Langer Grogan & Diver, PC PA, Narberth, Cary Flitter, Flitter Lorenz, P.C. PA, Broomall, Daniel DeLiberty, The DeLiberty Law Firm, P.C. SC, Florence, Penny Cauley, Hays Cauley, P.C. TX, Austin, Amy Kleinpeter, Hill Country Consumer Law TX, Houston, Dana Karni, Karni Law Firm, P.C. TX, Fort Worth, Jerry Jarzombek, The Law Office of Jerry Jarzombek, PLLC TX, Bellaire, Ira Joffe, Ira D. Joffe, Attorney at Law UT, Salt Lake City, Ronald Ady, Ronald Ady, PLLC VA, Petersburg, Dale Pittman, The Law Office of Dale W. Pittman, PC VT, Thetford Ctr, Clare Kelsey, Law in the Public Interest, WA, Bellingham, James Sturdevant, Law Office of James Sturdevant WI, Big Bend, Devonna ("Dani") Joy, Consumer Justice Law Center LLC

MATERIALS

22

1

Robert Hobbs

National Consumer Law Center

Author, Fair Debt Collection (7th Ed. 2011)

Boston, Ma.

Copyright National Consumer Law Center, Inc.® 2014

How Debts Are Collected

Michelle Weinberg

Legal Assistance Foundation of Chicago

Chicago, Ill.

Introduction to Representing Consumers Abused

by Debt Collectors

� There is much of law on fair debt collection practices, and we can only cover a small part of it in the next two days.

� At the end of the presentation I will recommend additional resources to dig deeper into this area of the law.

� A good starting point is NCLC’s Fair Debt Collection (7th Ed. 2011) treatise—now 1268 pages

CONSUMER COMPLAINTS ABOUT

DEBT COLLECTORS

� Consumers complain more about debt collectors to the Federal Trade Commission than any other industry.

� The number of complaints increased yearly to 2011, then dropped slightly in 2012.

� Complaints have grown from about 11,000 to over 100,000 in the last 14 years.

23

2

Consumer Complaints About Collections Reported to FTC

0

10

20

30

40

50

60

70

80

90

100

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

(Th

ousan

ds)

3rd Party In-House

Source: FTC Annual Reports on the FDCPA, 2000-2010http://www.ftc.gov/reports/index.shtm

Unemployment Rate, U.S.A.January, 1995-2010

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

(Perc

ent)

Source: Bureau of Labor Statisticshttp://www.bls.gov/data/

24

3

Source: FRB Statistical Releases

http://www.federalreserve.gov/datadownload/

Bank Credit Card Chargeoffs

0

2

4

6

8

10

12

1985

Q1

1986

Q1

1987

Q1

1988

Q1

1989

Q1

1990

Q1

1991

Q1

1992

Q1

1993

Q1

1994

Q1

1995

Q1

1996

Q1

1997

Q1

1998

Q1

1999

Q1

2000

Q1

2001

Q1

2002

Q1

2003

Q1

2004

Q1

2005

Q1

2006

Q1

2007

Q1

2008

Q1

2009

Q1

Perc

ent

How Debt Collectors Operate

� The Myth: “Consumers all owe the debts

anyway.” (“They are all deadbeats

anyway.”)

� The depressing life of a debt collector

�Who collects debts

� How they collect

� Debt collectors flood our courts

THE MYTH: “THEY ARE ALL DEADBEATS ANYWAY”

97+% of consumers

pay their bills on time every month

(in a good economy)

IT’S IMPORTANT TO DEVELOP THE CONSUMER’S STORY!

25

4

THE MYTH:

“THEY ARE ALL DEADBEATS ANYWAY”

3% do not pay because of reasons not totally

within their control:

• Laid off

• Sick, disabled, or dead (or death of a spouse)

• Family breakup (new expenses for 2nd household)

• Dispute the obligation (ID theft, scammed,etc.)

• Creditor marketing of excessive credit

These inform an important part of the consumer’s

story.

THE MYTH:

“THEY ARE ALL DEADBEATS ANYWAY”

Can pay but won’t is about .1% (one in

a thousand)

• These may be the “deadbeats”

• Many debt collectors will not spend time on these accounts (as a waste of time)

•Some debt collectors will quickly sue these

consumers

THE MYTH:

“THEY ARE ALL DEADBEATS ANYWAY”

The “Myth” is pervasive!

