EXEMPTIONS, ABATEMENTS & VALUATION … Shah...Mumbai ♦ Pune ♦ New Delhi ♦ Aurangabad ......

18

7/6/2012 1 Mumbai ♦ Pune ♦ New Delhi ♦ Aurangabad www.mzsk.in Pune Office Level 3, Business Bay, Plot No. 84 Wellesley Road, Near RTO, Pune 411 001, Maharashtra, India Tel: +91 20 26225500 EXEMPTIONS, ABATEMENTS & VALUATION UNDER SERVICE TAX Table of Contents Flow of Taxability Mega Exemptions Valuation Abatement Reverse Charge and Joint Charge Mechanism Point of Taxation Rules

Transcript of EXEMPTIONS, ABATEMENTS & VALUATION … Shah...Mumbai ♦ Pune ♦ New Delhi ♦ Aurangabad ......

7/6/2012

1

Mumbai ♦ Pune ♦ New Delhi ♦ Aurangabad

www.mzsk.in

Pune OfficeLevel 3, Business Bay, Plot No. 84

Wellesley Road, Near RTO,Pune 411 001, Maharashtra, India

Tel: +91 20 26225500

EXEMPTIONS, ABATEMENTS & VALUATION UNDER SERVICE TAX

Table of Contents

Flow of Taxability

Mega Exemptions

Valuation

Abatement

Reverse Charge and Joint Charge Mechanism

Point of Taxation Rules

7/6/2012

2

Flow to verify taxability

Mega Exemptions

Notification No 25/2012 S.T. dated 20.06.2012 provides for following exemptions

� Services provided to UN or other specified organizations.

� If service provider outsources the entire contract, whether the exemption will be available to the outsourced service provider?

� Health Care services

� Cosmetic surgery, hair transplant, etc are taxable

� Cosmetic surgery to remove inborn abnormalities are covered

� Service by veterinary clinics

� Renting of religious places meant for general public and conduct of any religious ceremony

� Religious property not meant for general public, if rented than taxable

� Whether conduct of marriage is a religious ceremony?

� Testing of drugs and vaccines by organizations approved by Drug Controller General of India

7/6/2012

3

Mega Exemptions

� Service provided by entity registered under Section 12AA of IT Act,1961 restricted to charitable activities

Charitable activities includes

Activities relating to Public heath

Advancement of religion and spirituality

Advancement of educational programmesor skill development for specified person

Preservation of environment, watershed, forests and wildlife

Advancement of any object of general public utility subject to specified monetary limits

� Trust providing autonomous courses are taxable (will education be covered in object of public utility) � Old age homes

Mega Exemptions

� Individual Advocate/Arbitral tribunal-

� This exemptions is important for everyone other than advocates as the entire liability is payable on reverse charge basis

� Consultants are now taxable

Arbitral Tribunal services provided to

• Any person other than business entities

• Business entity having turnover less than 10 lakhsin preceding financial year

Legal Services by advocate or firm of advocate

• To other advocate or firm of advocate

• Any person other than business entities

• Business entity having turnover less than 10 lakhsin preceding financial year

Services by member of arbitral tribunal (like judges)

