Factors Influencing the User Behaviour Intention of Online ...

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

17

FACTORS INFLUENCING CONSUMER INTENTION TOWARDS

INVESTMENT ACCOUNT: POST IFSA 2013

Azharul Adha Dzulkarnain

Universiti Teknologi MARA, Shah Alam, Malaysia

Mohammad Firdaus Mohammad Hatta

Universiti Teknologi MARA, Shah Alam, Malaysia

Abstract

This study aims to analyse the factors influencing consumer intention towards investment

account post Islamic Financial Services Act 2013 (IFSA). The establishment of IFSA

reclassify the deposit product to deposit and investment account. During Islamic Banking

Act 1983 (IBA), all monies accepted from depositors considered as deposit product. The

IFSA promote risk sharing instead of risk transfer. However, the investment account

shows the depletion since the introduction of IFSA in 2013. A consumer survey

comprises of 106 Muslim respondents from various ages, occupations, incomes, and

education levels. Religiosity, social influence, and knowledge have been selected as

factors that influence the consumer intention towards investment account. The theoretical

framework constructed based on past studies. This study applied multiple regression

analysis to test the hypothesis statement. The finding indicates the religiosity is the

primary factor influencing the consumer intention, followed by social influence.

However, the knowledge found no significant relationship with consumer intention.

Following these results, the researcher suggest the Islamic bank can look into religiosity

and social factor to strategize the development of products and in marketing activities.

Besides, the BNM and Islamic financial agencies need to endeavor to create positive

attitudes among consumer towards Islamic investment account post IFSA.

Keywords: Influencing; consumer intention; investment; IFSA 2013

Introduction

The Islamic Financial Services Act 2013 (IFSA) differentiates investment account

from Islamic deposit. Investment account is demarcated by the usage of Shariah contracts

(Hamza, 2013). The author further explains that the investment account has non-principal

guarantee feature for investment nature deposit. According to the author, the IFSA offers

adequate legal basis to upkeep the further solidification of investment account process

that provides proper protection to investment account holders (IAH) whilst safeguarding

financial stability of the Islamic banking system. Under the IFSA, the urgency of payment

for investment deposit account upon insolvency of the Islamic financial institution (IFI) is

treated separately from Islamic deposit, in accordance with the rights and obligations

accrued to the IAH (Hamza, 2013).

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

18

As per BNM’s Investment Account Policy, the new classification of the existing

deposit products shall take effect commencing on 1 July 2015. As for profit, the

investment account commensurate with the risk taken. The Islamic bank did not offer the

product if they think the product did not meet the consumer demand. Furthermore, the

demand of consumer will affect the performance of Islamic bank. As consumer intention

represents one of the indicators that explain the performance in an organization, hence

monitoring consumer intention and its related situation become more crucial (Awan &

Azhar, 2014).

As these issues, problem, and information demonstrate, consumer intention towards

investment account post IFSA is the important thing to look in Islamic banking industry.

This study, hence, aims to gauge the consumer intention towards investment account post

IFSA, which should be considered as an important contribution in filling the observed gap

in the literature.

Overview – Investment Account Post IFSA 2013

Islamic Banking and Takaful Department, Bank Negara Malaysia issued the

policy on 14 March 2014 to define the investment account distinguishes from Islamic

deposit, where investment account is defined by the application of Shariah contracts with

non-principal guarantee feature for the purpose of investment. Notwithstanding this, the

IFSA provides adequate legal basis to support the further strengthening of investment

account operation that provides appropriate protection to investment account holders

(IAH) whilst ensuring financial stability of the Islamic financial system. Under the IFSA,

the priority of payment for investment account upon liquidation of the Islamic financial

institution (IFI) is treated separately from Islamic deposit, in accordance with the rights

and obligations accrued to the IAH. Previously during IB 1983, all monies accepted

considered as deposit.

Isa & Zabid (2015) explain further that the IFSA distinguish deposits made for

saving - where the principal is guarantee from those made for investments - where the

principal is not guarantee. It gives regulators greater oversight over Islamic scholars

whose duties and functions are for advising to assure that Islamic financial products are in

compliance with shariah. Bank Negara Malaysia on the website dated 17 May 2016

announces Investment Account is a new banking product offered by Islamic banking

institutions. It provides the opportunity for the customer to invest and share the profits

from Shariah-compliant investment account. Investment account caters for a wide range

of investor risk return preferences that reflect the underlying assets performance.

Investors have the option of placing the funds in investment account that match their risk

appetite.

Thajudeen (2013) stated that the main difference pre and post IFSA is the clear

definition of what constitutes a deposit and what goes into an investment account. The

deposit account is guaranteed, while money that is put into an investment account such as

wakalah or mudharabah is not guaranteed. With IFSA the Profit Equalization Ratio (PER)

and PIDM insurance backing is no longer available for Mudharabah investment accounts.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

19

Consumer Intention

Generally, the consumer is the king of the market, the one that dominates

the market and the market trends. The consumer plays a very important role in the

demand and supply of economic system for any industry. Md Husin & Abd Rahman

(2016) explained that marketers should identify and understand the potential consumers.

They suggested that the higher individual awareness, knowledge, or exposure will have

positive attitude and intention towards takaful participants. They also added that the

participation in takaful with ease will have a positive impact on intentions as well as

behaviour.

In discussing the consumer intention, it is important to understand the reason how

the intention can affect the performance of an organization. Ghosh (1990) stated that

purchase intention is an effective tool use in predicting purchasing process. Once the

consumers decide to purchase the product in certain store, they will be driven by their

intention. Thu Ha & Gizaw (2014) further explained that the interpretation and decision

making is different among individuals and also influenced by internal consumer intention

(perception, attitude, motivation) and external factors (family roles, peer influence, group

influence). Individuals have exposed to different window of information and varieties of

products; many great deal of choices and options available in the market place impulse

their purchase decision.

The consumer intention has always been discussed extensively and is being studied

by many researchers even today. Previous researchers like Reni & Ahmad (2016) study

the intention to use Islamic banking in Indonesia and found five factors significant

relations which were attitude, subjective norm, religion, knowledge, and pricing. Alam,

Janor, Zanariah, Che Wel, & Ahsan (2012) analyze the religiosity factor to undertake

Islamic Home Financing in Klang Valley by using Theory Planned Behaviour (TPB) as

underlying theory and discovered relationship between religion, subjective norm, attitude,

and perceived behavioral control towards intention. While study by Rani (2014) conclude

the identifying and understanding the factors that influence the customers, brands have

the opportunity to develop a strategy, a marketing message (Unique Value Proposition)

and advertising campaigns more efficient and more in line with the needs and ways of

thinking of the target consumers, a real asset to better meet the needs of its customers, and

increase sales.

