Facts and figures 2007–08

12

Forests and forestry Facts and figures 2007–08 www.dpi.nsw.gov.au

Transcript of Facts and figures 2007–08

Forests and forestry

Facts and figures2007–08

www.dpi.nsw.gov.au

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

2

Forests NSWN

ORT

HEA

ST

CEN

TRA

LW

ESTE

RN

SOU

THER

N

NO

RTH

ERN

MA

CQU

ARI

E MO

NA

RO

HU

ME

Stat

e Fo

rest

Nat

ive

Har

dwoo

d Pl

anta

tion

Soft

woo

d Pl

anta

tion

Nat

ive

Fore

st R

egio

n Bo

unda

ry

Plan

ted

Fore

st R

egio

n Bo

unda

ry

Corp

orat

e O

�ce

Busi

ness

Ser

vice

Cen

tre

Regi

onal

o�

ce –

Nat

ive

Regi

onal

o�

ce –

Pla

nted

Fore

st C

entr

e

Nur

sery

Wor

ksho

p

Rese

arch

Cas

ino

Cof

fs H

arb

our

Gra

fton

Gle

n In

nes

Inve

rell

Dor

rigo

Kem

pse

y

Wau

chop

e

Wal

cha

Bul

ahd

elah

Bar

adin

eG

unne

dah

Mus

wel

lbro

ok

Mai

tland

Toro

nto

Syd

ney

Dub

bo

Bat

hurs

t

Forb

es

Mos

sVa

le

Bat

eman

s B

ay

Nar

oom

a

Ed

en

Bom

bal

a

Alb

ury

Tum

bar

umb

a

Tum

utB

atlo

w

Yanc

o Nar

rand

era

Wag

ga W

agga

Den

iliq

uin

Dar

eton

NO

RTH

EAST

CEN

TRA

LW

ESTE

RN

SOU

THER

N

NO

RTH

ERN

MA

CQU

ARI

E MO

NA

RO

HU

ME

Stat

e Fo

rest

Nat

ive

Har

dwoo

d Pl

anta

tion

Soft

woo

d Pl

anta

tion

Nat

ive

Fore

st R

egio

n Bo

unda

ry

Plan

ted

Fore

st R

egio

n Bo

unda

ry

Corp

orat

e O

�ce

Busi

ness

Ser

vice

Cen

tre

Regi

onal

o�

ce –

Nat

ive

Regi

onal

o�

ce –

Pla

nted

Fore

st C

entr

e

Nur

sery

Wor

ksho

p

Rese

arch

Cas

ino

Cof

fs H

arb

our

Gra

fton

Gle

n In

nes

Inve

rell

Dor

rigo

Kem

pse

y

Wau

chop

e

Wal

cha

Bul

ahd

elah

Bar

adin

eG

unne

dah

Mus

wel

lbro

ok

Mai

tland

Toro

nto

Syd

ney

Dub

bo

Bat

hurs

t

Forb

es

Mos

sVa

le

Bat

eman

s B

ay

Nar

oom

a

Ed

en

Bom

bal

a

Alb

ury

Tum

bar

umb

a

Tum

utB

atlo

w

Yanc

o Nar

rand

era

Wag

ga W

agga

Den

iliq

uin

Dar

eton

NO

RTH

EAST

CEN

TRA

LW

ESTE

RN

SOU

THER

N

NO

RTH

ERN

MA

CQU

ARI

E MO

NA

RO

HU

ME

Stat

e Fo

rest

Nat

ive

Har

dwoo

d Pl

anta

tion

Soft

woo

d Pl

anta

tion

Nat

ive

Fore

st R

egio

n Bo

unda

ry

Plan

ted

Fore

st R

egio

n Bo

unda

ry

Corp

orat

e O

�ce

Busi

ness

Ser

vice

Cen

tre

Regi

onal

o�

ce –

Nat

ive

Regi

onal

o�

ce –

Pla

nted

Fore

st C

entr

e

Nur

sery

Wor

ksho

p

Rese

arch

Cas

ino

Cof

fs H

arb

our

Gra

fton

Gle

n In

nes

Inve

rell

Dor

rigo

Kem

pse

y

Wau

chop

e

Wal

cha

Bul

ahd

elah

Bar

adin

eG

unne

dah

Mus

wel

lbro

ok

Mai

tland

Toro

nto

Syd

ney

Dub

bo

Bat

hurs

t

Forb

es

Mos

sVa

le

Bat

eman

s B

ay

Nar

oom

a

Ed

en

Bom

bal

a

Alb

ury

Tum

bar

umb

a

Tum

utB

atlo

w

Yanc

o Nar

rand

era

Wag

ga W

agga

Den

iliq

uin

Dar

eton

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

3

Our organisationForests NSW is a public trading enterprise within NSW Department of Primary Industries (NSW DPI), responsible for the sustainable management of more than 2 million hectares of multiple-use native forests and an expanding estate of hardwood and softwood planted forests.

