Faculty of Management and Social Sciences Abasyn ...

305

An Empirical Investigation into the Mediating Role of Internal Service Quality on the Linkage between Internal Organizational Factors and Organizational Performance By Khawaja Fawad Latif Registration No. AUP-11FL-Ph.D (MGT)-3124 Research Thesis Submitted to the Department of Management Sciences, Abasyn University, Peshawar in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy of the Abasyn University, Pakistan Faculty of Management and Social Sciences Abasyn University Peshawar Campus, Ring Road (Charsadda Link), Peshawar, Khyber Pakhtunkhwa 2015

Transcript of Faculty of Management and Social Sciences Abasyn ...

An Empirical Investigation into the Mediating Role of Internal Service Quality on the

Linkage between Internal Organizational Factors and Organizational Performance

By

Khawaja Fawad Latif

Registration No. AUP-11FL-Ph.D (MGT)-3124

Research Thesis Submitted to the Department of Management Sciences, Abasyn

University, Peshawar in Partial Fulfillment of the Requirements for the Degree of

Doctor of Philosophy of the Abasyn University, Pakistan

Faculty of Management and Social Sciences

Abasyn University Peshawar Campus, Ring Road (Charsadda Link), Peshawar,

Khyber Pakhtunkhwa 2015

ii

Certificate of Approval

I certify that I have read “An Empirical Investigation into the Mediating Role of Internal

Service Quality on the Linkage between Internal Organizational Factors and Organizational

Performance” by Khawaja Fawad Latif, AUP-11FL-Ph.D (MGT)-3124 and that in my opinion

this work meets the criteria for approving a thesis submitted in partial fulfillment of the

requirements for the degree of Ph.D. in Management Sciences at Abasyn University,

Peshawar.

Supervisor External Examiner (i)

______________________ ___________________________

Name: Dr. Qadar Bakhsh Baloch Name: Dr. Rashid Rehman

Date: ______________________ Date: ______________________

External Examiner (ii)

___________________________

Name: Dr. Raza Ullah

Date: ______________________

Internal Examiner

___________________________

Name: Dr. Shahid Jan Kakakhel

Date: ______________________

Head of Department

____________________________

Name: Prof. Dr. Aurangzeb

Date: ______________________

iii

Dedication

I dedicate this work to the most important pillars of my life, first and foremost, my

parents who sacrificed their comfort for my education; to my brothers; and to my beloved

wife and son for bearing with my lack of attention during the time I was writing the thesis.

iv

Acknowledgements

I confront scarcity of words to thank the Al-Mighty for granting me the virtue of

knowledge and making me a capable person to utilize the skills i acquired. Afterwards there

are certain other individuals who have helped in pursuing this literary journey. I would like to

extend my appreciation and thanks to my supervisor, Dr. Qadar Bakhsh Baloch for his

constant encouragement, counselling and support. I would like to extend my gratitude to my

teacher, Dr. Shahid Jan Kakakhel for his support and guidance. A special thanks is also due

to the Chancellor Abasyn University, Mr. Muhammad Imran Ullah, and Vice Chancellor,

Prof. Dr. Jamil Ahmad for their constant urge and drive to complete my thesis in time. I

render my earnest gratitude to Dean of Research Prof. Dr. Muhammad Iqbal for his unlimited

support and guidance. A special thanks to my work colleagues, Mr. Shahid Rashid, Mr. Irfan

Ullah, and Mr. Naveed Shinwari for sharing my work load. A note of thanks is also due to

Mr. Aziz Ahmad and Mr. Adeel Wahab Siddiqui for their support.

I would like to thank Mr. Amjad Ali, my teacher, former colleague, and my mentor

for his support and guidance at the start of my academic career. I would also like to extend

my regards to Mr. Sabur Sethi, President, City University of Science and Information

Technology for putting forth his trust in my competencies and providing me with an

opportunity to work at City University after my graduation.

I would like to express my heartfelt thanks to my dearest friend Abdul Wahab for his

constant and sincere prayers and support. Last but not the least a special acknowledgment to

my dear friend, colleague and fellow Ph.D. Scholar, Mr. Muhammad Usman Haider for his

conviction in my abilities and for being an indispensable helping hand at Abasyn University.

v

Table of Contents

Certificate of Approval .............................................................................................................. ii

Dedication ................................................................................................................................ iii

Acknowledgements ................................................................................................................... iv

Table of Contents ....................................................................................................................... v

List of Tables ............................................................................................................................ ix

List of Figures .......................................................................................................................... xii

Abstract ................................................................................................................................... xiv

Chapter 1 Introduction............................................................................................................ 1

1.1. Background ........................................................................................................................... 1

1.2. Statement of Problem ........................................................................................................... 7

1.3. Objectives of the Study ......................................................................................................... 7

1.4. Research Questions ............................................................................................................... 8

1.5. Summary of Theoretical Framework and Research Hypotheses ..................................... 9 1.5.1. Organizational Learning, ISQ and Organizational Performance .................................................. 9 1.5.2. Organizational Collaborative Culture, ISQ and Organizational Performance ............................ 10 1.5.3. Organizational Commitment, ISQ and Organizational Performance ......................................... 10 1.5.4. Perceived Organizational Support, ISQ and Organizational Performance ................................. 11 1.5.5. Role Stress, ISQ and Organizational Performance ..................................................................... 11 1.5.6. Internal Marketing, ISQ and Organizational Performance ......................................................... 11

1.6. Research Scope .................................................................................................................... 12 1.6.1. Conceptual scope ........................................................................................................................ 12 1.6.2. Choice of Data Context .............................................................................................................. 12 1.6.3. Population and Sample. .............................................................................................................. 13

1.7. Significance of the Study .................................................................................................... 13 1.7.1. Academic Significance ............................................................................................................... 13 1.7.2. Organizational Significance ....................................................................................................... 14 1.7.3. Managerial Significance ............................................................................................................. 14 1.7.4. Economic Significance ............................................................................................................... 15 1.7.5. Social Significance ..................................................................................................................... 15

1.8. The Research Contributions .............................................................................................. 15

1.9. Research Plan ...................................................................................................................... 16 1.9.1. Phase 1: Literature Review ......................................................................................................... 17 1.9.2. Phase 2: Research Methodology................................................................................................. 17 1.9.3. Phase 3: Data Analysis and Interpretation .................................................................................. 18

1.10. Organization of the Study .............................................................................................. 18

Chapter 2 Literature Review ................................................................................................ 20

2.1. Introduction ......................................................................................................................... 20

vi

2.2. The Concept of Quality....................................................................................................... 20

