Exploration and Production: Keys to Success and … and Production: Keys to Success and Common...

28

1 1 Exploration and Production: Exploration and Production: Keys to Success and Common Reasons Keys to Success and Common Reasons for Failure for Failure Robert Arnott Robert Arnott Oxford Institute for Energy Studies Oxford Institute for Energy Studies 22nd February 2005 22nd February 2005

Transcript of Exploration and Production: Keys to Success and … and Production: Keys to Success and Common...

11

Exploration and Production:Exploration and Production:

Keys to Success and Common Reasons Keys to Success and Common Reasons for Failurefor Failure

Robert ArnottRobert ArnottOxford Institute for Energy StudiesOxford Institute for Energy Studies

22nd February 200522nd February 2005

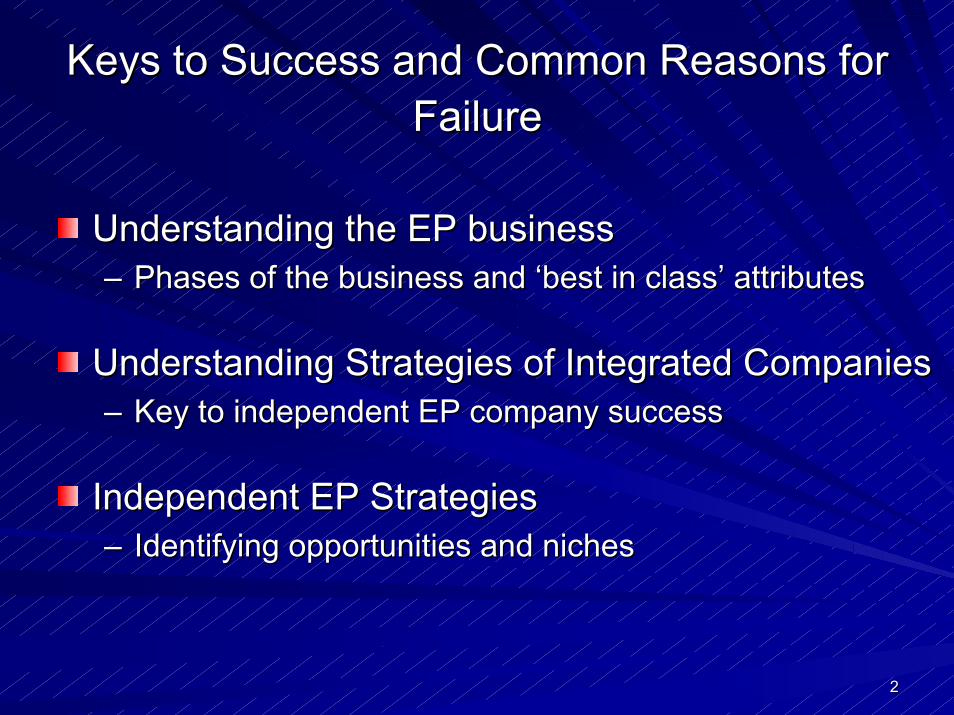

22

Keys to Success and Common Reasons for Keys to Success and Common Reasons for FailureFailure

Understanding the EP businessUnderstanding the EP business–– Phases of the business and ‘best in class’ attributesPhases of the business and ‘best in class’ attributes

Understanding Strategies of Integrated CompaniesUnderstanding Strategies of Integrated Companies–– Key to independent EP company successKey to independent EP company success

Independent EP StrategiesIndependent EP Strategies–– Identifying opportunities and niches Identifying opportunities and niches

33

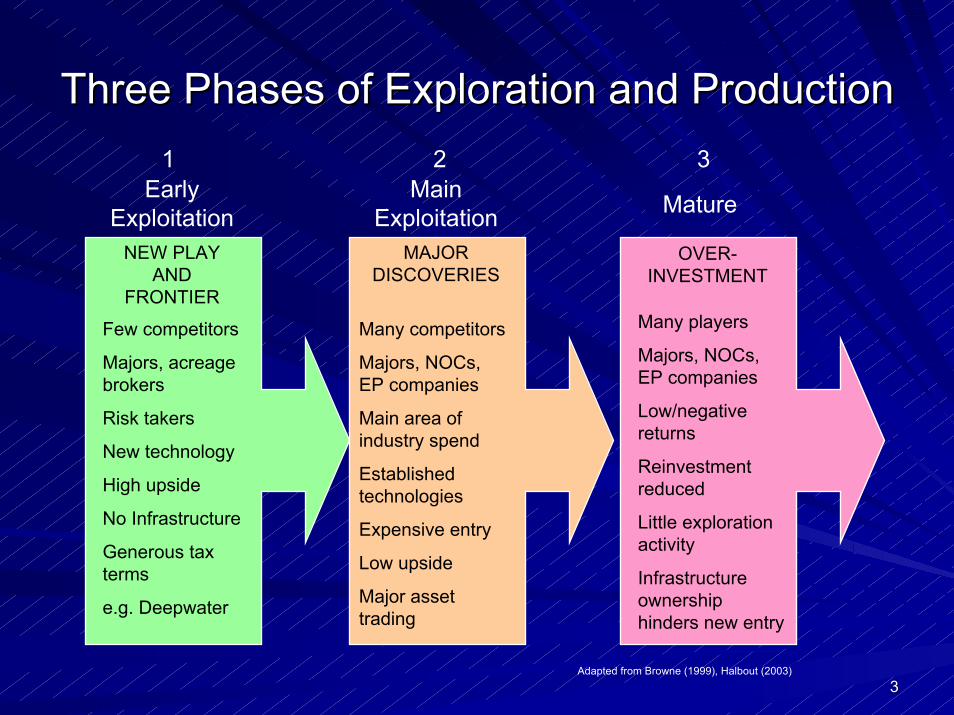

Three Phases of Exploration and ProductionThree Phases of Exploration and Production

