F Hotel Values & CAP Rates · F Hotel Values & CAP Rates Meet The Money® 2016 Presented by:...

29

- 1 - F F F F F F F F Hotel Values & CAP Rates Meet The Money® 2016 Presented by: Suzanne Mellen, MAI, CRE, FRICS, ISHC Senior Managing Director - Practice Leader Hotel and Casino Consulting & Valuation (415) 268-0351 [email protected] May 6, 2015 – Sheraton Gateway Hotel Los Angeles

Transcript of F Hotel Values & CAP Rates · F Hotel Values & CAP Rates Meet The Money® 2016 Presented by:...

- 1 -

F

F

F

F

F

F

F

F

Hotel Values & CAP Rates Meet The Money® 2016 Presented by: Suzanne Mellen, MAI, CRE, FRICS, ISHC

Senior Managing Director - Practice Leader Hotel and Casino Consulting & Valuation (415) 268-0351 [email protected]

May 6, 2015 – Sheraton Gateway Hotel Los Angeles

- 2 -

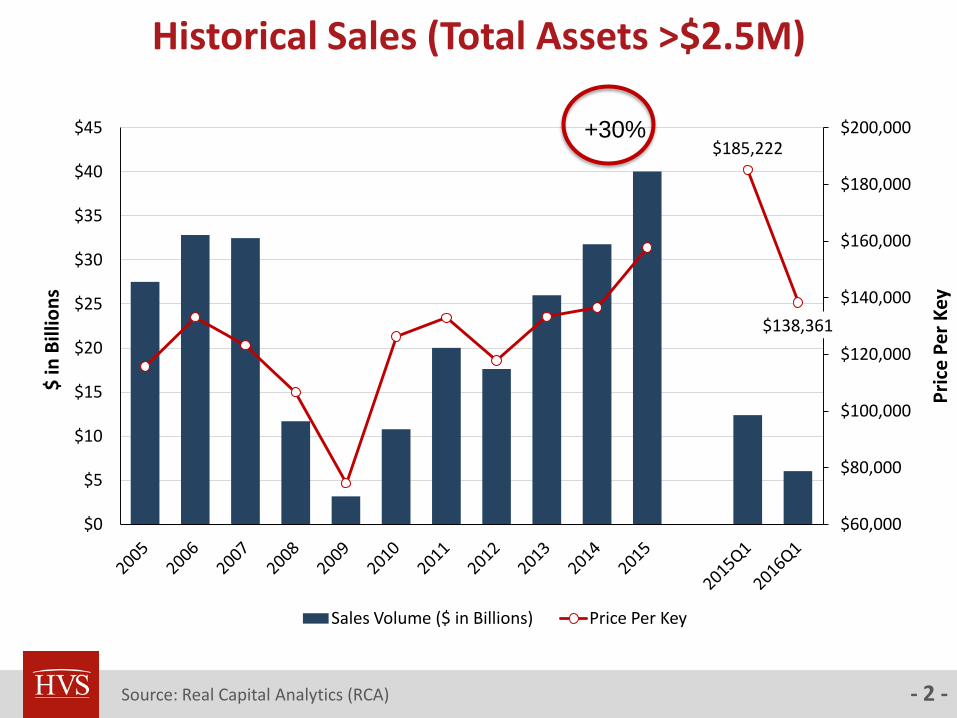

Historical Sales (Total Assets >$2.5M)

Source: Real Capital Analytics (RCA)

$185,222

$138,361

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Pri

ce P

er

Key

$ in

Bill

ion

s

Sales Volume ($ in Billions) Price Per Key

+30%

- 3 -

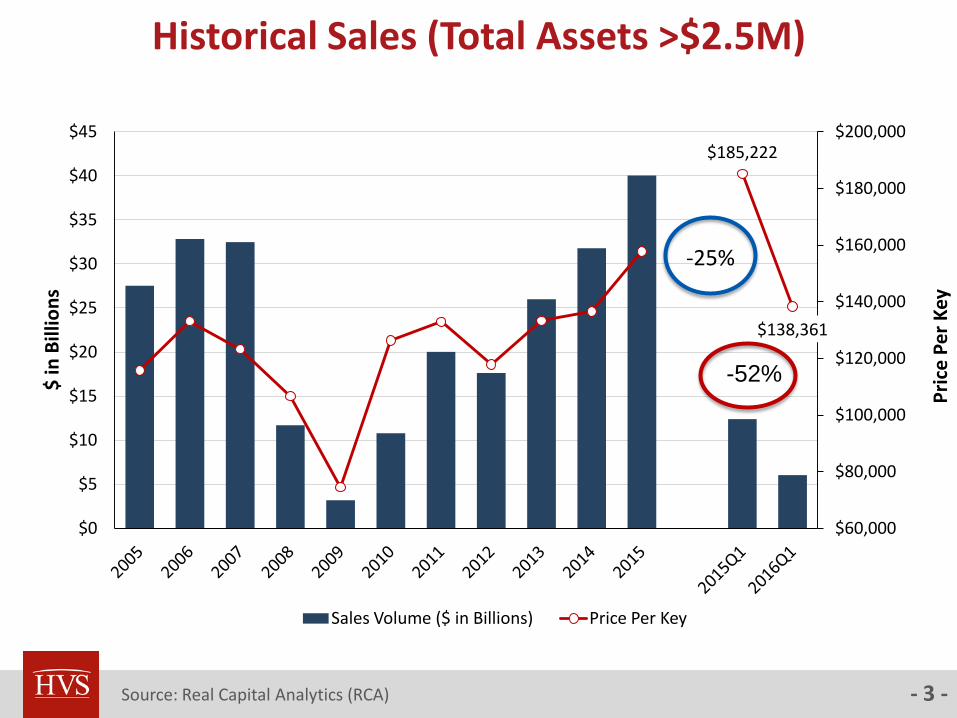

Historical Sales (Total Assets >$2.5M)

Source: Real Capital Analytics (RCA)