2.3. Internal Service Quality (ISQ) ........................................................................................... 24 2.3.1. Barriers to Internal Service Quality. ........................................................................................... 29 2.3.2. Fostering Internal Service Quality .............................................................................................. 32 2.3.3. Measuring ISQ ........................................................................................................................... 35 2.3.4. Banks and Internal Service Quality ............................................................................................ 40

2.4. Internal Organizational Factors ........................................................................................ 41 2.4.1. Organizational Learning ............................................................................................................. 52 2.4.2. Organizational Culture ............................................................................................................... 58 2.4.3. Organizational Commitment ...................................................................................................... 68 2.4.4. Perceived Organizational Support (POS) ................................................................................... 75 2.4.5. Role Stress .................................................................................................................................. 79 2.4.6. Internal Marketing ...................................................................................................................... 83

2.5. Organizational Performance .............................................................................................. 90 2.5.1. Earnings per Share ...................................................................................................................... 92 2.5.2. Return on Equity ........................................................................................................................ 92 2.5.3. Return on Assets ......................................................................................................................... 93

2.6. Service Quality and Organizational Performance ........................................................... 93

2.7. Mediating Role of Internal Service Quality ...................................................................... 95

2.8. Summary of Internal Organizational Factors and their Sources ................................... 97

Chapter 3 Conceptual Framework and Hypotheses........................................................... 99

3.1. Introduction ......................................................................................................................... 99

3.2. Conceptual Framework ...................................................................................................... 99

3.3. Research Hypotheses ........................................................................................................ 101 3.3.1. Organizational Learning, ISQ, and Organizational Performance ............................................. 102 3.3.2. Organizational Collaborative Culture, ISQ, and Organizational Performance ......................... 103 3.3.3. Organizational Commitment, ISQ, and Organizational Performance ...................................... 104 3.3.4. Perceived Organizational Support, ISQ, and Organizational Performance .............................. 105 3.3.5. Role Stress, ISQ, and Organizational Performance .................................................................. 106 3.3.6. Internal Marketing, ISQ, and Organizational Performance ...................................................... 107

3.4. Summary ............................................................................................................................ 108

Chapter 4 Research Methodology ...................................................................................... 109

4.1. Research Philosophy ......................................................................................................... 109

4.2. Nature of Research ........................................................................................................... 111

4.3. Research Design ................................................................................................................ 111

4.4. Population .......................................................................................................................... 112

4.5. Sample ................................................................................................................................ 113

4.6. Measurement ..................................................................................................................... 114 4.6.1. Internal Service Quality ............................................................................................................ 115 4.6.2. Organizational Learning ........................................................................................................... 117 4.6.3. Organizational Collaborative Culture ....................................................................................... 117 4.6.4. Organizational Commitment .................................................................................................... 118

vii

4.6.5. Perceived Organizational Support ............................................................................................ 119 4.6.6. Role Stress ................................................................................................................................ 119 4.6.7. Internal Marketing .................................................................................................................... 120 4.6.8. Subjective Organizational Performance ................................................................................... 121 4.6.9. Objective Organizational Performance .................................................................................... 122

4.7. Pre-testing .......................................................................................................................... 122 4.7.1. Stage-1 - Content validity ......................................................................................................... 122 4.7.2. Stage Two: Readability ............................................................................................................ 123 4.7.3. Stage Three: Pilot Study ........................................................................................................... 124 4.7.4. Stage Four: Mistake Elimination .............................................................................................. 125

4.8. Data Collection .................................................................................................................. 126

4.9. Data Analysis ..................................................................................................................... 127 4.9.1. Descriptive Analysis ................................................................................................................. 127 4.9.2. Factor Analysis ......................................................................................................................... 127 4.9.3. Validity of Research ................................................................................................................. 128 4.9.4. Reliability Assessment ............................................................................................................. 129 4.9.5. Correlation Analysis ................................................................................................................. 130 4.9.6. Structural Equation Modeling .................................................................................................. 131 4.9.7. Mediation Analysis ................................................................................................................... 133

4.10. Summary of Research Methodology ........................................................................... 135

Chapter 5 Data Analysis and Results ................................................................................. 136

5.1. Descriptive Statistics ......................................................................................................... 136 5.1.1. Data Screening and Cleaning ................................................................................................... 136 5.1.2. Demographic Profile of Respondents ....................................................................................... 136 5.1.3. Descriptive Statistics of Constructs (Means, Skewness and Kurtosis) ..................................... 144

5.2. Factor Analysis .................................................................................................................. 164 5.2.1. Assumptions ............................................................................................................................. 164 5.2.2. Component Matrix ................................................................................................................... 167 5.2.3. Summary of Factor Analysis .................................................................................................... 173

5.3. Reliability ........................................................................................................................... 174

5.4. Construct Validity ............................................................................................................. 176 5.4.1. Convergent Validity ................................................................................................................. 176 5.4.2. Discriminant Validity ............................................................................................................... 177

5.5. Structural Equation Modeling ......................................................................................... 178 5.5.1. Evaluations of Measurement Models ....................................................................................... 178 5.5.2. Hypotheses Testing .................................................................................................................. 192

5.6. ISQ and Employee Demographics ................................................................................... 220 5.6.1. ISQ and Gender ........................................................................................................................ 220 5.6.2. ISQ and Age ............................................................................................................................. 220 5.6.3. ISQ and Rank ........................................................................................................................... 221 5.6.4. ISQ and Employment Type ...................................................................................................... 222 5.6.5. ISQ and Banking System.......................................................................................................... 223 5.6.6. ISQ and Years of Education ..................................................................................................... 224 5.6.7. ISQ and Job Tenure .................................................................................................................. 224 5.6.8. ISQ and Type of Bank .............................................................................................................. 225

5.7. Summary of the Research Results ................................................................................... 225

viii

Chapter 6 Discussion and Conclusions .............................................................................. 230

6.1. What factors affect organizational performance? ......................................................... 230

6.2. What factors affect ISQ? .................................................................................................. 235

6.3. What is the impact of ISQ on organizational performance? ........................................ 238

6.4. Does ISQ act as mediator between internal organizational factors & organizational

performance?................................................................................................................................. 239

6.5. Discussion on Measurement and Structural Models ..................................................... 241

6.6. Conclusions ........................................................................................................................ 242

6.7. Implications of the Study .................................................................................................. 245

6.8. Limitations and Delimitations.......................................................................................... 248

6.9. Directions for Future Research ....................................................................................... 248

6.10. Recommendations ......................................................................................................... 249

References ............................................................................................................................. 252

ix

List of Tables

Table 2.1 Description of Concept of Quality ....................................................................................... 21

Table 2.2 Major Barriers to Internal Service Quality ......................................................................... 31

Table 2.3 Initiatives to foster ISQ ........................................................................................................ 35