Early Exploitation

Main Exploitation Mature

1 2 3

NEW PLAY AND

FRONTIER

MAJOR DISCOVERIES

OVER-INVESTMENT

Few competitors

Majors, acreage brokers

Risk takers

New technology

High upside

No Infrastructure

Generous tax terms

e.g. Deepwater

Many competitors

Majors, NOCs, EP companies

Main area of industry spend

Established technologies

Expensive entry

Low upside

Major asset trading

Adapted from Browne (1999), Halbout (2003)

Many players

Majors, NOCs, EP companies

Low/negative returns

Reinvestment reduced

Little exploration activity

Infrastructure ownership hinders new entry

44

Features of ‘Best In Class’Features of ‘Best In Class’Goal: A Portfolio of assets that minimises complex managerial Goal: A Portfolio of assets that minimises complex managerial structure and focuses on projects that offer the best opportunitstructure and focuses on projects that offer the best opportunity y for high profitability and growth in the near and long termfor high profitability and growth in the near and long term

VALUE CREATION

+ +

MATERIALITY CAPITAL EFFICIENCY

Number of high impact discoveries

Strategic focus

Preservation of regional knowledge

Optimised portfolio

Clear access strategy

Finding costs

Balances risk assessment

Optimised development of reserves

Clear exit strategy

Constant investment reviews

Cycle time to commercialisation

Realistic cycle times

Optimal shareholder management

Adapted from Wood (2000)

55

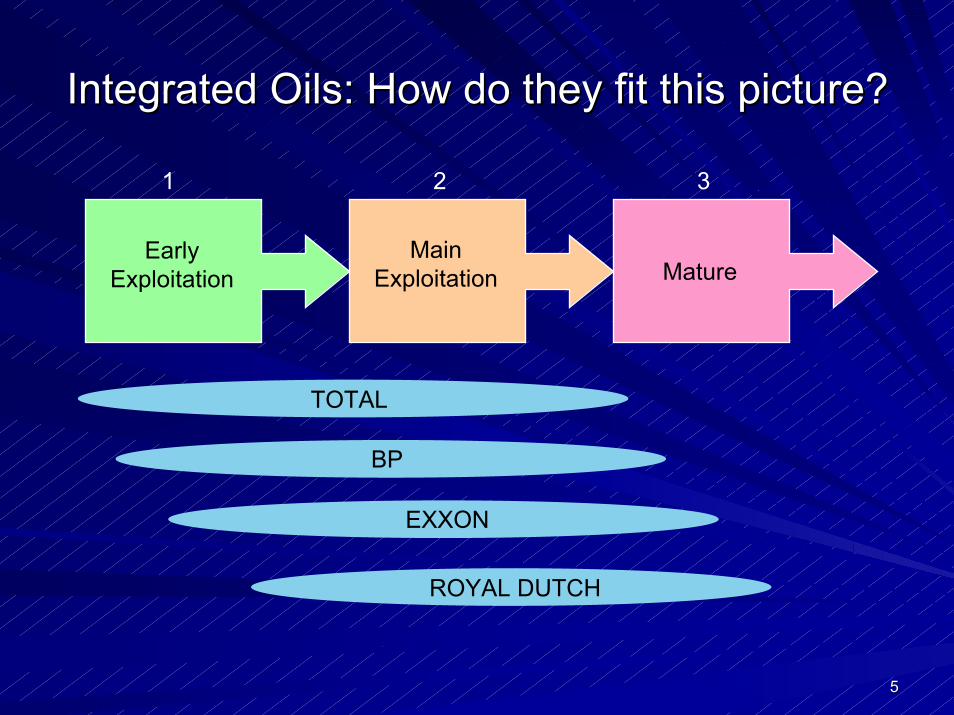

Integrated Oils: How do they fit this picture?Integrated Oils: How do they fit this picture?

Early Exploitation

Main Exploitation Mature

1 2 3

TOTAL

BP

EXXON

ROYAL DUTCH

66

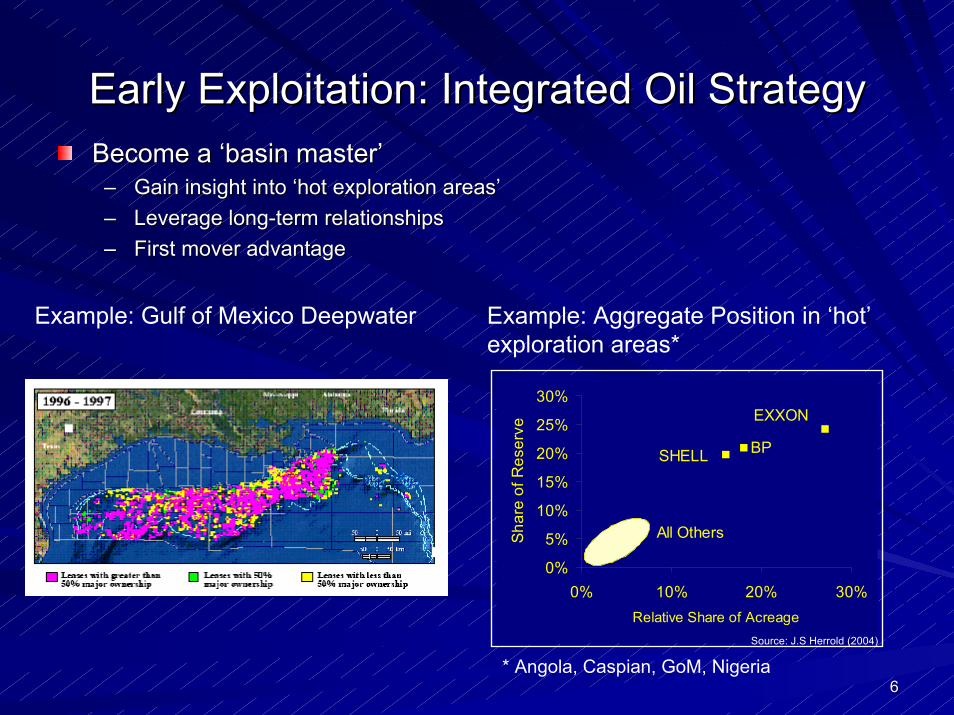

Early Exploitation: Integrated Oil StrategyEarly Exploitation: Integrated Oil StrategyBecome a ‘basin master’Become a ‘basin master’–– Gain insight into ‘hot exploration areas’Gain insight into ‘hot exploration areas’–– Leverage longLeverage long--term relationshipsterm relationships–– First mover advantageFirst mover advantage