• To an arbitral tribunal

7/6/2012

4

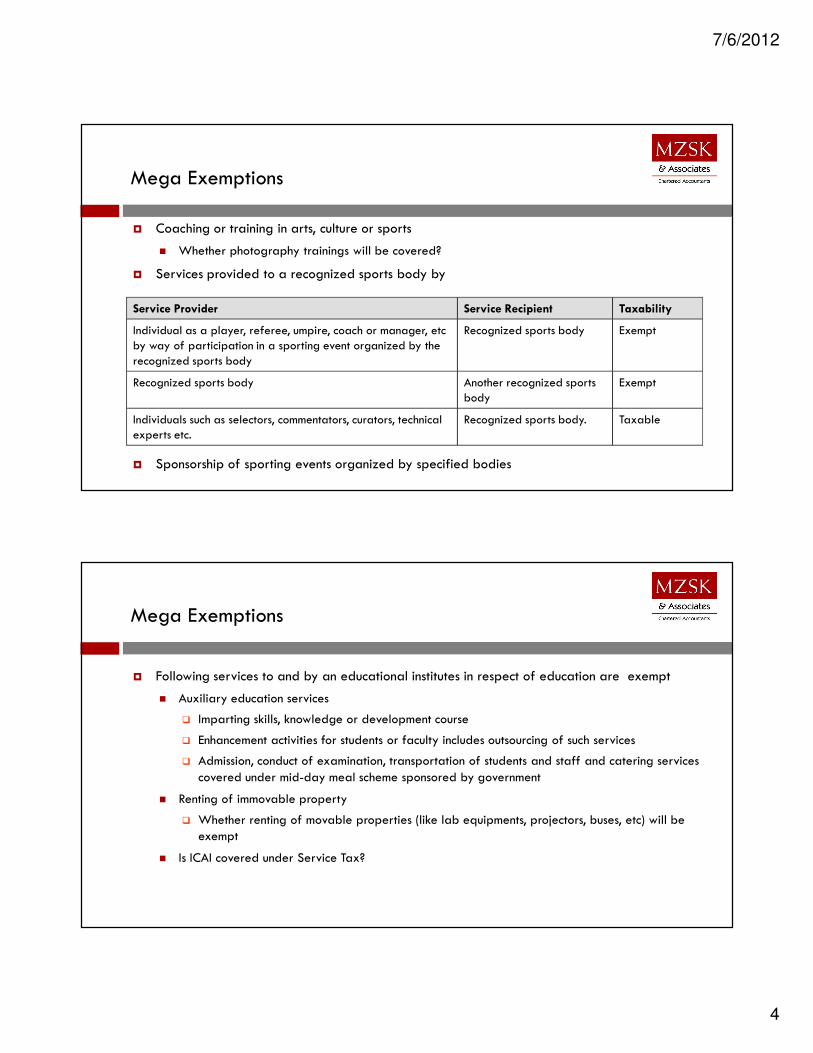

Mega Exemptions

� Coaching or training in arts, culture or sports

� Whether photography trainings will be covered?

� Services provided to a recognized sports body by

� Sponsorship of sporting events organized by specified bodies

Service Provider Service Recipient Taxability

Individual as a player, referee, umpire, coach or manager, etc by way of participation in a sporting event organized by the recognized sports body

Recognized sports body Exempt

Recognized sports body Another recognized sports body

Exempt

Individuals such as selectors, commentators, curators, technical experts etc.

Recognized sports body. Taxable

Mega Exemptions

� Following services to and by an educational institutes in respect of education are exempt

� Auxiliary education services

� Imparting skills, knowledge or development course

� Enhancement activities for students or faculty includes outsourcing of such services

� Admission, conduct of examination, transportation of students and staff and catering services covered under mid-day meal scheme sponsored by government

� Renting of immovable property

� Whether renting of movable properties (like lab equipments, projectors, buses, etc) will be exempt

� Is ICAI covered under Service Tax?

7/6/2012

5

Major Exclusions/Exemptions under Negative List and Mega Exemption notification

� The following services would be excluded in terms of the transactions as undertaken by the entities:

Nature of Services

Construction Erection,Commissioning and Installation

Completionand Finishing Services

Repairs and Maintenance

Renovation Site Formation

Road Non Taxable Non Taxable Non Taxable Non Taxable Non Taxable Taxable

Buildings-Religious Trust

Non Taxable Non Taxable Non Taxable Non Taxable Non Taxable Taxable

JNNURM Non Taxable Non Taxable Non Taxable Non Taxable Taxable Taxable

Airport/Port

Non Taxable Non Taxable Taxable Taxable Taxable Taxable

Single Residential Units

Non Taxable Non Taxable Taxable Taxable Taxable Taxable

Mega Exemptions

Services provided to the Government, a local authority or a governmental authority by way ofconstruction, erection, commissioning, installation, completion, fitting out, repair, maintenance,

renovation, or alteration of –

(site formation not covered)

Civil structure or any other original work not meant for business or commerce

a specified monument and structures

Educational, clinical and art/cultural structure

Canal, dam and other irrigational works

Pipeline, conduit or plant for water supply/treatment or sewage treatment/disposal