$185,222

$138,361

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Pri

ce P

er

Key

$ in

Bill

ion

s

Sales Volume ($ in Billions) Price Per Key

-52%

-25%

- 4 -

Major Hotel Sales Transactions

$0

$50,000

$100,000

$150,000

$200,000

$250,000

0

50

100

150

200

250

30019

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Avg

. Pri

ce P

er R

oo

m

Nu

mb

er o

f M

ajo

r Sa

les

Number of Hotels Average Price per Room

Source: HVS

- 5 -

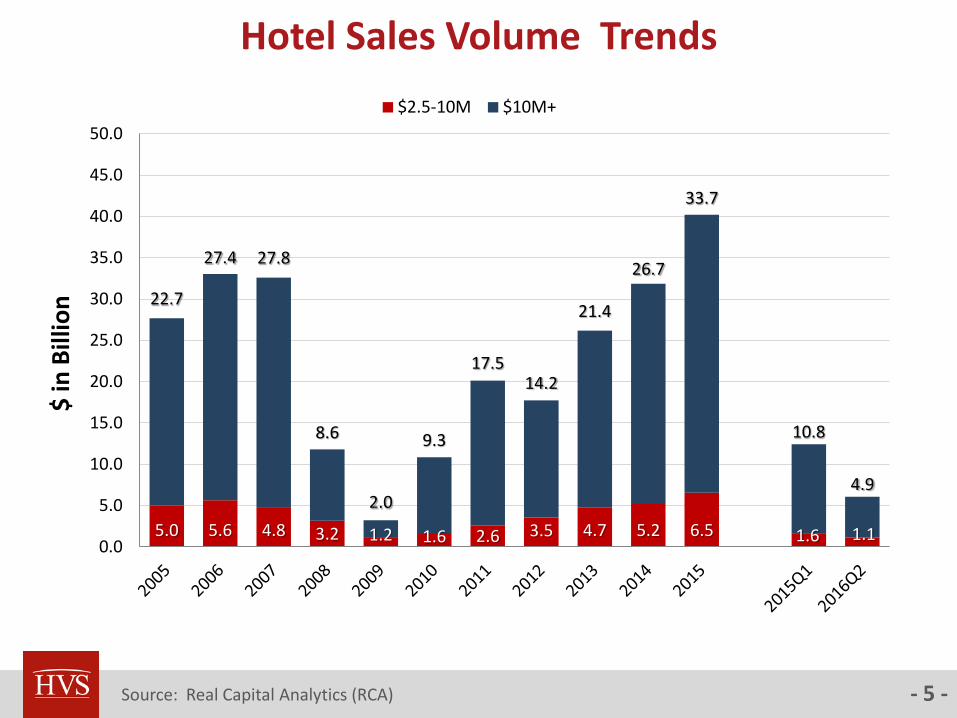

Hotel Sales Volume Trends

Source: Real Capital Analytics (RCA)

5.0 5.6 4.8 3.2 1.2 1.6 2.6 3.5 4.7 5.2 6.5 1.6 1.1

22.7

27.4 27.8

8.6

2.0

9.3

17.5 14.2

21.4

26.7

33.7

10.8

4.9

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

$ in

Bill

ion

$2.5-10M $10M+

- 6 -

Hotel Sales Volume Trends

Source: Real Capital Analytics (RCA)

5.0 5.6 4.8 3.2 1.2 1.6 2.6 3.5 4.7 5.2 6.5 1.6 1.1

22.7

27.4 27.8

8.6

2.0

9.3

17.5 14.2

21.4

26.7

33.7

10.8

4.9

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

$ in

Bill

ion

$2.5-10M $10M+

-55%

-32%

- 7 -

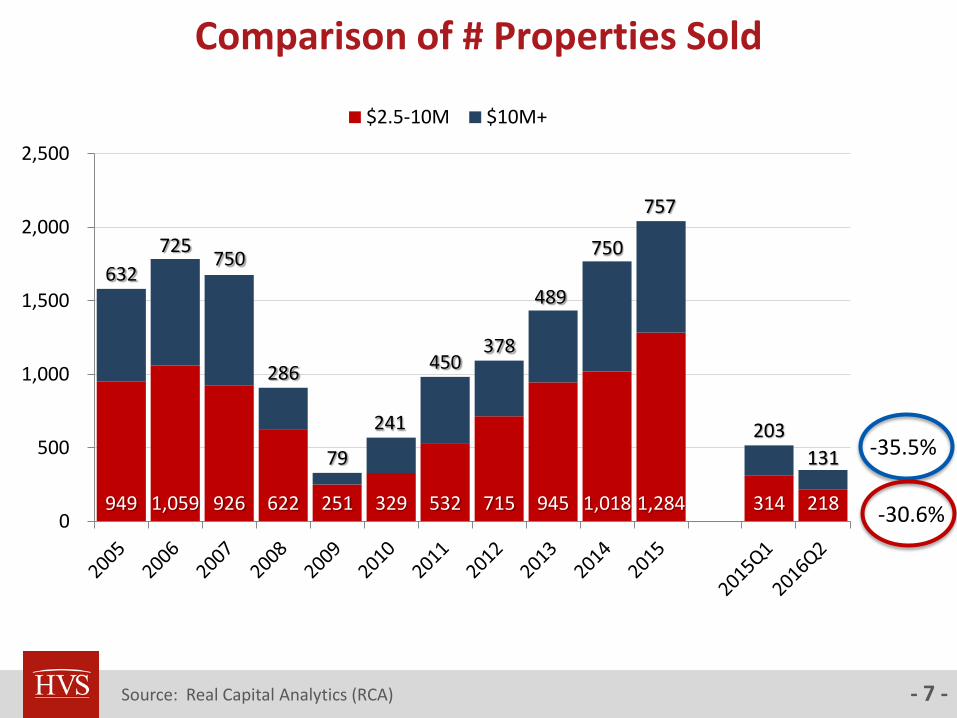

949 1,059 926 622 251 329 532 715 945 1,018 1,284 314 218

632

725 750

286

79

241

450 378

489

750

757

203

131

0

500

1,000

1,500

2,000

2,500

$2.5-10M $10M+

Comparison of # Properties Sold

Source: Real Capital Analytics (RCA)

-35.5%

-30.6%

- 8 -

Portfolio Sales Drove Overall Sales Volume Notable Portfolio Sales Since 2015

December 2015 Properties: 53 (Extended Stay)

Buyer: DW Crossland Owner LLC

Seller: ESH Hospitality, Inc.

Price: $285,000,000

Price/Room: $57,046

Buyout December 2015 Properties: 16 (Full Service)

Buyer: Blackstone Real Estate Partners VIII L.P.

Seller: Strategic Hotels & Resorts, Inc.

Price: $6,000,000,000

Price/Room: $792,498

Merger January 2015 183 (Select Service)

Buyer: Starwood Capital Group

Seller: TMI Hospitality, Inc.

