Exercise 4-6 Part A: Journal Entries Investment in Sales 350,000

18

-

Upload

karly-mcintyre -

Category

Documents

-

view

41 -

download

0

description

Exercise 4-6 Part A: Journal Entries Investment in Sales 350,000 Cash 350,000 Investment in Sales ($148,000)(.85)125,800 Equity in Subsidiary Income 125,800 Cash($50,000)(.85 ) 42,500 Investment in Sales42,500 - PowerPoint PPT Presentation

Transcript of Exercise 4-6 Part A: Journal Entries Investment in Sales 350,000

Exercise 4-6 Part A: Journal Entries Investment in Sales 350,000

Cash 350,000 Investment in Sales ($148,000)(.85) 125,800 Equity in Subsidiary Income 125,800

Cash ($50,000)(.85) 42,500Investment in Sales 42,500

To account for reduction in equity due to dividends

Part B:Workpaper Entries1- Equity income- Sales Company 125,800

Investment in Sales 125800

2- Investment 42500 Dividends declared 42500

3-Common Stock 100,000 Other Contributed Capital 40,000 Retained Earnings 1/1 140,000 Difference (IV and BV) 131,765

Investment in Sales 350,000 Noncontrolling Interest 61,765

4- Land 131,765 Difference (IV and BV) 131,765

Computation and Allocation of Difference between Implied and Book Value Acquired

Parent Non- Entire

Share Controlling ValueShare

Purchase price and implied value 350,000 61,765 411,765 *

Less: Book value of equity acquired: 238,000 42,000 280,000

Difference (IV and BV) 112,000 19,765 131,765

Allocated to land (112,000) (19,765) (131,765)

Balance - 0 - - 0 - - 0 -

Exercise 4-7 Part A: Journal Entries _2010Investment in Sales (.85)($190,000) 161,500

Equity in Subsidiary Income 161,500

Cash 42,500 Investment in Sales (.85)($50,000) 42,500

Part B: Workpaper Entries

1- Equity in Subsidiary Income 161,500 Investment in Sales 161500

2- Investment 42500 Dividends Declared 42500

3- Common Stock 100,000 Other Contributed Capital 40,000 Retained Earnings 1/1 * 238,000 Difference (IV and BV) 131,765 Investment in Sales ($350,000 + $83,300**)433,300 NCI ($61,765 + $14,700***) 76,465

* $140,000 + ($148,000 - $50,000)** ($148,000 - $50,000) x .85*** ($148,000 - $50,000) x .15