It must be pushed aside by the client’s - story

- the facts

- the documents and records

� The myth is held by some judges, court clerks, legislators, public officials –anticipate it.

� The industry relies on the myth, but usually won’t argue with the data.

26

5

The Depressing Life

of a Debt Collector

�No one went college to be a debt collector.

�Debt collectors call millions of consumers each day, but only reach a few.

�Debt collectors get paid more the more money they bring in.

�Some debt collectors make good salaries ($60k +); most don’t

Imagine a warehouse full of cubbies,

with autodialers lining up continuous

calls for 8 hours each day. Almost no

one answers!

TYPES OF DEBT COLLECTORS

& INCENTIVES

� Flat Rate Collection Agencies

� Contingent Fee Collection Agencies

� Debt Buyers

� Collection Law Firms/Collection Agencies

� Repo Companies

� Specialty Collection Agencies: (Foreclosure Law Firms, decedent’s

estates & survivors, medical, child

support, checks, shoplifting)

27

6

COMMON METHODS OF

COLLECTION

� Phone Calls: Good, bad, and ugly

� Letters ( "duns" or "dunning letters")

� Adverse credit reports (lowers credit

score)

� Foreclosure, Repossession, Eviction

� Late fees, collection attorney fees,

interest

� Suit

� Arbitration

COMMON ILLEGAL DEBT

COLLECTION CONDUCT:

- Cursing, obscenities, name calling

- Calling neighbors, relatives, workplace

- False threats, like suit, arrest, jail,

seizing social security or other exempt property

Collection Lawsuits� Will the Creditor Actually Sue You?

� How to Respond to the Collector’s Lawsuit

� Fighting Back by Raising Defenses and Counterclaims

� What a Court Judgment Against You Really Means

� What Property and Income Is at Risk

� How to Respond to a Debtor’s Examination

28

7

Finding Cocounsel to Help Sue a

Debt Collector

� Attorney Directory: www.naca.net

� What You Should Tell Your Client

� Start a telephone call log in case litigation becomes necessary.

� Write up a chronology of the debt collection abuse and the events leading to it

� What If the FDCPA Does Not Apply?

FROM "Collecting Consumer Debt in America" BY ROBERT M. HUNT

Debt Buyer Lawsuits as a Collection Tool

� 575,000 debt suits in Massachusetts, 2000-2005

� 457,000 suits by 26 debt buyers in NYC, 2006 -2008

� 375,000 suits by Encore Capital Group in 2009

� 420,000 suits by Mann Bracken in 2008

29

8

Debt Buyer Lawsuits as a

Collection Tool

“Do not be intimidated by the Court House. The Small Claims Court is going to actually help you make money. It is the vehicle that flushes out payment. ”

--Larry K. Neil, The Complete Guide to Buying Debt (2013) (available at www.beadebtcollector.com).

COMMON CREDIT CARD

LITIGATION PROBLEMS

� Suing wrong person:

� Identity theft

� Authorized user v. account holder

� Similar names, e.g. Sr. and Jr.

� Suing for wrong amount:

� Payment not credited

� Unauthorized fees (check contract, state law)

� Suing on time barred debt (which state’s SOL?)

400 CONSUMER ATTORNEYS to WORK with

YOU to SUE ABUSIVE DEBT COLLECTORS

� Find out from an experienced NACA attorney about co-counseling:

� Does this collector sue on this small a debt?

� How do the local courts respond to suits

� against collection lawyers?

� Does this collection lawyer regularly collect consumer

debts bringing him within the FDCPA’s

coverage?

� Search for co-counsel with the lawyer directory on:

www.naca.net

30

9

Preparing a Consumer

to Sue a Debt Collector

�Preparation for lawyer intake:� Consumer starts a telephone call login case litigation becomes necessary.

� Tape recording calls may be criminal; save voicemails & letters.

� Consumer writes up a chronology of the debt collection abuse and the events leading to it.

� Consumer preserves documentsrelated to the transaction.

More on Debt Buyers

� Jurgens & Hobbs, “The Debt Machine: How the Collection Industry Hounds Consumers and Overwhelms Courts” (July 2010), available free at www.nclc.org.

•“

D

e

b

t

W

•“Debt Deception, How Debt

Buyers Abuse the Legal System to Prey on Lower-

Income New Yorkers” (May 2010), available free at

www.mfy.org.