Forests NSW is working to be the best and safest commercial forest manager in Australasia.

Forests NSW key result areas are:

Focus on excellence in profitable and sustainable forest management•Organisational efficiency making optimal use of our assets•Revenue growth•Cost reductions•Simplification of the way we work.•

NSW DPI’s visionProfitable, adaptive and sustainable primary industries building vibrant communities.

NSW DPI’s key result areas are:

Strong economic performance of primary industries•Appropriate access to and wise management of natural resources•Safe, healthy and biosecure industries•A strong voice for primary industries•Excellence in people, innovation and service delivery.•

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

4

Forest statisticsDe

script

ionAu

strali

aNS

WFo

rests

NSW

Tota

l land

area

(milli

on ha

) 77

0 80

2.5To

tal p

opula

tion (

milli

on)

217

n/a

Fore

sts as

a pe

rcent

age o

f land

area

19%

33%

>99

%To

tal fo

rest

area

(milli

on ha

)14

926

.52.5

Nativ

e for

est a

rea (

milli

on ha

)114

726

.22.2

Area

of fo

rest

not l

egall

y res

tricte

d fro

m ti

mbe

r har

vesti

ng 11

319

.92.0

Nativ

e fore

st are

a in f

ormal

natu

re co

nserv

ation

rese

rves (

millio

n ha)

235.1

0.5m

ultipl

e-us

e pub

lic na

tive f

ores

ts (m

illion

ha)

9.42.0

Area

of na

tive p

rodu

ction

fore

st ha

rves

ted a

nnua

lly3

<1%

n/r

2.8%

Plant

ation

fore

st ar

ea (m

illion

ha)

1.97

0.34

0.27

New

area

of pl

anta

tion p

lante

d ha/

year

(ave

rage

2002

-200

6)2

60 12

013

645

7 114

Num

ber o

f peo

ple em

ploye

d in f

ores

t pro

duct

indus

tries

>83

000

>24

000

943

Tota

l exp

orts

of w

ood p

rodu

cts$2

.47 bi

llion

n/r

n/r

Majo

r exp

orts

to

Japan

(38%

), NZ (

17%

) & Ch

ina (1

6%)

n/r

n/r

Tota

l impo

rts of

woo

d pro

ducts

$4.40

billio

nn/

rn/

aM

ajor im

ports

from

NZ (1

9%), C

hina (

10%

) & In

done

sia (8

%)

n/r

n/a

Fore

sts co

ntrib

ution

to G

DP1%

n/r

n/r

Net a

mou

nt of

carb

on se

ques

tere

d (m

illion

tonn

es) b

y m

anag

ed na

tive f

ores

ts pe

r ann

um (e

-CO 2)4

43.5

n/r

4.2

Value

of tu

rnov

er in

fore

st pr

oduc

ts ind

ustri

es (b

illion

)19

n/r

0.31 In

clude

s nati

ve fo

rest re

mnan

ts wi

thin

plante

d fore

st es

tate f

or Fo

rests

NSW

2 Austr

alia’s

Plan

tation

s 200

8 Inv

entor

y figu

re for

NSW

2007

3 Fores

t NSW

only

remov

es a

propo

rtion

of th

e tree

s ove

r the

harve

sted a

reas, e

xcept

for C

ypres

s pine

(26%

)4 Au

strali

an fig

ure fro

m 20

05So

urces:

DAFF

State

of th

e Fore

sts Re

port

2008

, Fore

sts NS

W Se

eing R

eport

2007

-08,

Austr

alian

Burea

u of S

tatist

ics, D

AFF N

ation

al Pla

ntatio

n Inv

entor

y - 20

08

n/a:

Not a

pplic

able

n/r:

Not r

epor

ted

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

5

Economic benefits1.4 million hectares of native State forest available for timber harvesting•Over 7 700 hectares of new softwood plantation established•2.9 million m• 3 of sawlogs and 1.8 million tonnes of pulpwood harvested More than 690 000 greenhouse gas abatement certificates created, •representing the equivalent number of tonnes of CO2 stored100% of eligible plantations accredited for carbon trading•$24 400 profit per employee•

Timber productForests NSW main timber products are:

Hardwood17 000 m3/pa veneer805 000 m3/pa sawlogs606 000 tonnes/pa pulpwood

Softwood2 100 000 m3/pa sawlogs1 164 000 tonnes/pa pulpwood

Hardwood timber products Softwood timber products

0

10

20

30

40

50

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

0

10

20

30

40

50

60

70

80

Perc

enta

ge (%

)

Perc

enta

ge (%

)

Dry s

truct

ural

7%

Join

ery /

furn

iture

6%

Deck

ing

/ pan

ellin

g 6

%

Hous

e fra

min

g 14

%

Palle

ts 9

%

High

stre

ngth

stru

ctur

al 2

%

Fenc

ing

/ Lan

dsca

pe 8

%

Floor

boar

ds 4

8%

Hous

e fra

min

g 7

3%

Join

ery /

furn

iture

1%

Deck

ing

/ pan

ellin

g 6%

Floor

boar

ds /

bear

ers/j

oists

3%

Fenc

ing

/ Lan

dsca

pe 6

%

Othe

r pre

serv

atio

n 4%

Unse

ason

ed 7

%

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

6

Forests NSW major customersManufacture area Customer Products/ServicesPlywood Ausply, Big River Timbers and

Carter Holt Harvey Plywood flooring & stairs, structural bracing, Formply (concrete construction) and external cladding

Major softwood sawmillers

Auswest, Carter Holt Harvey, Colenden, Dale & Mayers, Highland Pine, Hyne & Son, Penrose Pine, Tarmac and Willmott Forest Products

Structural softwood timber for dwelling construction and renovation markets, internal joinery (e.g. windows and architraves) and furniture timbers, landscape timbers, treated softwood poles and treated decking

MDF and particleboard

Carter Holt Harvey and Monsbent Medium Density Flooring and particleboard products such as flooring, cabinets, bench tops and furniture

Softwood preservation

Pacpine, Penrose Pine and Wilmott Timbers

Treated timber for outdoor applications such as decks, pergolas and landscape timbers

Pulp and paper Midway, Sawmillers Export Pty Ltd, Norske Skog, Pentarch, Queensland Commodity Exports, South East Fibre Exports and Visy

Newsprint, writing paper, cardboard, tissues and paper towels

Major hardwood sawmillers

Australian Solar Timbers, Big River Timbers, Blue Ridge Hardwoods, Boral, Coffs Harbour Hardwoods, Davis & Herbert, Gunnedah Timbers, Grants Holdings, Gulpa Sawmill, Hurfords, ITC Timber, Koppers, Notaras J & Sons and Thora

Kiln dried and green structural timber, strip flooring, furniture and joinery timber, bridge and engineering timber products, power poles, plywood products and external cladding decking

Investors Agriwealth, ST Microelectronics and TEPCO

Plantation investment

Utilities and infrastructure

Country Energy, Crown Castle, Optus, Telstra and Vodafone

Telecommunications and electricity supplier

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

7

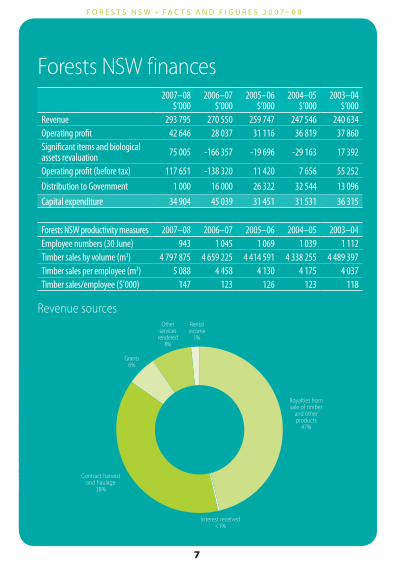

2007–08 $‘000

2006–07 $‘000

2005–06 $‘000

2004–05 $‘000

2003–04 $‘000

Revenue 293 795 270 550 259 747 247 546 240 634Operating profit 42 646 28 037 31 116 36 819 37 860Significant items and biological assets revaluation 75 005 -166 357 -19 696 -29 163 17 392

Operating profit (before tax) 117 651 -138 320 11 420 7 656 55 252Distribution to Government 1 000 16 000 26 322 32 544 13 096Capital expenditure 34 904 45 039 31 451 31 531 36 315

Forests NSW finances

Forests NSW productivity measures 2007–08 2006–07 2005–06 2004–05 2003–04Employee numbers (30 June) 943 1 045 1 069 1 039 1 112Timber sales by volume (m3) 4 797 875 4 659 225 4 414 591 4 338 255 4 489 397Timber sales per employee (m3) 5 088 4 458 4 130 4 175 4 037Timber sales/employee ($’000) 147 123 126 123 118