Researchers like Ali, Raza, & Puah (2015) further discussed matters surrounding

the Islamic home financing facility which relates to intention using TPB model as

underlying theory. All these studies signify the importance of research on consumer

intention or intention subject.

Religiosity

Ahmed & Haroon (2002) found that religion is an important factor in Islamic

banking. Muslims take Islamic banking as an ethical banking theory because it is interest

free banking and interest is prohibited in Islam that’s why they like Islamic banking

system as compared to conventional banking. They also found that Islamic banking is not

only popular in Muslims even non-Muslims having much information about the Islamic

banking system.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

20

Research on the factor influence customer to patron Islamic bank by Idris, Naziman,

Januri, Asari, Muhammad, Sabri, & Jusoff (2011) found that the religious value is the

most important factor in selecting Islamic bank followed by other factor. This finding is

in line with the previous studies by Metawa & Almossawi (1998). Other studies with

conclusion that support the religious factor are Gait & Andrew (2008) with finding the

religion factor is the primary motivation for the potential use of Islamic methods of

finance. Akhtar & Mehmood (2016) indicates that the religion factor has strong impact on

perception of customers in Islamic banking by using regression analysis. Research by

Imtiaz, Murtaza, Abaas, & Hayat (2013) conducted in the case of Pakistan support the

religion is primary and main factor of motivation to choose an Islamic banking system.

However, Tara, Irshad, Khan, Yamin, & Rizwan (2014) research in Pakistan focus on

adoption of Islamic banking found that the religion is not the most influential factor to

switch from conventional to Islamic banking. The study found religion as the third

influence factor behind financial teaching of Islam and reputation to adopt Islamic

banking in Pakistan.

There are various past studies that also look at the relationship between religion and

consumer intention towards Islamic banking product or services. Research by Mansor,

Masduki, Zulkarnain, & Aziz (2015) on Muslim’s preferences towards takaful product in

Malaysia investigates the causal relationship between consumer awareness, perception,

and religiosity towards Muslim’s preferences towards takaful product . The results

showed a positive significant between religion and perception towards Muslim’s

preferences. According to research by Abduh, Kassim, & Dahari (2013), the variable of

religion found to be statistically significant in influencing consumer switching intention

due to non-sharia compliance issues.

Social Influence

Sethi & Chawla (2014) reveals the social factors that influence the consumer

buying behavior includes reference groups, immediate family members, relatives, role in

the society, and social status. According to the authors, the family has the very important

role and influence in the buying behavior of the consumers that includes parents,

husband, wife, and children.

With the spirit of helping the economy of the ummah, Muslim consumers tend to

give their support to Muslim products. According to research by Fauzi, Mokhtar, &

Yusoff (2015), the result shown that Muslim products has a significant impact on the

patronage-intention of Muslim consumers. Muslim consumers have shown their social

responsibility in supporting the economics of the ummah and the responsibility to buy

local products (Al-Ajmi, Hussain, & Al-Salleh, 2009).

Social influence also said to have the positive relationship with consumer intention.

The intention can be changes depend on the world around us and how it works. Study by

Echchabi & Azouzi (2015) found that normative belief have a significant influence on

subjective norm, by particular reference to the parents, siblings, peers, and colleagues as

the main reference groups. The finding explains all the TPB have a significant impact on

the intention to adopt Islamic banking services in Tunisia. The study supports the TPB as

an underlying theory towards consumer intention.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

21

According to Iuliana, Munthiu, & Radulescu (2012), social factors that influence

consumer intention are family, social roles, and statuses. Another study by Echchabi &

Olaniyi (2012) on the patronisation intention of Islamic banks’ customer in Malaysia

market indicated that there is a positive relationship between subjective norm and attitude

on the intention to adopt Islamic banking services. The result showed the normative belief

and motivation to comply have a significant positive influence on the subjective norm.

Based on Haque, Osman, & Ismail (2009) findings, social and religious factor

expected to have great role for influencing customer mind. The impact on customer

preferences can affect the bank performance. Social and religious factor could make

Islamic banking easier and comfortable. Another study by Ali & Hong (2015), have

worked on factor affecting intention to use Islamic personal financing using modified

Theory Reasoned Action (TRA) model. Social influence and attitude found no

relationship with the intention. The significant factors are pricing, religiosity, and

government support.

Knowledge

Past studies like Loo (2010) found that Muslim respondent understanding towards

Islamic banking services influence their perception and attitudes. According to Abbas &

Kadir (2013), the product knowledge among academician and non-academician

specifically in Higher Education Institutions in Pahang are still low. They suggest Islamic

bank to put more effort in promoting the product and services. Harun, Abd Rashid, &

Hamed (2015) research for the products’ knowledge among Islamic banking employees

showed a significance influence relationship between understanding underlying principles

and product knowledge. According to their study, the employees itself should have

product knowledge to attract customer. Moreover, Islamic banking products do not just

focus among the Muslim customer but non-Muslim as well. Another research done by

Obeid & Kaabachi (2016) found that the amount of information as a second important

factor after religiosity to adopt the Islamic banking services. The clear understanding of

Islamic financial concept needed to enhance the motivation to use it.

Mehtab, Zaheer, & Ali (2015) have worked on knowledge, attitudes, and practice

on Islamic banking at Pesahawar, Pakistan by using attitude as mediating variable

between knowledge and practice. The study revealed that there is significant relationship

existed between the knowledge and practice of Islamic banking. However, the individual

must have positive attitude because if they have knowledge but with negative attitude, it

would impact the intention to practice Islamic banking. Other study by Bley & Kuehn

(2004), investigates the relationship between university students’ knowledge of relevant

financial concepts and terms in conventional and Islamic banking, the impact of religion

and language, and other individual variables on preferences for financial services. The

study found that the knowledge is not the strongest factor on preference for Islamic

banking services. The strongest factor is the religiosity.