Price: $1,100,000,000

Price/Room: $81,857

Source: Real Capital Analytics (RCA)

May 2015 Properties: 10 Waterpark Lodges

Buyer: Centerbridge

Seller: Great Wolf Lodge

Price: $1,350,000,000

Price/Room: $377,200

- 9 -

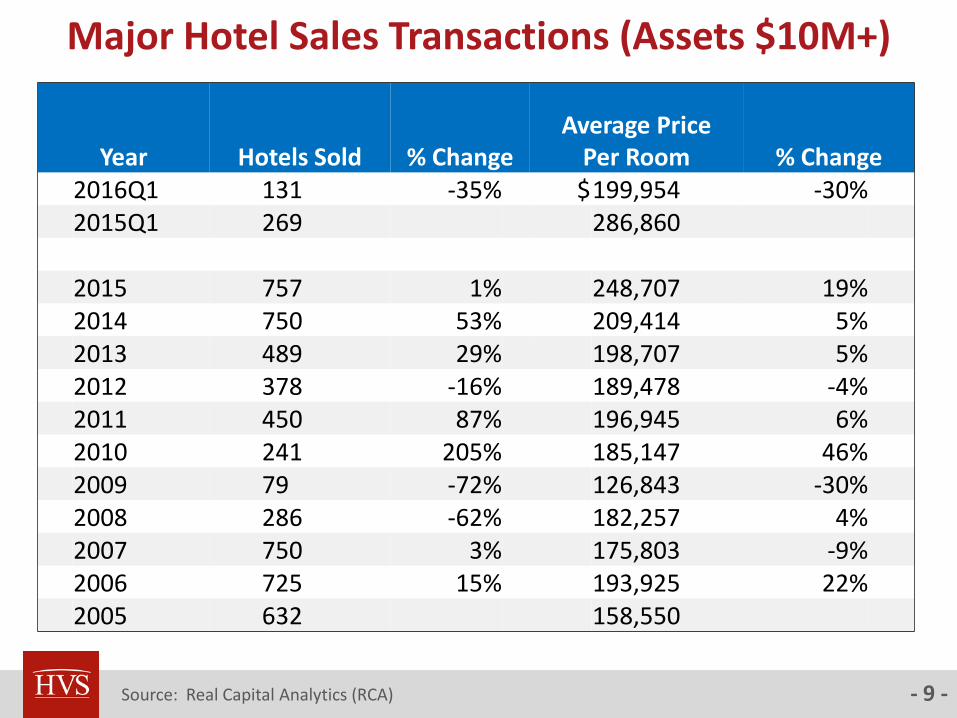

Major Hotel Sales Transactions (Assets $10M+)

Source: Real Capital Analytics (RCA)

Year Hotels Sold % Change Average Price

Per Room % Change 2016Q1 131 -35% $ 199,954 -30% 2015Q1 269 286,860 2015 757 1% 248,707 19% 2014 750 53% 209,414 5% 2013 489 29% 198,707 5% 2012 378 -16% 189,478 -4% 2011 450 87% 196,945 6% 2010 241 205% 185,147 46% 2009 79 -72% 126,843 -30% 2008 286 -62% 182,257 4% 2007 750 3% 175,803 -9% 2006 725 15% 193,925 22% 2005 632 158,550

- 10 -

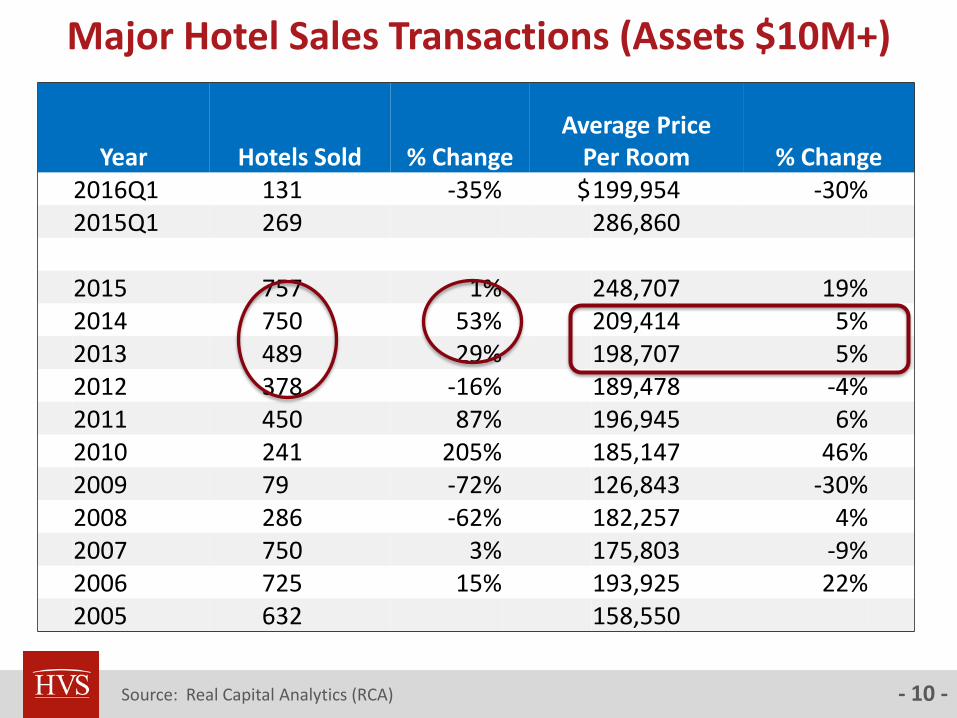

Year Hotels Sold % Change Average Price

Per Room % Change 2016Q1 131 -35% $ 199,954 -30% 2015Q1 269 286,860 2015 757 1% 248,707 19% 2014 750 53% 209,414 5% 2013 489 29% 198,707 5% 2012 378 -16% 189,478 -4% 2011 450 87% 196,945 6% 2010 241 205% 185,147 46% 2009 79 -72% 126,843 -30% 2008 286 -62% 182,257 4% 2007 750 3% 175,803 -9% 2006 725 15% 193,925 22% 2005 632 158,550

Major Hotel Sales Transactions (Assets $10M+)

Source: Real Capital Analytics (RCA)