Recorded Webinars for Free on www.nclc.org :

Free Resources for Fair Debt Collection Suits

Stopping Debt Collection Harassment and Responding to Debt Collection

Suits (May 2009) , Robert J. Hobbs, National Consumer Law Center®,

Michelle A. Weinberg, Legal Assistance Foundation of Metropolitan Chicago

Introduction to Representing Consumers Abused by Debt Collectors (July

2011), Robert Hobbs (NCLC), Robert Murphy (Law Offices of Robert W. Murphy).

Claudia Wilner (Neighborhood Economic Development Advocacy Project

(NEDAP)

31

10

Free Resources for Fair Debt Collection Suits

Excerpt from NCLC’s Fair Debt Collection p. 227

For More Information on Legal Remedies

to Fight Debt Collector Abuses

Visit the NCLC Exhibit Table forFair Debt Collection, Collection Actions and Surviving Debt :

Definitive Legal Practice Publications from National Consumer Law Center

www.nclc.org

32

11

SAVE THE DATE

CONSUMER RIGHTS LITIGATION CONFERENCE

Nov. 6-8 2014

TAMPA MARRIOT WATERSIDE TAMPA, FLORIDA

IDEAS INSPIRATION INSIGHT!

33

15 U.S.C. § 1692. Congressional findings and

declaration of purpose [FDCPA

§ 802]

(a) There is abundant evidence of the use of abusive, deceptive,

and unfair debt collection practices by many debt collectors.

Abusive debt collection practices contribute to the number of

personal bankruptcies, to marital instability, to the loss of jobs, and

to invasions of individual privacy.

(b) Existing laws and procedures for redressing these injuries are

inadequate to protect consumers.

(c) Means other than misrepresentation or other abusive debt

collection practices are available for the effective collection of

debts.

(d) Abusive debt collection practices are carried on to a substantial

extent in interstate commerce and through means and instrumen-

talities of such commerce. Even where abusive debt collection

practices are purely intrastate in character, they nevertheless di-

rectly affect interstate commerce.

(e) It is the purpose of this subchapter to eliminate abusive debt

collection practices by debt collectors, to insure that those debt

collectors who refrain from using abusive debt collection practices

are not competitively disadvantaged, and to promote consistent

State action to protect consumers against debt collection abuses.

15 U.S.C. § 1692a. Definitions [FDCPA § 803]

As used in this subchapter—

(1) The term ‘‘Bureau’’ means the Bureau of Consumer Finan-

cial Protection.

(2) The term ‘‘communication’’ means the conveying of infor-

mation regarding a debt directly or indirectly to any person

through any medium.

(3) The term ‘‘consumer’’ means any natural person obligated

or allegedly obligated to pay any debt.

(4) The term ‘‘creditor’’ means any person who offers or

extends credit creating a debt or to whom a debt is owed, but

such term does not include any person to the extent that he

receives an assignment or transfer of a debt in default solely for

the purpose of facilitating collection of such debt for another.

(5) The term ‘‘debt’’ means any obligation or alleged obligation

of a consumer to pay money arising out of a transaction in

which the money, property, insurance, or services which are the

subject of the transaction are primarily for personal, family, or

household purposes, whether or not such obligation has been

reduced to judgment.

(6) The term ‘‘debt collector’’ means any person who uses any

instrumentality of interstate commerce or the mails in any

business the principal purpose of which is the collection of any

debts, or who regularly collects or attempts to collect, directly or

indirectly, debts owed or due or asserted to be owed or due

another. Notwithstanding the exclusion provided by clause (F)

of the last sentence of this paragraph, the term includes any

creditor who, in the process of collecting his own debts, uses

any name other than his own which would indicate that a third

person is collecting or attempting to collect such debts. For the

purpose of section 1692f(6) of this title, such term also includes

any person who uses any instrumentality of interstate commerce

or the mails in any business the principal purpose of which is the

enforcement of security interests. The term does not include—

(A) any officer or employee of a creditor while, in the name

of the creditor, collecting debts for such creditor;

(B) any person while acting as a debt collector for another

person, both of whom are related by common ownership or

affiliated by corporate control, if the person acting as a debt

collector does so only for persons to whom it is so related or

affiliated and if the principal business of such person is not

the collection of debts;