4- Land 131,765 Difference (IV and BV) 131,765

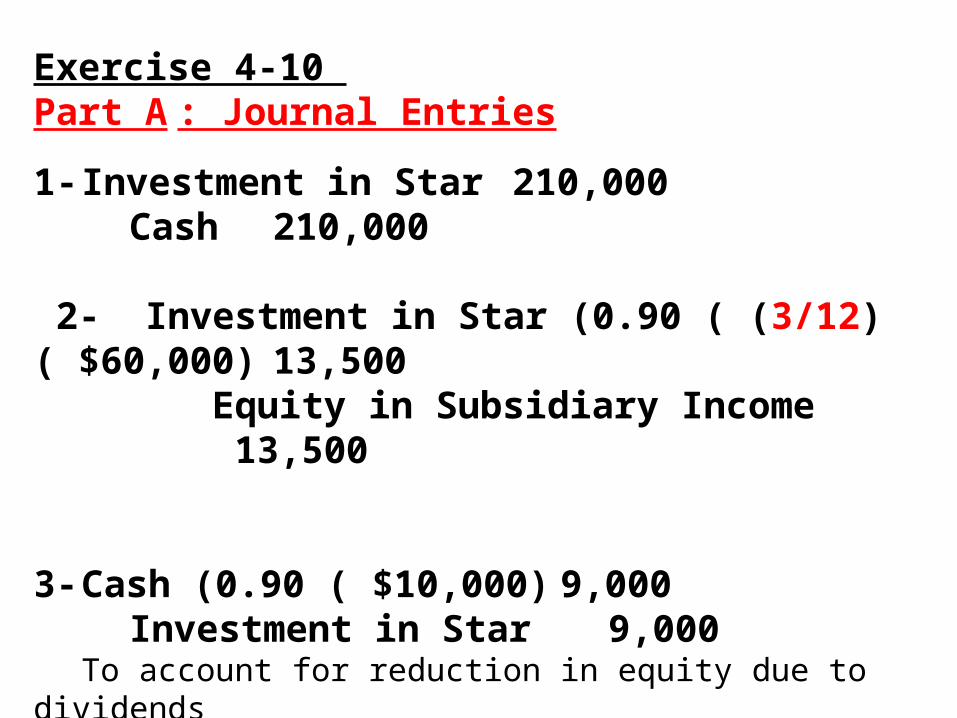

Exercise 4-10 Part A: Journal Entries

1- Investment in Star 210,000 Cash 210,000

2- Investment in Star (0.90 ( (3/12) ( $60,000) 13,500 Equity in Subsidiary Income 13,500

3- Cash (0.90 ( $10,000) 9,000

Investment in Star 9,000 To account for reduction in equity due to dividends

Part B:Workpaper Entries

1- Equity in Subsidiary Income 13,500 Investment in Star 13500

2- Investment in Star 9000 Dividends declared 9000

3- Common Stock - Star 70,000 Other Contributed Capital – Star 30,000 Retained Earnings – Star * 115,000 Difference between Implied and Book Value ** 18,333

Investment in Star 210,000Noncontrolling Interest 23,333

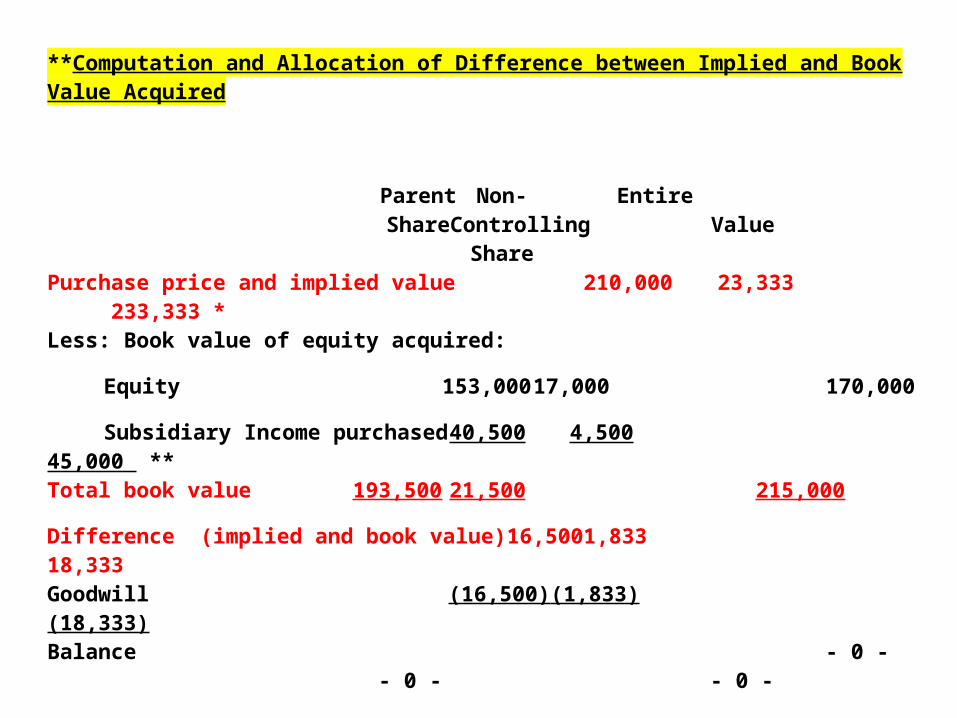

**Computation and Allocation of Difference between Implied and Book Value Acquired

Parent Non- EntireShare Controlling Value

SharePurchase price and implied value 210,000 23,333 233,333 *

Less: Book value of equity acquired:

Equity 153,000 17,000 170,000

Subsidiary Income purchased 40,500 4,500 45,000 **

Total book value 193,500 21,500 215,000

Difference (implied and book value) 16,500 1,833 18,333

Goodwill (16,500) (1,833) (18,333)