Table 2.4 Measuring Internal Service Quality ..................................................................................... 39

Table 2.5 Theoretical and Empirical foundation for identification of organizational factors ............ 48

Table 2.6 Summary of Internal Organizational Factors and their Sources ......................................... 98

Table 4.1 Characteristics of Positivism ............................................................................................. 110

Table 4.2 Sample Frame .................................................................................................................... 113

Table 4.3 Internal Service Quality Scale ........................................................................................... 116

Table 4.4 Organizational Learning scale items ................................................................................. 117

Table 4.5 Organizational collaborative culture scale items .............................................................. 118

Table 4.6 Organizational Commitment Scale .................................................................................... 118

Table 4.7 Perceived Organizational Support Scale ........................................................................... 119

Table 4.8 Role Stress Scale ................................................................................................................ 120

Table 4.9 Internal Marketing Scale ................................................................................................... 121

Table 4.10 Subjective organizational performance scale items ......................................................... 122

Table 4.11 Items removed at content validity stage ........................................................................... 123

Table 4.12 Mean Comparison for Constructs .................................................................................... 124

Table 4.13 Items removed during pilot testing stage ......................................................................... 125

Table 4.14 Questionnaires Response Details .................................................................................... 126

Table 4.15 Summary of Recommended fit Indices ............................................................................. 133

Table 5.1 Age Distribution of Respondents ....................................................................................... 137

Table 5.2 Gender distribution of respondents ................................................................................... 138

Table 5.3 Respondent’s years of education ....................................................................................... 139

Table 5.4 Nature of Employment ....................................................................................................... 140

Table 5.5 Rank distribution of respondents ....................................................................................... 141

Table 5.6 Descriptive statistics for Tenure ........................................................................................ 142

Table 5.7 Respondent’s distribution by banking system .................................................................... 142

Table 5.8 Respondent’s distribution by banking system .................................................................... 143

Table 5.9 Descriptive Statistics for organizational learning ............................................................. 145

Table 5.10 Normality distribution testing of organizational learning ............................................... 146

Table 5.11 Descriptive Statistics of organizational commitment ....................................................... 147

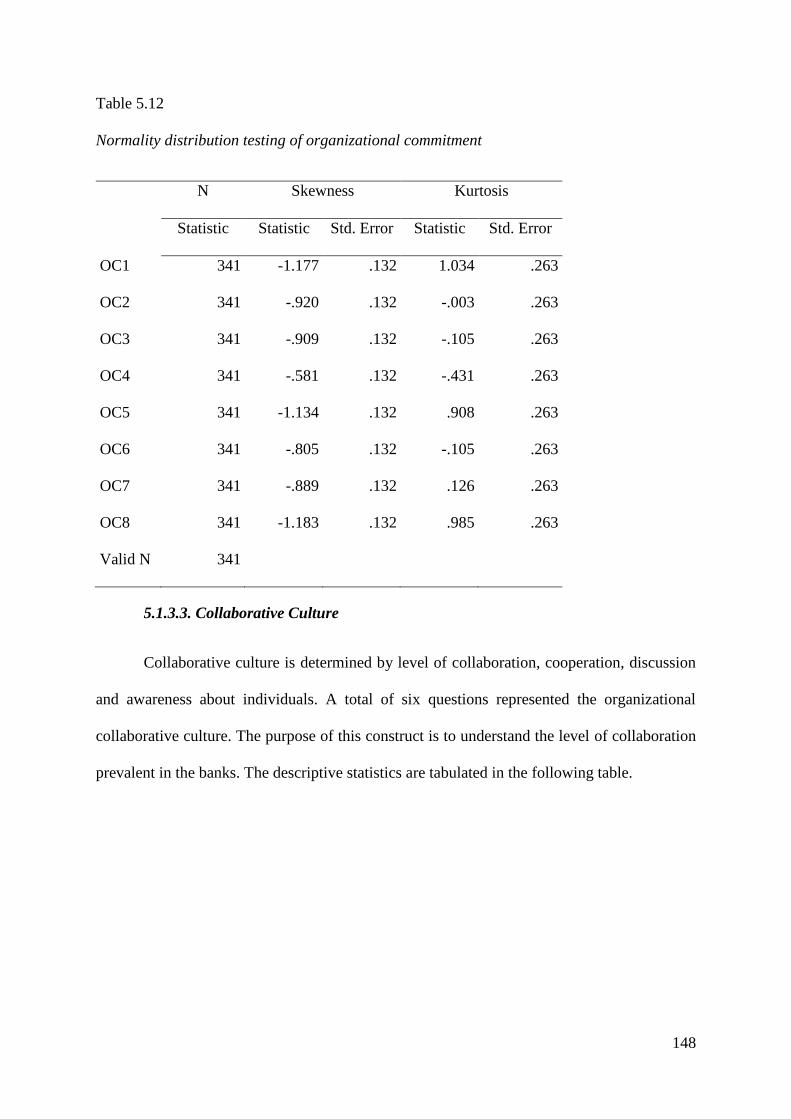

Table 5.12 Normality distribution testing of organizational commitment ......................................... 148

Table 5.13 Descriptive Statistics of collaborative culture ................................................................. 149

Table 5.14 Normality distribution testing of collaborative culture ................................................... 150

Table 5.15 Descriptive statistics for perceived organizational support ............................................ 151

Table 5.16 Normality distribution testing of perceived organizational support ................................ 152

Table 5.17 Descriptive statistics for role ambiguity .......................................................................... 153

Table 5.18 Normality distribution testing of role ambiguity .............................................................. 153

Table 5.19 Descriptive statistics for role conflict .............................................................................. 154

Table 5.20 Normality distribution testing of role conflict.................................................................. 155

Table 5.21 Descriptive statistics for internal marketing .................................................................... 155

Table 5.22 Normality testing of internal marketing ........................................................................... 156

Table 5.23 Descriptive statistics for Reliability ................................................................................. 157

Table 5.24 Normality distribution testing of reliability ..................................................................... 158

x

Table 5.25 Descriptive statistics for assurance. ................................................................................ 159

Table 5.26 Normality testing for assurance ....................................................................................... 159

Table 5.27 Descriptive statistics for empathy .................................................................................... 160

Table 5.28 Normality testing of empathy ........................................................................................... 161

Table 5.29 Descriptive statistics for responsiveness.......................................................................... 161

Table 5.30 Normality testing of responsiveness ................................................................................. 162

Table 5.31 Descriptive statistics for organizational performance ..................................................... 163

Table 5.32 Normality testing of organizational performance ............................................................ 163

Table 5.33 Summary of inter-variable correlation ............................................................................ 165

Table 5.34 Assumptions’ statistics for factor analysis ....................................................................... 167