(C) any officer or employee of the United States or any State

to the extent that collecting or attempting to collect any debt

is in the performance of his official duties;

(D) any person while serving or attempting to serve legal

process on any other person in connection with the judicial

enforcement of any debt;

(E) any nonprofit organization which, at the request of con-

sumers, performs bona fide consumer credit counseling and

assists consumers in the liquidation of their debts by receiv-

ing payments from such consumers and distributing such

amounts to creditors; and

(F) any person collecting or attempting to collect any debt

owed or due or asserted to be owed or due another to the

extent such activity (i) is incidental to a bona fide fiduciary

obligation or a bona fide escrow arrangement; (ii) concerns a

debt which was originated by such person; (iii) concerns a

debt which was not in default at the time it was obtained by

such person; or (iv) concerns a debt obtained by such person

as a secured party in a commercial credit transaction involv-

ing the creditor.

(G) Redesignated (F).2

(7) The term ‘‘location information’’ means a consumer’s place

of abode and his telephone number at such place, or his place of

employment.

(8) The term ‘‘State’’ means any State, territory, or possession of

the United States, the District of Columbia, the Commonwealth

of Puerto Rico, or any political subdivision of any of the

foregoing.

[Pub. L. No. 111-203, tit. X, § 1089(2), 124 Stat. 2092 (July 21,

2010)]

15 U.S.C. § 1692b. Acquisition of location

information [FDCPA § 804]

Any debt collector communicating with any person other than the

consumer for the purpose of acquiring location information about

the consumer shall—

(1) identify himself, state that he is confirming or correcting

location information concerning the consumer, and, only if

expressly requested, identify his employer;

(2) not state that such consumer owes any debt;

(3) not communicate with any such person more than once

unless requested to do so by such person or unless the debt

collector reasonably believes that the earlier response of such

2 15 U.S.C. § 1692a(6)(E), (F), (G) amended by Pub. L. No.

99-361, 100 Stat. 768 (July 9, 1986). See §§ 3.3.2, 5.5.14, supra.

Appx. A.2 Fair Debt Collection

71834

person is erroneous or incomplete and that such person now has

correct or complete location information;

(4) not communicate by post card;

(5) not use any language or symbol on any envelope or in the

contents of any communication effected by the mails or tele-

gram that indicates that the debt collector is in the debt collec-

tion business or that the communication relates to the collection

of a debt; and

(6) after the debt collector knows the consumer is represented

by an attorney with regard to the subject debt and has knowl-

edge of, or can readily ascertain, such attorney’s name and

address, not communicate with any person other than that

attorney, unless the attorney fails to respond within a reasonable

period of time to communication from the debt collector.

15 U.S.C. § 1692c. Communication in connection

with debt collection [FDCPA

§ 805]

(a) Communication with the consumer generally

Without the prior consent of the consumer given directly to the

debt collector or the express permission of a court of competent

jurisdiction, a debt collector may not communicate with a con-

sumer in connection with the collection of any debt—

(1) at any unusual time or place or a time or place known or

which should be known to be inconvenient to the consumer. In

the absence of knowledge of circumstances to the contrary, a

debt collector shall assume that the convenient time for com-

municating with a consumer is after 8 o’clock antemeridian and

before 9 o’clock postmeridian, local time at the consumer’s

location;

(2) if the debt collector knows the consumer is represented by an

attorney with respect to such debt and has knowledge of, or can

readily ascertain, such attorney’s name and address, unless the

attorney fails to respond within a reasonable period of time to a

communication from the debt collector or unless the attorney

consents to direct communication with the consumer; or

(3) at the consumer’s place of employment if the debt collector

knows or has reason to know that the consumer’s employer

prohibits the consumer from receiving such communication.

(b) Communication with third parties

Except as provided in section 1692b of this title, without the prior

consent of the consumer given directly to the debt collector, or the

express permission of a court of competent jurisdiction, or as

reasonably necessary to effectuate a postjudgment judicial remedy,

a debt collector may not communicate, in connection with the

collection of any debt, with any person other than the consumer,

his attorney, a consumer reporting agency if otherwise permitted

by law, the creditor, the attorney of the creditor, or the attorney of

the debt collector.

