Factsheet: Asian Local Bond Index (ALBI)-Fixed Income · The HSBC Asian Local Bond Index (ALBI) ......

20

abc Global Research The HSBC Asian Local Bond Index (ALBI) tracks the total return 1 performance of liquid bonds, denominated in local currencies, in China, Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan and Thailand Non-government bond issues, which account for more than half of the ALBI in terms of total number of issues, are included in our China offshore, Hong Kong SAR, Malaysia, Singapore and Thailand sub-indices The index constituents’ selection criteria for each country and country weightings for the ALBI are set to balance the desire for liquidity and stability While each individual local bond index is designed to serve the needs of both domestic and external investors, the ALBI is created to serve the needs of the latter investor base for a regional benchmark index for domestic bond markets and to assist their global asset allocation decisions Local domestic capital markets continue to generate robust interest, both domestically and internationally. We have witnessed strong growth in this segment of the market, as evidenced by the growth of liquidity and strength. Understanding the important role that debt capital markets play, governments in the region have continued to push forward with the development of local currency debt markets. Therefore, it is not surprising that there is a growing need from onshore and offshore investors for a robust benchmark index. Consequently, we continue to see a growing investor base that tracks our ALBI on a regular basis. Since the inception of the ALBI, not only has the investor base that follows this index grown, but the size of the index has grown as well. The ALBI tracks the US dollar total return performance of liquid domestic bonds, denominated in local currencies, in China, Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan and Thailand. It complements our Asian Dollar Bond Index (ADBI), which tracks the performance of liquid external debt in Asia ex Japan. ______________________________________ 1 Total return defined as the sum of local currency capital and accrual returns plus FX returns, stated in USD 5 December 2013 Factsheet: Asian Local Bond Index (ALBI) Fixed Income Asia Louisa Lam Analyst The Hongkong and Shanghai Banking Corporation Limited + 852 2822 4527 [email protected] Kelly Fu Credit Associate The Hongkong and Shanghai Banking Corporation Limited + 852 3941 7066 [email protected] Zhi Ming Zhang Head of China Research The Hongkong and Shanghai Banking Corporation Limited +852 2822 4523 [email protected] View HSBC Global Research at: http://www.research.hsbc.com Issuer of report The Hongkong and Shanghai Banking Corporation Limited Disclaimer & Disclosures. This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, that form p art of it.

Transcript of Factsheet: Asian Local Bond Index (ALBI)-Fixed Income · The HSBC Asian Local Bond Index (ALBI) ......

abcGlobal Research

The HSBC Asian Local Bond Index (ALBI) tracks the total

return1 performance of liquid bonds, denominated in local currencies, in China, Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan and Thailand

Non-government bond issues, which account for more than half of the ALBI in terms of total number of issues, are included in our China offshore, Hong Kong SAR, Malaysia, Singapore and Thailand sub-indices

The index constituents’ selection criteria for each country and country weightings for the ALBI are set to balance the desire for liquidity and stability

While each individual local bond index is designed to serve the needs of both domestic and external investors, the ALBI is created to serve the needs of the latter investor base for a regional benchmark index for domestic bond markets and to assist their global asset allocation decisions

Local domestic capital markets continue to generate robust interest, both domestically and

internationally. We have witnessed strong growth in this segment of the market, as

evidenced by the growth of liquidity and strength. Understanding the important role that

debt capital markets play, governments in the region have continued to push forward with

the development of local currency debt markets. Therefore, it is not surprising that there is

a growing need from onshore and offshore investors for a robust benchmark index.

Consequently, we continue to see a growing investor base that tracks our ALBI on a

regular basis. Since the inception of the ALBI, not only has the investor base that follows

this index grown, but the size of the index has grown as well.

The ALBI tracks the US dollar total return performance of liquid domestic bonds,

denominated in local currencies, in China, Hong Kong, India, Indonesia, Korea, Malaysia,

the Philippines, Singapore, Taiwan and Thailand. It complements our Asian Dollar Bond

Index (ADBI), which tracks the performance of liquid external debt in Asia ex Japan.

______________________________________ 1 Total return defined as the sum of local currency capital and accrual returns plus FX returns, stated in USD

5 December 2013

Factsheet: Asian Local Bond Index (ALBI)

Fixed Income Asia

Louisa Lam Analyst The Hongkong and Shanghai Banking Corporation Limited + 852 2822 4527 [email protected]

Kelly Fu Credit Associate The Hongkong and Shanghai Banking Corporation Limited + 852 3941 7066 [email protected]

Zhi Ming Zhang Head of China Research The Hongkong and Shanghai Banking Corporation Limited +852 2822 4523 [email protected]

View HSBC Global Research at: http://www.research.hsbc.com

Issuer of report

The Hongkong and Shanghai Banking Corporation Limited

Disclaimer & Disclosures. This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, that form part of it.

2

Fixed Income Asia 5 December 2013

abc

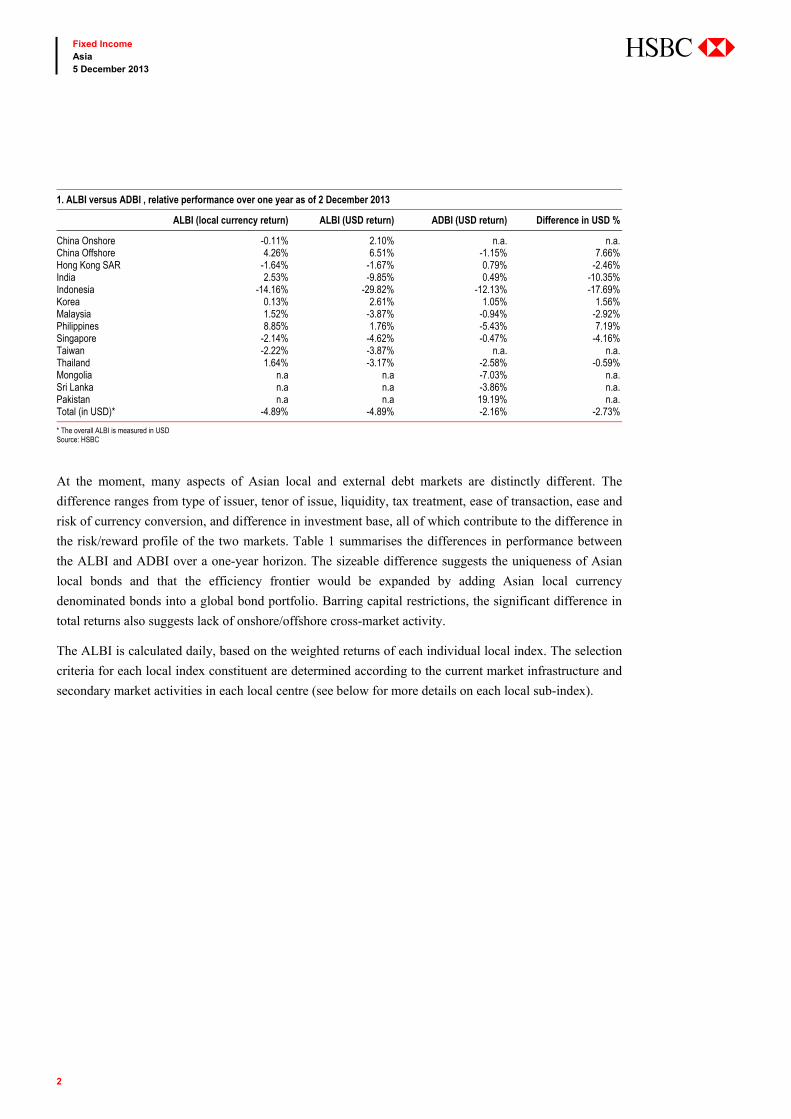

At the moment, many aspects of Asian local and external debt markets are distinctly different. The

difference ranges from type of issuer, tenor of issue, liquidity, tax treatment, ease of transaction, ease and

risk of currency conversion, and difference in investment base, all of which contribute to the difference in

the risk/reward profile of the two markets. Table 1 summarises the differences in performance between

the ALBI and ADBI over a one-year horizon. The sizeable difference suggests the uniqueness of Asian

local bonds and that the efficiency frontier would be expanded by adding Asian local currency

denominated bonds into a global bond portfolio. Barring capital restrictions, the significant difference in

total returns also suggests lack of onshore/offshore cross-market activity.

The ALBI is calculated daily, based on the weighted returns of each individual local index. The selection

criteria for each local index constituent are determined according to the current market infrastructure and

secondary market activities in each local centre (see below for more details on each local sub-index).

1. ALBI versus ADBI , relative performance over one year as of 2 December 2013

ALBI (local currency return) ALBI (USD return) ADBI (USD return) Difference in USD %

China Onshore -0.11% 2.10% n.a. n.a. China Offshore 4.26% 6.51% -1.15% 7.66% Hong Kong SAR -1.64% -1.67% 0.79% -2.46% India 2.53% -9.85% 0.49% -10.35% Indonesia -14.16% -29.82% -12.13% -17.69% Korea 0.13% 2.61% 1.05% 1.56% Malaysia 1.52% -3.87% -0.94% -2.92% Philippines 8.85% 1.76% -5.43% 7.19% Singapore -2.14% -4.62% -0.47% -4.16% Taiwan -2.22% -3.87% n.a. n.a. Thailand 1.64% -3.17% -2.58% -0.59% Mongolia n.a n.a -7.03% n.a. Sri Lanka n.a n.a -3.86% n.a. Pakistan n.a n.a 19.19% n.a. Total (in USD)* -4.89% -4.89% -2.16% -2.73%

* The overall ALBI is measured in USD Source: HSBC

3

Fixed Income Asia 5 December 2013

abc

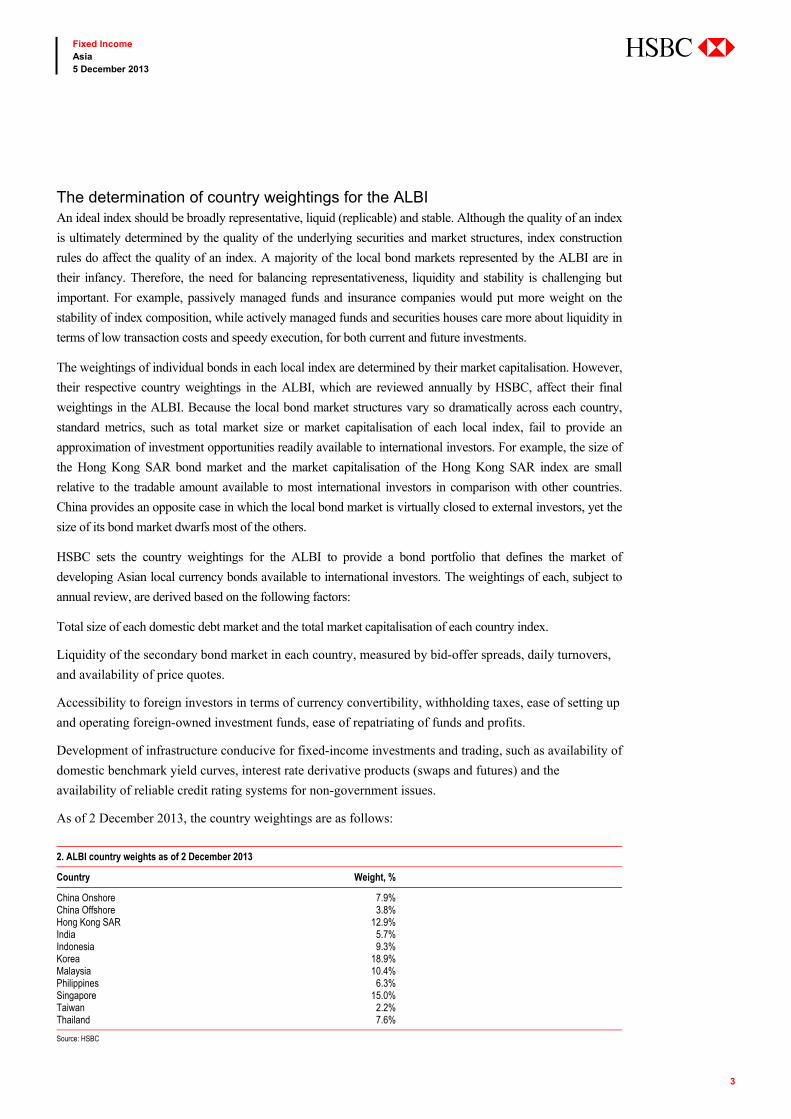

The determination of country weightings for the ALBI An ideal index should be broadly representative, liquid (replicable) and stable. Although the quality of an index

is ultimately determined by the quality of the underlying securities and market structures, index construction

rules do affect the quality of an index. A majority of the local bond markets represented by the ALBI are in

their infancy. Therefore, the need for balancing representativeness, liquidity and stability is challenging but

important. For example, passively managed funds and insurance companies would put more weight on the

stability of index composition, while actively managed funds and securities houses care more about liquidity in

terms of low transaction costs and speedy execution, for both current and future investments.