Table 5.35 Component Matrix for Organizational Learning............................................................. 168

Table 5.36 Component Matrix for organizational commitment ......................................................... 169

Table 5.37 Component Matrix for Organizational collaborative culture .......................................... 169

Table 5.38 Component Matrix for perceived organizational support ............................................... 170

Table 5.39 Component Matrix for role stress .................................................................................... 170

Table 5.40 Component matrix for internal marketing ....................................................................... 171

Table 5.41 Component matrix for internal service quality ................................................................ 172

Table 5.42 Component matrix for organizational performance ........................................................ 173

Table 5.43 Summary of factor analysis .............................................................................................. 174

Table 5.44 Reliability analysis of the constructs ............................................................................... 175

Table 5.45 AVE for constructs ........................................................................................................... 177

Table 5.46 Comparison of Square root of AVE and Inter-Construct Correlations ........................... 178

Table 5.47 Summary of initial and attained findings: Organizational Learning ............................... 179

Table 5.48 Summary of initial and attained findings: Organizational Collaborative Culture .......... 181

Table 5.49 Summary of initial and attained findings: Organizational Commitment ......................... 182

Table 5.50 Summary of initial and attained findings: Organizational Commitment ......................... 184

Table 5.51 Summary of initial and attained findings: Role Stress ..................................................... 185

Table 5.52 Summary of initial and attained findings: Internal Marketing ........................................ 186

Table 5.53 Summary of initial and attained findings: Internal Service Quality ................................ 188

Table 5.54 Summary of initial and attained findings: Organizational Performance ........................ 190

Table 5.55 Summary of the measurement models .............................................................................. 191

Table 5.56 Summary of initial and attained findings: Structural Model A ........................................ 193

Table 5.57 Summary of measurements: Internal Organizational Factors and ISQ .......................... 195

Table 5.58 Summary of initial and attained findings: Structural Model B ........................................ 196

Table 5.59 Summary of measurements: Internal Organizational Factors & Organizational

Performance ........................................................................................................................................ 198

Table 5.60 Summary of initial and attained findings: Structural Model C1-2-3 ............................... 199

Table 5.61 Summary of measurements: Internal Organizational Factors & Organizational

Performance ........................................................................................................................................ 203

Table 5.62 Summary of initial and attained findings: Structural Model D ....................................... 204

Table 5.63 Summary of measurements: ISQ and Organizational Performance (OP) ....................... 205

Table 5.64 Summary of initial and attained findings: Structural Model E1-2-3 ............................... 205

Table 5.65 Summary of measurements: ISQ and Organizational Performance ................................ 207

Table 5.66 Mediation analysis ISQ between OL and OP .................................................................. 209

Table 5.67 Mediation analysis ISQ between CC and OP .................................................................. 210

Table 5.68 Mediation analysis ISQ between OC and OP .................................................................. 211

Table 5.69 Mediation analysis ISQ between POS and OP ................................................................ 212

Table 5.70 Mediation analysis ISQ between RS and OP ................................................................... 213

xi

Table 5.71 Mediation analysis ISQ between IM and OP ................................................................... 214

Table 5.72 Mediation analysis ISQ between OL and ROE ................................................................ 215

Table 5.73 Mediation analysis ISQ between CC and ROE ................................................................ 216

Table 5.74 Mediation analysis ISQ between IM and ROE ................................................................ 217

Table 5.75 Mediation analysis ISQ between OC and ROA ............................................................... 218

Table 5.76 Mediation analysis ISQ between OC and ROE ............................................................... 219

Table 5.77 Compare Means, ISQ with respect to Gender ................................................................. 220

Table 5.78 Compare Means, ISQ with respect to Age ....................................................................... 221

Table 5.79 ANOVA Results, ISQ and Job Rank ................................................................................. 222

Table 5.80 Multiple Comparison across Job Ranks .......................................................................... 222

Table 5.81 Compare Means, ISQ with respect to Employment Type ................................................. 223

Table 5.82 Compare Means, ISQ with respect to Banking System .................................................... 224

Table 5.83 ANOVA results, ISQ across Years of Education .............................................................. 224

Table 5.84 ANOVA results, ISQ across different job tenures ............................................................ 225

Table 5.85 Compare Means, ISQ with respect to Type of Bank ........................................................ 225

Table 5.86 Summary of Hypotheses Results ...................................................................................... 227

xii

List of Figures

Figure 1.1. Theoretical Framework for the Study .................................................................................. 9

Figure 1.2. Research Phase 1 ................................................................................................................ 17

Figure 1.3. Research Phase 2 ................................................................................................................ 18

Figure 1.4. Research Phase 3 ................................................................................................................ 18

Figure 3.1. Conceptual Framework .................................................................................................... 101

Figure 4.1. Research Design ............................................................................................................... 112

Figure 4.2. Diagrammatic Representation of Mediation Analysis ..................................................... 134

Figure 5.1. Age wise distribution of respondents ............................................................................... 137

Figure 5.2. Gender wise distribution of respondents .......................................................................... 138

Figure 5.3. Distribution of respondents on years of education ........................................................... 139

Figure 5.4. Respondent’s nature of employment ................................................................................ 140

Figure 5.5. Distribution by job rank ................................................................................................... 141

Figure 5.6. Distribution by Banking System (Source: Field Data) .................................................... 142

Figure 5.7. Distribution by Bank Type ............................................................................................... 143

Figure 5.8. Measurement model for organizational learning ............................................................. 180

Figure 5.9. Measurement model for collaborative culture ................................................................. 181

Figure 5.10. Measurement model for organizational commitment .................................................... 183

Figure 5.11. Measurement model for perceived organizational support ............................................ 184

Figure 5.12. Measurement model for role stress ................................................................................ 186

Figure 5.13. Measurement model for internal marketing ................................................................... 187

Figure 5.14. Measurement model for ISQ .......................................................................................... 189

Figure 5.15. Measurement model for organizational performance .................................................... 191

Figure 5.16. Structural Model A: Internal organizational factors and ISQ ........................................ 194

Figure 5.17. Structural Model B: Internal organizational factors and organizational performance ... 197

Figure 5.18. Structural Model C1: Internal organizational factors and organizational performance . 200

Figure 5.19. Structural Model C2: Internal organizational factors and organizational performance . 201

Figure 5.20. Structural Model C3: Internal organizational factors and organizational performance . 202

Figure 5.21. Structural Model D: ISQ and organizational performance ............................................ 204

Figure 5.22. Structural Model E1: ISQ and Objective Organizational Performance ......................... 206

Figure 5.23. Structural Model E2: ISQ and Objective Organizational Performance ......................... 206