Example: Gulf of Mexico Deepwater Example: Aggregate Position in ‘hot’ exploration areas*

* Angola, Caspian, GoM, Nigeria

SHELL BP

EXXON

0%

5%

10%

15%

20%

25%

30%

0% 10% 20% 30%Relative Share of Acreage

Shar

e of

Res

erve

All Others

Source: J.S Herrold (2004)

77

Majors have flexibility to optimise the portfolioMajors have flexibility to optimise the portfolio

Average global success rate is 1 in 6Average global success rate is 1 in 6

Need to balance risk and rewardNeed to balance risk and reward

LOW

UK

Source: Wood Mackenzie (2003)

TYPICAL PROSPECT PORTFOLIO

RIS

K

REWARD HIGHLOW

DESIGNERFR

ON

TIE

R

Optimising the Risk

0%

10%

20%

30%

40%

50%

60%

0 200 400 600 800

Number of Wells Drilled (91-00)

Suc

cess

Rat

e

Average Commercial Success Rates

Angola (Deep)

US GoM

Source: After Wood (2000)

88

Exploration: Majors Track RecordExploration: Majors Track RecordOnly just replaced reserves annually since 1990Only just replaced reserves annually since 1990Big difference between the various companiesBig difference between the various companiesSEC reserves do no reflect actual performanceSEC reserves do no reflect actual performance

Source: Wood Mackenzie (2003)

020406080

100120140160

90 91 92 93 94 95 96 97 98 99 00 01 02 03

0

50

100

150

200

250

BG

.L

CO

P.N

TOTF

.PA

RE

P.M

C

EN

I.M

BP

.L

NH

Y.O

L

CV

X.N

PC

A.T

O

OX

Y.N

STL

.OL

XO

M.N

SH

EL.

L

AH

C.N

MR

O.N

Organic RR Ratio 90-03

MROAHC

SHEL XOM

STL OXYPCA

CVX

NHY

BPENI

REP

TOT

COP

0

20

40

60

80

100

120

140

160

180

200

0 50 100 150 200SEC RR Ratio 2001-2003

Woo

d M

acke

nzie

Est

imat

e 20

01-2

0

Reconciling SEC versus Actual

Source: Company Data

99

Exploration: Have the Majors Added Value?Exploration: Have the Majors Added Value?

Majors have invested $50 billion from 1996Majors have invested $50 billion from 1996--20012001Only created $23 billion in valueOnly created $23 billion in valueOnly 13 out of 25 companies have added valueOnly 13 out of 25 companies have added value

Exploration spend vs NPV Value Added vs Income

0

2000

4000

6000

8000

10000

12000

14000

96 97 98 99 00 01 02 03

US

D m

illio

Total Exploration CostNPV of Discoveries

XOMBPCHV

TOT]SHEL

TOT

SHELTOT

CHV XOMBP

SHEL

CHV

BP XOM

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

0.0 2.0 4.0 6.0 8.0 10.0

Net Income per Barrel

Valu

e A

dded

/USD

Spe

Source: OIES (2005)Source: Wood Mackenzie (2003)

1010

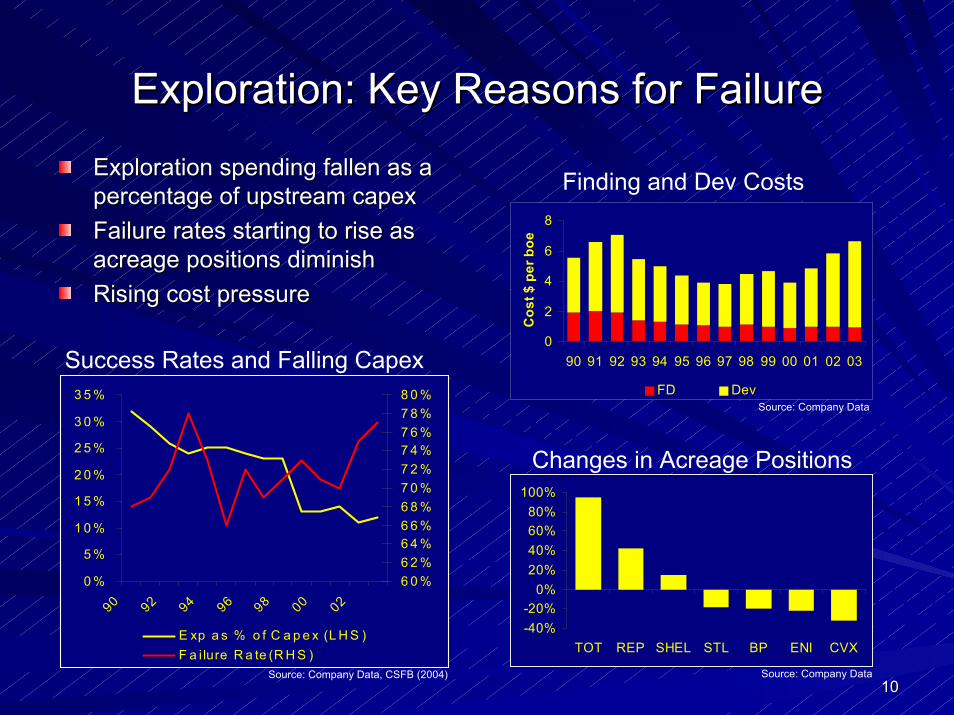

Exploration: Key Reasons for FailureExploration: Key Reasons for Failure

0 %

5 %

1 0 %

1 5 %

2 0 %

2 5 %

3 0 %

3 5 %

90 92 94 96 98 00 02

6 0 %6 2 %6 4 %6 6 %6 8 %7 0 %7 2 %7 4 %7 6 %7 8 %8 0 %

E xp a s % o f C a p e x (L H S )F a i lure R a te (R H S )