The weightings of individual bonds in each local index are determined by their market capitalisation. However,

their respective country weightings in the ALBI, which are reviewed annually by HSBC, affect their final

weightings in the ALBI. Because the local bond market structures vary so dramatically across each country,

standard metrics, such as total market size or market capitalisation of each local index, fail to provide an

approximation of investment opportunities readily available to international investors. For example, the size of

the Hong Kong SAR bond market and the market capitalisation of the Hong Kong SAR index are small

relative to the tradable amount available to most international investors in comparison with other countries.

China provides an opposite case in which the local bond market is virtually closed to external investors, yet the

size of its bond market dwarfs most of the others.

HSBC sets the country weightings for the ALBI to provide a bond portfolio that defines the market of

developing Asian local currency bonds available to international investors. The weightings of each, subject to

annual review, are derived based on the following factors:

Total size of each domestic debt market and the total market capitalisation of each country index.

Liquidity of the secondary bond market in each country, measured by bid-offer spreads, daily turnovers,

and availability of price quotes.

Accessibility to foreign investors in terms of currency convertibility, withholding taxes, ease of setting up

and operating foreign-owned investment funds, ease of repatriating of funds and profits.

Development of infrastructure conducive for fixed-income investments and trading, such as availability of

domestic benchmark yield curves, interest rate derivative products (swaps and futures) and the

availability of reliable credit rating systems for non-government issues.

As of 2 December 2013, the country weightings are as follows:

2. ALBI country weights as of 2 December 2013

Country Weight, %

China Onshore 7.9% China Offshore 3.8%Hong Kong SAR 12.9%India 5.7%Indonesia 9.3%Korea 18.9%Malaysia 10.4%Philippines 6.3%Singapore 15.0%Taiwan 2.2%Thailand 7.6%

Source: HSBC

4

Fixed Income Asia 5 December 2013

abc

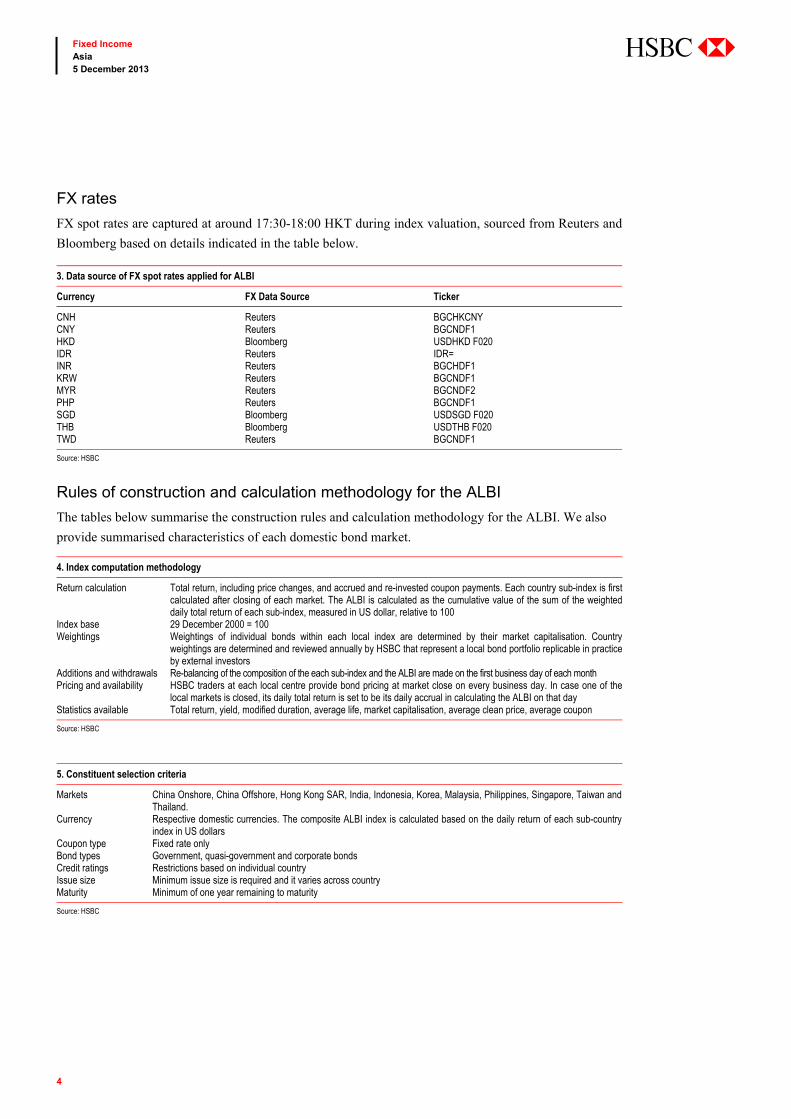

FX rates

FX spot rates are captured at around 17:30-18:00 HKT during index valuation, sourced from Reuters and

Bloomberg based on details indicated in the table below.

Rules of construction and calculation methodology for the ALBI

The tables below summarise the construction rules and calculation methodology for the ALBI. We also

provide summarised characteristics of each domestic bond market.

4. Index computation methodology

Return calculation Total return, including price changes, and accrued and re-invested coupon payments. Each country sub-index is first calculated after closing of each market. The ALBI is calculated as the cumulative value of the sum of the weighteddaily total return of each sub-index, measured in US dollar, relative to 100

Index base 29 December 2000 = 100 Weightings Weightings of individual bonds within each local index are determined by their market capitalisation. Country

weightings are determined and reviewed annually by HSBC that represent a local bond portfolio replicable in practiceby external investors

Additions and withdrawals Re-balancing of the composition of the each sub-index and the ALBI are made on the first business day of each month Pricing and availability HSBC traders at each local centre provide bond pricing at market close on every business day. In case one of the

local markets is closed, its daily total return is set to be its daily accrual in calculating the ALBI on that day Statistics available Total return, yield, modified duration, average life, market capitalisation, average clean price, average coupon

Source: HSBC

5. Constituent selection criteria

Markets China Onshore, China Offshore, Hong Kong SAR, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand.

Currency Respective domestic currencies. The composite ALBI index is calculated based on the daily return of each sub-country index in US dollars

Coupon type Fixed rate only Bond types Government, quasi-government and corporate bondsCredit ratings Restrictions based on individual country Issue size Minimum issue size is required and it varies across countryMaturity Minimum of one year remaining to maturity

Source: HSBC

3. Data source of FX spot rates applied for ALBI

Currency FX Data Source Ticker

CNH Reuters BGCHKCNY CNY Reuters BGCNDF1HKD Bloomberg USDHKD F020IDR Reuters IDR=INR Reuters BGCHDF1KRW Reuters BGCNDF1MYR Reuters BGCNDF2PHP Reuters BGCNDF1SGD Bloomberg USDSGD F020THB Bloomberg USDTHB F020TWD Reuters BGCNDF1

Source: HSBC

5

Fixed Income Asia 5 December 2013

abc

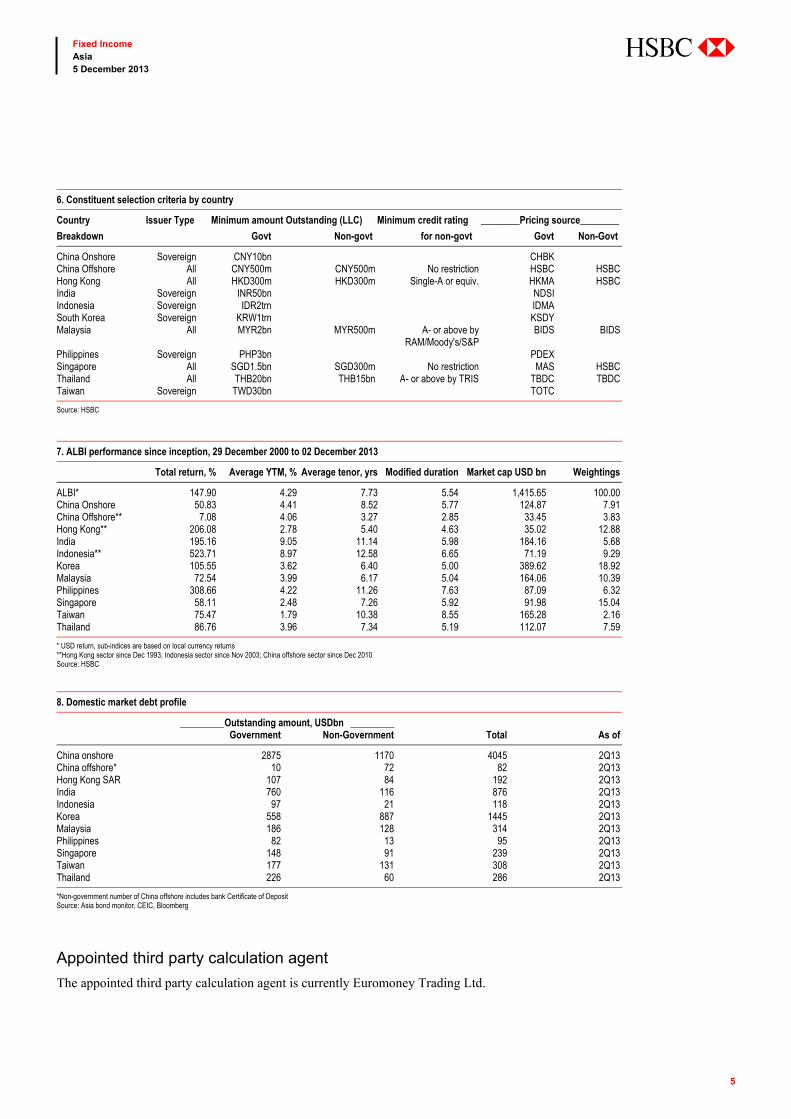

7. ALBI performance since inception, 29 December 2000 to 02 December 2013

Total return, % Average YTM, % Average tenor, yrs Modified duration Market cap USD bn Weightings

ALBI* 147.90 4.29 7.73 5.54 1,415.65 100.00 China Onshore 50.83 4.41 8.52 5.77 124.87 7.91 China Offshore** 7.08 4.06 3.27 2.85 33.45 3.83 Hong Kong** 206.08 2.78 5.40 4.63 35.02 12.88 India 195.16 9.05 11.14 5.98 184.16 5.68 Indonesia** 523.71 8.97 12.58 6.65 71.19 9.29 Korea 105.55 3.62 6.40 5.00 389.62 18.92 Malaysia 72.54 3.99 6.17 5.04 164.06 10.39 Philippines 308.66 4.22 11.26 7.63 87.09 6.32 Singapore 58.11 2.48 7.26 5.92 91.98 15.04 Taiwan 75.47 1.79 10.38 8.55 165.28 2.16 Thailand 86.76 3.96 7.34 5.19 112.07 7.59

* USD return, sub-indices are based on local currency returns **Hong Kong sector since Dec 1993; Indonesia sector since Nov 2003; China offshore sector since Dec 2010 Source: HSBC

8. Domestic market debt profile

_________ Outstanding amount, USDbn _________ Government Non-Government Total As of

China onshore 2875 1170 4045 2Q13 China offshore* 10 72 82 2Q13 Hong Kong SAR 107 84 192 2Q13 India 760 116 876 2Q13 Indonesia 97 21 118 2Q13 Korea 558 887 1445 2Q13 Malaysia 186 128 314 2Q13 Philippines 82 13 95 2Q13 Singapore 148 91 239 2Q13 Taiwan 177 131 308 2Q13 Thailand 226 60 286 2Q13

*Non-government number of China offshore includes bank Certificate of Deposit Source: Asia bond monitor, CEIC, Bloomberg

Appointed third party calculation agent

The appointed third party calculation agent is currently Euromoney Trading Ltd.