According to Noonari, Memon, Mangi, Pathan, Khajjak, & Jamali (2015),

consumer need to be facilitating with the understanding of Islamic products and making

the comparability with similar conventional products easier will help consumers make

better choices. This is to ensure the long term growth and prosperity of the Islamic

finance sector. Study by Wahyuni (2012) found that with better knowledge has greater

intention to use the Islamic banks. These results also indicate that the knowledge variable

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

22

must be considered in building a model of the behavior of a selection or use of products,

including Islamic banks.

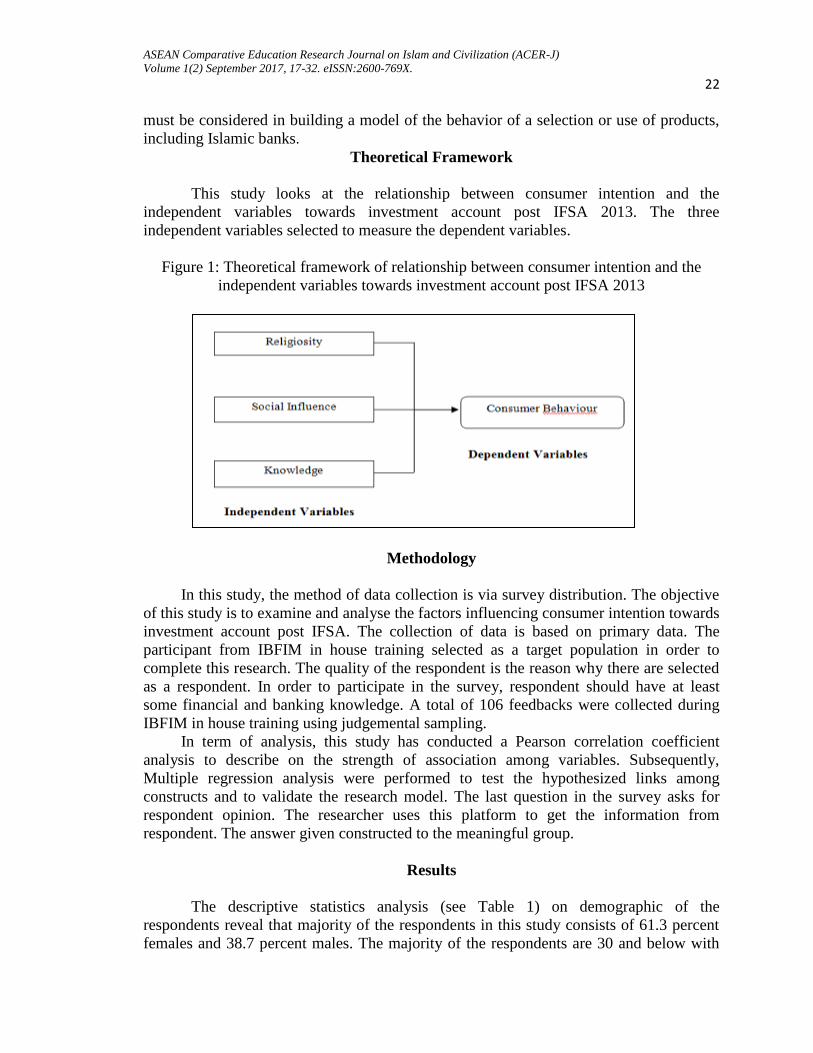

Theoretical Framework

This study looks at the relationship between consumer intention and the

independent variables towards investment account post IFSA 2013. The three

independent variables selected to measure the dependent variables.

Figure 1: Theoretical framework of relationship between consumer intention and the

independent variables towards investment account post IFSA 2013

Methodology

In this study, the method of data collection is via survey distribution. The objective

of this study is to examine and analyse the factors influencing consumer intention towards

investment account post IFSA. The collection of data is based on primary data. The

participant from IBFIM in house training selected as a target population in order to

complete this research. The quality of the respondent is the reason why there are selected

as a respondent. In order to participate in the survey, respondent should have at least

some financial and banking knowledge. A total of 106 feedbacks were collected during

IBFIM in house training using judgemental sampling.

In term of analysis, this study has conducted a Pearson correlation coefficient

analysis to describe on the strength of association among variables. Subsequently,

Multiple regression analysis were performed to test the hypothesized links among

constructs and to validate the research model. The last question in the survey asks for

respondent opinion. The researcher uses this platform to get the information from

respondent. The answer given constructed to the meaningful group.

Results

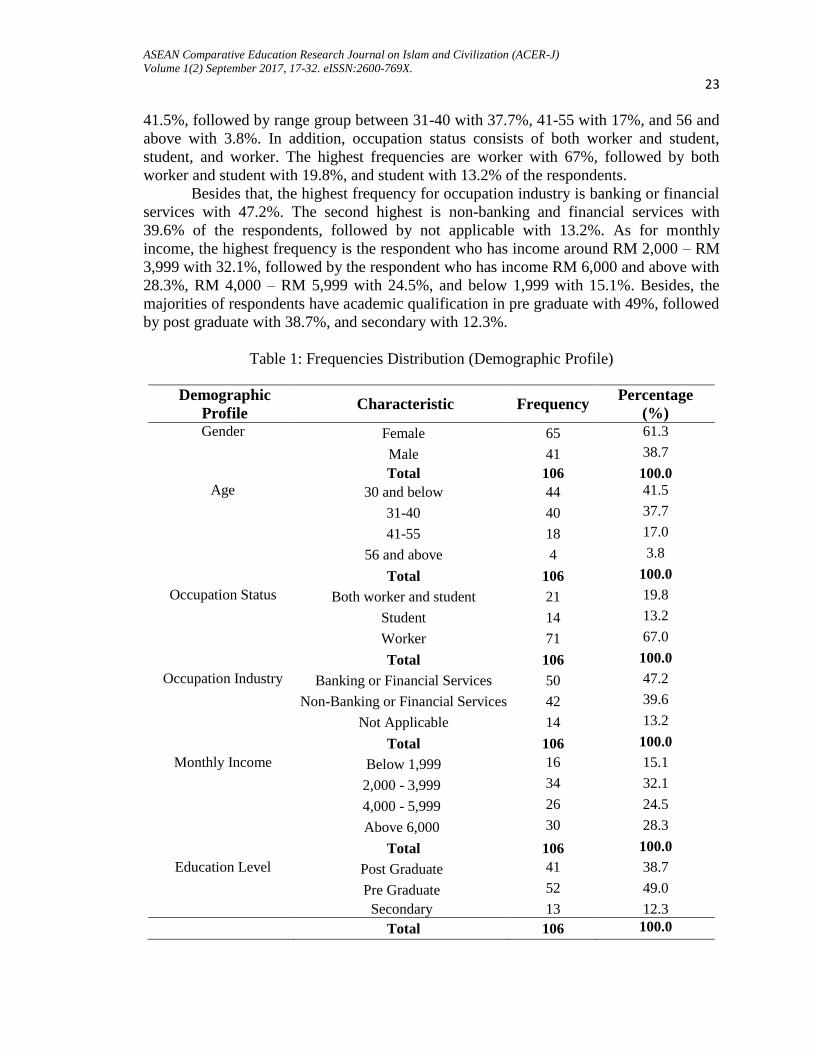

The descriptive statistics analysis (see Table 1) on demographic of the

respondents reveal that majority of the respondents in this study consists of 61.3 percent

females and 38.7 percent males. The majority of the respondents are 30 and below with