0

2

4

6

8

90 91 92 93 94 95 96 97 98 99 00 01 02 03

Cos

t $ p

er b

oe

FD Dev

-40%-20%

0%20%40%60%80%

100%

TOT REP SHEL STL BP ENI CVX

Finding and Dev Costs

Changes in Acreage Positions

Success Rates and Falling Capex

Source: Company Data, CSFB (2004)

Source: Company Data

Source: Company Data

Exploration spending fallen as a Exploration spending fallen as a percentage of upstream capexFailure rates starting to rise as Failure rates starting to rise as acreage positions diminishRising cost pressure

percentage of upstream capex

acreage positions diminishRising cost pressure

1111

Exploration: Where next for the majors?Exploration: Where next for the majors?Access is an issue for all companiesAccess is an issue for all companiesAlliances with NOC are inevitableAlliances with NOC are inevitableFurther consolidation in the absence of growthFurther consolidation in the absence of growth

EMV: Deepwater Attractive

0

50

100

150

200

250

Rem

aini

ngG

iant

Fie

lds

Hig

hA

cces

sibl

e*

Med

ium

Acc

essi

ble*

*

Low

Acc

essi

ble*

**

No.

of F

ield

s

Undiscovered 500 mmbbl fields

CameronNetherlands JDA

UK ShelfAngola Deepwater

KazakhstanBangladesh

Venezuela

Source: Deutsche Bank (2003)

GoM (Deepwater)

Nigeria Deepwater

* All others ** China, Oman, Russia, Venezuela

*** Algeria, Iran, Kuwait, Libya, Mexico, Saudi Arabia, UAESource: USGS, JS Herrold

1212

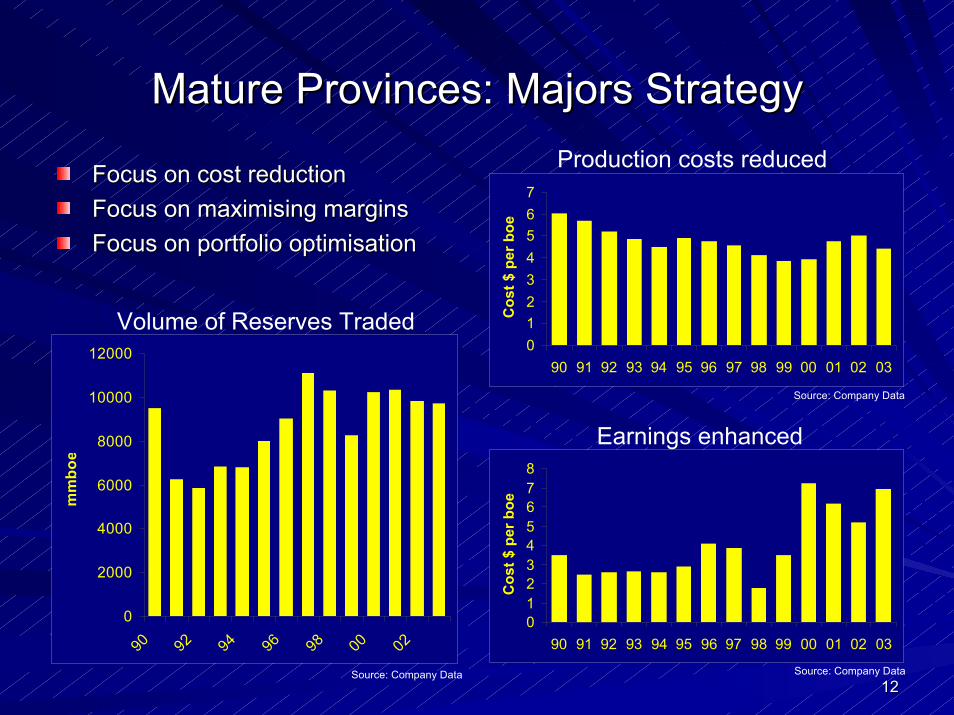

Mature Provinces: Majors StrategyMature Provinces: Majors Strategy

01234567

90 91 92 93 94 95 96 97 98 99 00 01 02 03

Cos

t $ p

er b

oe

012345678

90 91 92 93 94 95 96 97 98 99 00 01 02 03

Cos

t $ p

er b

oe

0

2000

4000

6000

8000

10000

12000

90 92 94 96 98 00 02

mm

boe

Volume of Reserves Traded

Production costs reduced

Earnings enhanced

Source: Company Data

Source: Company Data

Source: Company Data

Focus on cost reductionFocus on maximising marginsFocus on portfolio optimisation

Focus on cost reductionFocus on maximising marginsFocus on portfolio optimisation