- 11 -

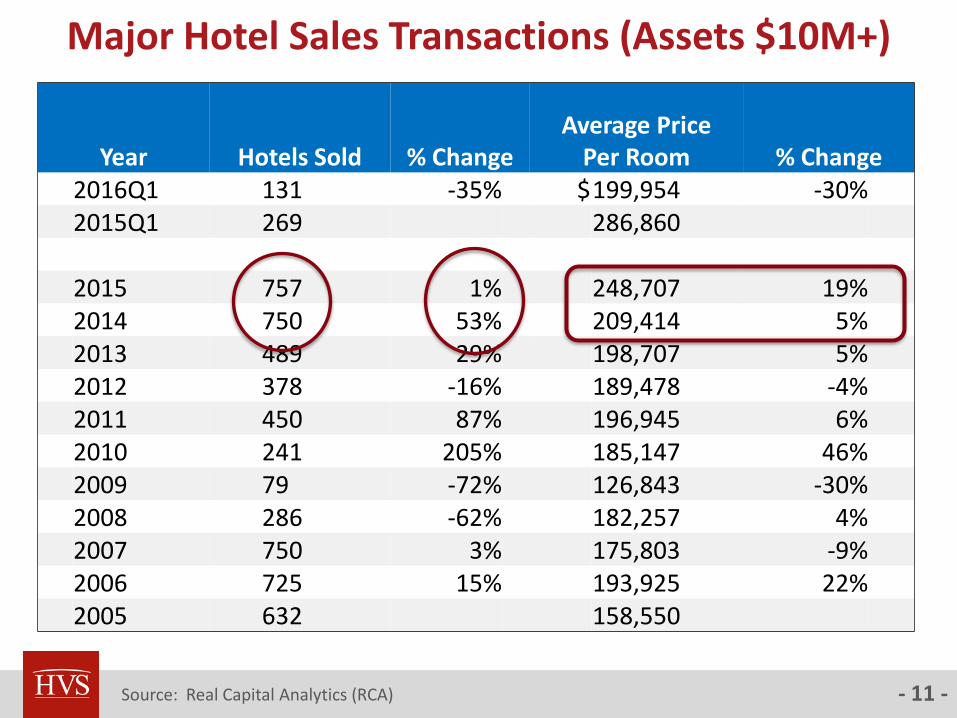

Year Hotels Sold % Change Average Price

Per Room % Change 2016Q1 131 -35% $ 199,954 -30% 2015Q1 269 286,860 2015 757 1% 248,707 19% 2014 750 53% 209,414 5% 2013 489 29% 198,707 5% 2012 378 -16% 189,478 -4% 2011 450 87% 196,945 6% 2010 241 205% 185,147 46% 2009 79 -72% 126,843 -30% 2008 286 -62% 182,257 4% 2007 750 3% 175,803 -9% 2006 725 15% 193,925 22% 2005 632 158,550

Major Hotel Sales Transactions (Assets $10M+)

Source: Real Capital Analytics (RCA)

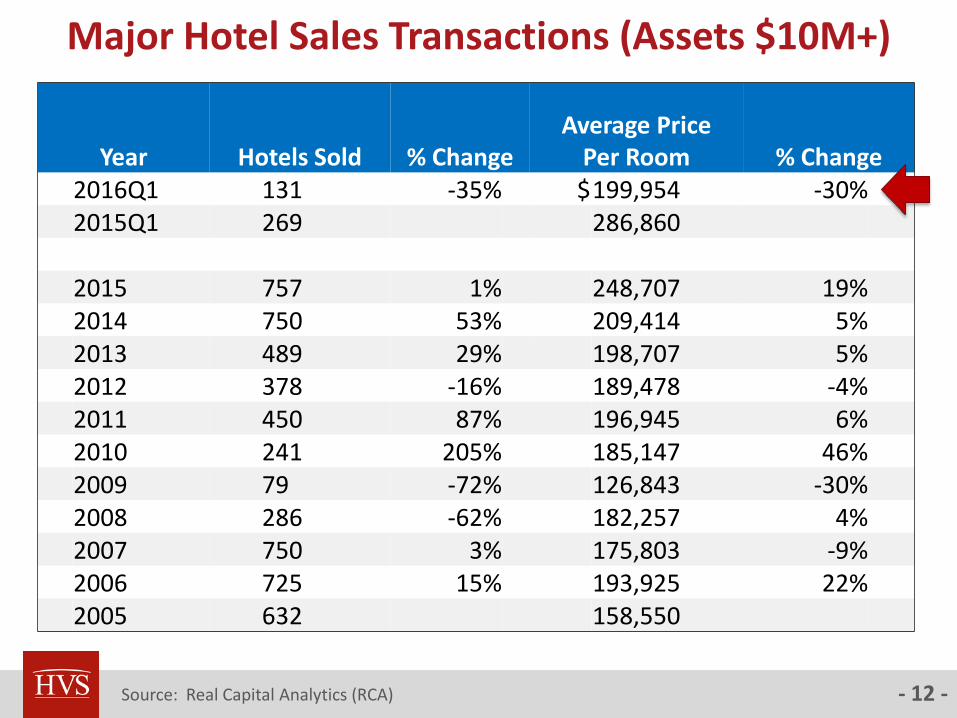

- 12 -

Year Hotels Sold % Change Average Price

Per Room % Change 2016Q1 131 -35% $ 199,954 -30% 2015Q1 269 286,860 2015 757 1% 248,707 19% 2014 750 53% 209,414 5% 2013 489 29% 198,707 5% 2012 378 -16% 189,478 -4% 2011 450 87% 196,945 6% 2010 241 205% 185,147 46% 2009 79 -72% 126,843 -30% 2008 286 -62% 182,257 4% 2007 750 3% 175,803 -9% 2006 725 15% 193,925 22% 2005 632 158,550

Major Hotel Sales Transactions (Assets $10M+)

Source: Real Capital Analytics (RCA)