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

23

41.5%, followed by range group between 31-40 with 37.7%, 41-55 with 17%, and 56 and

above with 3.8%. In addition, occupation status consists of both worker and student,

student, and worker. The highest frequencies are worker with 67%, followed by both

worker and student with 19.8%, and student with 13.2% of the respondents.

Besides that, the highest frequency for occupation industry is banking or financial

services with 47.2%. The second highest is non-banking and financial services with

39.6% of the respondents, followed by not applicable with 13.2%. As for monthly

income, the highest frequency is the respondent who has income around RM 2,000 – RM

3,999 with 32.1%, followed by the respondent who has income RM 6,000 and above with

28.3%, RM 4,000 – RM 5,999 with 24.5%, and below 1,999 with 15.1%. Besides, the

majorities of respondents have academic qualification in pre graduate with 49%, followed

by post graduate with 38.7%, and secondary with 12.3%.

Table 1: Frequencies Distribution (Demographic Profile)

Demographic

Profile Characteristic Frequency

Percentage

(%) Gender Female 65 61.3

Male 41 38.7

Total 106 100.0

Age 30 and below 44 41.5

31-40 40 37.7

41-55 18 17.0

56 and above 4 3.8

Total 106 100.0

Occupation Status Both worker and student 21 19.8

Student 14 13.2

Worker 71 67.0

Total 106 100.0

Occupation Industry Banking or Financial Services 50 47.2

Non-Banking or Financial Services 42 39.6

Not Applicable 14 13.2

Total 106 100.0

Monthly Income Below 1,999 16 15.1

2,000 - 3,999 34 32.1

4,000 - 5,999 26 24.5

Above 6,000 30 28.3

Total 106 100.0

Education Level Post Graduate 41 38.7

Pre Graduate 52 49.0

Secondary 13 12.3

Total 106 100.0

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

24

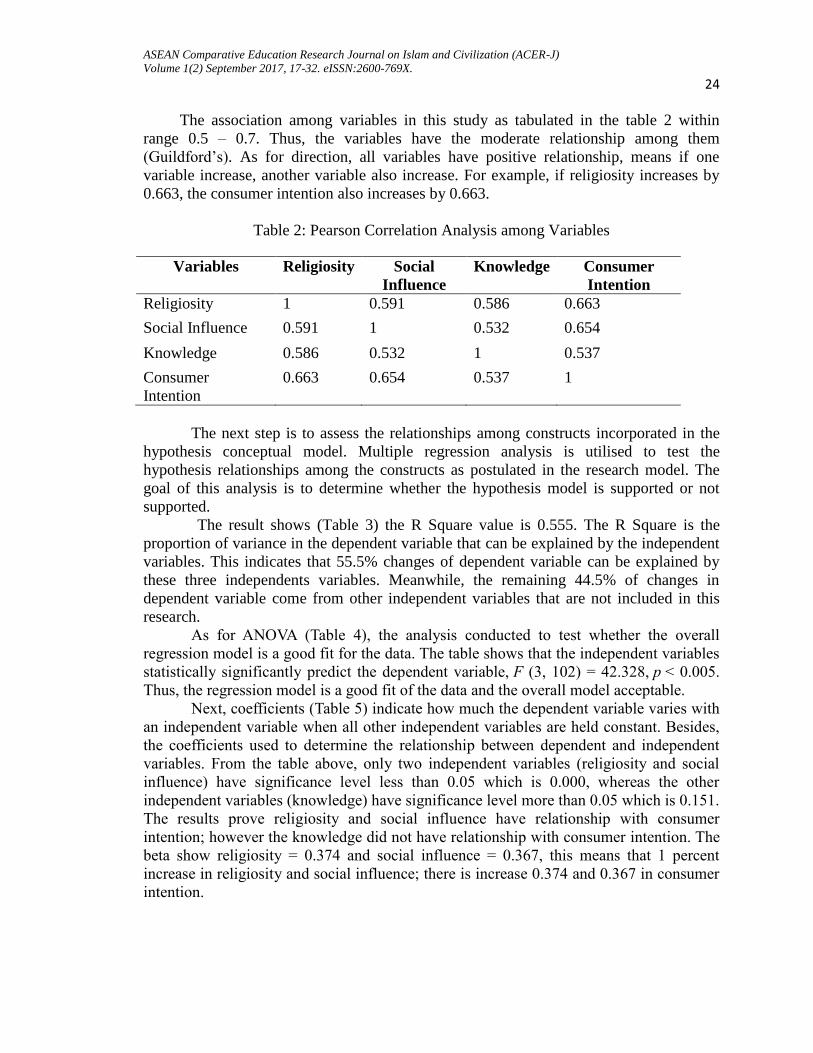

The association among variables in this study as tabulated in the table 2 within

range 0.5 – 0.7. Thus, the variables have the moderate relationship among them

(Guildford’s). As for direction, all variables have positive relationship, means if one

variable increase, another variable also increase. For example, if religiosity increases by

0.663, the consumer intention also increases by 0.663.

Table 2: Pearson Correlation Analysis among Variables

Variables Religiosity Social

Influence

Knowledge Consumer

Intention

Religiosity 1 0.591 0.586 0.663

Social Influence 0.591 1 0.532 0.654

Knowledge 0.586 0.532 1 0.537

Consumer

Intention

0.663 0.654 0.537 1

The next step is to assess the relationships among constructs incorporated in the

hypothesis conceptual model. Multiple regression analysis is utilised to test the

hypothesis relationships among the constructs as postulated in the research model. The

goal of this analysis is to determine whether the hypothesis model is supported or not

supported.