1313

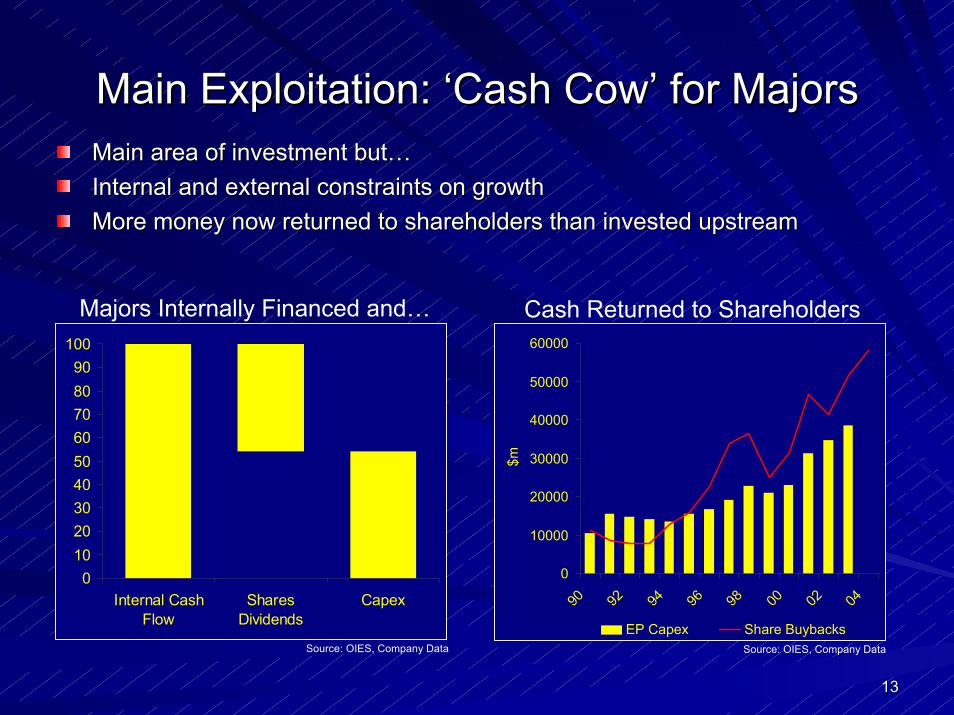

Main Exploitation: ‘Cash Cow’ for MajorsMain Exploitation: ‘Cash Cow’ for MajorsMain area of investment but…Main area of investment but…Internal and external constraints on growthInternal and external constraints on growthMore money now returned to shareholders than invested upstreamMore money now returned to shareholders than invested upstream

0102030405060708090

100

Internal CashFlow

SharesDividends

Capex

Majors Internally Financed and…

Source: OIES, Company Data

0

10000

20000

30000

40000

50000

60000

90 92 94 96 98 00 02 04

$m

EP Capex Share Buybacks

Cash Returned to Shareholders

Source: OIES, Company Data

1414

Majors EP Strategy: ConclusionsMajors EP Strategy: Conclusions

To be successful a company has to spend enough To be successful a company has to spend enough money on new business to ensure it has a significant money on new business to ensure it has a significant share of initial findsshare of initial finds

To be successful a company must know when it has To be successful a company must know when it has reached the point where further investment would be reached the point where further investment would be unproductiveunproductive

IN

OUT

1515

What Determines EP Company Success?What Determines EP Company Success?

Operations

Reserves Growth

Production Growth

Finance

Cash Flow Growth

NAV Growth

Equity Market

Where in the cycle?

Access to funding

Commodity Prices

Oil/Gas Prices

TOTAL SHAREHOLDER

RETURN

Growth in Capital

Return of Capital

WITHIN CONTROL OUT OF CONTROL

1616

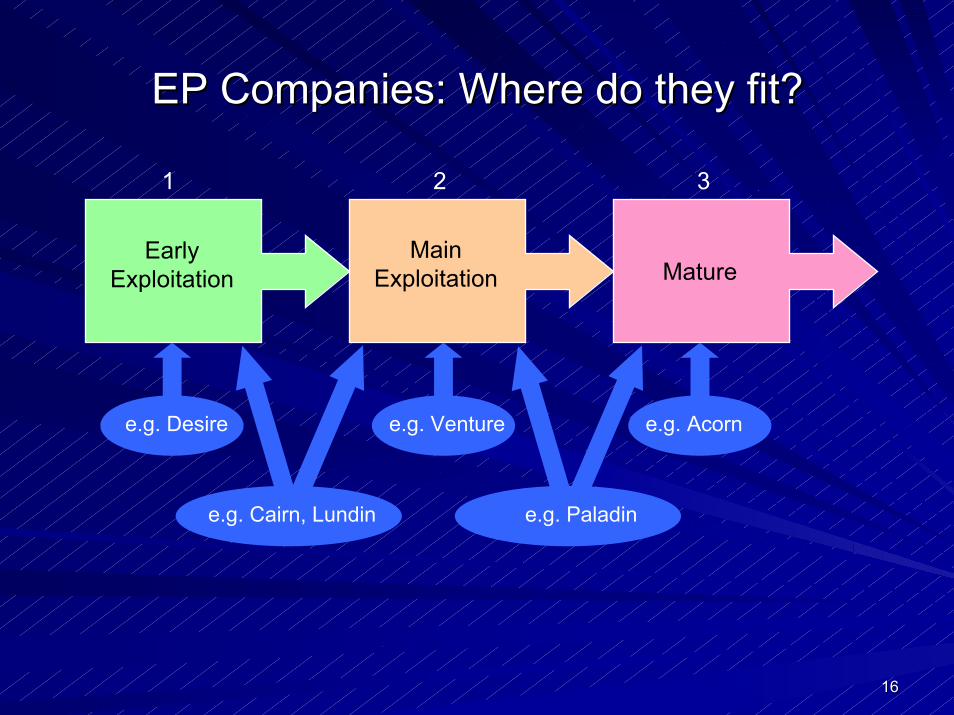

EP Companies: Where do they fit?EP Companies: Where do they fit?