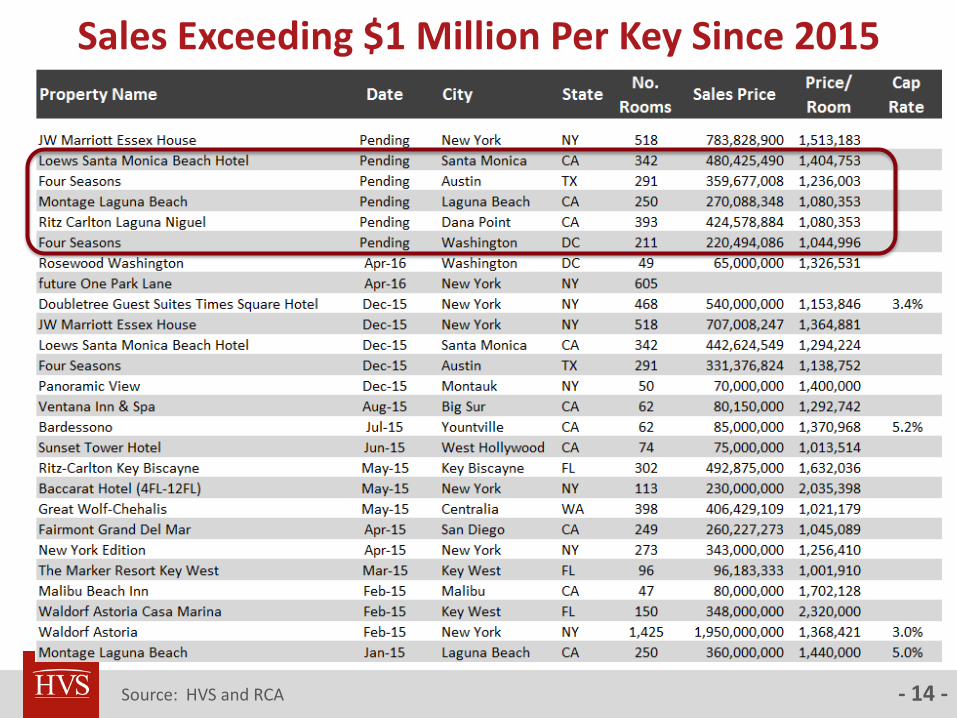

- 13 - Source: HVS and RCA

Sales Exceeding $1 Million Per Key Since 2015

- 14 - Source: HVS and RCA

Sales Exceeding $1 Million Per Key Since 2015

- 15 -

Rosewood, Washington D.C.

- 16 -

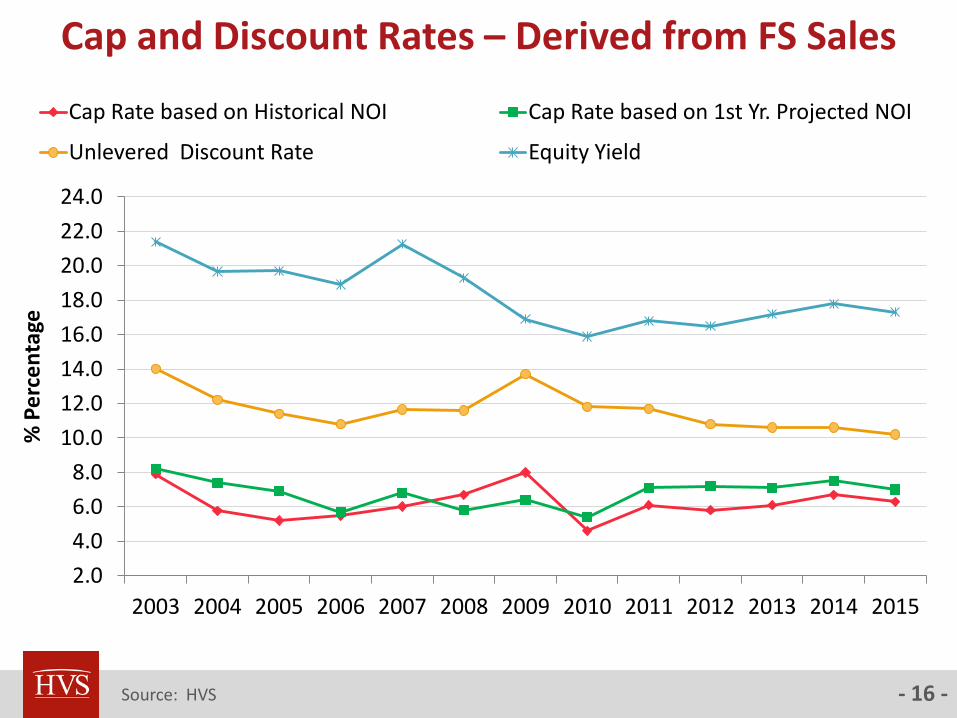

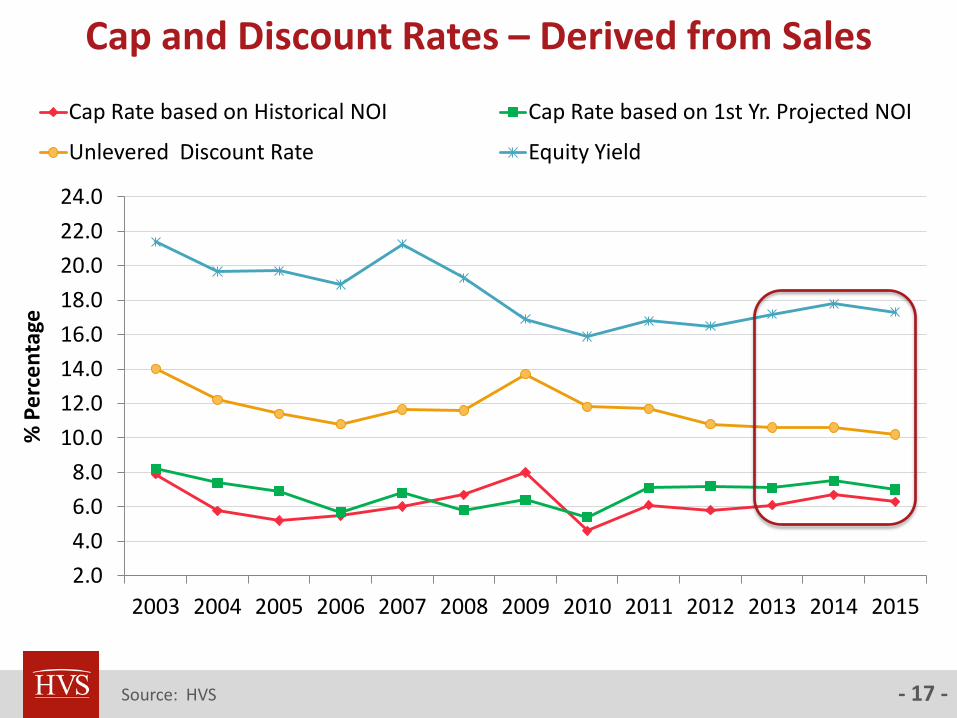

Cap and Discount Rates – Derived from FS Sales

Source: HVS

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% P

erc

en

tage

Cap Rate based on Historical NOI Cap Rate based on 1st Yr. Projected NOI

Unlevered Discount Rate Equity Yield

- 17 -

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% P

erc

en

tage

Cap Rate based on Historical NOI Cap Rate based on 1st Yr. Projected NOI

Unlevered Discount Rate Equity Yield

Cap and Discount Rates – Derived from Sales

Source: HVS

- 18 -

Impact of Great Recession – Full Service Hotels

Full Service Hotels 2007 2009

Occupancy 70.0% 62.5%

Avg. No. Rooms 306 292

Average Rate $166.7 $146.74

RevPAR $116.7 $91.7

% Change -21%

Revenue PAR $67,301 52,650

Expenses PAR $50,298 43,143

NOI PAR $17,003 9,507

% change -44%

NOI % 25.3% 18.1%

Multiple of NOI Change to RevPAR Change: 2.06 X

*Source: STR Annual HOST Reports – Composite US Performance

- 19 -

Full-Service Hotels Have Fully Recovered* Illustration of Operating Leverage – Revenue and NOI Relationship