Balance - 0 - - 0 - - 0 -

4- Goodwill 18,333 Difference (Implied and Book Value) 18,333

* Retained earnings on 10/1/10Retained earnings on 1/1/10 $ 70,000Income purchased to 10/1/10 (9/12 x $60,000) 45,000Retained earnings on 10/1/10 $ 115,000

Exercise 4-10 Part A: Journal Entries

1- Investment in Star 210,000 Cash 210,000

2- Investment in Star (0.90 ( (3/12) ( $60,000) 13,500 Equity in Subsidiary Income 13,500

3- Cash (0.90 ( $10,000) 9,000

Investment in Star 9,000 To account for reduction in equity due to dividends

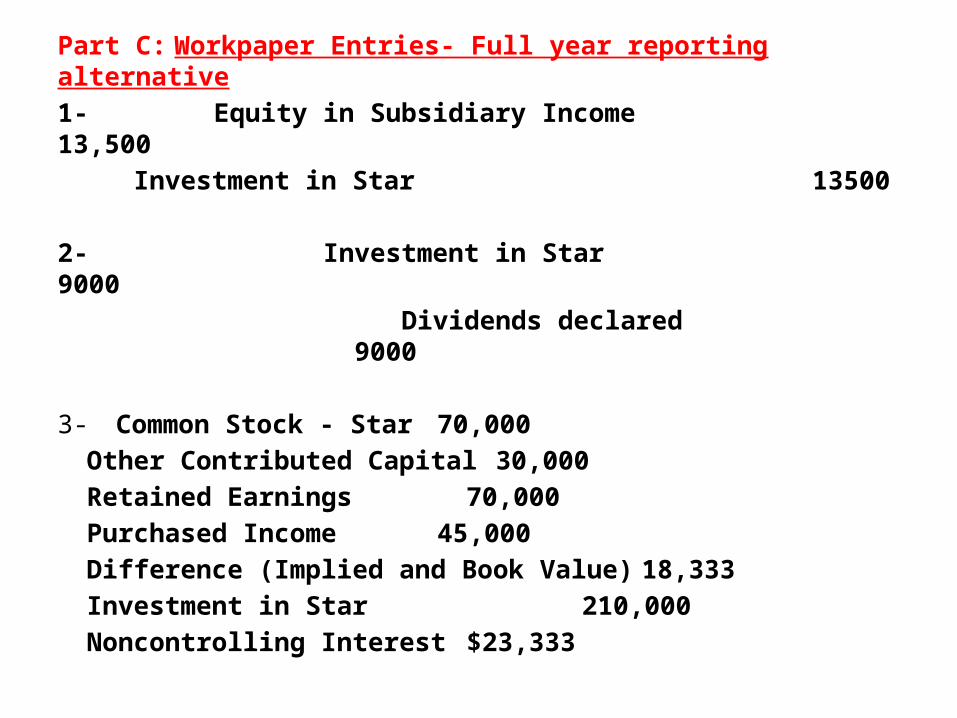

Part C: Workpaper Entries- Full year reporting alternative

1- Equity in Subsidiary Income 13,500 Investment in Star 13500

2- Investment in Star 9000 Dividends declared 9000

3- Common Stock - Star 70,000 Other Contributed Capital 30,000 Retained Earnings 70,000 Purchased Income 45,000Difference (Implied and Book Value) 18,333

Investment in Star 210,000Noncontrolling Interest $23,333

**Computation and Allocation of Difference between Implied and Book Value Acquired

Parent Non- EntireShare Controlling Value

SharePurchase price and implied value 210,000 23,333 233,333 *

Less: Book value of equity acquired:

Equity 153,000 17,000 170,000

Subsidiary Income purchased 40,500 4,500 45,000 **

Total book value 193,500 21,500 215,000

Difference (implied and book value) 16,500 1,833 18,333

Goodwill (16,500) (1,833) (18,333)

Balance - 0 - - 0 - - 0 -

4- Goodwill 18,333 Difference (Implied and Book Value) 18,333