Early Exploitation

Main Exploitation Mature

1 2 3

e.g. Desire e.g. Venture e.g. Acorn

e.g. Cairn, Lundin e.g. Paladin

1717

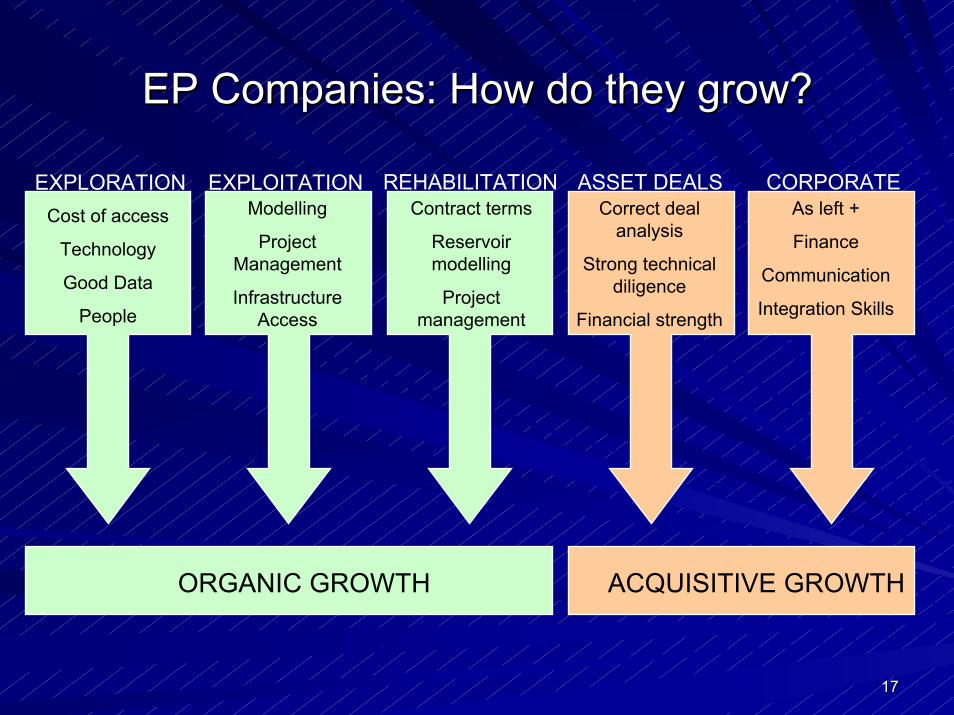

EP Companies: How do they grow?EP Companies: How do they grow?

CORPORATECost of Access

Technology

Data

People

EXPLORATION EXPLOITATION REHABILITATION ASSET DEALSModelling

Project Management

Infrastructure Access

Contract terms

Reservoir modelling

Project management

Correct deal analysis

Strong technical diligence

Financial strength

As left +

Finance

Communication

Integration Skills

Cost of access

Technology

Good Data

People

ORGANIC GROWTH ACQUISITIVE GROWTH

1818

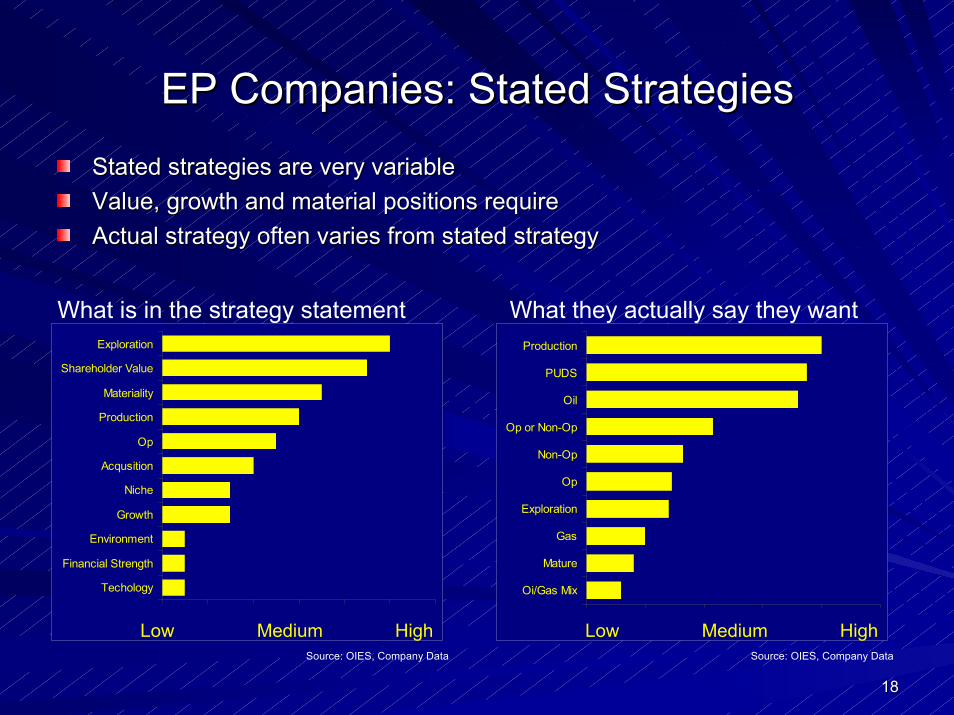

EP Companies: Stated StrategiesEP Companies: Stated Strategies

Stated strategies are very variableStated strategies are very variableValue, growth and material positions requireValue, growth and material positions requireActual strategy often varies from stated strategyActual strategy often varies from stated strategy

What is in the strategy statement What they actually say they want

Oi/Gas Mix

Mature

Gas

Exploration

Op

Non-Op

Op or Non-Op

Oil

PUDS

Production

Techology

Financial Strength

Environment

Growth

Niche

Acqusition

Op

Production

Materiality

Shareholder Value

Exploration

Low Medium High Low Medium HighSource: OIES, Company Data Source: OIES, Company Data

1919

EP Companies: Strategic DifferentiationEP Companies: Strategic DifferentiationDespite offering balance strategies clear distinction between :Despite offering balance strategies clear distinction between :–– Companies who have added all reserves through acquisitionsCompanies who have added all reserves through acquisitions–– Companies who have added all reserves through explorationCompanies who have added all reserves through exploration