Full Service Hotels 2007 2009 2014

Occupancy 70.0% 62.5% 73.9%

Avg. No. Rooms 306 292 299

Average Rate $166.7 $146.74 $180.94

RevPAR $116.7 $91.7 $133.7

% Change -21% 46%

Revenue PAR $67,301 52,650 74,975

Expenses PAR $50,298 43,143 55,911

NOI PAR $17,003 9,507 19,064

% change -44% 101%

NOI % 25.3% 18.1% 25.4%

Multiple of NOI Change to RevPAR Change: 2.06 X 2.19 X

*Source: STR Annual HOST Reports – Composite US Performance

- 20 -

Limited Service Hotels 2007 2009 2014

Occupancy 69.2% 63.3% 74.2%Avg. No. Rooms 117 113 116

Average Rate $94.94 $85.26 $102.45

RevPAR $65.70 $53.97 $76.01

% Change -18% 41%

Revenue PAR $24,349 $20,128 28,516

Expenses PAR $14,606 $13,583 17,710

NOI PAR $9,743 $6,545 10,806

% Change -33% 65%

NOI % 40.0% 32.5% 37.9%

Multiple of NOI Change to RevPAR Change: 1.84 X 1.59 X

Limited-Service Hotels Have Fully Recovered* Illustration of Operating Leverage – Revenue and NOI Relationship

*Source: STR Annual HOST Reports – Composite US Performance

- 21 -

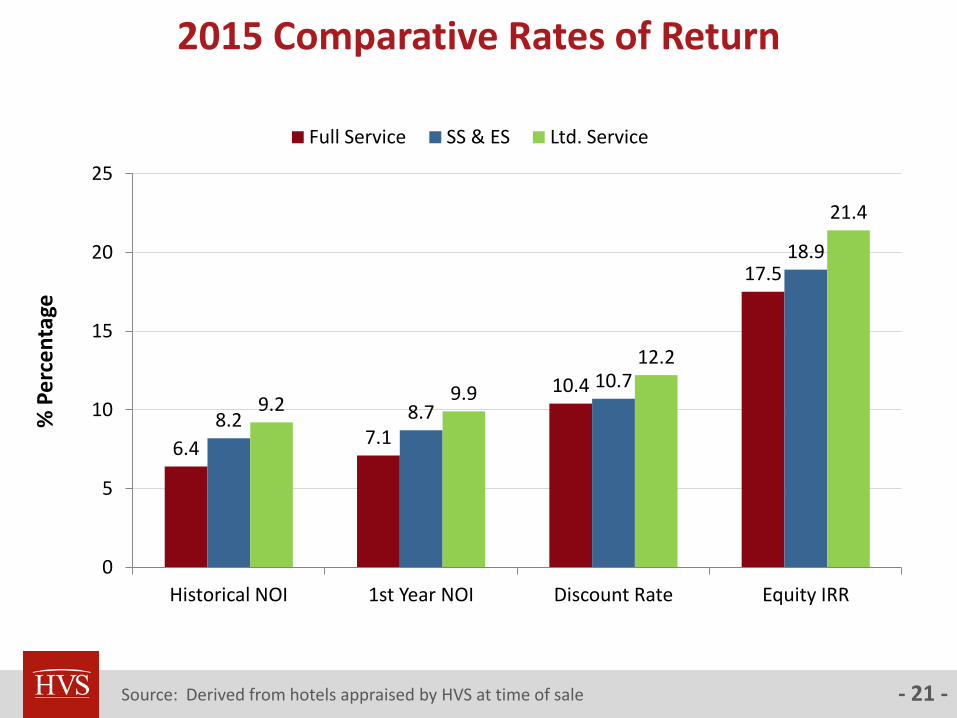

2015 Comparative Rates of Return

Source: Derived from hotels appraised by HVS at time of sale

6.4 7.1

10.4

17.5

8.2 8.7

10.7

18.9

9.2 9.9

12.2

21.4

0

5

10

15

20

25

Historical NOI 1st Year NOI Discount Rate Equity IRR

% P

erc

en

tage

Full Service SS & ES Ltd. Service

- 22 -

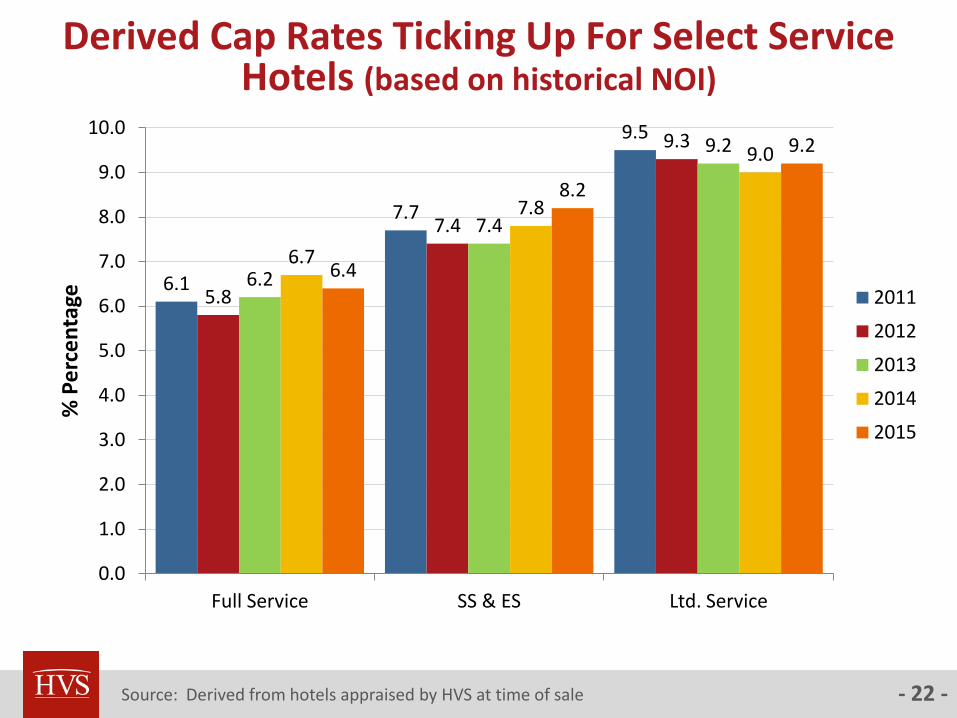

Derived Cap Rates Ticking Up For Select Service Hotels (based on historical NOI)