6. Constituent selection criteria by country

Country Issuer Type

Breakdown

Minimum amount Outstanding (LLC)

Govt Non-govt

Minimum credit rating

for non-govt

________Pricing source________

Govt Non-Govt

China Onshore Sovereign CNY10bn CHBK China Offshore All CNY500m CNY500m No restriction HSBC HSBC Hong Kong All HKD300m HKD300m Single-A or equiv. HKMA HSBC India Sovereign INR50bn NDSI Indonesia Sovereign IDR2trn IDMA South Korea Sovereign KRW1trn KSDY Malaysia All MYR2bn MYR500m A- or above by

RAM/Moody's/S&PBIDS BIDS

Philippines Sovereign PHP3bn PDEX Singapore All SGD1.5bn SGD300m No restriction MAS HSBC Thailand All THB20bn THB15bn A- or above by TRIS TBDC TBDC Taiwan Sovereign TWD30bn TOTC

Source: HSBC

6

Fixed Income Asia 5 December 2013

abc

Sub-index constraints/boundaries

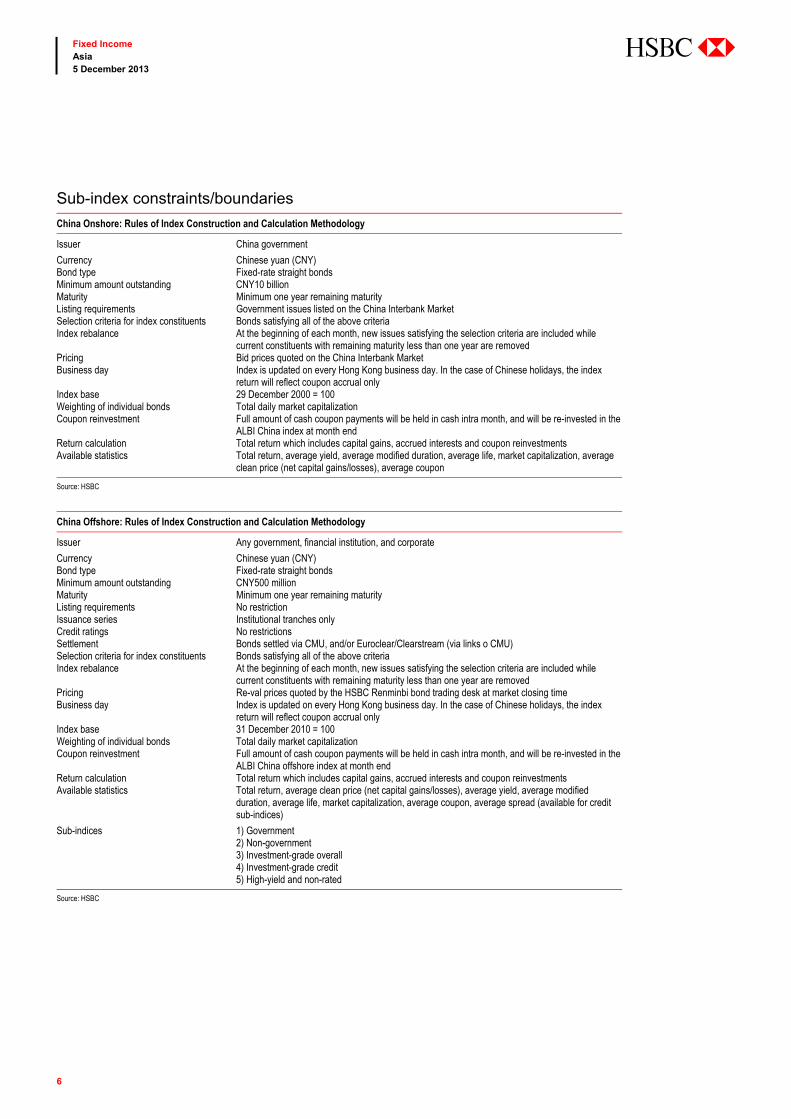

China Onshore: Rules of Index Construction and Calculation Methodology

Issuer China government

Currency Chinese yuan (CNY) Bond type Fixed-rate straight bondsMinimum amount outstanding CNY10 billion Maturity Minimum one year remaining maturity Listing requirements Government issues listed on the China Interbank MarketSelection criteria for index constituents Bonds satisfying all of the above criteriaIndex rebalance At the beginning of each month, new issues satisfying the selection criteria are included while

current constituents with remaining maturity less than one year are removed Pricing Bid prices quoted on the China Interbank MarketBusiness day Index is updated on every Hong Kong business day. In the case of Chinese holidays, the index

return will reflect coupon accrual only Index base 29 December 2000 = 100Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI China index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestments Available statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Source: HSBC

China Offshore: Rules of Index Construction and Calculation Methodology

Issuer Any government, financial institution, and corporate

Currency Chinese yuan (CNY) Bond type Fixed-rate straight bondsMinimum amount outstanding CNY500 million Maturity Minimum one year remaining maturity Listing requirements No restriction Issuance series Institutional tranches onlyCredit ratings No restrictions Settlement Bonds settled via CMU, and/or Euroclear/Clearstream (via links o CMU)Selection criteria for index constituents Bonds satisfying all of the above criteriaIndex rebalance At the beginning of each month, new issues satisfying the selection criteria are included while

current constituents with remaining maturity less than one year are removed Pricing Re-val prices quoted by the HSBC Renminbi bond trading desk at market closing time Business day Index is updated on every Hong Kong business day. In the case of Chinese holidays, the index

return will reflect coupon accrual only Index base 31 December 2010 = 100Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI China offshore index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestments Available statistics

Sub-indices

Total return, average clean price (net capital gains/losses), average yield, average modified duration, average life, market capitalization, average coupon, average spread (available for credit sub-indices)

1) Government 2) Non-government 3) Investment-grade overall 4) Investment-grade credit 5) High-yield and non-rated

Source: HSBC

7

Fixed Income Asia 5 December 2013

abc

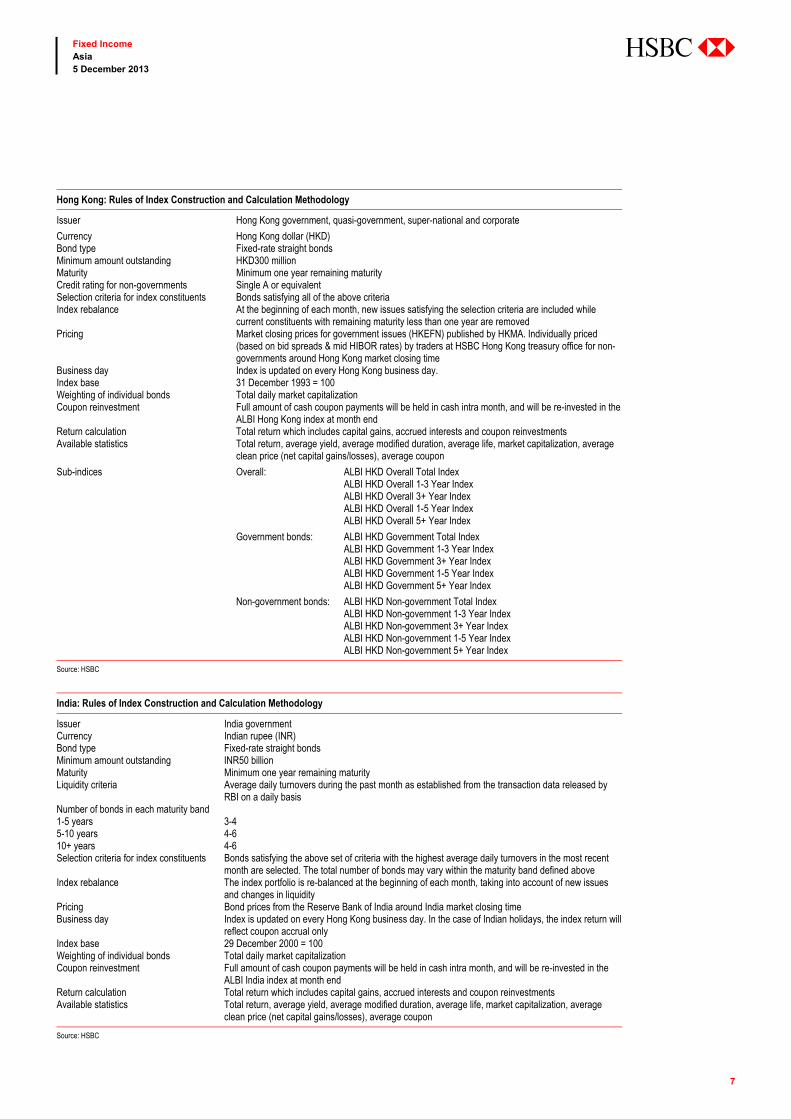

Hong Kong: Rules of Index Construction and Calculation Methodology

Issuer Hong Kong government, quasi-government, super-national and corporate

Currency Hong Kong dollar (HKD) Bond type Fixed-rate straight bondsMinimum amount outstanding HKD300 million Maturity Minimum one year remaining maturity Credit rating for non-governments Single A or equivalent Selection criteria for index constituents Bonds satisfying all of the above criteria Index rebalance At the beginning of each month, new issues satisfying the selection criteria are included while

current constituents with remaining maturity less than one year are removed Pricing Market closing prices for government issues (HKEFN) published by HKMA. Individually priced

(based on bid spreads & mid HIBOR rates) by traders at HSBC Hong Kong treasury office for non-governments around Hong Kong market closing time

Business day Index is updated on every Hong Kong business day. Index base 31 December 1993 = 100Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Hong Kong index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestments Available statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Sub-indices Overall: ALBI HKD Overall Total IndexALBI HKD Overall 1-3 Year Index ALBI HKD Overall 3+ Year Index ALBI HKD Overall 1-5 Year Index ALBI HKD Overall 5+ Year Index

Government bonds: ALBI HKD Government Total IndexALBI HKD Government 1-3 Year Index ALBI HKD Government 3+ Year Index ALBI HKD Government 1-5 Year Index ALBI HKD Government 5+ Year Index

Non-government bonds: ALBI HKD Non-government Total IndexALBI HKD Non-government 1-3 Year Index ALBI HKD Non-government 3+ Year Index ALBI HKD Non-government 1-5 Year Index ALBI HKD Non-government 5+ Year Index

Source: HSBC

India: Rules of Index Construction and Calculation Methodology

Issuer India government Currency Indian rupee (INR) Bond type Fixed-rate straight bonds Minimum amount outstanding INR50 billion Maturity Minimum one year remaining maturity Liquidity criteria Average daily turnovers during the past month as established from the transaction data released by

RBI on a daily basis Number of bonds in each maturity band 1-5 years 3-45-10 years 4-610+ years 4-6Selection criteria for index constituents Bonds satisfying the above set of criteria with the highest average daily turnovers in the most recent

month are selected. The total number of bonds may vary within the maturity band defined above Index rebalance The index portfolio is re-balanced at the beginning of each month, taking into account of new issues

and changes in liquidity Pricing Bond prices from the Reserve Bank of India around India market closing timeBusiness day Index is updated on every Hong Kong business day. In the case of Indian holidays, the index return will

reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI India index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestmentsAvailable statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Source: HSBC