Residential complex meant for self use/employee

7/6/2012

6

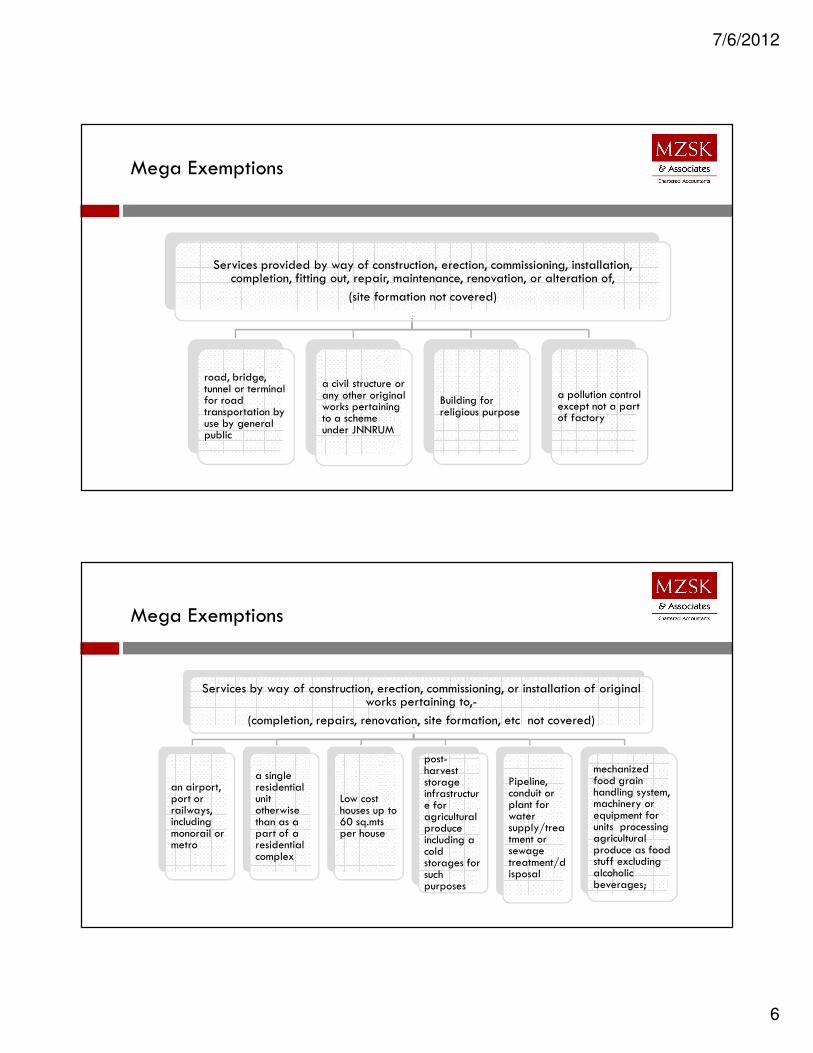

Services provided by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, or alteration of,

(site formation not covered)

road, bridge, tunnel or terminal for road transportation by use by general public

a civil structure or any other original works pertaining to a scheme under JNNRUM

Building for religious purpose

a pollution control except not a part of factory

Mega Exemptions

Services by way of construction, erection, commissioning, or installation of original works pertaining to,-

(completion, repairs, renovation, site formation, etc not covered)

an airport, port or railways, including monorail or metro

a single residential unit otherwise than as a part of a residential complex

Low cost houses up to 60 sq.mts per house

post-harvest storage infrastructure for agricultural produce including a cold storages for such purposes

Pipeline, conduit or plant for water supply/treatment or sewage treatment/disposal

mechanized food grain handling system, machinery or equipment for units processing agricultural produce as food stuff excluding alcoholic beverages;

Mega Exemptions

7/6/2012

7

Mega Exemptions

� Copyright

� Transportation of passengers with or without belongings subject to few conditions

� Services by way of parking to general public

� Whether parking of malls, multiplex etc. will also be exempt?

� Selected general insurance business services provided under specified scheme.

Temporary transfer /permitting the

use of Copyright relating to

Taxability Explanation

a) Original literary, dramatic, musical, artistic work or cinematographic film.

Exempt For example: Author having copy right of a book written by him would not be required to pay service tax on royalty amount received from the publisher for publishingthe book.

b)Other than (a) Taxable For example: Sound recording

Mega Exemptions

� Services by a performing artist in folk or classical art forms of (i) music, or (ii) dance, or (iii) theatre, excluding services provided by such artist as a brand ambassador.

� Is performance in western music exempt?

� Services by way of collecting or providing news by an independent journalist, Press Trust of

India or United News of India.

� Accommodation facilities by hotels, etc : Declared tariff of a room below INR 1000 per day.

� Restaurant not having air-conditioning/central air-heating facility and liquor license

� Services by way of transportation by rail or a vessel from one Place in India to another of

specified goods.