Source: Derived from hotels appraised by HVS at time of sale

6.1

7.7

9.5

5.8

7.4

9.3

6.2

7.4

9.2

6.7

7.8

9.0

6.4

8.2

9.2

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Full Service SS & ES Ltd. Service

% P

erc

en

tage

2011

2012

2013

2014

2015

- 23 -

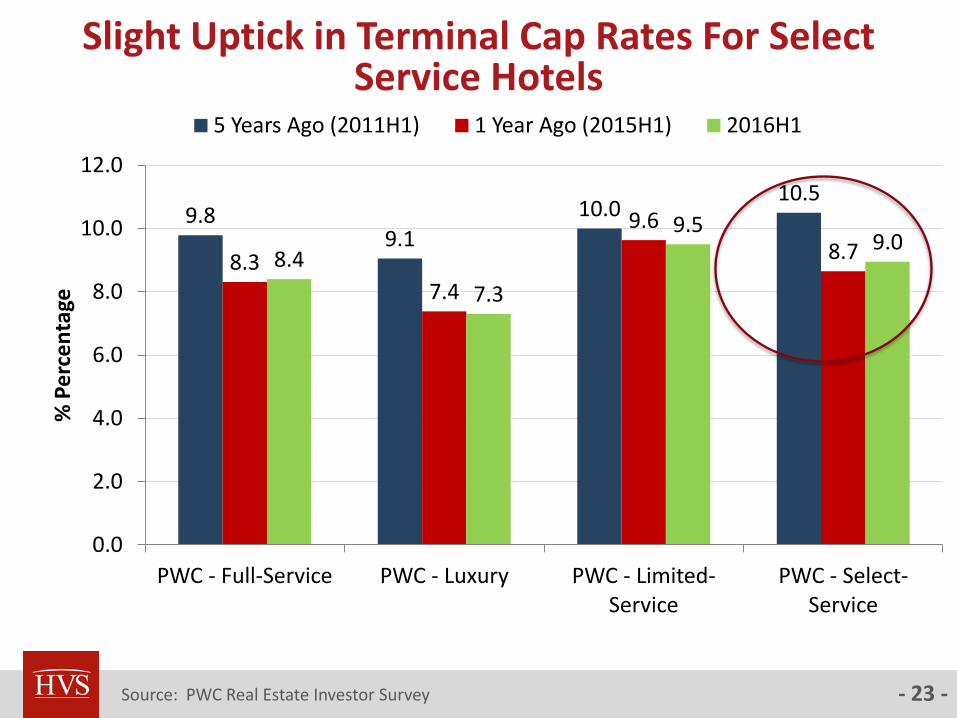

Slight Uptick in Terminal Cap Rates For Select Service Hotels

Source: PWC Real Estate Investor Survey

9.8 9.1

10.0 10.5

8.3 7.4

9.6

8.7 8.4

7.3

9.5 9.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

PWC - Full-Service PWC - Luxury PWC - Limited-Service

PWC - Select-Service

% P

erc

en

tage

5 Years Ago (2011H1) 1 Year Ago (2015H1) 2016H1

- 24 -

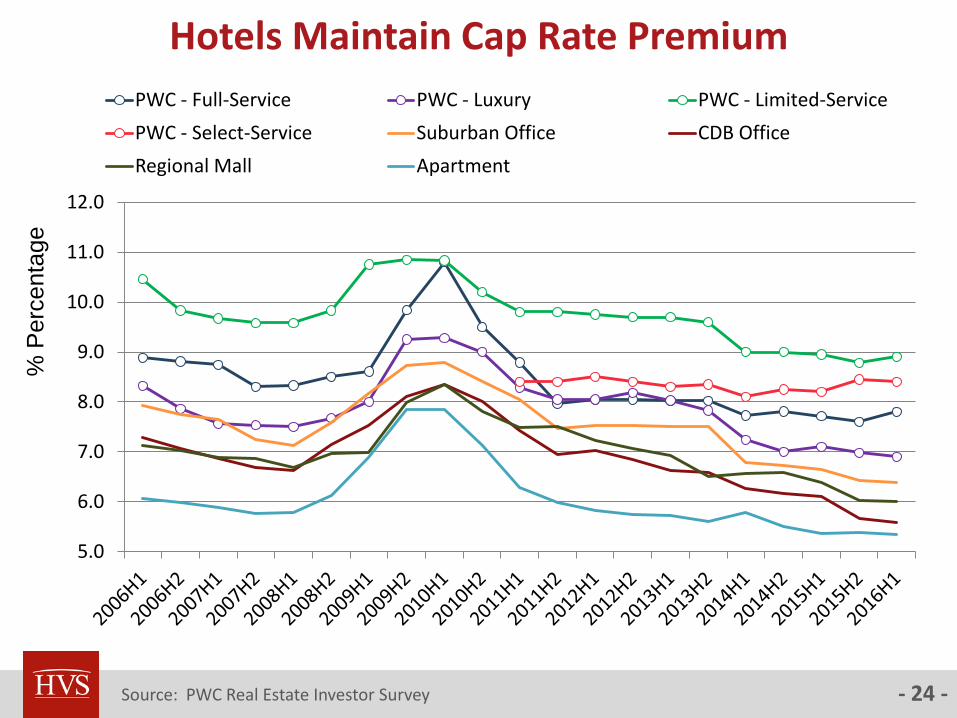

Hotels Maintain Cap Rate Premium

Source: PWC Real Estate Investor Survey

% P

erc

enta

ge

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

PWC - Full-Service PWC - Luxury PWC - Limited-Service

PWC - Select-Service Suburban Office CDB Office

Regional Mall Apartment

- 25 -

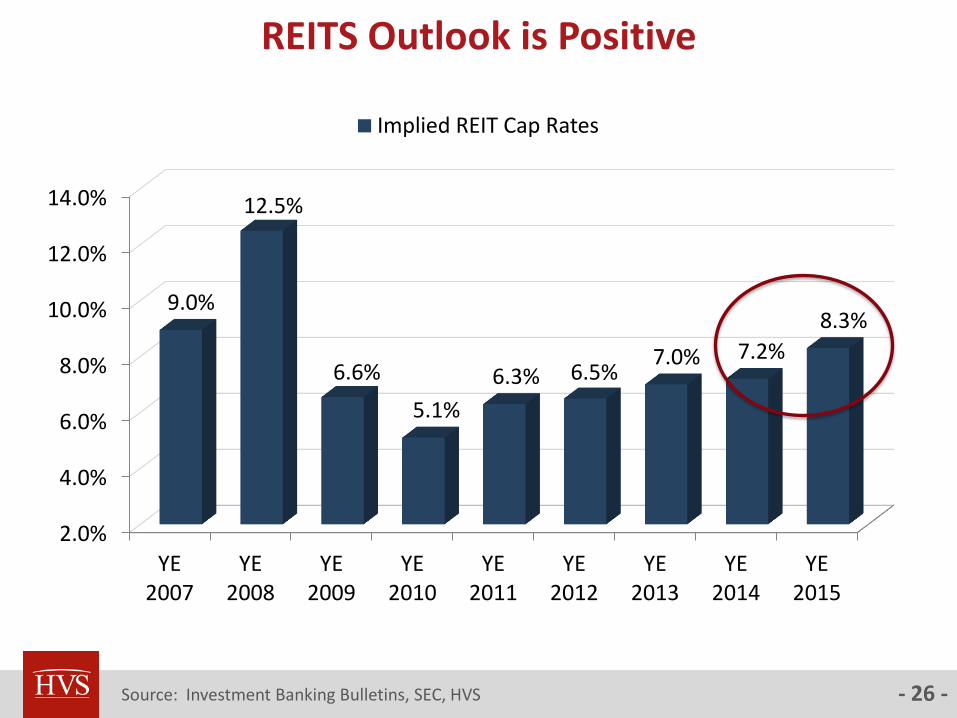

Publicly Traded REIT Cap Rates Trending Up

Source: Investment Banking Bulletins, SEC, HVS

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

YE 2007

YE 2008

YE 2009

YE 2010

YE 2011

YE 2012

YE 2013

YE 2014

YE 2015

9.0%

12.5%

6.6%

5.1%

6.3% 6.5% 7.0% 7.2%

8.3%

Implied REIT Cap Rates

- 26 -

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