Figure 5.24. Structural Model E3: ISQ and Objective Organizational Performance ......................... 207

Figure 5.25. Mediation: ISQ, OL and OP ........................................................................................... 209

Figure 5.26. Mediation: ISQ, CC and OP ........................................................................................... 210

Figure 5.27. Mediation: ISQ, OC and OP .......................................................................................... 211

Figure 5.28. Mediation: ISQ, POS and OP ......................................................................................... 212

Figure 5.29. Mediation: ISQ, RS and OP ........................................................................................... 213

Figure 5.30. Mediation: ISQ, IM and OP ........................................................................................... 214

Figure 5.31. Mediation: ISQ, OL and ROE ........................................................................................ 215

Figure 5.32. Mediation: ISQ, CC and ROE ........................................................................................ 216

Figure 5.33. Mediation: ISQ, IM and ROE ......................................................................................... 217

Figure 5.34. Mediation: ISQ, OC and ROA ....................................................................................... 218

Figure 5.35. Mediation: ISQ, OC and ROE ....................................................................................... 219

xiii

Abbreviations

Abbreviation Description

ISQ Internal Service Quality

OL Organizational Learning

OC Organizational Commitment

CC Collaborative Culture

POS Perceived Organizational Support

IM Internal Marketing

RS Role Stress

POP Perceived Organizational Performance

ROE Return on Equity

ROA Return on Average Assets

EPS Earnings Per Share

SEM Structural Equation Modelling

CFA Confirmatory Factor Analysis

EFA Exploratory Factor Analysis

AVE Average Variance Extracted

xiv

Abstract

The study seeks to evaluate the mediating role of ISQ on the relationship between

different internal organizational factors and organization performance, furthermore the study

also ascertains the influence of internal organizational factors on ISQ and organizational

performance. Additionally the study also evaluates the impact of ISQ on organizational

performance. The internal organizational factors include; organizational learning,

collaborative culture, organizational commitment, perceived organizational support, role

stress & internal marketing. The study is a descriptive cum correlational, focusing on the

performance and ISQ of different banks operating in Peshawar. The sample included 80 bank

branches, the data was collected from the employees working in different bank branches

located within the city of Peshawar. Banks selected as part of the population required to have

more than five branches. Stratified random sampling technique was utilized to collect the data

from different banks operating in the city of Peshawar. A total of 564 questionnaires were

distributed in 80 different branches of medium and large sized banks. In the present study 404

questionnaires were returned, constituting the response rate of 71.63%. A total of 63

questionnaires were rejected. The total number of questionnaires usable for the study was

341.

Evaluating the impact of different internal organizational factors on ISQ revealed that

three out of six internal organizational factors namely; organizational commitment, role

stress, and internal marketing have a significant influence on the internal service quality.

While three factors namely; organizational learning, collaborative culture and perceived

organizational support did not have a significant influence on the internal service quality. The

results revealed that four out of six internal organizational factors namely; organizational

learning, organizational commitment, role stress, and internal marketing have a significant

influence on the perceived organizational performance. While two factors namely;

xv

collaborative culture and perceived organizational support did not have a significant

influence on the perceived organizational performance. Mediation analysis proved partial

mediation between all internal organizational factors and perceived organizational

performance. The objective measure for bank performance used in the present study included

Return on Equity (ROE), Earnings per Share (EPS) and Return on Assets (ROA). Mediation

analysis between different internal organizational factors and financial organizational

performance showed that ISQ fully mediates the path between organizational learning and

Return on Equity (ROE), collaborative culture and ROE, and internal marketing and ROE.

The study ascertains that ISQ has a significant influence in predicting both subjective and

objective organizational performance measures. The present research strengthens the

theoretical assertions that unless ISQ is not strengthened, the organization will not be able to

attain external service quality, growth and profit. The mediated effect of ISQ is important to

top management, implying their responsibility for investing to create an environment that

nurtures trust, understanding, commitment, provision of timely service, and positivity in

attitude and behavior. Management which expects to reap benefits of service quality must

understand the need of better ISQ and should invest in the intangible factors that have been

proven to affect the tangible profits. The research study affirms that it is not only external

service quality that adds to the profitability of the organizations. Therefore, it is found

imperative for the banks to foster ISQ in their workplace environment.

Keywords: Organizational Learning, Organizational Commitment, Organizational Culture,

Perceived Organizational Support, Role Stress, Internal Marketing, Internal Service Quality,

Organizational Performance

1

Chapter 1

Introduction

1.1. Background

Organizations operate in an extremely competitive, vibrant, challenging, and dynamic

business environment. In response to the pressures of running business in such an

environment, organizations seek ways to add value to the services offered and improve their

service quality. One way to achieve optimal level of service quality is through focus on the

human resources. The role of human resource in the attainment of desired profits is

increasingly catching the focus of the organizations. There is a move from concern for

production to concern for people. This shift is especially true for service industries. The

change in focus is dictated by the understanding that services are created, nurtured, and

delivered through people. Lack of attention towards human resources can seriously hamper

the value of service. This is because in customer contact businesses, quality of service

delivered is strongly linked with the quality of service providers. It is for this reason that the

need for quality improvement continues unabated both in the manufacturing and service

sector (Longenecker & Scazzero, 2000). The challenge to provide efficient and effective

service is dictated by the fact that today’s customers are more informed, knowledgeable, and

experienced about the variety of products and services being offered in the market. This

awareness about product quality, shape customers’ expectations about the product, and

compels the business world to meet the expectations and anticipations of the customers

(Prakash & Mohanty, 2012). Improvements in service quality are also necessitated by the fact

that Liberalisation has provided customers the opportunity to choose their service provider.

Thus, customers demand better quality or otherwise they have the chance to shift to another

supplier (Pina, Torres, & Bachiller, 2014).

2

Parasuraman (2002) stressed that scholarly literature attests to the benefits of

providing superior customer service. Emphasis is laid on the business to create meaningful,

memorable customer experiences (Prakash & Mohanty, 2012). This user satisfaction will

come from service quality (Hernon & Whitman, 2001; Wang & Shieh, 2006). Service quality

is an important tool that not only ensures survival but growth in the extremely competitive

business environment. Businesses requires user satisfaction for survival and growth.

Businesses make progress based on the level of relationship it has with the customers. The

key to better relationship is the quality of service customers receive that would make them

come back for the service. Service quality is thus a business imperative, especially for service

sector. The user satisfaction flows from the employees, and employees will not be able to

generate quality service unless or until the services exchanged between different employees

are worthy and valued. Hence, the service providers have placed more emphasis on the

significance of service quality as a way of attaining competitive advantage (Gustaffson, 2009;

Sureshchander, Rajendran, & Anatharaman, 2002; Vanniarajan & Subbash, 2011).