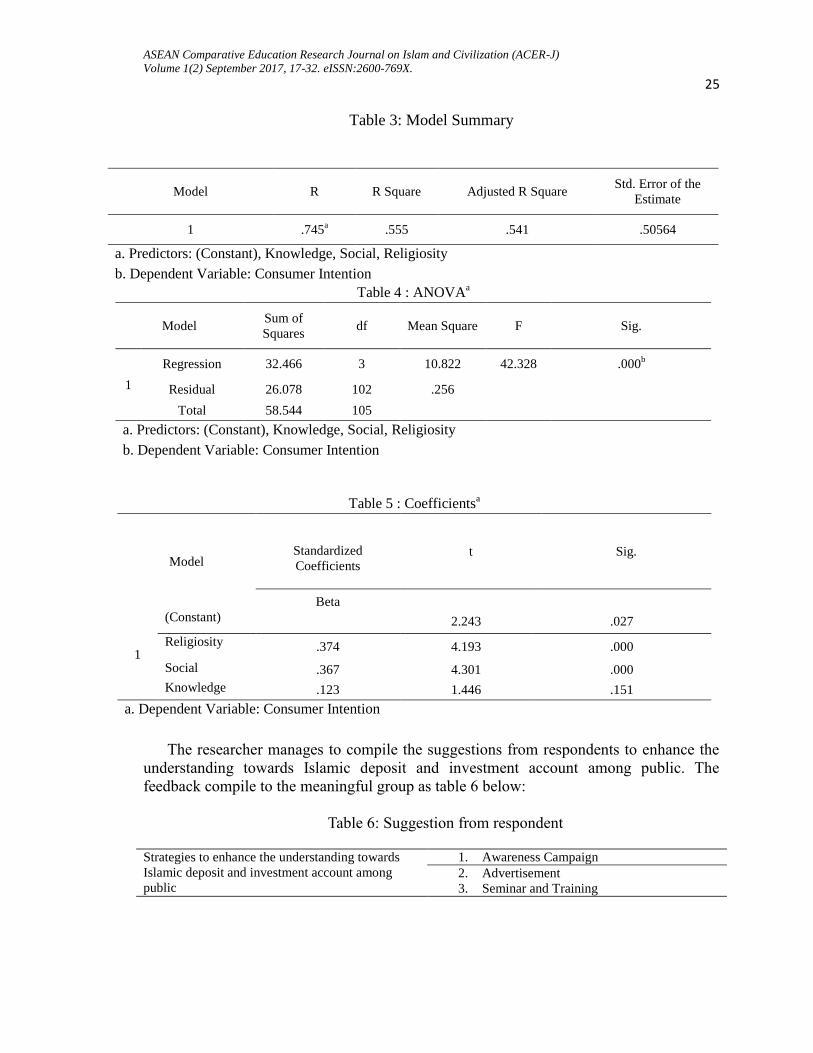

The result shows (Table 3) the R Square value is 0.555. The R Square is the

proportion of variance in the dependent variable that can be explained by the independent

variables. This indicates that 55.5% changes of dependent variable can be explained by

these three independents variables. Meanwhile, the remaining 44.5% of changes in

dependent variable come from other independent variables that are not included in this

research.

As for ANOVA (Table 4), the analysis conducted to test whether the overall

regression model is a good fit for the data. The table shows that the independent variables

statistically significantly predict the dependent variable, F (3, 102) = 42.328, p < 0.005.

Thus, the regression model is a good fit of the data and the overall model acceptable.

Next, coefficients (Table 5) indicate how much the dependent variable varies with

an independent variable when all other independent variables are held constant. Besides,

the coefficients used to determine the relationship between dependent and independent

variables. From the table above, only two independent variables (religiosity and social

influence) have significance level less than 0.05 which is 0.000, whereas the other

independent variables (knowledge) have significance level more than 0.05 which is 0.151.

The results prove religiosity and social influence have relationship with consumer

intention; however the knowledge did not have relationship with consumer intention. The

beta show religiosity = 0.374 and social influence = 0.367, this means that 1 percent

increase in religiosity and social influence; there is increase 0.374 and 0.367 in consumer

intention.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

25

Table 3: Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .745a .555 .541 .50564

a. Predictors: (Constant), Knowledge, Social, Religiosity

b. Dependent Variable: Consumer Intention

Table 4 : ANOVAa

Model Sum of

Squares df Mean Square F Sig.

1

Regression 32.466 3 10.822 42.328 .000b

Residual 26.078 102 .256

Total 58.544 105

a. Predictors: (Constant), Knowledge, Social, Religiosity

b. Dependent Variable: Consumer Intention

Table 5 : Coefficientsa

Model Standardized

Coefficients

t Sig.

Beta

1

(Constant) 2.243 .027

Religiosity .374 4.193 .000

Social .367 4.301 .000

Knowledge .123 1.446 .151

a. Dependent Variable: Consumer Intention

The researcher manages to compile the suggestions from respondents to enhance the

understanding towards Islamic deposit and investment account among public. The

feedback compile to the meaningful group as table 6 below:

Table 6: Suggestion from respondent

Strategies to enhance the understanding towards

Islamic deposit and investment account among

public

1. Awareness Campaign

2. Advertisement

3. Seminar and Training

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

26

Table 7: Hypothesis Result

Hypothesis Result Significant

Level

Beta

Hypothesis 1: H1: There is a significant relationship between

religiosity and consumer intention

Supported 0.000 0.374

Hypothesis 2:

H2: There is a significant relationship between

social influence and consumer intention

Supported. 0.000 0.367

Hypothesis 3:

H3: There is a significant relationship between

knowledge and consumer intention

Not Supported. 0.151 0.123

Conclusion and Recommendation

Religiosity and social influence are directly impacted the consumer intention and

the Islamic bank tend to be more strategize since studies have proven that the two factors

can affect the consumer intention. Since the objective of IFSA is to promote risk sharing

instead of risk transfer, the Islamic bank should be more open to develop the new product

based on wakalah or mudharabah contract.