Revenue sourcesRental

income 1%

Other services

rendered 8%

Grants 6%

Contract harvest and haulage

38%

Royalties from sale of timber

and other products

47%

Interest received <1%

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

8

Social benefits 943 people directly employed by Forests NSW, with more than •6 000 forest-dependent jobs and 14 000 indirect employment$7.58 million spent on research•786 regional forums attended by Forests NSW staff•104 meetings health and safety meetings staged•More than 31 000 public enquiries addressed•More than $120 000 in corporate sponsorships and support•4 171 people participating in programs at Cumberland State Forest•141km of dedicated mountain bike tracks developed & maintained•

Forest sector employment dependant on State forestsHarvesting / Haulage 1 087Primary processing 4 483Apiary 352Grazing 530Eco-tourism 10Other 52Forest Management 947Total direct employment 7 461Estimated Indirect employment 14 000

Forests NSW Safety Performance (Frequency Rate)*

2002-03 3.6

2003-04 2.8

2004-05 3.1

2005-06 2.7

2006-07 3.3

2007-08 4.5* Number of Lost Time Incidents per 200 000 hours worked

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

9

Environmental benefitsTotal forest estate over 2.49 million hectares•1.99 million hectares of native forests managed•2• 053 sightings of 34 targeted species during pre-harvest surveys Almost $10 million spent on firefighting and bushfire prevention•22% of State forests treated by fuel management strategies•More than $1.1 million spent on feral animal control•8 million tonnes additional of CO• 2-equivalent stored in State forests350 000 environmental compliance items checked in 4• 000 internal compliance efforts8.4 million seedlings grown in our nurseries (age-class 2006)•

Wildfires and prescribed burns trend as a percentage of Forests NSW estate

0

1

2

3

4

5

6

Perc

enta

ge (%

)

0

1

2

3

4

5

6

99–00 00–01 01–02 02–03 03–04 04–05 05–06 06–07 07–08

Wildfire percentage of total area

Prescribed burning percentage of total area

Wildfire linear trend

Prescribed burning linear trend

Reporting periods

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

10

Sustainability 1.4 million hectares available for timber production on State forests•

Mean annual increment for softwood plantations 16.3 m• 3/ha/yr and for hardwood plantations 13.6 m3/ha/yr

Actual annual yield of high quality sawlogs as a percentage of allowable volume: •94% native hardwood forests; 96% cypress and 98% softwood plantations.

What does sustainability mean for Forests NSW?Managing State forests for the long term and retaining opportunities for future generations to meet their needs and expectations, while providing for the present.

Forest Management CertificationForests NSW maintained certification to the Australian Forestry Standard (AFS).

AFS gives independent assurance that Forests NSW management of NSW forests is consistent with internationally recognised principles of sustainable forest management.

Timber buyers wanting an assurance of sustainability should choose timber products displaying the logo for AFS and its over-arching scheme, Programme for the Endorsement of Forestry Certification (PEFC).

ph

oto

sy

nt

he

sis

CO

2 is sequestered

Gr

ow

. Ha

rv

es

t. st

or

e...

Fo

re

st

s –

pa

rt

oF

tH

e c

lim

at

e c

Ha

nG

e s

ol

ut

ion

Re

CyC

LinG

Dis

po

sA

L

Litter and other forest biom

ass

So

il organ

ic matter

Deco

mp

ositio

n

respiratio

n

Anim

als excretion

Carb

on

store

tiM

Be

Rh

AR

Ve

st

inG

Litte

R

LAye

R

FiRe

tiM

Be

Rp

Ro

Ce

ss

inG

tiM

Be

Rp

Ro

DU

Ct

s

LeG

en

DCapturing C

arbon

Releasing C

arbon

Moving carbon

en

eR

Gy

Fos

siL FU

eLs

F O R E S T S N S W • F A C T S A N D F I G U R E S 2 0 0 7 – 0 8

This document has been prepared as a summary. More detailed information can be viewed in Forests NSW Annual and Seeing (Sustainability) Reports online at www.dpi.nsw.gov.au/forests

For more information or copies of these documents contact Forests NSW Information Centre

T 1300 655 687 or 02 9871 3377

W www.dpi.nsw.gov.au/forests

This Facts and Figures is one of a set of summaries relating to primary industries in New South Wales. For details on agriculture, mineral resources and fisheries management in NSW see NSW Department of Primary Industries website www.dpi.nsw.gov.au

DPI

JN 9

297