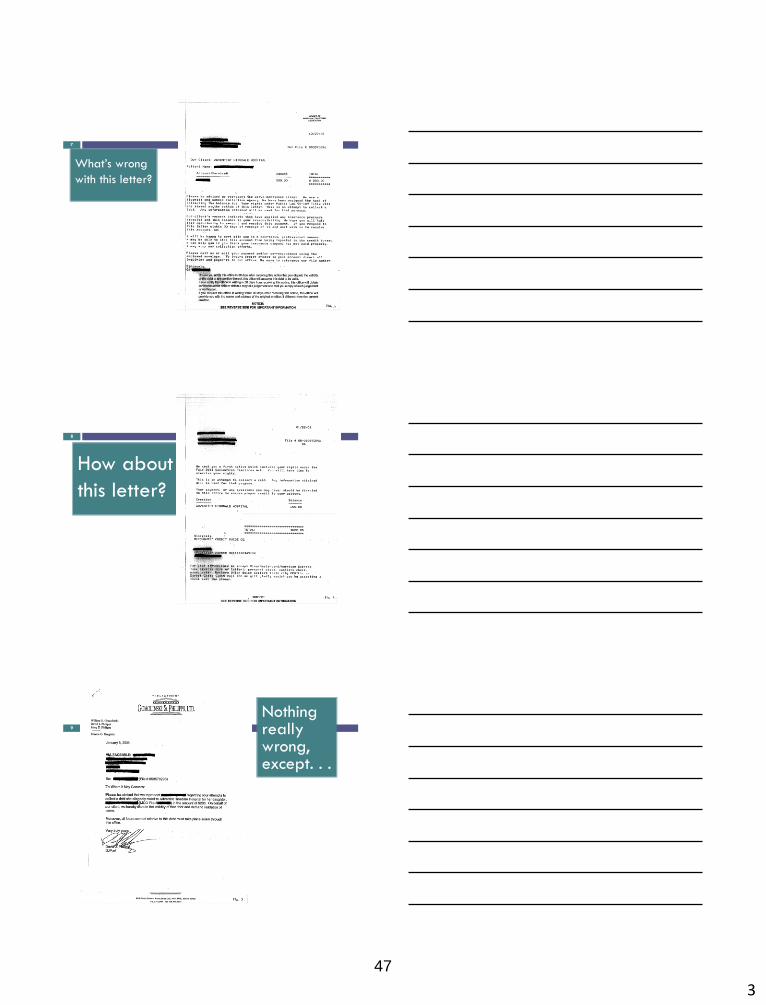

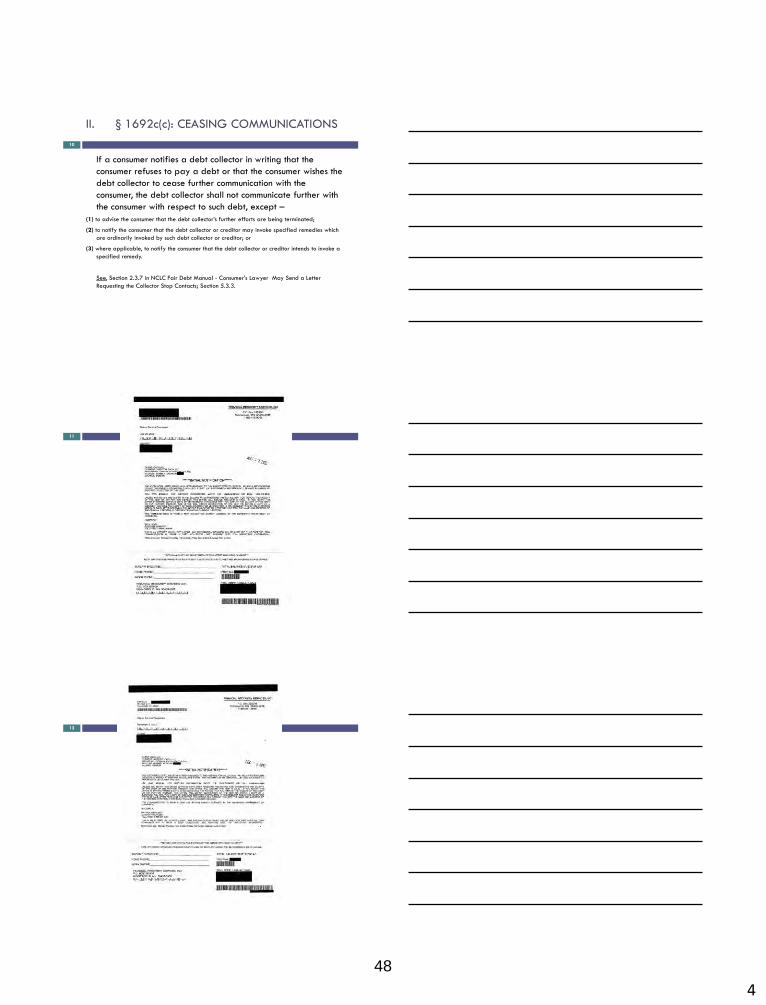

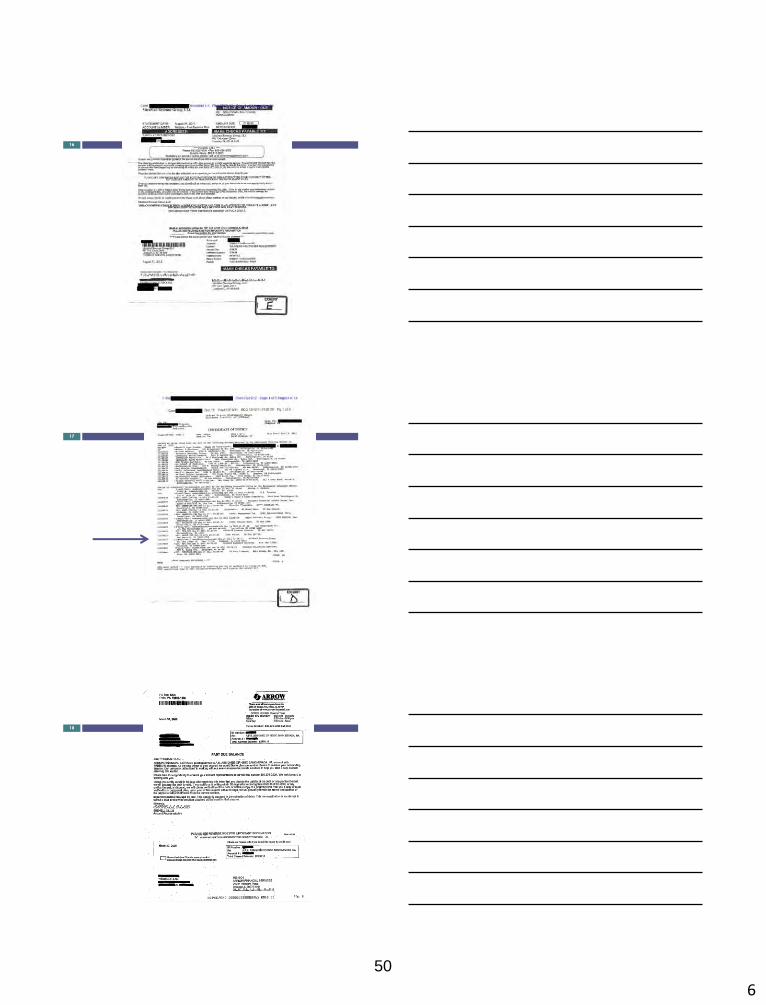

(c) Ceasing communication

If a consumer notifies a debt collector in writing that the consumer

refuses to pay a debt or that the consumer wishes the debt collector

to cease further communication with the consumer, the debt col-

lector shall not communicate further with the consumer with

respect to such debt, except—

(1) to advise the consumer that the debt collector’s further

efforts are being terminated;

(2) to notify the consumer that the debt collector or creditor may

invoke specified remedies which are ordinarily invoked by such

debt collector or creditor; or

(3) where applicable, to notify the consumer that the debt

collector or creditor intends to invoke a specified remedy.

If such notice from the consumer is made by mail, notification

shall be complete upon receipt.

(d) ‘‘Consumer’’ defined

For the purpose of this section, the term ‘‘consumer’’ includes the

consumer’s spouse, parent (if the consumer is a minor), guardian,

executor, or administrator.

15 U.S.C. § 1692d. Harassment or abuse [FDCPA

§ 806]

A debt collector may not engage in any conduct the natural

consequence of which is to harass, oppress, or abuse any person in

connection with the collection of a debt. Without limiting the

general application of the foregoing, the following conduct is a

violation of this section:

(1) The use or threat of use of violence or other criminal means

to harm the physical person, reputation, or property of any

person.