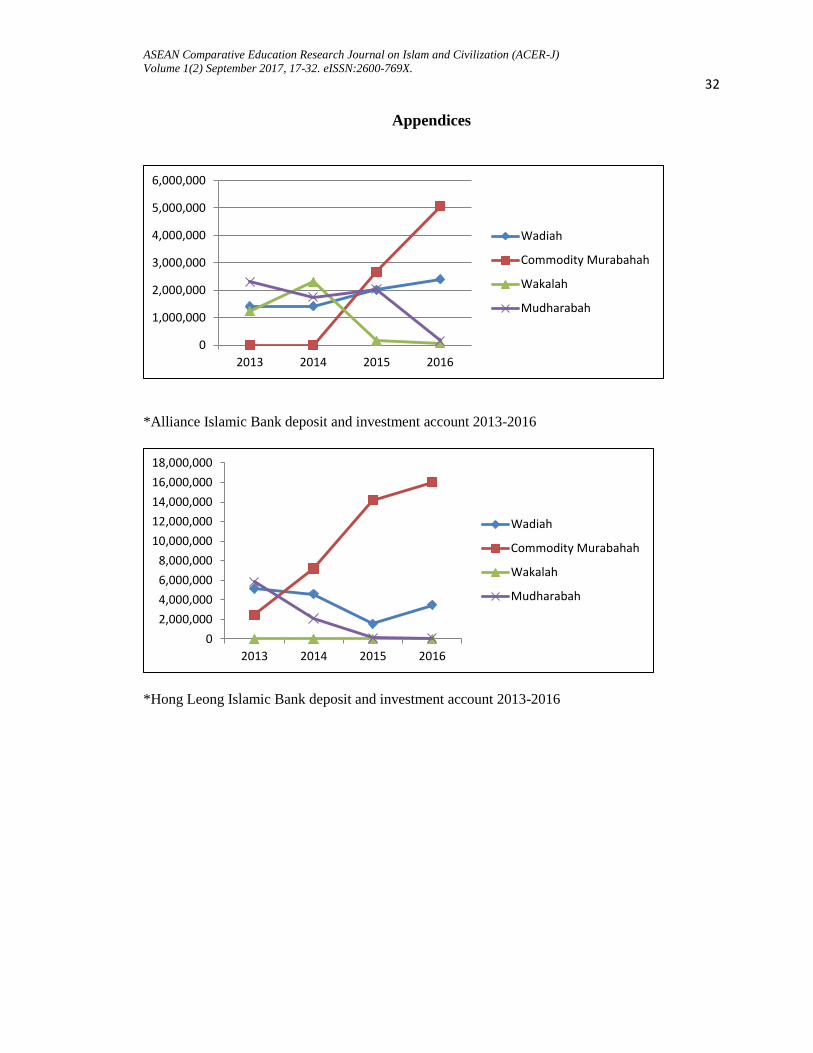

The Islamic bank prefers to develop new product based on commodity murabahah

contract because it can give upfront profit to depositor and PIDM guarantee. The reason

may be to ensure the market share did not loss to conventional market. The researcher

manages to observe the financial statement of Hong Leong Islamic Bank and Alliance

Islamic Bank from 2013 to 2016, found the increase in commodity murabahah account

and the decrease in mudharabah account.

It looks like the strict deposit reclassification by IFSA has made the industry jittery

to Islamic banking concept and marginalized the investment account. Hence, with the

finding from this study, Islamic bank can look into religiosity and social factor to

strategize the development of products and in marketing activities.

The deposit reclassification has impacted the product development of investment

account. This study perhaps will help to give an idea to the BNM and Islamic financial

agencies such as AIBIM and IBFIM to enhance consumer awareness and therefore, some

strategies or policies can be further improved.

Besides, the BNM and Islamic financial agencies need to endeavor to create

positive attitudes among consumer towards Islamic investment account post IFSA. They

can do this by concentrating on the motivational factors that lead to positive or negative

attitudes towards Islamic banking among both Islamic and conventional bank consumers.

This is important as negative attitudes can prevent individuals from opening an account

with an Islamic bank even if they have knowledge of certain Islamic banking principles

(Mehtab, Zaheer, and Ali, 2015). The positive attitudes can influence individuals to select

Islamic products in case of some factor such as religiosity.

Besides, the researcher manages to get some information from respondent regarding

their suggestion to enhance understanding towards Islamic deposit and investment

account post IFSA. The researcher manages to convert suggestions to the meaningful

group which are awareness campaign, advertisement, seminar, and training. The

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

27

respondents want Islamic banking industry to do the awareness campaign related with

Islamic banking product and how they differ with conventional banking. For example,

every year Association of Islamic Banking Institution in Malaysia (AIBIM) with

cooperation from Islamic bank can organize the ‘Islamic Banking Week’ and during the

week, they can conduct many activities such as quiz, information counter booth, and other

activities as long it can create awareness to the public regarding Islamic banking product

and activity.

Other suggestion is to create more advertisement in the media channel to introduce

and familiarize the public with the Islamic banking product and activity. As regulator,

Bank Negara Malaysia (BNM) can take an initiative to produce the short advertisement

regarding Islamic banking industry. The advertisement must be simple and easy to

understand but is full with message and information.

The third suggestion is to conduct seminar or training to enhance consumer

understanding. IBFIM as one of the industry player in Islamic banking can conduct

seminar or training to the government or private sector. During seminar, IBFIM can use

the opportunity to share the information in Islamic banking industry and at least it will

create two way communications about any dispute or less understanding in regards of

Islamic banking.

This study contributes further to the literature of IFSA, Islamic investment account,

consumer intention, religiosity, social influence, and knowledge factor. Furthermore,

researchers may use the findings of this study as reference to continue with further

research in similar area. The researcher suggests future researchers to add attitude as

moderating variable between knowledge and intention as suggested by Mehtab et.al

(2015) and to use the wide area of population.

References

Abbas, R. B., & Abd Kadir, M. R. (2013). Customers Preferences towards Syariah

Compliant Products and Services: The Case Study among Academician and Non

Academician in Higher Education Institutions (HEIs) in Pahang. Jurnal

Muamalat, Bil. 6.

Abduh, M., Kassim, S. H., & Dahari, Z. (2013). Factors Influence Switching Behavior of

Islamic Bank Customers in Malaysia. Journal of Islamic Finance, 12-19.

Abdullah, S. N., Hassan, S. H., & Masron, T. A. (2016). Switching Intention of Muslim

Depositors in Islamic Deposit Account. International Journal of Economics,

Management and Accounting 24, no. 1, 83-106.

Ahmad, N., & Haron, S. (2002). Perceptions of Malaysian corporate customers towards

Islamic banking products and services. International Journal of Islamic Financial

Services, 13-29.