Longenecker and Scazzero (2000) further highlight the value of service quality by referring

to history when quality was referred to as competitive advantage. Today’s businesses run the

risk of being driven out if they fail to improve the quality, and they referred to quality as a

market segment mandate.

In general, quality is recognized as basic value capable of generating a competitive

advantage through product/service differentiation (Hamid Reza Ghasemian, Azad, &

Seyedaliakbar, 2014). The differentiation of service stimulates customer satisfaction, it can

pay rich dividends like customer retention, cost reduction and increased profits (Zeithaml,

Bitner, & Gremler, 2006). Moreover, businesses should note that service quality is an asset

that needs to be managed, after all, it is more complicated to do service well than to change

the price or to alter the inventory of goods available (Prakash & Mohanty, 2012). This is in

3

fact, due to the complex nature of the service, the people involved, and the nature of the

exchange between the service providers. Effective and efficient management of this asset

would enable businesses to stand out from their competitors (Gracia, Cifre, & Grau, 2010).

Service quality has been identified as one of the key features that ultimately leads to

organizational success; however a decline in service quality leads to deterioration in the level

of customer satisfaction (Frost & Kumar, 2000) which adversely affects organizational

performance. However, increased level of service quality has been found to produce greater

satisfaction amongst customers that could lead to patronage intentions and increased sales

(Prakash & Mohanty, 2012).

Service Quality takes two different forms i-e, external and internal. External service

quality relates to assessment based on what the customers’ value and what they are willing to

pay for (Dinitzen & Bohlbro, 2010). External service quality is strongly contingent to internal

service i-e, employees receiving high quality internal services would strive to provide higher

quality external service. Internal service quality (ISQ), on the other hand, points to services

provided by distinctive organizational units or the people working in different departments to

other departments or employees within the organization (Stauss, 1995). ISQ refers to an

organization's ability to attract, develop, motivate and retain quality employees (Mok, Sparks,

& Kadampully, 2001). Thus, in order to achieve optimal level of ISQ, organizations will have

to focus on its employees. This is imperative for most services, as the delivery of services

occurs through human interaction (Boshoff & Mels, 1995). While human factors are

significant in all quality enhancement initiatives, they are critical in service industries

(Longenecker & Scazzero, 2000). The level of internal customer (employee) service quality

has an essential impact on the service value provided to the external customer (Bouranta,

Chitiris, & Paravantis, 2009). This is because many of the employees working in an

organization might seldom or never have a direct interaction with the external customers,

4

however the performance and interaction between employees working in different

departments have a direct effect on the service quality perceived by the external customers.

This understanding has stimulated organizational focus on the development of better ISQ that

would aid in fostering external service which would in turn results in attaining healthier

organizational results. It is widely believed that traits related to service personnel have a key

part in determining customer contentment (Hays & Hill, 2001). It is important to study ISQ,

unless the concerns of ISQ are addressed business will not be able to increase the level of

external service quality, and attain growth and profitability (Cook, 2004). The need to study

ISQ is further highlighted by the fact that the quality of external service delivery is a

reflection of the quality of service that people in the organization provide to each other

(Cook, 2008).

Extensive research is available on service quality from the external customer

perspective, however, relatively few studies have concentrated on the factors that

significantly influence employees’ (Internal Customers) service quality. These researches

which has been carried out in the area of ISQ are in the fields’ of Healthcare (Gunawardane,

2009; Pantouvakis & Mpogiatzidis, 2013), Insurance (Boshoff & Mels, 1995), Food Industry

(Wildes, 2007; Wildes & Parks, 2005), Banks (Bellou & Andronikidis, 2008; Vanniarajan &

Subbash, 2011), University (Jun & Cai, 2010), hotels (Bai, Brewer, Sammons, & Swerdlow,

2006; Paraskevas, 2001), Pharmaceuticals (ELSamen & Alshurideh, 2012), and Airline (Frost

& Kumar, 2001).

Though, there are numerous research studies on external service quality, only limited

studies have focused on internal service quality especially in commercial banks. Hence, the

present study is operationalized among banks. The banking sector is a demand driven

industry and represents a vital section of the services industry in any country (Mishkin,

2001). The current rapidly changing environment is compelling the attention of banking

5

institutions towards service quality, and retail banks are striving towards increasing customer

satisfaction through improved service quality (Choudury, 2014). This is because growth in

the banking sector and the ever increasing competition among banks has clearly highlighted

the need for customer satisfaction and optimization of customer service for a surge in market

shares and profitability (Anderson et al., 1994). It is however important to note that for many

organizations, quality means meeting customers' requirements. However, customer may not

refer to people outside the organization only, Juran (1988) defined customers as persons who

are not only the organization's customers but also its employees. He included all persons in

customers who are affected by an organization’s processes and products. Organizations

understanding of how a person working within the organization is affected by the activities

within the organization can not only aid in designing strategies and practices that would offer

a more congenial business environment but also make employee reciprocate with level of

performance desired by the organization.

Existing research studies have identified the need to look at different factors and its

influence on service quality and organizational performance. Different researchers have

studied different factors that can impact on internal service quality, however, there are gaps in

the existing research that suggest directions for further research. Boshoff and Mels (1995)

suggest that future endeavors in the study of ISQ shall include variables other than

organizational commitment. Tsaur and Lin (2004) who studied HRM practices impact on

service quality recommended that future research should present other factors in the study to

help clarify the antecedents of service behavior. Furthermore, they also noted that the earlier

literature suggests that organizational issues could also be predictors of service behavior.

Vella, Gountas, and Walker (2009) stressed that in an organization, there are too many

factors that can impact on service quality, hence services research requires suitable focus and

a manageable count of constructs that appear to be more significant to explain service quality

6

from the employee’s viewpoint only. Similarly Slatten (2009) recommended that future

research on service quality could include relevant managerial practices other than reward and

support. Andrews, Boyne and Walker (2006) calls for the study of a wider set of measures

that may reveal a stronger link of ISQ with organizational performance. Similarly gaps in the

literature pertinent to organizational performance are also highlighted. Kim (2005) utilized

only four individual-level variables to predict organizational performance and proposed that

future research should look for additional factors that affect organizational performance.

Tseng (2010) suggests the inclusion of a different set of attitudes and behaviors and evaluate

how they impact organizational performance. Hence, based on the limitations of existing

research and future research directions that calls for the inclusion of additional factors that

may carry a significant impact on the ISQ and organizational performance form part of the

present study. The selection of factors is based on the literature pertinent to quality

management, service quality GAPS, and organizational performance. These factors include

Organizational Learning, Collaborative Organizational Culture, Organizational Commitment,

Perceived Organizational Support, Role Stress, and Internal Marketing. The present study

intends to focus on factors that shall be considered by the management to ensure better ISQ

that ultimately leads to improved service delivery to the customers. The factors are derived

from literature and are discussed in detail in chapter 2.