7/6/2012

8

Mega Exemptions

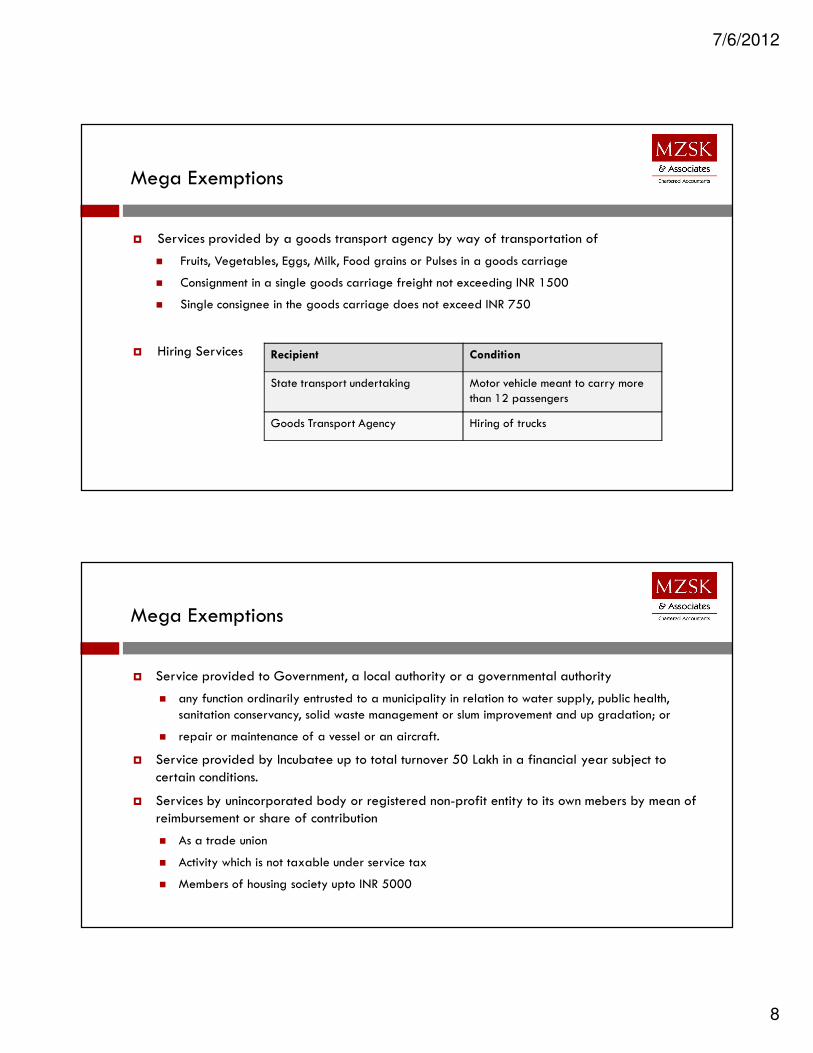

� Services provided by a goods transport agency by way of transportation of

� Fruits, Vegetables, Eggs, Milk, Food grains or Pulses in a goods carriage

� Consignment in a single goods carriage freight not exceeding INR 1500

� Single consignee in the goods carriage does not exceed INR 750

� Hiring Services Recipient Condition

State transport undertaking Motor vehicle meant to carry more than 12 passengers

Goods Transport Agency Hiring of trucks

� Service provided to Government, a local authority or a governmental authority

� any function ordinarily entrusted to a municipality in relation to water supply, public health, sanitation conservancy, solid waste management or slum improvement and up gradation; or

� repair or maintenance of a vessel or an aircraft.

� Service provided by Incubatee up to total turnover 50 Lakh in a financial year subject to certain conditions.

� Services by unincorporated body or registered non-profit entity to its own mebers by mean of reimbursement or share of contribution

� As a trade union

� Activity which is not taxable under service tax

� Members of housing society upto INR 5000

Mega Exemptions

7/6/2012

9

� Services by the following persons in respective capacities

Service Provider Service Recipient

A Sub-broker or an authorised person Stock broker

An Authorised person A Member of a Commodity Exchange

A Mutual fund agent or distributor Mutual Fund or Asset Management Companyfor distribution or marketing of Mutual fund

Selling or Marketing agent of lottery Tickets A Distributer or a Selling Agent

Selling Agent or a distributor of SIM cards or recharge coupon vouchers

A Business facilitator or a business correspondent A Banking Company or an Insurance Company in a Rural Area

Sub-contractor providing works contract services Another contractor providing exempt works contract services

Mega Exemptions

� Intermediate production process amounting to job work in relation to

� Agriculture, printing, textile, specified jewellery, specified coatings in relation to cycles or sewing machines

� Any goods on which duty is to be paid by principal manufacturer

� Services by an organizers to any person in respect of a business exhibition held outside India.