Akhtar, N., & Mehmood, M. T. (2016). Factors Influencing the Perception of Customers

in Islamic Banking: A Case Study in Pakistan. International Review of

Management and Business Research.

Al‐Ajmi, J., Hussain, H. A., & Al‐Saleh, N. (2009). Clients of conventional and Islamic

banks in Bahrain: How they choose which bank to patronize. International

Journal of Social Economics 1086 - 1112.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

28

Alam, S. S., Janor, H., Zanariah, Che Wel, C. A., & Ahsan, M. N. (2012). Is Religiosity

an Important Factor in Influencing the Intention to Undertake Islamic Home

Financing in Klang Valley? World Applied Sciences Journal 19 (7), 1030-1041.

Ali, M., Ali, R. S., & Hong, P. C. (2015). Factors affecting intention to use Islamic

personal financing in Pakistan : Evidence from the modified TRA model. Munich

Personal RePEc Archive, 1-28.

Ali, M., Raza, S. A., & Puah, C. H. (2015). Islamic home financing in Pakistan : A SEM

based approach using modified TPB model. Munich Personal RePEc Archive, 1-

33.

Ali, S., Md Zani, R., & Kasim, K. (2014). Factors Influencing Investors’ Behavior in

Islamic Unit Trust: An Application of Theory of Planned Behavior. Journal of

Islamic Economics, Banking and Finance, 1-19.

Alliance Islamic Bank. (2017). Retrieved May 12, 2017 from

https://www.allianceislamicbank.com.my/AnnualReports

Amin, H. (2013). Some Viewpoints of Islamic Banking Retail Deposit Products in

Malaysia. Journal of Internet Banking and Commerce, 1-13.

Awan, A. G., & Azhar, M. (2014). Consumer Behaviour Towards Islamic Banking in

Pakistan. European Journal of Accounting Auditing and Finance Research, 42-65.

BankIslam. (2017).Retrieved May 12, 2017 from

http://www.bankislam.com.my/home/assets/uploads/AnalystBriefing-

InvestmentAccountANewFrontier.pdf

Bank Negara Malaysia. (2016). Retrieved April 15,2016 from

http://www.bnm.gov.my/?ch=li&cat=islamic&type=IB&lang=en

Bank Negara Malaysia. (2016). Retrieved April 15,2016 from

http://www.bnm.gov.my/index.php?ch=en_publication&en&pub=msbarc

Bickman, L., & J. Rog, D. (1998). Handbook of Applied Social Research Methods. Sage

Publications.

Bley, J., & Kuehn, K. (2004). Conventional Versus Islamic Finance : Student Knowledge

and Perception in the United Arab Emirates. International Journal of Islamic

Financial Services , 1-13.

Cetina, I., Munthiu, M. C., & Radulescu, V. (2012). Psychological and social factors that

influence online consumer. Procedia - Social and Behavioral Sciences 62, 184-

188.

Department, I. B. (2014, March 14). Investment Account Policy. Bank Negara Malaysia.

Echchabi, A., & Azouzi, D. (2015). Predicting customers’ adoption of Islamic banking

services in Tunisia:A Decomposed Theory of Planned Behaviour approach.

Tazkia Islamic Finance and Business Review, 19-40.

Echchabi, A., & Olaniyi, O. N. (2012). Using Theory of Reasoned Action to model the

Patronisation Behavior of Islamic Banks' Customers in Malaysia. Research

Journal of Business Management, 1-13.

Fauzi, W. I., Mohd Mokhtar, S. S., & Yusoff, R. Z. (2015). The Effect of Muslim

Products as Islamic Retail Store Attribute : A Study on Muslim Consumer

Patronage Behaviour in Malaysia. IJMS 22, Special Issue, 21-31.

Gait, A. H., & A. C. (2008). Attitudes, Perceptions and Motivations of Libyan Retail

Consumers toward Islamic Methods of Finance. Griffith Business School, Griffith

University.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

29

Gosh, A. (1990). Retail management. Chicago: Drydden press.

Gumel, A. M., Othman, M. A., & Yusof, R. M. (2015). Critical Insights Into an

Integrated Literature Review on Customers' Adoption of Islamic Banking Research.

International Journal of Scientific Research and Innovative Technology, 2313-

3759

Hamza, H. (2016). Does Investment Deposit Return in Islamic banks Reflect PLS

principle? Borsa _Istanbul Review 16-1, 32-42.

Hamzah, A. A., Ruzaiman, F. S., & Gazali, H. M. (2014). Islamic Investment Deposit

Account Through Mudarabah & Commodity Murabahah Contract: An Overview.

PROSIDING PERKEM ke-9, (pp. 28 - 33).

Hanif, M. (2011). Differences and Similarities in Islamic and Conventional Banking.

International Journal of Business and Social Science, 166-175.

Haque, A., J. O., & Hj Ismail, A. Z. (2009). Factor Influences Selection of Islamic

Banking: A Study on Malaysian Customer Preferences. American Journal of

Applied Sciences 6 (5), 922-928.

Harun, T. W., Ab Rashid, R., & Hamed, A. B. (2015). Factors Influencing Products’

Knowledge of Islamic Banking Employees. Journal of Islamic Studies and

Culture, 23-33.

Hassan, R., & Hussain, M. A. (2013). Scrutinizing the Malaysian Regulatory Framework

on Shari’ah Advisors for Islamic Financial Institutions. Journal of Islamic

Finance, 038-047.

Hong Leong Islamic Bank. (2017). Retrieved April 15, 2016 from

https://www.hlisb.com.my/about-us/investor-relations/annual-report

Hong Leong Islamic Bank. (2017). Retrieved April 15, 2016 from

https://www.hlisb.com.my/news/20130416-01-adoption-of-new-mechanism-for-

all-mudharabah-based-products

Idris, A. R., Naziman, K. N., Januri, S. S., Abu Hassan Asari, F. F., N. M., S. M., & K. J.

(2011). Religious Value as the Main Influencing Factor to Customers Patronizing

Islamic Bank. World Applied Sciences Journal 12 (Special Issue on Bolstering

Economic Sustainability), 8-13.

Imtiaz, N., Murtaza, A., Abaas, M. A., & Hayat, K. (2013). Factors Affecting the

Individuals' Behavior towards Islamic Banking in Pakistan: An Empirical Study.