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

ED

G.L

CN

E.L

CU

X.L

JKX

.L

PM

O.L

MR

S.L

DN

O.N

O

VP

C.L

DN

X.L

TLW

.L

PLR

.L

SIA

.L

BU

R.L

RO

S.L

Acquisitions Exploration

Additions through E or A

-50%

0%

50%

100%

150%

200%

250%

-50.0% 0.0% 50.0% 100.0% 150.0%

Proportion of Cashflow Spent on Acquisitions

Pro

porti

on o

f Cas

hflo

w S

pent

on

Expl

orat

E Driven

A Driven

Capex is either E or A driven

Source: OIES, Company DataSource: OIES, Company Data

2020

EP Companies: Just how successful?EP Companies: Just how successful?Most of the growth in the sector comes through acquisitions (cheMost of the growth in the sector comes through acquisitions (cheaper)aper)Step change exploration success is rare (volatile)Step change exploration success is rare (volatile)

012345678

99 00 01 02 03

$/bo

e

Proved Acquistion Cost FD Cost

0%10%20%30%40%50%60%70%80%90%

100%

ED

G.L

SIA

.L

CN

E.L

PM

O.L

DN

X.L

SE

:LU

PE

DN

O.N

O

MR

S.L

TLW

.L

PLR

.L

JKX

.L

BU

R.L

CU

X.L

RO

S.L

Exploration Development Acqusitions

0

10

20

30

40

50

90 91 92 93 94 95 96 97 98 99 00 01 02 03

$/bo

e

0.7

42.638.9

6.9 4.00.8

11.3

3.6 5.3 7.1

19.1

2.7

23.7

0.50.05.0

10.015.020.025.030.035.040.045.0

BU

R.L

CN

E.L

CU

X.L

DN

X.L

DN

O.N

O

EDG

.L

JKX

.L

MR

S.L

PLR

.L

PM

O.L

RO

S.L

SIA

.L

TLW

.L

LUP

E:ST

$/bo

e

Erratic FD track record Cheaper to buy than explore

FD Cost 01-03 Hit or miss! Capital Allocation 01-03

Source: OIES, Company Data Source: OIES, Company Data

Source: OIES, Company DataSource: OIES, Company Data

2121

EP Companies: Only a short time to deliverEP Companies: Only a short time to deliverAverage life of project from 1Average life of project from 1stst exploration to abandonment is 25 yearsexploration to abandonment is 25 yearsAverage life of EP company is less than 10 yearsAverage life of EP company is less than 10 yearsManagement Management has has deliver outstanding results and quicklydeliver outstanding results and quickly

0

10

20

30

40

50

60

70

80

90

1980 2004

05

101520253035404550

US Canada

1997 2004

25 Years

US EP Companies to Survive 25 Years

Change in EP Company Numbers 97-04

Source: JS Herrold, Harrison Lovegrove Source: Morgan Stanley

2222

EP Companies Usually Capital ConstrainedEP Companies Usually Capital Constrained

Most EP companies rely on ‘Other Peoples Money’ to:Most EP companies rely on ‘Other Peoples Money’ to:–– Finance the gap between cash flow and explorationFinance the gap between cash flow and exploration–– Run the business as a going concernRun the business as a going concern

Failure to maintain a robust balance sheet is common concernFailure to maintain a robust balance sheet is common concern

020406080

100120140160180200

Internal CashFlow

OutsideFinance

Capex

Living Outside of Means (01-03)

Source: OIES, Company Data

EQUITY

FAILURESUCCESS

OPPORTUNITY BEGGING BOWL

A Fine Line between Success & Failure

Source: OIES

2323

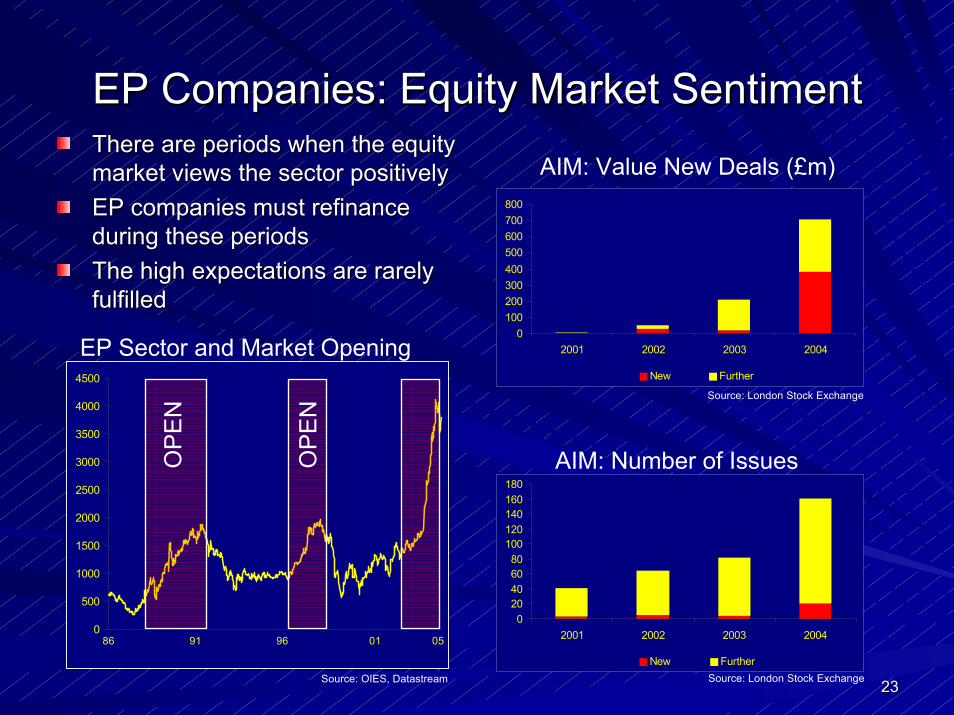

EP Companies: Equity Market SentimentEP Companies: Equity Market SentimentThere are periods when the equity There are periods when the equity market views the sector positivelyEP companies must refinance EP companies must refinance during these periodsThe high expectations are rarely The high expectations are rarely fulfilled

AIM: Value New Deals (£m)market views the sector positively

020406080

100120140160180

2001 2002 2003 2004

New Further

0100200300400500600700800

2001 2002 2003 2004

New Further

AIM: Number of Issues

Source: OIES, Datastream

Source: London Stock Exchange

Source: London Stock Exchange

0

500

1000

1500

2000

2500

3000

3500

4000

4500

OP

EN

OP

EN

EP Sector and Market Opening

86 91 96 01 05

during these periods

fulfilled

2424

EP Companies: So who has succeeded?EP Companies: So who has succeeded?