(2) The use of obscene or profane language or language the

natural consequence of which is to abuse the hearer or reader.

(3) The publication of a list of consumers who allegedly refuse

to pay debts, except to a consumer reporting agency or to

persons meeting the requirements of section 1681a(f) or 1681b(3)

of this title.

(4) The advertisement for sale of any debt to coerce payment of

the debt.

(5) Causing a telephone to ring or engaging any person in

telephone conversation repeatedly or continuously with intent to

annoy, abuse, or harass any person at the called number.

(6) Except as provided in section 1692b of this title, the

placement of telephone calls without meaningful disclosure of

the caller’s identity.

15 U.S.C. § 1692e. False or misleading

representations [FDCPA § 807]

A debt collector may not use any false, deceptive, or misleading

representation or means in connection with the collection of any

debt. Without limiting the general application of the foregoing, the

following conduct is a violation of this section:

(1) The false representation or implication that the debt collector

is vouched for, bonded by, or affiliated with the United States or

any State, including the use of any badge, uniform, or facsimile

thereof.

(2) The false representation of—

(A) the character, amount, or legal status of any debt; or

(B) any services rendered or compensation which may be

lawfully received by any debt collector for the collection of a

debt.

(3) The false representation or implication that any individual is

an attorney or that any communication is from an attorney.

Text of the Fair Debt Collection Practices Act Appx. A.2

71935

(4) The representation or implication that nonpayment of any

debt will result in the arrest or imprisonment of any person or

the seizure, garnishment, attachment, or sale of any property or

wages of any person unless such action is lawful and the debt

collector or creditor intends to take such action.

(5) The threat to take any action that cannot legally be taken or

that is not intended to be taken.

(6) The false representation or implication that a sale, referral,

or other transfer of any interest in a debt shall cause the

consumer to—

(A) lose any claim or defense to payment of the debt; or

(B) become subject to any practice prohibited by this sub-

chapter.

(7) The false representation or implication that the consumer

committed any crime or other conduct in order to disgrace the

consumer.

(8) Communicating or threatening to communicate to any per-

son credit information which is known or which should be

known to be false, including the failure to communicate that a

disputed debt is disputed.

(9) The use or distribution of any written communication which

simulates or is falsely represented to be a document authorized,

issued, or approved by any court, official, or agency of the

United States or any State, or which creates a false impression

as to its source, authorization, or approval.

(10) The use of any false representation or deceptive means to

collect or attempt to collect any debt or to obtain information

concerning a consumer.

(11) The failure to disclose in the initial written communication

with the consumer and, in addition, if the initial communication

with the consumer is oral, in that initial oral communication,

that the debt collector is attempting to collect a debt and that any

information obtained will be used for that purpose, and the

failure to disclose in subsequent communications that the com-

munication is from a debt collector, except that this paragraph

shall not apply to a formal pleading made in connection with a

legal action.3

(12) The false representation or implication that accounts have

been turned over to innocent purchasers for value.

(13) The false representation or implication that documents are

legal process.

(14) The use of any business, company, or organization name

other than the true name of the debt collector’s business, com-

pany, or organization.

(15) The false representation or implication that documents are

not legal process forms or do not require action by the con-

sumer.

(16) The false representation or implication that a debt collector

operates or is employed by a consumer reporting agency as

defined by section 1681a(f) of this title.

15 U.S.C. § 1692f. Unfair practices [FDCPA § 808]

A debt collector may not use unfair or unconscionable means to

collect or attempt to collect any debt. Without limiting the general

application of the foregoing, the following conduct is a violation of

this section:

(1) The collection of any amount (including any interest, fee,

charge, or expense incidental to the principal obligation) unless

such amount is expressly authorized by the agreement creating

the debt or permitted by law.

(2) The acceptance by a debt collector from any person of a

check or other payment instrument postdated by more than five

days unless such person is notified in writing of the debt

collector’s intent to deposit such check or instrument not more

than ten nor less than three business days prior to such deposit.

(3) The solicitation by a debt collector of any postdated check

or other postdated payment instrument for the purpose of threat-

ening or instituting criminal prosecution.

(4) Depositing or threatening to deposit any postdated check or

other postdated payment instrument prior to the date on such

check or instrument.