Educational Research International

Isa, M. Y., & Zabid, M. (2015, May). Islamic Deposits and Investment Accounts in

income smoothing in post-reclassification of the Islamic Financial Service Act

2013. Retrieved April 15, 2016 from

https://www.researchgate.net/publication/268212158

Jaffar, M. A., & Musa, R. (2013). Determinants of Attitude towards Islamic Financing

among Halal Certified Micro and SMEs: A Preliminary Investigation. Procedia -

Social and Behavioral Sciences 130, 135-144.

Karim, A. A., & Affif, A. Z. (2005). Islamic Banking Consumer Behaviour. Jakarta.

Khayruzzaman. (2016). Impact of Religiosity on Buying Behavior of Financial Products:

A Literature Review. International Journal of Finance and Banking Research, 18-

23.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

30

Loo, M. (2010). Attitudes and Perceptions towards Islamic Banking among Muslims and

Non-Muslims in Malaysia: Implications for Marketing to Baby Boomers and X-

Generation. International Journal of Arts and Sciences 3(13), 453-485.

Malaysia, B. N. (2014). Financial Stability and Payment System Report. BNM.

Mamman, M., Ogunbado, A. F., & Abu-Bakr, A. S. (2016). Factors Influencing

Customer’s Behavioral Intention to Adopt Islamic Banking in Northern Nigeria: a

Proposed Framework. IOSR Journal of Economics and Finance (IOSR-JEF), 51-55.

Mansor, K. A., Masduki, R. M., Zulkarnain, N., & Aziz, N. A. (2015). A Study on

Factors Influencing Muslim’s Consumers Preferences Towards Takaful Products

In Malaysia. Romanian Statistical Review, 78-85.

Md Husin, M., & Abd Rahman, A. (2016). Do Muslims Intend to Participate in Islamic

Insurance. Journal of Islamic Accounting and Business Research, 42-58.

Mehtab, H., Zaheer, Z., & Ali, S. (2015). Knowledge, Attitudes and Practices (KAP)

Survey: A Case Study on Islamic Banking at Peshawar, Pakistan. FWU Journal of

Social Sciences, Winter 2015, 1-13.

Metawa, & Almossawi. (1998). Banking behaviour of Islamic bank customers:

perspectives and implications. International Journal of Bank Marketing, 299-315.

Mokhtar, H. S., Abdullah, N., & M. Al Habshi, S. (2006). Efficiency of Islamic Banking

in Malaysia : A Stochastic Frontier Approach . Journal of Economic Cooperation,

37-70.

Morris, J., Marzano, M., Dandy, N., & O’Brien, L. (2012). Theories and models of

behaviour and behaviour change. Forest Research.

Noonari, S., Memon, I. N., Mangi, J. A., Pathan, M., Khajjak, A. K., Memon, Z., . . .

Pathan, A. (2015). Knowledge and Perception of Students Regarding Islamic

Banking: A Case Study of Hyderabad Sindh Pakistan. Information and Knowledge

Management, ISSN 2224-5758 (Paper) ISSN 2224-896X (Online), 1-15.

Obeid, H., & Kaabachi, S. (2016). Empirical Investigation Into Customer Adoption Of

Islamic Banking Services In Tunisia. The Journal of Applied Business Research –

July/August 2016, 1-14.

Obeid, H., & Kaabachi, S. (2016). Empirical Investigation Into Customer Adoption Of

Islamic Banking Services In Tunisia. The Journal of Applied Business Research,

1243-1256.

Oseni, U. A. (2009). Dispute Resolution in Islamic Banking and Finance: Current Trends

and Future Perspective. International Conference on Islamic Financial Services:

Emerging Opportunities for Law/Economic Reforms of the Developing Nations,,

(pp. 1-25). Nigeria.

P., G. J. (1965). Fundamental Statistics in Psychology and Education. New York:

McGraw-Hill.

Rani, P. (2014). Factors Influencing Consumer Behaviour.

Int.J.Curr.Res.Aca.Rev.2014;2(9), 52-61.

Reni, A., & Ahmad, N. H. (2016). Application of Theory Reasoned Action in Intention to

Use Islamic Banking in Indonesia. Jurnal Ilmu Ekonomi Syariah (Journal of

Islamic Economics), 137-148.

Sekaran, U., & Bougie, R. (2013). Research Methods for Business. United Kingdom:

John Wiley and Sons.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

31

Sethi, I., & Chawla, A. (2014). Influence of Cultural, Social and Marketing Factors on the

Buying Behavior of Telecom Users: A Comparative Study of Rural, Semi-Urban

and Urban Areas in and Around Chandigarh. Journal of Marketing Management,

98-109.

Sheikh, M. A., Taseen, U., Haider, S. A., & Naeem, M. (no date). Islamic Vs

Conventional Banks in Pakistan. pakistan.

Sheppard, B. H., Hartwick, J., & Warshaw, P. R. (1988). The Theory of Reasoned

Action: A Meta-Analysis of Past Research with Recommendations for

Modifications and Future Research. The Journal of Consumer Research, 325-343.

Siddiqi, M. N. (2006). Islamic Banking and Finance in Theory and Practice : A Survey of

State of the Art. Islamic Economic Studies, 1-48.

Tabachnick, B. G., & S.Fidell, L. (2007). Using Multivariate Statistics (5th Edition).

Allyn & Bacon.

Thu Ha, N., & Gizaw, A. (2014). Factors that Influence Consumer Purchasing Decisions

of Private Label Food Products.

Wahyuni, S. (2012). Moslem Community Behavior in The Conduct of Islamic Bank: The

Moderation Role of Knowledge and Pricing. Procedia - Social and Behavioral

Sciences 57, 290-298.

Zauro, N. A., Sawandia, N., & Saad, R. A. (2016). Determinants of Qardhul Hassan

Financing Acceptance in Nigeria. ISSC 2016 : International Soft Science

Conference (pp. 1-7). Sintok: Future Academy.

ASEAN Comparative Education Research Journal on Islam and Civilization (ACER-J) Volume 1(2) September 2017, 17-32. eISSN:2600-769X.

32

Appendices

*Alliance Islamic Bank deposit and investment account 2013-2016

*Hong Leong Islamic Bank deposit and investment account 2013-2016

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2013 2014 2015 2016

Wadiah

Commodity Murabahah

Wakalah

Mudharabah

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

2013 2014 2015 2016

Wadiah

Commodity Murabahah

Wakalah

Mudharabah