8

Fixed Income Asia 5 December 2013

abc

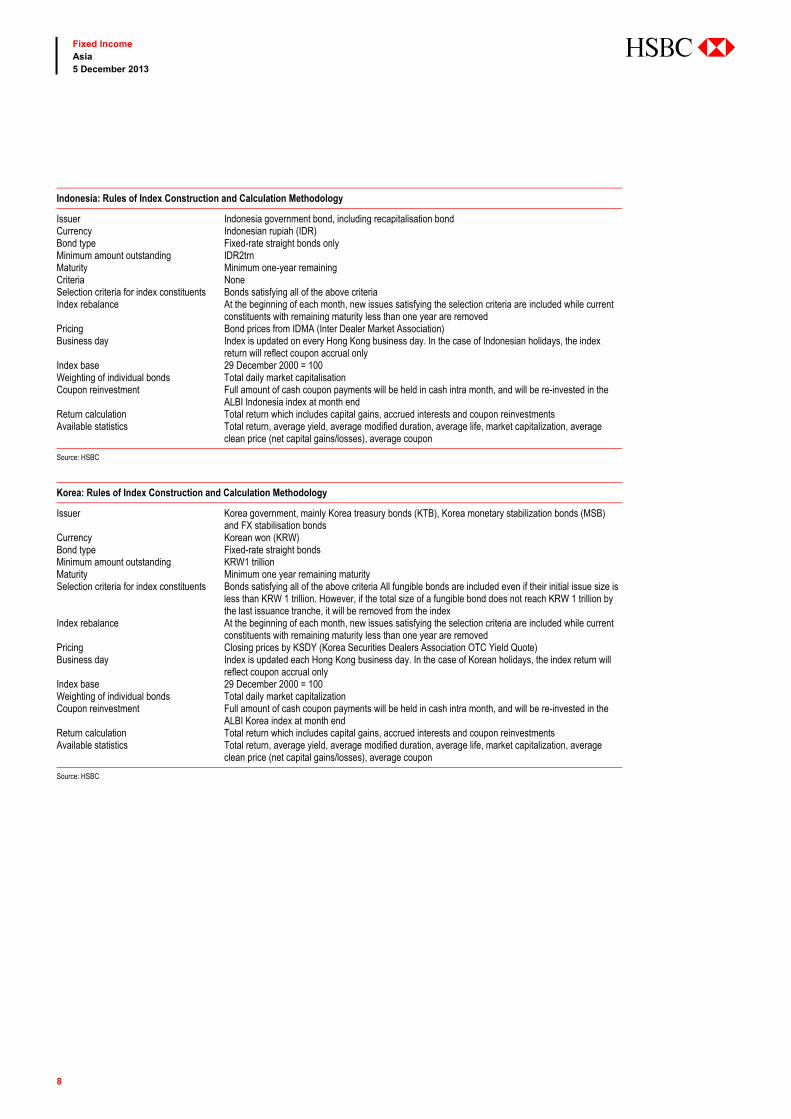

Indonesia: Rules of Index Construction and Calculation Methodology

Issuer Indonesia government bond, including recapitalisation bond Currency Indonesian rupiah (IDR) Bond type Fixed-rate straight bonds onlyMinimum amount outstanding IDR2trn Maturity Minimum one-year remainingCriteria NoneSelection criteria for index constituents Bonds satisfying all of the above criteriaIndex rebalance At the beginning of each month, new issues satisfying the selection criteria are included while current

constituents with remaining maturity less than one year are removed Pricing Bond prices from IDMA (Inter Dealer Market Association)Business day Index is updated on every Hong Kong business day. In the case of Indonesian holidays, the index

return will reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalisationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Indonesia index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestmentsAvailable statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Source: HSBC

Korea: Rules of Index Construction and Calculation Methodology

Issuer Korea government, mainly Korea treasury bonds (KTB), Korea monetary stabilization bonds (MSB) and FX stabilisation bonds

Currency Korean won (KRW) Bond type Fixed-rate straight bonds Minimum amount outstanding KRW1 trillion Maturity Minimum one year remaining maturity Selection criteria for index constituents Bonds satisfying all of the above criteria All fungible bonds are included even if their initial issue size is

less than KRW 1 trillion. However, if the total size of a fungible bond does not reach KRW 1 trillion by the last issuance tranche, it will be removed from the index

Index rebalance At the beginning of each month, new issues satisfying the selection criteria are included while current constituents with remaining maturity less than one year are removed

Pricing Closing prices by KSDY (Korea Securities Dealers Association OTC Yield Quote)Business day Index is updated each Hong Kong business day. In the case of Korean holidays, the index return will

reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Korea index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestmentsAvailable statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Source: HSBC

9

Fixed Income Asia 5 December 2013

abc

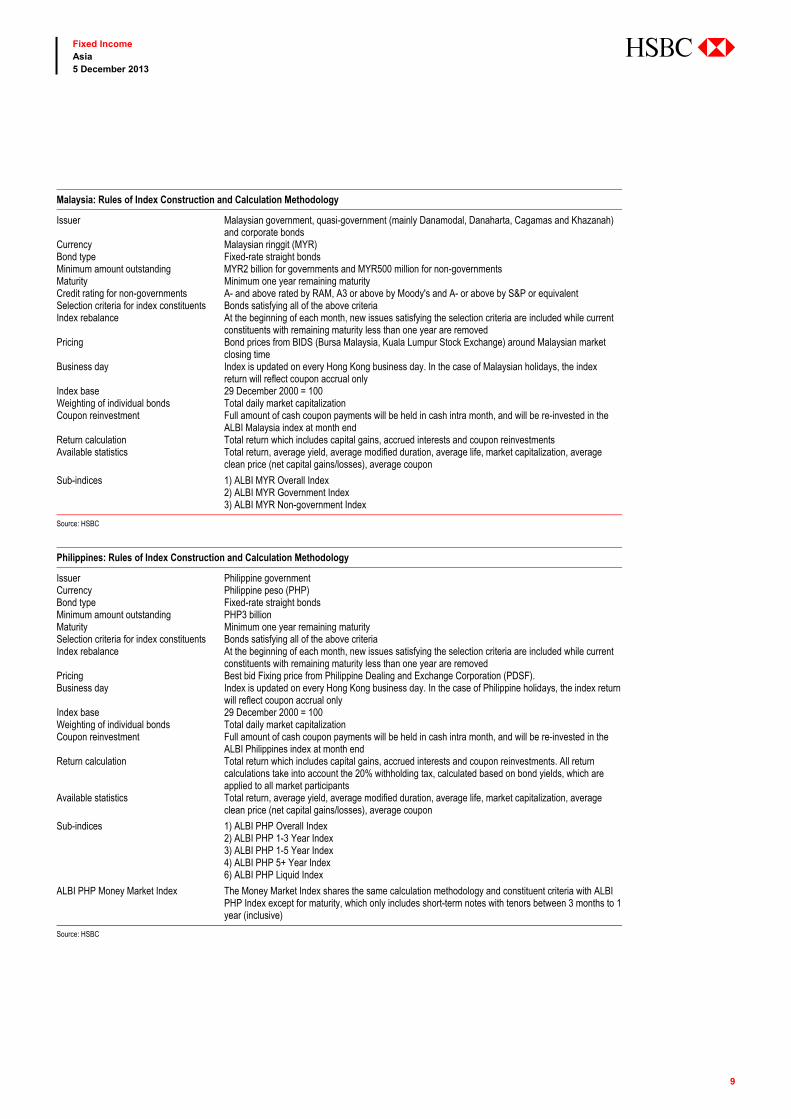

Malaysia: Rules of Index Construction and Calculation Methodology

Issuer Malaysian government, quasi-government (mainly Danamodal, Danaharta, Cagamas and Khazanah) and corporate bonds

Currency Malaysian ringgit (MYR) Bond type Fixed-rate straight bonds Minimum amount outstanding MYR2 billion for governments and MYR500 million for non-governmentsMaturity Minimum one year remaining maturity Credit rating for non-governments A- and above rated by RAM, A3 or above by Moody's and A- or above by S&P or equivalent Selection criteria for index constituents Bonds satisfying all of the above criteria Index rebalance At the beginning of each month, new issues satisfying the selection criteria are included while current

constituents with remaining maturity less than one year are removed Pricing Bond prices from BIDS (Bursa Malaysia, Kuala Lumpur Stock Exchange) around Malaysian market

closing time Business day Index is updated on every Hong Kong business day. In the case of Malaysian holidays, the index

return will reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Malaysia index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestmentsAvailable statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Sub-indices 1) ALBI MYR Overall Index2) ALBI MYR Government Index 3) ALBI MYR Non-government Index

Source: HSBC

Philippines: Rules of Index Construction and Calculation Methodology

Issuer Philippine government Currency Philippine peso (PHP) Bond type Fixed-rate straight bonds Minimum amount outstanding PHP3 billion Maturity Minimum one year remaining maturity Selection criteria for index constituents Bonds satisfying all of the above criteria Index rebalance At the beginning of each month, new issues satisfying the selection criteria are included while current

constituents with remaining maturity less than one year are removed Pricing Best bid Fixing price from Philippine Dealing and Exchange Corporation (PDSF).Business day Index is updated on every Hong Kong business day. In the case of Philippine holidays, the index return

will reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Philippines index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestments. All return

calculations take into account the 20% withholding tax, calculated based on bond yields, which are applied to all market participants

Available statistics Total return, average yield, average modified duration, average life, market capitalization, average clean price (net capital gains/losses), average coupon

Sub-indices 1) ALBI PHP Overall Index2) ALBI PHP 1-3 Year Index 3) ALBI PHP 1-5 Year Index 4) ALBI PHP 5+ Year Index 6) ALBI PHP Liquid Index

ALBI PHP Money Market Index The Money Market Index shares the same calculation methodology and constituent criteria with ALBI PHP Index except for maturity, which only includes short-term notes with tenors between 3 months to 1 year (inclusive)

Source: HSBC

10

Fixed Income Asia 5 December 2013

abc

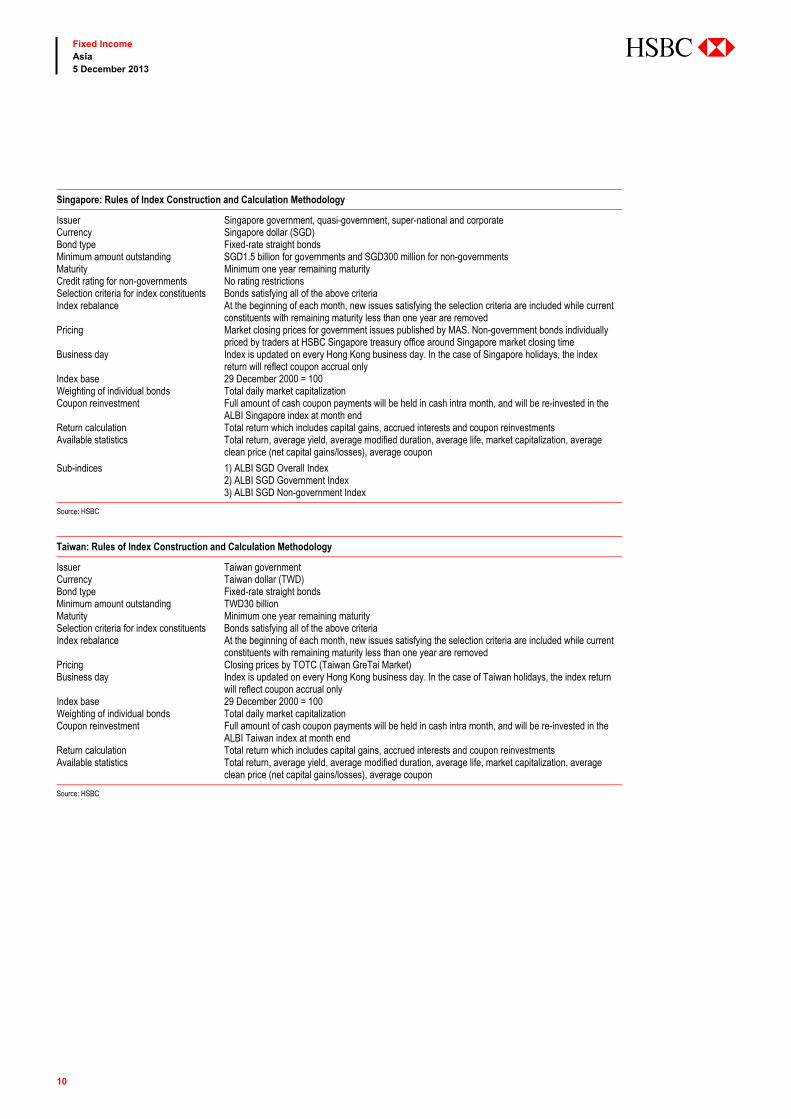

Singapore: Rules of Index Construction and Calculation Methodology

Issuer Singapore government, quasi-government, super-national and corporate Currency Singapore dollar (SGD) Bond type Fixed-rate straight bonds Minimum amount outstanding SGD1.5 billion for governments and SGD300 million for non-governmentsMaturity Minimum one year remaining maturity Credit rating for non-governments No rating restrictions Selection criteria for index constituents Bonds satisfying all of the above criteriaIndex rebalance At the beginning of each month, new issues satisfying the selection criteria are included while current

constituents with remaining maturity less than one year are removed Pricing Market closing prices for government issues published by MAS. Non-government bonds individually

priced by traders at HSBC Singapore treasury office around Singapore market closing time Business day Index is updated on every Hong Kong business day. In the case of Singapore holidays, the index

return will reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Singapore index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestmentsAvailable statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Sub-indices 1) ALBI SGD Overall Index2) ALBI SGD Government Index 3) ALBI SGD Non-government Index