� Making telephone Calls From.

� Departmentally run public telephone

� Guaranteed Public Telephone operating only for Local Calls

� Free telephone at Airport and hospital where no bills are being issued.

� Services by way of slaughtering of bovine animals.

Mega Exemptions

7/6/2012

10

Mega Exemptions

� Provided by service provider located in a non- taxable territory.

� Services by ESIC- (Whether PF will be exempt? )

� Services by public library, public toilet, municipal functions by municipality.

� Service by way of transfer of going concern

Service Provider Service Recipient

Service provider located in a non- taxable territory E.g. Jammu & Kashmir

Government, a local authority or an individual in relation to any purpose other than industry, business or commerce.

Charitable entity as per section 12AA of the Income tax Act, 1961

Person located in a non-taxable territory

Valuation

� Charging section-Section 67 of Finance Act 1994

� Valuation of taxable services shall be done as per the new sec. 67A which states that the

The rate of service tax, value of a taxable service and rate of exchange shall be the rate as applicable atthe time when the taxable service has been provided or agreed to be provided.

"rate of exchange" means the rate of exchange referred to in the Explanation to section 14 of the

Customs Act, 1962.‘;

� This has a impact in cases where invoices are issued but payment is received in installments later

and there is a difference in the value in Rupees owing to foreign exchange fluctuations.

� Major Impact on ITSS service provider as exchange rate for export billing shall be taken as per

rate of exchange notified by CBEC as per Custom Act.

7/6/2012

11

Consideration: Meaning

� Consideration includes monetary as well as non-monetary consideration…. Is this right??

� Non obligatory grants/donations are not consideration

� Consideration not linked to services not covered.

� For e.g. Security deposits forfeited for damages done.

� However advances received for cancellation of contract for service would be taxable.

Valuation – For Works Contractor (composition option)

Nature of service

• A) Original works

• B) maintenance or repair or reconditioning or restoration or servicing of any goods,

• C) All works contract other (A) and (B in relation to immoveable property

From 01.07.2012

(Taxable %)

• 40%

• 70%

• 60%

Conditions for CENVAT

• All the case CENVAT credit in respect of input services and capital goods is eligible

Note : Alternate option of paying under rule 2A (deduction of material is also available)

7/6/2012

12

Valuation for sale of Flats - Abatement

� Option to pay tax on 25% value of flat/unit if the same includes value of land. (effective rate 3.09%)

� In case of extra work, if a part of the agreement – can avail abatement.

� In case of extra work not a part of agreement, tax to be paid as per Works Contract composition scheme on 60% of the value. (Effectively @ 7.42%).

� In case of maintenance deposit which is refundable and accounts are provided, no tax needs be paid. However in case of maintenance charges being collected, tax needs to be discharged @ 12.36% on 60% value (effectively @ 7.42%)

� In case of miscellaneous charges collected over and above flat value, to be taxed @ 12.36%.

Valuation- Hospitality

Nature of service From 01.07.2012 (Taxable %) Impact (Effective Rate)

Accommodation service 60% 7.2% + 3% cess on tax

Restaurant services 40% 4.8% + 3% cess on tax

Mandap keeper services 70% 8.4% + 3% cess on tax

Outdoor caterer 60% 7.2% + 3% cess on tax

Bundled Services (Food+ accommodation +renting of premises)

70% 8.4% + 3% cess on tax

All other services( excluding banking and financial Services)

100% 12% + 3% cess on tax

Please note that availing the above abatement and paying taxes in all cases as against any of the existing methods followed is advised to avoid litigation and get maximum benefits.

7/6/2012

13

Valuation- Tours and Travels

Nature of Services Abatement

Rate

Conditions

Services by a tour operator in relation to,-(i) a package tour

25 (i) No CENVAT credit(ii) Invoice is issued of inclusive of charges of tour

(ii) a tour, if the tour operator is providing

services solely of arranging or booking

accommodation for any person in relation

to a tour

10 (i) No CENVAT credit(ii) Invoice should be indicative of accommodationcharges(iii) Not available when income earned as commissionagent

(iii) any services other than specified at (i)and (ii) above.