Quality of service and enhanced organizational performance can be warranted through

adoption of two different strategies. One is reactive while the other is proactive. Where

performance management techniques and rewards for better service or performance can be

termed as reactive approaches, since the employee is compensated afterwards and have a

short term influence. These measures may not guarantee optimal service or performance.

Organizational focus on proactive measures that bring about change in how people feel,

perceive, and behave can have a long term effect. Organizations need to focus on the

7

personality of their employees, and how well they interact and respond to each other. This is

possible only through paying attention to organizational initiatives, employee behaviors and

attitudes. Focusing on these factors will lead to changes in the values of the employee. It is

for this reason that the present study attempts to evaluate the influence of different

organizational initiatives and attitudes on both ISQ and organizational performance.

The present study not only brings together different organizational factors, and

evaluates its impact on ISQ but also evaluates the linkage of ISQ with organizational

performance. Further empirical investigation is needed on service quality and its relationship

with organizational performance, especially among different service organizations (Al-Enezi,

2012). The study further evaluates whether ISQ mediates between different internal

organizational factors and organizational performance or not. Since existing studies have

identified how ISQ influences or is influenced by other factors in different industries.

Research has shown the influence of different internal organizational factors on

organizational performance. A causal link could be established based on the existing

literature that shows the influence of different internal organizational factors on ISQ and their

direct impact on organizational performance.

1.2. Statement of Problem

The research reasons that organizational performance will improve on the basis of

ISQ rather than the influence of internal organizational factors alone. The present study seeks

to ascertain if ISQ mediates between internal organizational factors and organizational

performance or otherwise.

1.3. Objectives of the Study

The overarching goal of this research is to examine whether ISQ acts as a mediator

between different internal organizational factors and organizational performance or

8

otherwise. The scarcity of the research in this area highlights a knowledge gap. This study

aims to address this gap. The specific objectives of the study are as under

a. To evaluate factors (organizational learning, organizational collaborative culture,

organizational commitment, perceived organizational support, role stress, and internal

marketing) that significantly influence organizational performance.

b. To investigate factors (organizational learning, organizational collaborative culture,

organizational commitment, perceived organizational support, role stress, and internal

marketing) that significantly influence ISQ.

c. To evaluate the impact of ISQ on Organizational Performance

d. To investigate if ISQ acts as a mediator between internal organizational factors and

organizational performance.

1.4. Research Questions

In order to seek the solution of the research question/problem, the research focused to

find answers to the following questions.

a. What are the internal organizational factors (organizational learning, organizational

collaborative culture, organizational commitment, perceived organizational support,

role stress, and internal marketing) that affect organizational performance?

b. What are the internal organizational factors (organizational learning, organizational

collaborative culture, organizational commitment, perceived organizational support,

role stress, and internal marketing) that affect ISQ?

c. What is the impact of ISQ on organizational performance

d. Does ISQ act as a mediator between internal organizational factors and organizational

performance?

9

1.5. Summary of Theoretical Framework and Research Hypotheses

A number of diverse studies on different internal organizational factors, ISQ and

organizational performance have been studied to draw the theoretical framework for the

current study. The study not only evaluates the direct influence of different internal

organizational factors on ISQ but also on organizational performance. Furthermore, the study

also evaluates the mediating role of ISQ. Based on the extensive review of literature the

following framework of proposed to study the relationships.

Figure 1.1. Theoretical Framework for the Study

Based on the aforementioned framework, following set of hypotheses are proposed to test the

relationships

1.5.1. Organizational Learning, ISQ and Organizational Performance

H1a: There is a significant impact of Organizational Learning on ISQ

H1b: There is a significant impact of Organizational Learning on Perceived Organizational

Performance

H1c1-2-3: There is a significant impact of Organizational Learning on Objective

Organizational Performance (EPS, ROE, & ROA)

Organizational Performance Objective Performance

Subjective Performance

Internal

Service Quality

Internal Organizational Factors

Organizational Learning

Collaborative Culture

Internal Marketing

Organizational Commitment

Perceived Organizational Support

Role Stress

10

H1d: ISQ mediates between Organizational Learning and Perceived Organizational

Performance

H1e1-2-3: ISQ mediates between Organizational Learning and Objective Organizational

Performance (EPS, ROE, & ROA)

1.5.2. Organizational Collaborative Culture, ISQ and Organizational

Performance

H2a: There is a significant impact of Organizational Collaborative Culture on ISQ

H2b: There is a significant impact of organizational collaborative culture on Perceived

Organizational Performance

H2c1-2-3: There is a significant impact of organizational collaborative culture on objective

organizational performance (EPS, ROE, & ROA)

H2d: ISQ mediates between Organizational Culture and Perceived Organizational Performance

H2e1-2-3: ISQ mediates between Organizational Culture and Objective Organizational

Performance (EPS, ROE, & ROA)

1.5.3. Organizational Commitment, ISQ and Organizational Performance

H3a: There is a significant impact of Organizational Commitment on ISQ.

H3b: There is a significant impact of Organizational Commitment on Perceived Organizational

Performance

H3c1-2-3: There is a significant impact of organizational commitment on objective

organizational performance (EPS, ROE, & ROA)

H3d: ISQ mediates between Organizational Commitment and Perceived Organizational

Performance

H3e1-2-3: ISQ mediates between Organizational Commitment and Objective Organizational

Performance (EPS, ROE, & ROA)

11

1.5.4. Perceived Organizational Support, ISQ and Organizational Performance

H4a: There is a significant impact of perceived organizational support on ISQ

H4b: There is a significant impact of perceived organizational support on perceived

organizational performance

H4c1-2-3: There is a significant impact of perceived organizational support on objective

organizational performance (EPS, ROE, & ROA)

H4d: ISQ mediates between Perceived Organizational Support and Perceived Organizational

Performance

H4e1-2-3: ISQ mediates between Perceived Organizational Support and Objective

Organizational Performance (EPS, ROE, & ROA)

1.5.5. Role Stress, ISQ and Organizational Performance

H5a: There is a significant impact of Role Stress on ISQ

H5b: There is a significant impact of Role Stress on Perceived Organizational Performance

H5c1-2-3: There is a significant impact of Role Stress on objective organizational performance

(EPS, ROE, & ROA)

H5d: ISQ mediates between Role Stress and Perceived Organizational Performance

H5e1-2-3: ISQ mediates between Role Stress and Objective Organizational Performance (EPS,

ROE, & ROA)

1.5.6. Internal Marketing, ISQ and Organizational Performance

H6a: There is a significant impact of Internal Marketing on ISQ

H6b: There is a significant impact of Internal Marketing on Perceived Organizational

Performance

H6c1-2-3: There is a significant impact of Internal Marketing on objective organizational

performance (EPS, ROE, & ROA)

H6d: ISQ mediates between Internal Marketing and Perceived Organizational Performance

12

H6e1-2-3: ISQ mediates between Internal Marketing and Objective Organizational

Performance (EPS, ROE, & ROA)

H7a: There is a significant impact of ISQ on Perceived Organizational Performance

H7b1-2-3: There is a significant impact of ISQ on objective organizational performance (EPS,

ROE, & ROA)

1.6. Research Scope

1.6.1. Conceptual scope

The study examined the relationship between internal organizational factors

(independent variable), ISQ (mediating variable) and organizational performance (dependent

variable) in the context of banking sector.