Source: HSBC

Taiwan: Rules of Index Construction and Calculation Methodology

Issuer Taiwan government Currency Taiwan dollar (TWD) Bond type Fixed-rate straight bonds Minimum amount outstanding TWD30 billion Maturity Minimum one year remaining maturity Selection criteria for index constituents Bonds satisfying all of the above criteriaIndex rebalance At the beginning of each month, new issues satisfying the selection criteria are included while current

constituents with remaining maturity less than one year are removed Pricing Closing prices by TOTC (Taiwan GreTai Market)Business day Index is updated on every Hong Kong business day. In the case of Taiwan holidays, the index return

will reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Taiwan index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestmentsAvailable statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Source: HSBC

11

Fixed Income Asia 5 December 2013

abc

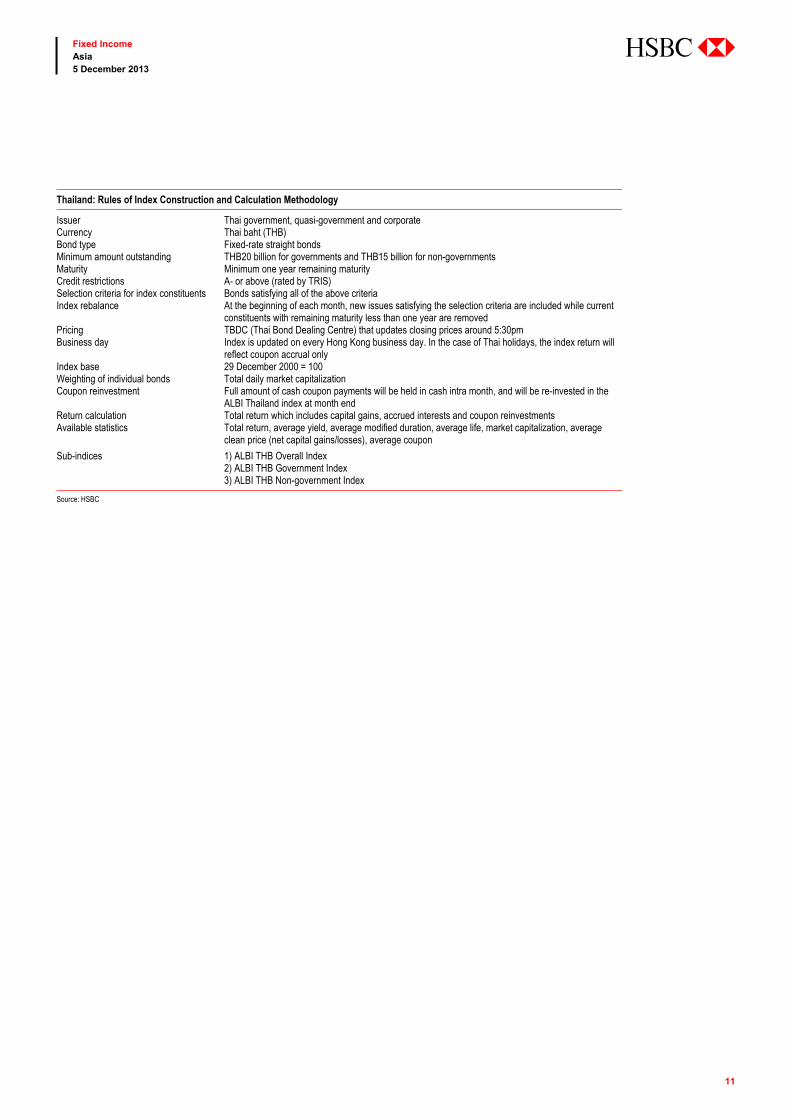

Thailand: Rules of Index Construction and Calculation Methodology

Issuer Thai government, quasi-government and corporate Currency Thai baht (THB) Bond type Fixed-rate straight bonds Minimum amount outstanding THB20 billion for governments and THB15 billion for non-governmentsMaturity Minimum one year remaining maturity Credit restrictions A- or above (rated by TRIS)Selection criteria for index constituents Bonds satisfying all of the above criteria Index rebalance At the beginning of each month, new issues satisfying the selection criteria are included while current

constituents with remaining maturity less than one year are removed Pricing TBDC (Thai Bond Dealing Centre) that updates closing prices around 5:30pmBusiness day Index is updated on every Hong Kong business day. In the case of Thai holidays, the index return will

reflect coupon accrual only Index base 29 December 2000 = 100 Weighting of individual bonds Total daily market capitalizationCoupon reinvestment Full amount of cash coupon payments will be held in cash intra month, and will be re-invested in the

ALBI Thailand index at month end Return calculation Total return which includes capital gains, accrued interests and coupon reinvestmentsAvailable statistics Total return, average yield, average modified duration, average life, market capitalization, average

clean price (net capital gains/losses), average coupon

Sub-indices 1) ALBI THB Overall Index2) ALBI THB Government Index 3) ALBI THB Non-government Index

Source: HSBC

12

Fixed Income Asia 5 December 2013

abc

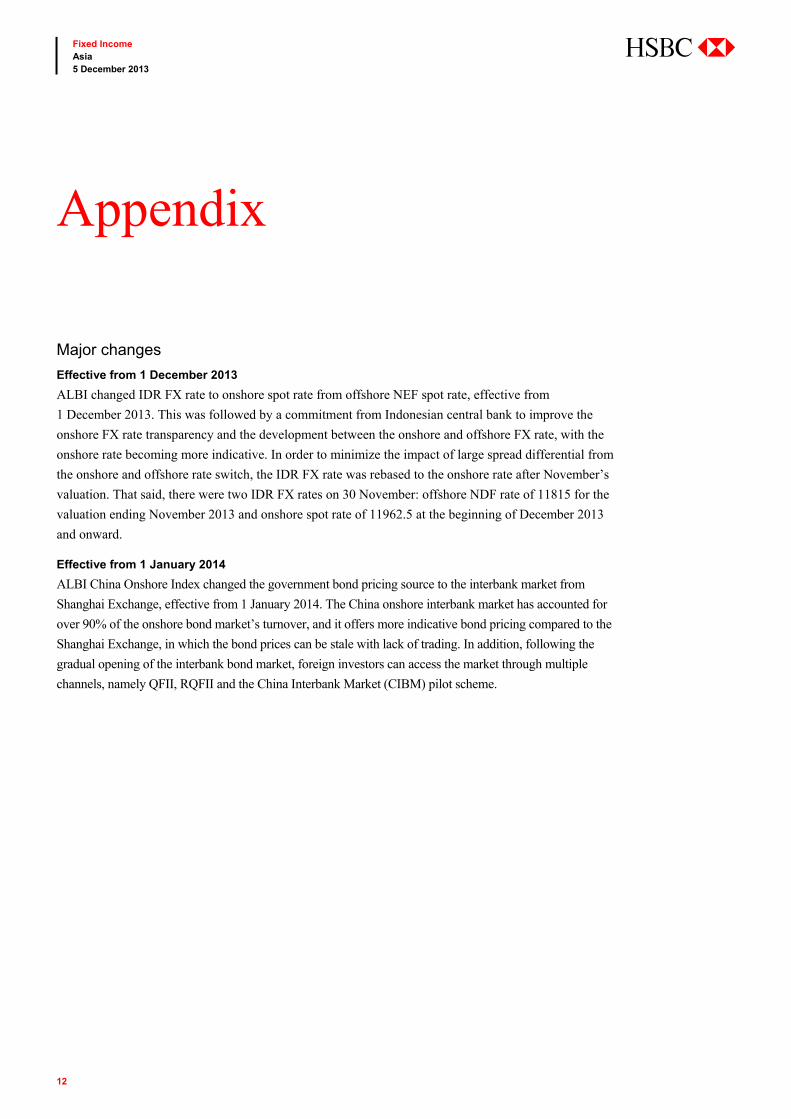

Major changes

Effective from 1 December 2013

ALBI changed IDR FX rate to onshore spot rate from offshore NEF spot rate, effective from

1 December 2013. This was followed by a commitment from Indonesian central bank to improve the

onshore FX rate transparency and the development between the onshore and offshore FX rate, with the

onshore rate becoming more indicative. In order to minimize the impact of large spread differential from

the onshore and offshore rate switch, the IDR FX rate was rebased to the onshore rate after November’s

valuation. That said, there were two IDR FX rates on 30 November: offshore NDF rate of 11815 for the

valuation ending November 2013 and onshore spot rate of 11962.5 at the beginning of December 2013

and onward.

Effective from 1 January 2014

ALBI China Onshore Index changed the government bond pricing source to the interbank market from

Shanghai Exchange, effective from 1 January 2014. The China onshore interbank market has accounted for

over 90% of the onshore bond market’s turnover, and it offers more indicative bond pricing compared to the

Shanghai Exchange, in which the bond prices can be stale with lack of trading. In addition, following the

gradual opening of the interbank bond market, foreign investors can access the market through multiple

channels, namely QFII, RQFII and the China Interbank Market (CIBM) pilot scheme.

Appendix

13

Fixed Income Asia 5 December 2013

abc

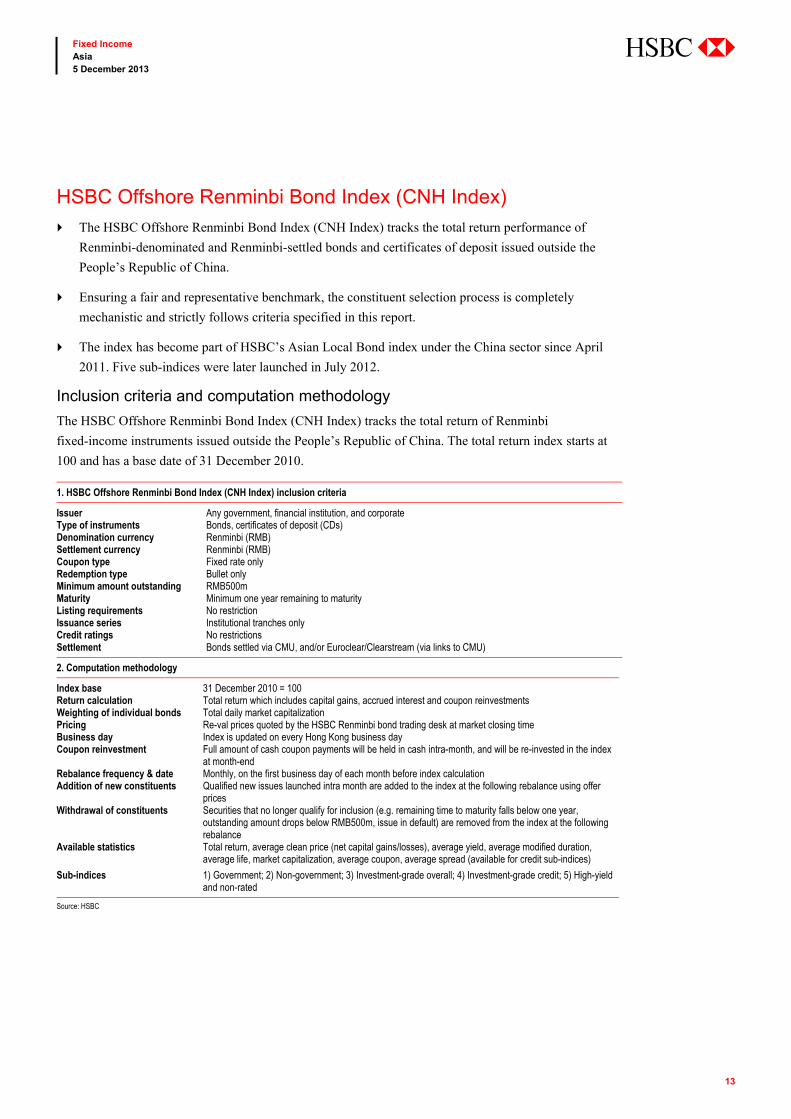

HSBC Offshore Renminbi Bond Index (CNH Index)

The HSBC Offshore Renminbi Bond Index (CNH Index) tracks the total return performance of

Renminbi-denominated and Renminbi-settled bonds and certificates of deposit issued outside the

People’s Republic of China.