40 (i) No CENVAT credit(ii)Invoice is issued for gross charges of the tour

Valuation- General

� Money Changing Services

� Reimbursement of expenses in case of reverse mechanism : Erstwhile rule 7 of valuation rules dealing withconsideration paid in case of import of services has been deleted and has been brought on line withdomestic services.

Slabs of the sum Service tax payable

If the sum is upto Rs 100,000 0.12% of the sum, subject to minimum of Rs30

If the sum is between Rs 100,000 and Rs10,00,000

Rs 120 + 0.06% of the sum exceeding Rs

1,00,000

If the sum is greater than Rs 10,00,000 Rs 660 + 0.012% of the sum exceeding Rs

10,00,000 subject to maximum of Rs 6000

7/6/2012

14

Other abatements

Description of taxable

service

Percent-

age

Conditions

Services in relation to financial leasingincluding hire purchase

10 Nil.

Transport of passengers, with or withoutaccompanied belongings by rail

30 Nil.

Transport of passengers by air, with or withoutaccompanied belongings

40 No CENVAT credit of Inputs or capital goodsshould be taken

Services of goods transport agency in relationto transportation of goods.

25 No CENVAT credit

Services provided in relation to chit 70 No CENVAT credit

Renting of any motor vehicle designed tocarry passengers

40 No CENVAT credit

Transport of goods in a vessel 50 No CENVAT credit

Reverse Charge Mechanism

� Meaning: The reverse charge mechanism means a mechanism where the 'Service recipient’ isliable to pay service tax instead of 'Service provider’.

� In this reverse charge mechanism provided under service tax law, the 'Service recipient’ isliable to pay whole of service tax.

� The notification deals with what are the services on which reverse charge mechanism isapplicable and the proportion in which the 'Service recipient’ of services is liable to pay theservice tax.

7/6/2012

15

Reverse Charge Mechanism w.e.f .01.07.2012 (relevant extract)

Service nature Liability of

Service

Provider

Liability of

Service

Recipient

Goods Transport Agencies (in case of specified service recipient)

Note: The abatement of 75% continues

NIL 100%

Sponsorships provided to partnership firm or corporate entity NIL 100%

Services provided by Individual/Firm of Advocate to business entity NIL 100%

Services provided by a person in non taxable territory to a person located

in taxable territory (i.e. import of service)

NIL 100%

Support Services Provided by Government excluding renting of immovable

property

NIL 100%

Joint Charge Mechanism

� Meaning: Joint charge mechanism means a mechanism where the 'Service recipient’ is alsomade liable to pay service tax on a specified percentage of the service along with the‘Service provider’ instead of the 'Service provider’ being liable for the entire liabilitypayment.

� The notification specifies the services on which joint charge mechanism is applicable and theproportion in which the 'Service recipient’ of services is liable to pay the service tax.

� Joint charge mechanism is applicable when provided by a non – corporate service providerto a corporate business entity. Cenvat credit of the tax paid can be availed on the part ofservice tax paid even by the service recipient.

7/6/2012

16

Joint Charge Mechanism w.e.f .01.07.2012 (relevant extract)

Service nature Liability of

Service

Provider

Liability of

Service

Recipient

Rent – a – Cab where abatement 60% is availed

Note : Where abatement is not availed, service provider and service receiver

are liable to pay on 60% and 40% of service value respectively. However as

per the common industry practice, is for availing abatement by small service

providers and hence it is always advisable to pay tax on 100% amount by the

service provider.

NIL 100%

Supply of Manpower for any purpose 25% 75%

Works Contract Service 50% 50%

Note: Care needs to be taken in case of reimbursements to employees etc.

Impact of Point of taxation Rules

� Time of provision of service shall be earliest of the following dates:

� Date on which invoice is issued (If invoice is not issued within 30 days (45 days in caseof Banking and Financial Services) of completion of provision of Service, then: Dateof Completion of Service)

OR

� Date of receipt of payment (including advance payment)

Exemption is provided to non corporates having turnover less than 50 lakhs from the application ofthe above. These assessees can opt to pay tax on receipts basis.