YE 2007

YE 2008

YE 2009

YE 2010

YE 2011

YE 2012

YE 2013

YE 2014

YE 2015

9.0%

12.5%

6.6%

5.1%

6.3% 6.5% 7.0% 7.2%

8.3%

Implied REIT Cap Rates

REITS Outlook is Positive

Source: Investment Banking Bulletins, SEC, HVS

- 27 -

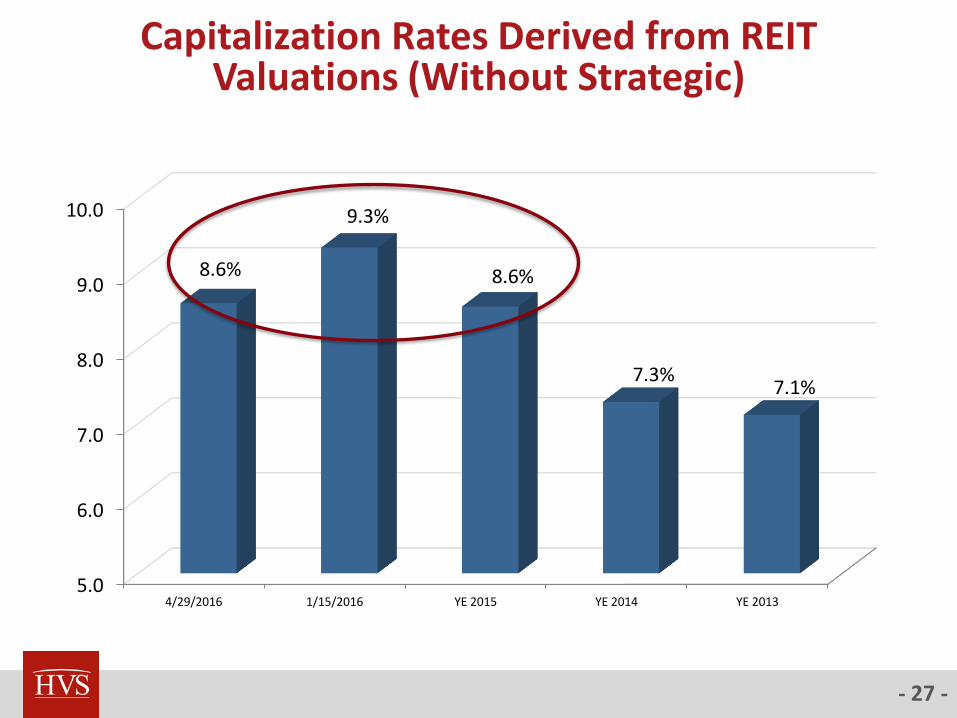

Capitalization Rates Derived from REIT Valuations (Without Strategic)

5.0

6.0

7.0

8.0

9.0

10.0

4/29/2016 1/15/2016 YE 2015 YE 2014 YE 2013

8.6%

9.3%

8.6%

7.3% 7.1%

- 28 -

Summary

2015 will be remembered as the peak year of the post Great Recession cycle

New supply concerns and global economic factors impacting outlook

for hotel performance and investment

Debt more challenging to procure, though interest rates remain low

Gap between buyer and seller expectations stalling transaction market

Cap rates have risen 50 bps for most assets but remain low for high quality full service and luxury hotels in prime markets

Aging hotels once again challenged due to lender pullback, cap ex and new supply

Higher cap rates will be offset by rising NOI in strong markets sustaining values

Higher cap rates will negatively impact values in markets facing supply and demand challenges and stagnant or declining NOI

- 29 -

Any Questions?

Suzanne Mellen, MAI, CRE, FRICS, ISHC

Practice Leader

[email protected] | (415) 268-0351

Superior results through unrivalled hospitality intelligence. Everywhere