1.6.2. Choice of Data Context

The referent data set for the study was obtained from the banking industry in Pakistan.

The focus on banking sector in the present study is dictated by the growth of service sector

that gives a new dimension of stability to Pakistan’s growth process (Ahmed & Ahsan, 2011).

Furthermore, the banking industry provides the financial foundation for growth and stability

in any economy and particularly in the developing economies (Uzkurt, Kumar, Kimzan, &

Eminoglu, 2013). The transformation of the Pakistani banking sector over the past 15 years

through liberalization, establishment of private banks, the privatization of public-sector

banks, and the tightening of prudential regulations has resulted in superior banking

performance (di Patti & Hardy, 2005). Similarly State Bank of Pakistan reports that most of

the banks operating in Pakistan are stable, this shows that Pakistani banking industry has

matured and is found to have been working on improving service quality both for the internal

and external customers. Consequently, the study is based in the context of Banking Industry

in Pakistan and aims to interpret findings from the study for support in designing internal

13

organizational strategies and fostering internal service quality to improve organizational

performance.

1.6.3. Population and Sample.

This research is restricted to the Banking sector. The Data was collected from the

Banks located in Peshawar. The population frame for the study was drawn from the banks

listed in Karachi Stock Exchange (KSE) with over five branches in the city of Peshawar. The

banks were selected on the basis that they had more than five branches in the city in order to

have a representative sample. Out of 24 banks listed in KSE, banks with more than 5

branches in the city were included in the study.

The research divided banks into two strata, i-e, Medium and Large Banks. Since

smaller banks had less than or equal to 5 branches in Peshawar. Therefore, they were

excluded from the study. Since Haksever, Cook, & Chaganti (1997) concluded that causes

that lead to service GAPS in large corporations do not exist in smaller firms. The stratified

random sampling technique is utilized, as taking a random sample might not lead to accurate

results and hence they might not be truly a representative of the population, as with the

increase in the magnitude of bank, the timing of service, stress, learning opportunities would

change. It is for this purpose that stratified random sampling technique has been adopted.

Banks with total assets in excess of Rs. 500 billion are categorized as “Large Banks”, banks

with total assets in between Rs. 100 billion to Rs. 500 billion are categorized as “Medium

Size Banks”. The research adopted the stratified random sampling technique and distributed

banks in homogeneous groups of medium and large banks.

1.7. Significance of the Study

1.7.1. Academic Significance

Service Quality has been identified by both academicians and practitioners as

imperative for organizational survival and growth. The findings of the research will add to

14

the knowledge and understanding of the subject of ISQ. Lack of research in the area of ISQ,

factors that influence ISQ and its relationship with the organizational performance highlight a

knowledge gap. The present study will add to the existing body of knowledge and further

elucidate the phenomenon and its linkage with different internal organizational factors and

organizational performance.

1.7.2. Organizational Significance

The study may help in generating greater awareness among banks on the importance

of having better ISQ, as it would serve as a vehicle for organizational effectiveness.

Additionally the research can help business to understand the value and potential contribution

of different internal organizational factors in organizational performance. Furthermore,

internal service quality is an underdeveloped area. This highlights a prospect for service

organizations that operate in highly competitive and often technologically sophisticated

markets to gain an understanding of further ways to extract any potential advantage over their

rivals (Krios, 2005). Conducting this study in Pakistan is also of great value since limited

work is done on service quality in the banking sector.

1.7.3. Managerial Significance

The present study provides significant insight for HR managers in the banking sector.

The study will assist HR managers in developing better understanding of ISQ and whether

ISQ is worth investment and also in evaluating which factors significantly impact ISQ. With

the findings of this study, HR managers can outline policies and procedures that would help

in the establishment of better ISQ. Furthermore, the research would help the business

managers to determine the key factors that contribute towards organizational performance.

Business executives and managers can then channelize their energies towards variables that

are the most significant.

15

1.7.4. Economic Significance

Banks can significantly contribute to the economic development of a country. Banks,

who perform well can help improve the economy of the country since they would be in a

better position to contribute towards the growth of the economy through assistance of

business. A well performing bank also fuels economic activity by permitting businesses to

invest beyond the available cash that impacts the job market through the creation of

opportunities and potentially helps in improving overall productivity of the country.

1.7.5. Social Significance

The research may help in improving people’s conduct and behaviour. Developing an

understanding of factors that can significant influence employee’s ability to communicate,

understand, show empathy, being responsive towards others can help shape better employee

behaviour both on and off the job. An employee who shows the necessary work related

behaviours can be a valuable member of the society, since he would be in a better position to

balance both work and personal life. Failing to deliver appropriate internal service quality can

significantly hamper employee’s ability to deal with people outside work. Since organizations

do not operate in vacuum, they are filled with people from the society, what people

experience at work, they bring it back home to their social life. Hence, better understanding

of how different factors influence ISQ and fostering ISQ have its social implications.

1.8. The Research Contributions

There are both theoretical and practical justifications for the present study. The

theoretical contributions include a better understanding of the different factors that can affect

ISQ, organizational performance and the effects of ISQ on organizational performance.

Furthermore the study also investigates if ISQ mediates between the direct influence of

internal organizational factors and organizational performance, further highlighting the role

16

of ISQ in the indirect influence of different internal organizational factors and organizational

performance. This will further clarify the need for businesses

To focus on skill acquisition that would not only help in performance

improvements, but also aid in timely delivery of service;

To foster collaboration through the establishment of a strong organizational

culture;

To employ internal marketing techniques that lead to consistency in service

quality;

To minimize role ambiguity and conflict that reduces instability and fosters

focus on the job;

To employ supportive management techniques that would induce benevolence

and display favorable attitudes and behaviors ensuring empathy.

The theoretical contribution also takes account of the value of ISQ for the banking