7/6/2012

17

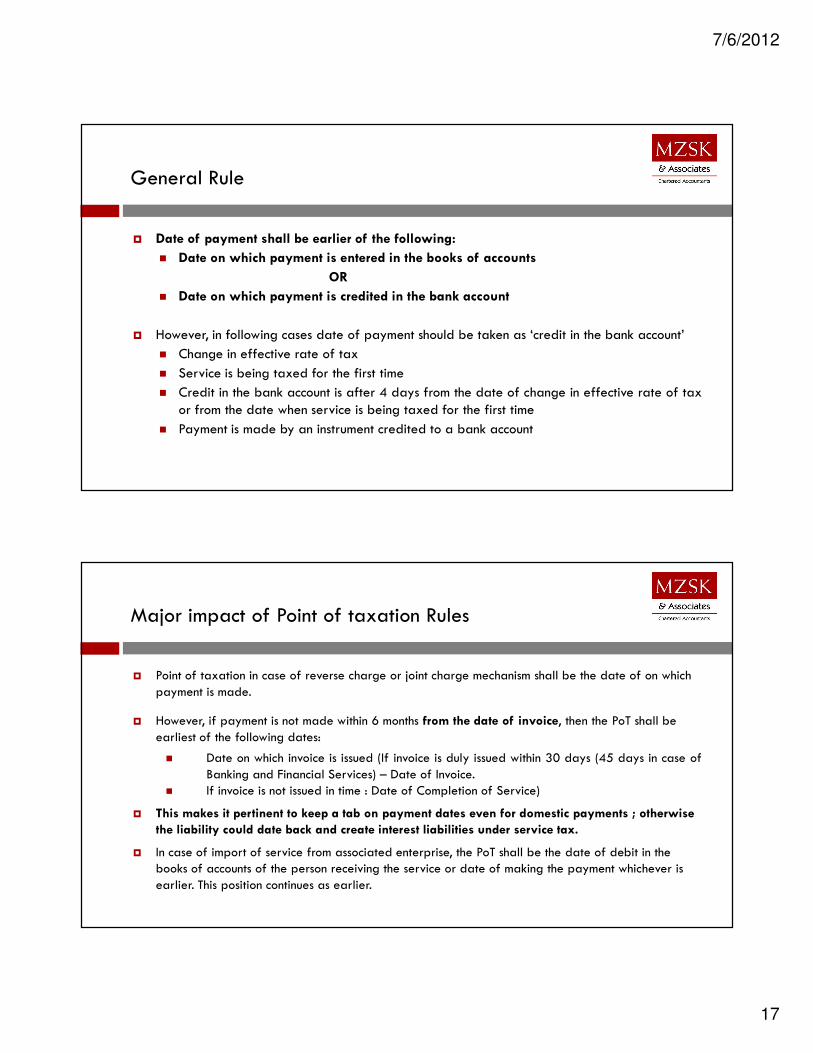

General Rule

� Date of payment shall be earlier of the following:

� Date on which payment is entered in the books of accounts

OR

� Date on which payment is credited in the bank account

� However, in following cases date of payment should be taken as ‘credit in the bank account’

� Change in effective rate of tax

� Service is being taxed for the first time

� Credit in the bank account is after 4 days from the date of change in effective rate of taxor from the date when service is being taxed for the first time

� Payment is made by an instrument credited to a bank account

Major impact of Point of taxation Rules

� Point of taxation in case of reverse charge or joint charge mechanism shall be the date of on which payment is made.

� However, if payment is not made within 6 months from the date of invoice, then the PoT shall be earliest of the following dates:

� Date on which invoice is issued (If invoice is duly issued within 30 days (45 days in case ofBanking and Financial Services) – Date of Invoice.

� If invoice is not issued in time : Date of Completion of Service)

� This makes it pertinent to keep a tab on payment dates even for domestic payments ; otherwise

the liability could date back and create interest liabilities under service tax.

� In case of import of service from associated enterprise, the PoT shall be the date of debit in the books of accounts of the person receiving the service or date of making the payment whichever is earlier. This position continues as earlier.

7/6/2012

18

www.mzsk.in

Mumbai Office

The Ruby, Level 9, North West Wing, Senapati Bapat Marg, Dadar (W),

Mumbai – 400028, INDIA

New Delhi Office

L-11, Lower Ground Floor, Malviya Nagar,

New Delhi – 110017, INDIA

Pune Office

Level 3, Business Bay, Wellesley Road, Near RTO, Pune – 411001, INDIA

Aurangabad Office

C-6, Balaji Apartments, Behind Kohinoor Plaza, Nirala Bazar, Aurangabad – 431001, INDIA

Thank You…

CA Sagar ShahPartner