R2 = 0.0053

-100%-50%

0%50%

100%150%200%250%

-100% 0% 100% 200% 300%TSR 01-04 Annualised

Pro

duct

ion

Gro

wth

Production Growth vs TSR

Reserves Growth vs TSR

Source: OIES, Company Data

Source: OIES, Company Data

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

LUP

E.S

T

CU

X.L

JKX

.L

CN

E.L

MR

S.L

PLR

.L

DN

X.L

ED

G.L

PM

O.L

DN

O.N

O

TLW

.L

SIA

.L

RO

S.L

R2 = -0.1029

-200%-100%

0%100%200%300%400%500%600%

-100% 0% 100% 200% 300%TSR 01-04 Annulaised

Res

erve

Gro

wth

TSR (Annualised) 01-04

Source: OIES, Company Data

There is no consistent patternEquity markets now discounting Equity markets now discounting exploration success which is a exploration success which is a risk

There is no consistent pattern

risk

2525

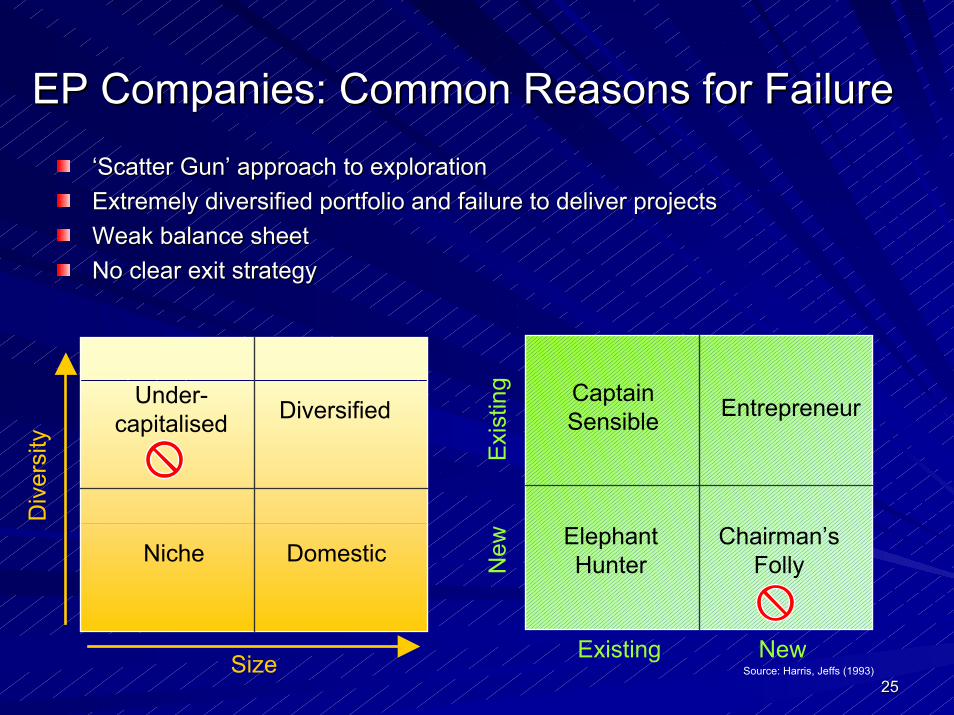

EP Companies: Common Reasons for FailureEP Companies: Common Reasons for Failure

‘Scatter Gun’ approach to exploration‘Scatter Gun’ approach to explorationExtremely diversified portfolio and failure to deliver projects Extremely diversified portfolio and failure to deliver projects Weak balance sheet Weak balance sheet No clear exit strategyNo clear exit strategy

Source: Harris, Jeffs (1993)

Niche Domestic

DiversifiedUnder-capitalised

Size

Div

ersi

ty

Elephant Hunter

Chairman’s Folly

EntrepreneurCaptain Sensible

NewExisting

Exi

stin

gN

ew

2626

EP Companies: Common Reasons for SuccessEP Companies: Common Reasons for SuccessFocus:Focus:–– Offset the advantage of size through strategic differentiationOffset the advantage of size through strategic differentiation

Competence:Competence:–– Recognise where in the chain you have competence and exploit itRecognise where in the chain you have competence and exploit it

Opportunistic:Opportunistic:–– Be opportunistic and take advantage of deals where you have insiBe opportunistic and take advantage of deals where you have insightght

0

10

20

30

40

50

60

Top Bottom Middle No Cycle No View

05

1015202530354045

Top Bottom Middle No Cycle No View

Is there a cycle? Financial view Is there a cycle? Industry view

V

Source: OIESSource: OIES

2727

Even Fools are Lucky!Even Fools are Lucky!

But to achieve consistency need to:But to achieve consistency need to:

–– Deliver above average results. This typically occurs when a nichDeliver above average results. This typically occurs when a niche is exploitede is exploited

–– Remain entrepreneurial, flexible and opportunistic, keeping all Remain entrepreneurial, flexible and opportunistic, keeping all options openoptions open

–– Remember that teams are usually too small to deal with more thanRemember that teams are usually too small to deal with more than a 3 core a 3 core area strategy. area strategy.

Remember that:Remember that:–– The growth potential of an individual company that competently eThe growth potential of an individual company that competently exploits axploits a

niche is significantly higher than all the factors that infniche is significantly higher than all the factors that influence the entire groupluence the entire group

2828

Exploration and Production:Exploration and Production:

Keys to Success and Common Reasons Keys to Success and Common Reasons for Failurefor Failure

Robert ArnottRobert ArnottOxford Institute for Energy StudiesOxford Institute for Energy Studies

22nd February 200522nd February 2005