Ensuring a fair and representative benchmark, the constituent selection process is completely

mechanistic and strictly follows criteria specified in this report.

The index has become part of HSBC’s Asian Local Bond index under the China sector since April

2011. Five sub-indices were later launched in July 2012.

Inclusion criteria and computation methodology

The HSBC Offshore Renminbi Bond Index (CNH Index) tracks the total return of Renminbi

fixed-income instruments issued outside the People’s Republic of China. The total return index starts at

100 and has a base date of 31 December 2010. 1. HSBC Offshore Renminbi Bond Index (CNH Index) inclusion criteria

Issuer Any government, financial institution, and corporate Type of instruments Bonds, certificates of deposit (CDs)Denomination currency Renminbi (RMB) Settlement currency Renminbi (RMB) Coupon type Fixed rate only Redemption type Bullet only Minimum amount outstanding RMB500m Maturity Minimum one year remaining to maturityListing requirements No restriction Issuance series Institutional tranches only Credit ratings No restrictions Settlement Bonds settled via CMU, and/or Euroclear/Clearstream (via links to CMU)

2. Computation methodology

Index base 31 December 2010 = 100 Return calculation Total return which includes capital gains, accrued interest and coupon reinvestmentsWeighting of individual bonds Total daily market capitalization Pricing Re-val prices quoted by the HSBC Renminbi bond trading desk at market closing timeBusiness day Index is updated on every Hong Kong business dayCoupon reinvestment Full amount of cash coupon payments will be held in cash intra-month, and will be re-invested in the index

at month-end Rebalance frequency & date Monthly, on the first business day of each month before index calculationAddition of new constituents Qualified new issues launched intra month are added to the index at the following rebalance using offer

prices Withdrawal of constituents Securities that no longer qualify for inclusion (e.g. remaining time to maturity falls below one year,

outstanding amount drops below RMB500m, issue in default) are removed from the index at the following rebalance

Available statistics Total return, average clean price (net capital gains/losses), average yield, average modified duration, average life, market capitalization, average coupon, average spread (available for credit sub-indices)

Sub-indices 1) Government; 2) Non-government; 3) Investment-grade overall; 4) Investment-grade credit; 5) High-yield and non-rated

Source: HSBC

14

Fixed Income Asia 5 December 2013

abc

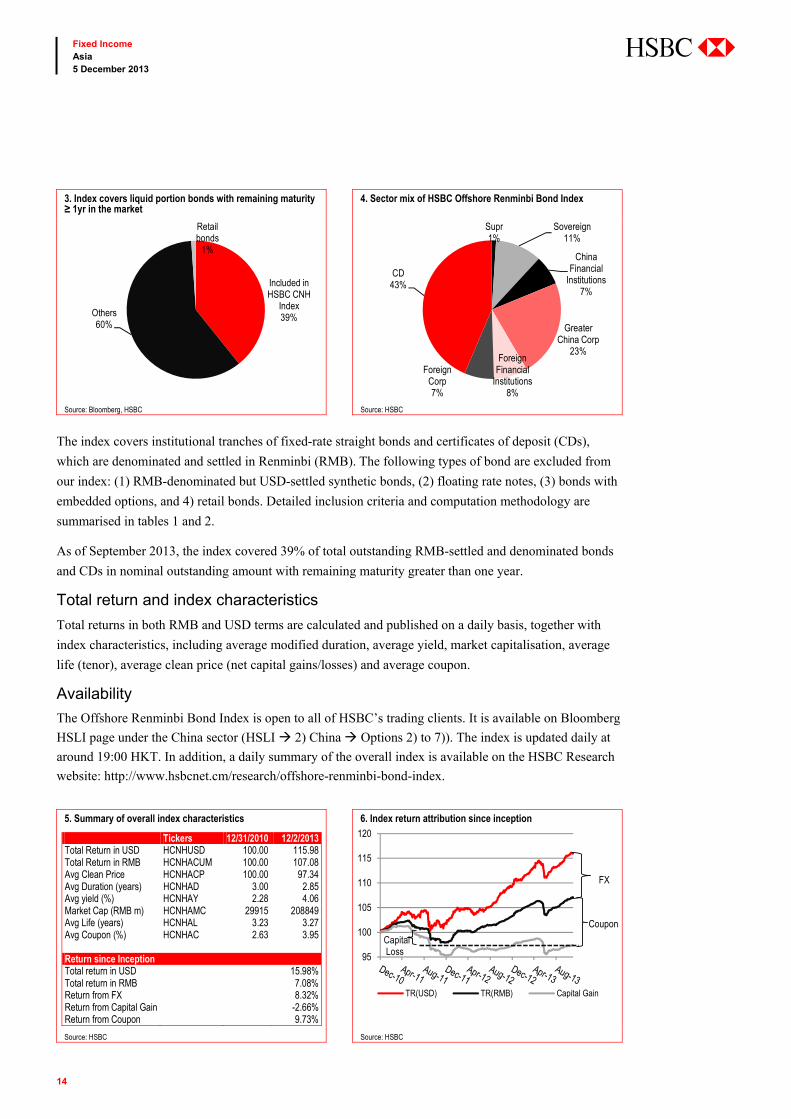

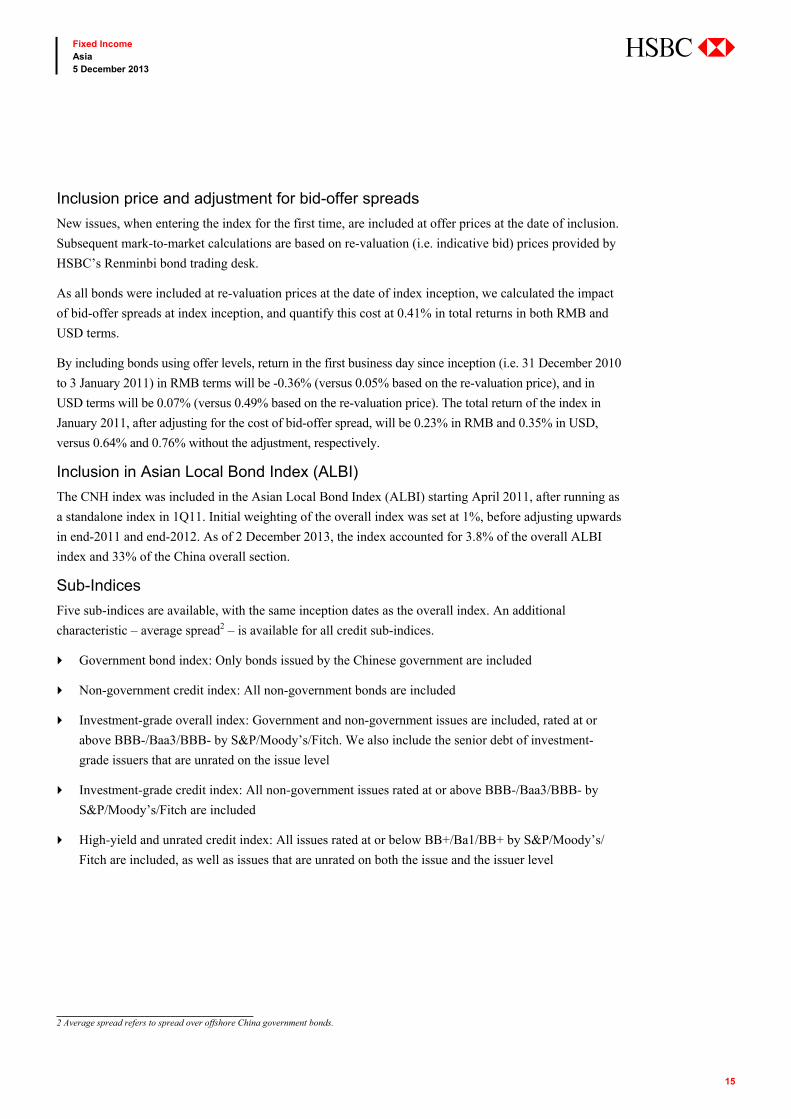

The index covers institutional tranches of fixed-rate straight bonds and certificates of deposit (CDs),

which are denominated and settled in Renminbi (RMB). The following types of bond are excluded from

our index: (1) RMB-denominated but USD-settled synthetic bonds, (2) floating rate notes, (3) bonds with

embedded options, and 4) retail bonds. Detailed inclusion criteria and computation methodology are

summarised in tables 1 and 2.

As of September 2013, the index covered 39% of total outstanding RMB-settled and denominated bonds

and CDs in nominal outstanding amount with remaining maturity greater than one year.

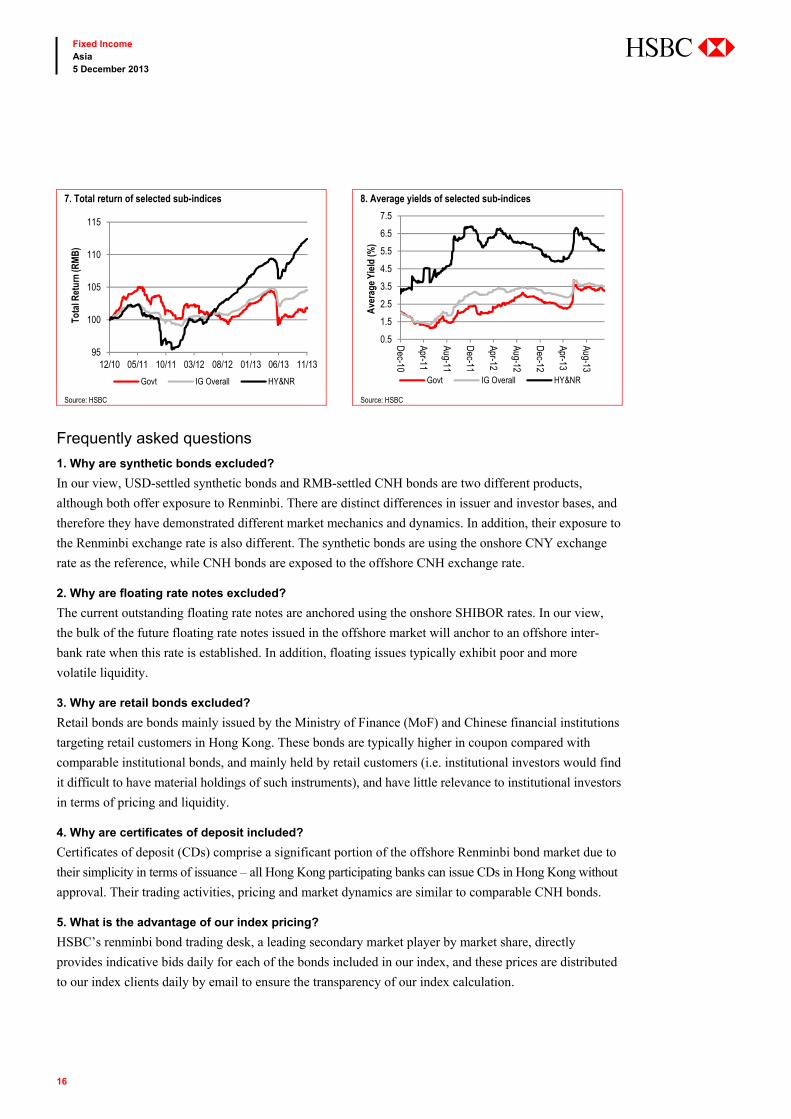

Total return and index characteristics

Total returns in both RMB and USD terms are calculated and published on a daily basis, together with

index characteristics, including average modified duration, average yield, market capitalisation, average

life (tenor), average clean price (net capital gains/losses) and average coupon.

Availability

The Offshore Renminbi Bond Index is open to all of HSBC’s trading clients. It is available on Bloomberg

HSLI page under the China sector (HSLI 2) China Options 2) to 7)). The index is updated daily at

around 19:00 HKT. In addition, a daily summary of the overall index is available on the HSBC Research

website: http://www.hsbcnet.cm/research/offshore-renminbi-bond-index.

3. Index covers liquid portion bonds with remaining maturity ≥ 1yr in the market

4. Sector mix of HSBC Offshore Renminbi Bond Index

Source: Bloomberg, HSBC Source: HSBC

5. Summary of overall index characteristics 6. Index return attribution since inception

Source: HSBC Source: HSBC

Included in HSBC CNH

Index39%Others

60%

Retail bonds

1%

Supr1%

Sovereign11%

China Financial

Institutions7%

Greater China Corp

23%Foreign

Financial Institutions

8%

Foreign Corp7%

CD43%

Tickers 12/31/2010 12/2/2013 Total Return in USD HCNHUSD 100.00 115.98 Total Return in RMB HCNHACUM 100.00 107.08 Avg Clean Price HCNHACP 100.00 97.34 Avg Duration (years) HCNHAD 3.00 2.85 Avg yield (%) HCNHAY 2.28 4.06 Market Cap (RMB m) HCNHAMC 29915 208849 Avg Life (years) HCNHAL 3.23 3.27 Avg Coupon (%) HCNHAC 2.63 3.95 Return since Inception Total return in USD 15.98% Total return in RMB 7.08% Return from FX 8.32% Return from Capital Gain -2.66% Return from Coupon 9.73%

95

100

105

110

115

120

TR(USD) TR(RMB) Capital Gain

FX

Coupon

CapitalLoss

15

Fixed Income Asia 5 December 2013

abc

Inclusion price and adjustment for bid-offer spreads

New issues, when entering the index for the first time, are included at offer prices at the date of inclusion.

Subsequent mark-to-market calculations are based on re-valuation (i.e. indicative bid) prices provided by

HSBC’s Renminbi bond trading desk.

As all bonds were included at re-valuation prices at the date of index inception, we calculated the impact

of bid-offer spreads at index inception, and quantify this cost at 0.41% in total returns in both RMB and

USD terms.

By including bonds using offer levels, return in the first business day since inception (i.e. 31 December 2010

to 3 January 2011) in RMB terms will be -0.36% (versus 0.05% based on the re-valuation price), and in

USD terms will be 0.07% (versus 0.49% based on the re-valuation price). The total return of the index in

January 2011, after adjusting for the cost of bid-offer spread, will be 0.23% in RMB and 0.35% in USD,

versus 0.64% and 0.76% without the adjustment, respectively.

Inclusion in Asian Local Bond Index (ALBI)

The CNH index was included in the Asian Local Bond Index (ALBI) starting April 2011, after running as

a standalone index in 1Q11. Initial weighting of the overall index was set at 1%, before adjusting upwards

in end-2011 and end-2012. As of 2 December 2013, the index accounted for 3.8% of the overall ALBI

index and 33% of the China overall section.

Sub-Indices

Five sub-indices are available, with the same inception dates as the overall index. An additional

characteristic – average spread2 – is available for all credit sub-indices.

Government bond index: Only bonds issued by the Chinese government are included

Non-government credit index: All non-government bonds are included

Investment-grade overall index: Government and non-government issues are included, rated at or

above BBB-/Baa3/BBB- by S&P/Moody’s/Fitch. We also include the senior debt of investment-

grade issuers that are unrated on the issue level

Investment-grade credit index: All non-government issues rated at or above BBB-/Baa3/BBB- by

S&P/Moody’s/Fitch are included

High-yield and unrated credit index: All issues rated at or below BB+/Ba1/BB+ by S&P/Moody’s/

Fitch are included, as well as issues that are unrated on both the issue and the issuer level

______________________________________ 2 Average spread refers to spread over offshore China government bonds.

16

Fixed Income Asia 5 December 2013

abc

Frequently asked questions

1. Why are synthetic bonds excluded?

In our view, USD-settled synthetic bonds and RMB-settled CNH bonds are two different products,

although both offer exposure to Renminbi. There are distinct differences in issuer and investor bases, and

therefore they have demonstrated different market mechanics and dynamics. In addition, their exposure to

the Renminbi exchange rate is also different. The synthetic bonds are using the onshore CNY exchange

rate as the reference, while CNH bonds are exposed to the offshore CNH exchange rate.

2. Why are floating rate notes excluded?

The current outstanding floating rate notes are anchored using the onshore SHIBOR rates. In our view,

the bulk of the future floating rate notes issued in the offshore market will anchor to an offshore inter-

bank rate when this rate is established. In addition, floating issues typically exhibit poor and more

volatile liquidity.

3. Why are retail bonds excluded?

Retail bonds are bonds mainly issued by the Ministry of Finance (MoF) and Chinese financial institutions

targeting retail customers in Hong Kong. These bonds are typically higher in coupon compared with

comparable institutional bonds, and mainly held by retail customers (i.e. institutional investors would find

it difficult to have material holdings of such instruments), and have little relevance to institutional investors

in terms of pricing and liquidity.

4. Why are certificates of deposit included?

Certificates of deposit (CDs) comprise a significant portion of the offshore Renminbi bond market due to

their simplicity in terms of issuance – all Hong Kong participating banks can issue CDs in Hong Kong without

approval. Their trading activities, pricing and market dynamics are similar to comparable CNH bonds.

5. What is the advantage of our index pricing?

HSBC’s renminbi bond trading desk, a leading secondary market player by market share, directly

provides indicative bids daily for each of the bonds included in our index, and these prices are distributed

to our index clients daily by email to ensure the transparency of our index calculation.

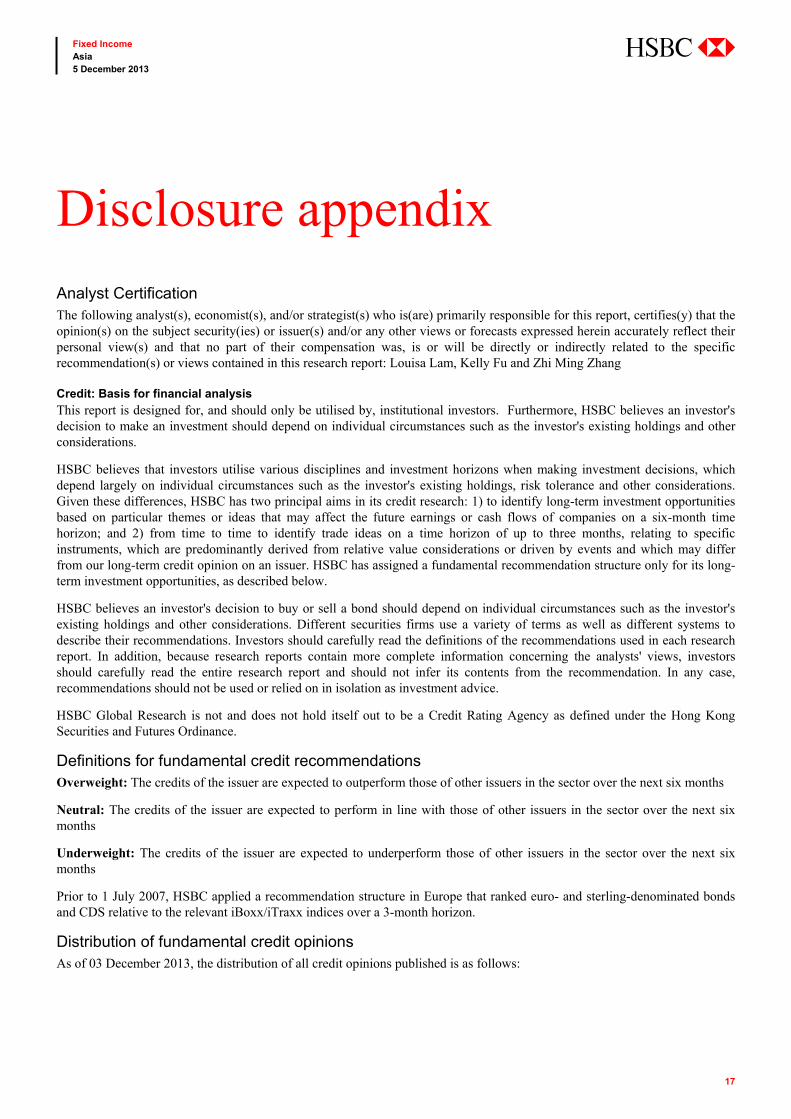

7. Total return of selected sub-indices 8. Average yields of selected sub-indices

Source: HSBC Source: HSBC

95

100

105

110

115

12/10 05/11 10/11 03/12 08/12 01/13 06/13 11/13

Tota

l Ret

urn

(RM

B)

Govt IG Overall HY&NR

0.5

1.5

2.5

3.5

4.5

5.5

6.5

7.5

Dec-10

Apr-11

Aug-11

Dec-11

Apr-12

Aug-12

Dec-12

Apr-13

Aug-13

Ave

rage

Yie

ld (%

)Govt IG Overall HY&NR

17

Fixed Income Asia 5 December 2013

abc

Disclosure appendix Analyst Certification The following analyst(s), economist(s), and/or strategist(s) who is(are) primarily responsible for this report, certifies(y) that the opinion(s) on the subject security(ies) or issuer(s) and/or any other views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Louisa Lam, Kelly Fu and Zhi Ming Zhang

Credit: Basis for financial analysis

This report is designed for, and should only be utilised by, institutional investors. Furthermore, HSBC believes an investor's decision to make an investment should depend on individual circumstances such as the investor's existing holdings and other considerations.

HSBC believes that investors utilise various disciplines and investment horizons when making investment decisions, which depend largely on individual circumstances such as the investor's existing holdings, risk tolerance and other considerations. Given these differences, HSBC has two principal aims in its credit research: 1) to identify long-term investment opportunities based on particular themes or ideas that may affect the future earnings or cash flows of companies on a six-month time horizon; and 2) from time to time to identify trade ideas on a time horizon of up to three months, relating to specific instruments, which are predominantly derived from relative value considerations or driven by events and which may differ from our long-term credit opinion on an issuer. HSBC has assigned a fundamental recommendation structure only for its long-term investment opportunities, as described below.

HSBC believes an investor's decision to buy or sell a bond should depend on individual circumstances such as the investor's existing holdings and other considerations. Different securities firms use a variety of terms as well as different systems to describe their recommendations. Investors should carefully read the definitions of the recommendations used in each research report. In addition, because research reports contain more complete information concerning the analysts' views, investors should carefully read the entire research report and should not infer its contents from the recommendation. In any case, recommendations should not be used or relied on in isolation as investment advice.

HSBC Global Research is not and does not hold itself out to be a Credit Rating Agency as defined under the Hong Kong Securities and Futures Ordinance.

Definitions for fundamental credit recommendations Overweight: The credits of the issuer are expected to outperform those of other issuers in the sector over the next six months

Neutral: The credits of the issuer are expected to perform in line with those of other issuers in the sector over the next six months

Underweight: The credits of the issuer are expected to underperform those of other issuers in the sector over the next six months

Prior to 1 July 2007, HSBC applied a recommendation structure in Europe that ranked euro- and sterling-denominated bonds and CDS relative to the relevant iBoxx/iTraxx indices over a 3-month horizon.

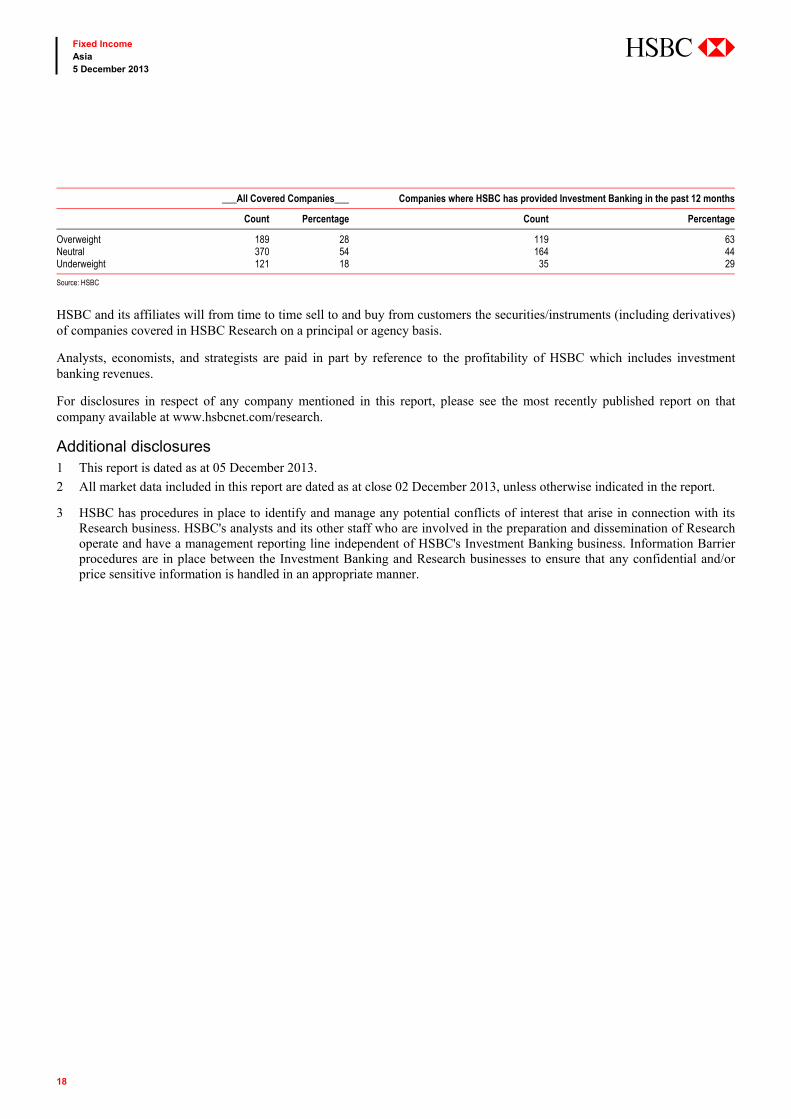

Distribution of fundamental credit opinions As of 03 December 2013, the distribution of all credit opinions published is as follows:

18

Fixed Income Asia 5 December 2013

abc

___All Covered Companies___ Companies where HSBC has provided Investment Banking in the past 12 months

Count Percentage Count Percentage

Overweight 189 28 119 63Neutral 370 54 164 44Underweight 121 18 35 29

Source: HSBC

HSBC and its affiliates will from time to time sell to and buy from customers the securities/instruments (including derivatives) of companies covered in HSBC Research on a principal or agency basis.

Analysts, economists, and strategists are paid in part by reference to the profitability of HSBC which includes investment banking revenues.

For disclosures in respect of any company mentioned in this report, please see the most recently published report on that company available at www.hsbcnet.com/research.

Additional disclosures 1 This report is dated as at 05 December 2013.

2 All market data included in this report are dated as at close 02 December 2013, unless otherwise indicated in the report.

3 HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

19

Fixed Income Asia 5 December 2013

abc

Disclaimer * Legal entities as at 8 August 2012 ‘UAE’ HSBC Bank Middle East Limited, Dubai; ‘HK’ The Hongkong and Shanghai Banking Corporation Limited, Hong Kong; ‘TW’ HSBC Securities (Taiwan) Corporation Limited; 'CA' HSBC Bank Canada, Toronto; HSBC Bank, Paris Branch; HSBC France; ‘DE’ HSBC Trinkaus & Burkhardt AG, Düsseldorf; 000 HSBC Bank (RR), Moscow; ‘IN’ HSBC Securities and Capital Markets (India) Private Limited, Mumbai; ‘JP’ HSBC Securities (Japan) Limited, Tokyo; ‘EG’ HSBC Securities Egypt SAE, Cairo; ‘CN’ HSBC Investment Bank Asia Limited, Beijing Representative Office; The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch; HSBC Securities (South Africa) (Pty) Ltd, Johannesburg; HSBC Bank plc, London, Madrid, Milan, Stockholm, Tel Aviv; ‘US’ HSBC Securities (USA) Inc, New York; HSBC Yatirim Menkul Degerler AS, Istanbul; HSBC México, SA, Institución de Banca Múltiple, Grupo Financiero HSBC; HSBC Bank Brasil SA – Banco Múltiplo; HSBC Bank Australia Limited; HSBC Bank Argentina SA; HSBC Saudi Arabia Limited; The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch incorporated in Hong Kong SAR

Issuer of report

The Hongkong and Shanghai Banking Corporation Limited Level 19, 1 Queen's Road Central

Hong Kong SAR

Telephone: +852 2843 9111

Telex: 75100 CAPEL HX

Fax: +852 2801 4138

Website: www.research.hsbc.com

The Hongkong and Shanghai Banking Corporation Limited (“HSBC”) has issued this research material. The Hongkong and Shanghai Banking Corporation Limited is regulated by the Hong Kong Monetary Authority. This material is distributed in the United Kingdom by HSBC Bank plc. In Australia, this publication has been distributed by The Hongkong and Shanghai Banking Corporation Limited (ABN 65 117 925 970, AFSL 301737) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). Where distributed to retail customers, this research is distributed by HSBC Bank Australia Limited (AFSL No. 232595). These respective entities make no representations that the products or services mentioned in this document are available to persons in Australia or are necessarily suitable for any particular person or appropriate in accordance with local law. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. This publication is distributed in New Zealand by The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch incorporated in Hong Kong SAR. This material is distributed in Japan by HSBC Securities (Japan) Limited. HSBC Securities (USA) Inc. accepts responsibility for the content of this research report prepared by its non-US foreign affiliate. All US persons receiving and/or accessing this report and intending to effect transactions in any security discussed herein should do so with HSBC Securities (USA) Inc. in the United States and not with its non-US foreign affiliate, the issuer of this report. In Korea, this publication is distributed by either The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch ("HBAP SLS") or The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch ("HBAP SEL") for the general information of professional investors specified in Article 9 of the Financial Investment Services and Capital Markets Act (“FSCMA”). This publication is not a prospectus as defined in the FSCMA. It may not be further distributed in whole or in part for any purpose. Both HBAP SLS and HBAP SEL are regulated by the Financial Services Commission and the Financial Supervisory Service of Korea. In Singapore, this publication is distributed by The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch for the general information of institutional investors or other persons specified in Sections 274 and 304 of the Securities and Futures Act (Chapter 289) (“SFA”) and accredited investors and other persons in accordance with the conditions specified in Sections 275 and 305 of the SFA. This publication is not a prospectus as defined in the SFA. It may not be further distributed in whole or in part for any purpose. The Hongkong and Shanghai Banking Corporation Limited Singapore Branch is regulated by the Monetary Authority of Singapore. Recipients in Singapore should contact a "Hongkong and Shanghai Banking Corporation Limited, Singapore Branch" representative in respect of any matters arising from, or in connection with this report. In the UK this material may only be distributed to institutional and professional customers and is not intended for private customers. It is not to be distributed or passed on, directly or indirectly, to any other person. HSBC México, S.A., Institución de Banca Múltiple, Grupo Financiero HSBC is authorized and regulated by Secretaría de Hacienda y Crédito Público and Comisión Nacional Bancaria y de Valores (CNBV). HSBC Bank (Panama) S.A. is regulated by Superintendencia de Bancos de Panama. Banco HSBC Honduras S.A. is regulated by Comisión Nacional de Bancos y Seguros (CNBS). Banco HSBC Salvadoreño, S.A. is regulated by Superintendencia del Sistema Financiero (SSF). HSBC Colombia S.A. is regulated by Superintendencia Financiera de Colombia. Banco HSBC Costa Rica S.A. is supervised by Superintendencia General de Entidades Financieras (SUGEF). Banistmo Nicaragua, S.A. is authorized and regulated by Superintendencia de Bancos y de Otras Instituciones Financieras (SIBOIF). Any recommendations contained in it are intended for the professional investors to whom it is distributed. This material is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. HSBC has based this document on information obtained from sources it believes to be reliable but which it has not independently verified; HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of HSBC only and are subject to change without notice. The decision and responsibility on whether or not to invest must be taken by the reader. HSBC and its affiliates and/or their officers, directors and employees may have positions in any securities mentioned in this document (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). HSBC and its affiliates may act as market maker or have assumed an underwriting commitment in the securities of any companies discussed in this document (or in related investments), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform banking or underwriting services for or relating to those companies. This material may not be further distributed in whole or in part for any purpose. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. (070905) In Canada, this document has been distributed by HSBC Bank Canada and/or its affiliates. Where this document contains market updates/overviews, or similar materials (collectively deemed “Commentary” in Canada although other affiliate jurisdictions may term “Commentary” as either “macro-research” or “research”), the Commentary is not an offer to sell, or a solicitation of an offer to sell or subscribe for, any financial product or instrument (including, without limitation, any currencies, securities, commodities or other financial instruments). © Copyright 2013, The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited. MICA (P) 118/04/2013, MICA (P) 068/04/2013 and MICA (P) 110/01/2013

abc

Rates EMEA Bert Lourenco Head of Rates Research, EMEA +44 20 7991 1352 [email protected]

Subhrajit Banerjee +44 20 7991 6851 [email protected]

Theologis Chapsalis +44 20 7992 3706 [email protected]

Wilson Chin, CFA +44 20 7991 5983 [email protected]

Di Luo +44 20 7991 6753 [email protected]

Chris Attfield +44 20 7991 2133 [email protected]

Sebastian von Koss +49 211 910 3391 [email protected]

Asia André de Silva, CFA Head of Rates Research, Asia-Pacific +852 2822 2217 [email protected]

Pin-ru Tan +852 2822 4665 [email protected]

Himanshu Malik +852 3941 7006 [email protected]

Dayeon Hong +852 3941 7009 [email protected]

Americas Larry Dyer +1 212 525 0924 [email protected]

Jae Yang +1 212 525 0861 [email protected]

Pablo Goldberg Head of Global Emerging Markets Research +1 212 525 8729 [email protected]

Bertrand Delgado +1 212 525 0745 [email protected]

Gordian Kemen Head of Latin America Fixed Income Research +1 212 525 2593 [email protected]

Victor Fu +1 212 525 4219 [email protected]

Alejandro Mártinez-Cruz +52 55 5721 2380 [email protected]

Credit EMEA Lior Jassur Head of Credit Research, EMEA +44 20 7991 5632 [email protected]

Dominic Kini +44 20 7991 5599 [email protected]

Laura Maedler +44 20 7991 1402 [email protected]

Anna Schena +44 20 7991 5919 [email protected]

Pavel Simacek, CFA +44 20 7992 3714 [email protected]

Reza-ul Karim +44 20 7992 3703 [email protected]

Raffaele Semonella +971 4423 6554 [email protected]

Ivan Zubo +44 20 7991 5975 [email protected]

Asia Dilip Shahani Head of Global Research, Asia-Pacific +852 2822 4520 [email protected]

Zhiming Zhang +852 2822 4523 [email protected]

Devendran Mahendran +852 2822 4521 [email protected]

Philip Wickham +65 6658 0618 [email protected]

Keith Chan +852 2822 4522 [email protected]

Louisa Lam +852 2822 4527 [email protected]

Yi Hu +852 2996 6539 [email protected]

Helen Huang +852 2996 6585 [email protected]

Crystal Zhao +852 2996 6514 [email protected]

Kelly Fu +852 3941 7066 [email protected]

Lan Lan +852 3941 7186 [email protected]

Christopher Li +852 2822 3232 [email protected]

Americas Sarah R Leshner +1 212 525 3231 [email protected]

Sean Glickenhaus +1 212 525 4131 [email protected]

Steven Major, CFA Global Head of Fixed Income Research +44 20 7991 5980 [email protected]

Global Fixed Income Research Team